Question

What is a Statement of Affairs? How does it differ from the Balance Sheet?

|

|

Basis

|

Balance Sheet

|

Statement of Affairs

|

|

1

|

Objective

|

The main objective of preparing Balance Sheet is to know about the financial position of the business.

|

The main objective of preparing Statement of Affairs is to know about capital at a point of time.

|

|

2

|

Accounting System

|

Balance Sheet is prepared when accounts are maintained under Double Entry System.

|

Statement of Affairs is prepared when accounts are maintained under Single Entry System.

|

|

3

|

Accounts and Information

|

This is prepared exclusively on the basis of ledger accounts.

|

In view of incomplete accounts, its preparation is based on limited accounts, calculations, estimates and other information.

|

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

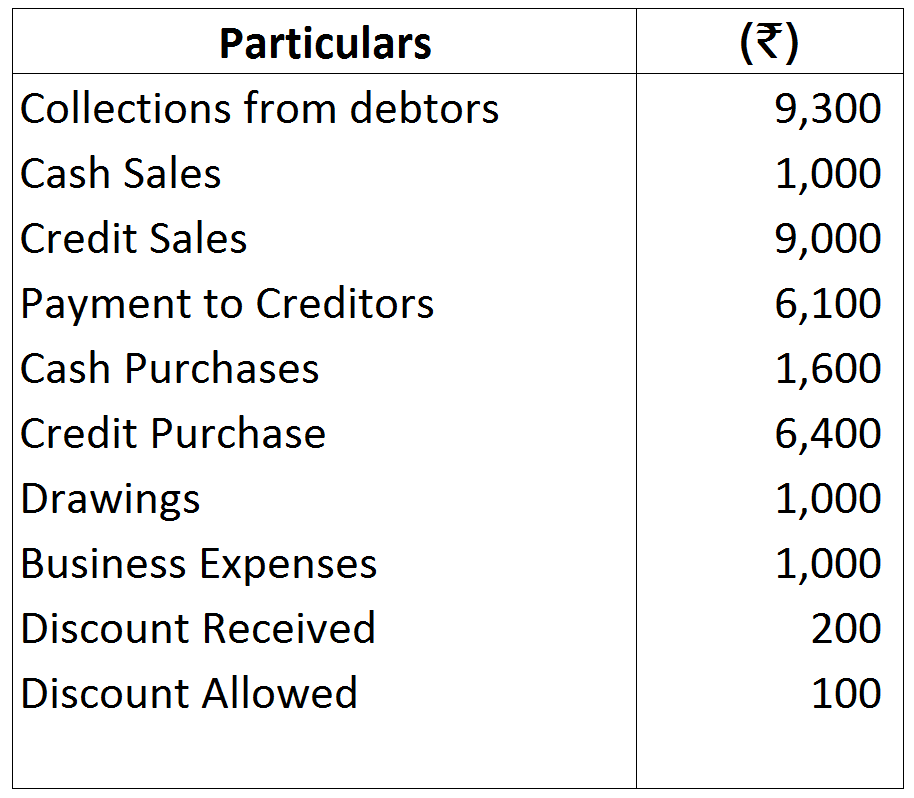

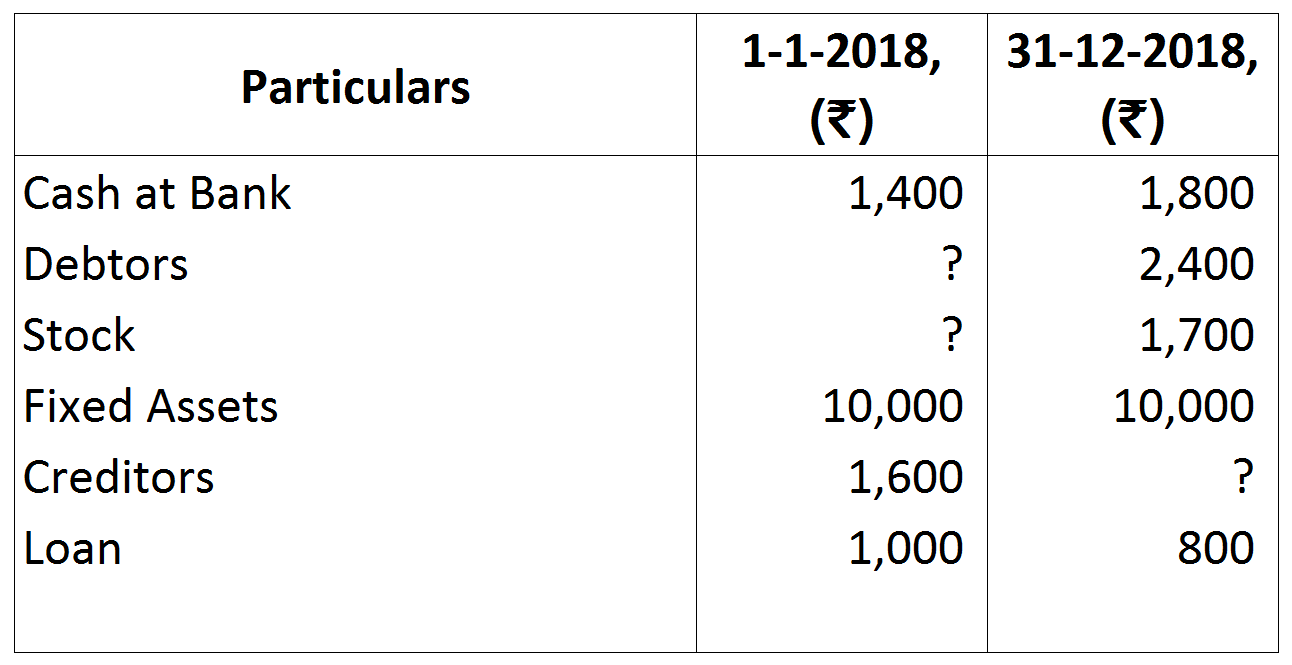

Transactions during the year 2018:

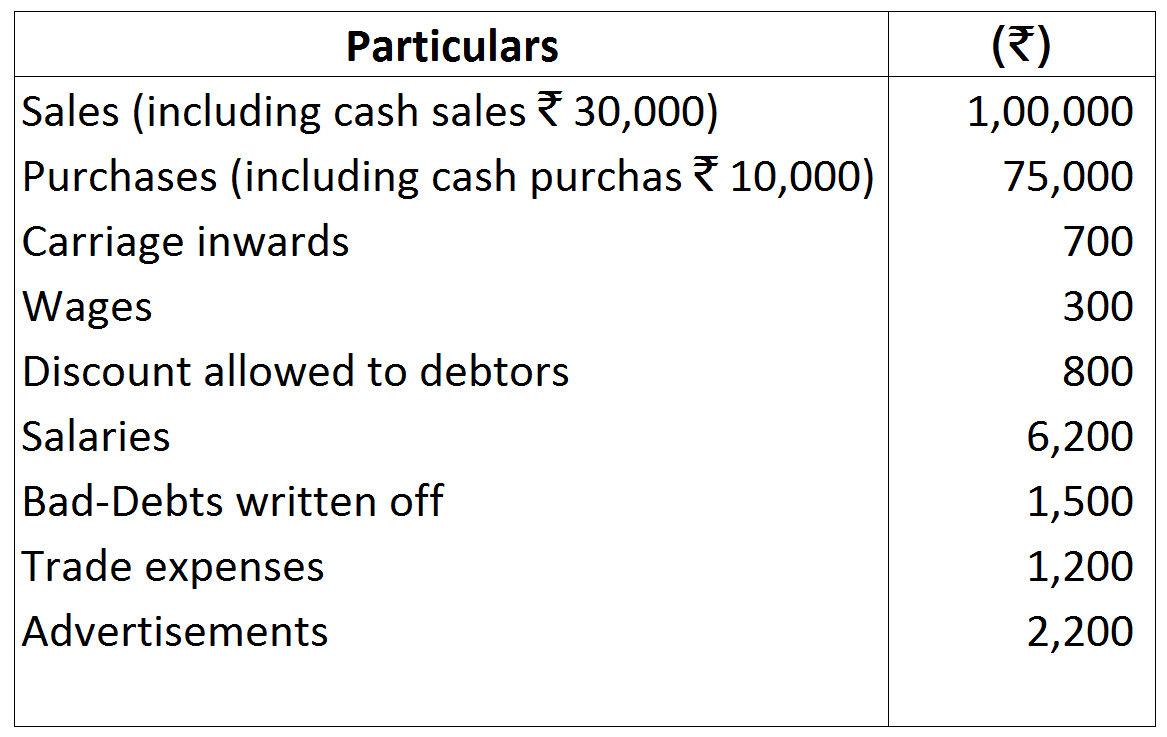

Transactions during the year 2018: