Question

What is a production possibility frontier?

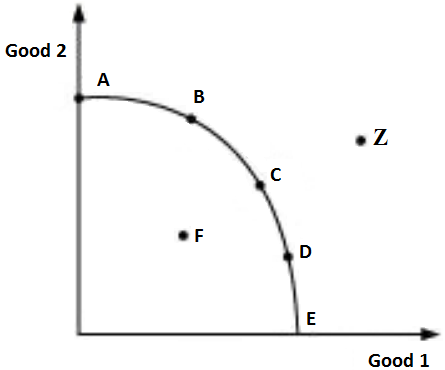

All the points lying on the PPC, that is curve AE, are associated with different quantities of good 1 and good 2 produced, by employing the available resources fully and in an efficient manner. While any point lying under the curve, like F, depicts inefficiency or under utilisation of available resources. Whereas any point lying outside the curve, like Z, depicts over utilisation of the available endowment of resources and technology; making it non-feasible.

All the points lying on the PPC, that is curve AE, are associated with different quantities of good 1 and good 2 produced, by employing the available resources fully and in an efficient manner. While any point lying under the curve, like F, depicts inefficiency or under utilisation of available resources. Whereas any point lying outside the curve, like Z, depicts over utilisation of the available endowment of resources and technology; making it non-feasible.Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| Units sold | 10 | 9 | 8 | 7 | 6 | 5 | 4 |

| Price (₹) | 1 | 2 | 3 | 4 | 5 | 6 | 7 |

| Output (units) ₹ | Total Revenue ₹ | Total Cost ₹ |

| 1 | 10 | 8 |

| 2 | 18 | 15 |

| 3 | 24 | 21 |

| 4 | 28 | 25 |

| 5 | 30 | 33 |