Question 13 Marks

Why the statement of assets and liabilities prepared under Single Entry System at the end of the accounting period is called a Statement of Affairs instead of Balance Sheet?

Answer

View full question & answer→Although Statement of Affairs, like Balance Sheet, shows assets and liabilities yet it is not a Balance Sheet. It is so because the values of the assets and liabilities, shown in the Statement of Affairs are merely the result of estimates made by the owner and no Ledger Accounts exist for them. Since, these amounts are not drawn from the accounts, they cannot strictly be called balances and their depiction as liabilities and assets in a Balance Sheet.

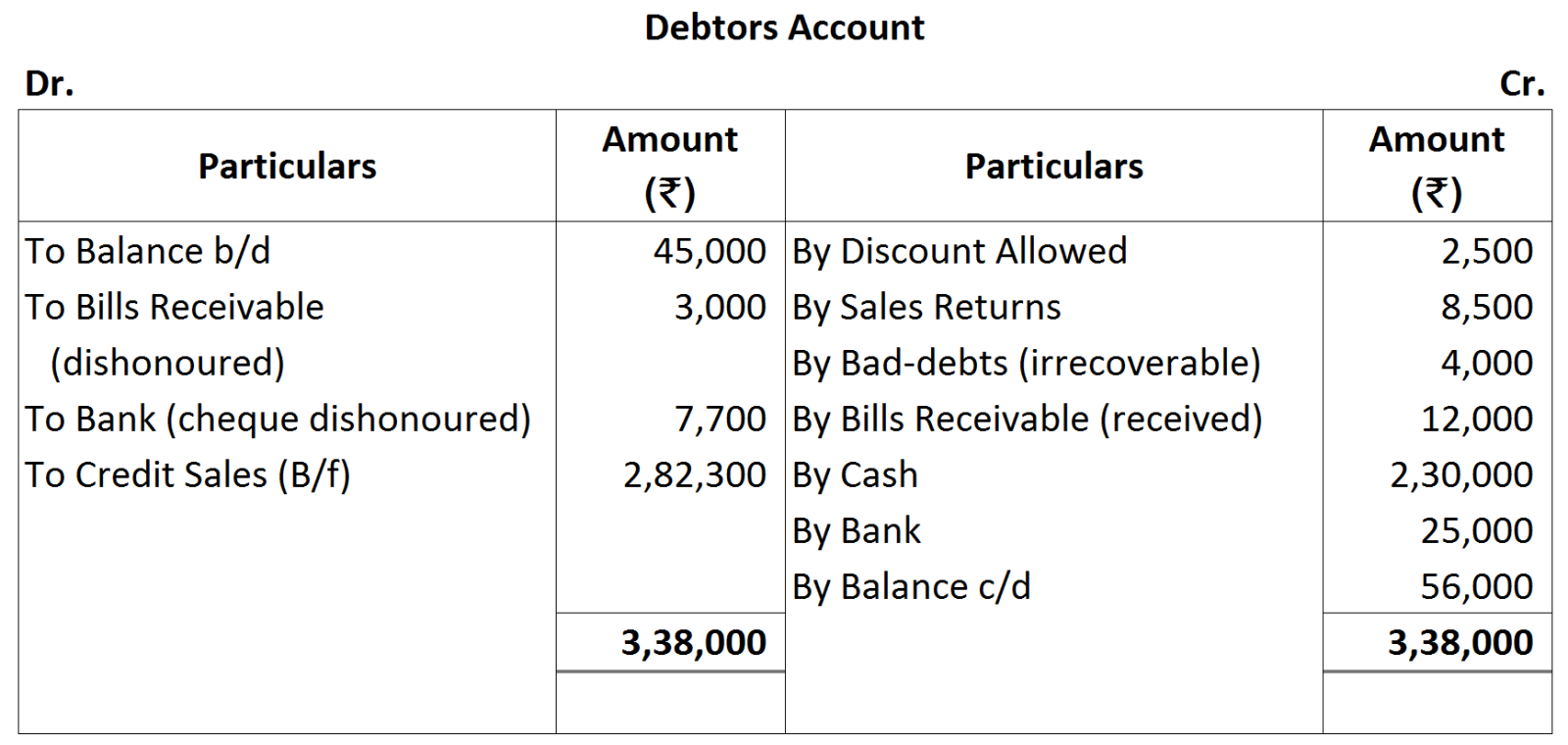

Total Sales = Cash Sales + Credit Sales

Total Sales = Cash Sales + Credit Sales

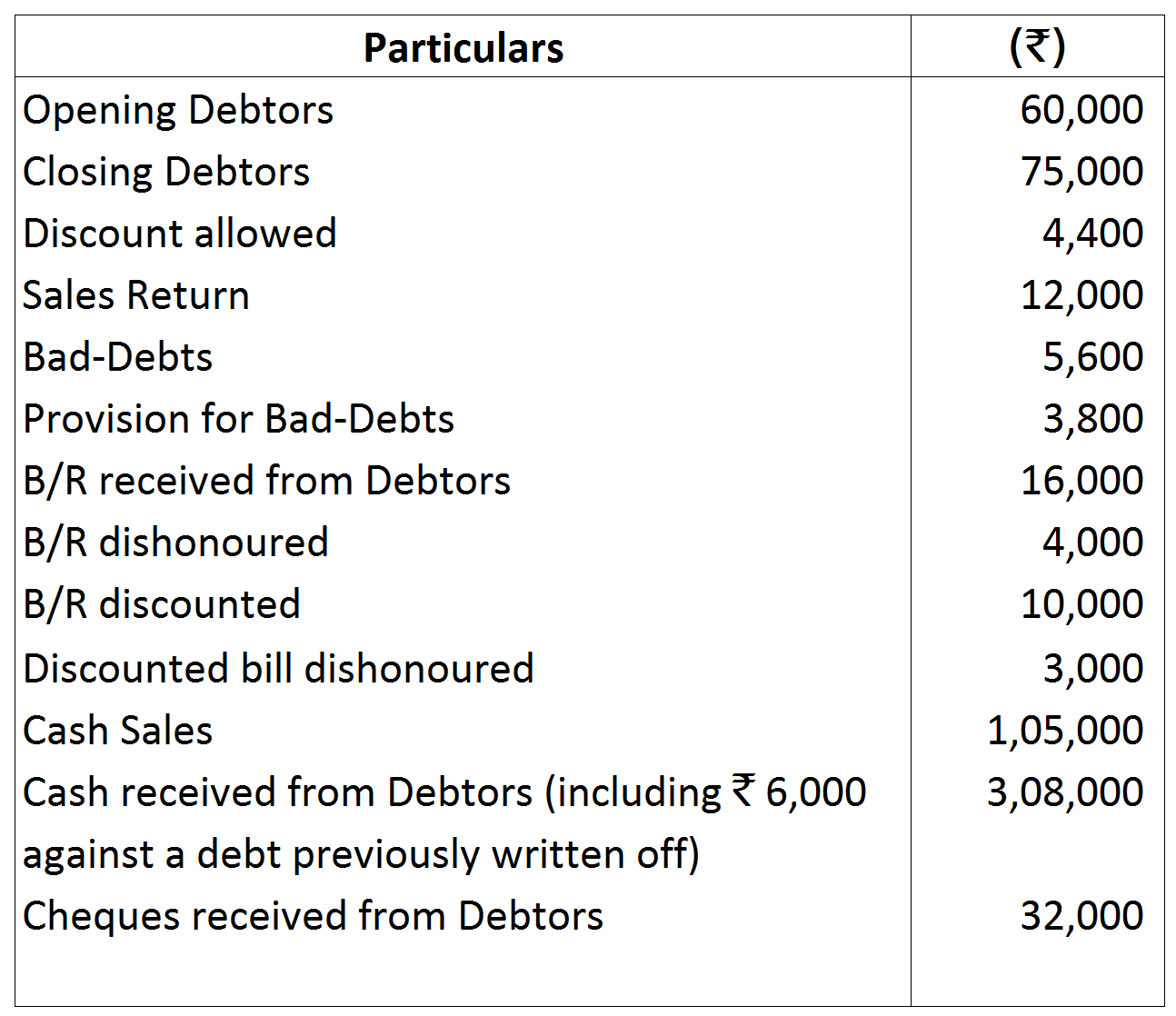

Note: Drawings include loan to brother, withdrawals in cash, rent and electricity charges.

Note: Drawings include loan to brother, withdrawals in cash, rent and electricity charges.

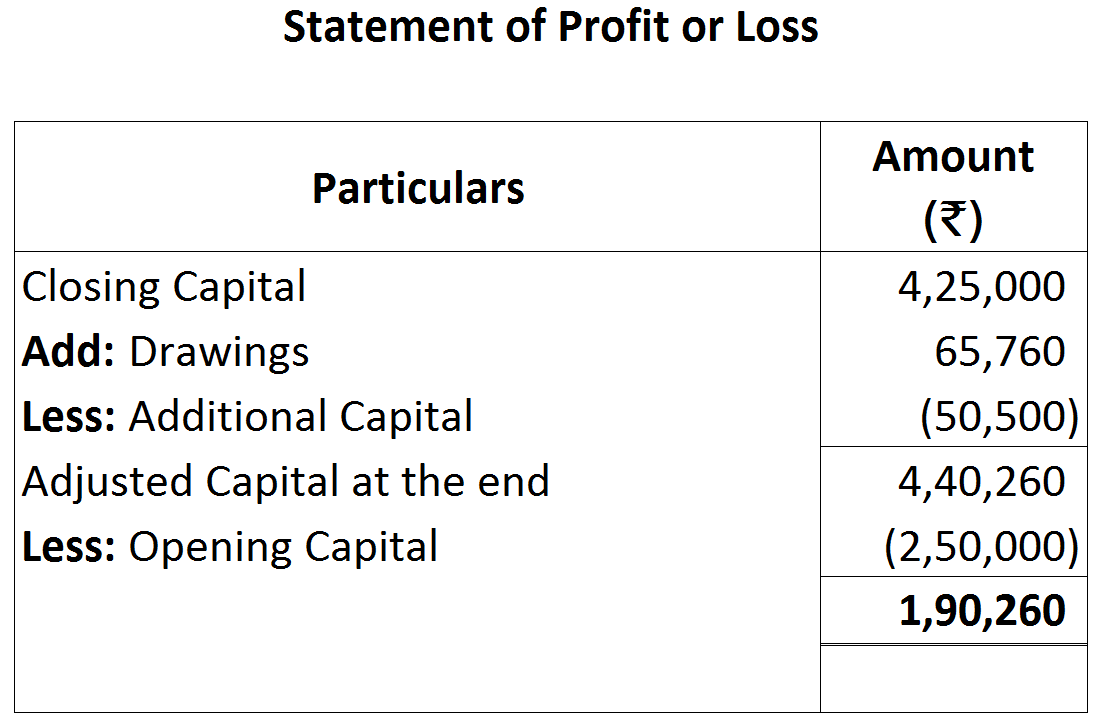

Cash withdrawn = ₹ (20,000 × 12) = ₹ 2,40,000

Cash withdrawn = ₹ (20,000 × 12) = ₹ 2,40,000