Question 14 Marks

Why is Balance Sheet prepared?

Answer

View full question & answer→Balance Sheet is the statement prepared after preparing Trading and Profit and Loss Account. Balance Sheet is “a statement which sets out the assets and liabilities of a firm or an institution as at a certain date.”

In the words of Francis R. Stead. "A Balance Sheet is a screen picture of the financial position of a going business at a certain moment."

In the words of Francis R. Stead. "A Balance Sheet is a screen picture of the financial position of a going business at a certain moment."

Notes:

Notes:

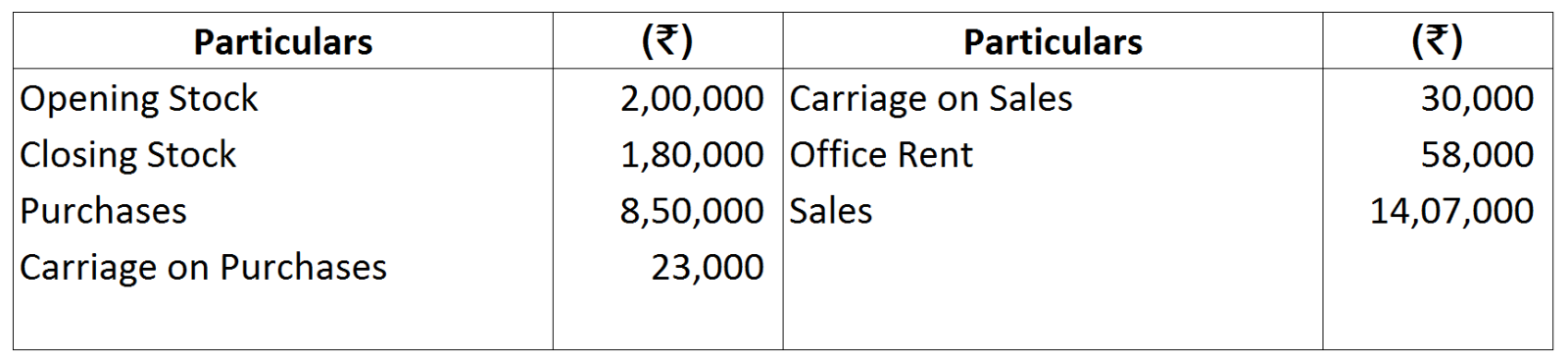

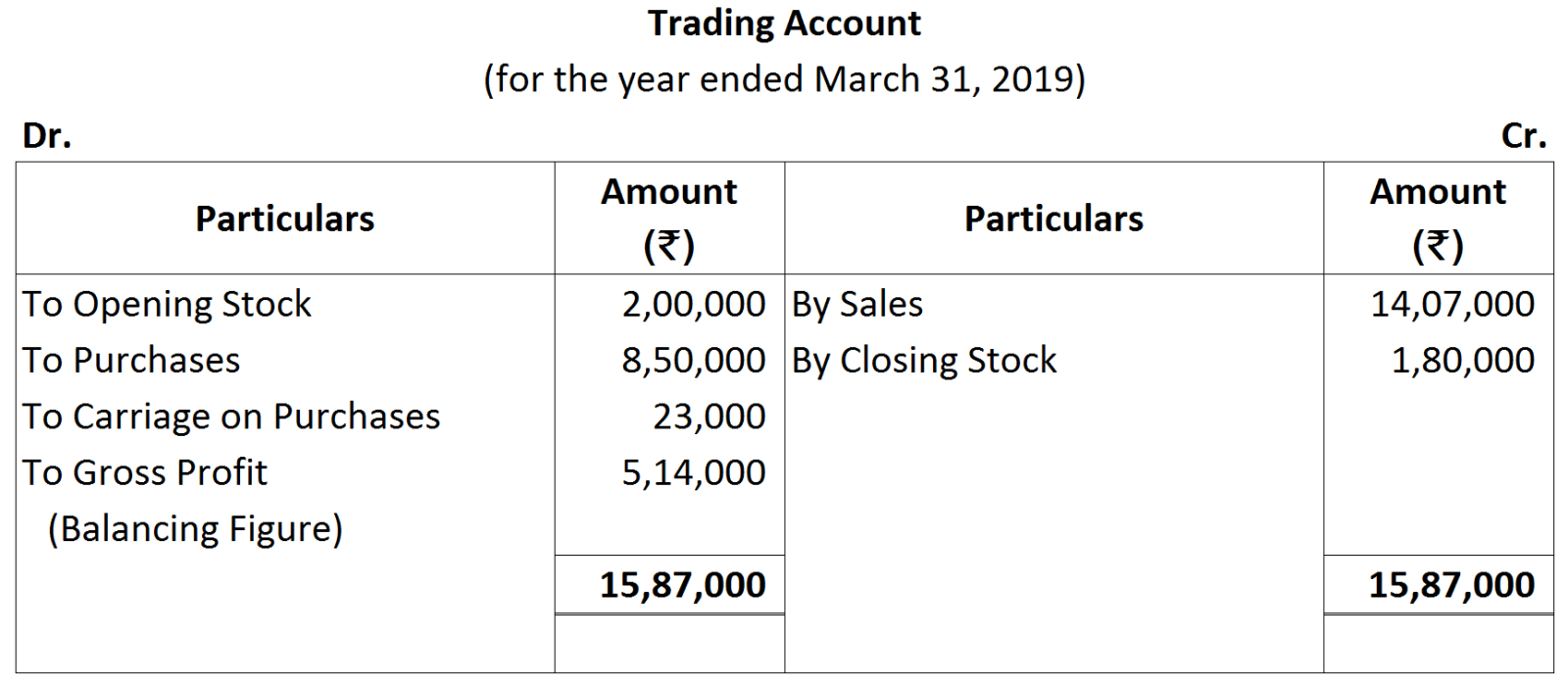

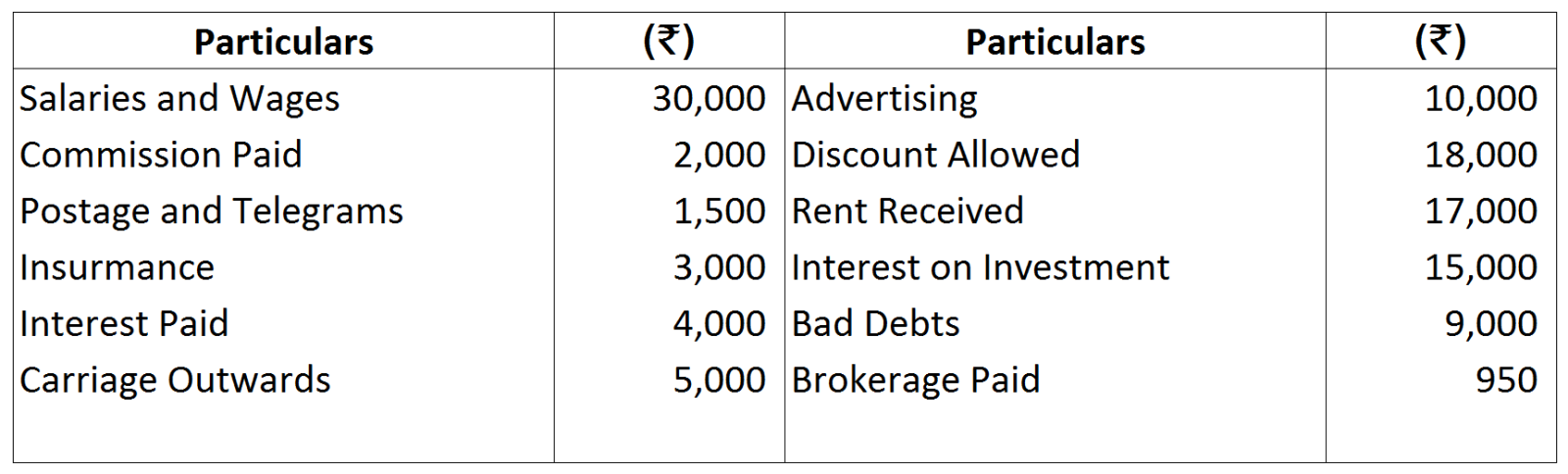

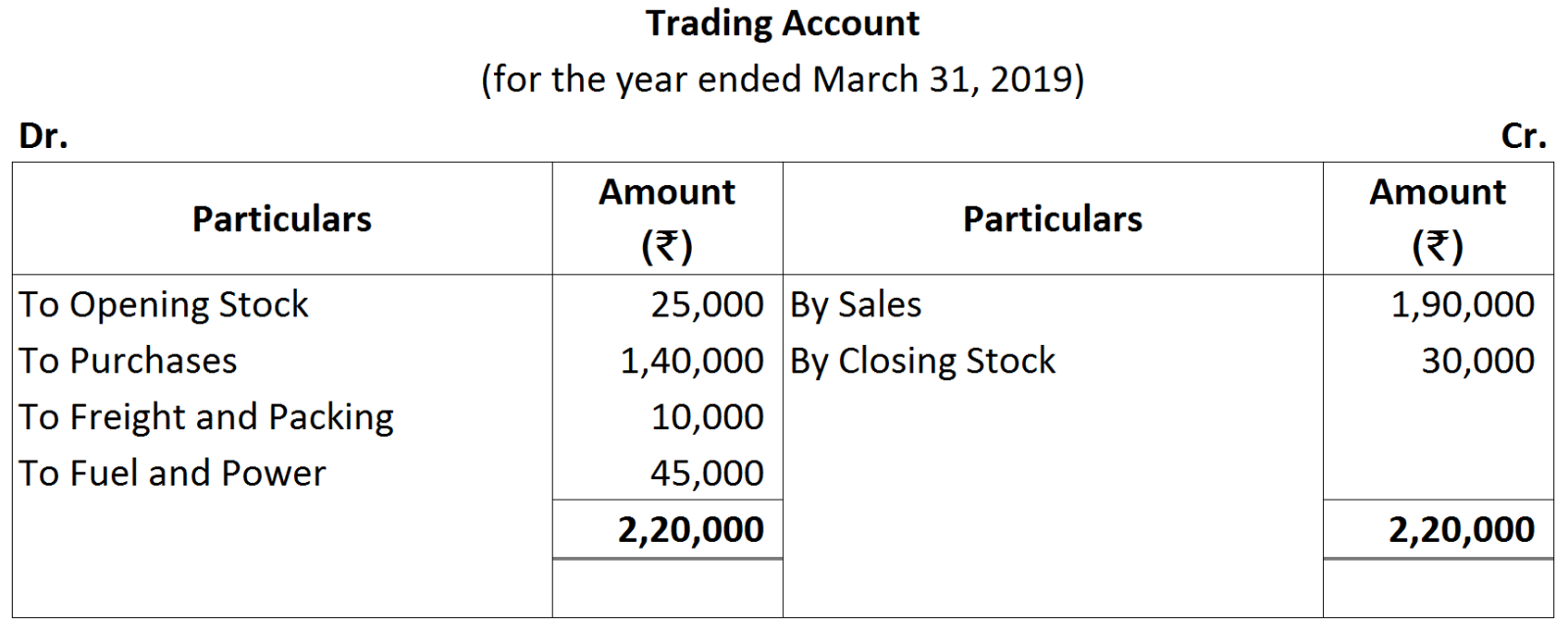

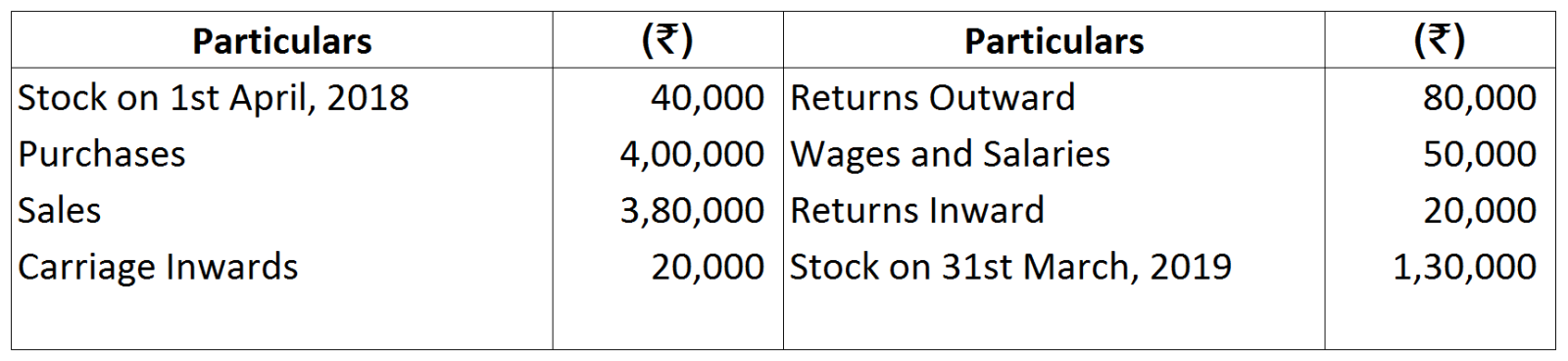

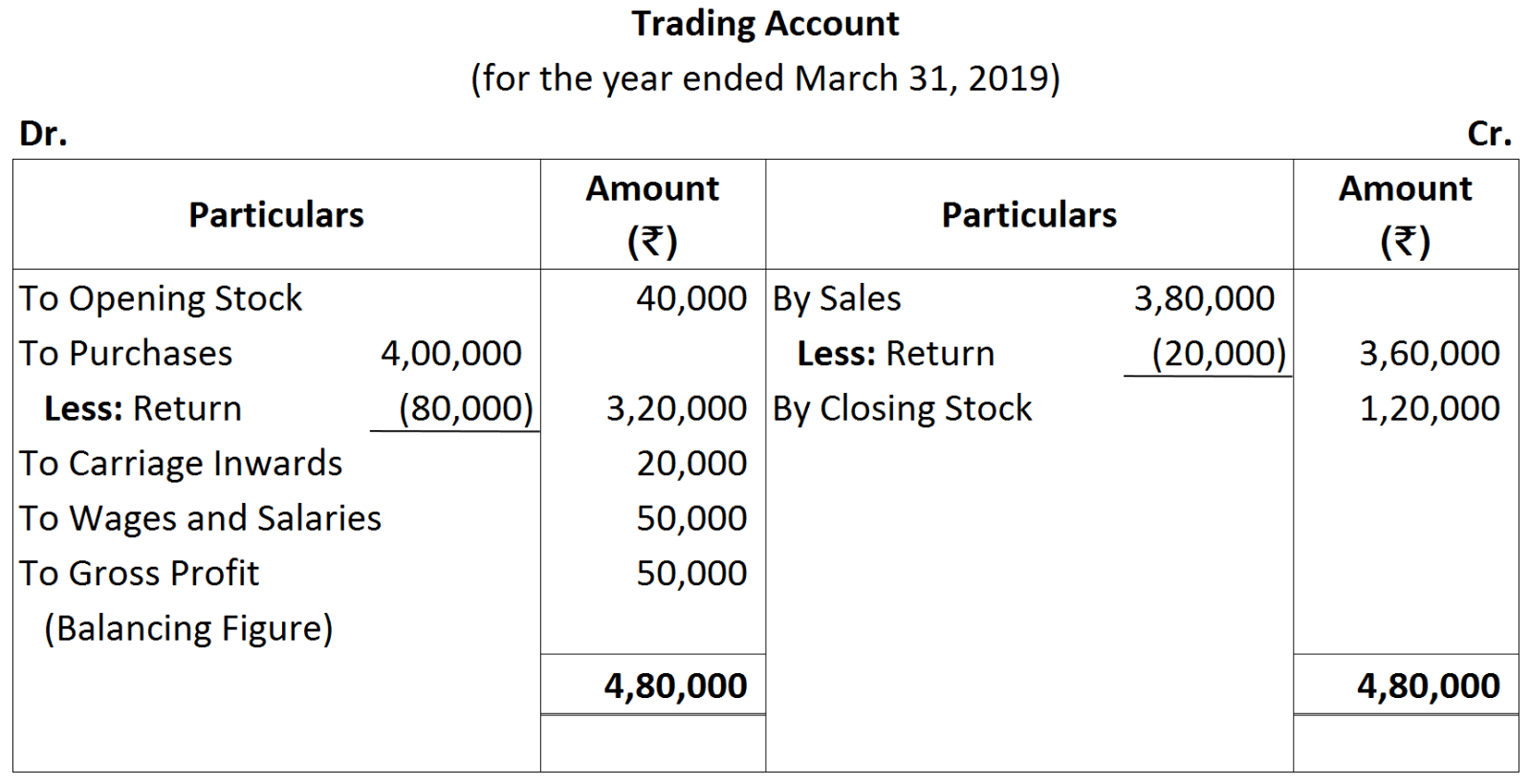

Note: Carriage on Sales and Office Rent are the Indirect Expenses, therefore, these are not considered to compute the amount of Gross Profit.

Note: Carriage on Sales and Office Rent are the Indirect Expenses, therefore, these are not considered to compute the amount of Gross Profit.

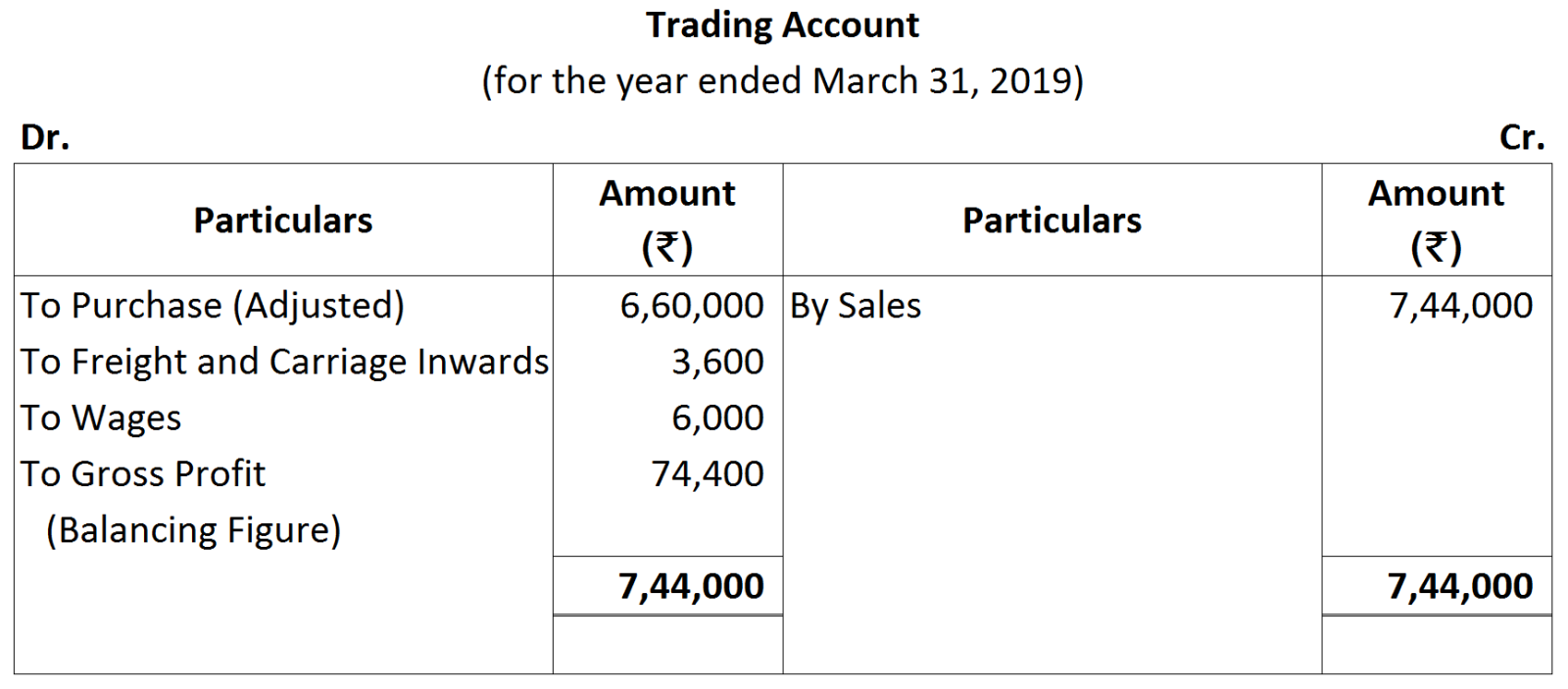

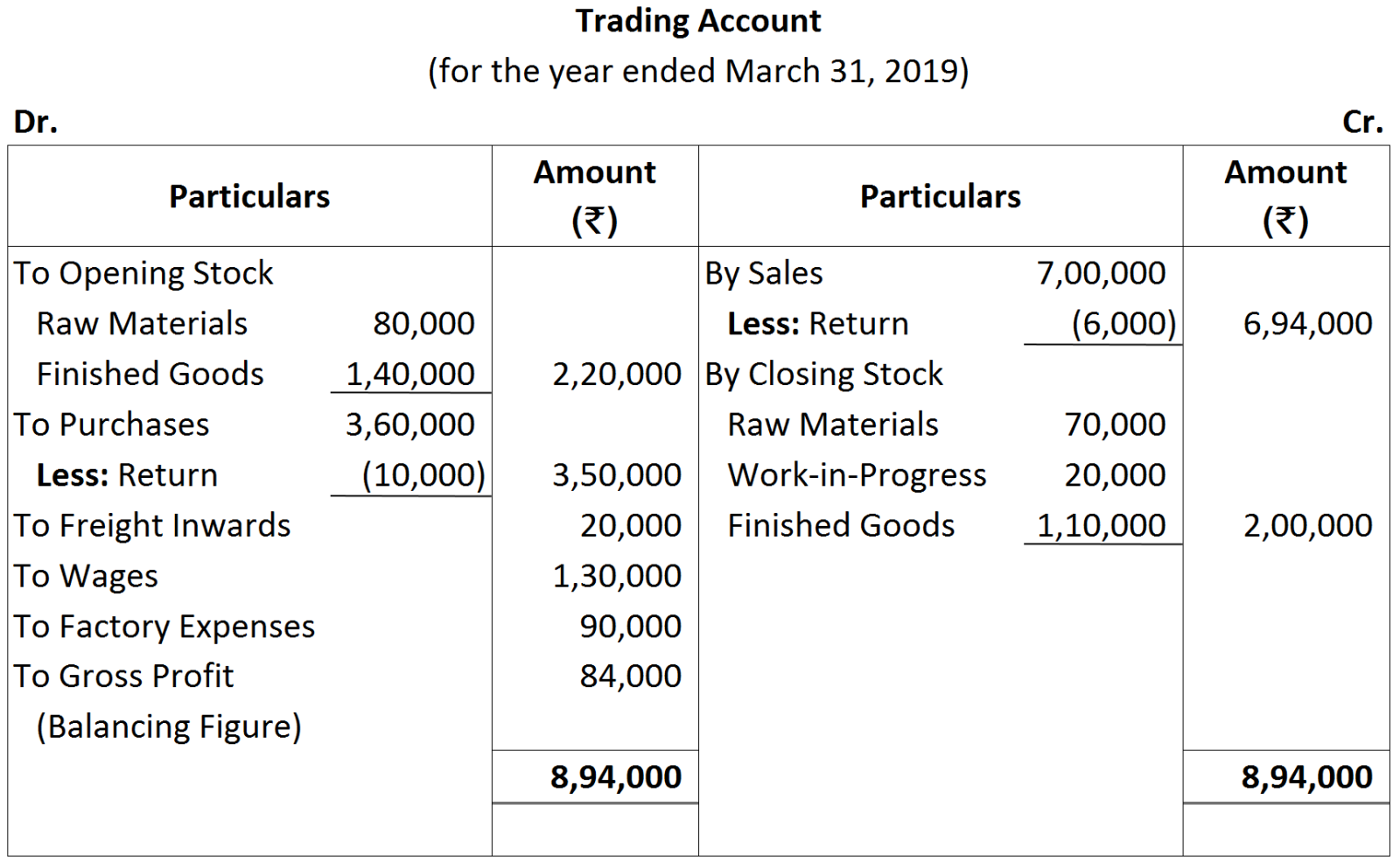

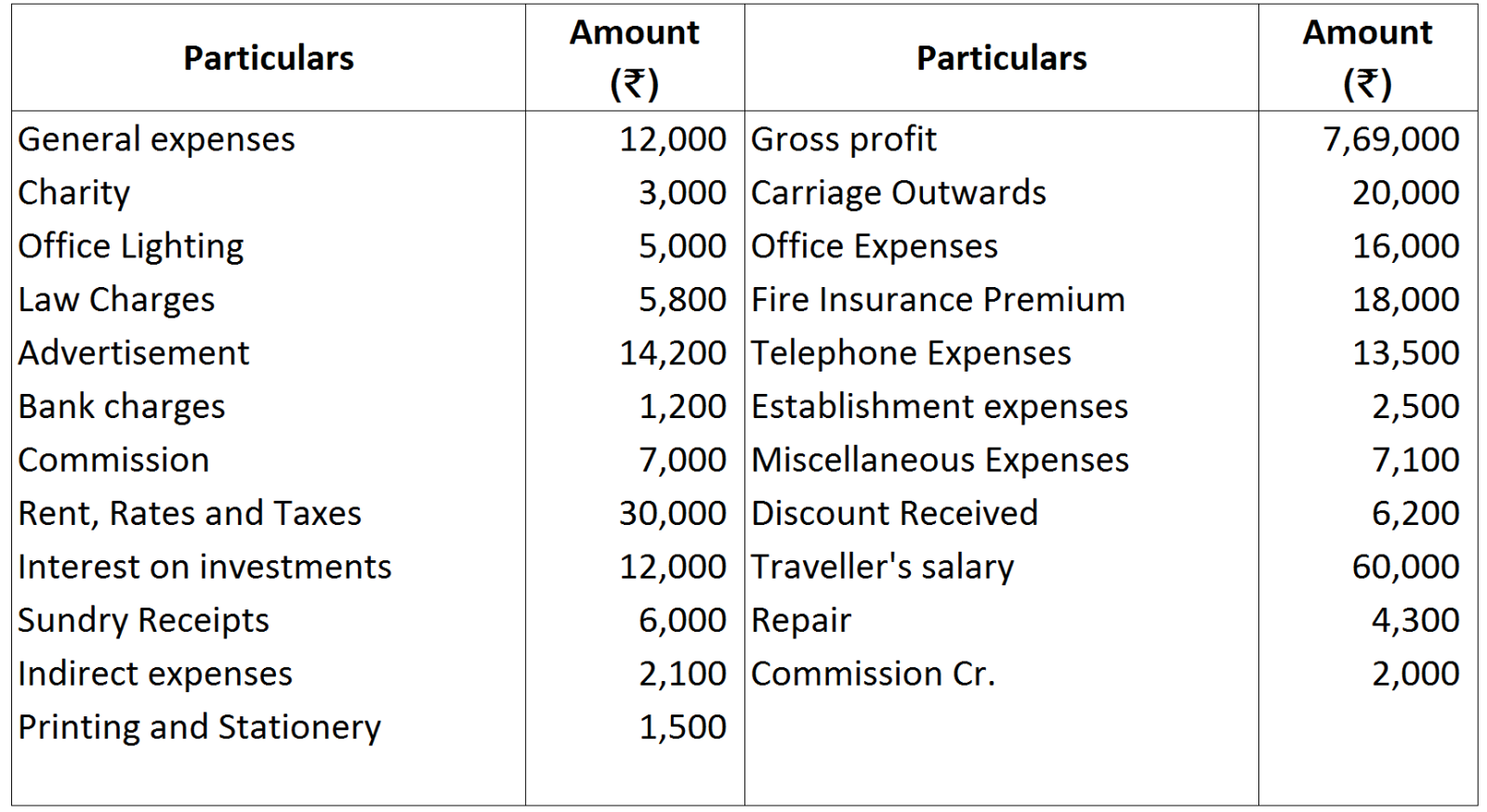

Note: Freight outwards is an indirect expense. It will be recorded in Profit & Loss A/c.

Note: Freight outwards is an indirect expense. It will be recorded in Profit & Loss A/c.

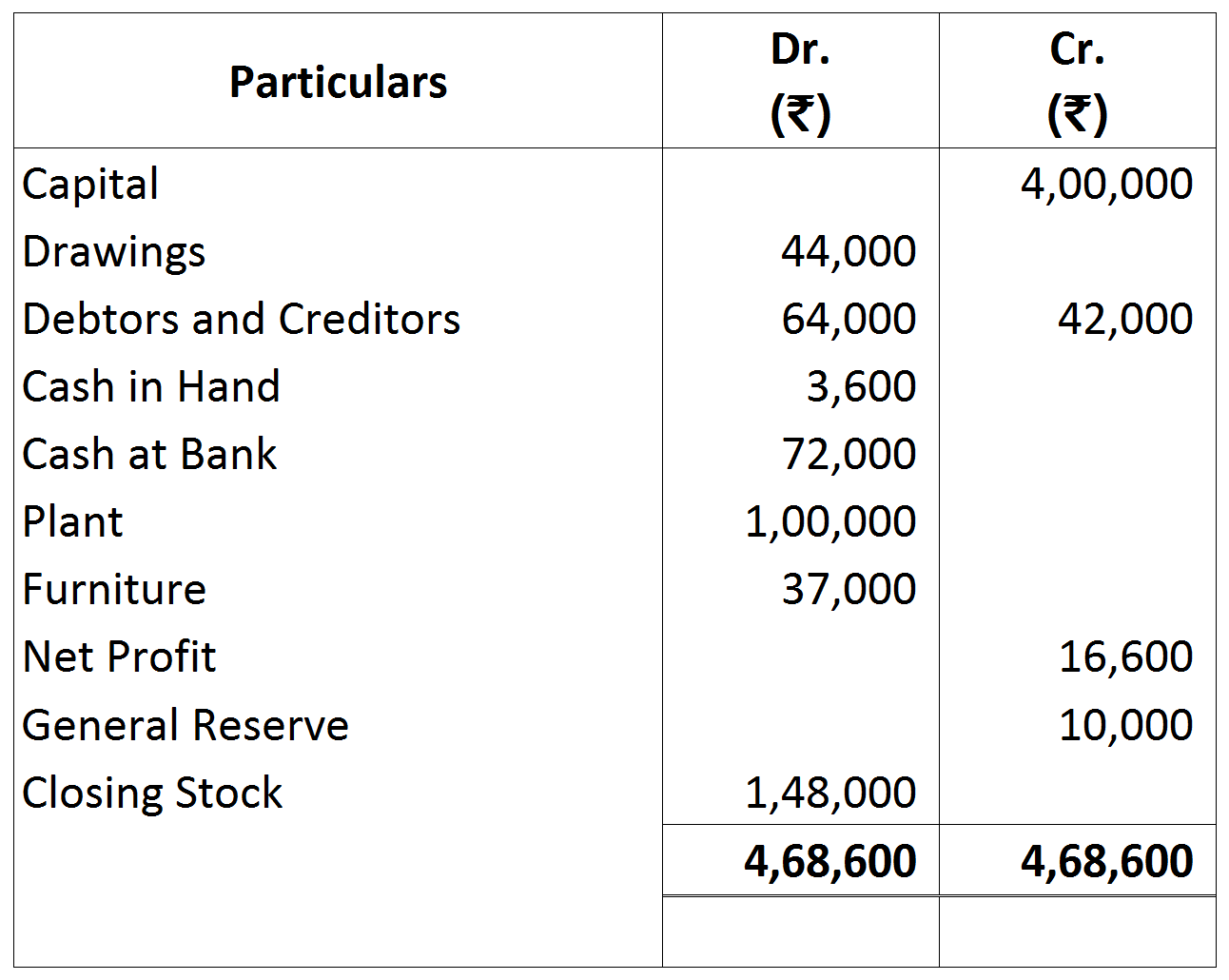

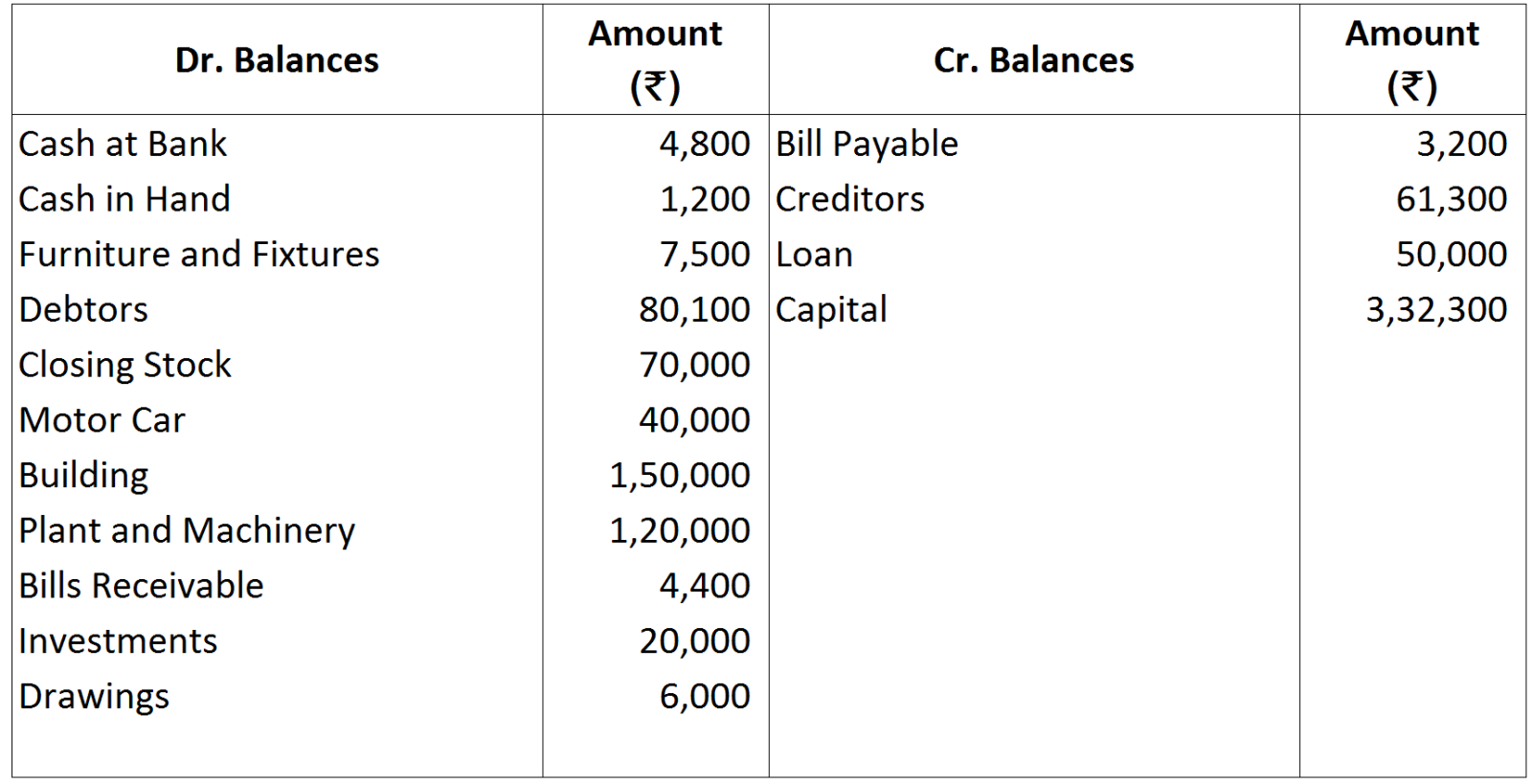

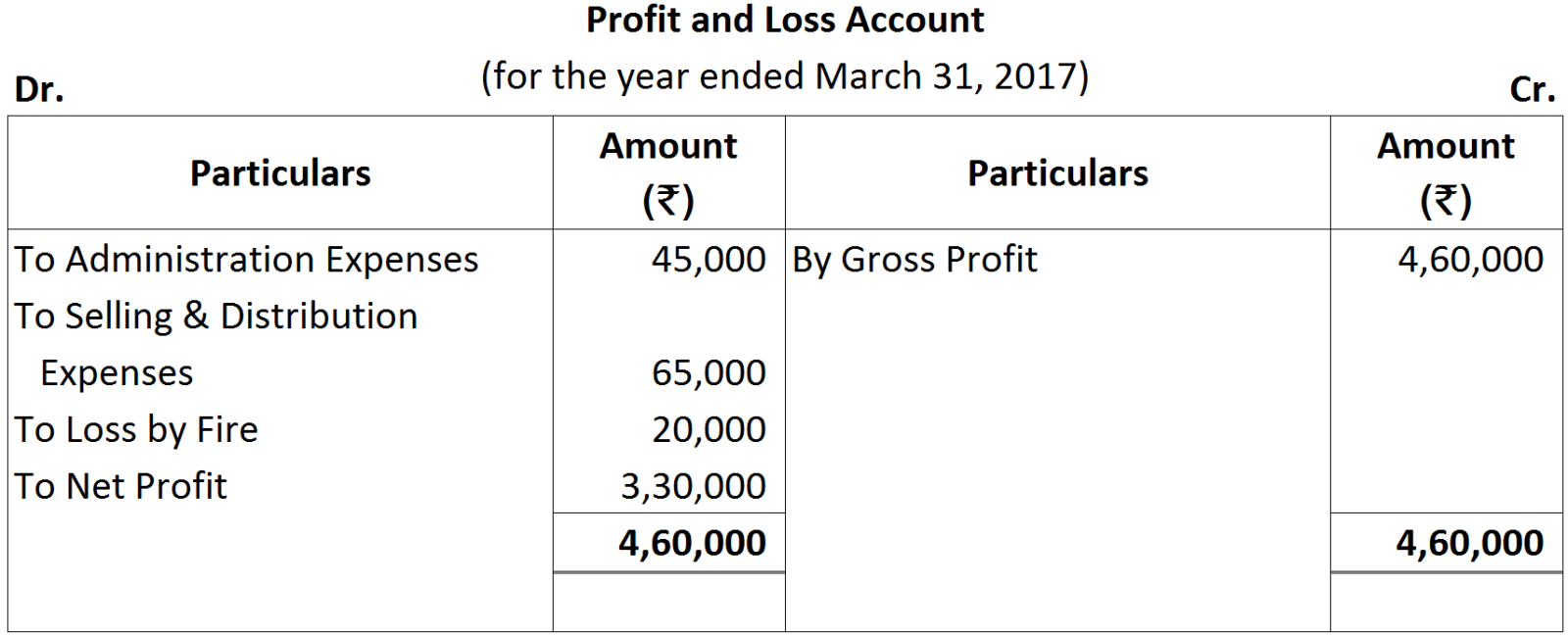

Prepare his Balance Sheet as at 31st March, 2017.

Prepare his Balance Sheet as at 31st March, 2017.

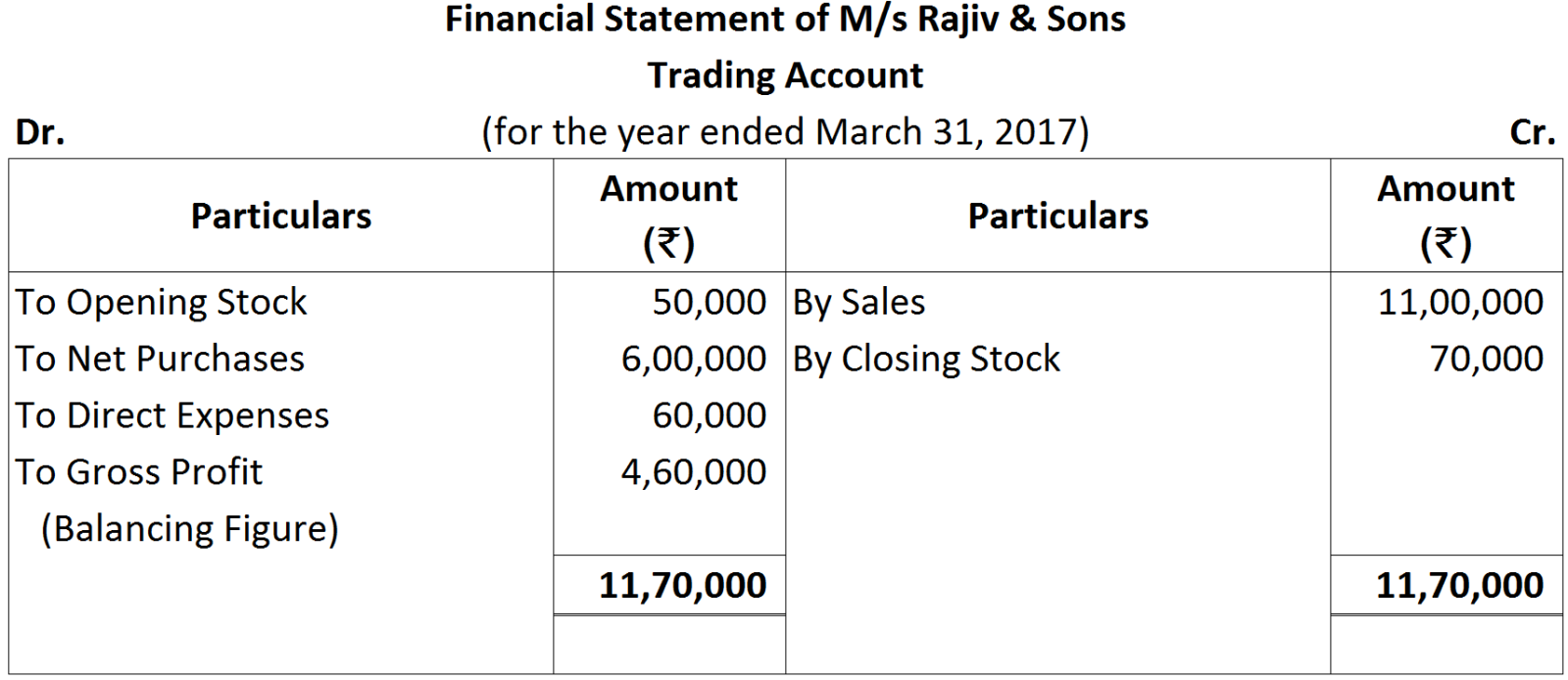

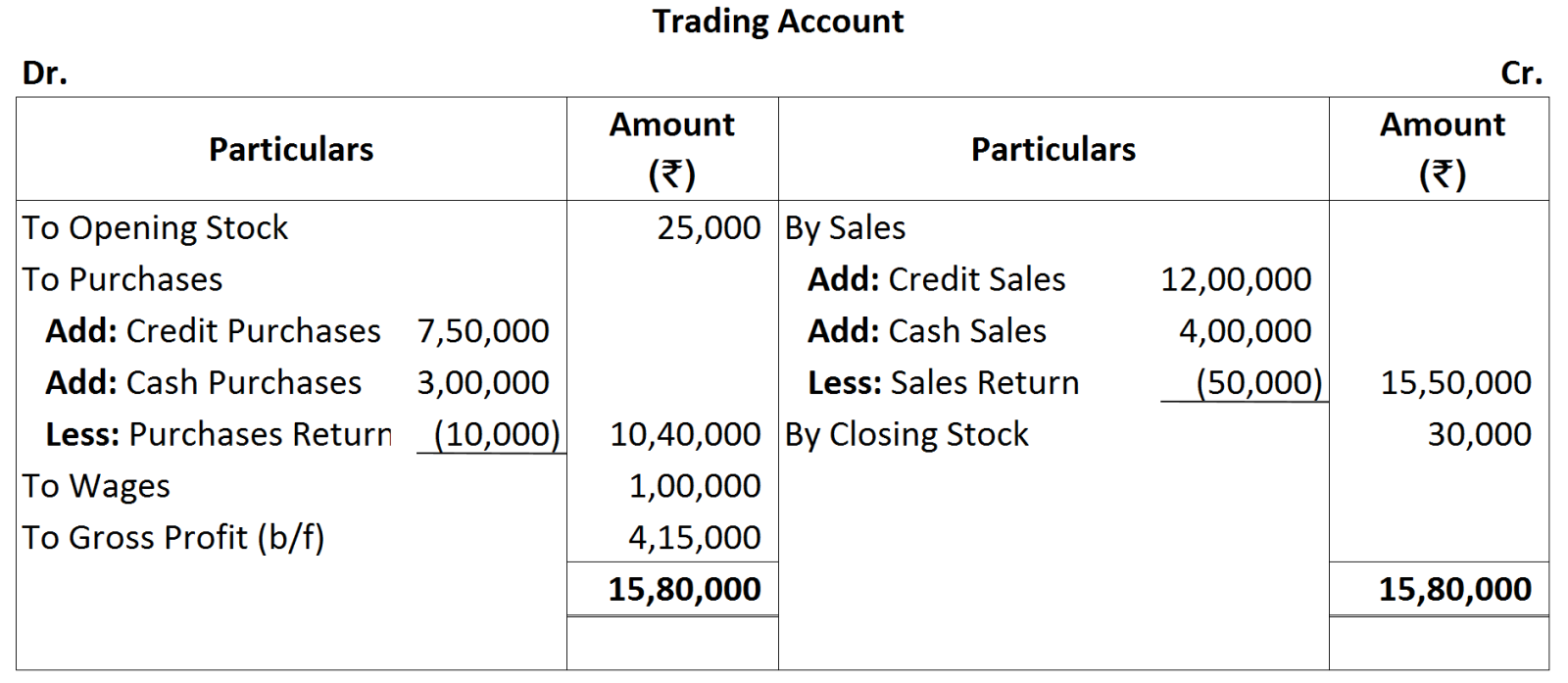

Working Notes:

Working Notes:

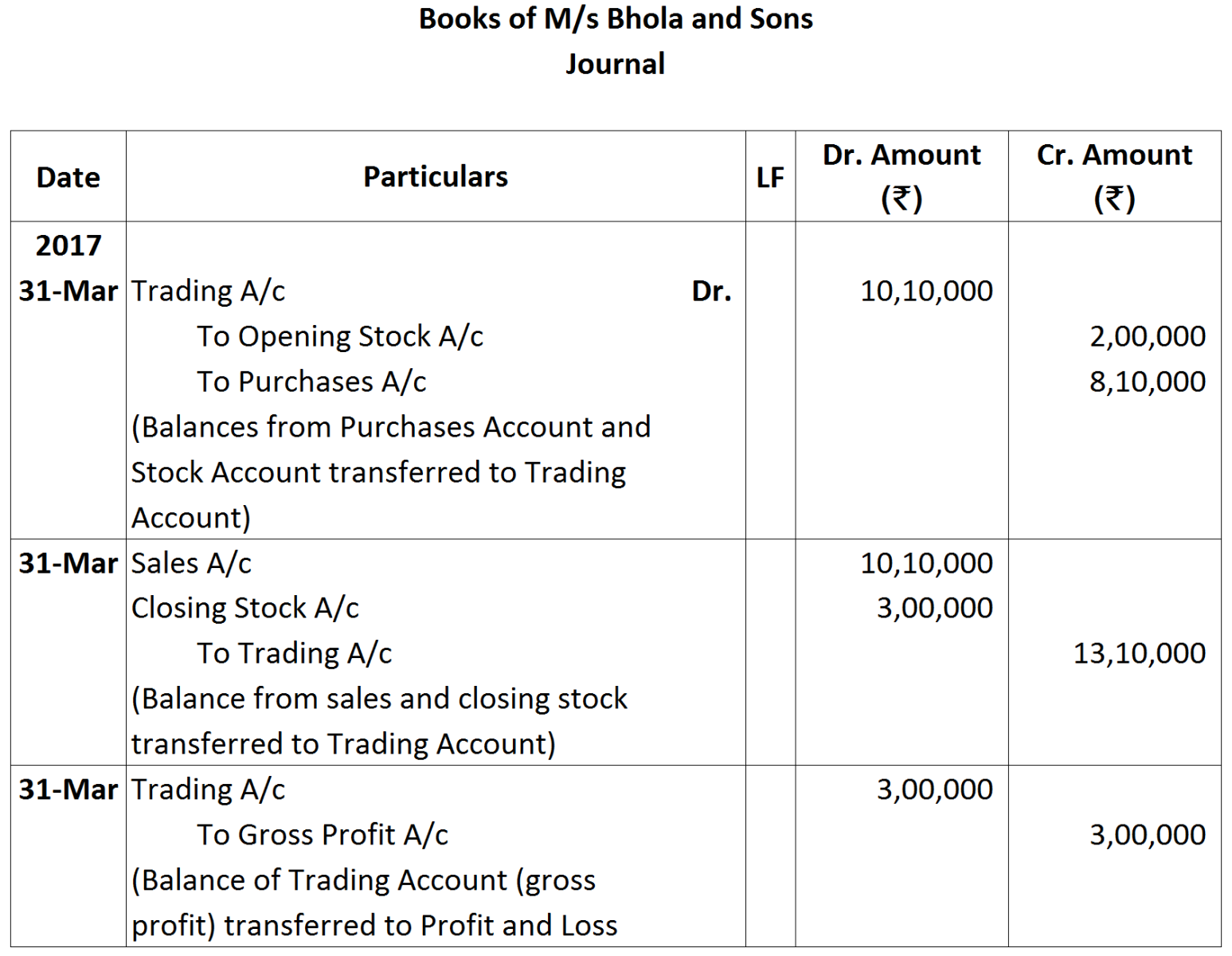

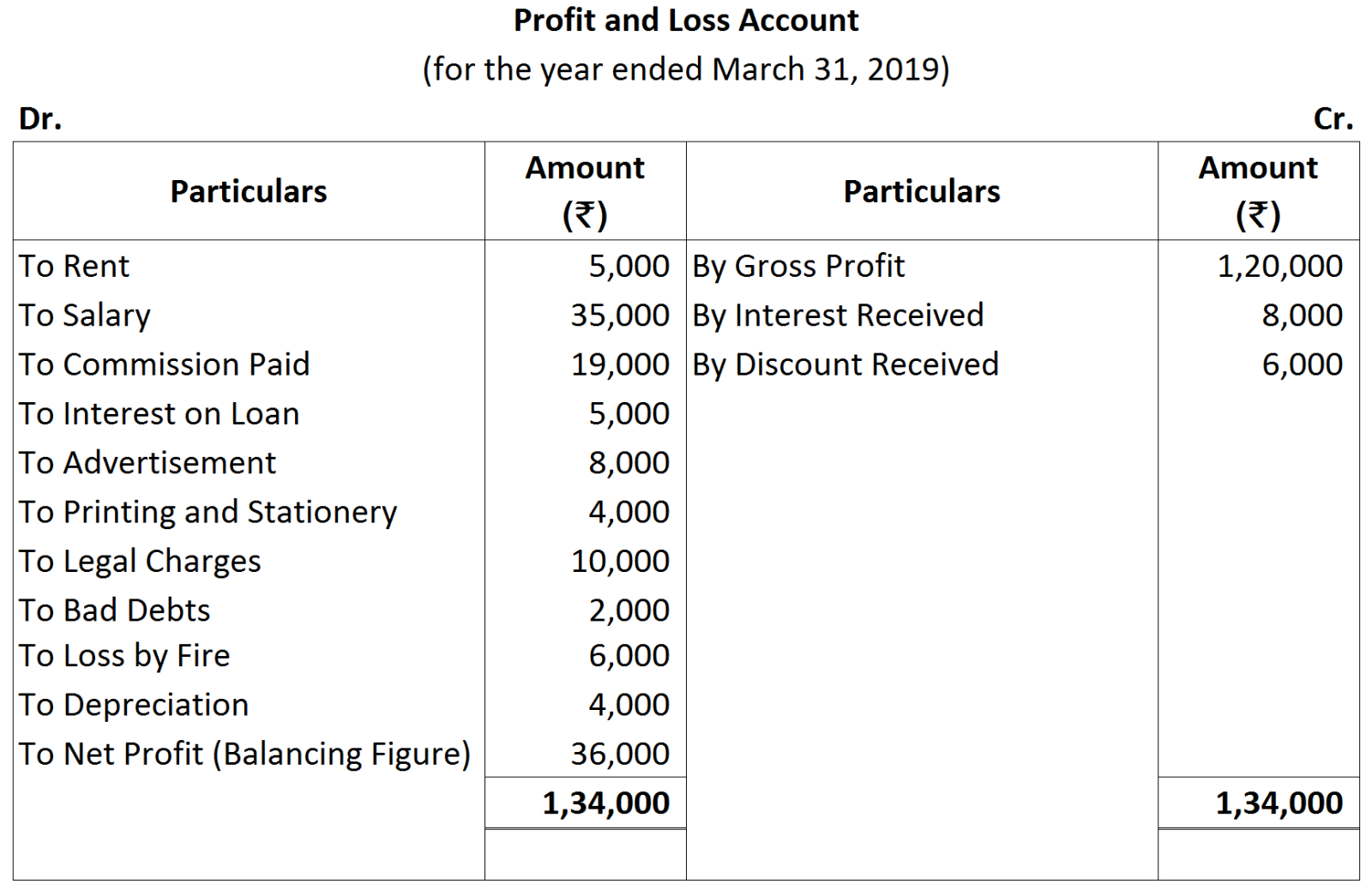

Note: ₹ 1,000 Input IGST after adjusting against Output IGST will be shown on the asset side of the balance sheet.

Note: ₹ 1,000 Input IGST after adjusting against Output IGST will be shown on the asset side of the balance sheet.