Question 11 Mark

What is the adjustment entry passed for provision for discount on Debtors?

33 questions · timed · auto-graded

|

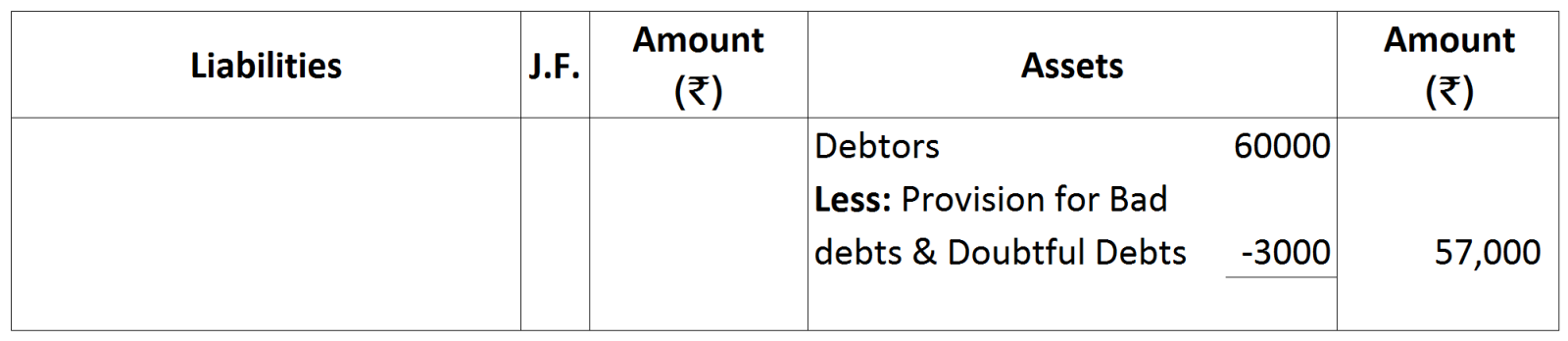

Sundry Debtors (including a B/R for ₹ 5,000 received from Giriraj)

|

|

|

|

Bad Debts

|

1,20,000

|

|

|

Provision for Doubtful Debts

|

3,000

|

1,800

|

| adjustment entry | Treatment in P & L A/C | Treatment in Balance Sheet | ||

| i. | Accrued Income. | Added in income on credit side of Profit & Loss A/c. | Shown on the Assets side. | |

| ii. | Unearned Income. | Deducted from income on the credit side of Profit & Loss A/c. | Shown on the Liabilities side. |

|

|

|

|

Treatment in P & L a/c

|

Treatment in Balance Sheet

|

|

i.

|

Outstanding Salaries

|

|

Added in Salaries the Debit side of Profit & Loss a/c

|

Shown on the Liabilities side.

|

|

ii.

|

Accrued Interest

|

|

Added to Interest Received on the Credit side of Profit & Loss a/c

|

Shown on the Assets side.

|