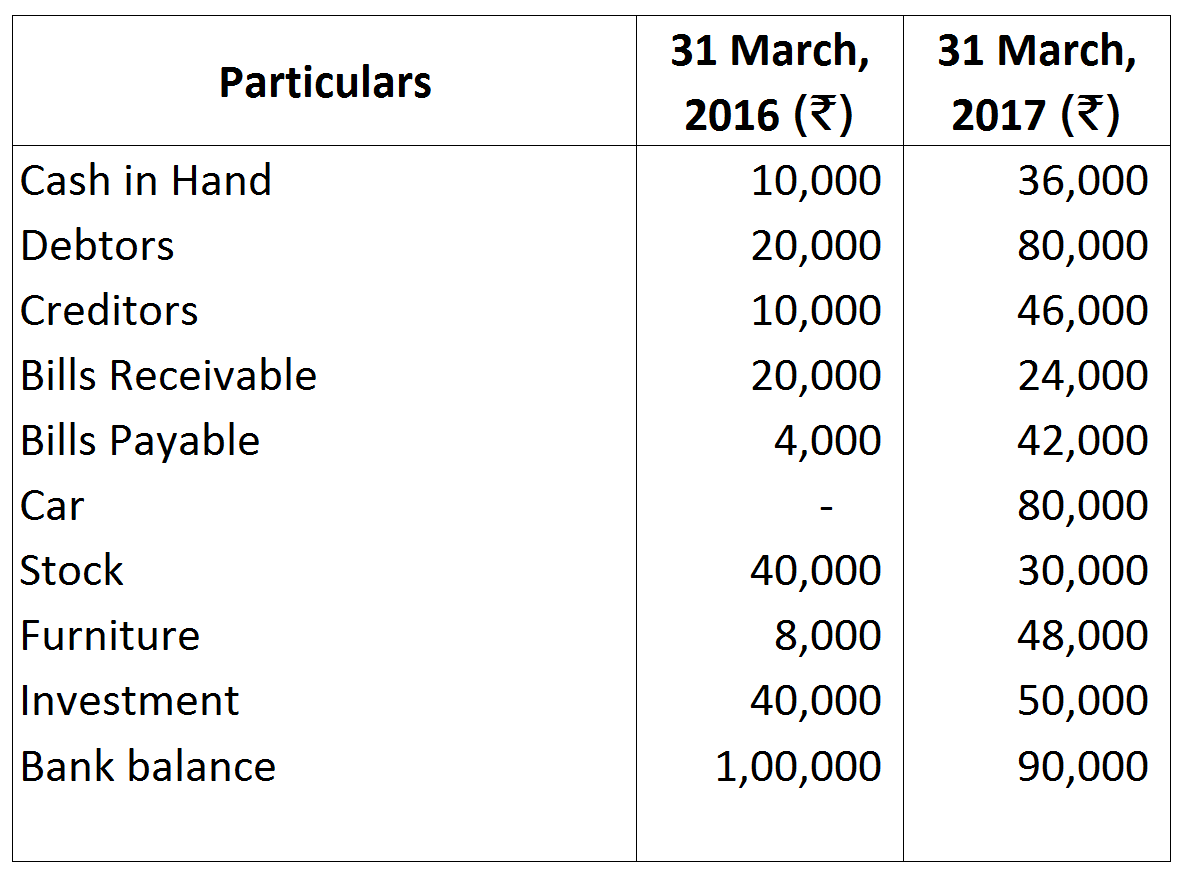

Question 16 Marks

‘Is it possible to prepare the profit and loss account and the balance sheet from the incomplete book of accounts kept by a trader’? Do you agree? Explain.

Answer

View full question & answer→The Profit and Loss Account and the Balance Sheet can be prepared from the incomplete book of accounts through Conversion Method. According to this method, incomplete records are converted into double entry records. In case of incomplete records, details of some transactions are easily available like cash sales, cash purchases, creditors, debtors; however, there are number of transactions, the details of which may not be available directly. Yet, these details can be found out indirectly or logically. Some of the important items that are vital for preparing Balance Sheet are given below.

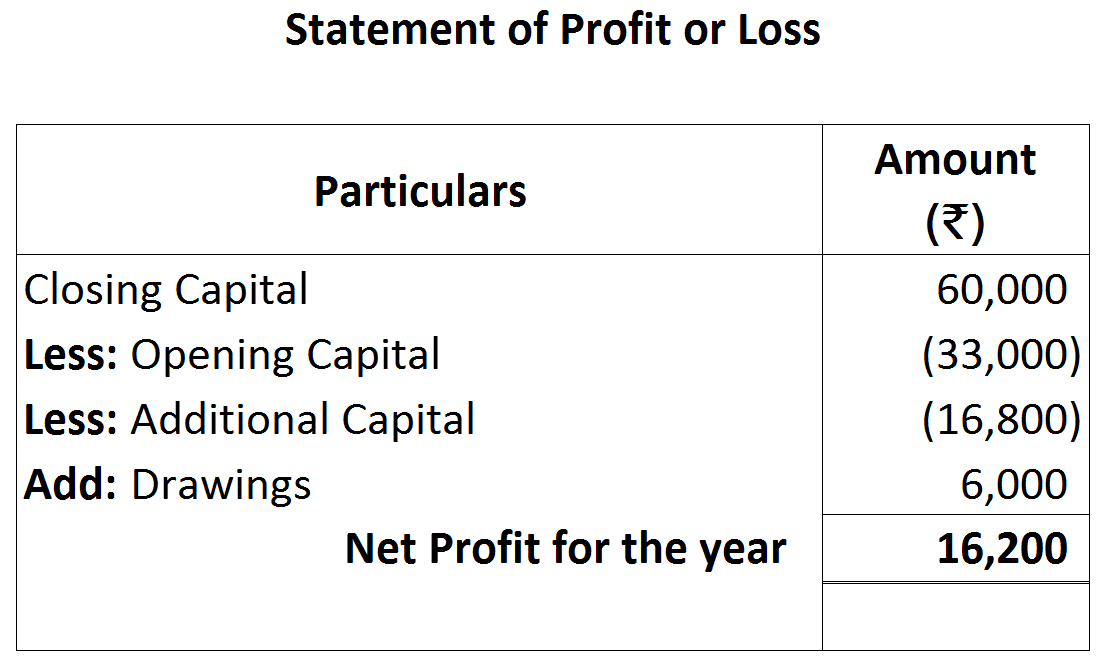

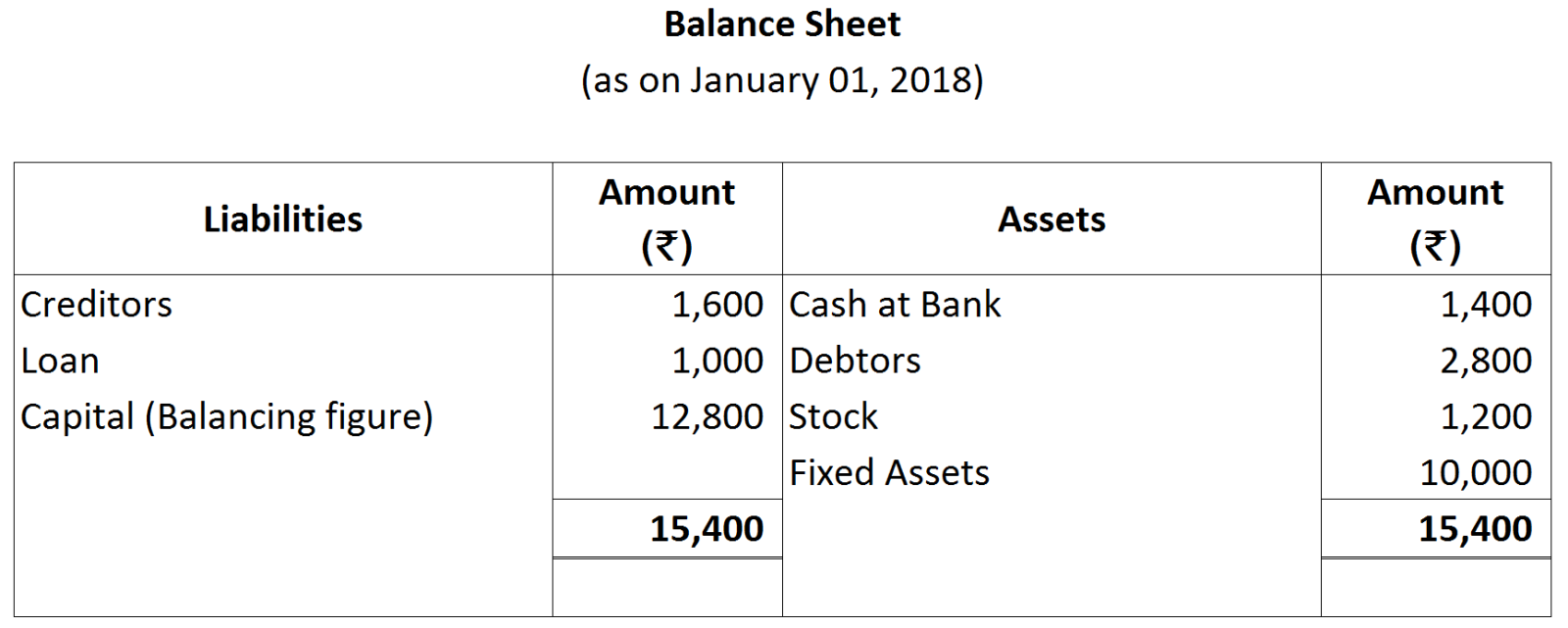

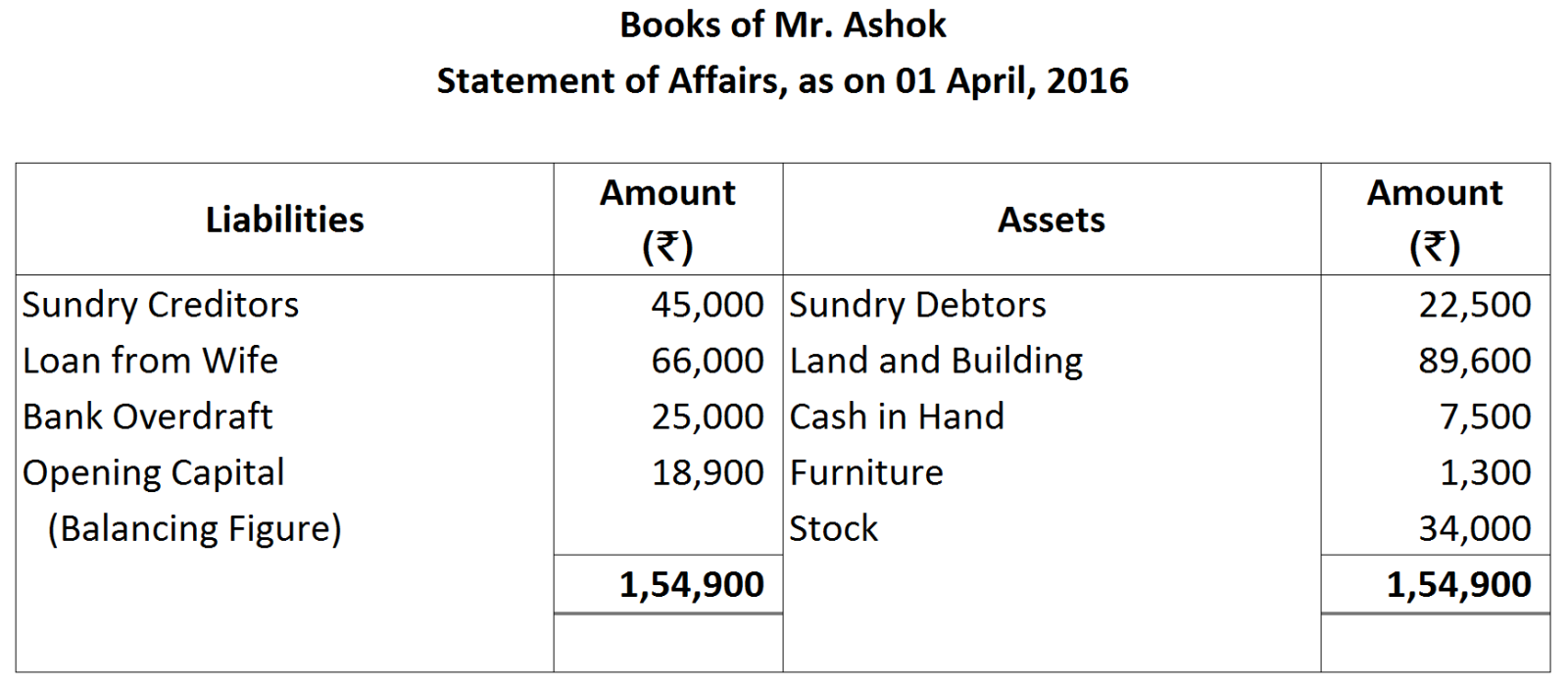

- Opening Capital.

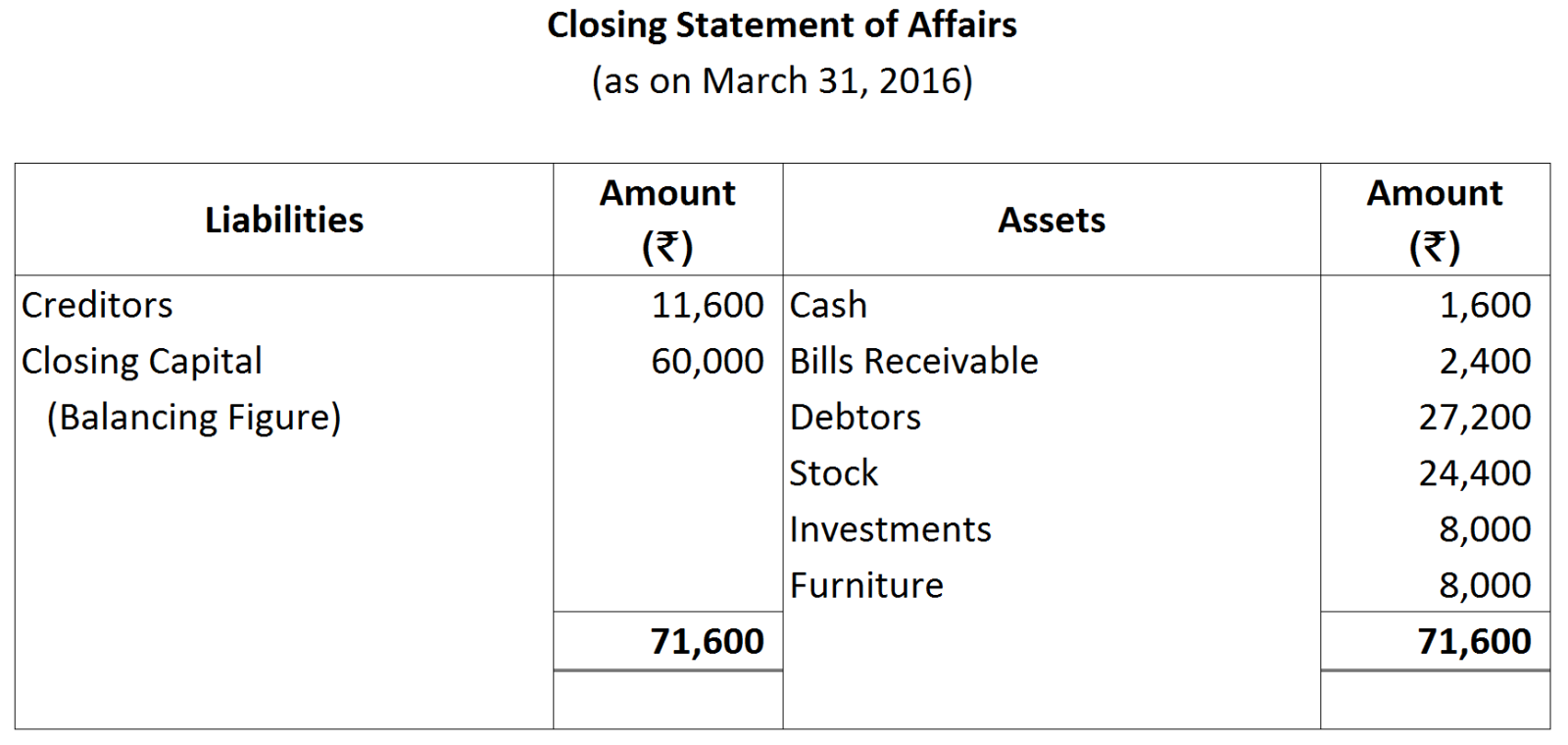

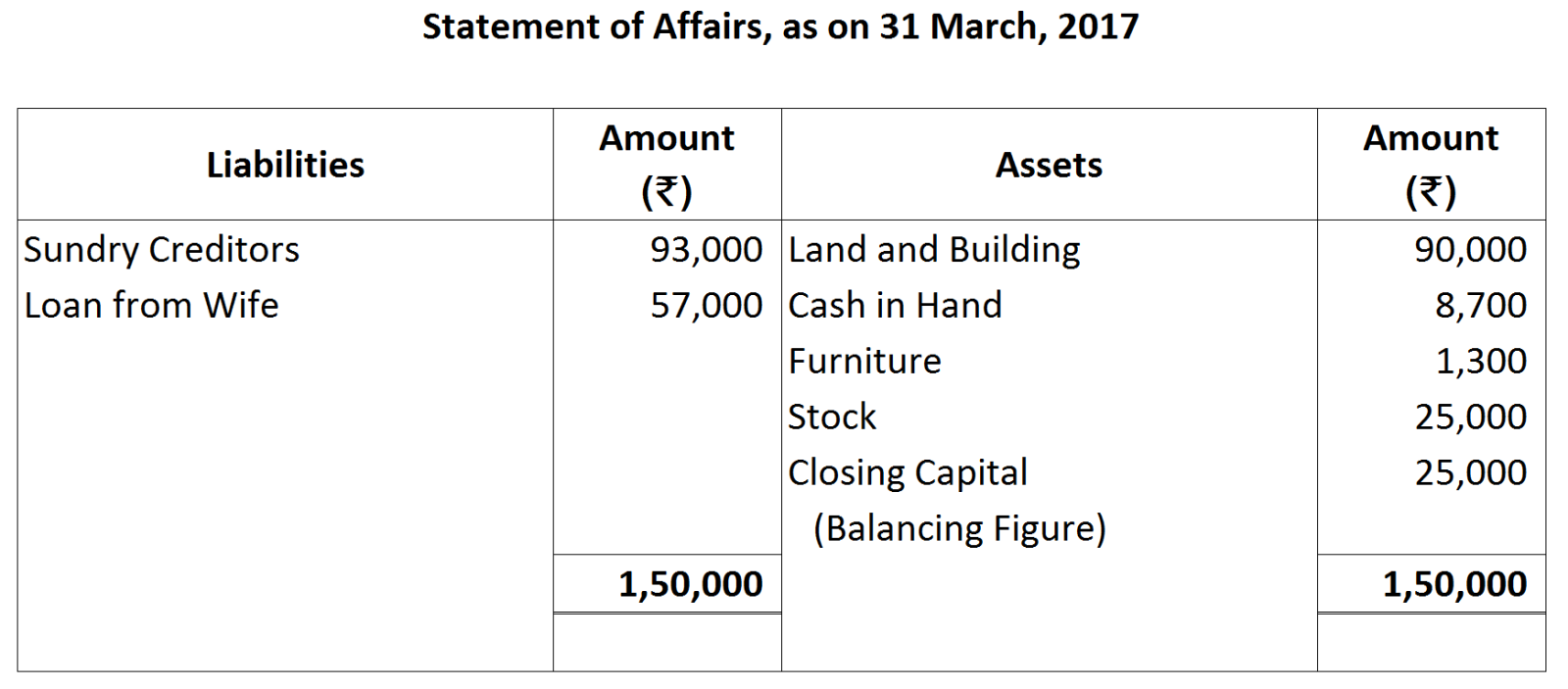

- Closing Capital.

- Credit Purchases.

- Cash Purchases.

- Credit Sales.

- Cash Sales.

- Payment from Debtors.

- Payment to Creditors.

- Opening Stock.

- Closing Stock.

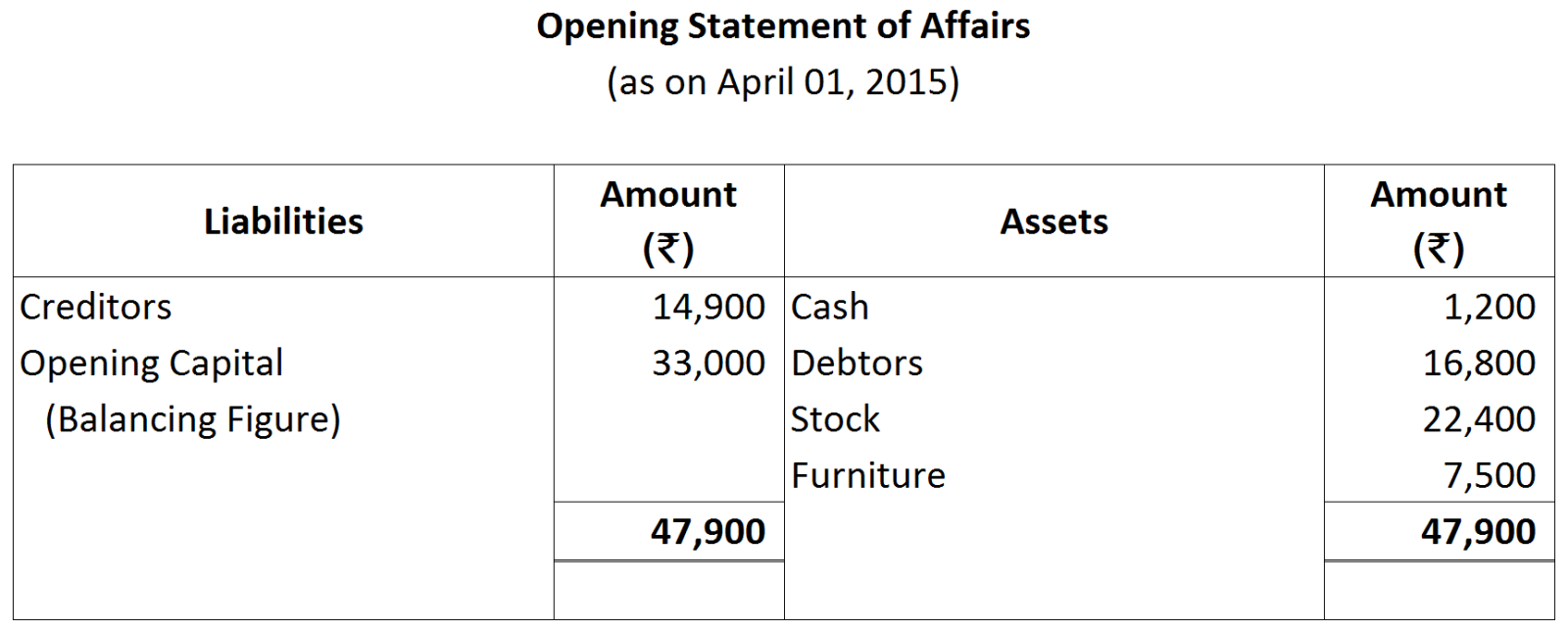

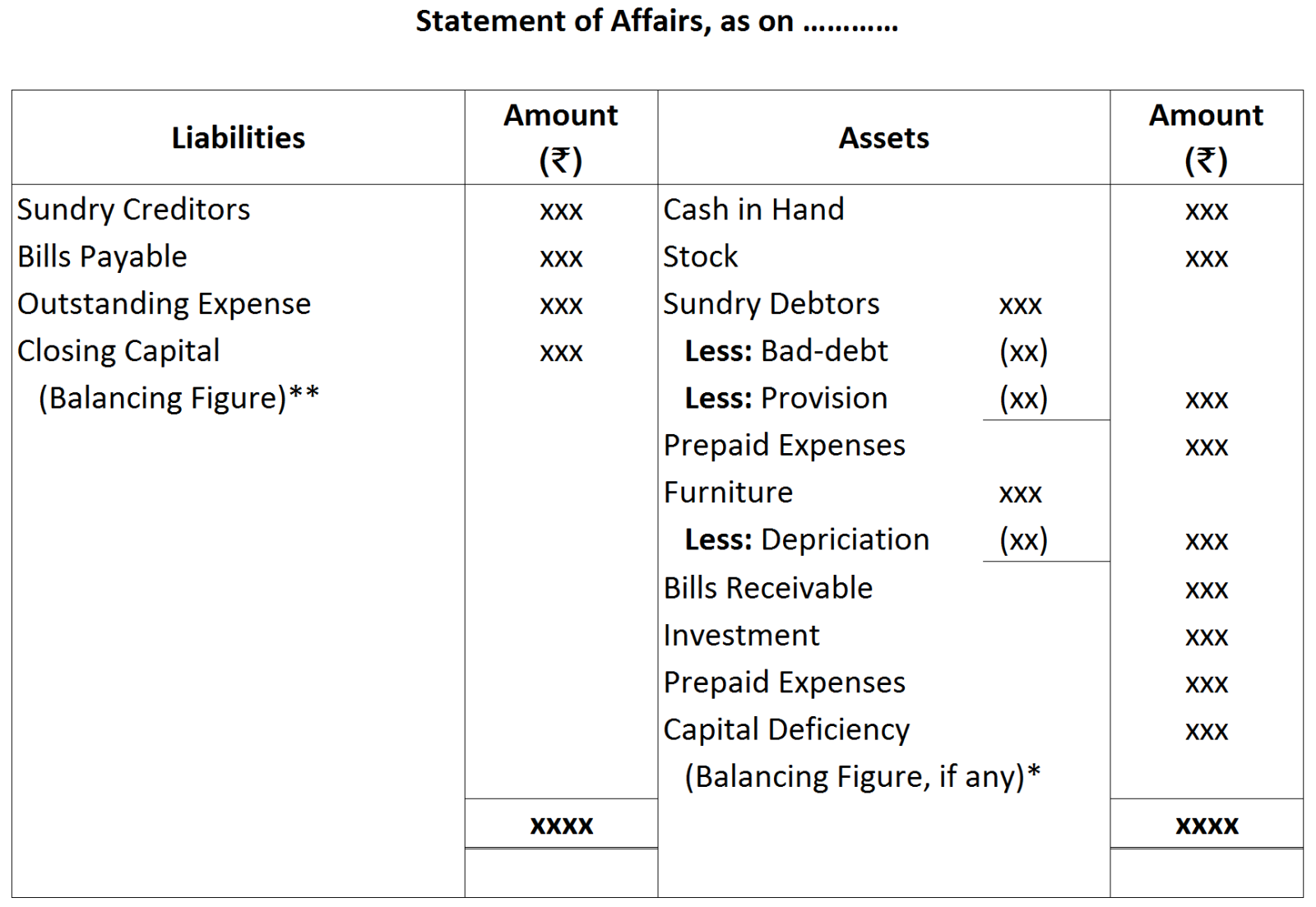

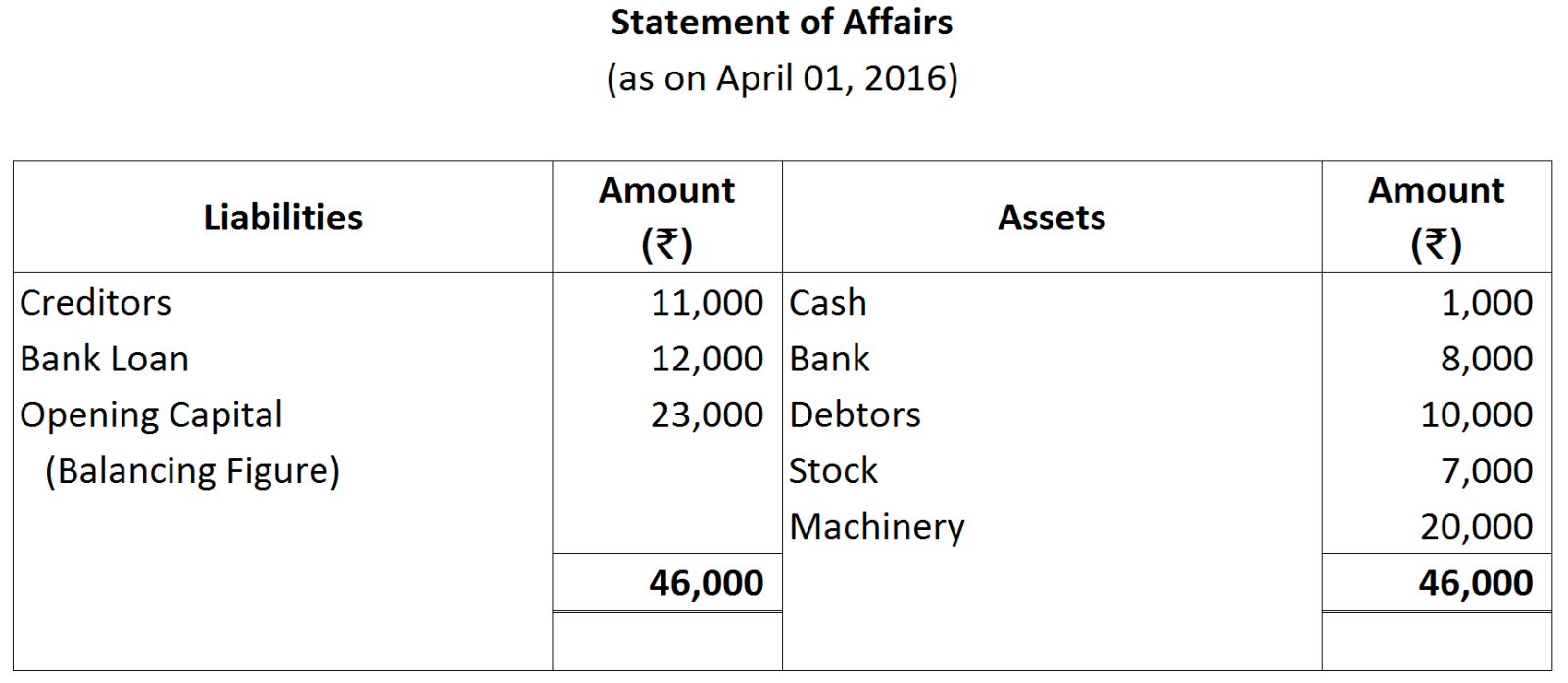

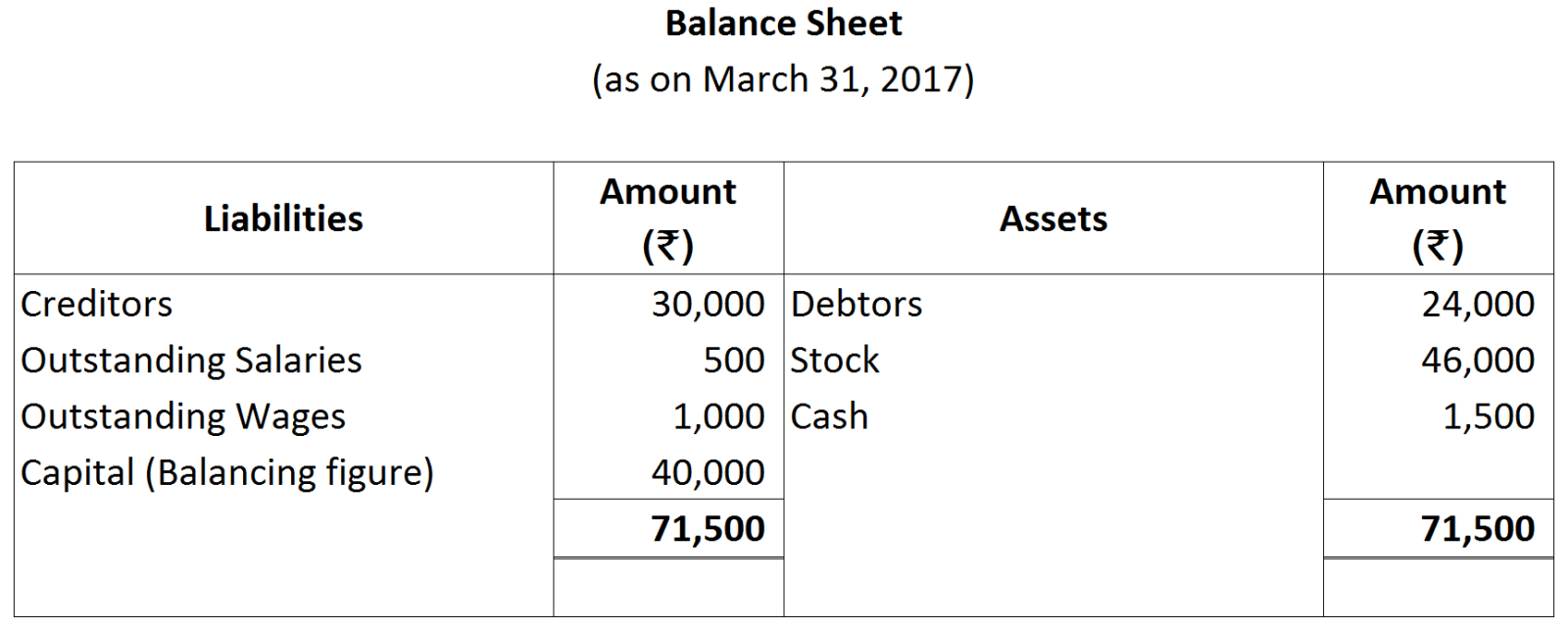

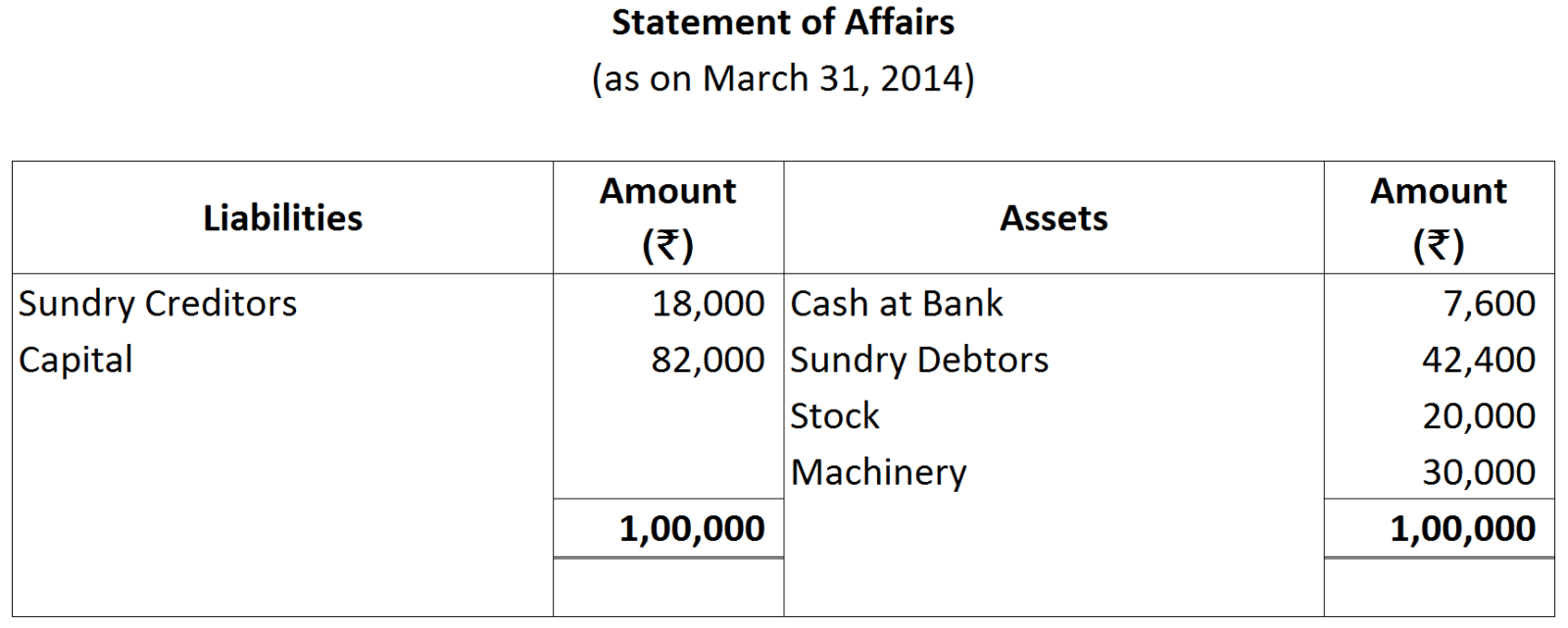

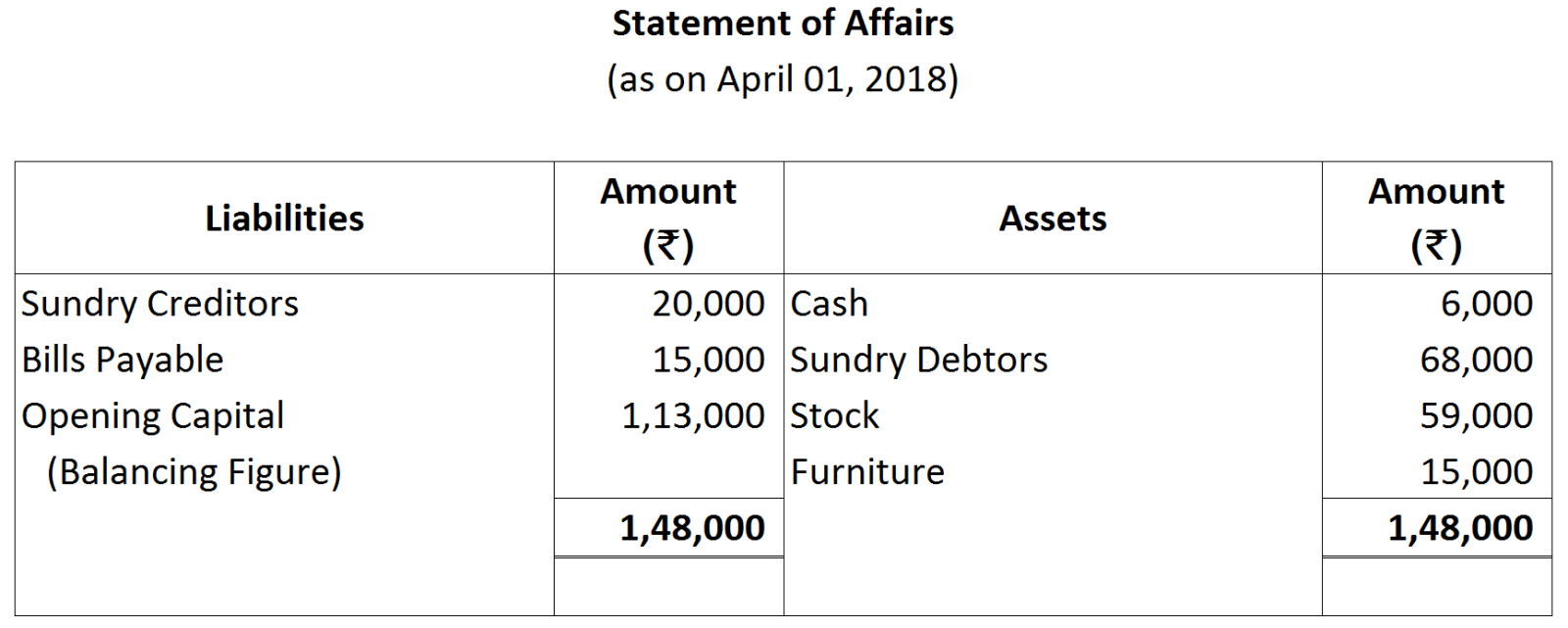

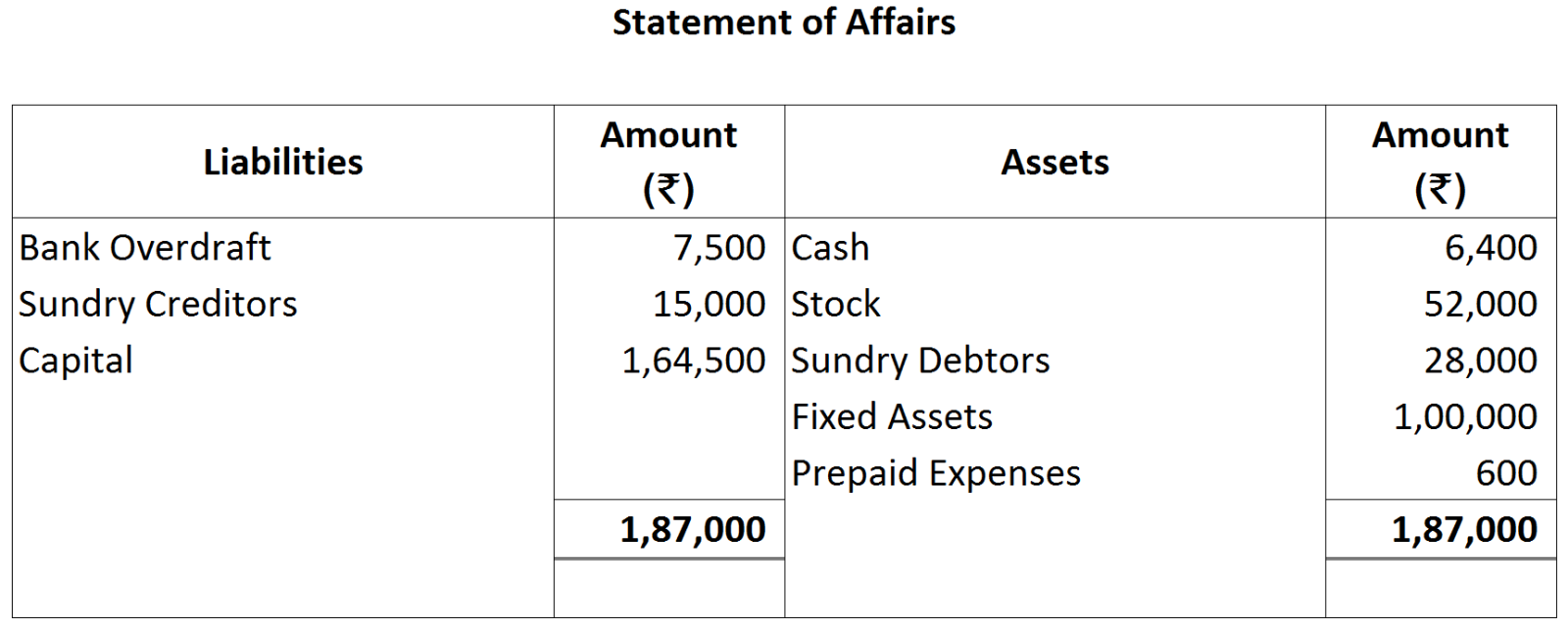

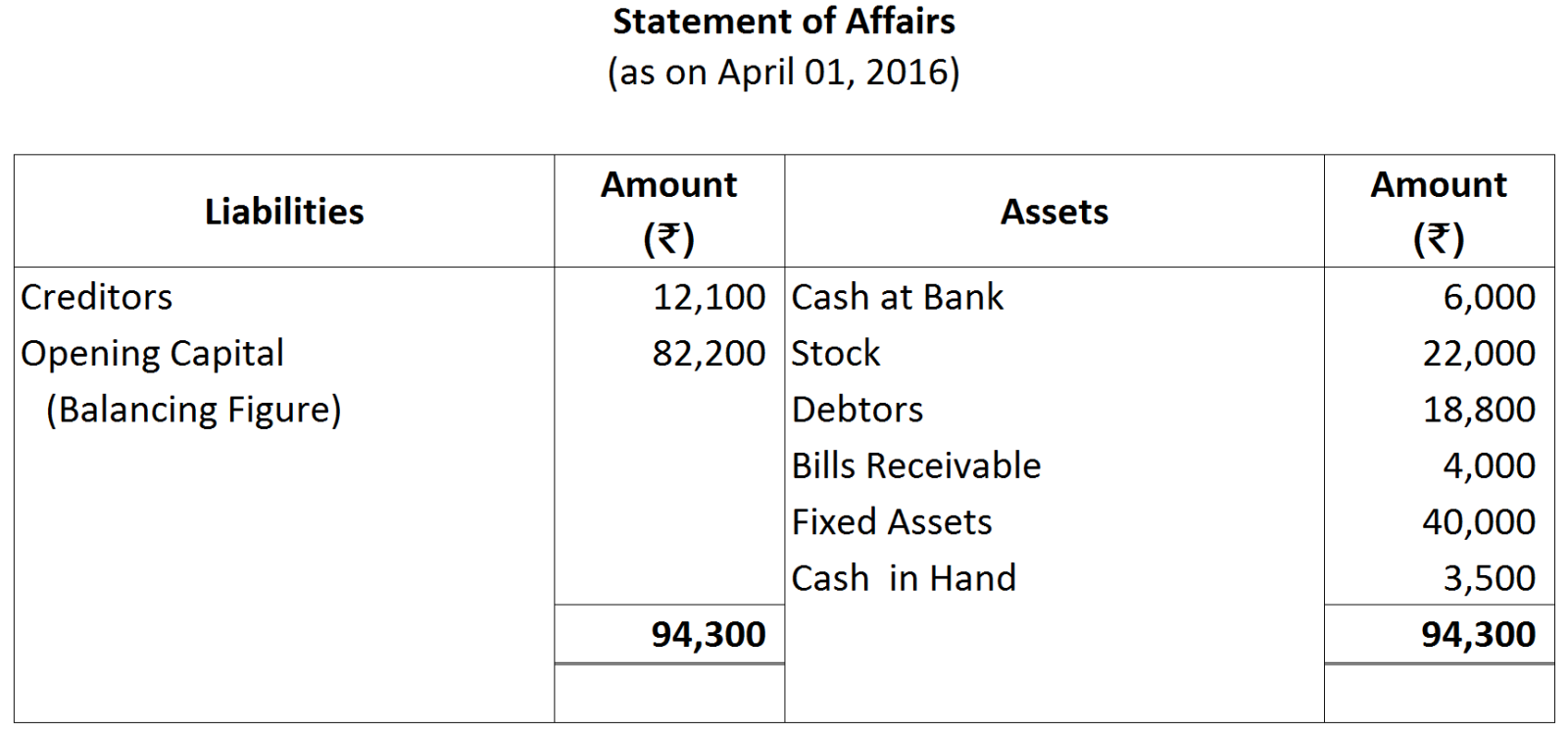

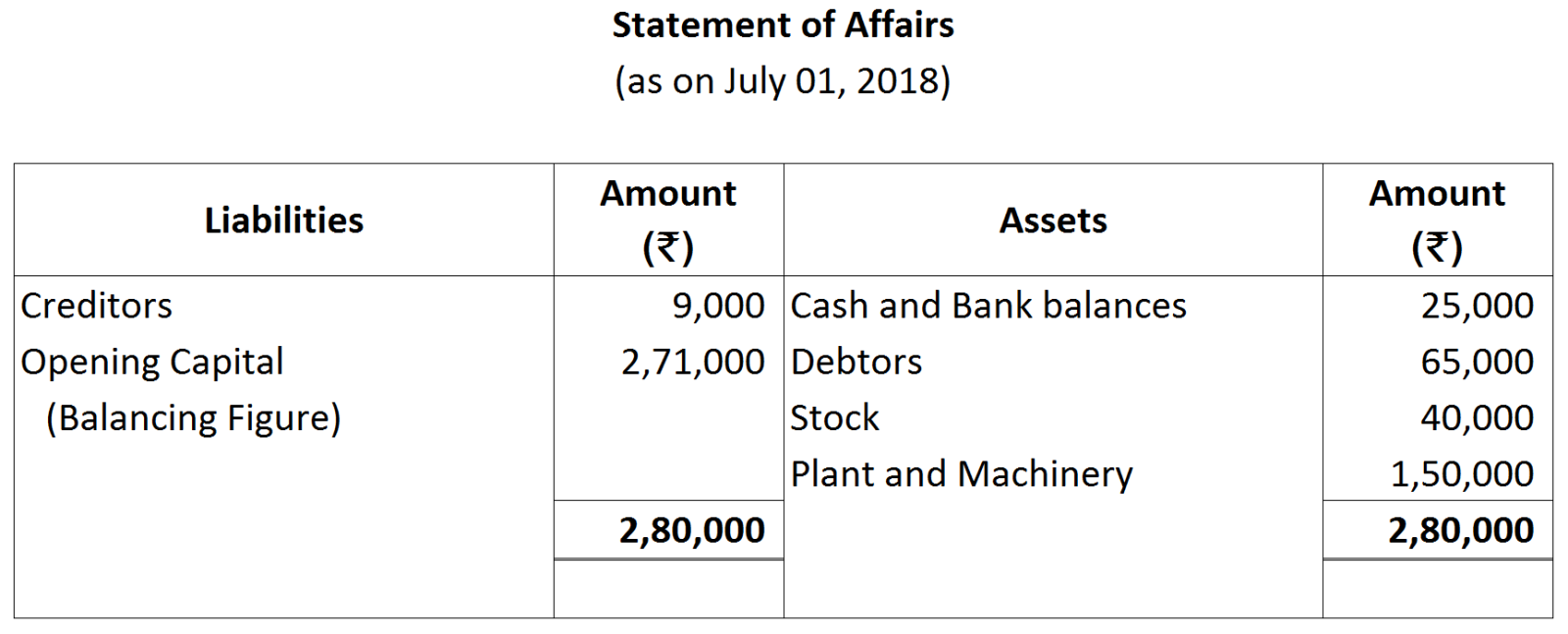

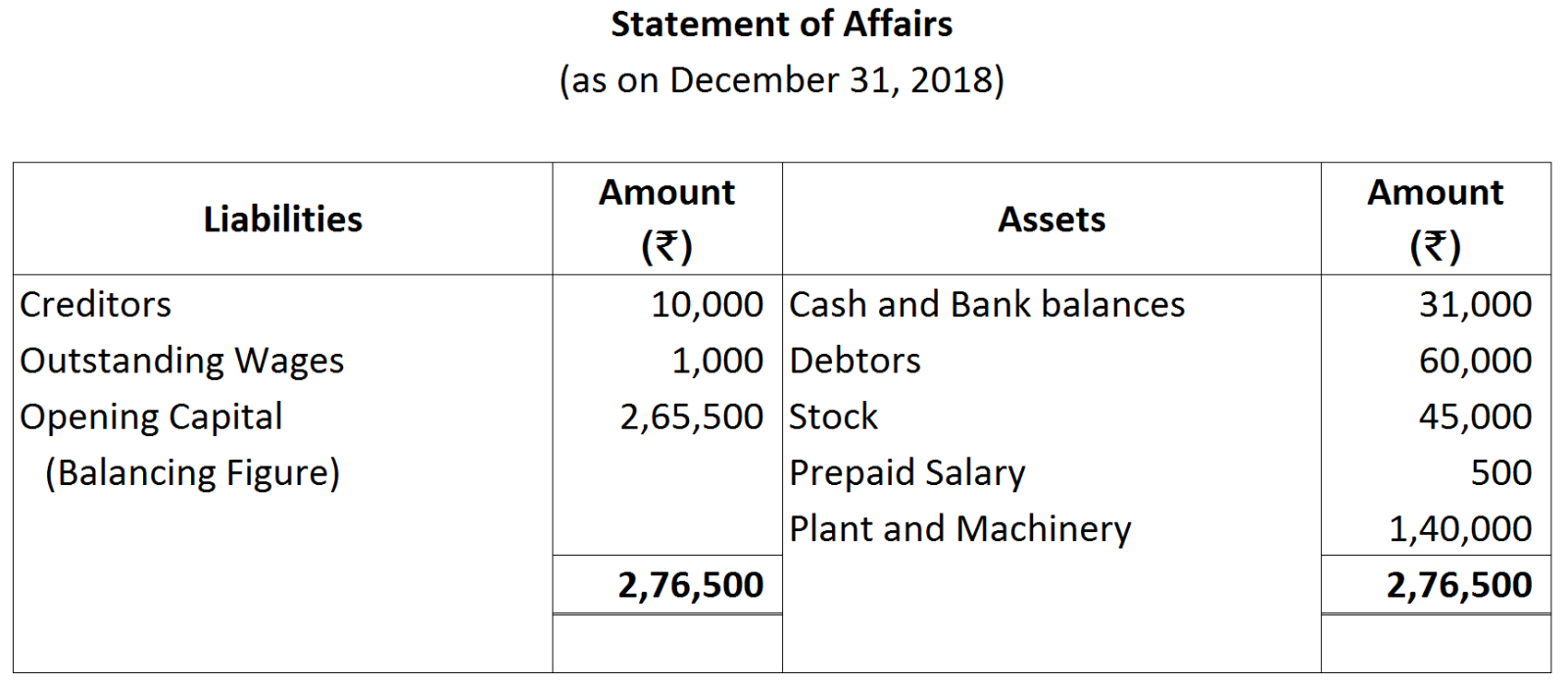

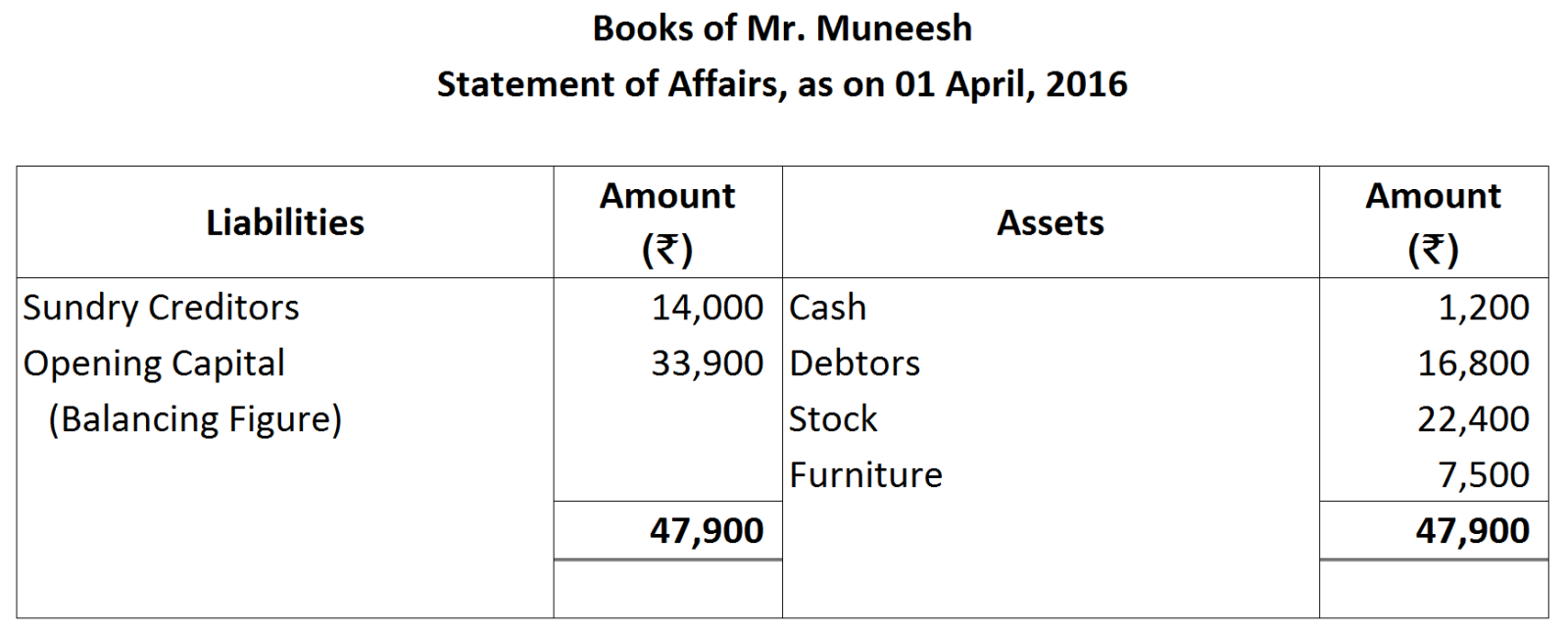

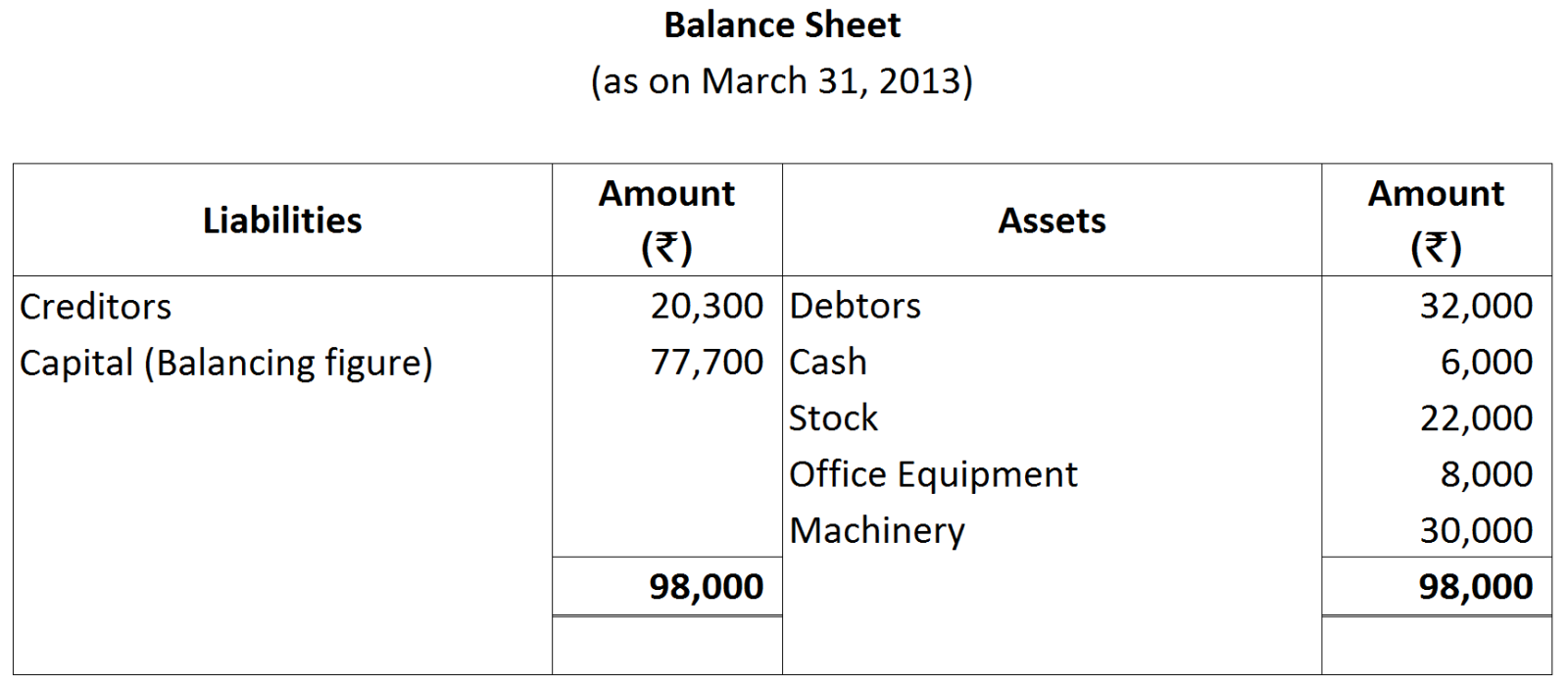

- If opening capital is not given, then the first step is to prepare opening Statement of Affairs that gives the Opening Capital.

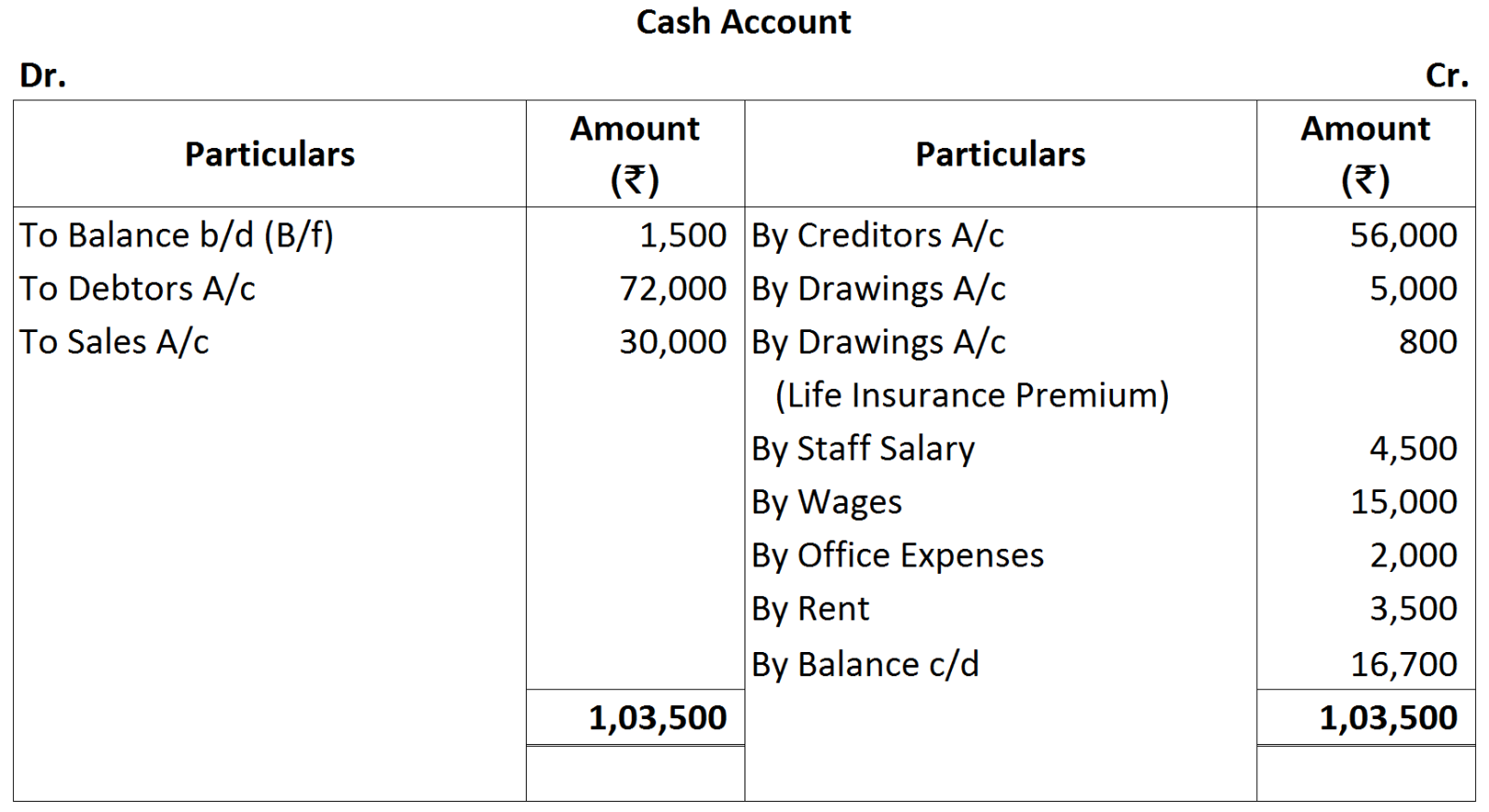

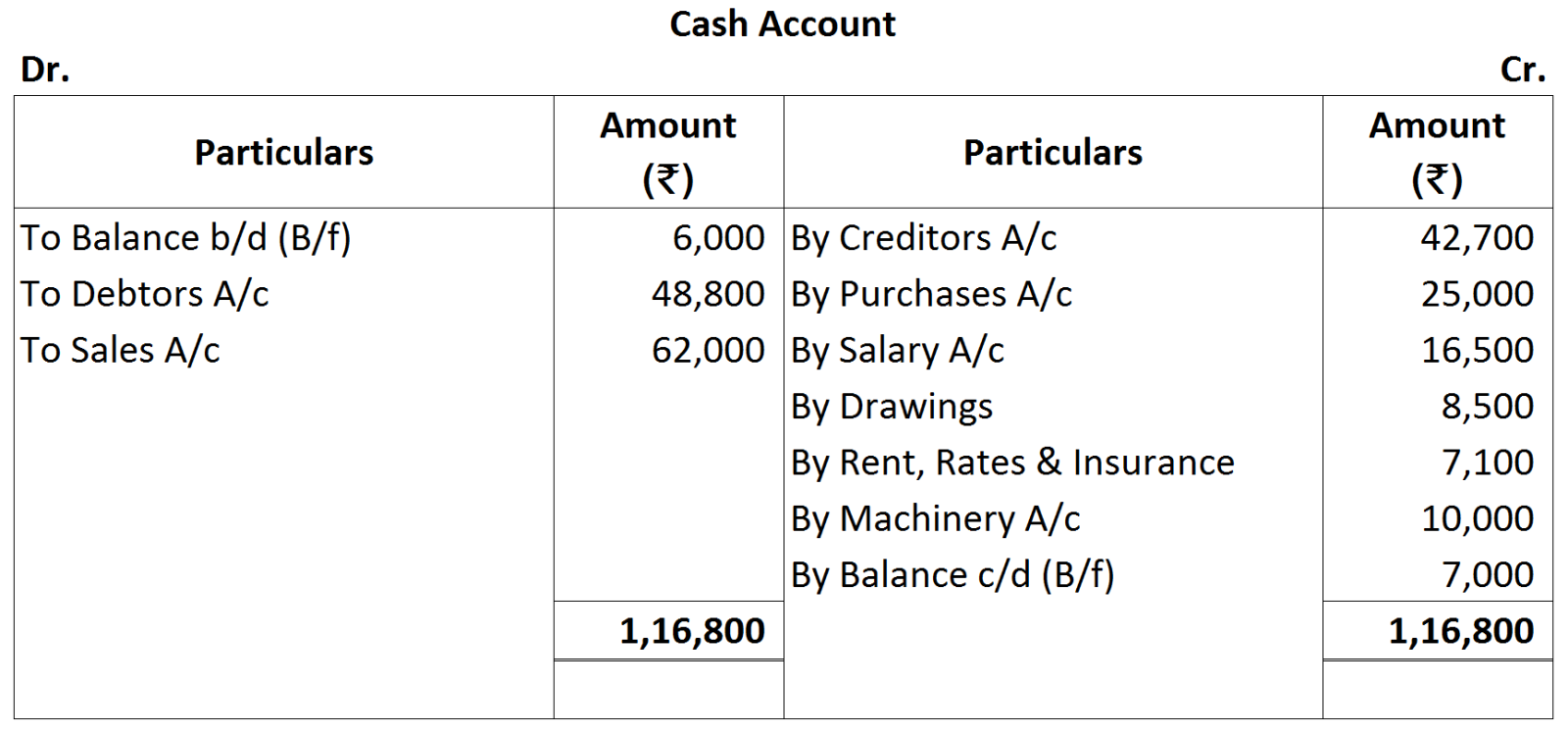

- The second step is to prepare Cash Book that gives the opening or the closing cash and bank balance.

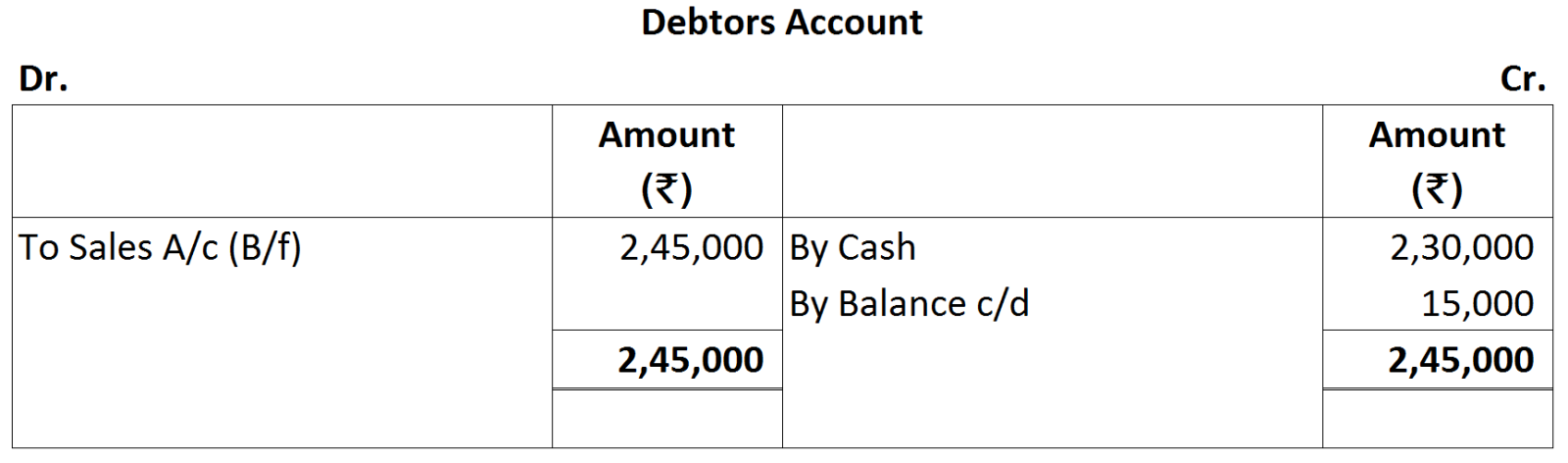

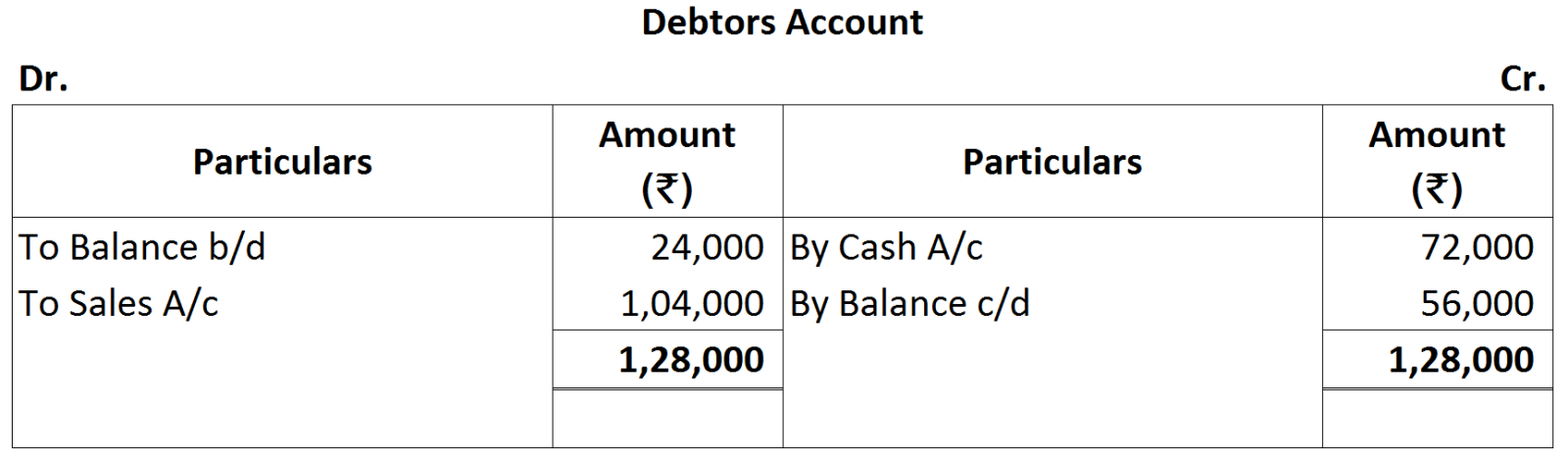

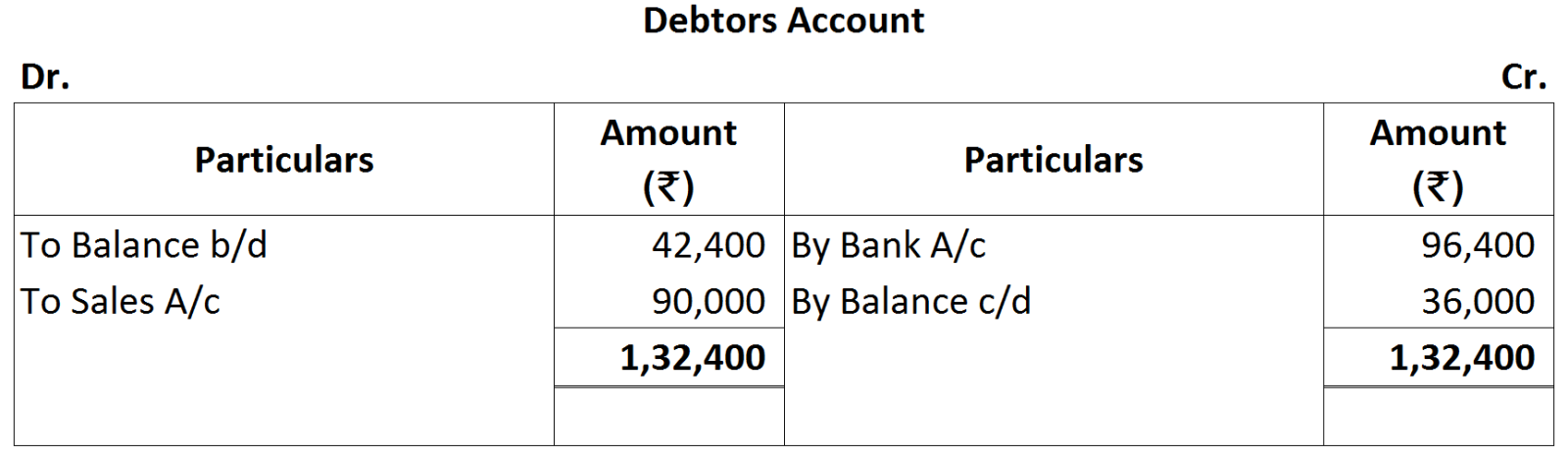

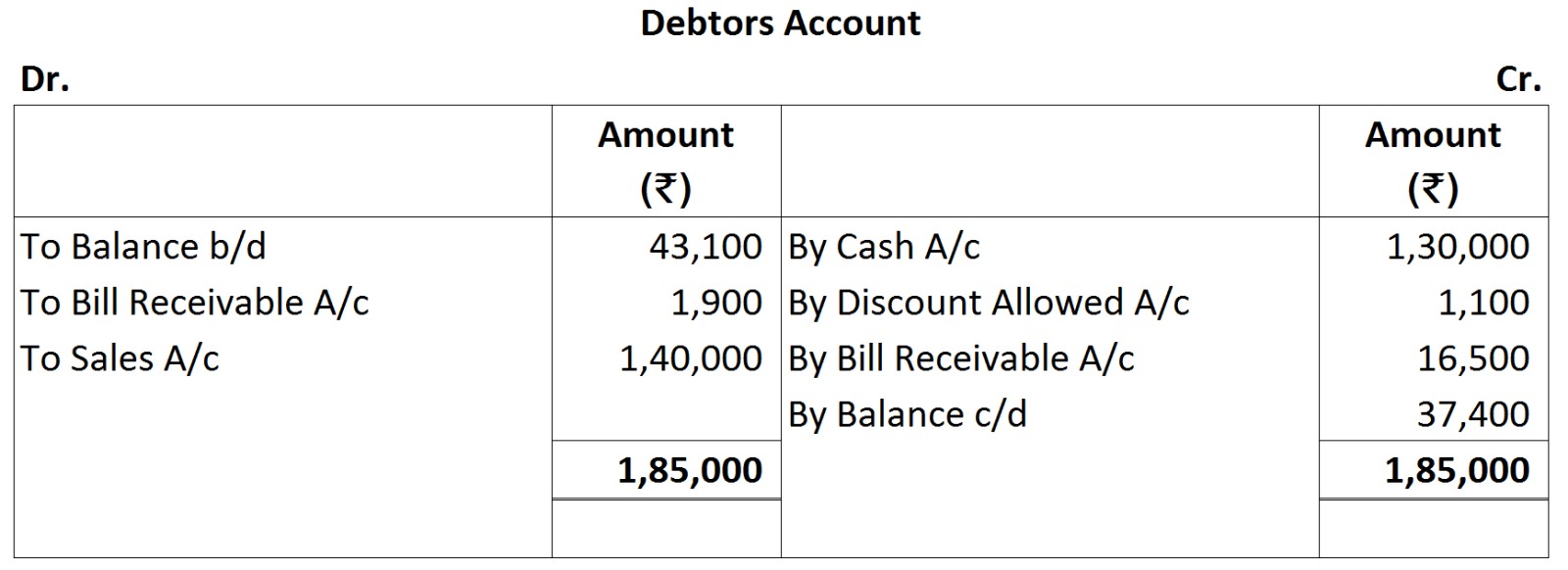

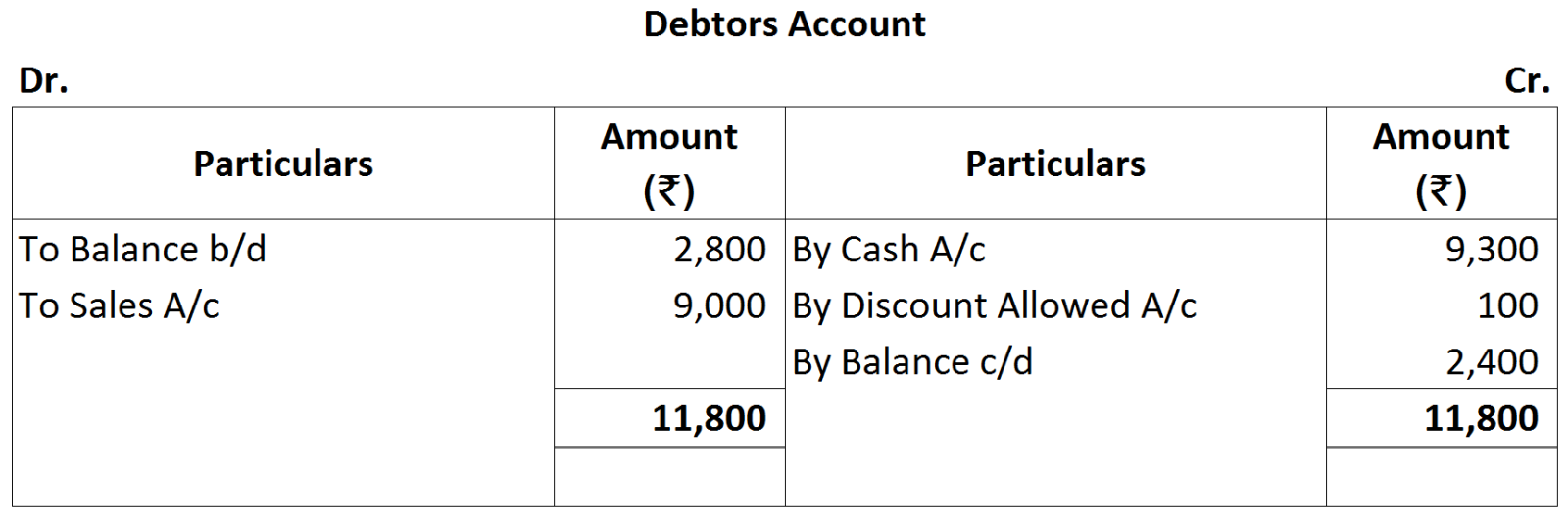

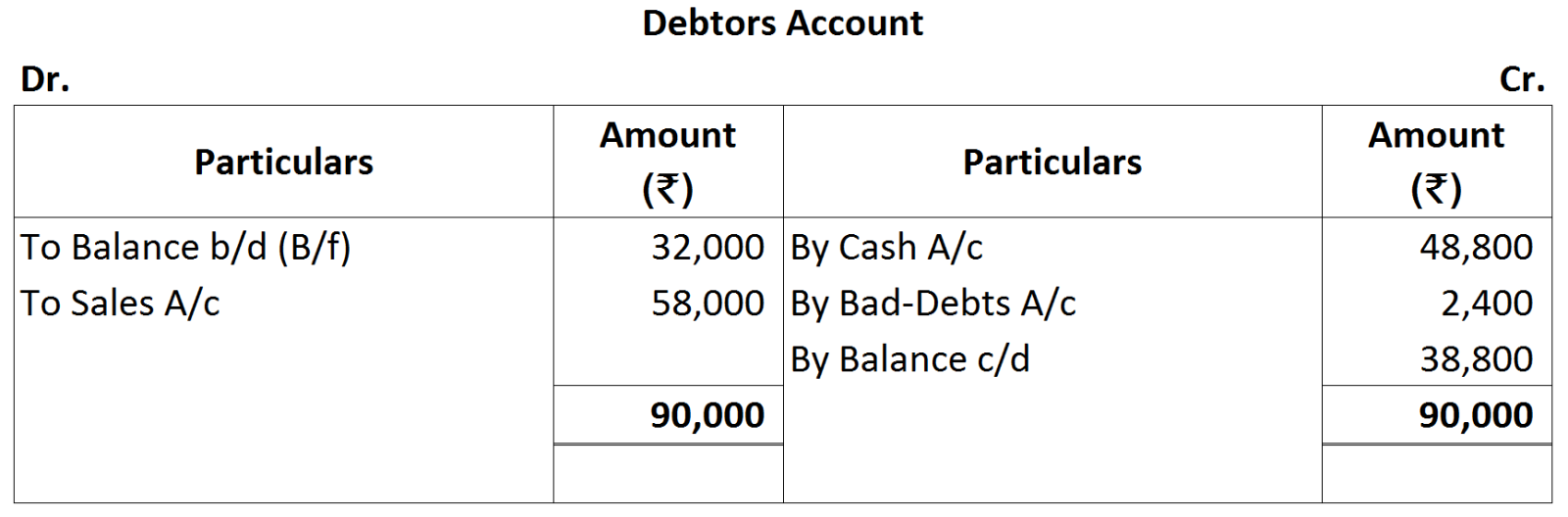

- The next step is to prepare Total Debtors Account. It is prepared in order to find out one of the missing figures, such ascredit sales, opening debtors, closing debtors and cash received from debtors.

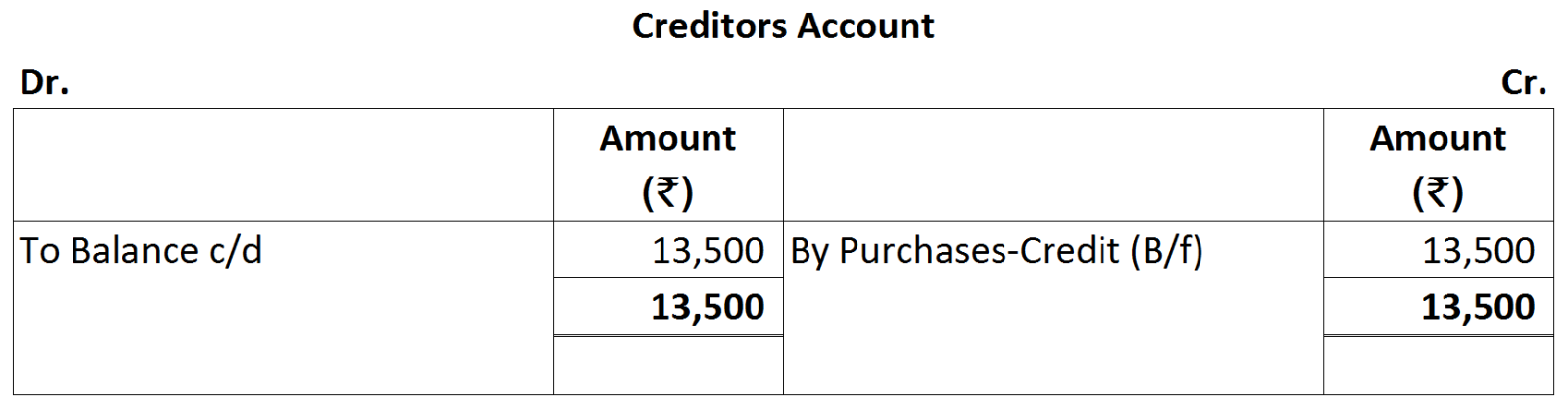

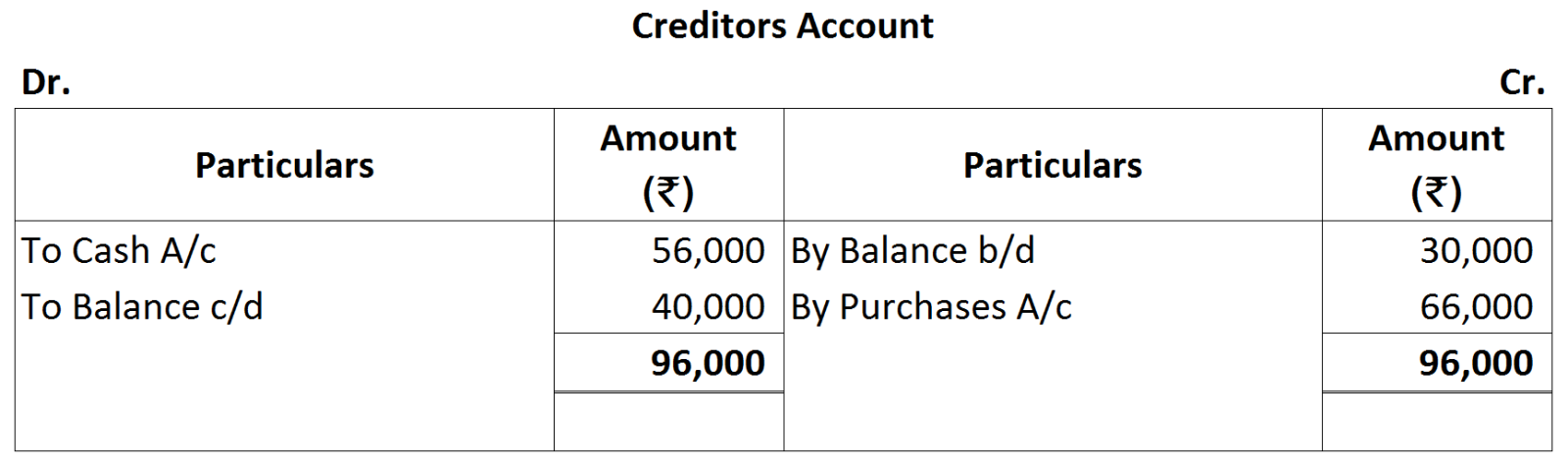

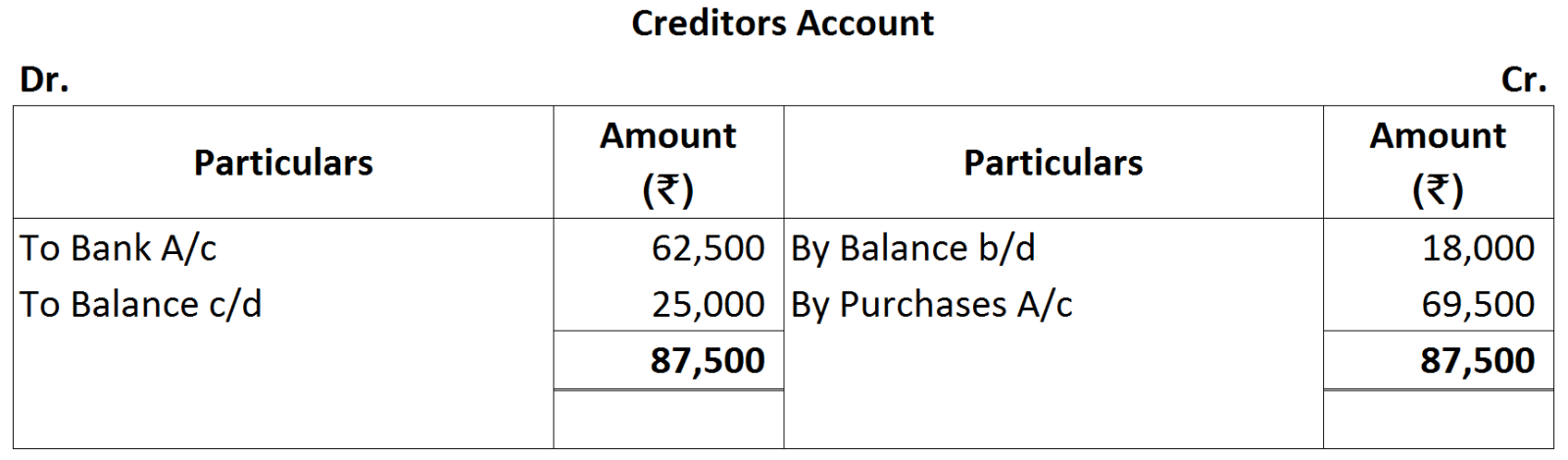

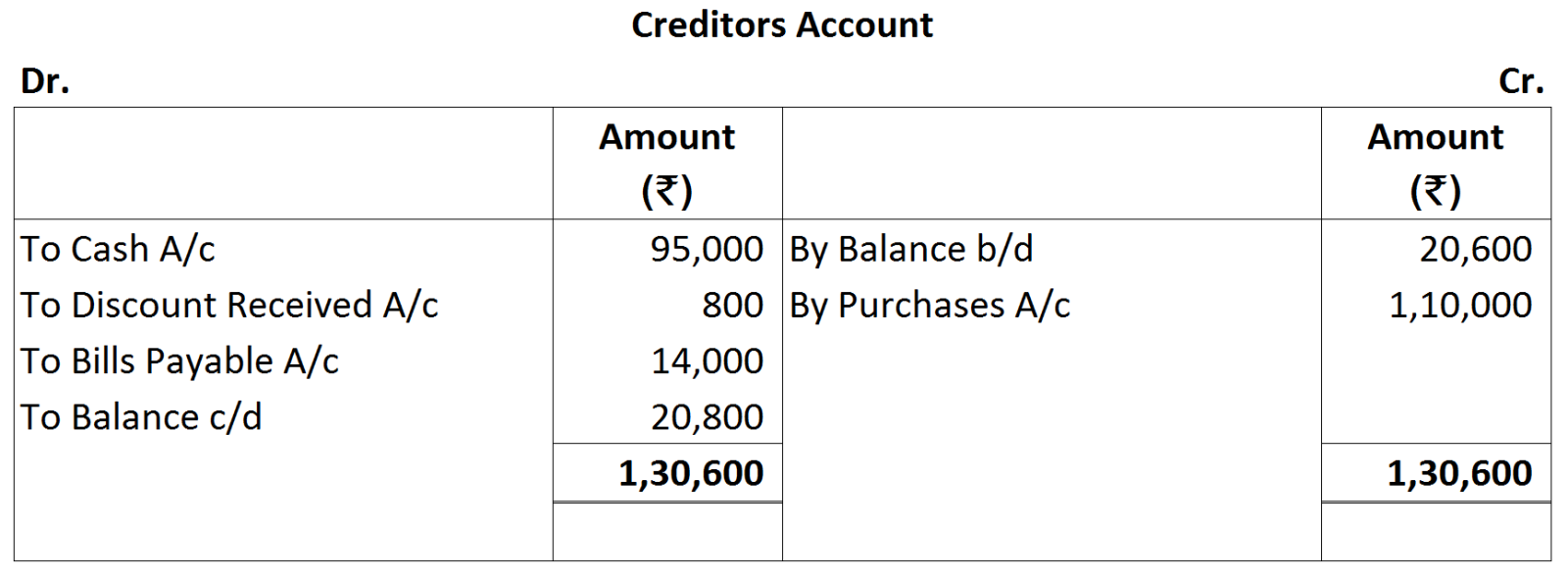

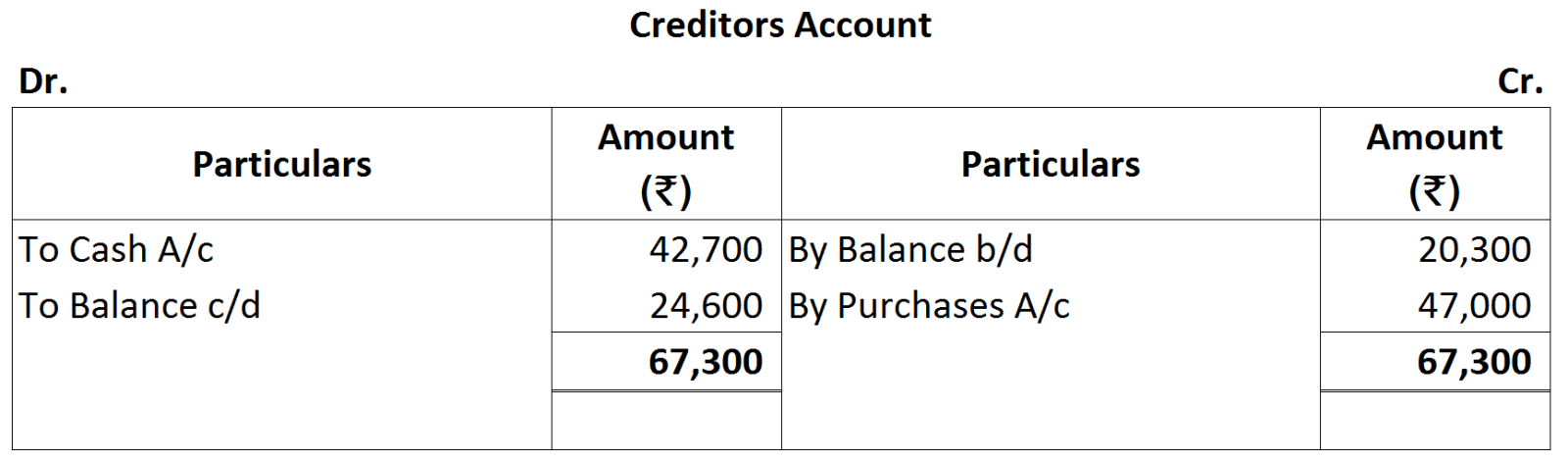

- The subsequent step is to prepare Total Creditors Account to ascertain one of the missing figures, such as credit sales, opening creditors, closing creditors and cash paid to the creditors.

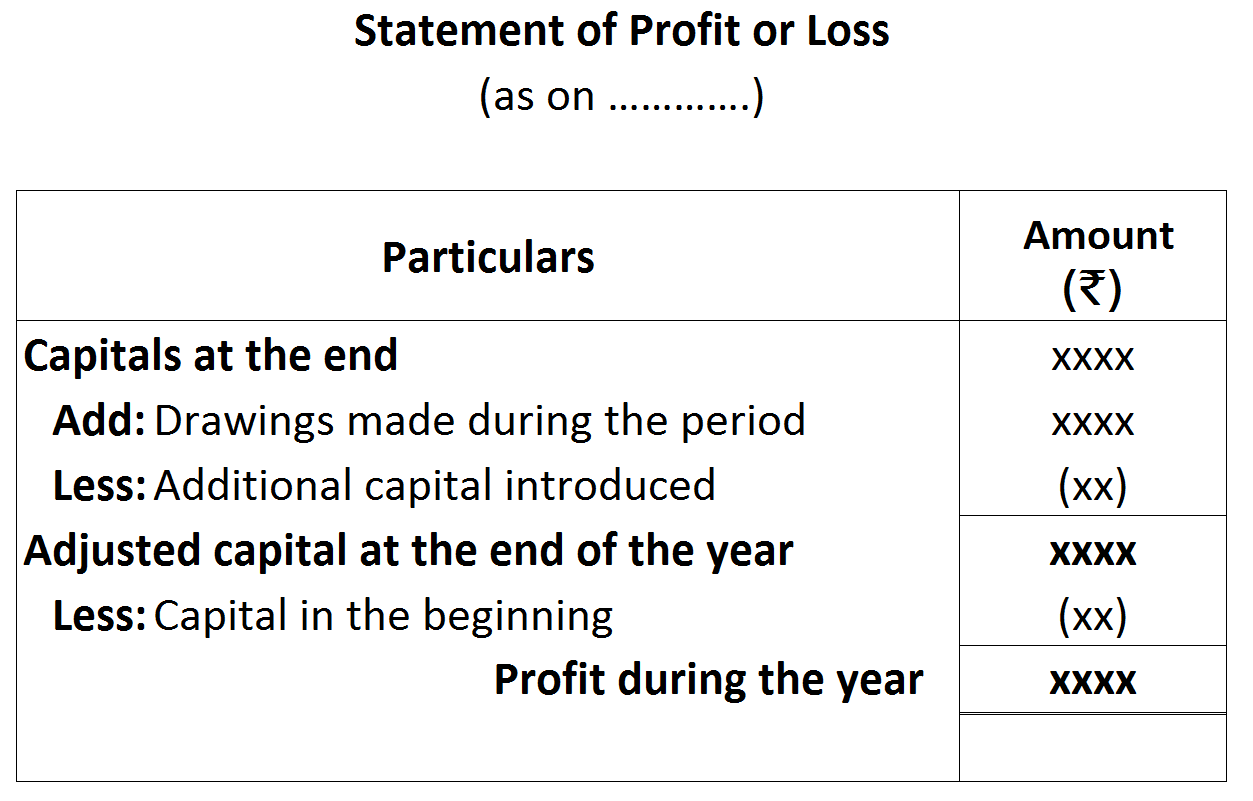

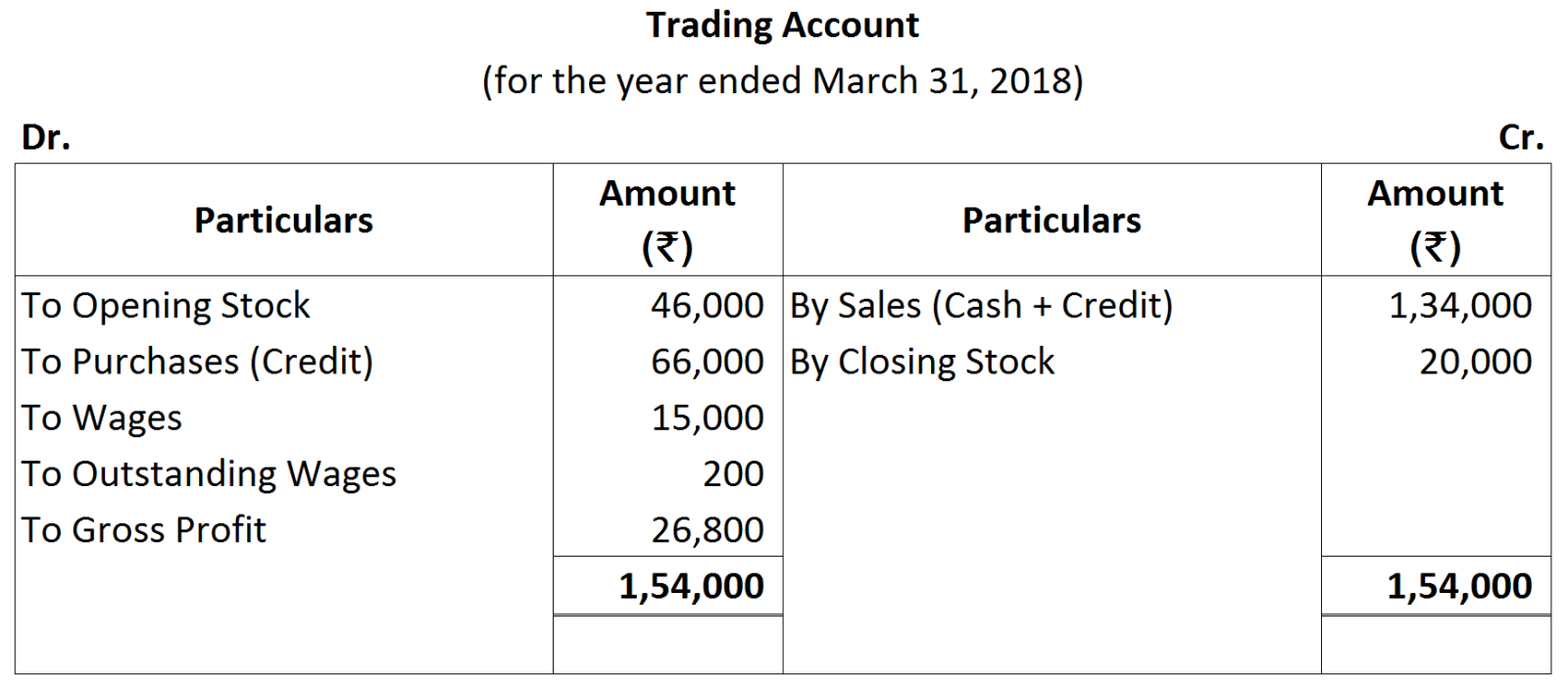

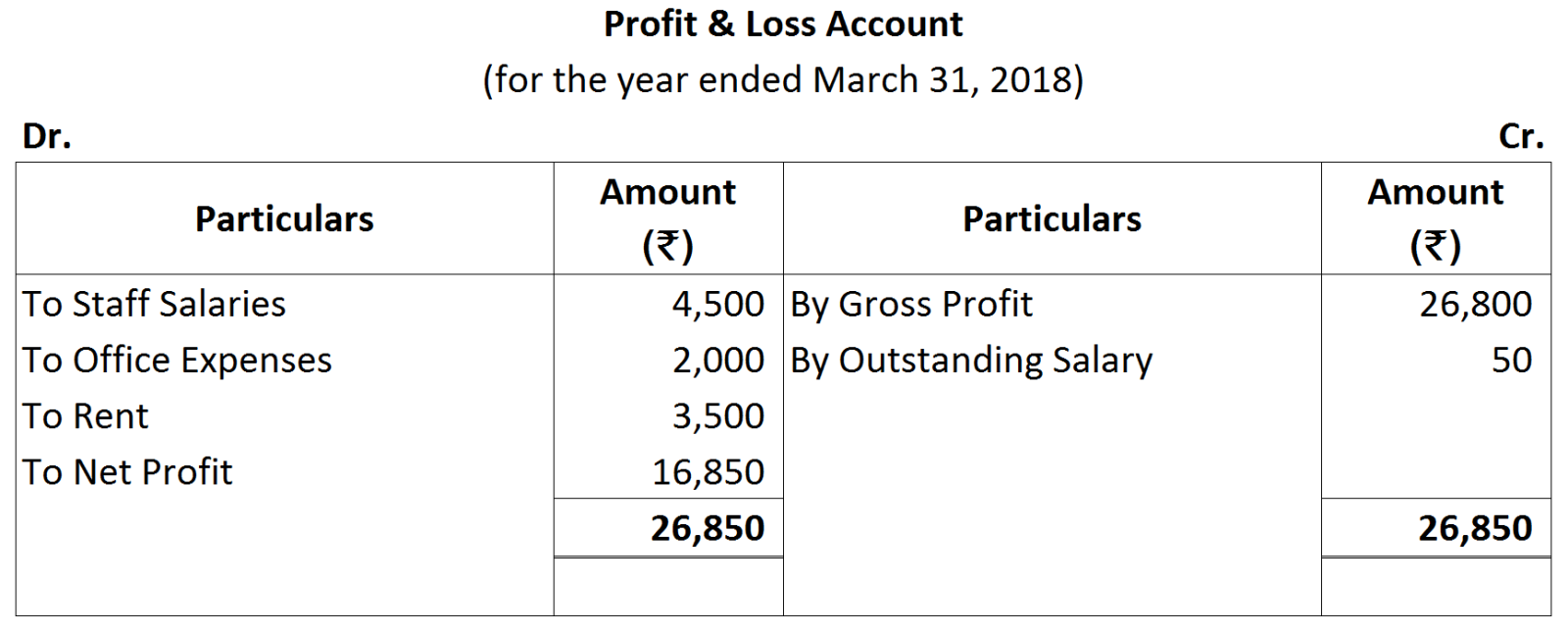

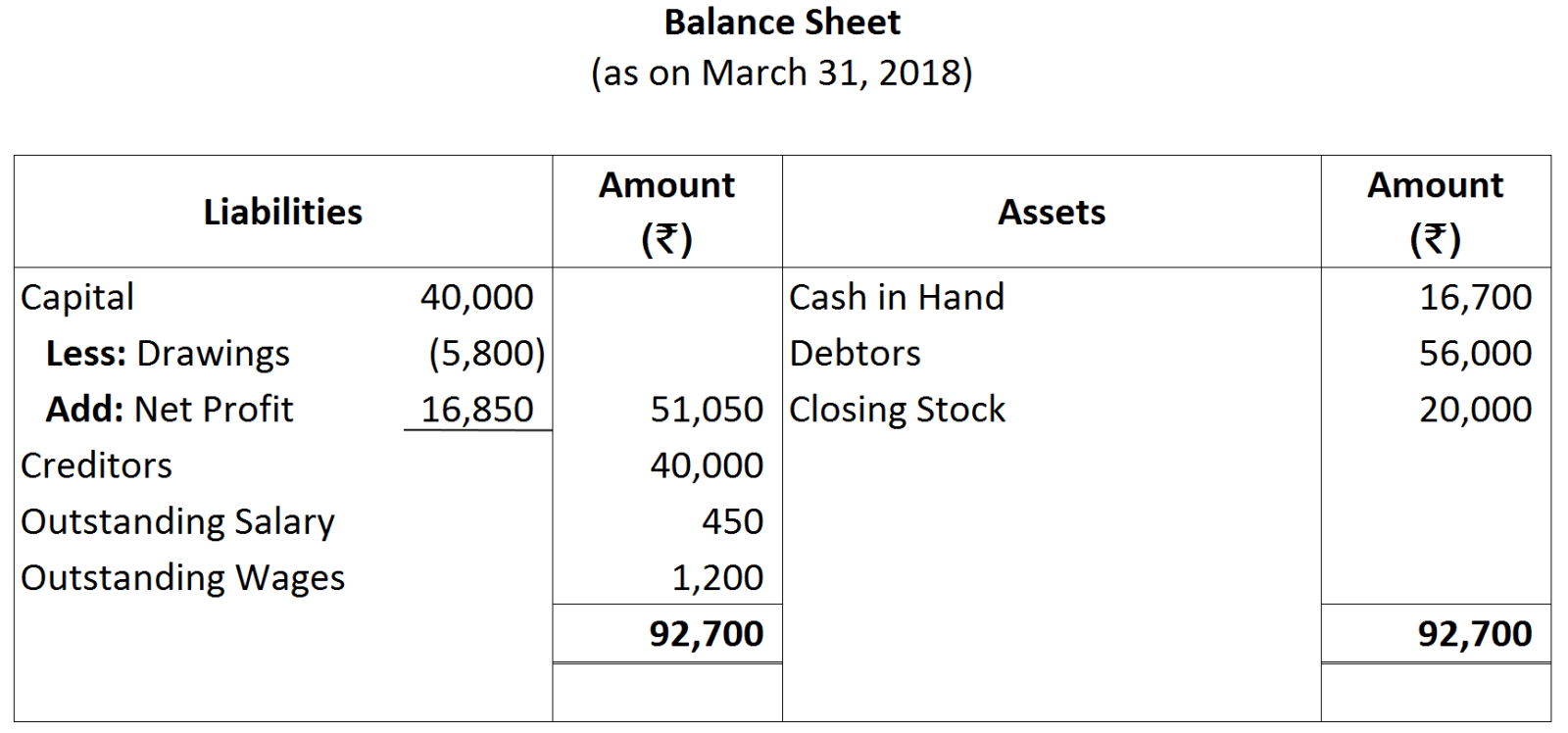

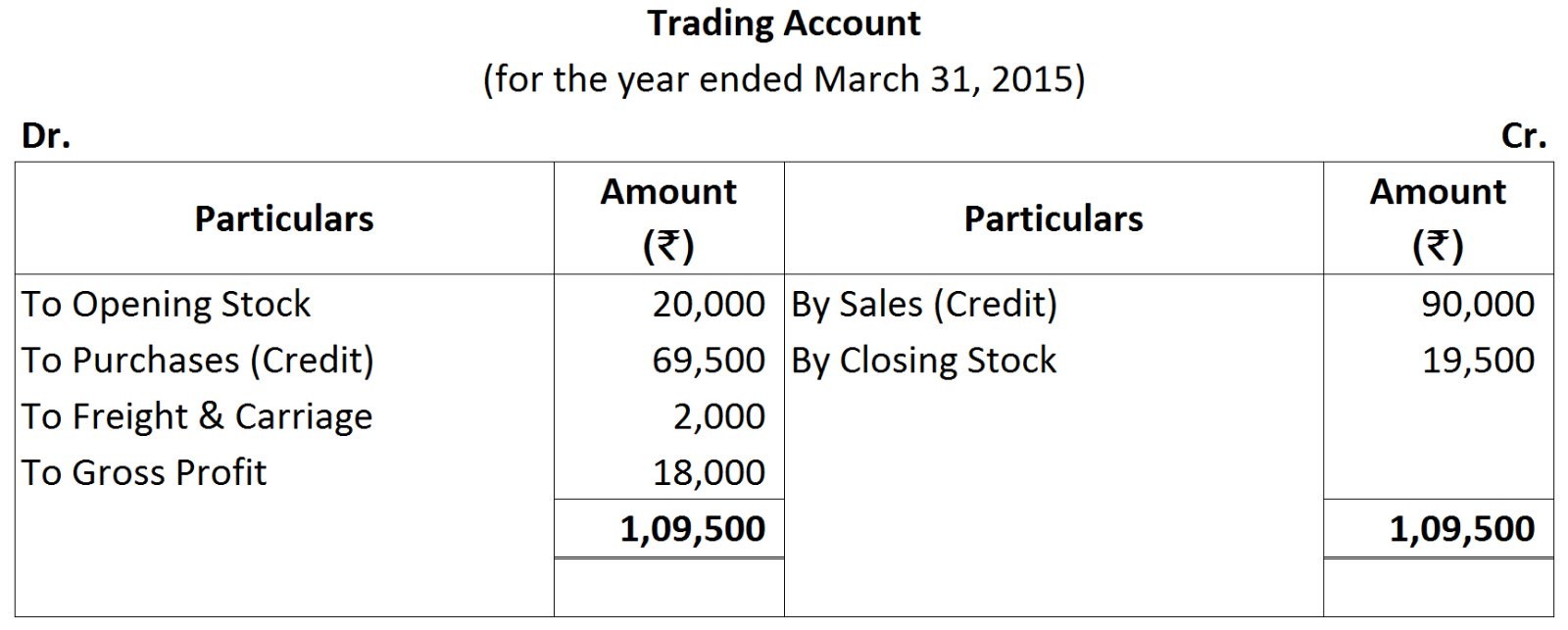

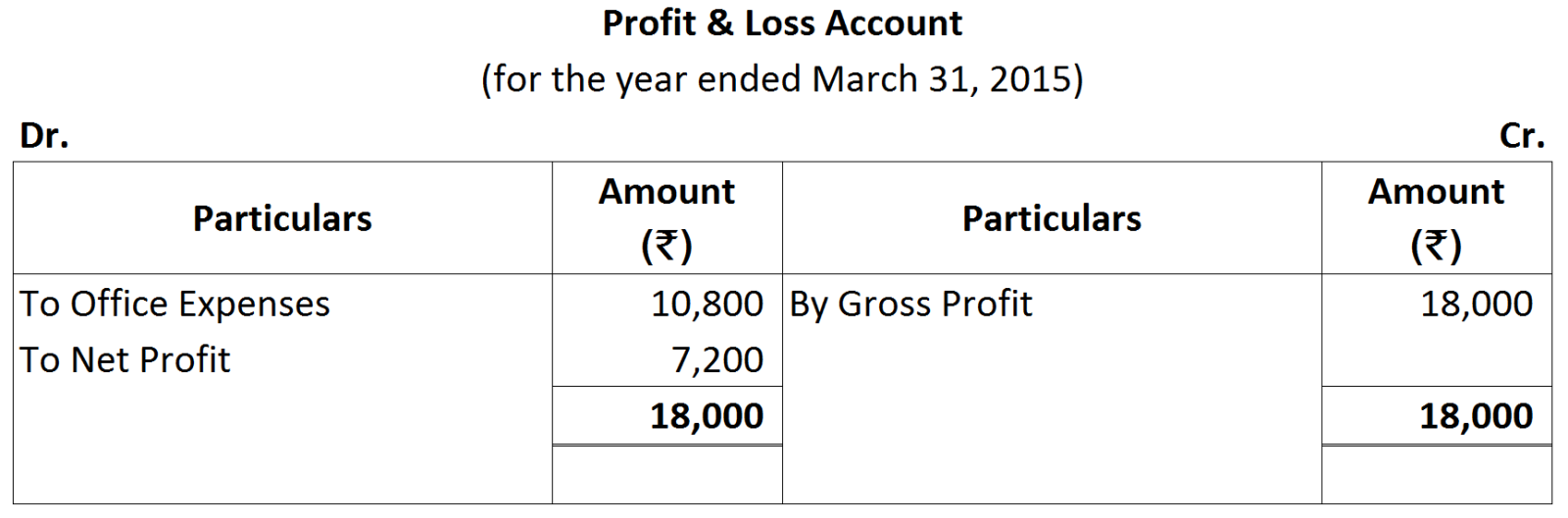

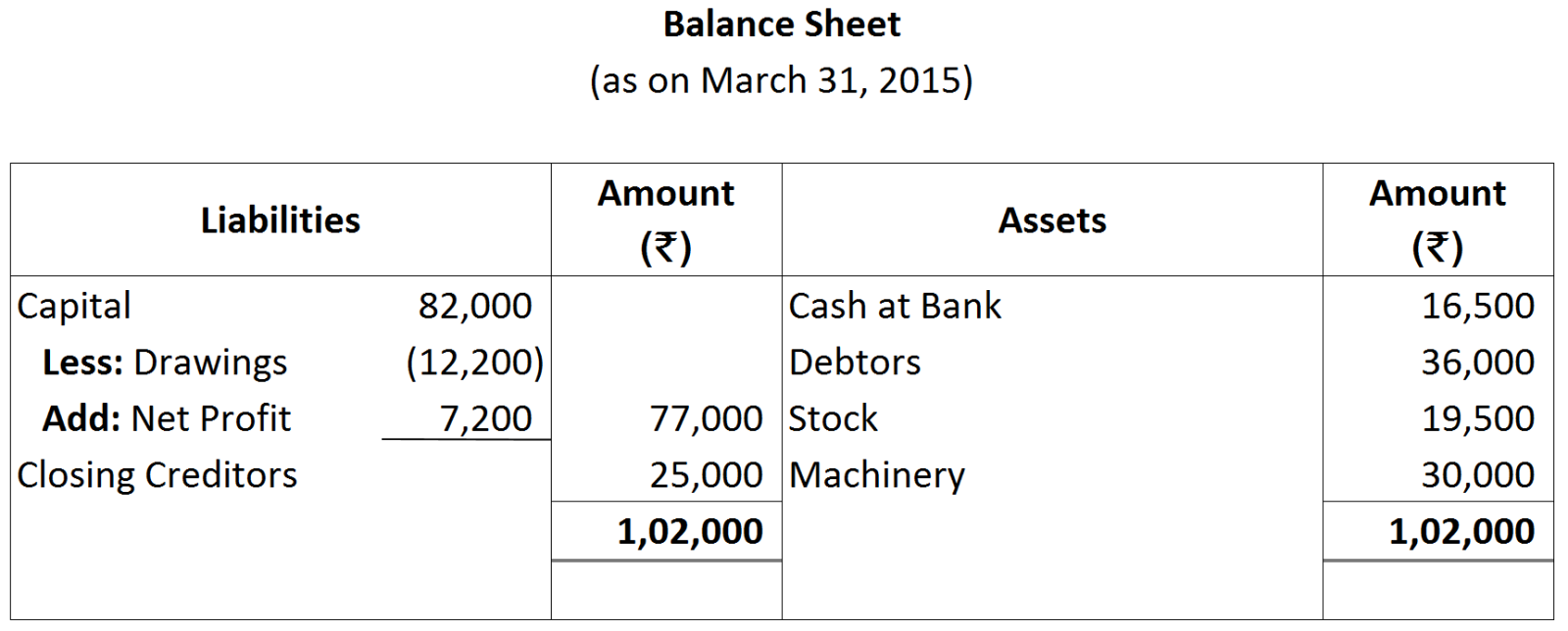

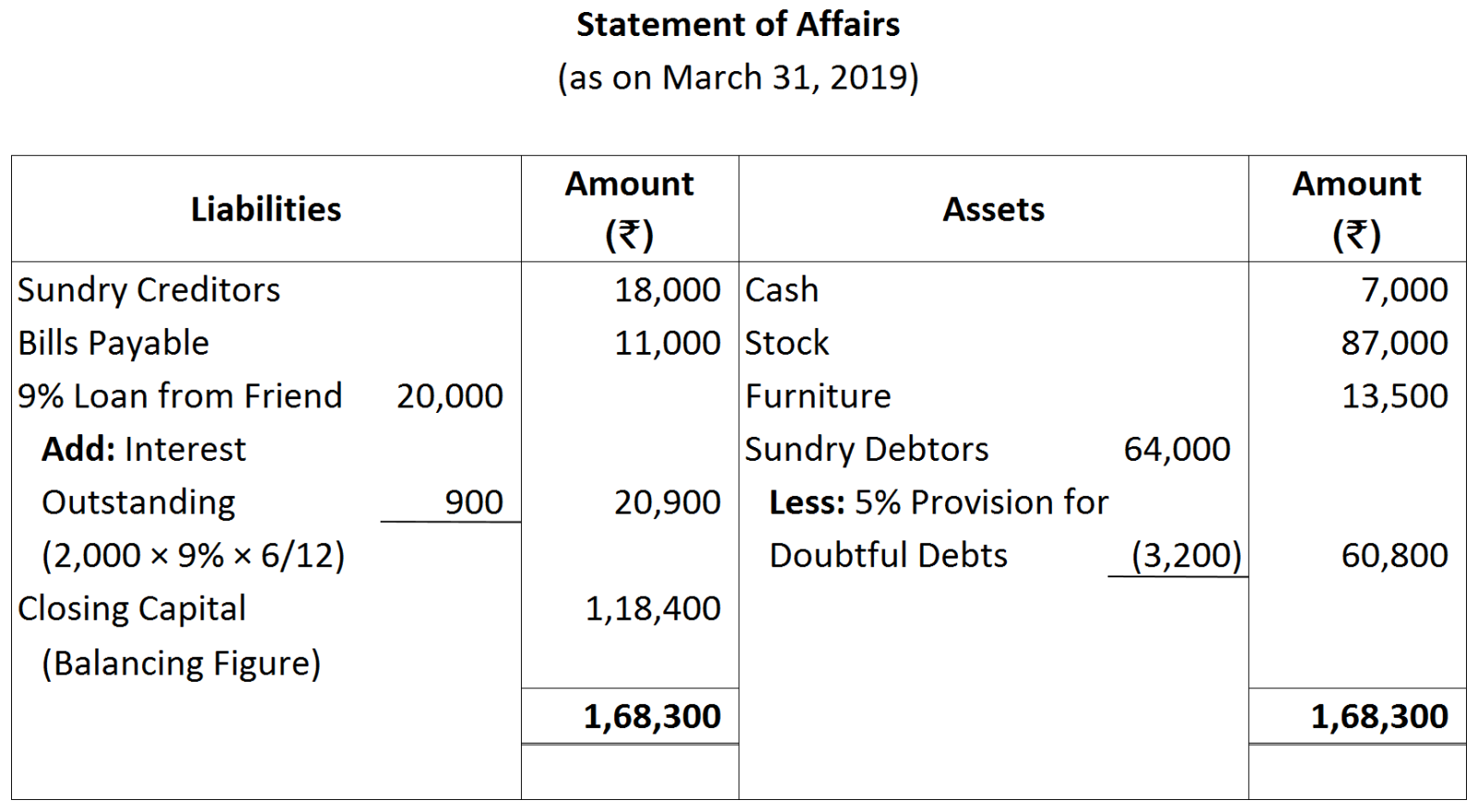

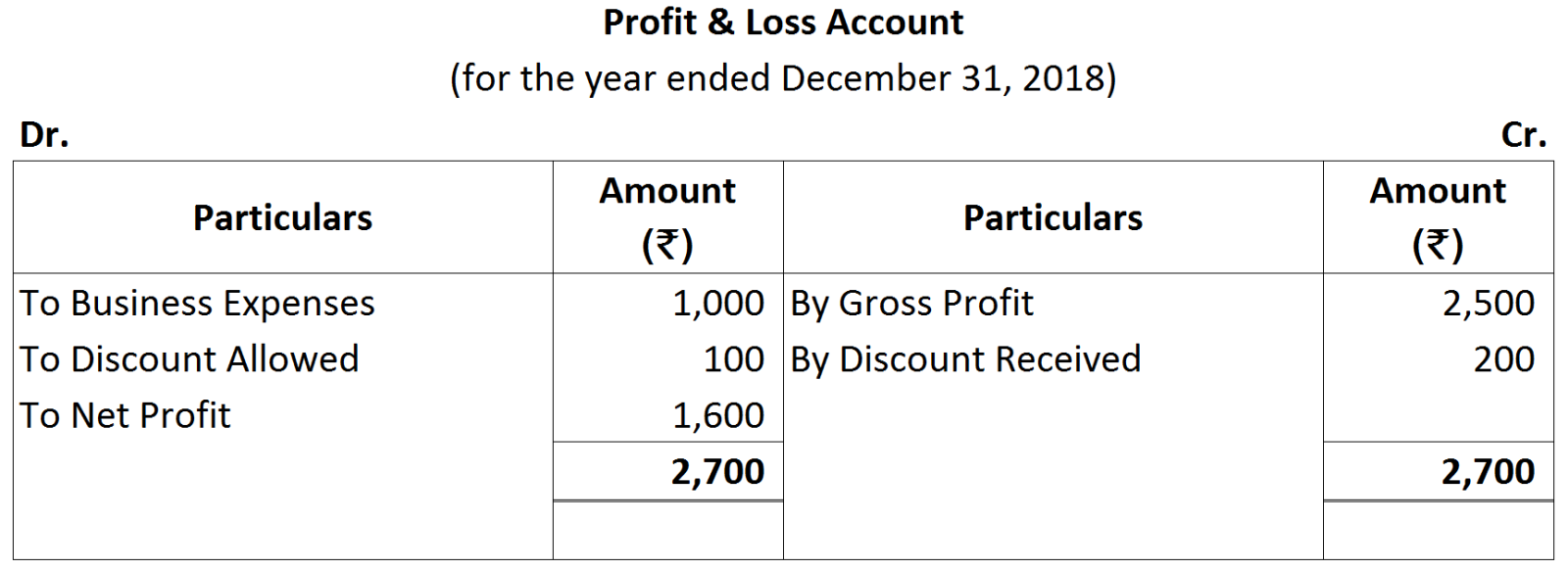

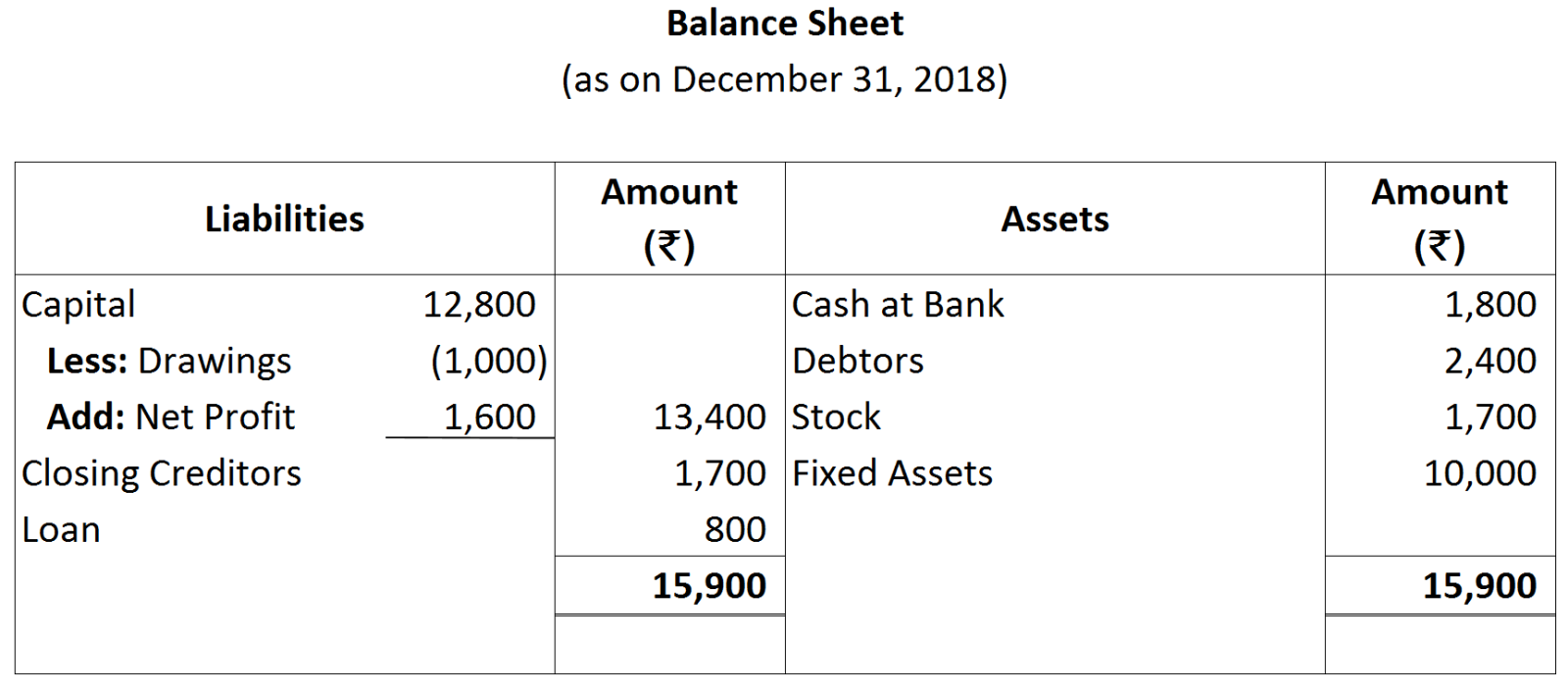

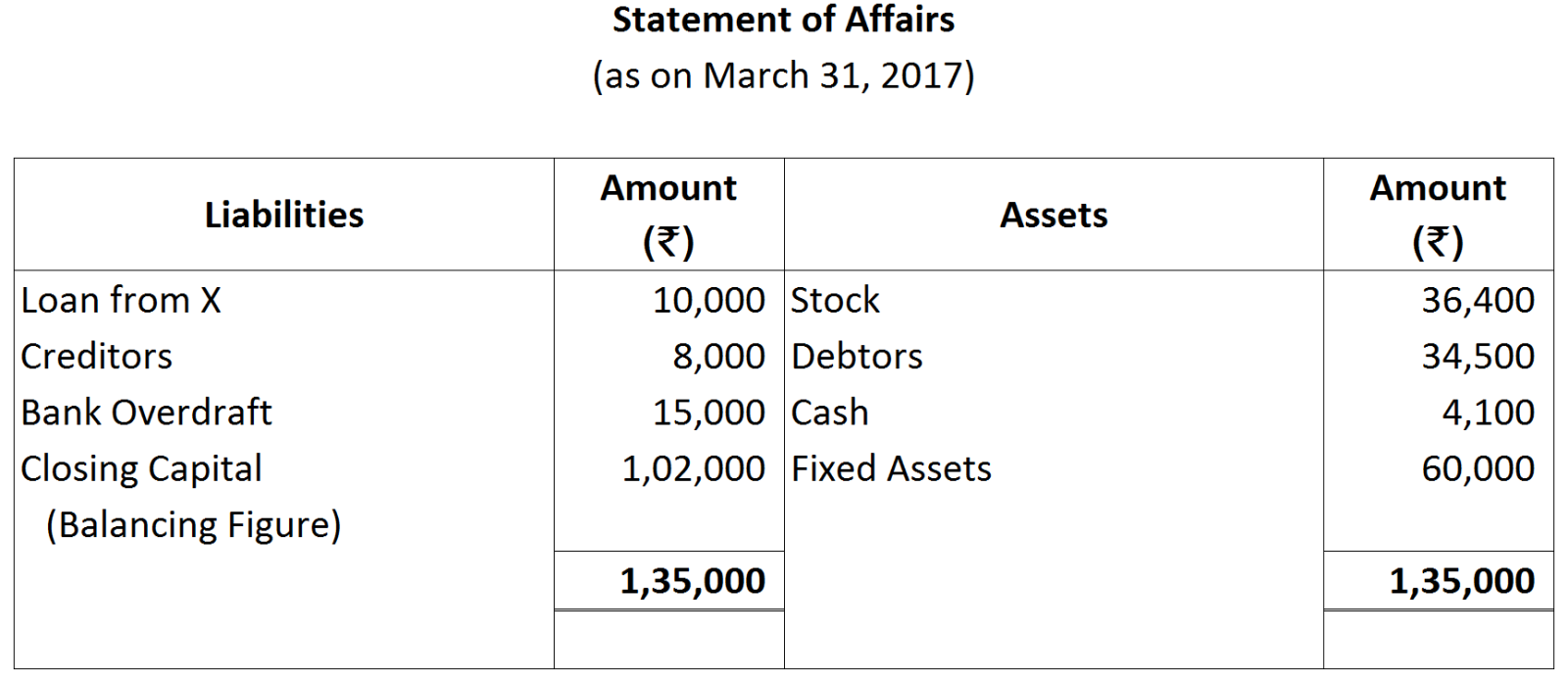

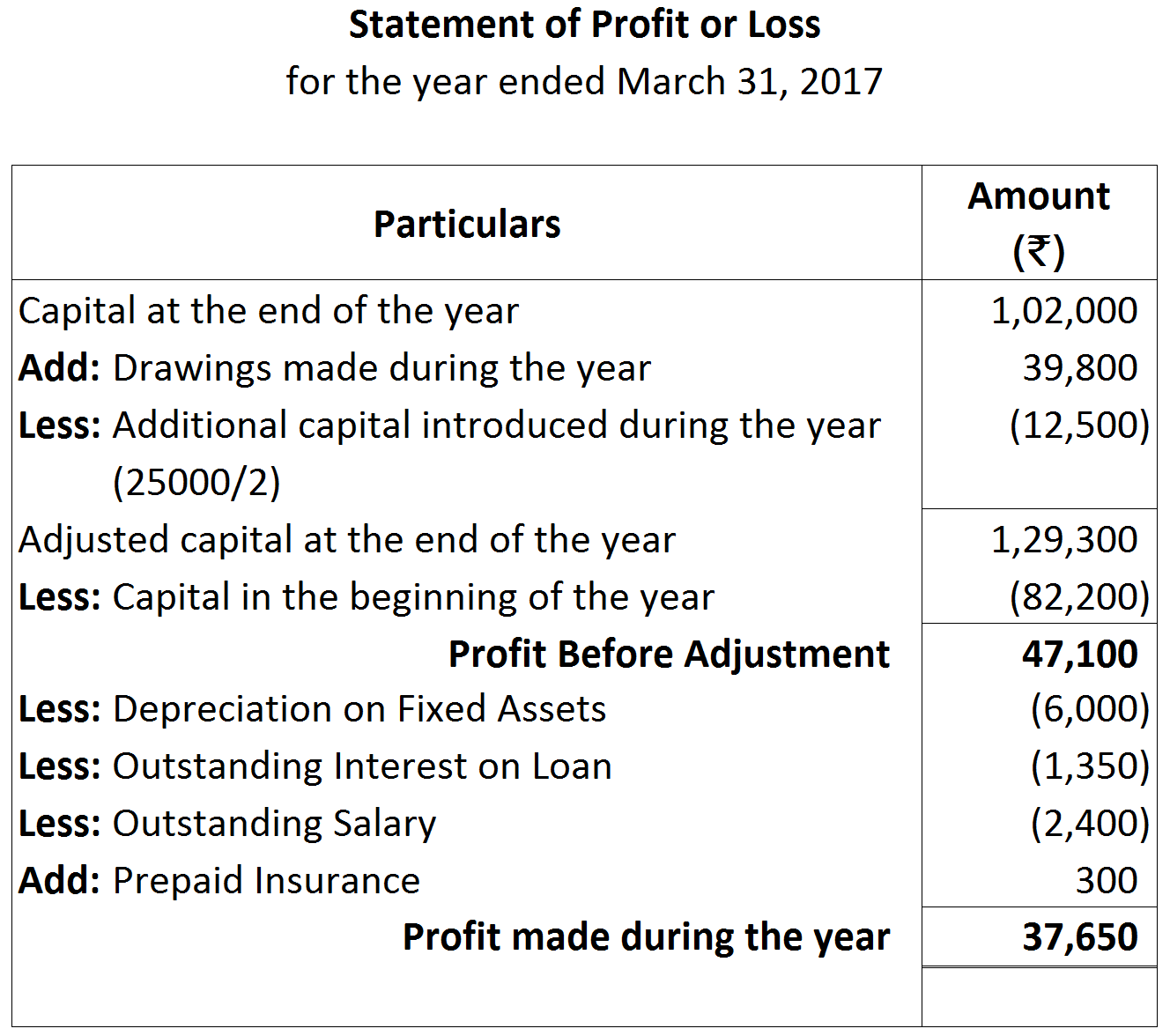

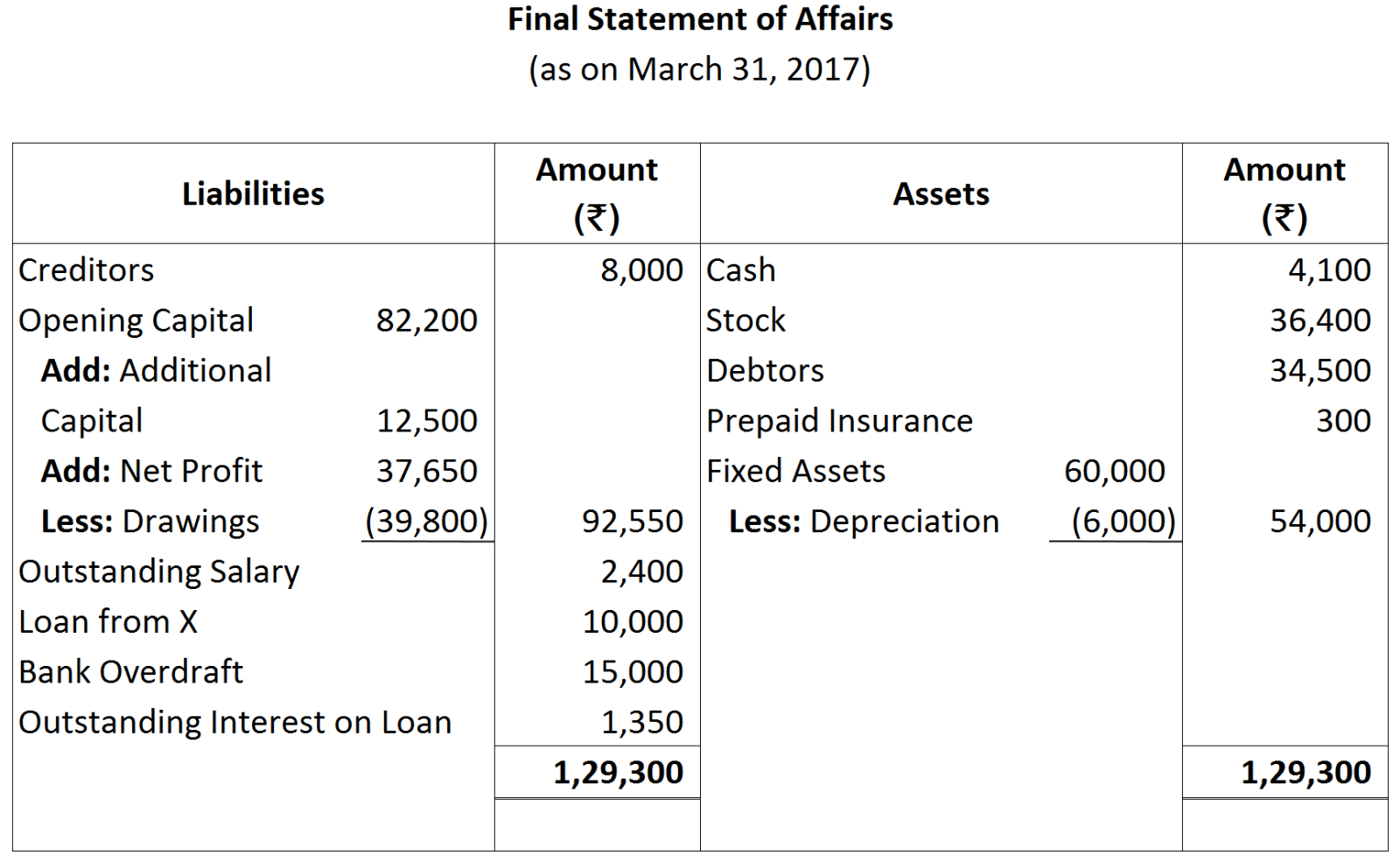

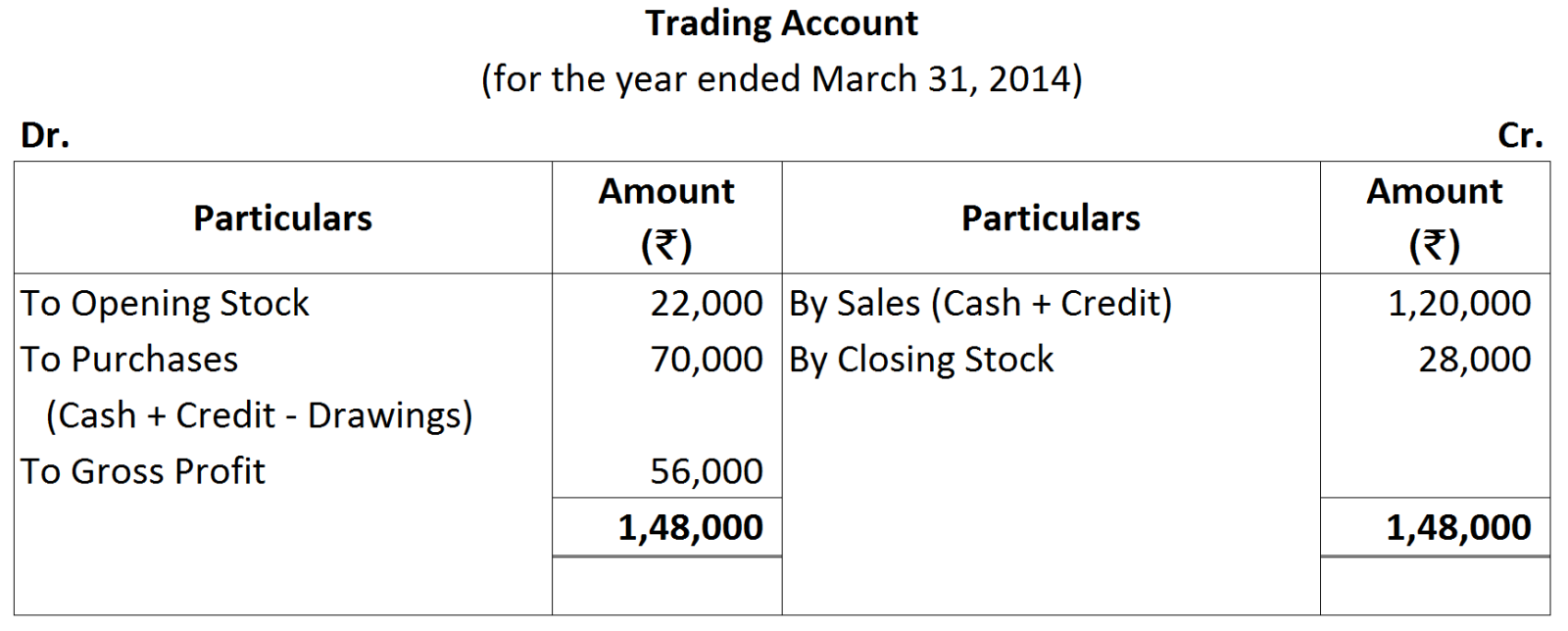

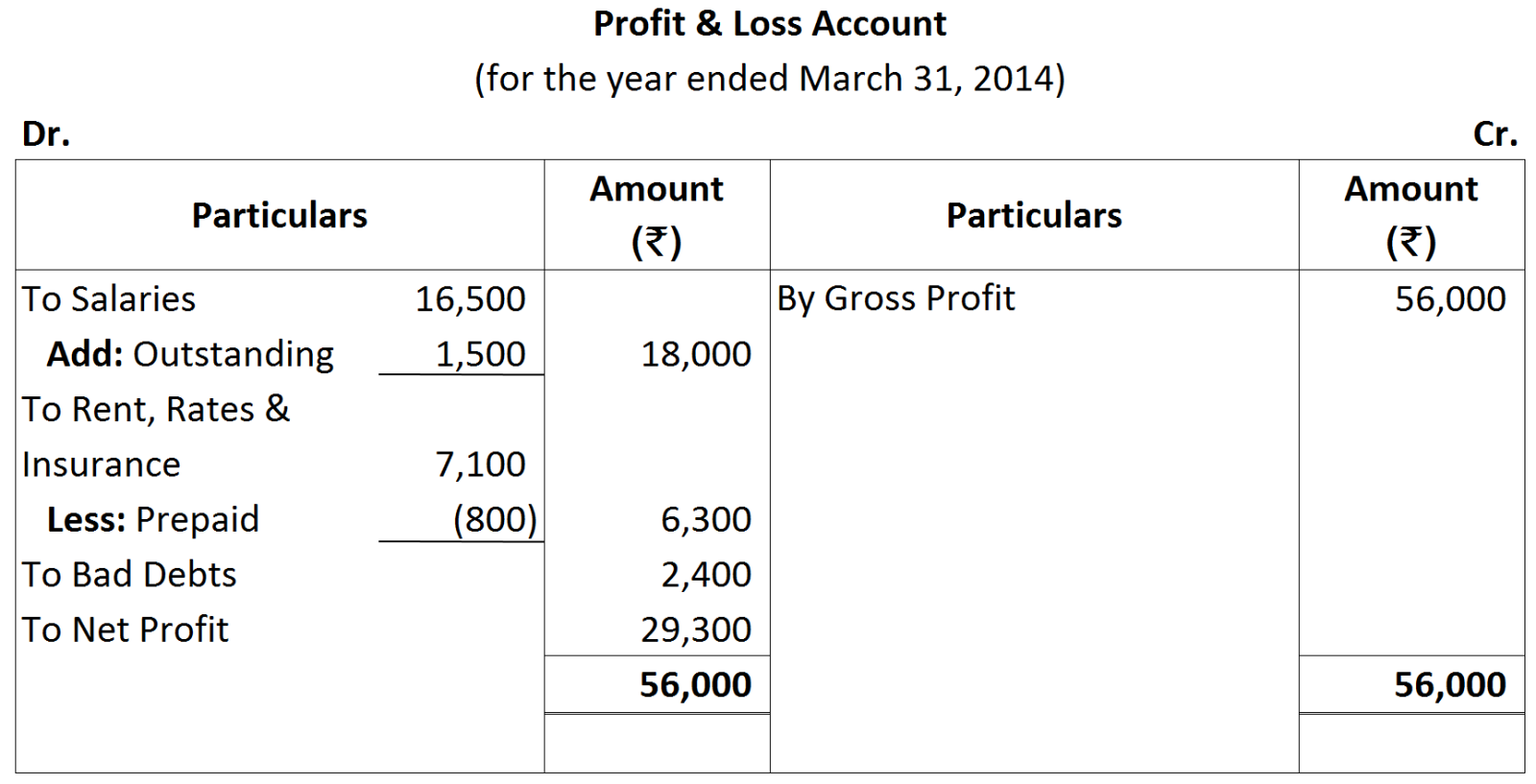

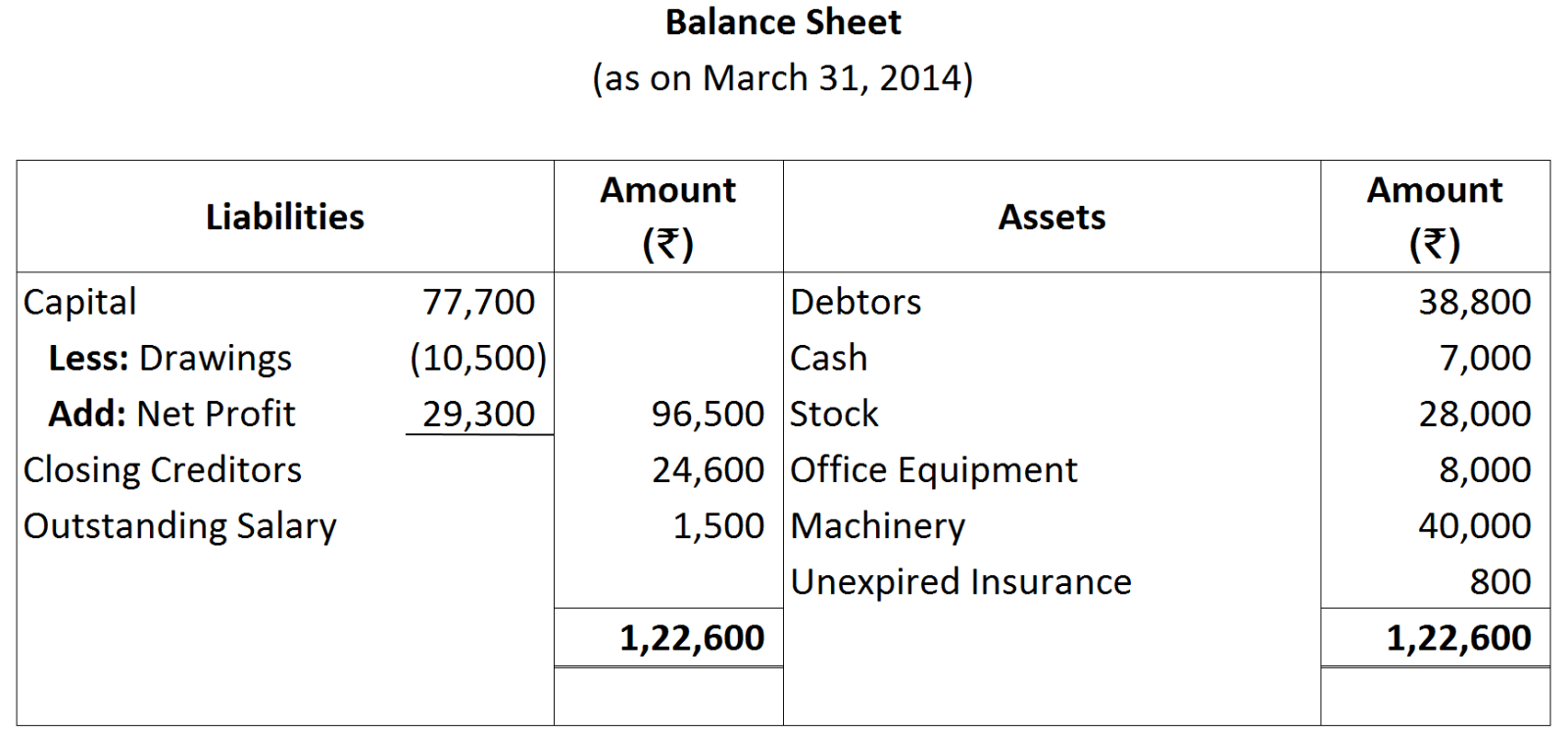

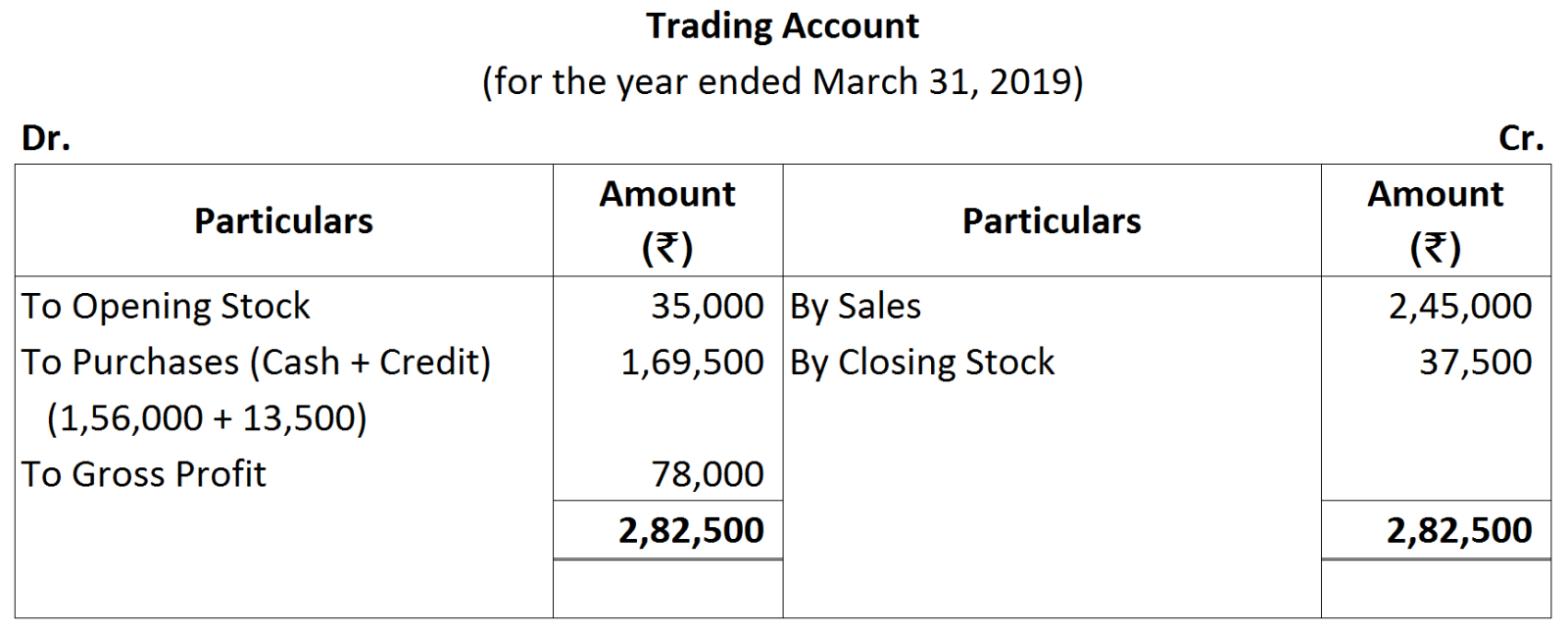

- The last step is to prepare final accounts. On the basis of the missing figures ascertained in each of the above steps, along with other mentioned information, Trading and Profit and Loss Account and Balance Sheet can be prepared.

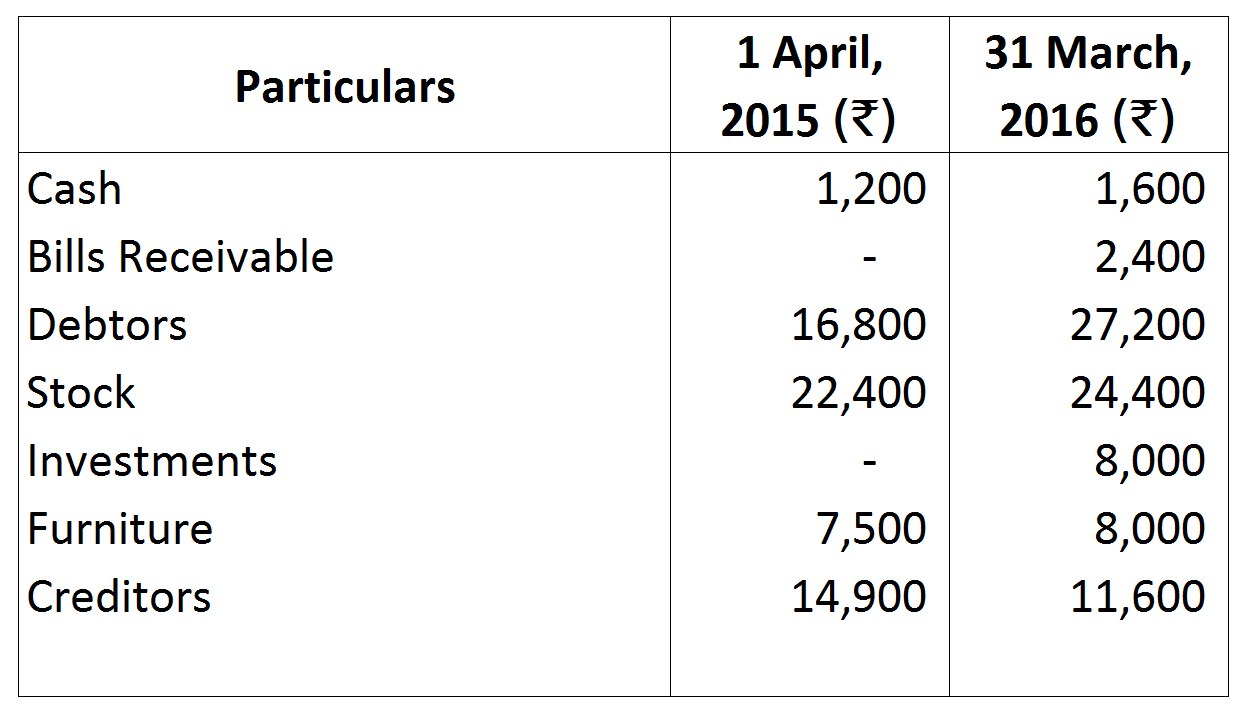

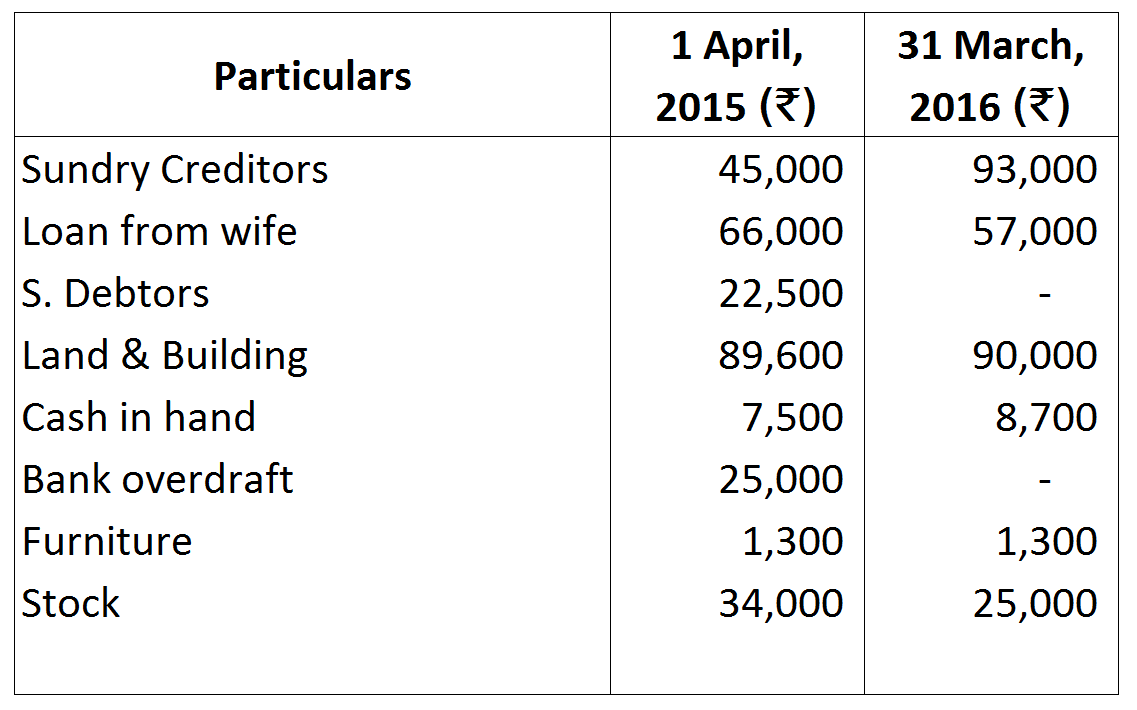

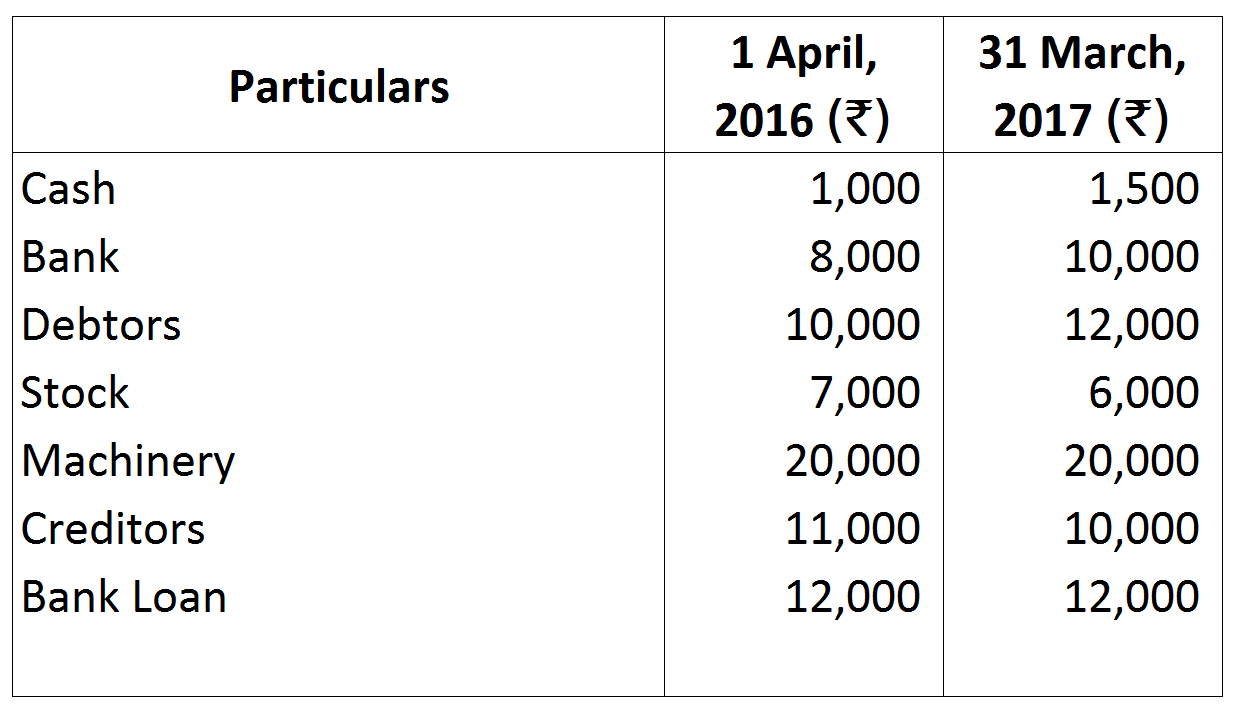

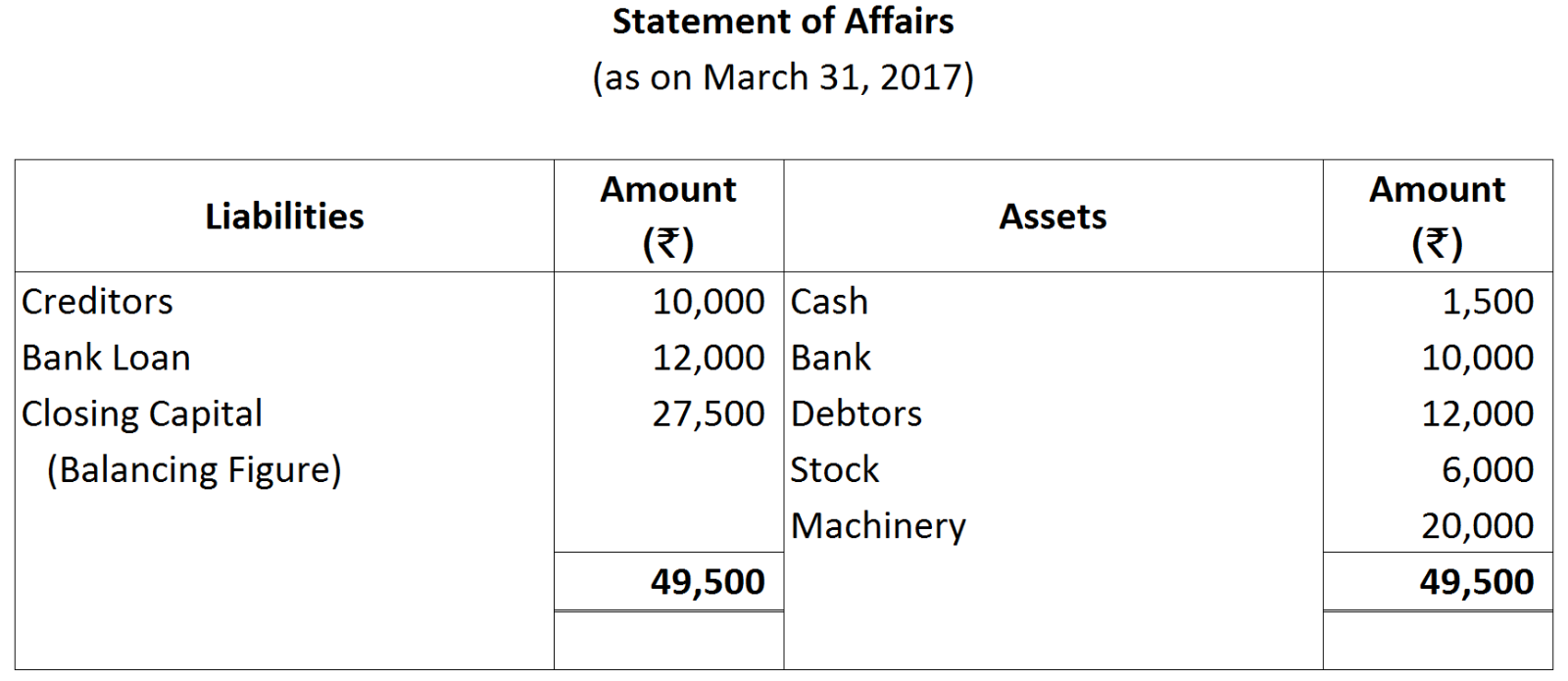

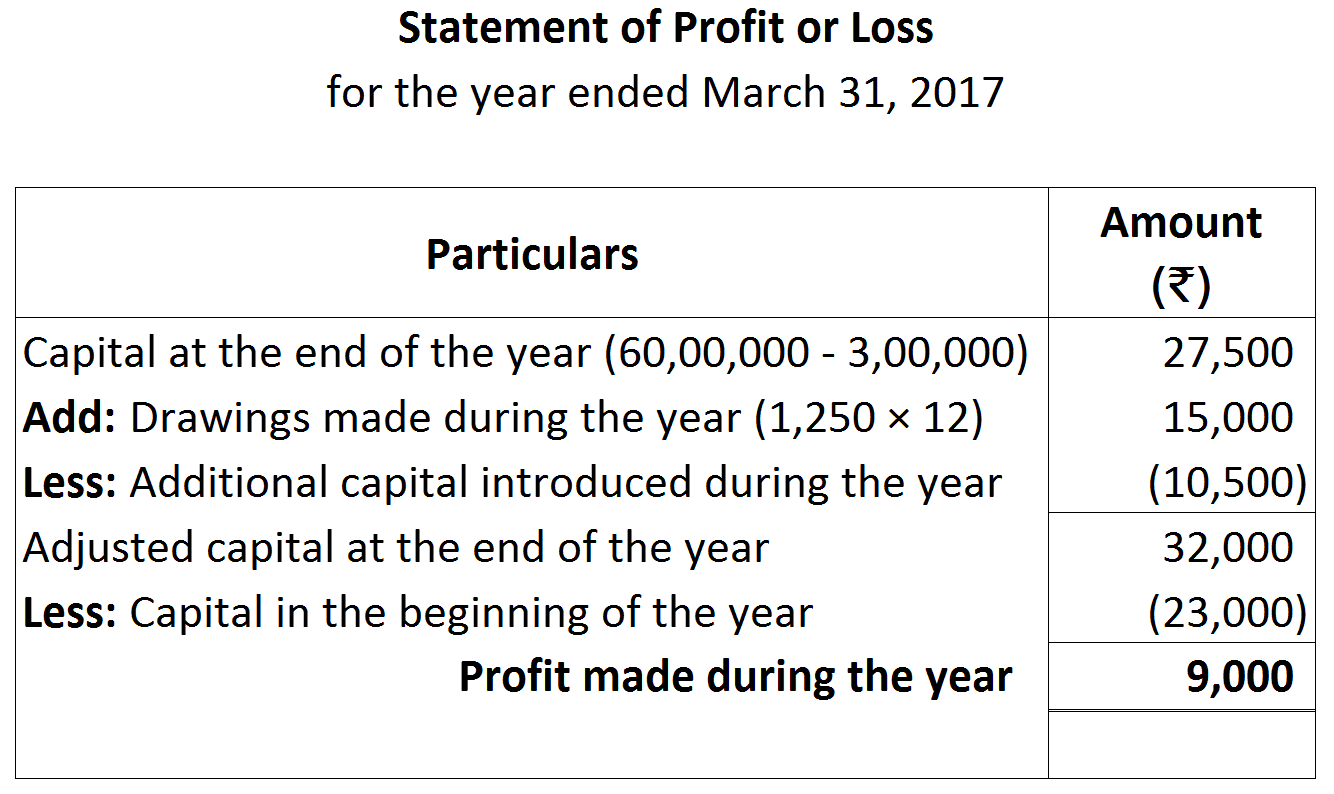

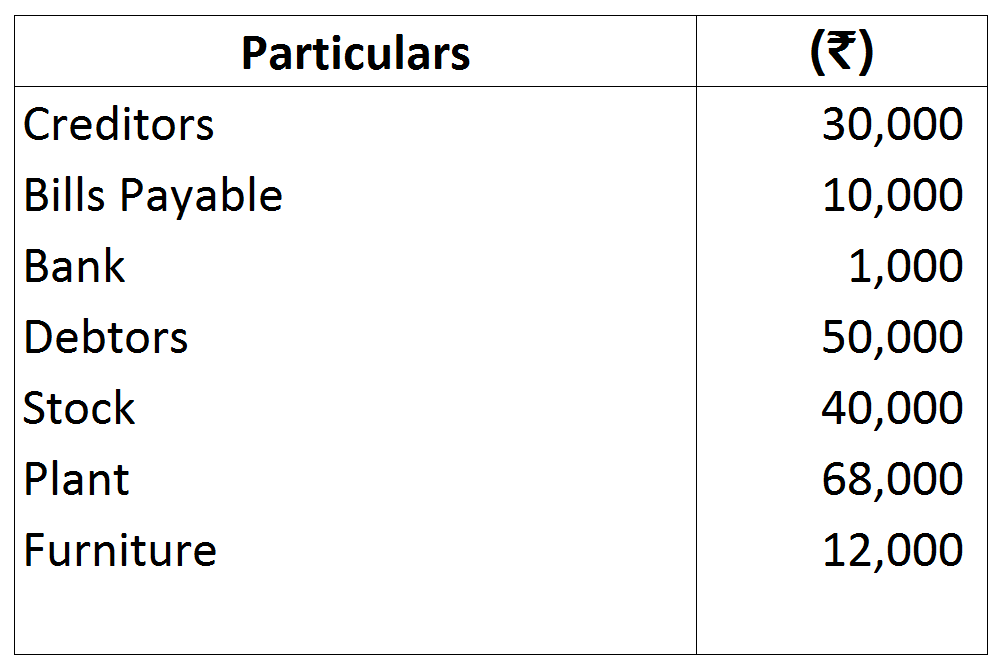

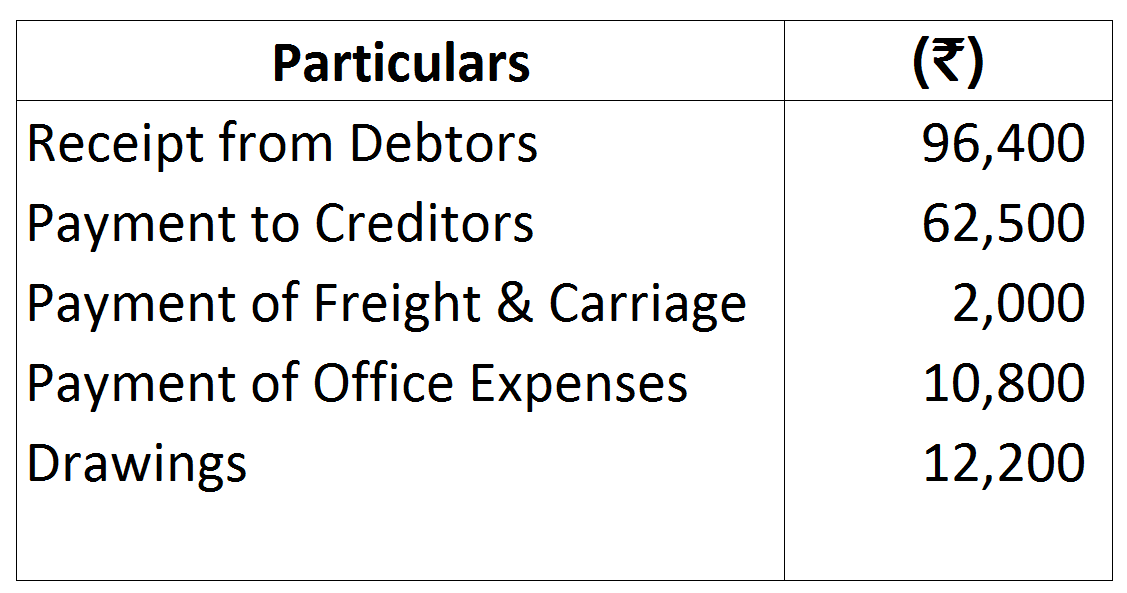

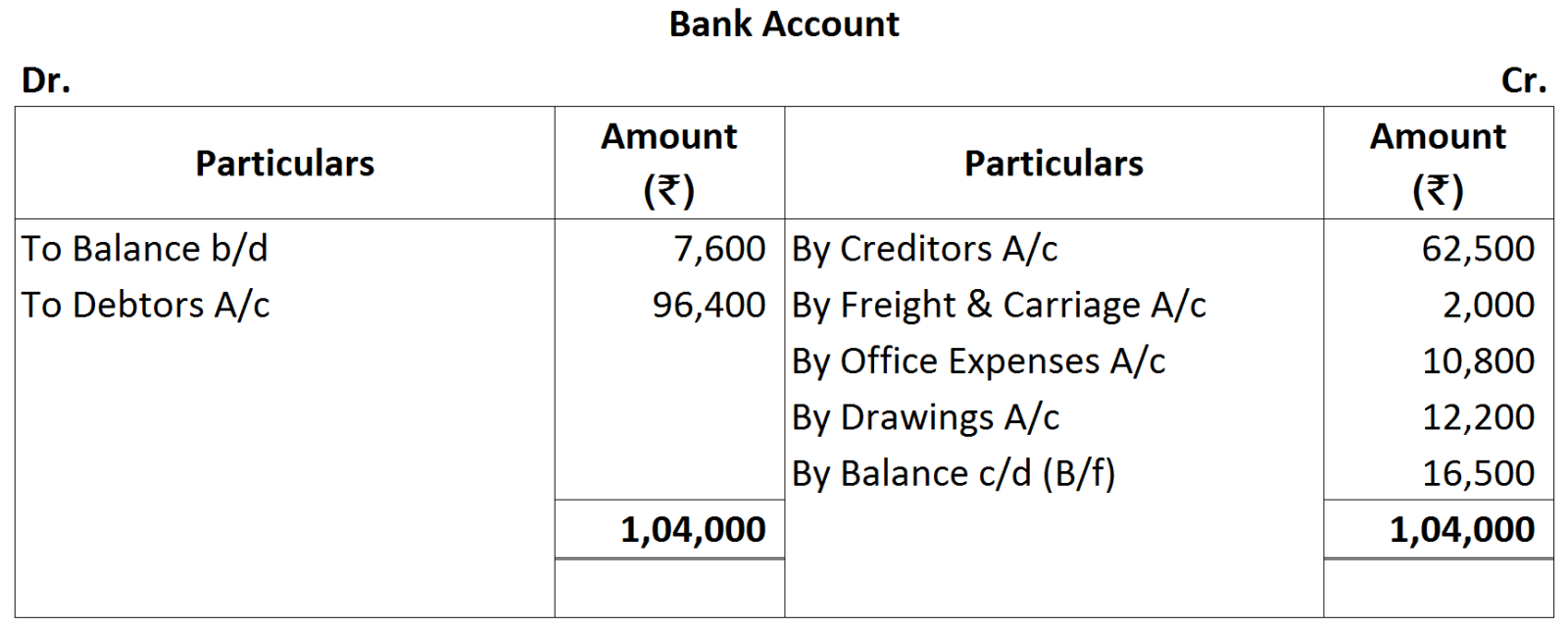

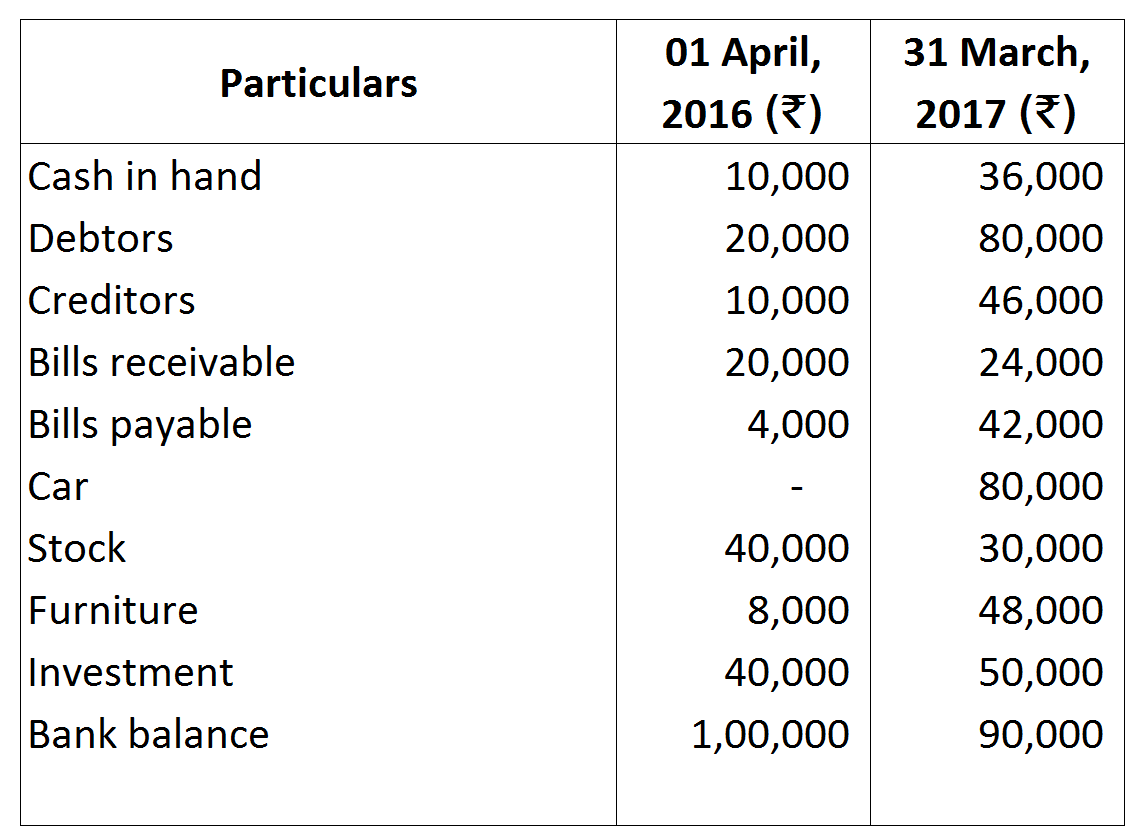

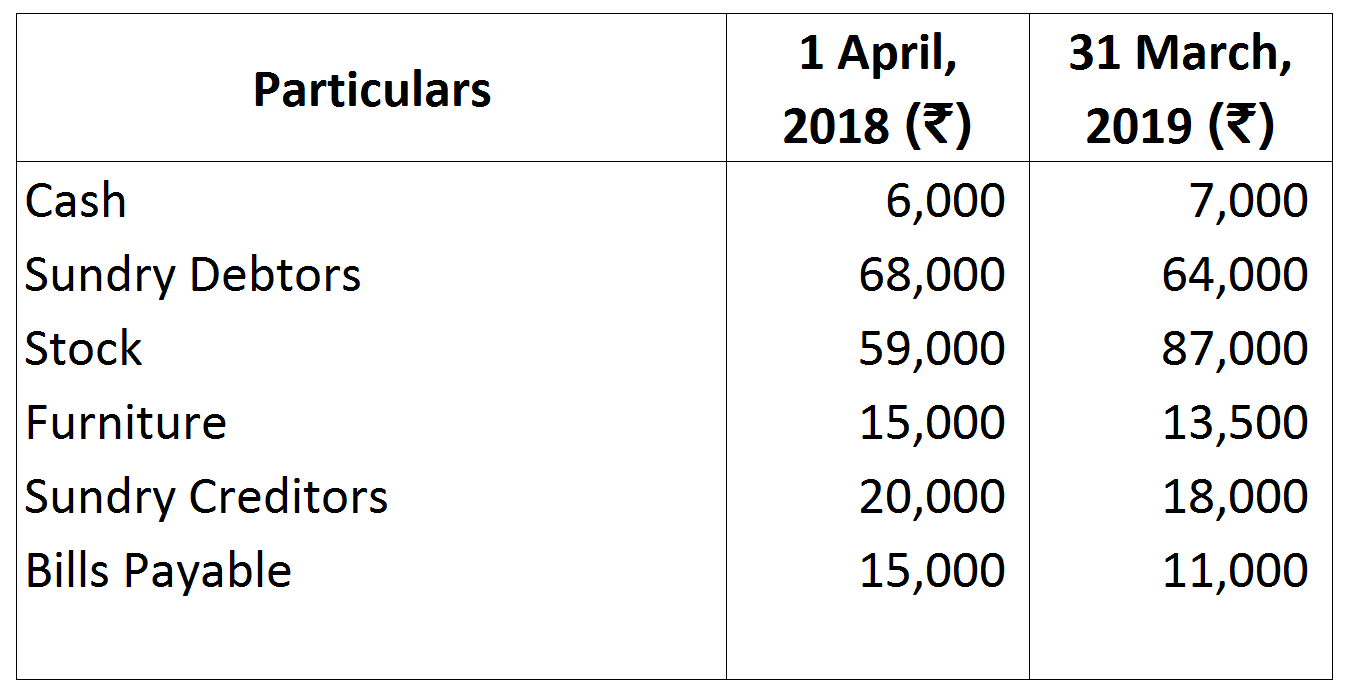

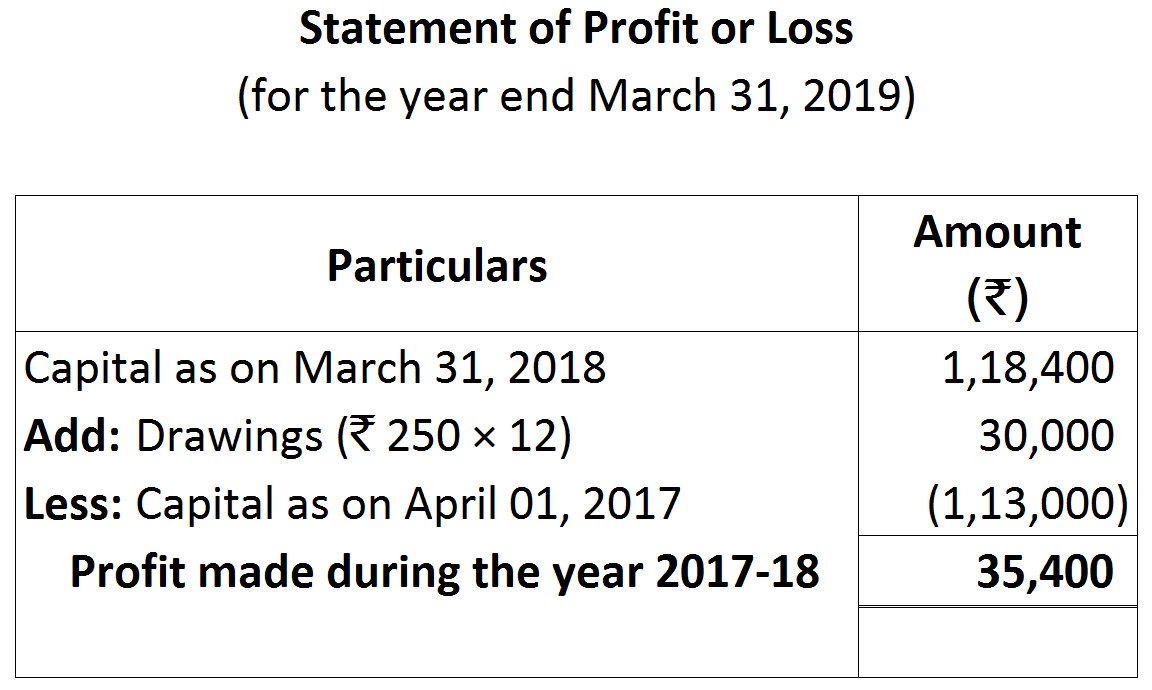

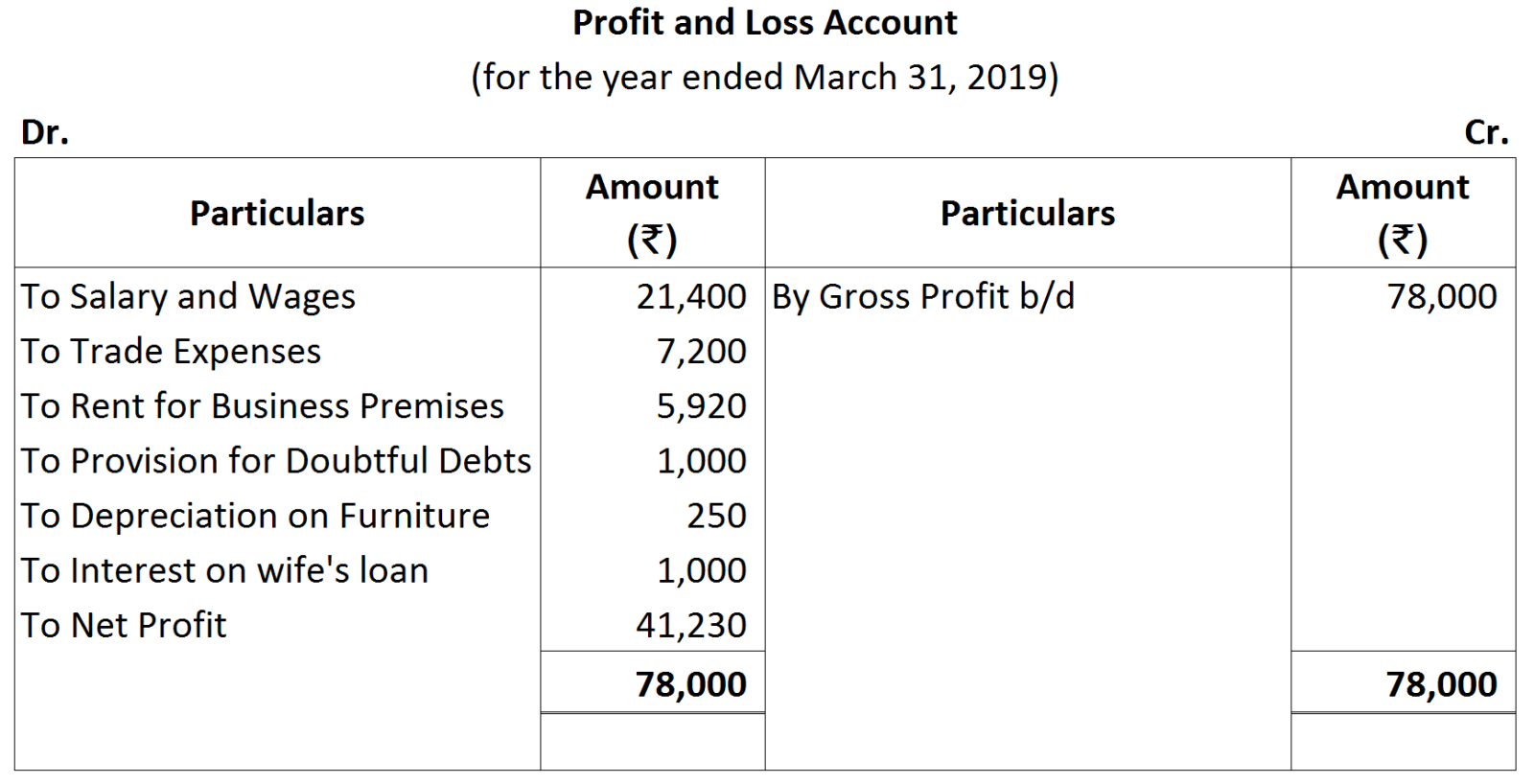

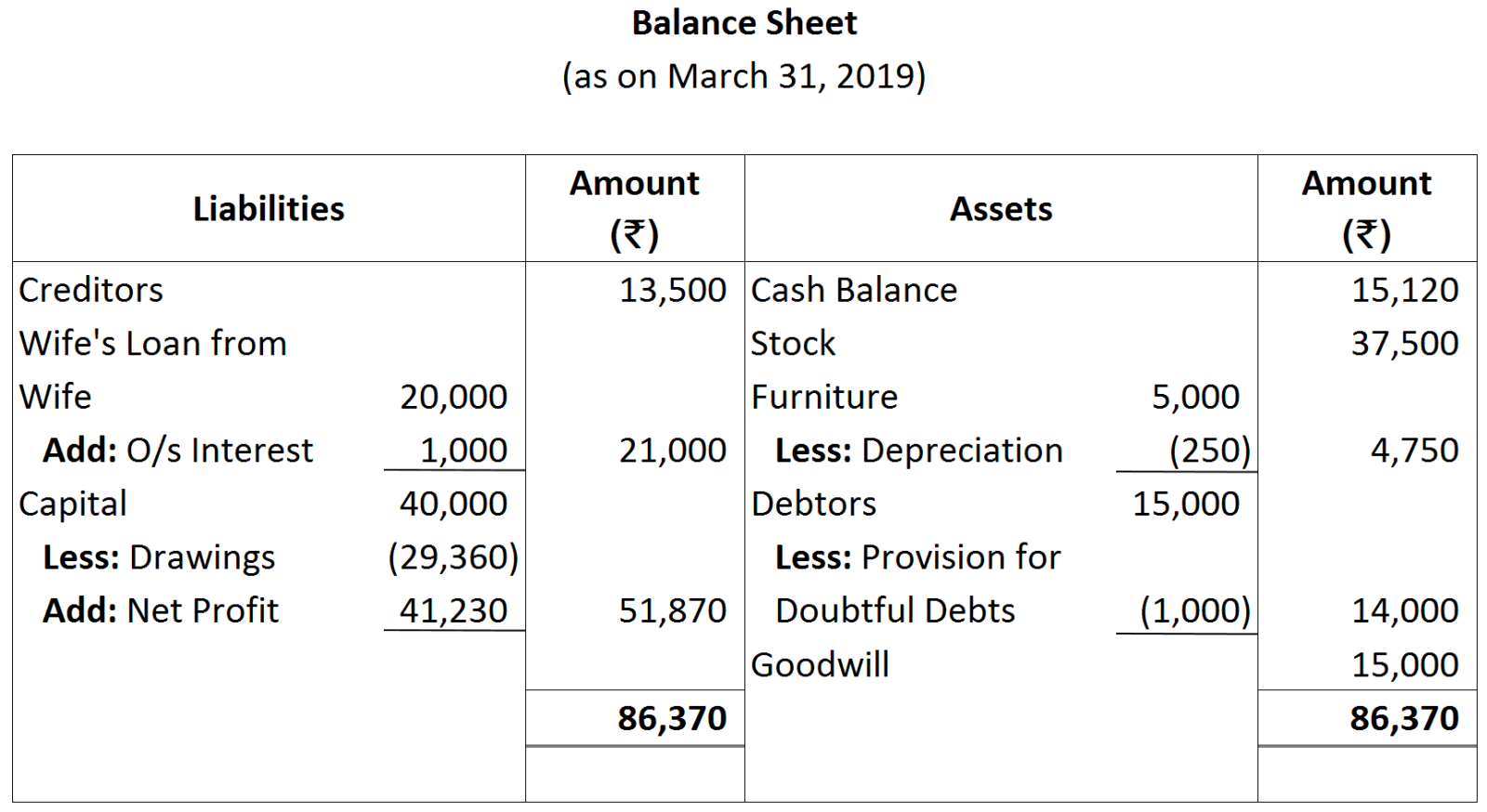

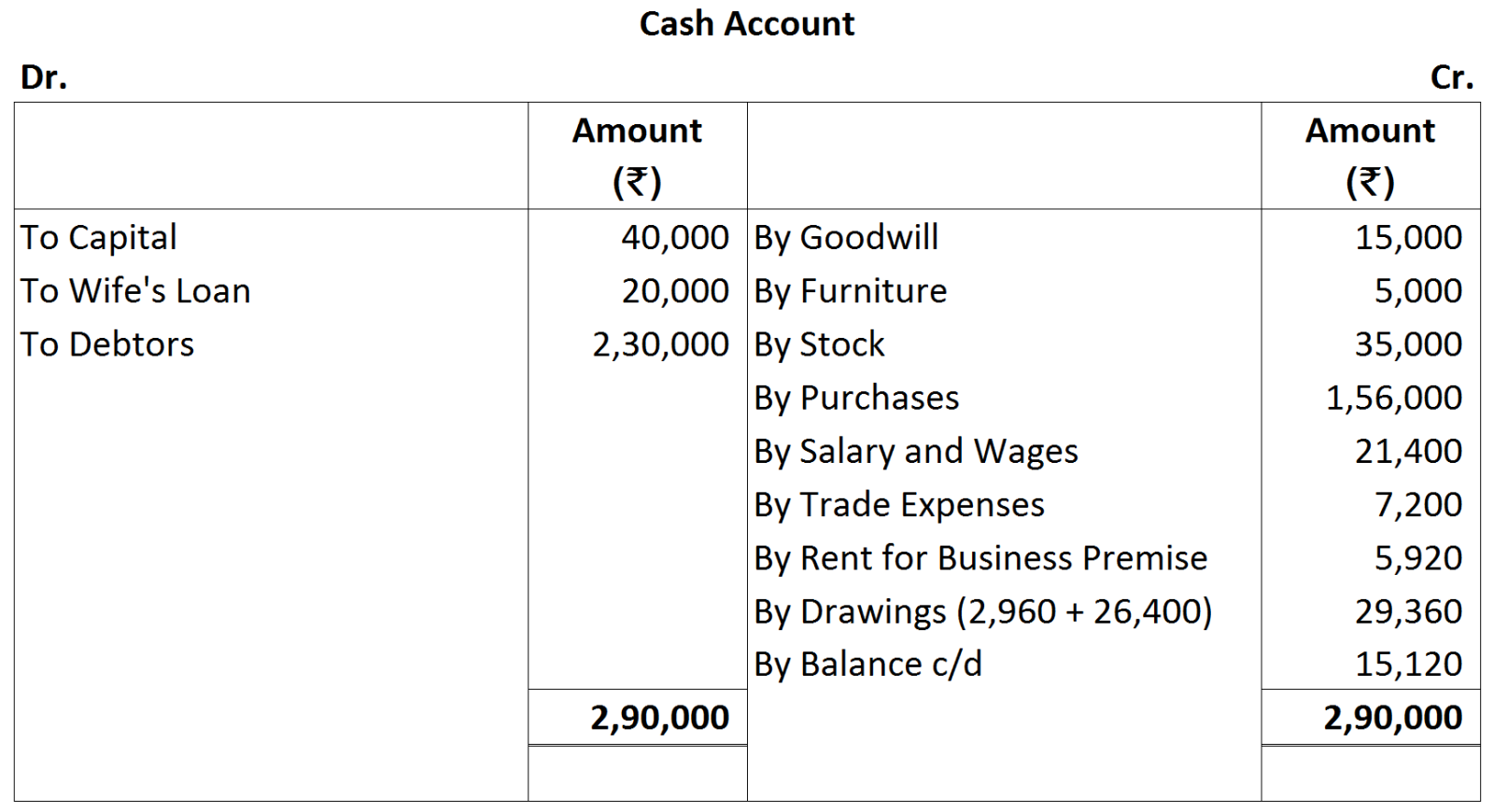

Working Notes:

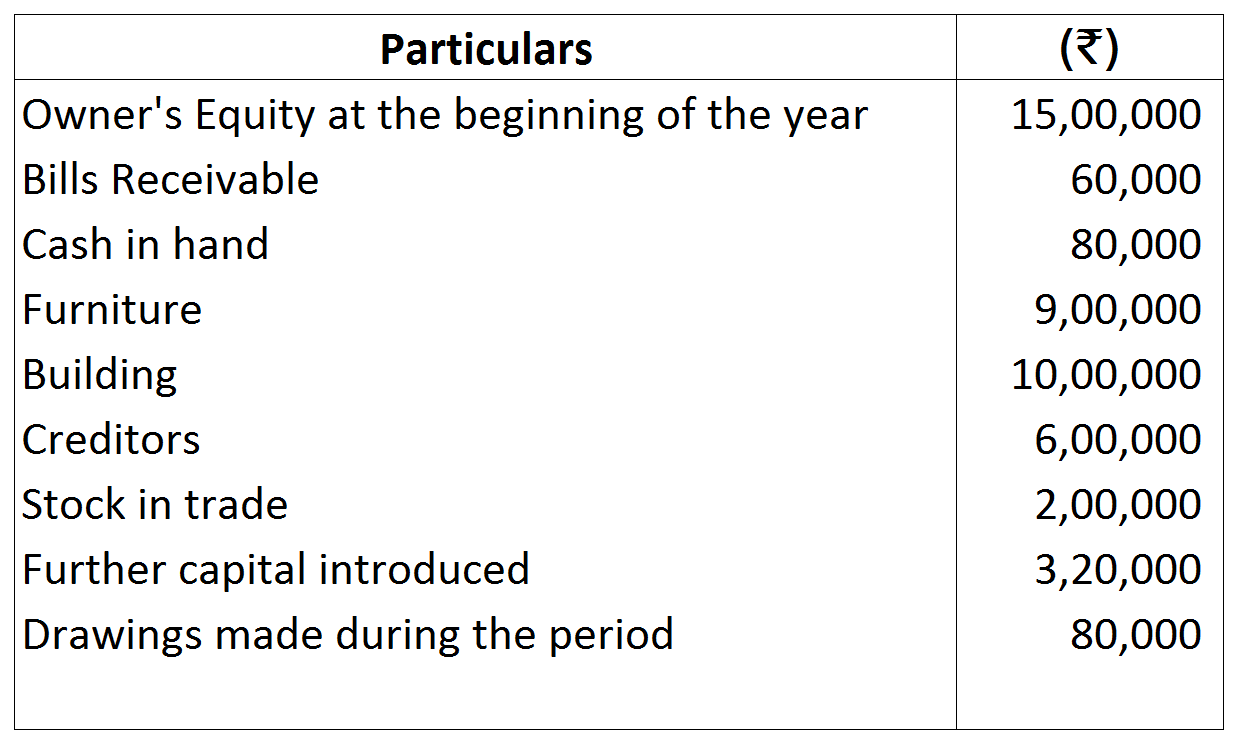

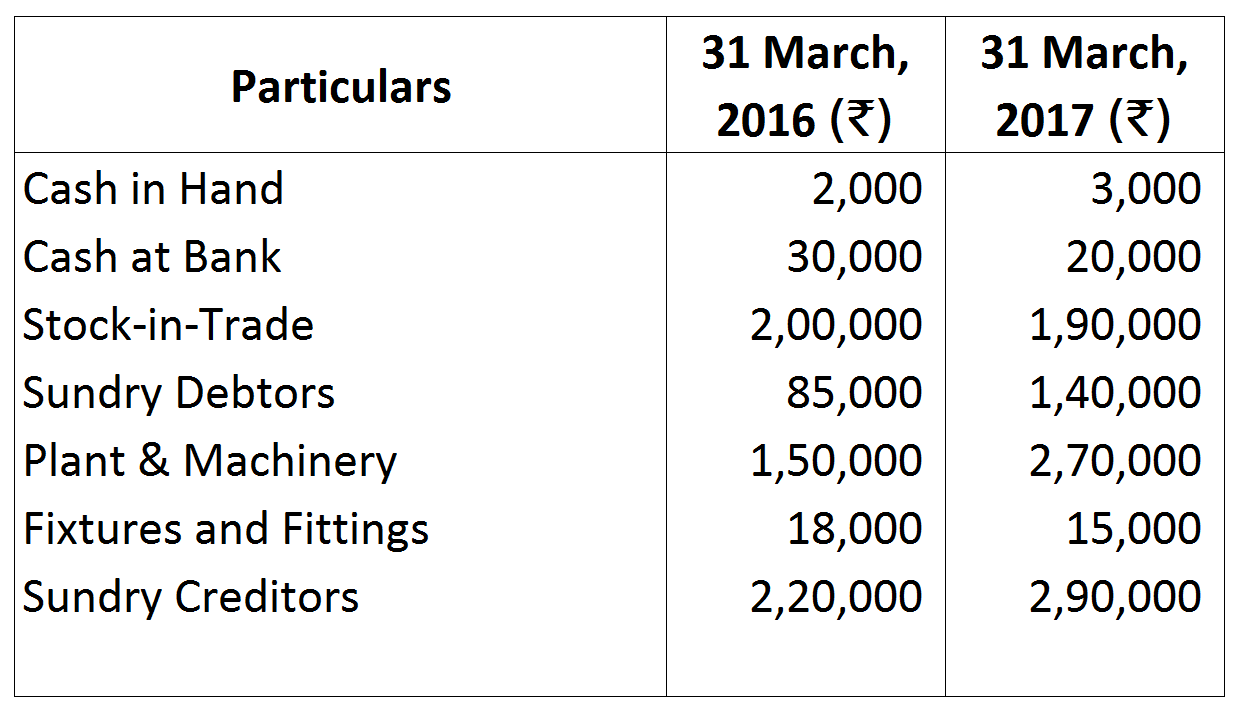

Working Notes:

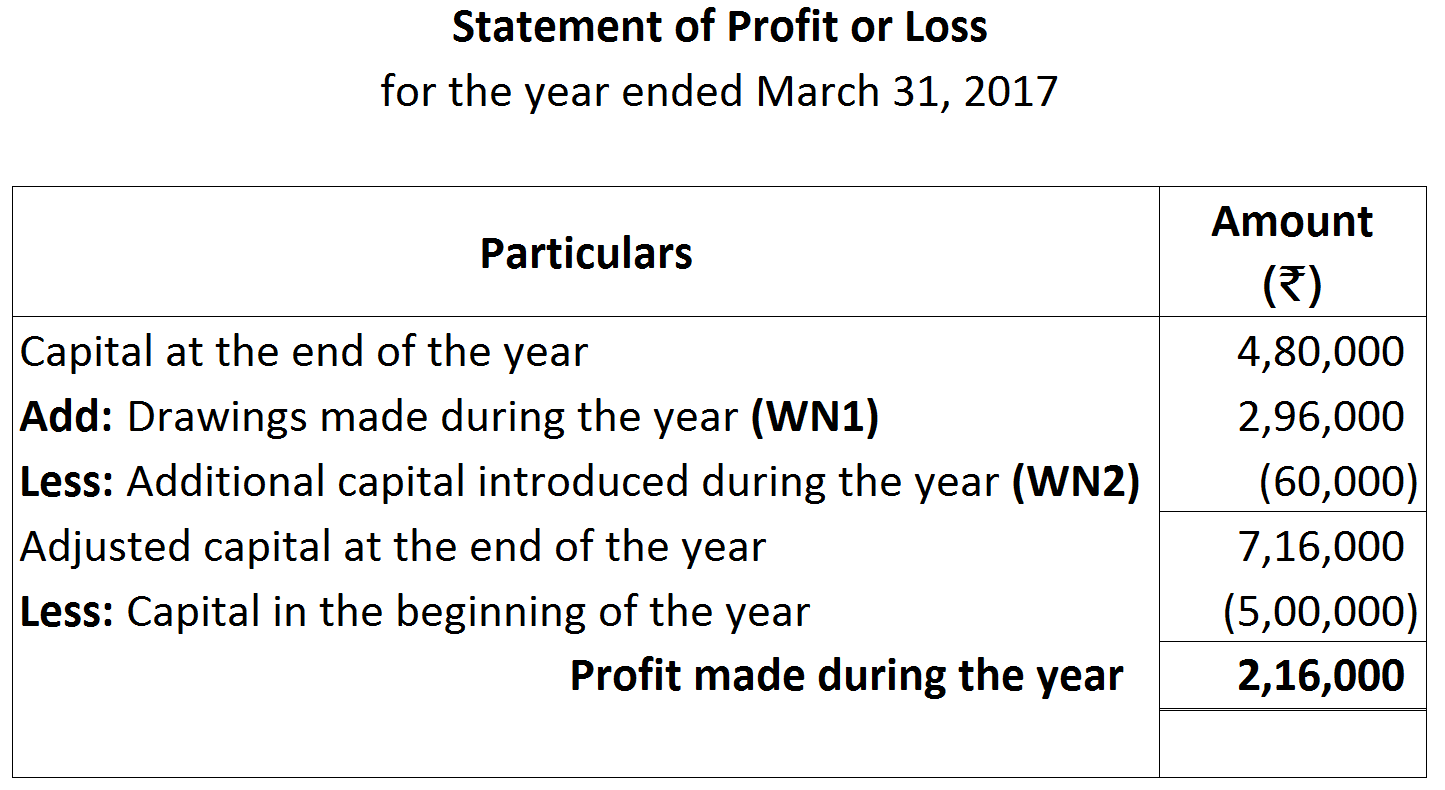

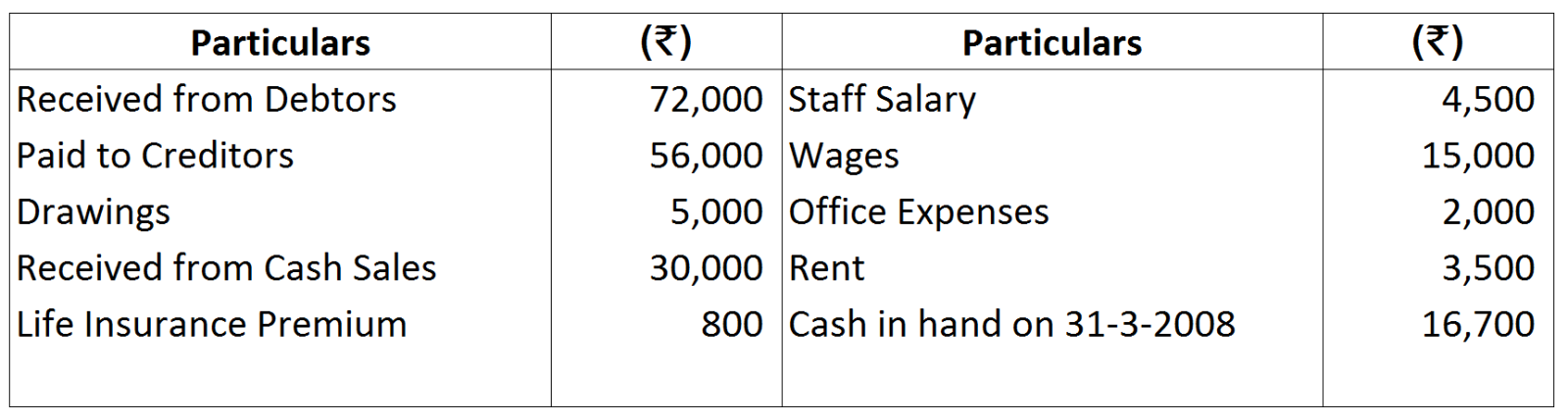

Working Notes:

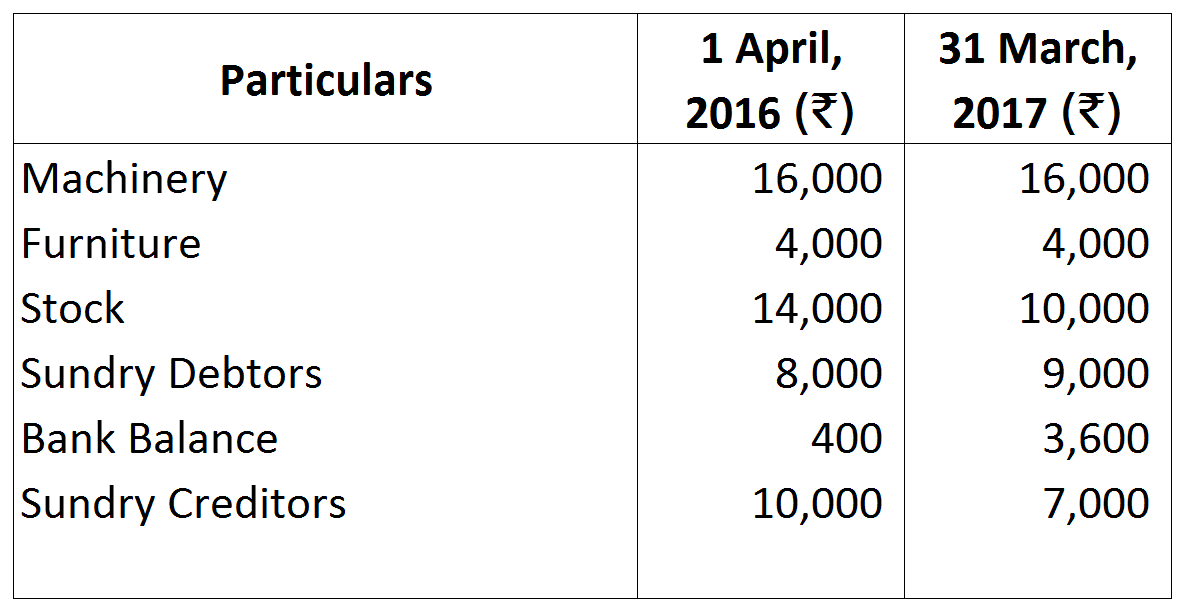

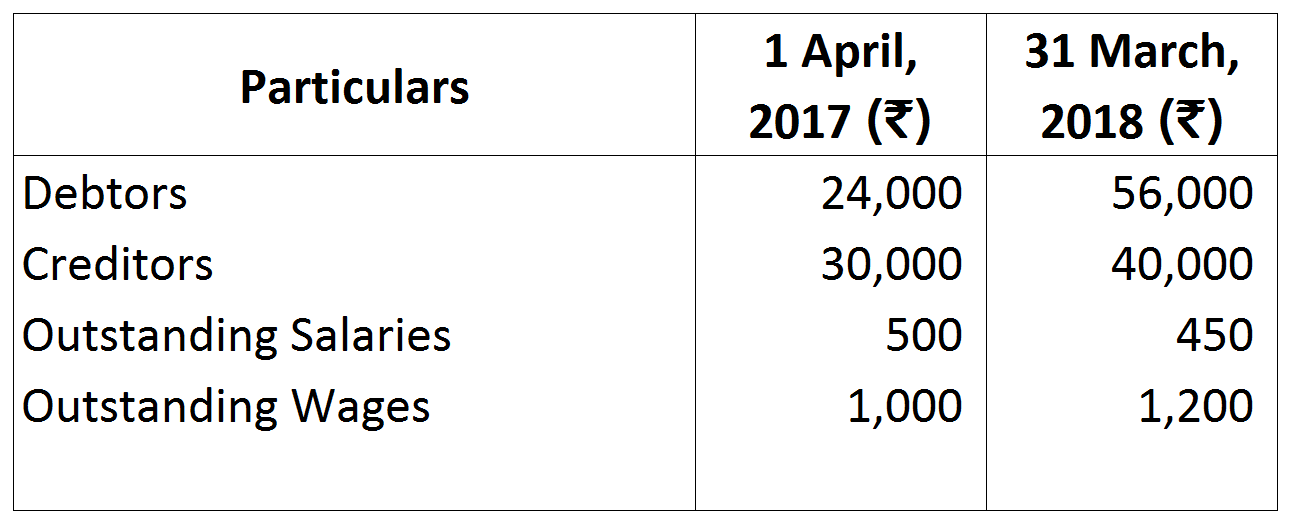

Working Notes:

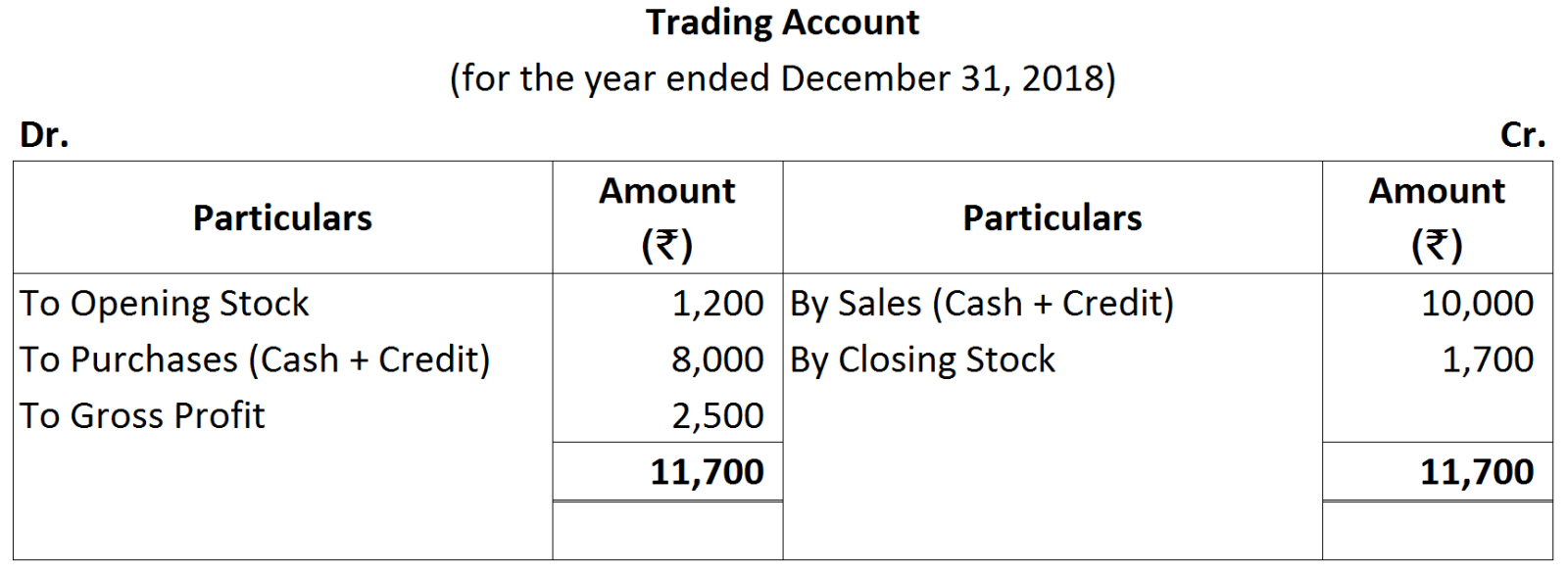

Rate of Gross Profit (on sales) = 20%

Rate of Gross Profit (on sales) = 20% Cost of Goods Sold = Opening Stock + Purchases - Closing Stock

Cost of Goods Sold = Opening Stock + Purchases - Closing Stock

.

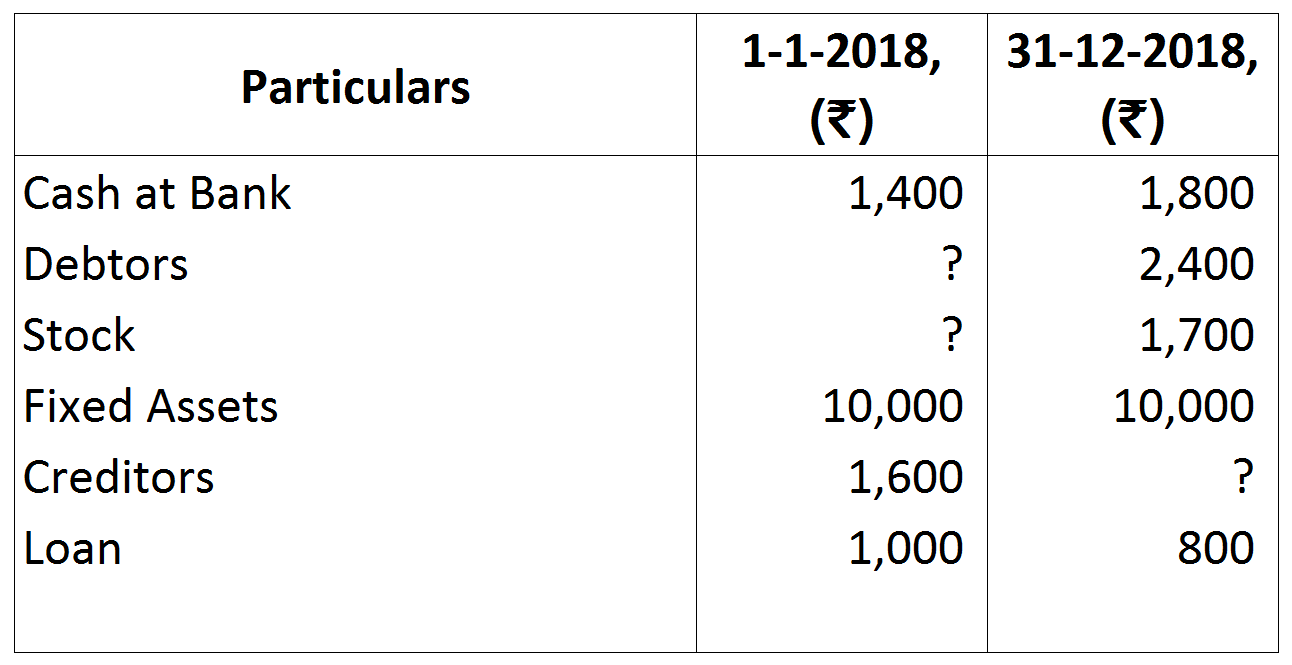

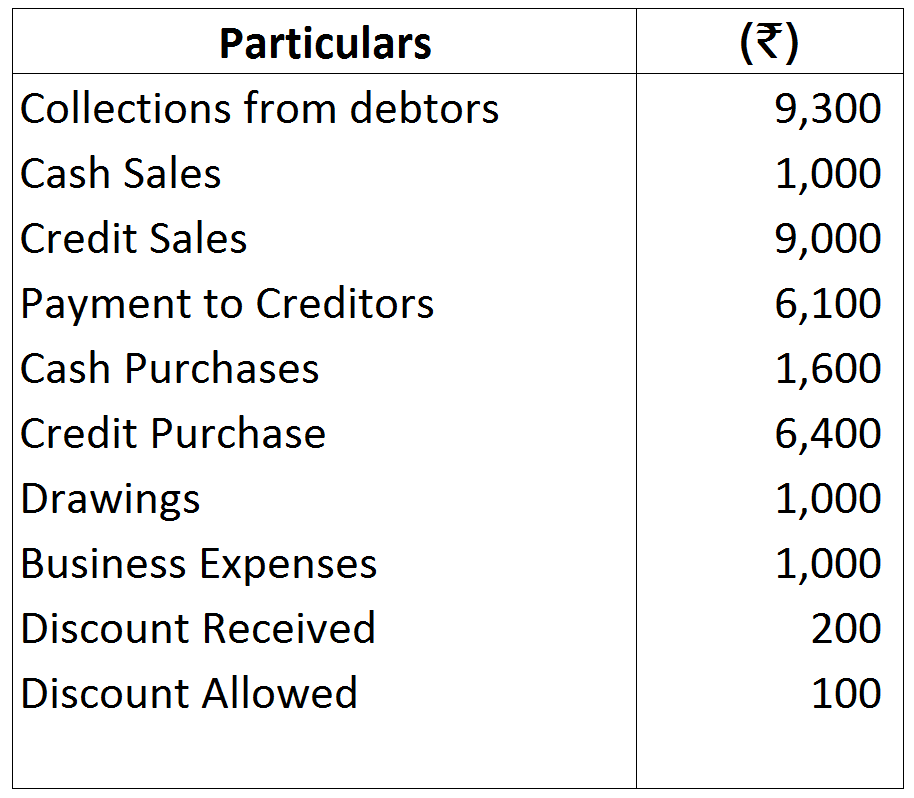

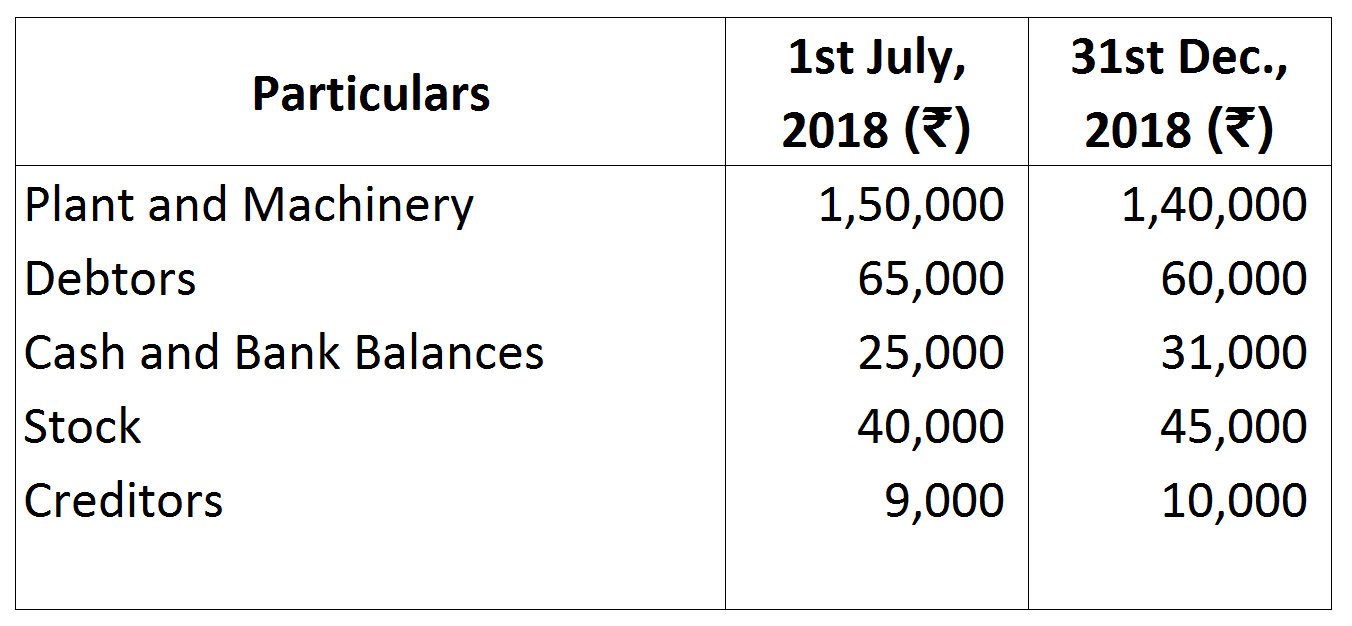

. Transactions during the year 2018:

Transactions during the year 2018:

Note: As per the solution, the loss incurred during the year 2011 is ₹ 60,900; while the answer given in the book shows ₹ 57,900.

Note: As per the solution, the loss incurred during the year 2011 is ₹ 60,900; while the answer given in the book shows ₹ 57,900.

Working Note:

Working Note:

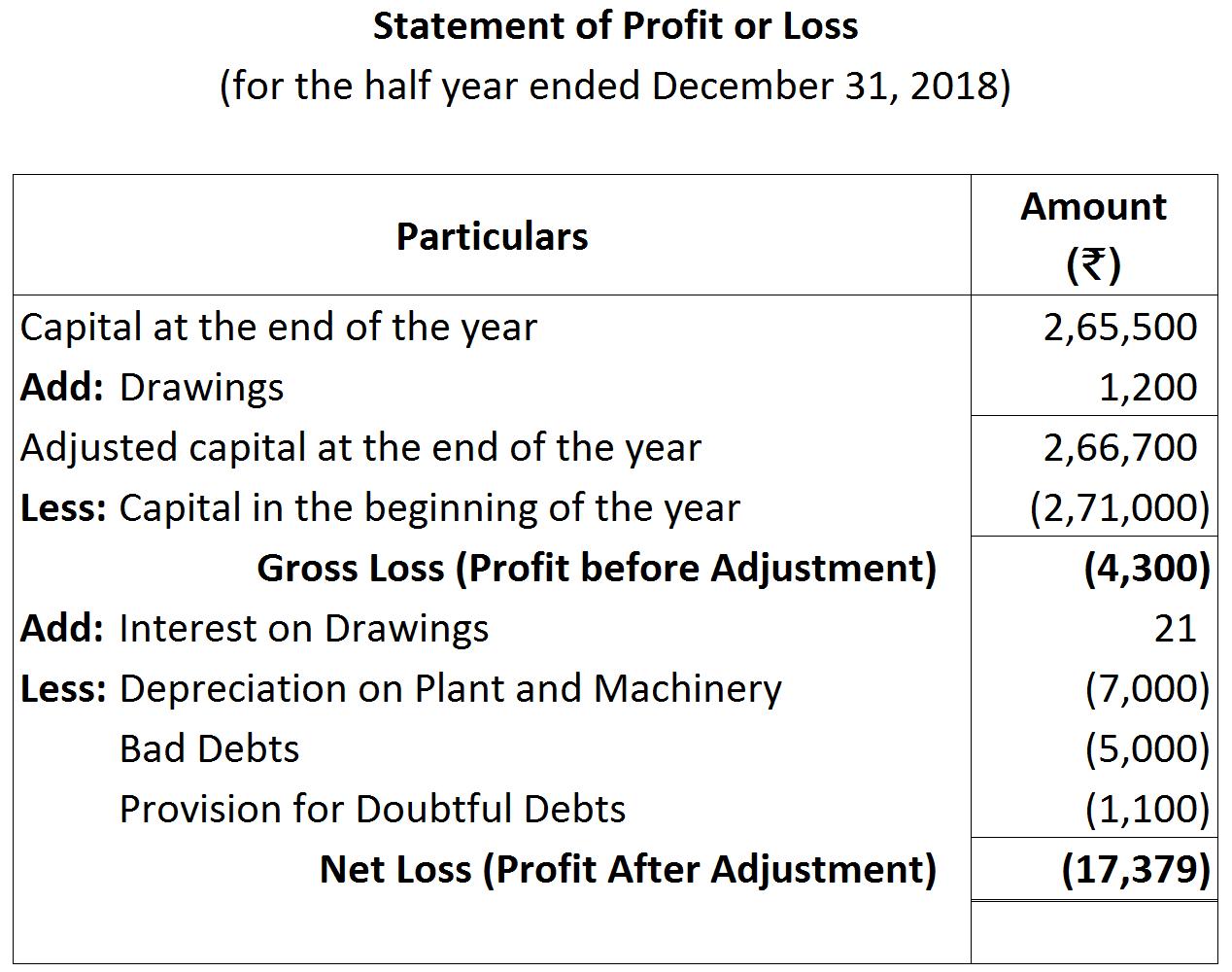

Working Notes:

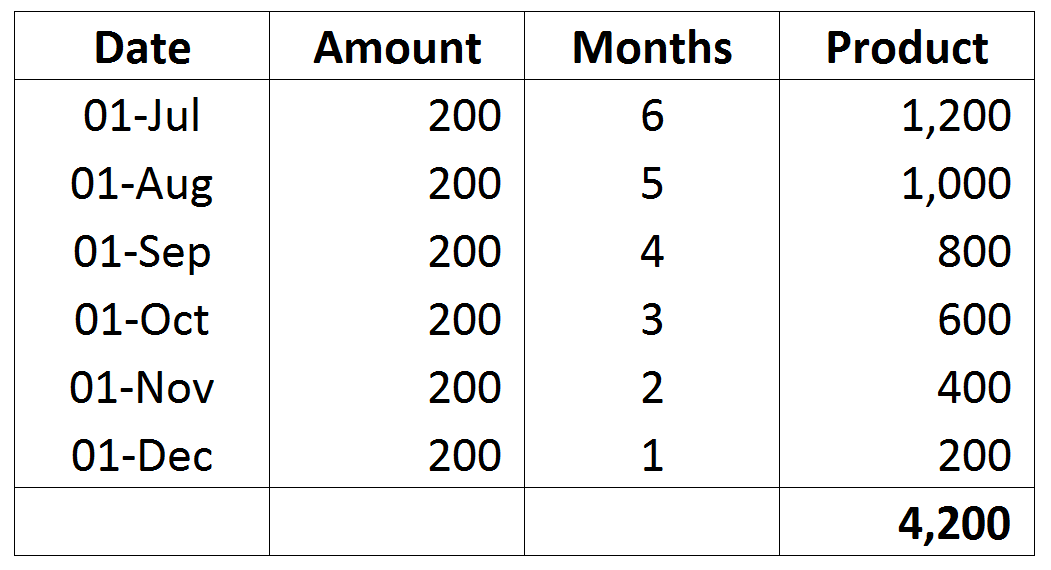

Working Notes: Interest on Drawings $=\frac{4,200\times6\times1}{100\times12}=₹ \ 21$

Interest on Drawings $=\frac{4,200\times6\times1}{100\times12}=₹ \ 21$

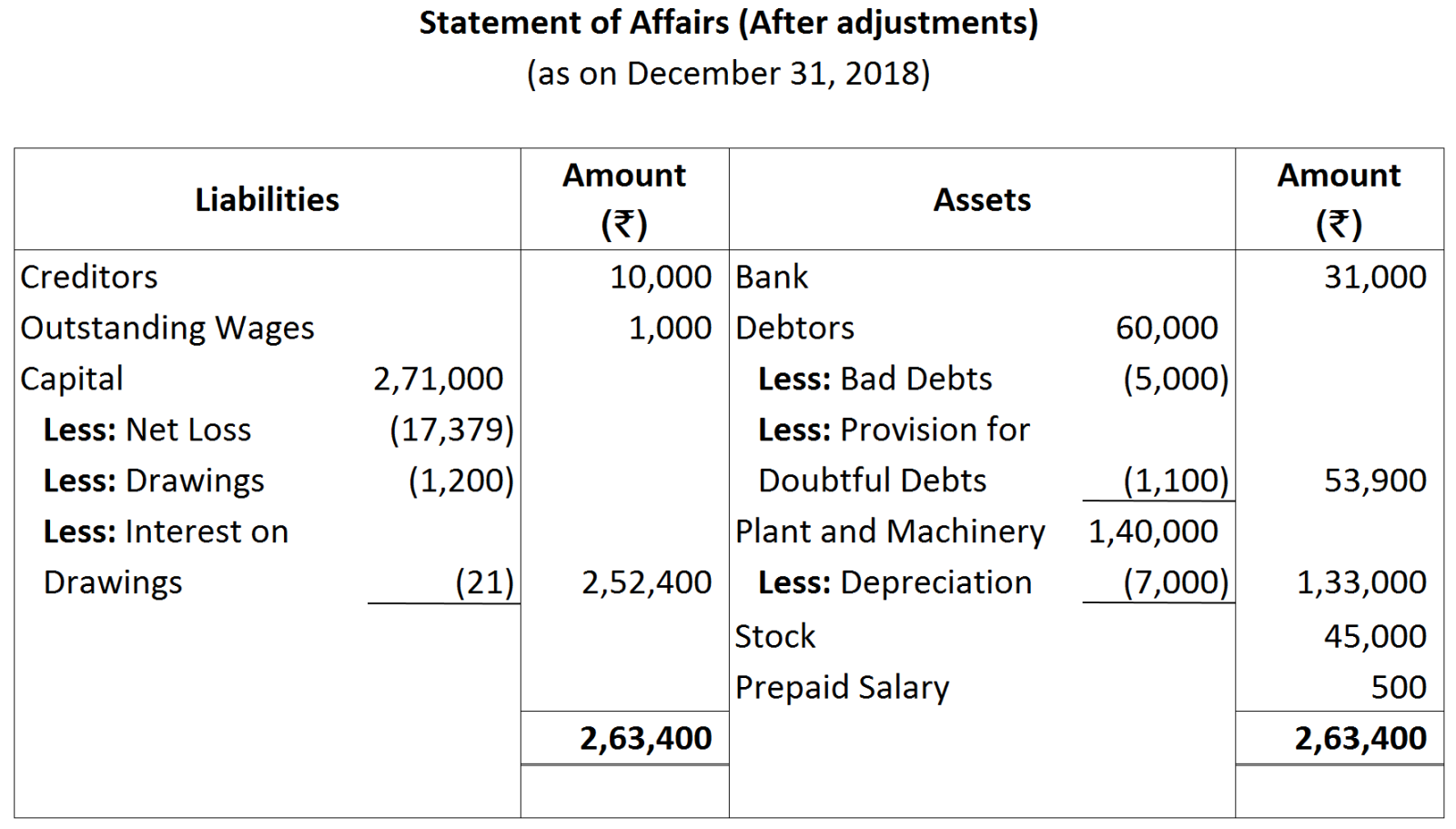

Working Note:

Working Note:

Working Notes:

Working Notes:

Working Notes:

Working Notes: