Question 14 Marks

Define depreciation. State any two reasons for providing depreciation.

Answer

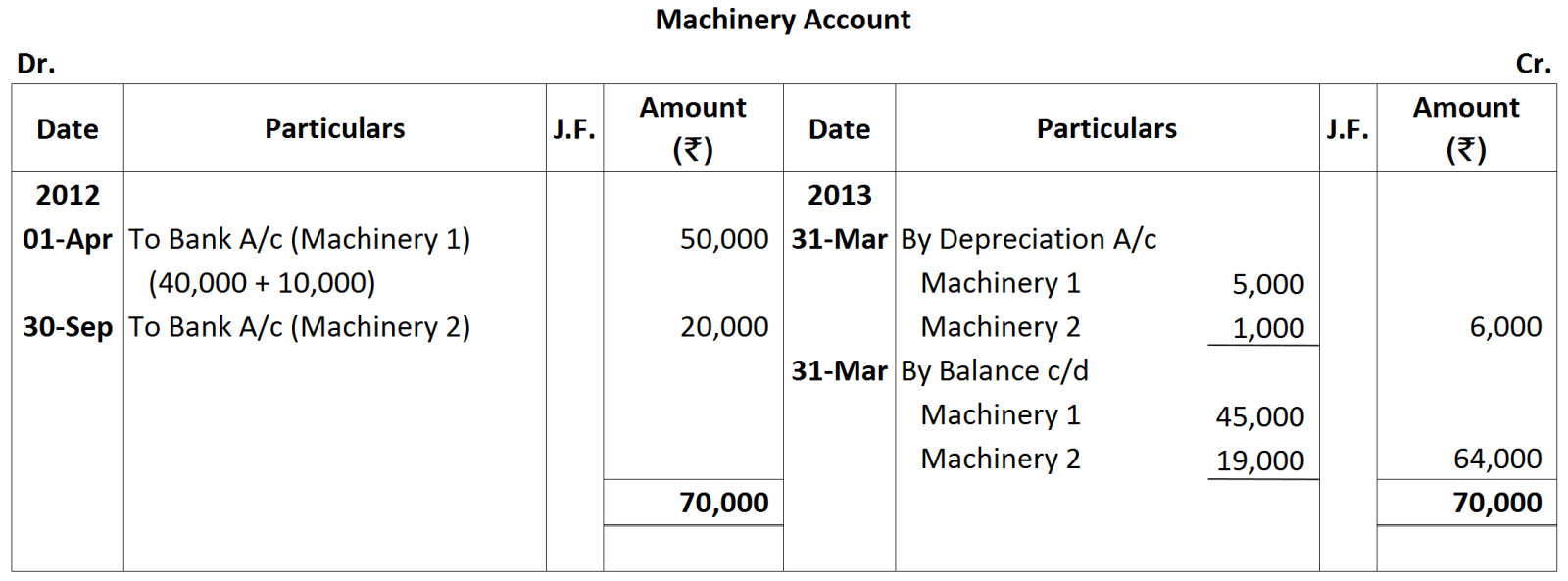

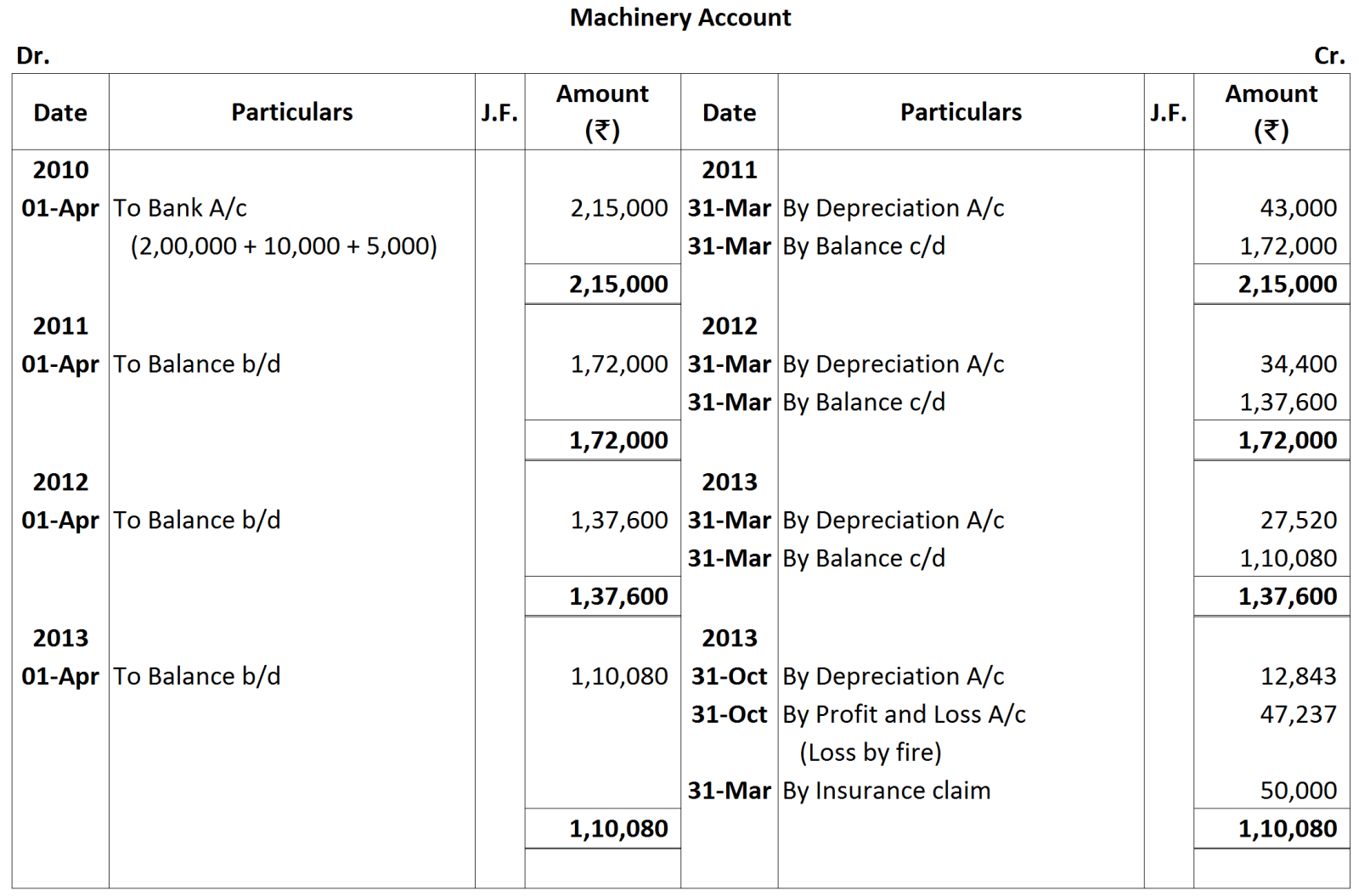

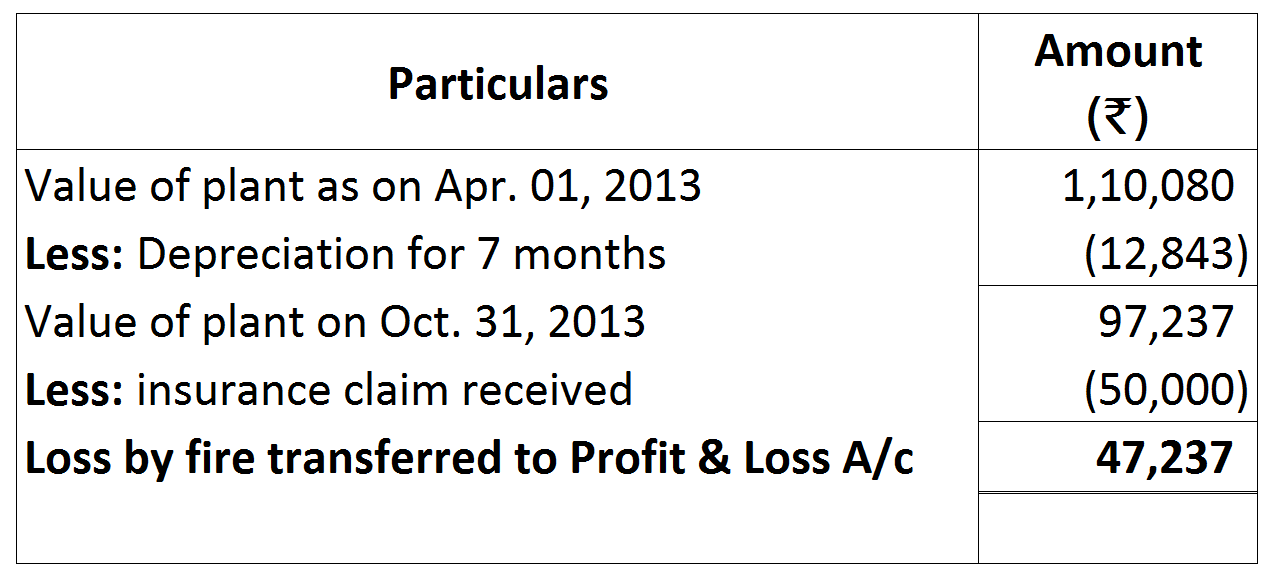

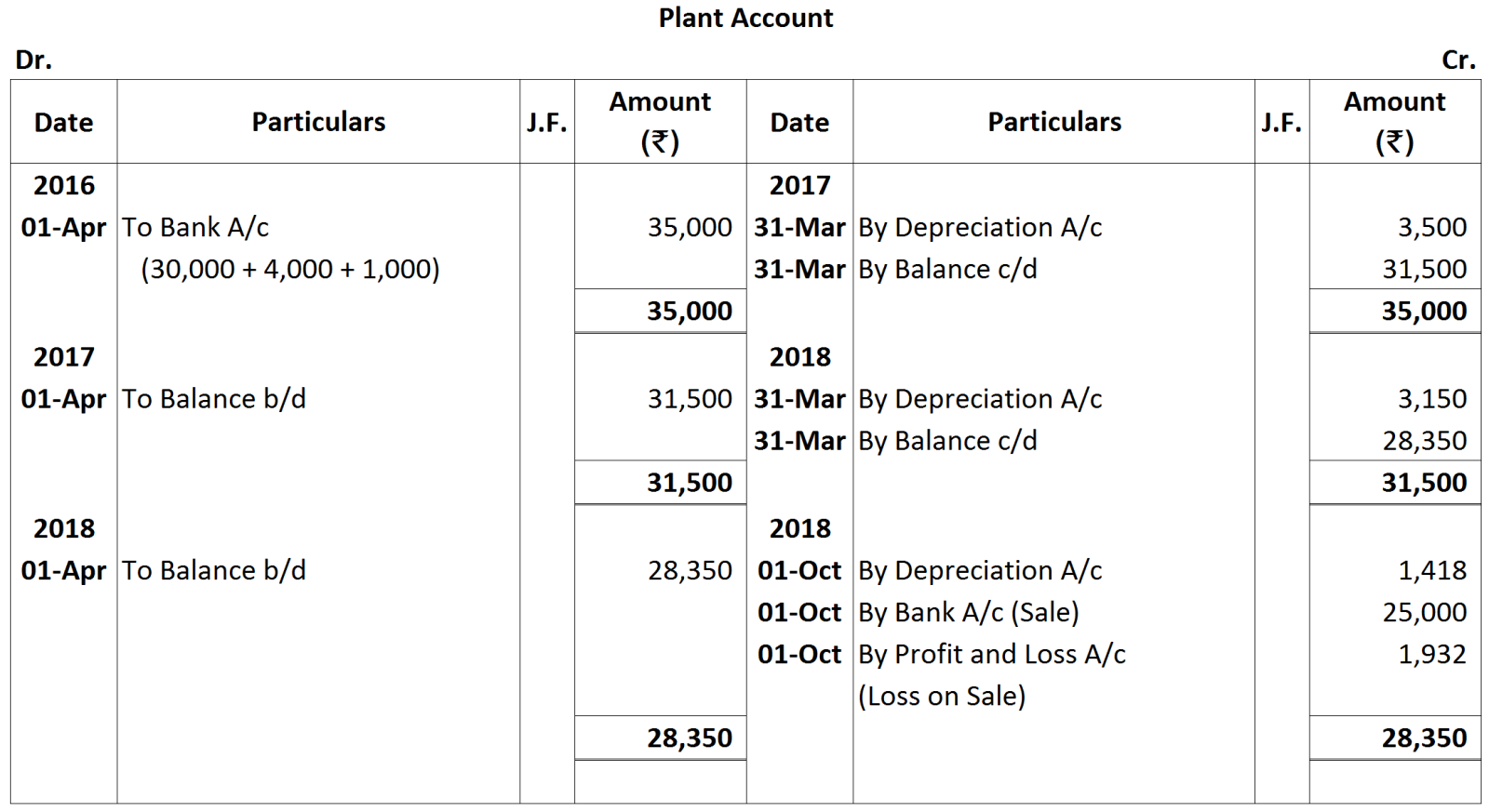

View full question & answer→In every business there are certain assets of a fixed nature that are needed for the conduct of business operations. Some examples of such assets are Building, Plant and Machinery, Motor Vehicles, Furniture, Office equipments etc. These assets have a definite span of life after the expiry of which the assets will lose their usefulness for the business operations. Fall in the value and utility of such assets due to their constant use and expiry of tine is termed as depreciation. In other words, the process of allocation of the cost of a fixed asset over its useful life is known as depreciation.

The causes (reasons) of Depreciation are:

The causes (reasons) of Depreciation are:

- Use of Asset: Use of asset leads to its wear and tear and thus fall in its value.

- Obsolescence: If a better and cost effective machine becomes available, old machine may have to be discarded even though it is capable of being used. Thus, it leads to reduction of useful life of the asset.

- Accidents: Accidental loss may be permanent but is not continuing and gradual.