Question

What do you mean by programmed or casual reports?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

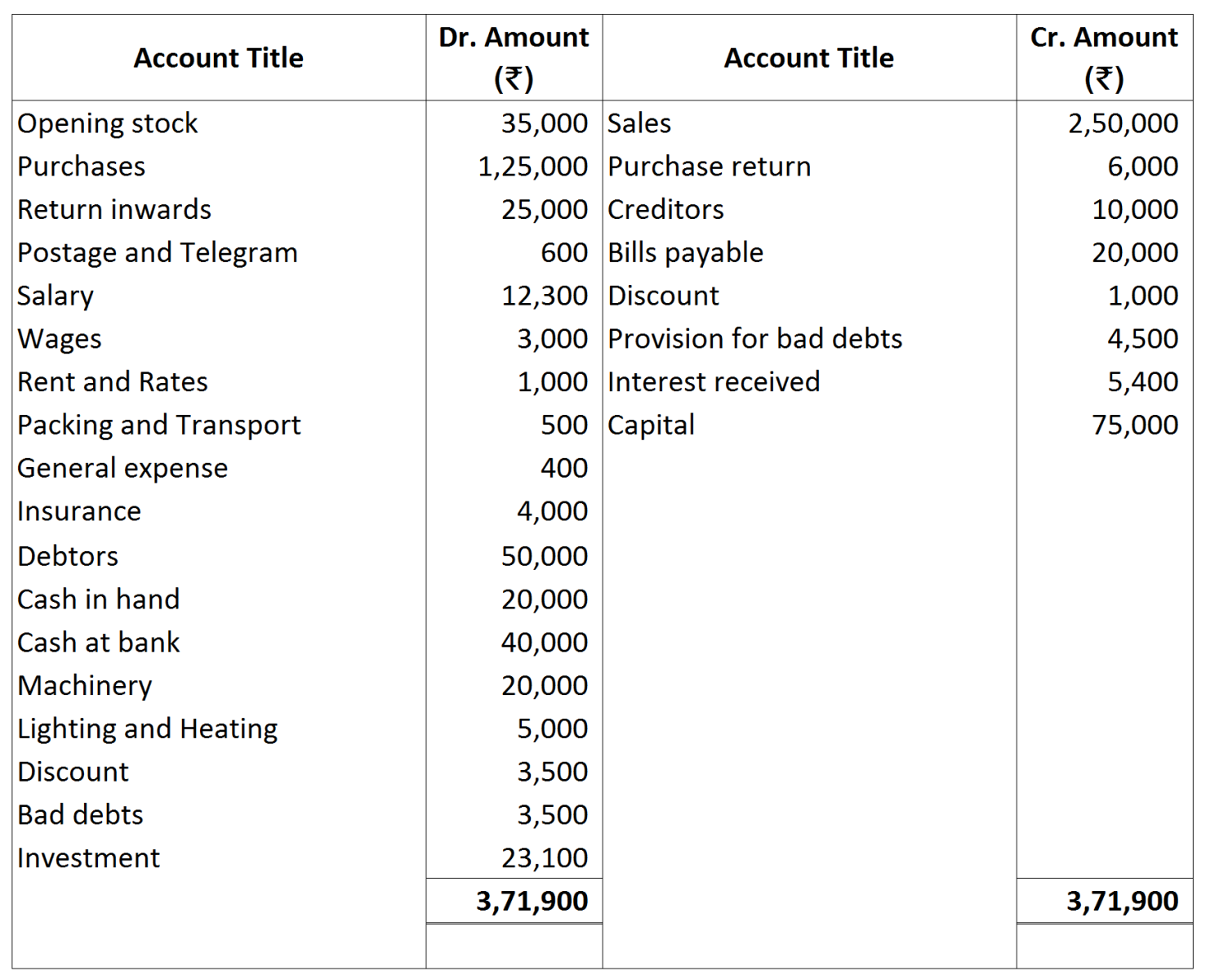

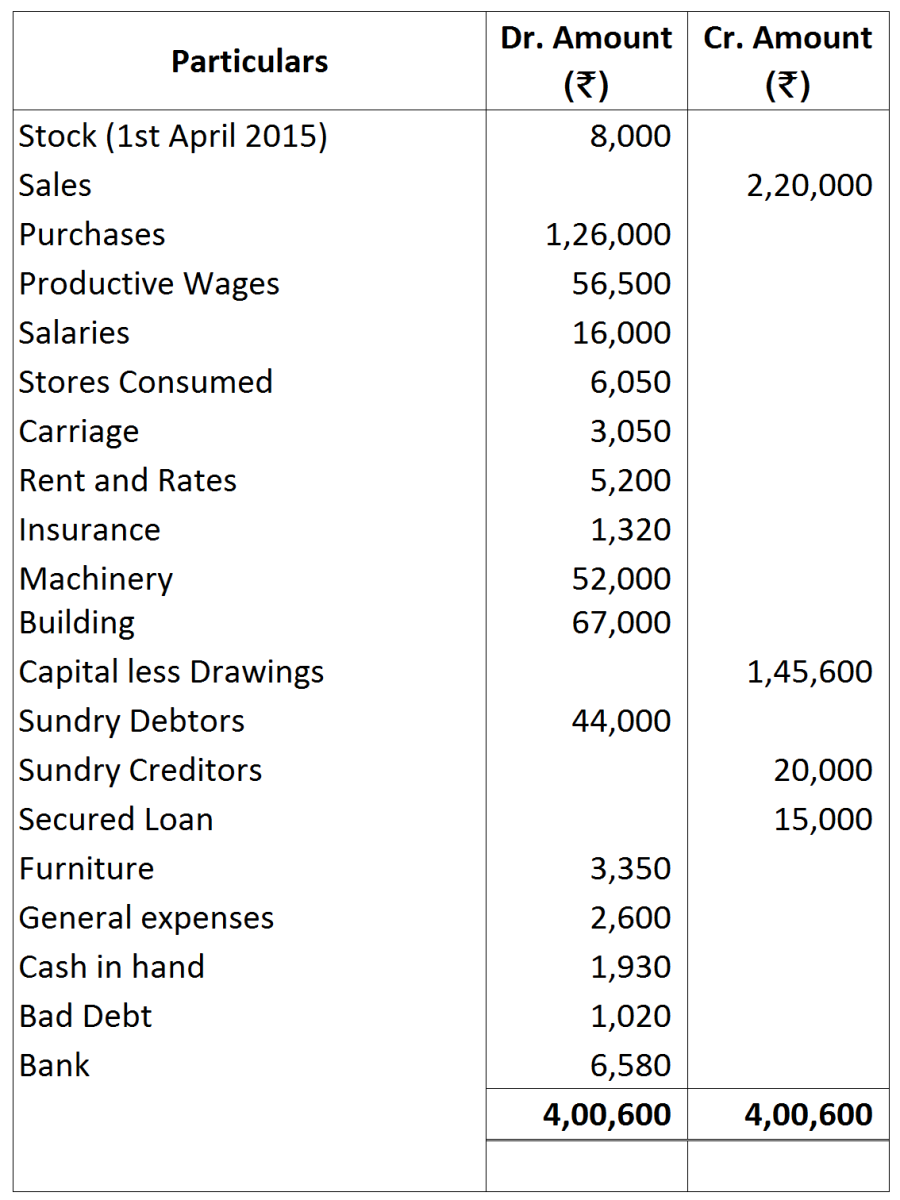

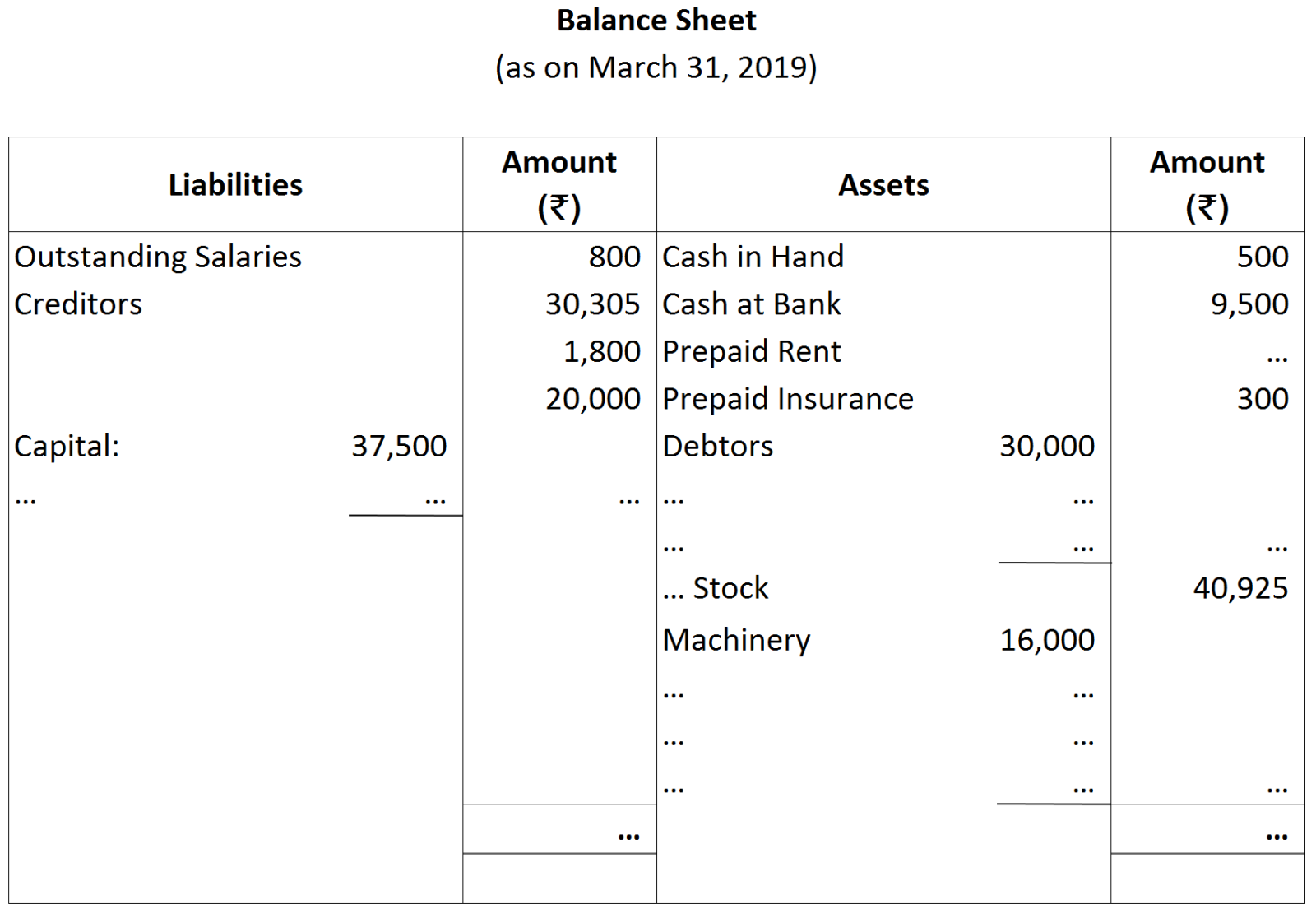

Adjustments:

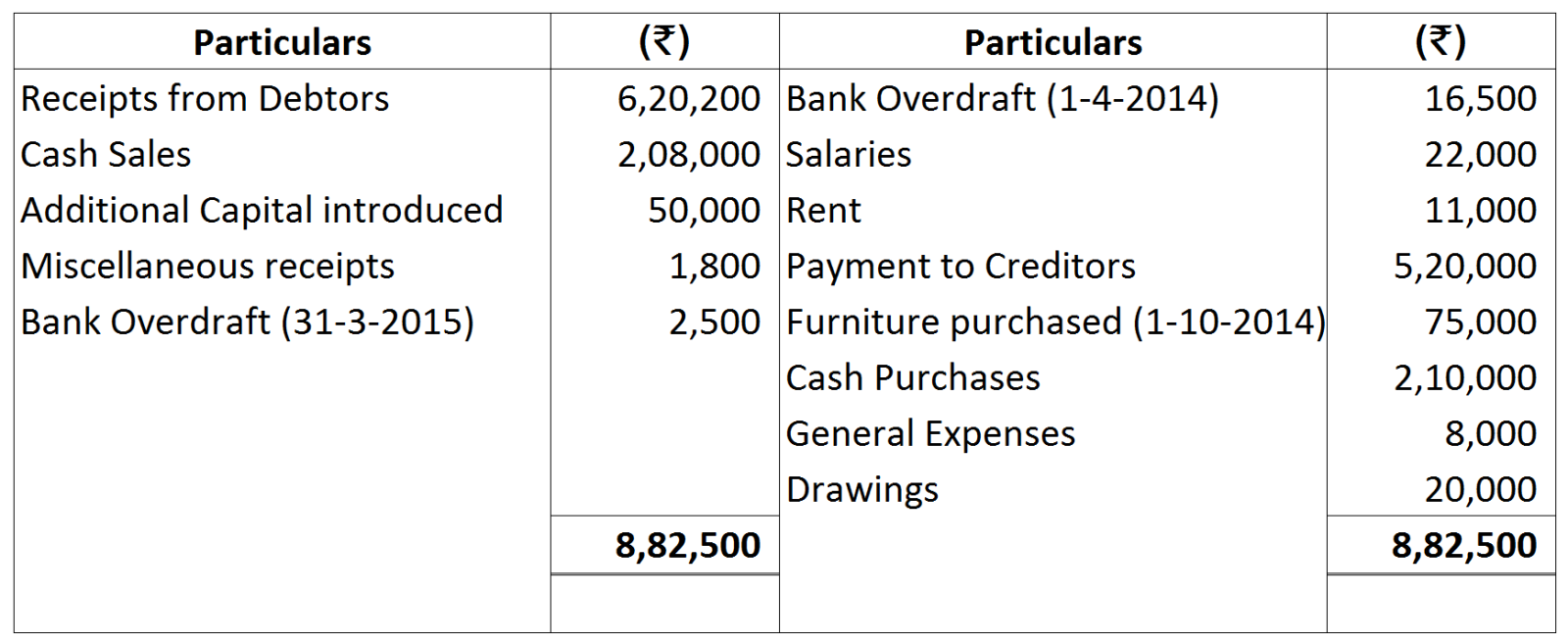

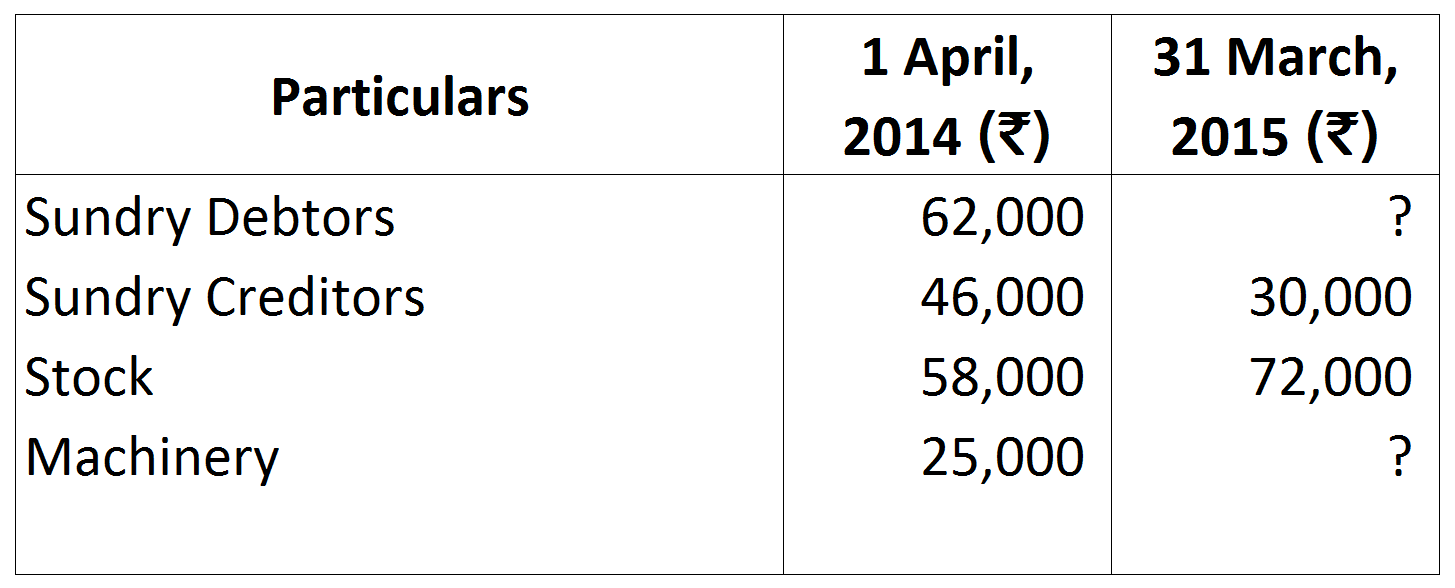

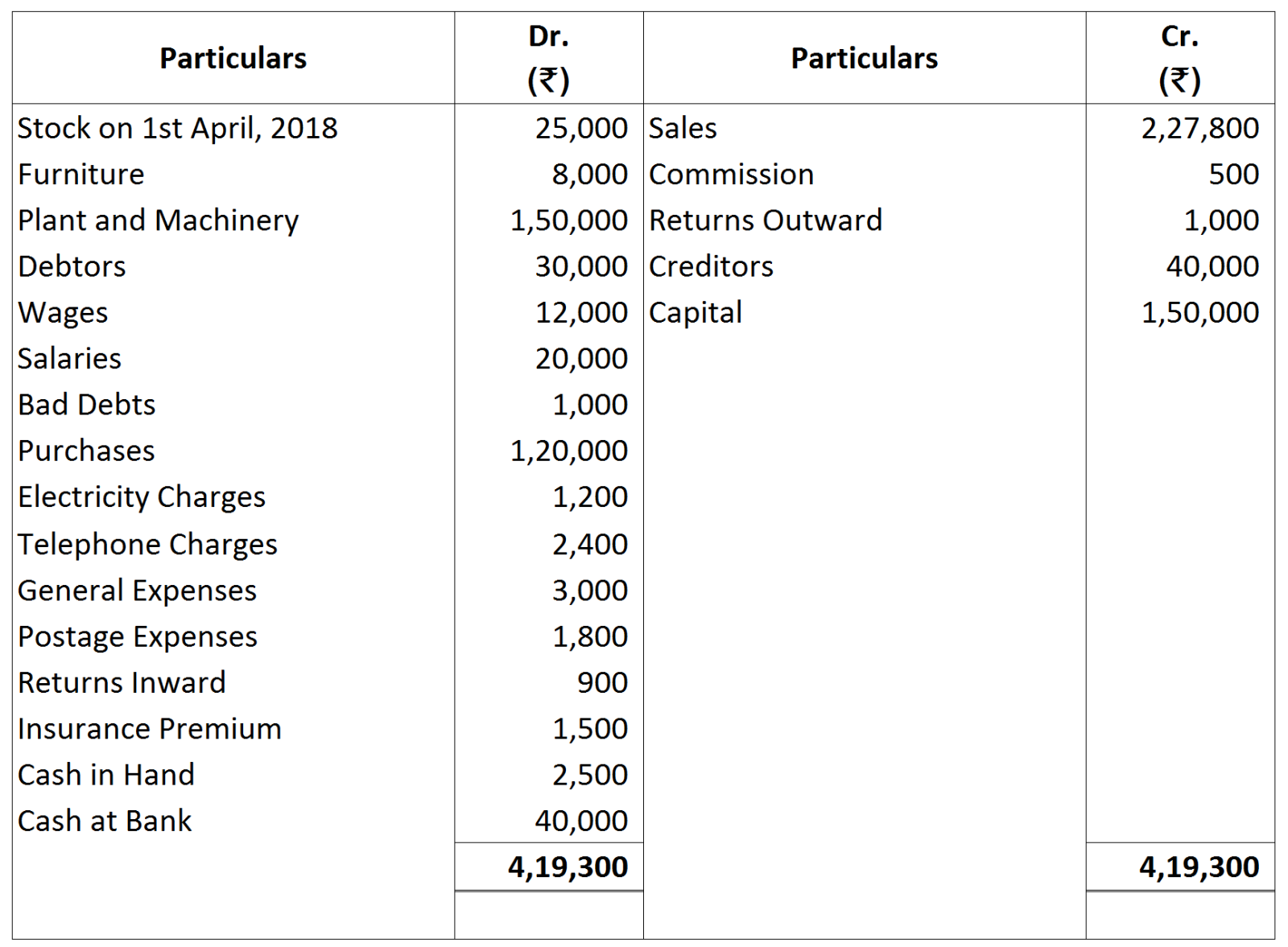

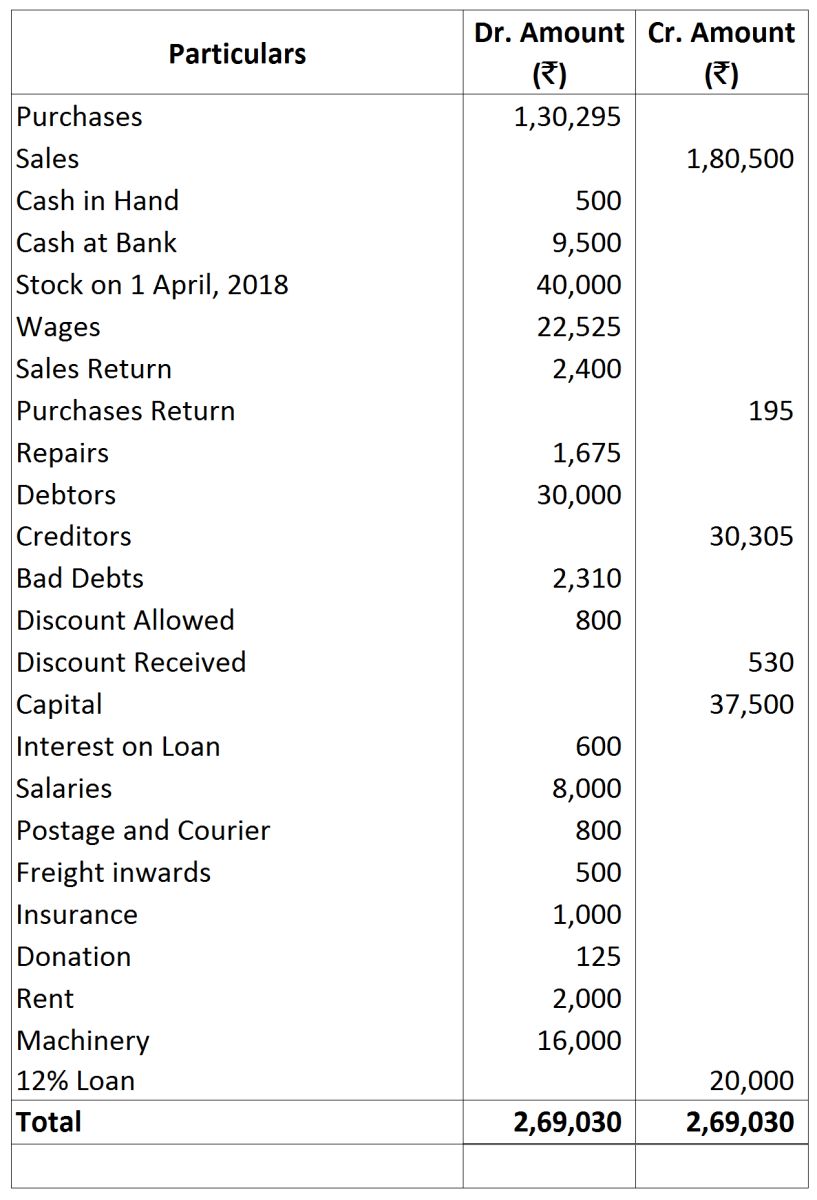

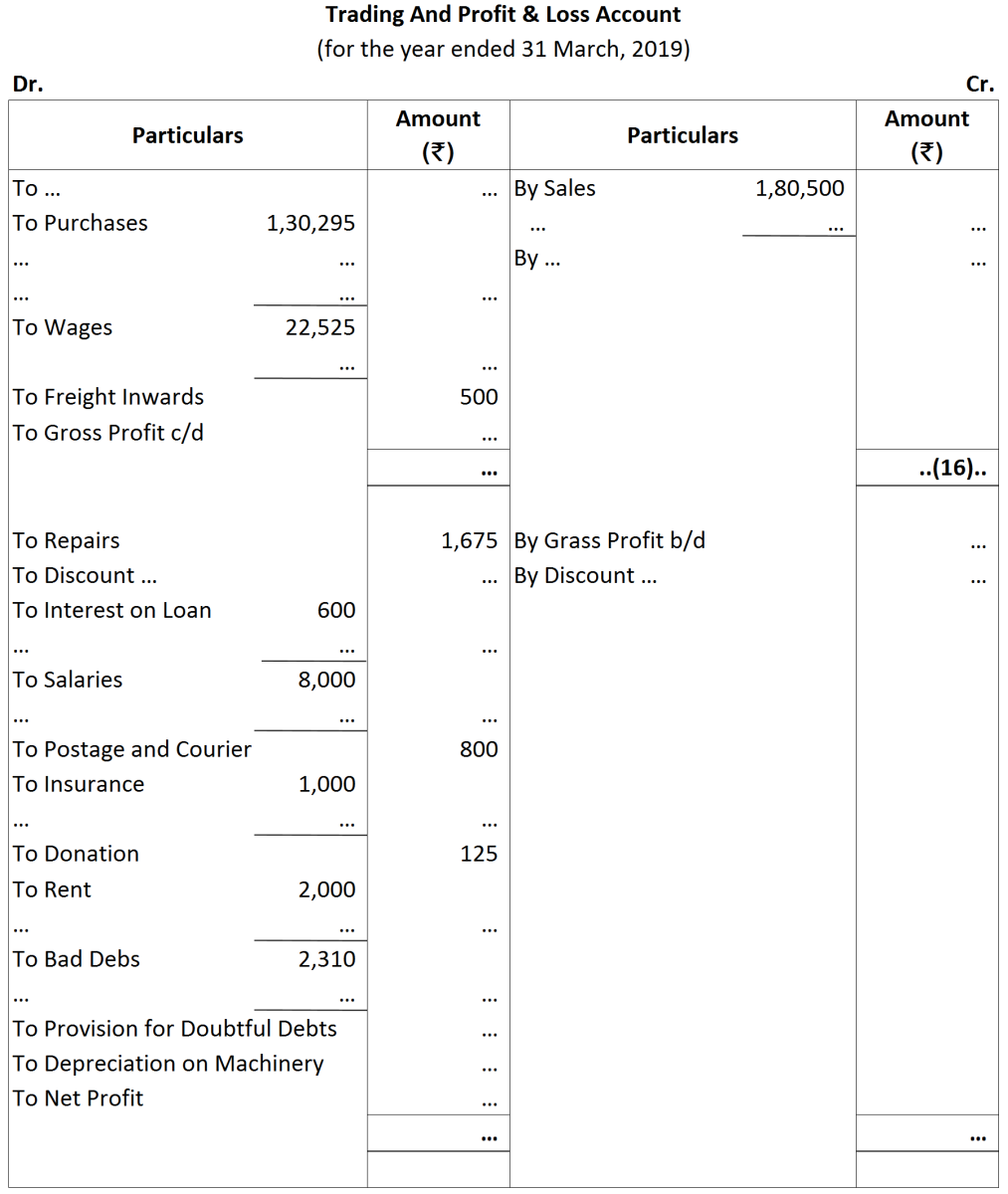

Adjustments:

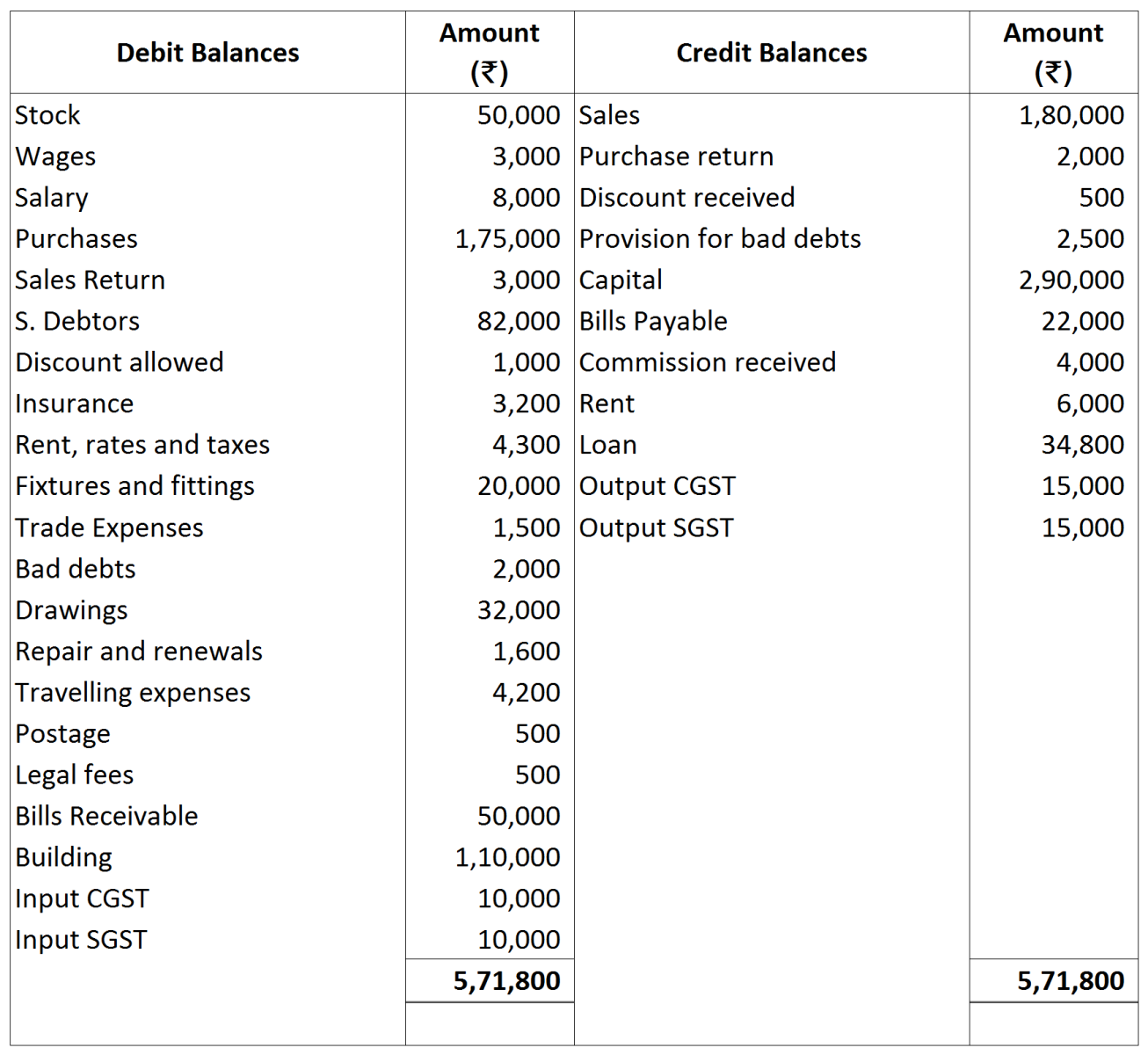

| Name of Accounts | Amt(Rs) | Name of Accounts | Amt(Rs) |

| Capital | 80,000 | Insurance | 600 |

| Purchases | 82,000 | Salaries | 12,500 |

| Sales | 1,10,000 | Bad Debts | 200 |

| Return Outwards | 1,000 | Carriage on purchases | 200 |

| Building | 45,000 | Commission (credit) | 1,500 |

| Opening Stock | 15,000 | Cash in hand | 5,000 |

| Debtors | 20,100 | Cash at Bank | 25,000 |

| Creditors | 28,000 | Sales tax paid | 5,000 |

| Furniture | 7,000 | Sales tax collected | 3,500 |

| Wages | 1,800 | Interest on investment | 500 |

| Rent | 5,100 |