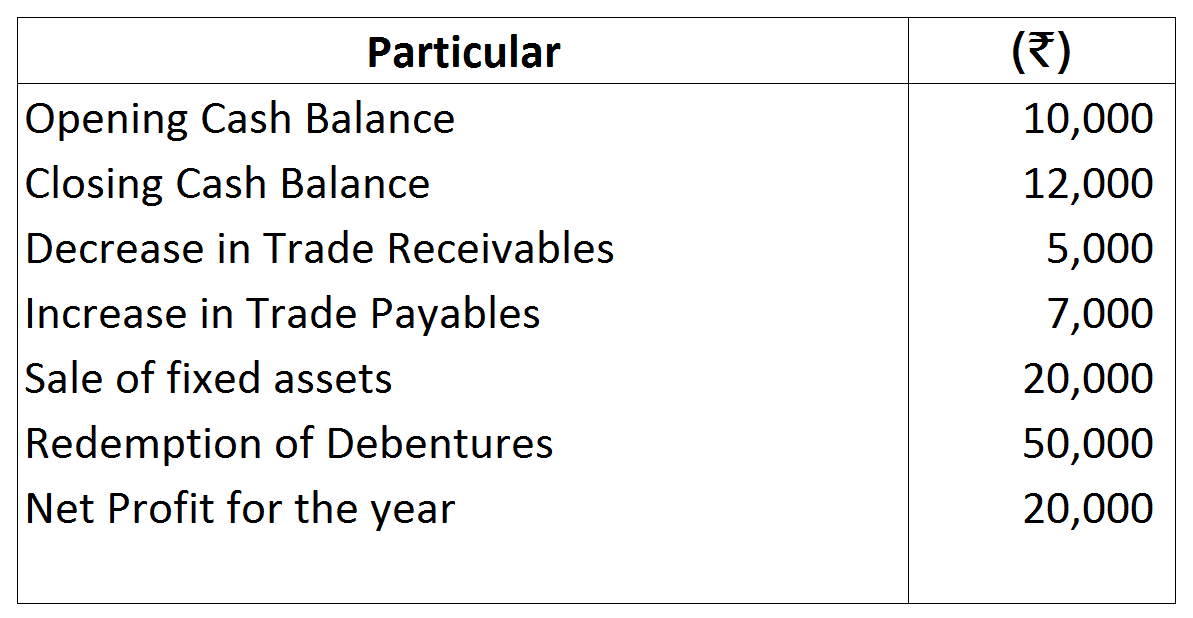

Question 14 Marks

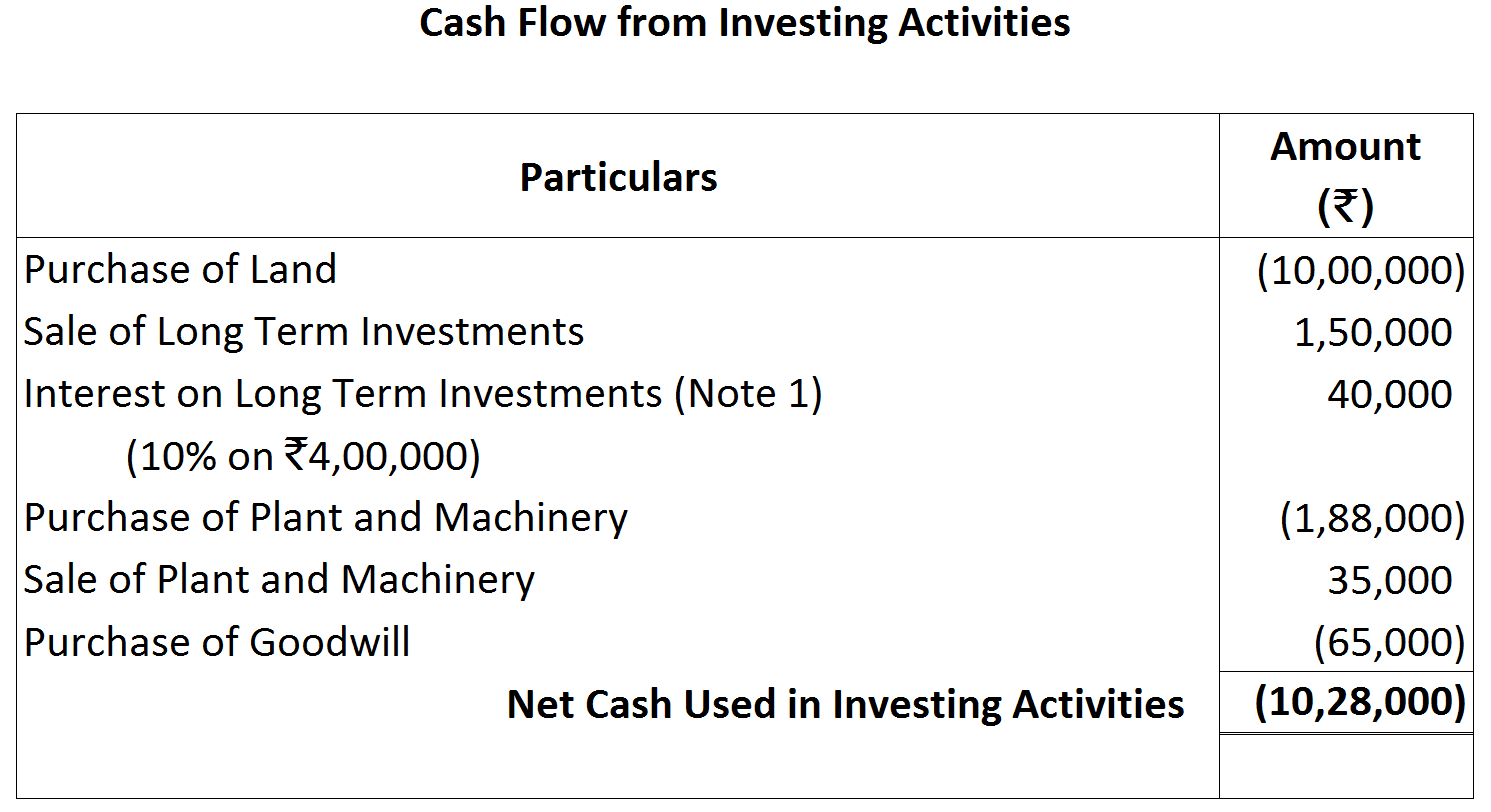

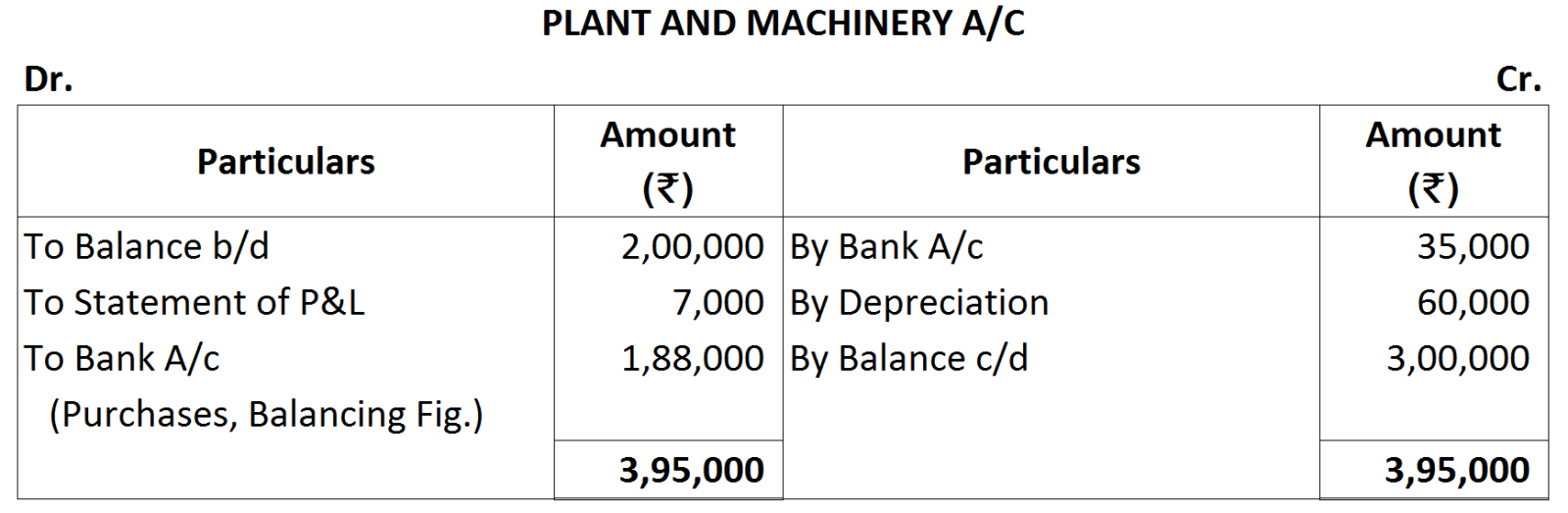

The following information has been extracted from the books of Pure Con Company. Using the information, calculate the Cash Flow from Investing Activities.

33 questions · timed · auto-graded

|

|

|

₹

|

|

a.

|

Depreciation on fixed assets

|

10,000

|

|

b.

|

Amortization of Goodwill

|

5,000

|

|

c.

|

Loss on sale of Machinery

|

7,000

|

|

d.

|

Profit on sale of Land

|

3,000

|

Notes:

Notes:  Additional Information:

Additional Information:

Notes:

Notes:

|

|

₹

|

|

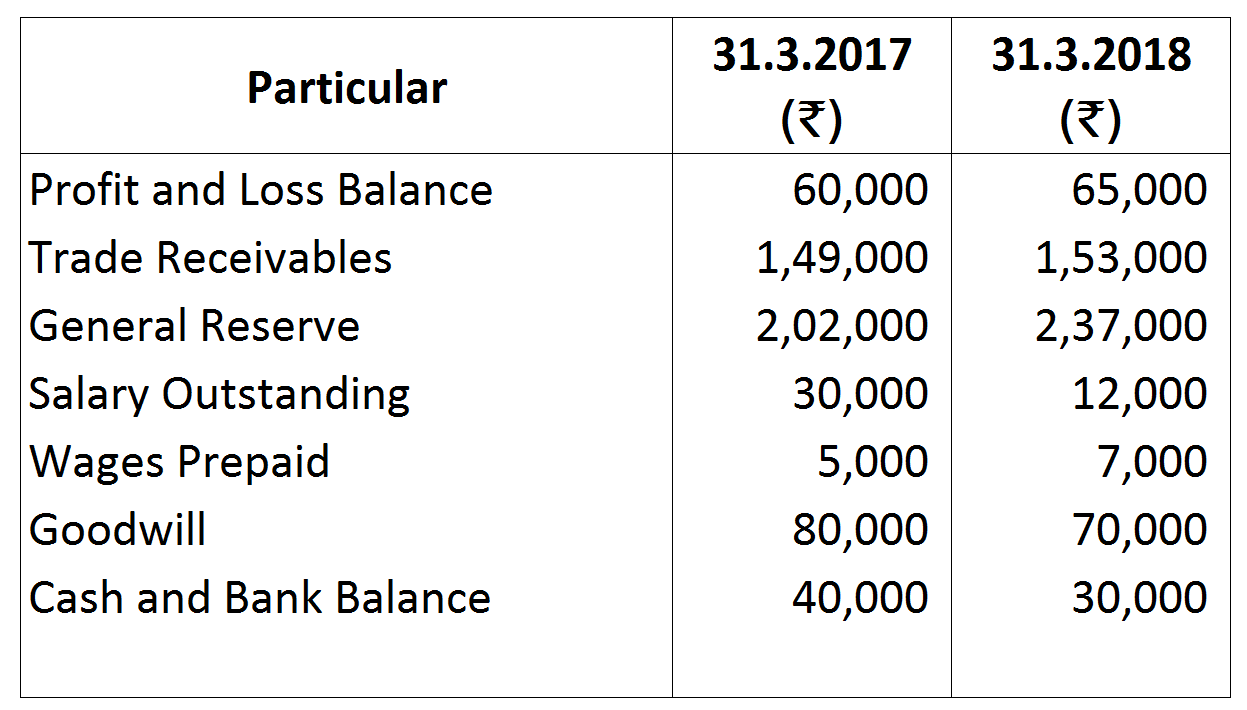

Negative Balance of P & Lon 31.3.2017

|

(20,000)

|

|

(+) Positive Balance of P & Lon 31.3.2018

|

50,000

|

|

|

70,000

|

|

Add: Transfer to General Reserve

|

20,000

|

|

|

90,000

|

|

|

|

| ₹ | ||

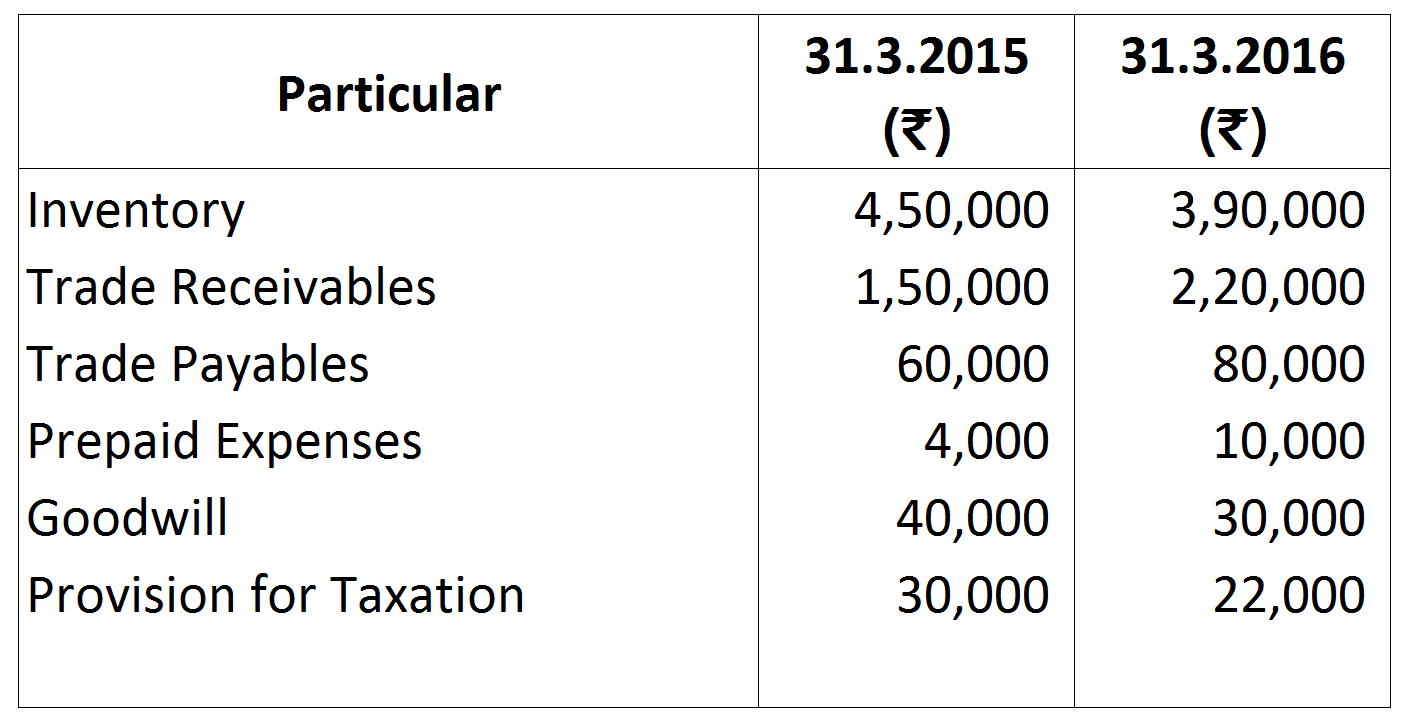

| 1. | Bad Debts written off during the year | 10,000 |

| 2. | Depreciation on fixed assets charged during the year | 34,000 |

Note:

Note:

|

|

₹

|

|

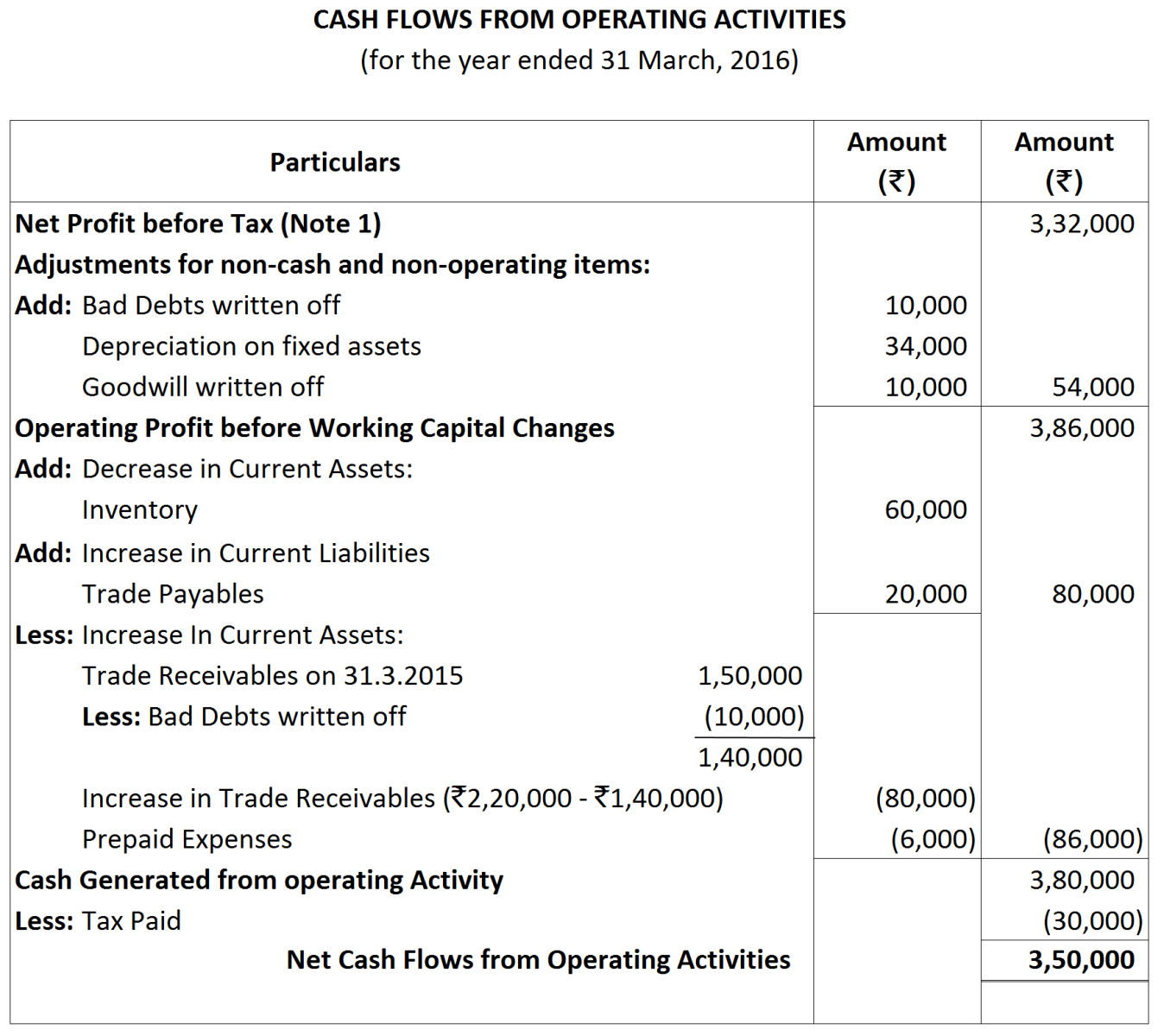

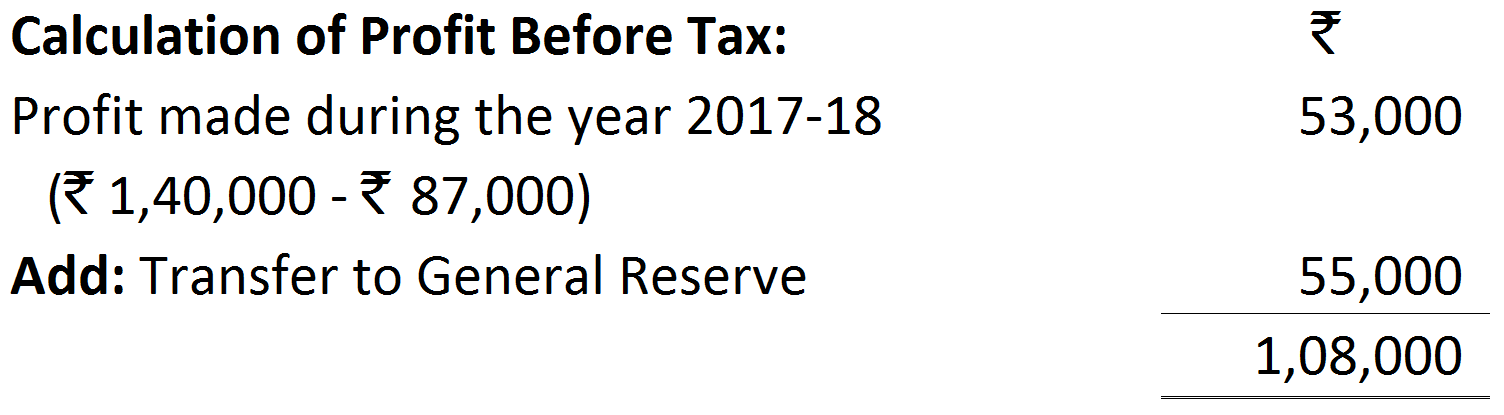

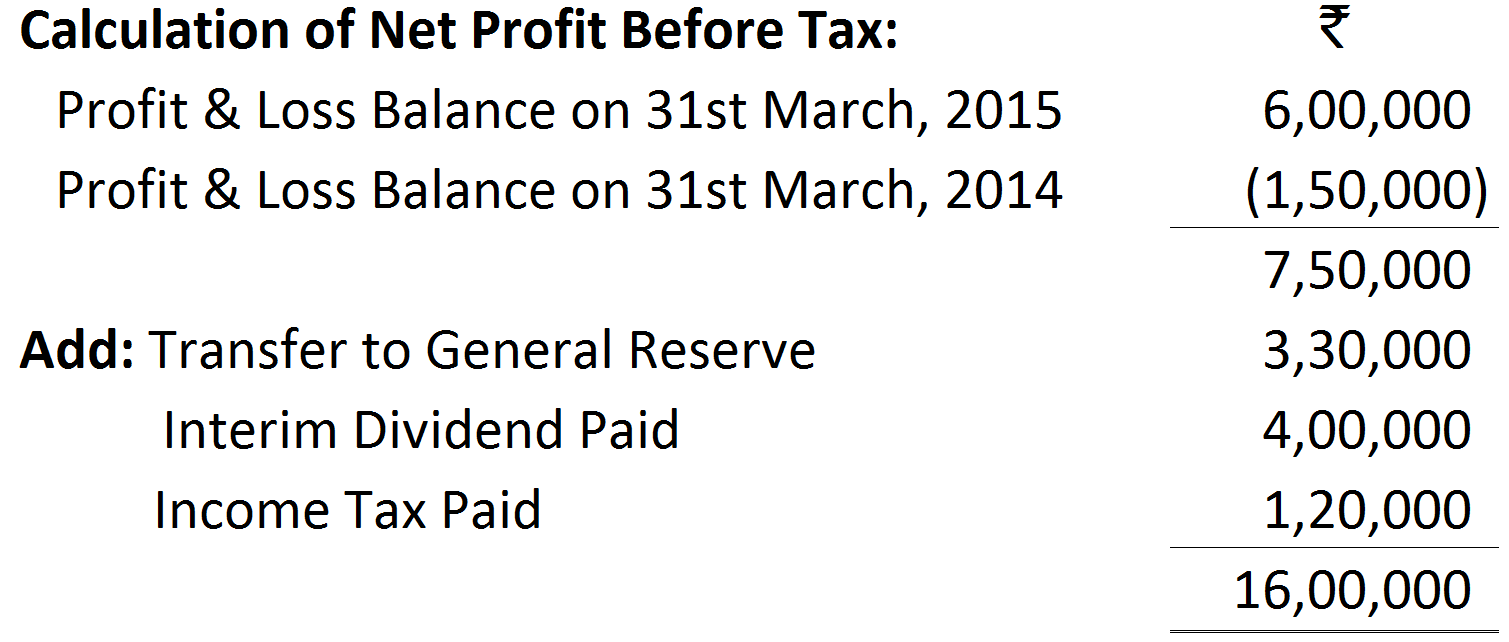

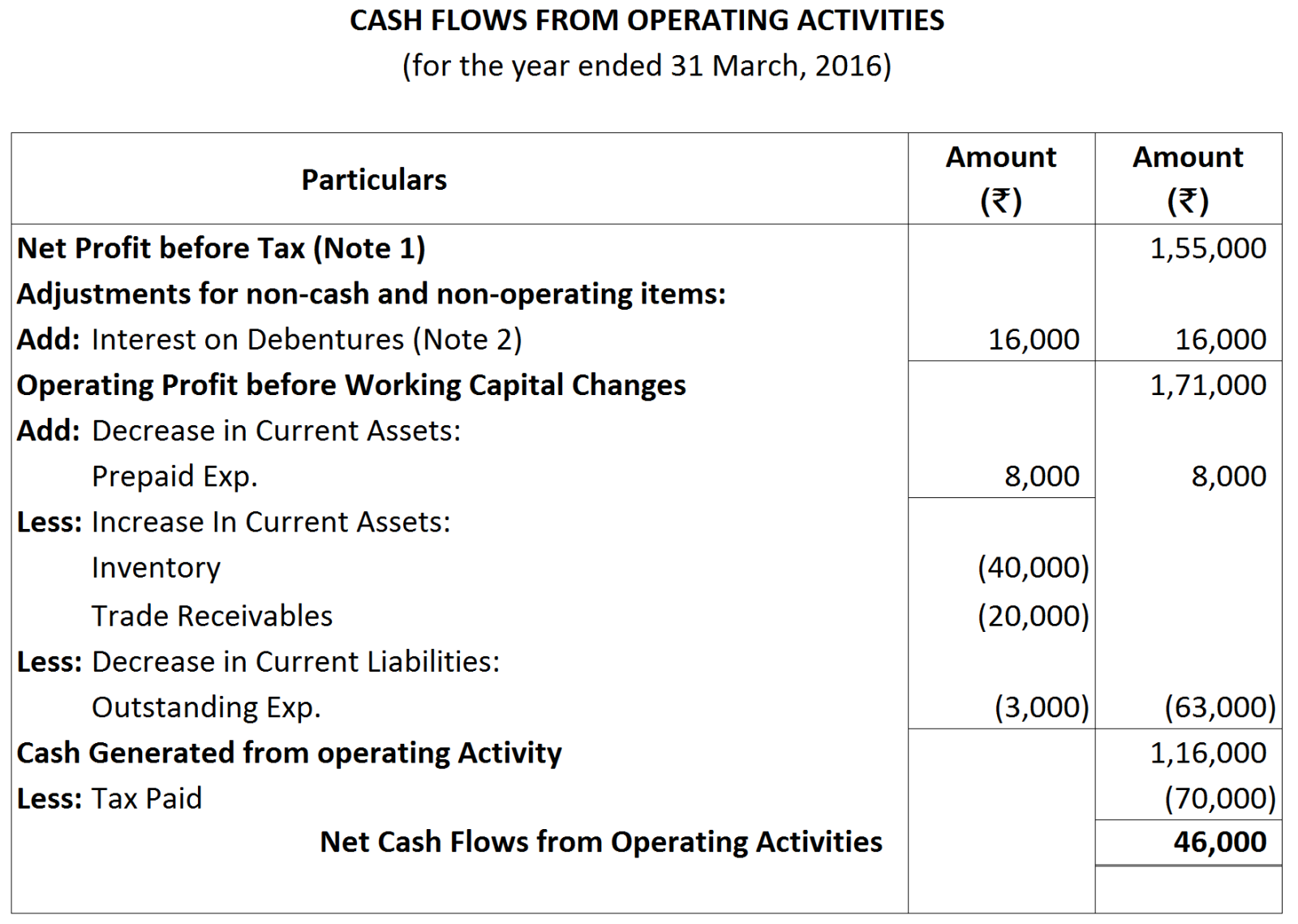

Calculation of Net Profit before Tax:

|

3,10,000

|

|

Add: Provision for Tax for the Current year

|

22,000

|

|

Net Profit made during the year

|

3,32,000

|

Working Note:

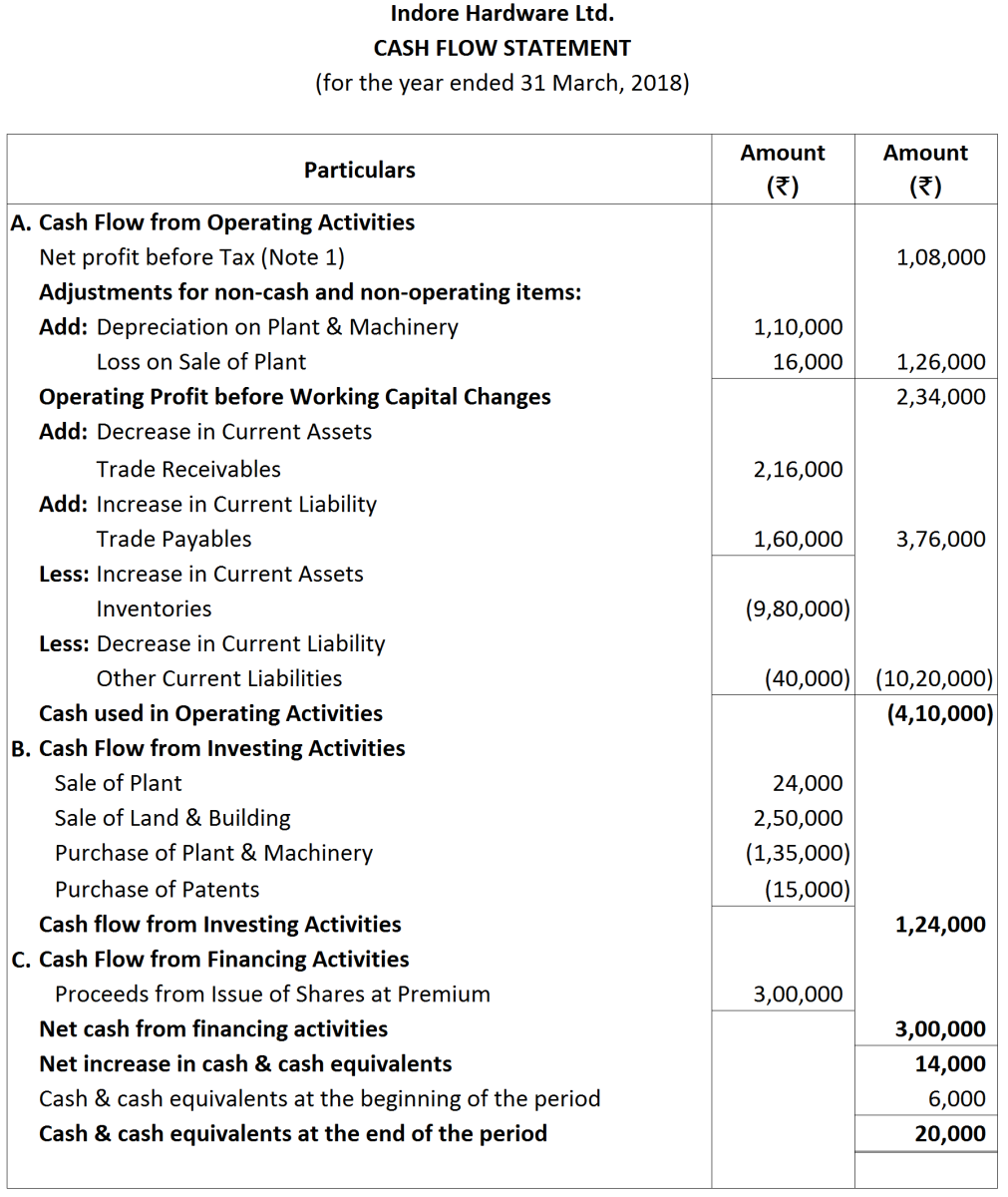

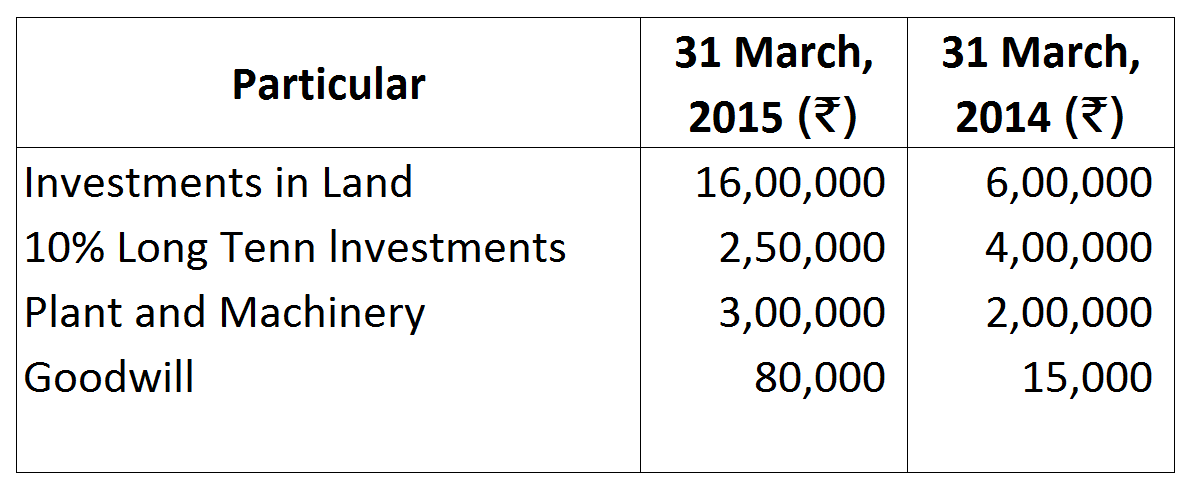

Working Note: * Cash Flow from Investing Activities ₹ 1,24,000 is the balancing figure of Cash flow statement.

* Cash Flow from Investing Activities ₹ 1,24,000 is the balancing figure of Cash flow statement.

Note:

Note:

|

|

₹

|

|

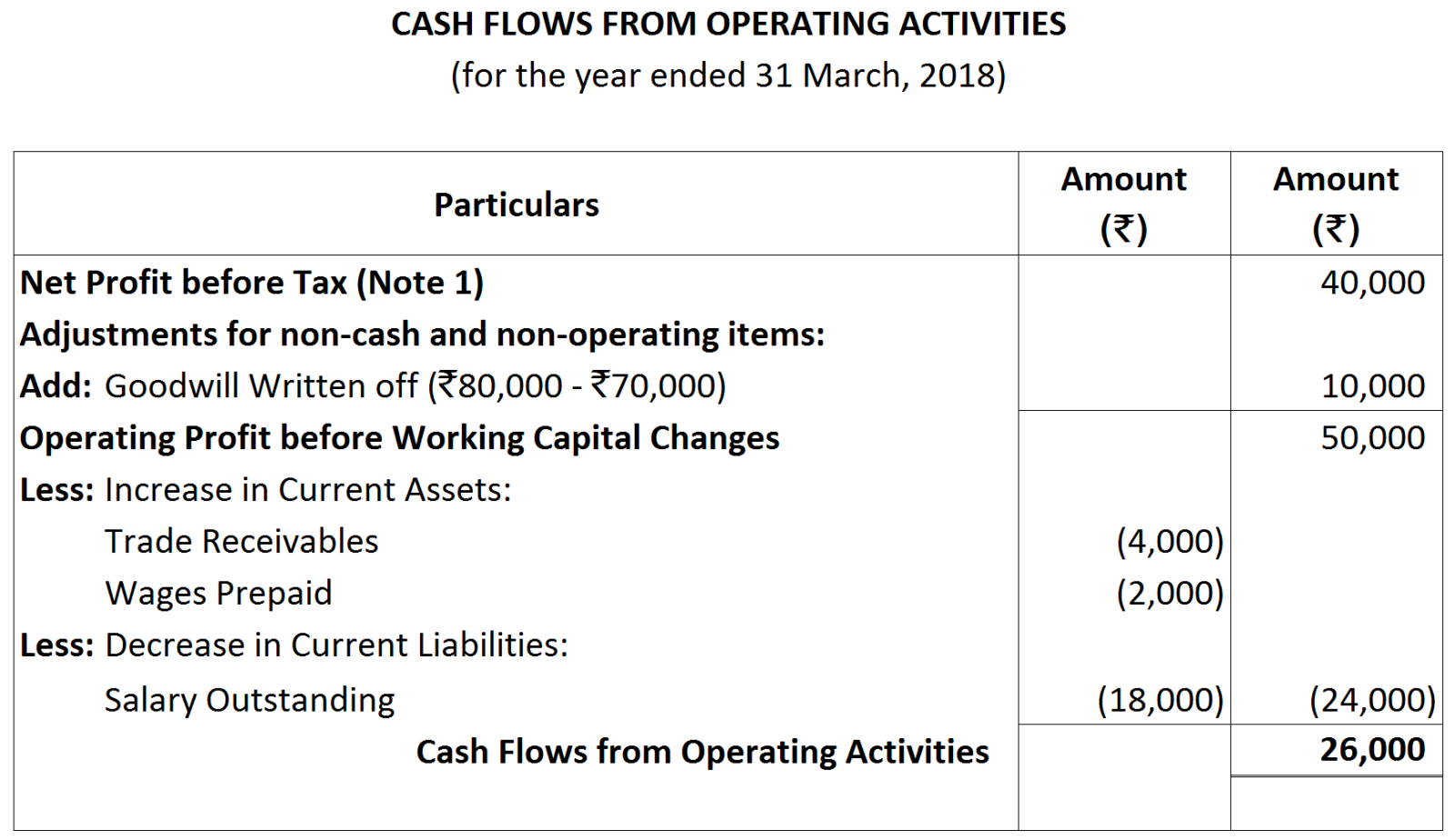

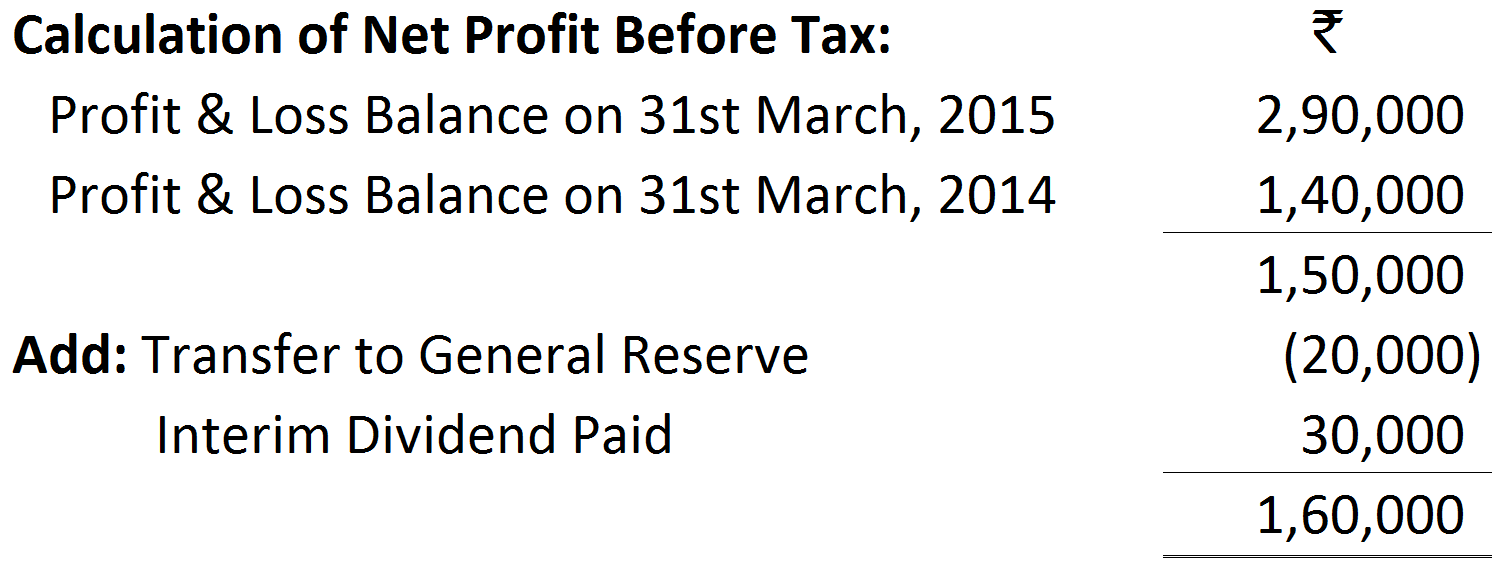

Profit & Loss Balance on 31st March, 2018

|

65,000

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(60,000)

|

|

|

5,000

|

|

Add: Transfer to General Reserve (₹ 2,37,000 - ₹ 2,02,000)

|

35,000

|

|

Net Profit before Tax

|

40,000

|

Note:

Note:

|

Calculation of Net Profit before Tax:

|

₹

|

|

Profit & .Loss Balance on 31st March, 2018

|

30,000

|

|

less: Profit & Loss Balance on 31st March, 2017

|

(20,000)

|

|

|

10,000

|

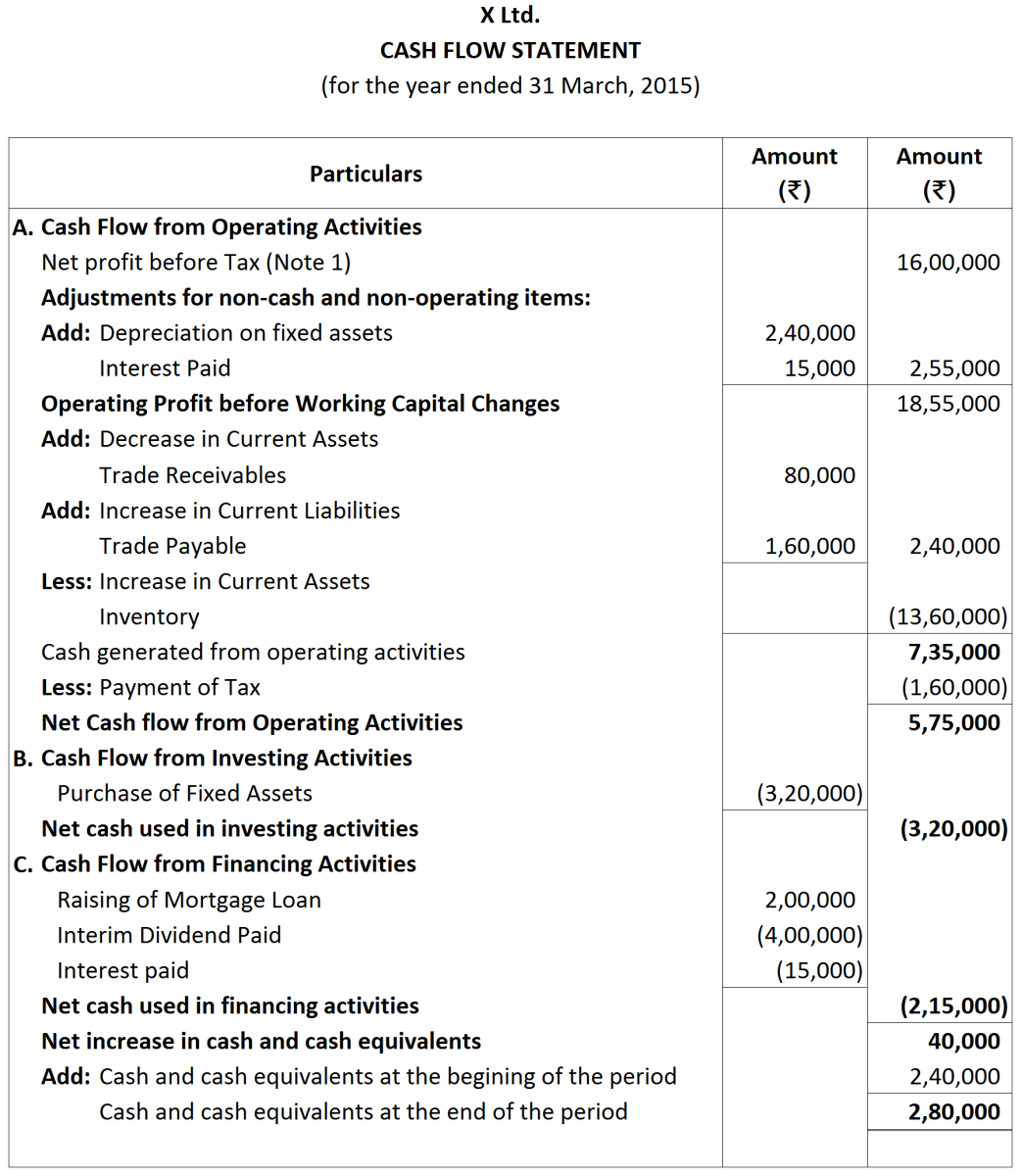

Net Profit before Tax ₹ 16,00,000; Cash Flow from Operating Activities ₹ 5,75,000; Cash using in Investing Activities ₹ 3,20,000; Cash used in Financing Activities ₹ 2,15,000.

Net Profit before Tax ₹ 16,00,000; Cash Flow from Operating Activities ₹ 5,75,000; Cash using in Investing Activities ₹ 3,20,000; Cash used in Financing Activities ₹ 2,15,000.

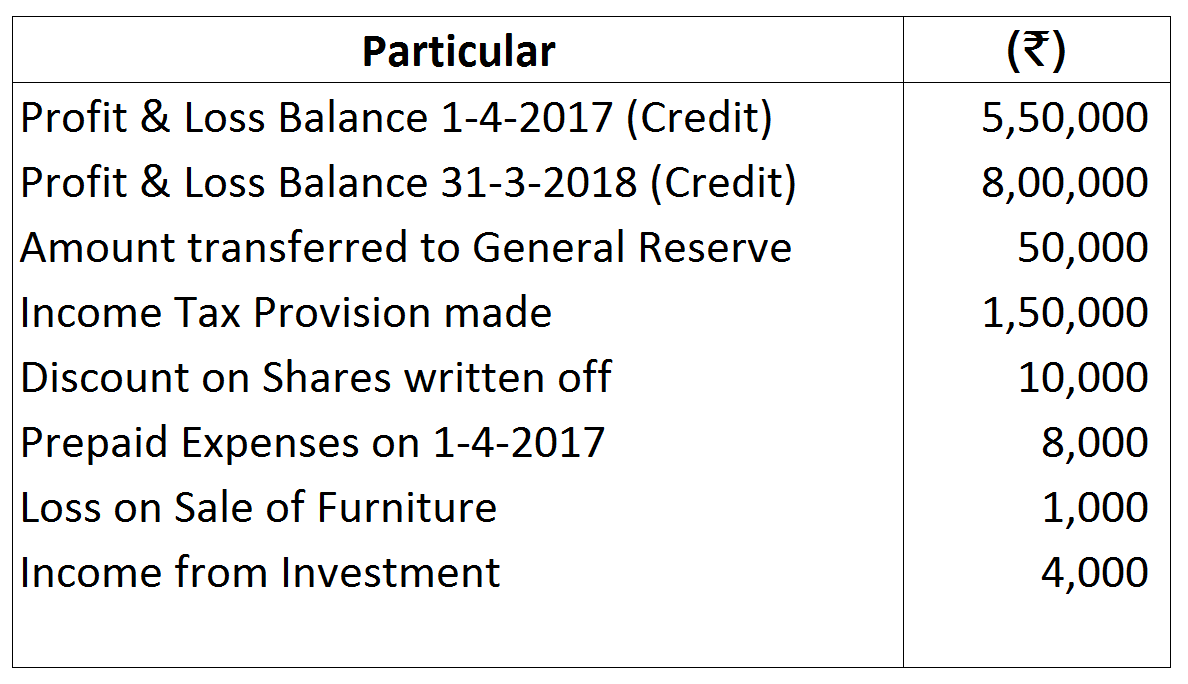

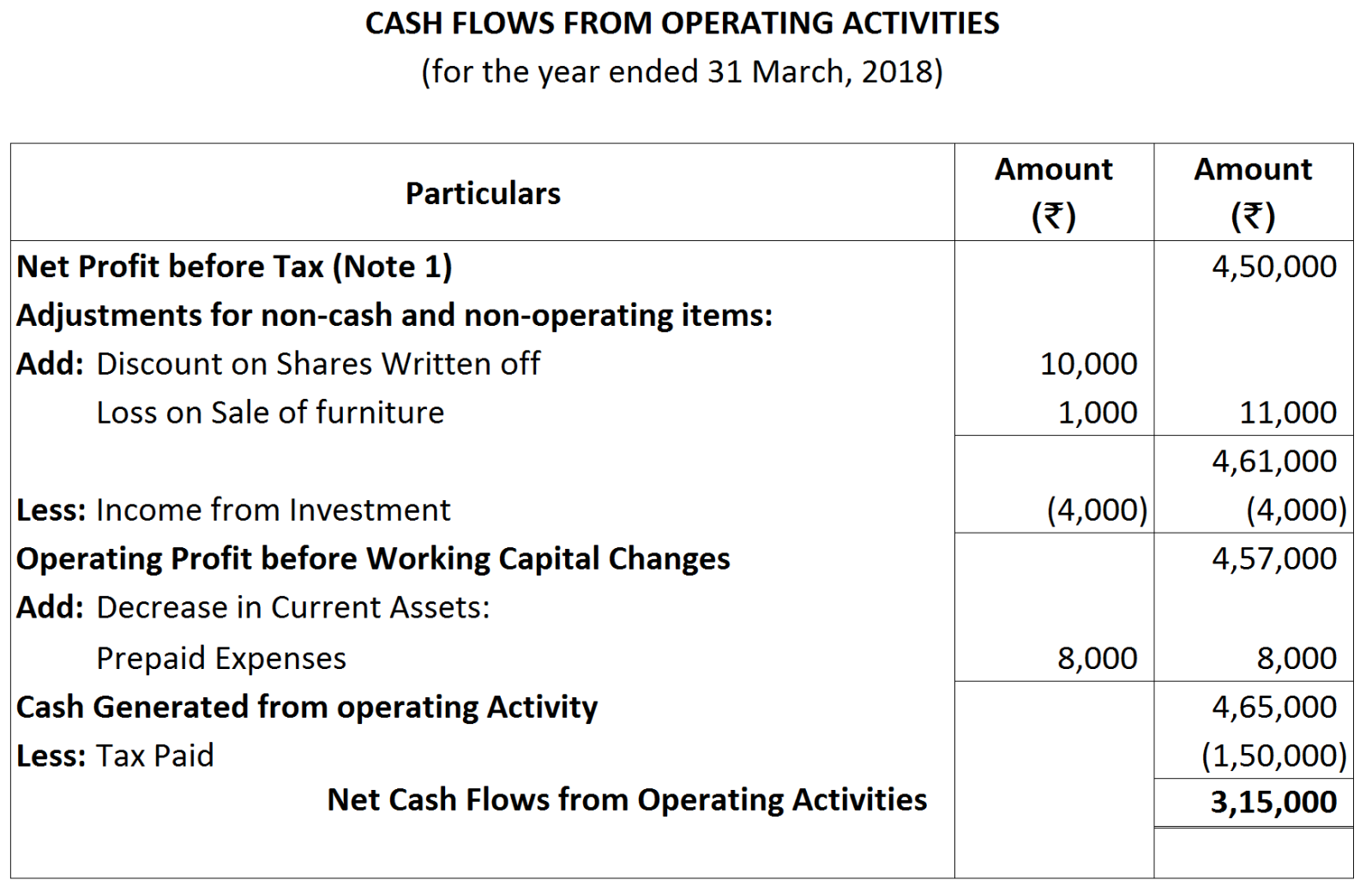

| ₹ | |

| Profit & Loss Balance on 31st March, 2018 | 8,00,000 |

| Less: Profit & Loss Balance on 1st April, 2017 | (5,50,000) |

| 2,50,000 | |

| Add: Transfer to General Reserve | 50,000 |

| Provision for Tax made during the Current year | 1,50,000 |

| Net Profit before Tax | 4,50,000 |

|

1.

|

Interest paid.

|

Financing Activities

|

|

2.

|

Interest paid on long-tenn loans by.

|

|

|

|

a. Finance Company.

|

Operating Activities

|

|

|

b. Non-finance Company.

|

Financing Activities

|

|

3.

|

Interest received.

|

Investing Activities

|

|

4.

|

Interest received on Investments by a bank.

|

Operating Activities

|

|

5.

|

Interest received on investments by a manufacturing company.

|

Investing Activities

|

|

6.

|

Dividend received.

|

Investing Activities

|

|

7.

|

Dividend received by a Mutual Fund Company.

|

Operating Activities

|

|

8.

|

Purchase oflnvestments.

|

Investing Activities

|

|

9.

|

Purchase of Investments by a finance company.

|

Operating Activities

|

|

10.

|

Purchase of Investments by a non-finance company.

|

Investing Activities

|

|

11.

|

Bank balance.

|

Cash Equivalents

|

|

12.

|

Short-term deposits in banks.

|

Cash Equivalents

|

|

13.

|

Bank Overdratl.

|

Financing Activities

|

|

14.

|

Marketable Securities.

|

Cash Equivalents

|

Note:

Note:

|

Calculation of Net Profit before Tax:

|

₹

|

|

Profit & .Loss Balance on 31st March, 2018

|

3,00,000

|

|

less: Profit & Loss Balance on 31st March, 2017

|

(5,00,000)

|

| 2,00,000 | |

|

Add: Transfer to Debenture Sinking Fund (₹ 1,25,000 - ₹ 1,00,000)

|

25,000

|

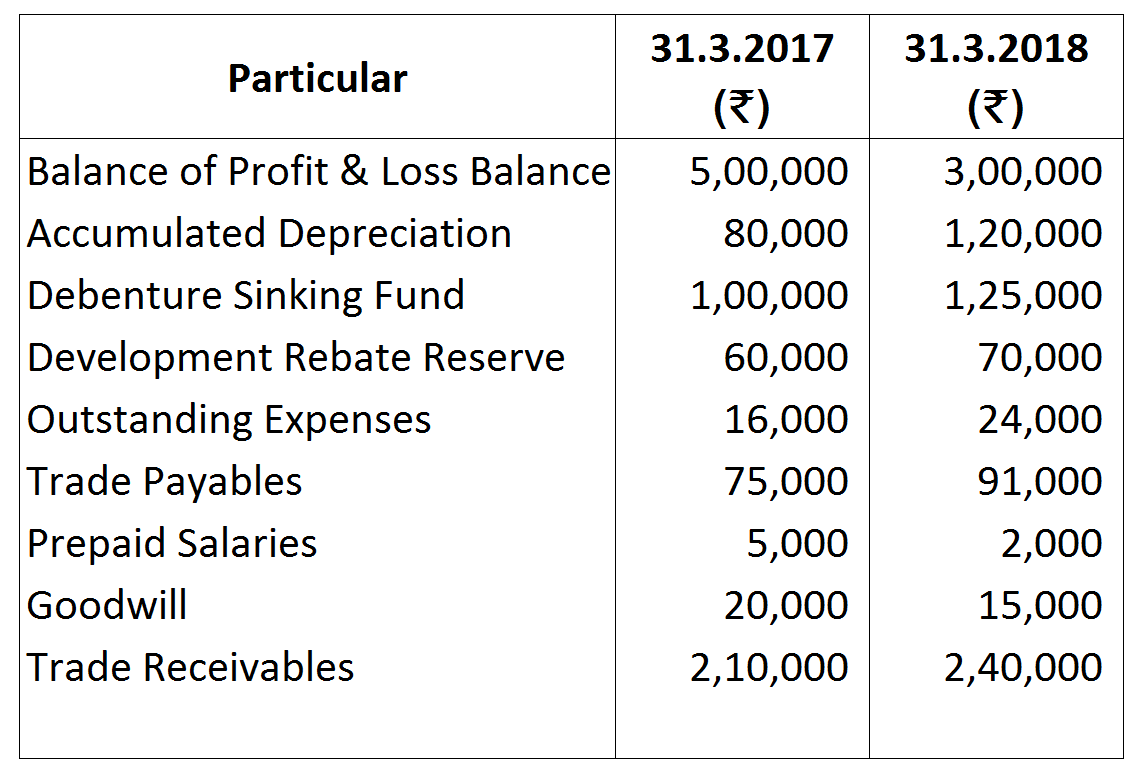

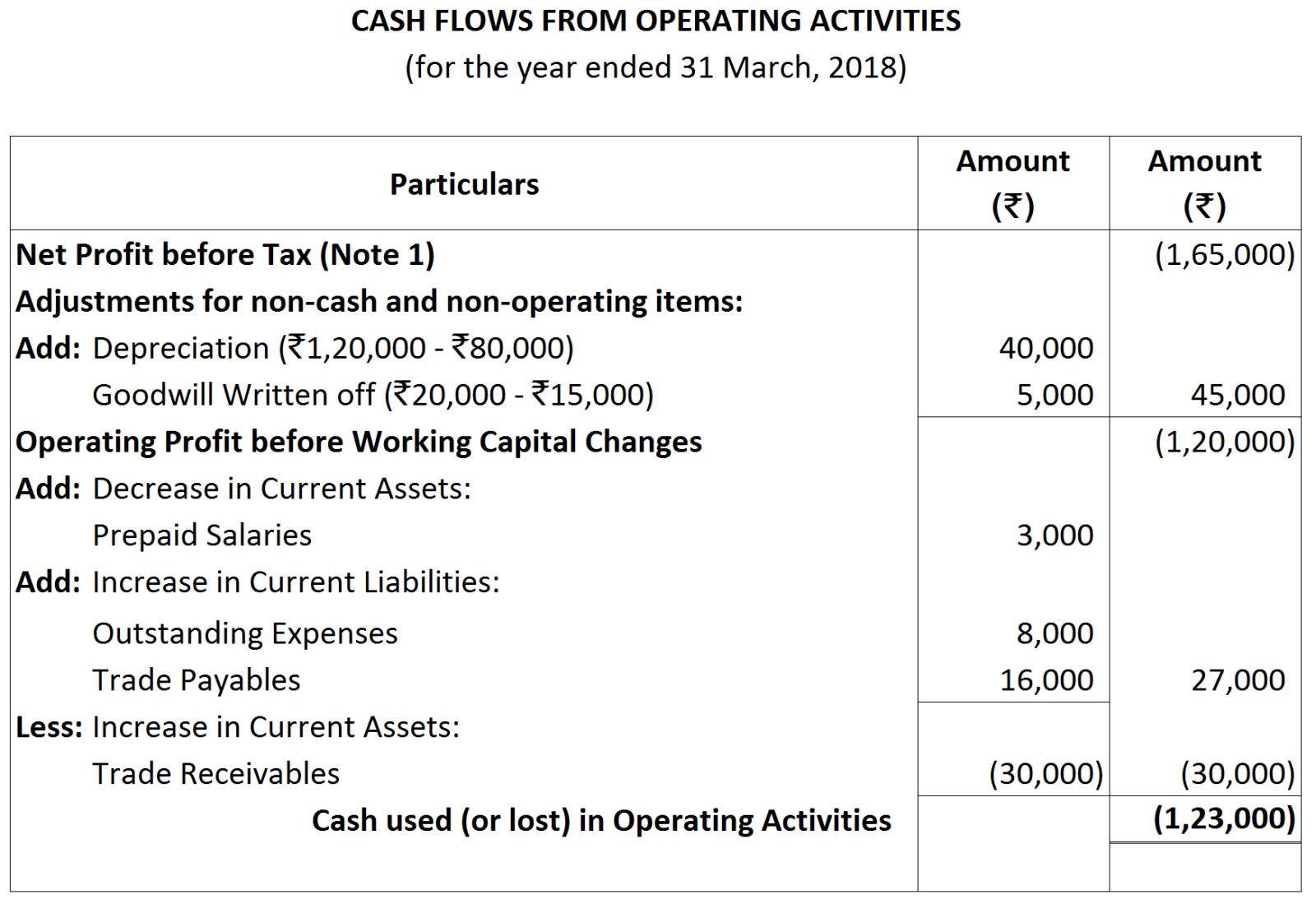

| Transfer to Development Rebate Reserve (₹ 70,000 - ₹ 60,000) | 10,000 |

| Net Profit before Tax | (1,65,000) |

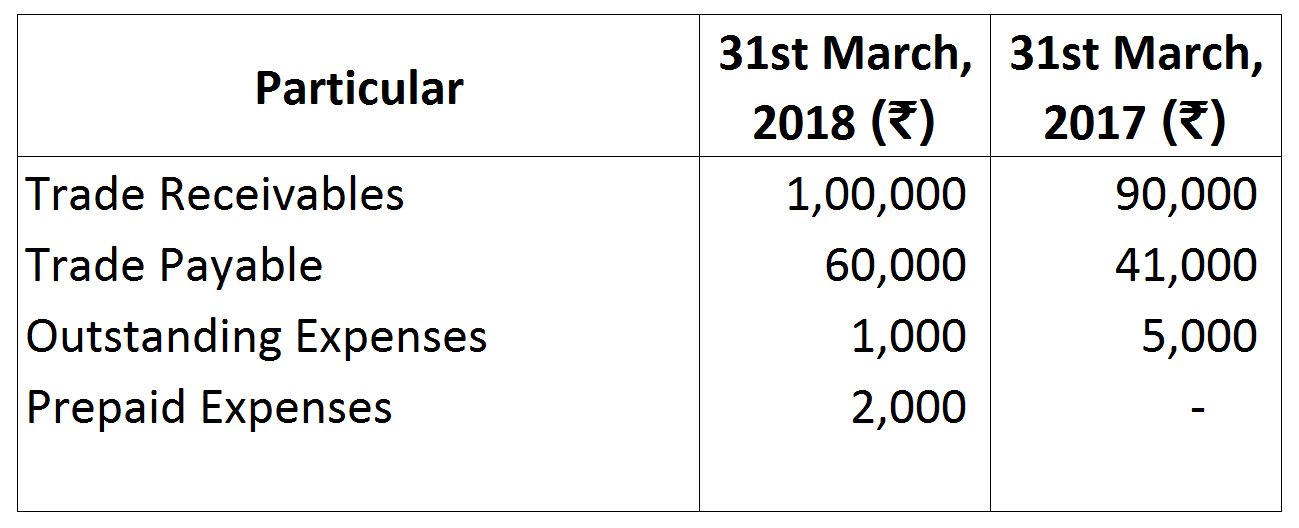

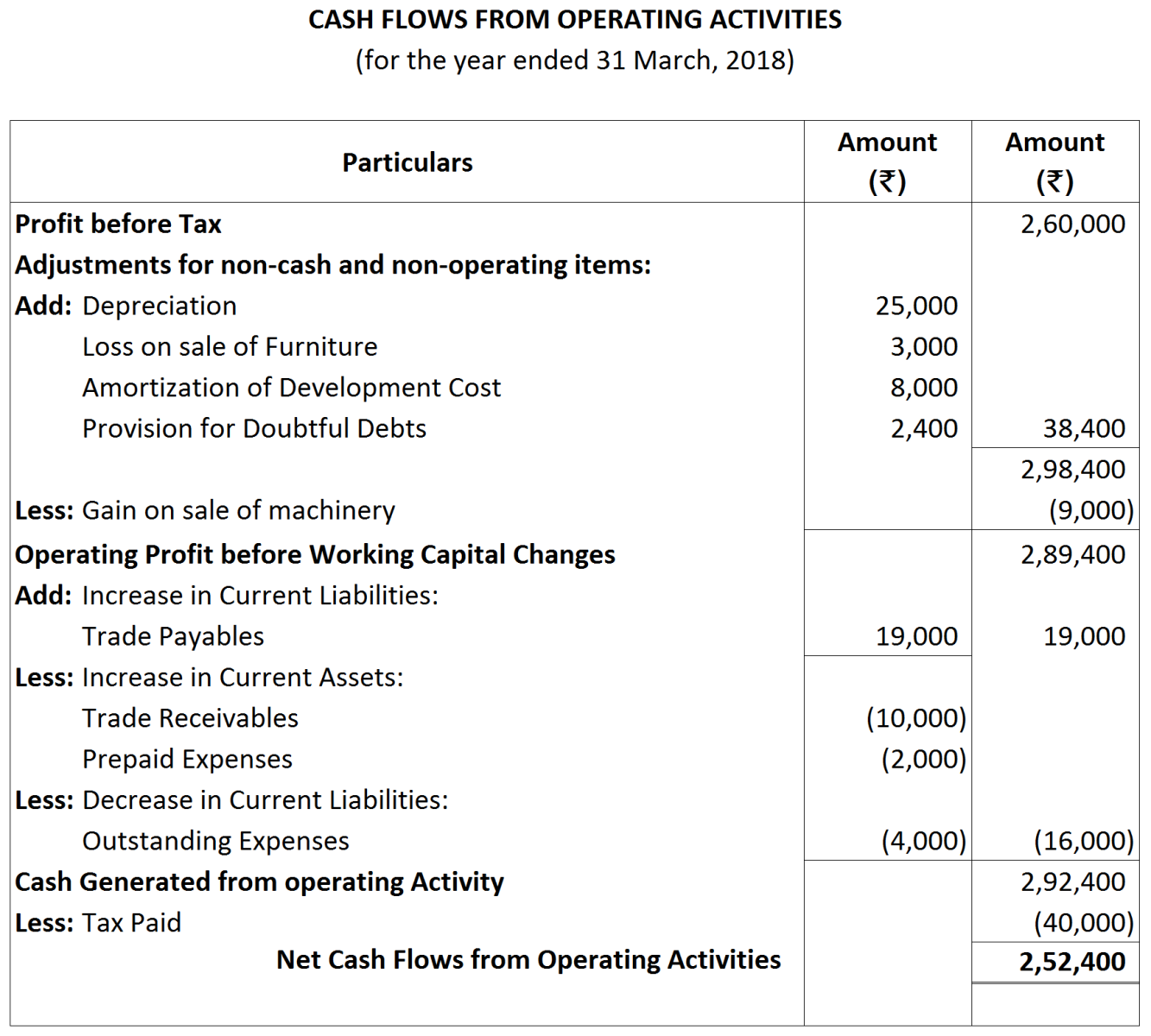

| ₹ | ||

| 1. | Depreciation on Fixed Assets | 25,000 |

| 2. | Loss on Sale of Furniture | 3,000 |

| 3. | Amortization of Development Cost | 8,000 |

| 4. | Provision for Doubtful Debts | 2,400 |

| 5. | Provision for Taxation | 40,000 |

| 6. | Transfer to General Reserve | 20,000 |

| 7. | Gain on Sale of Machinery | 9,000 |

Note:

Note:

|

|

₹

|

|

Profit for the year

|

2,00,000

|

|

Add: Provision for Tax

|

40,000

|

|

Transfer to General Reserve

|

20,000

|

|

Profit before Tax

|

2,60,000

|

Note:

Note:

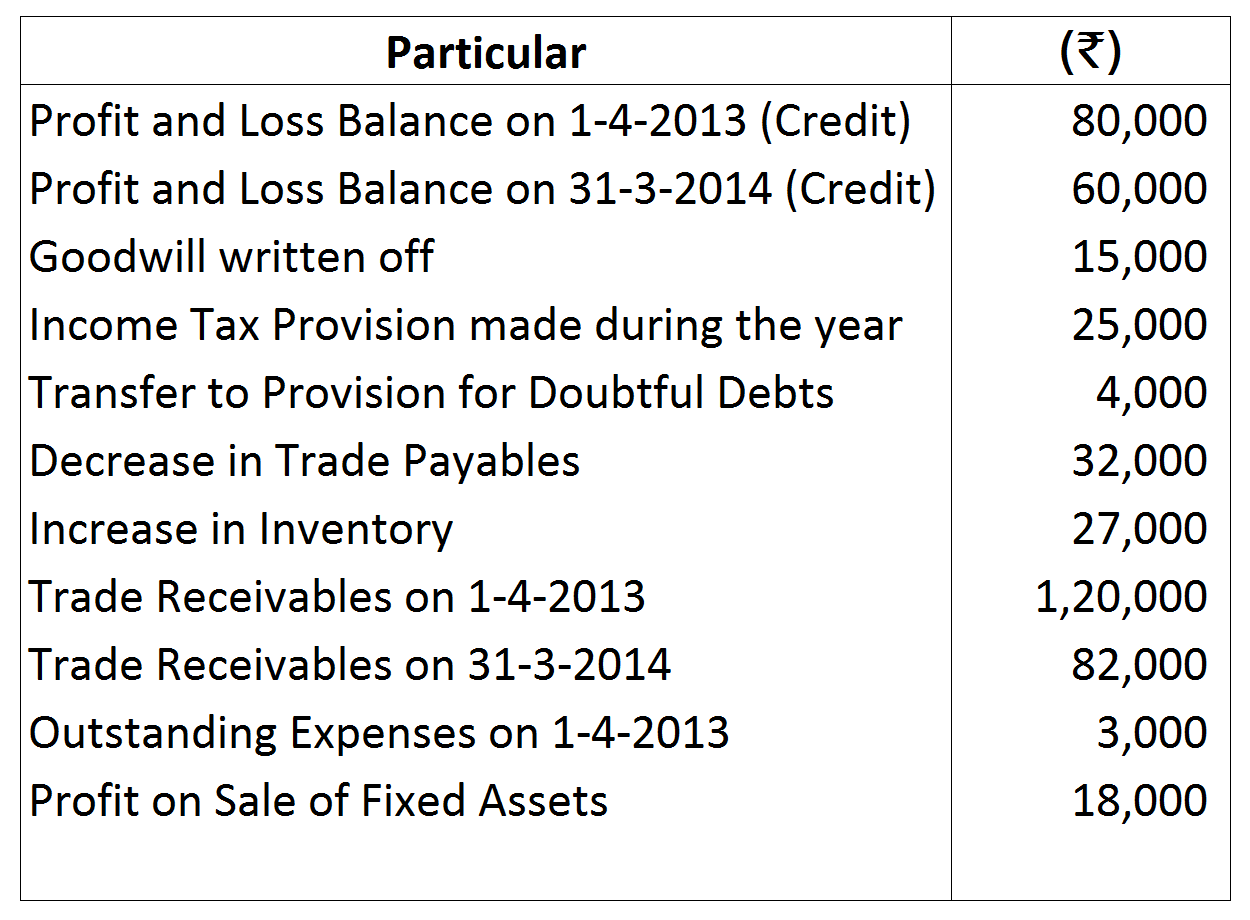

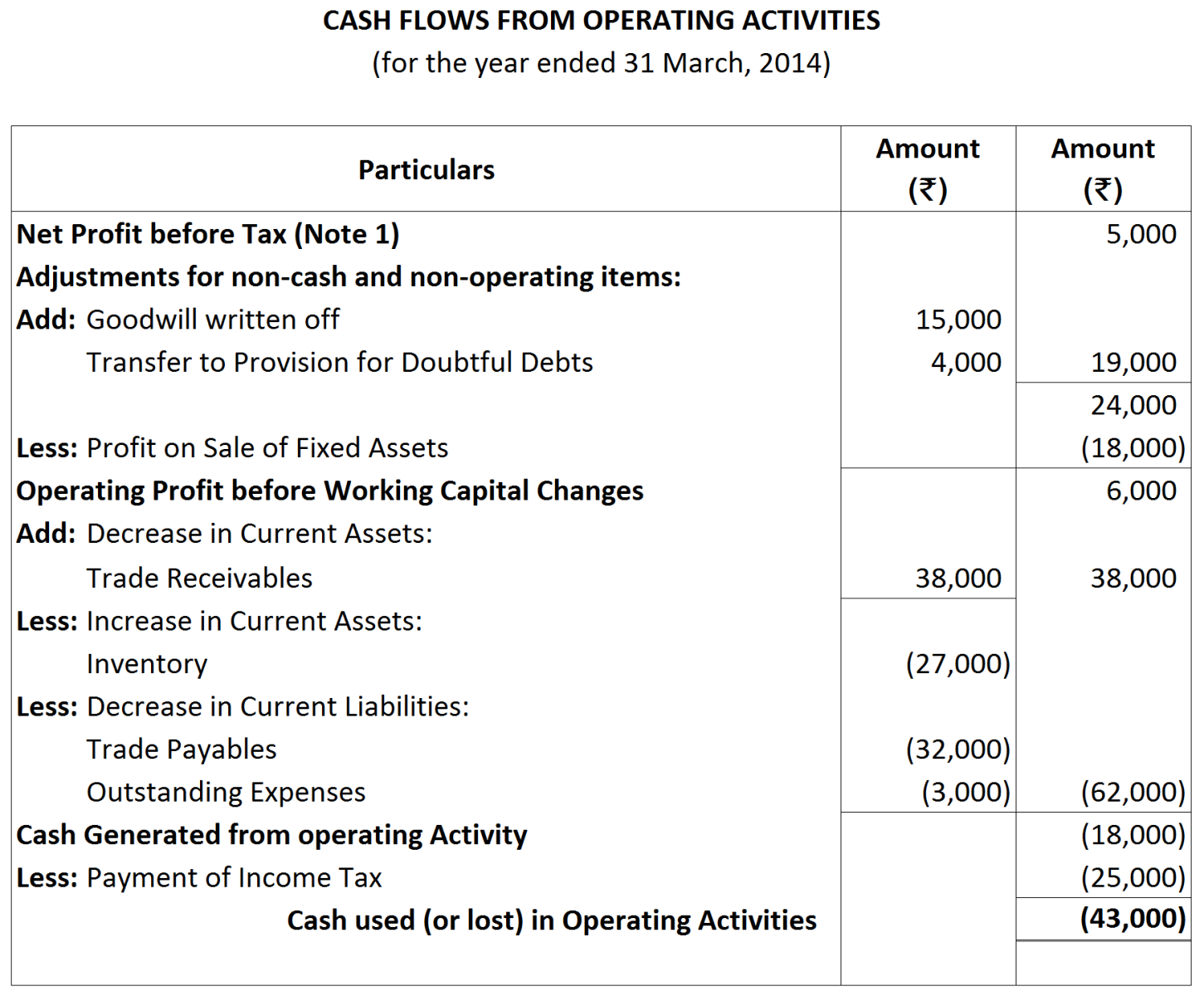

| Calculation of Net Profit before Tax: | ₹ |

| Profit & Loss Balance on 31st March, 2014 | 60,000 |

| Less: Profit & Loss Balance on 31st March, 2013 | (80,000) |

| 20,000 | |

| Add: Provision for Tax made during the Current year | 25,000 |

| 5,000 |

Working Notes:

Working Notes:

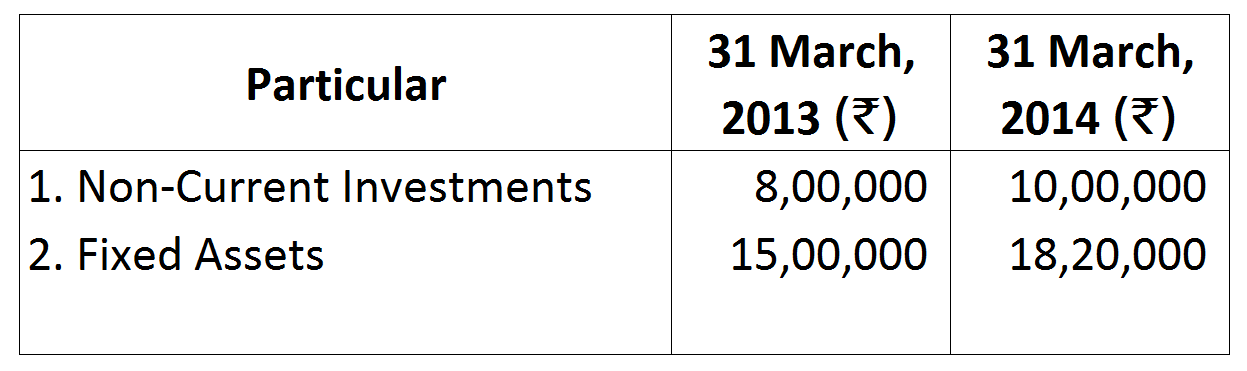

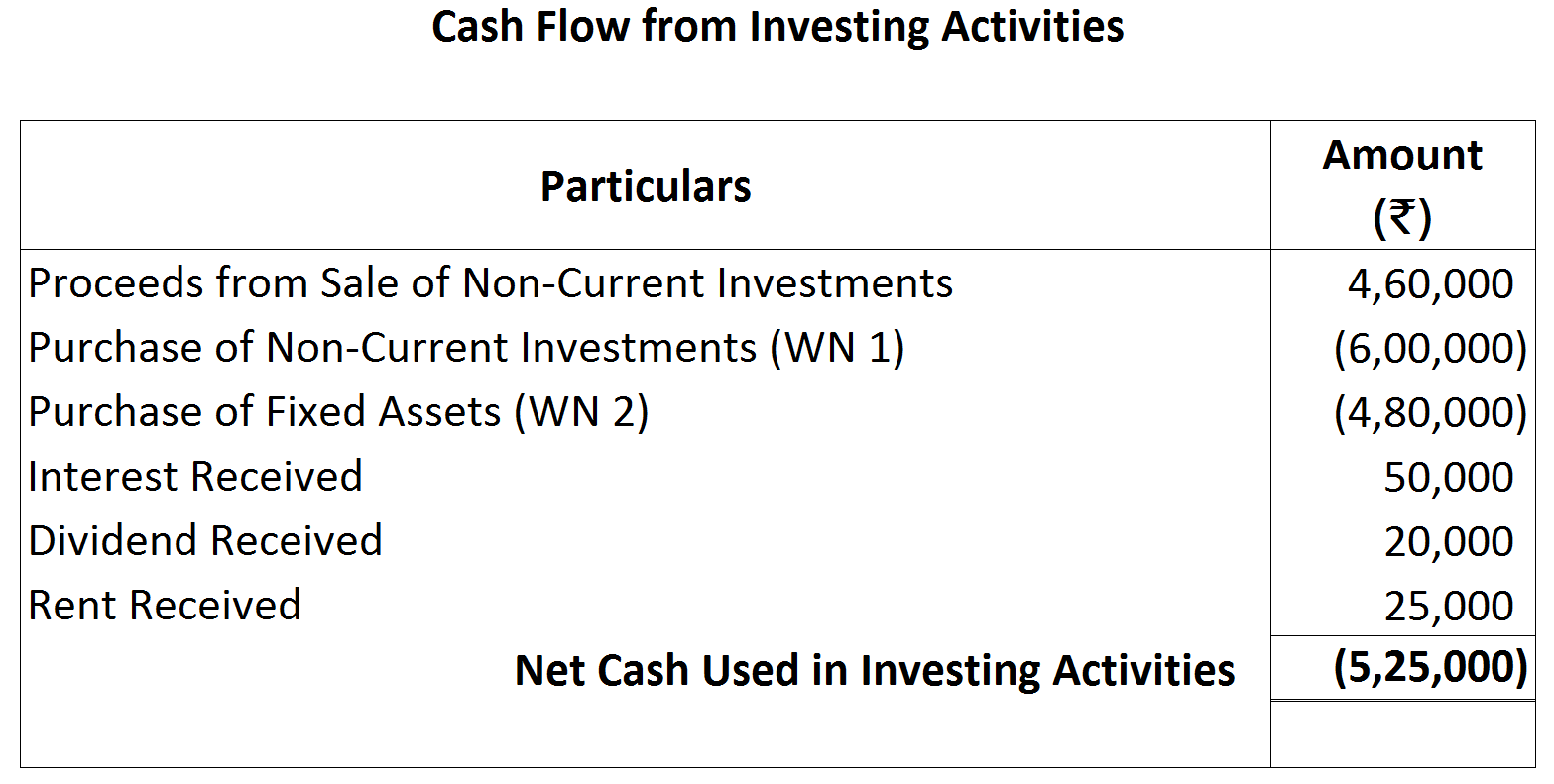

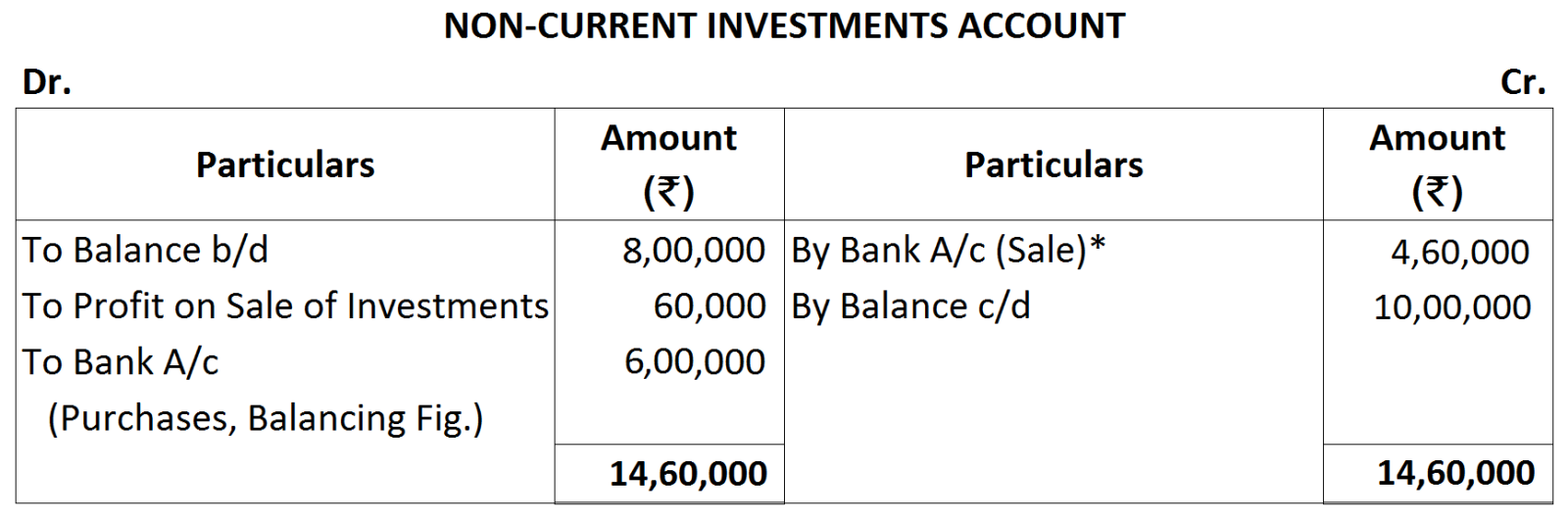

| Sale of Non-Current Investments | = | ₹ 4,00,000 |

| 1/2 of ₹ 8,00,000 | = | ₹ 60,000 |

| Profit 15% of ₹ 4,00,000 | ₹ 4,60,000 | |

| Sale Proceeds |

| 1. | Purchase of Shares of a Company. | Operating Activities |

| 2. | Proceeds from sale of Shares. | Operating Activities |

| 3. | Brokerage paid on purchase of Shares. | Operating Activities |

| 4. | Loans and Advances made to third parties | Operating Activities |

| 5. | Dividend and interest received on Securities. | Operating Activities |

| 6. | Salary paid to employees. | Operating Activities |

| 7. | Interest paid on debentures. | Operating Activities |

| 8. | Dividend paid to Shareholders | Financing Activities |

| 1. | Purchase of Shares of a Company. | Investing Activities |

| 2. | Proceeds from sale of Shares. | Investing Activities |

| 3. | Brokerage paid on purchase of Shares. | Investing Activities |

| 4. | Loans and Advances made to third parties | Investing Activities |

| 5. | Dividend and interest received on Securities. | Investing Activities |

| 6. | Salary paid to employees. | Operating Activities |

| 7. | Interest paid on debentures. | Financing Activities |

| 8. | Dividend paid to Shareholders | Financing Activities |

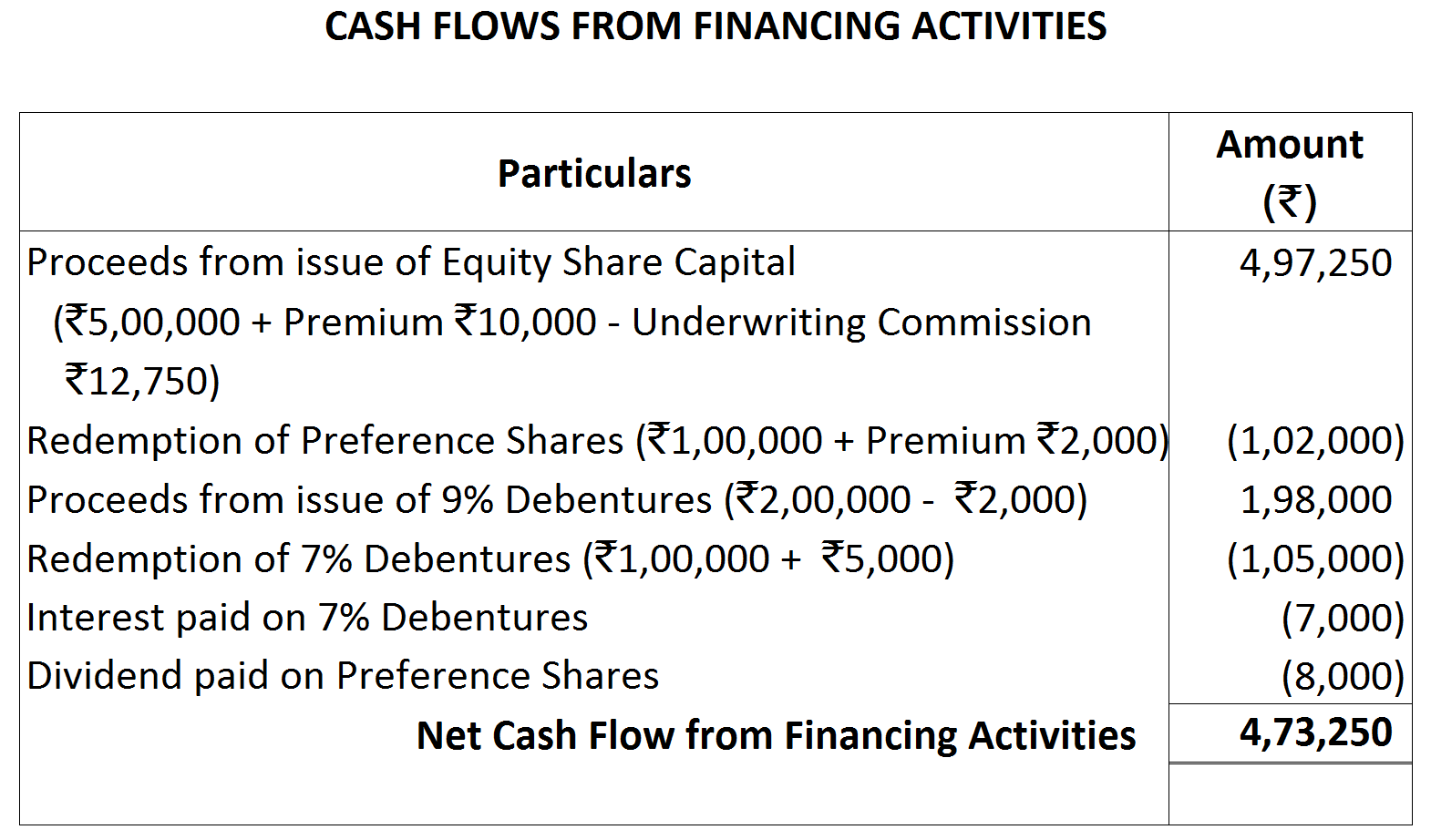

Note: Underwriting commission will be 2.5% on (5,00,000 + 10,000).

Note: Underwriting commission will be 2.5% on (5,00,000 + 10,000).

| 1. |

Calculation of Net Profit before Tax:

|

₹

|

|

|

Balance of Reserve & Surplus on 31st March, 2018

|

2,00,000

|

|

|

(-) Balance of Reserve & Surplus on 31st March, 2017

|

1,20,000

|

|

|

|

80,000

|

|

|

Add: Provision for Tax

|

75,000

|

|

|

|

1,55,000

|

|

2.

|

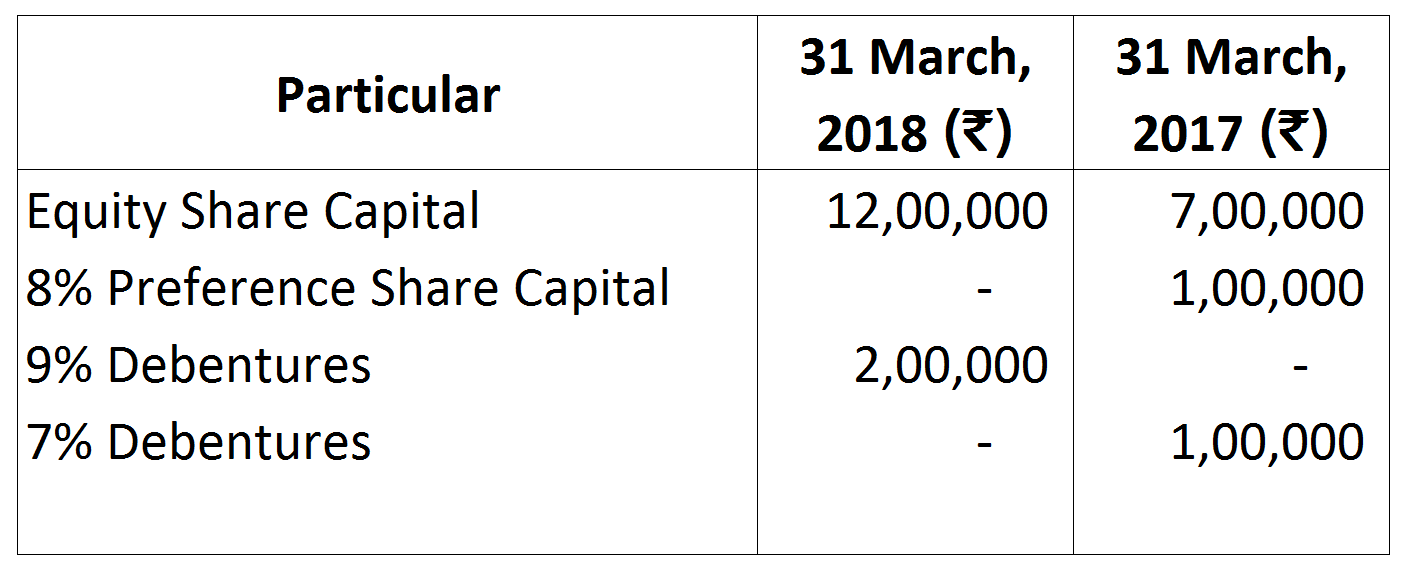

It has been assumed that new debentures have been issued on 31.3.2018. As such interest on Debentures = 8% on ₹ 2,00,000 = ₹ 16,000.

|

|

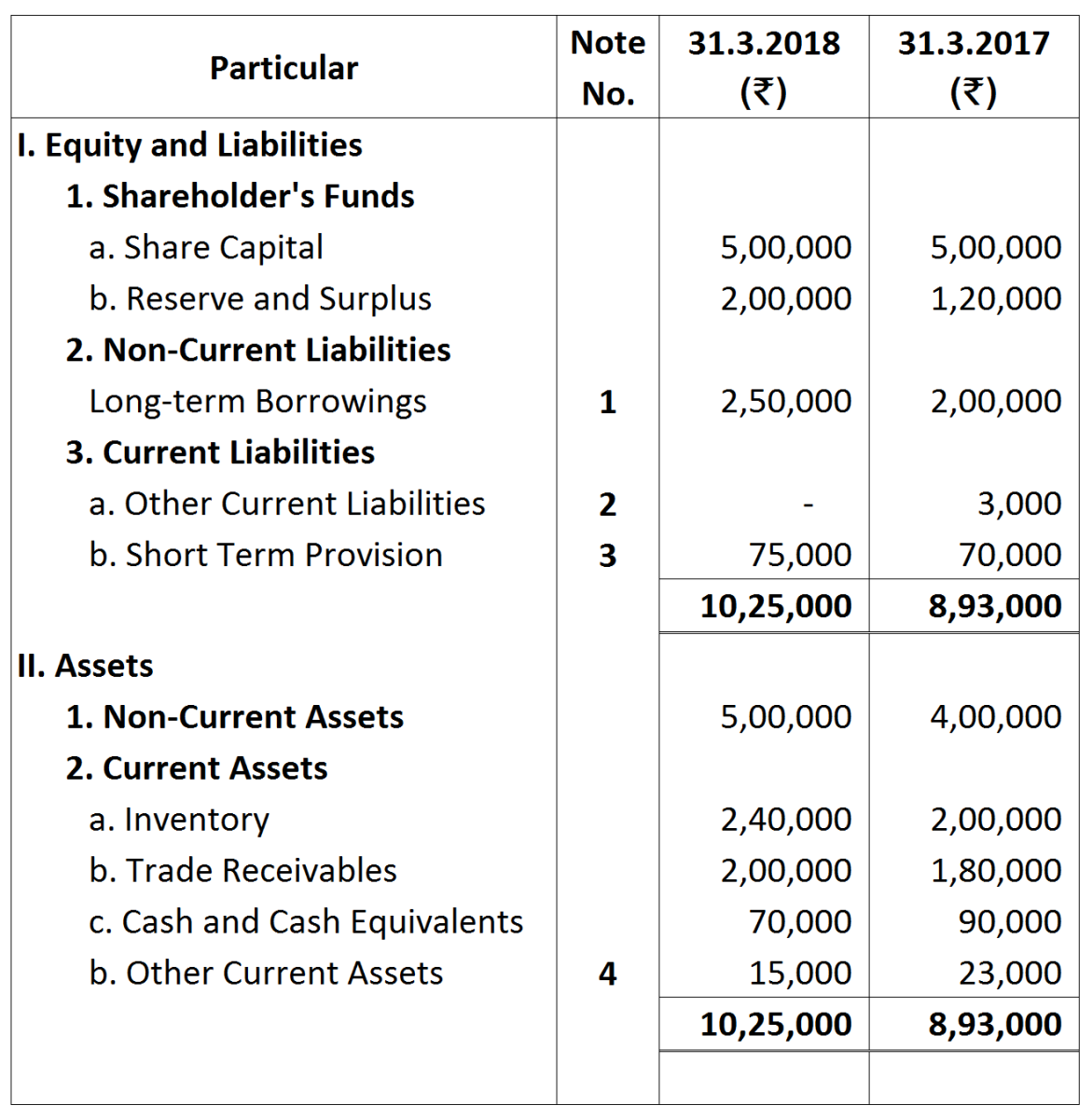

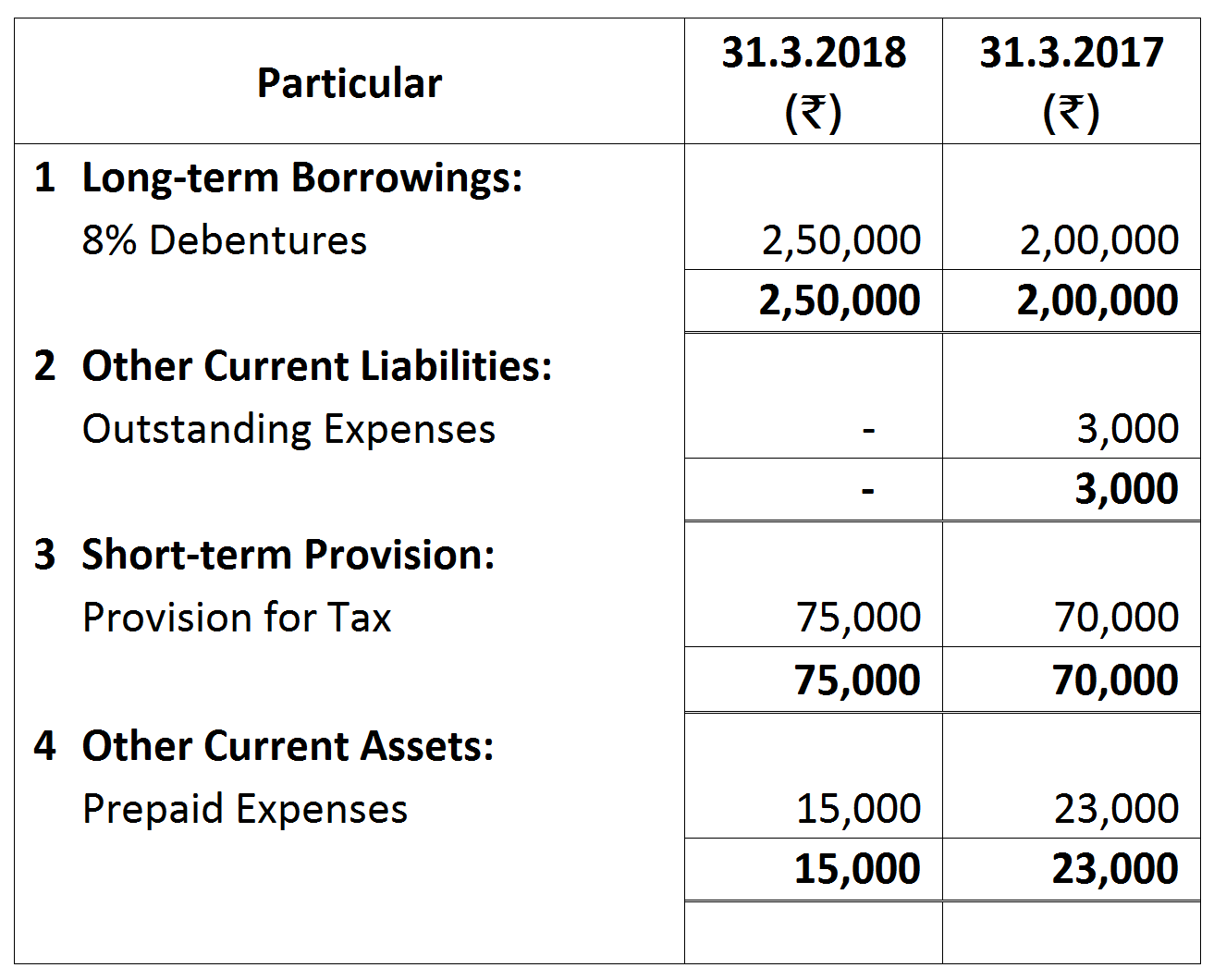

|

Outstanding Wages

|

40,000

|

|

Outstanding Salaries

|

30,000

|

|

Prepaid Insurance

|

3,000

|

Note: Since profit made during 2017 is clearly stated in the question, this is the profit before any appropriations such as transfer to General Reserve. Hence, there will be no entry for transfer to General Reserve.

Note: Since profit made during 2017 is clearly stated in the question, this is the profit before any appropriations such as transfer to General Reserve. Hence, there will be no entry for transfer to General Reserve.

Note:

Note:

|

Profit & Loss Balance on 31st March, 2018

|

60,000

|

|

Profit & Loss Balance on 31st March, 2017

|

75,000

|

|

Net Profit before Tax

|

(15,000)

|

Note:

Note:

|

Calculation of Net Profit before Tax

|

₹

|

|

Profit & Loss Balance on 31st March, 2018

|

60,000

|

|

Less: Profit & Loss Balance on 1st April, 2017

|

(12,000)

|

|

|

72,000

|

|

Add: Transfer to General Reserve

|

40,000

|

|

|

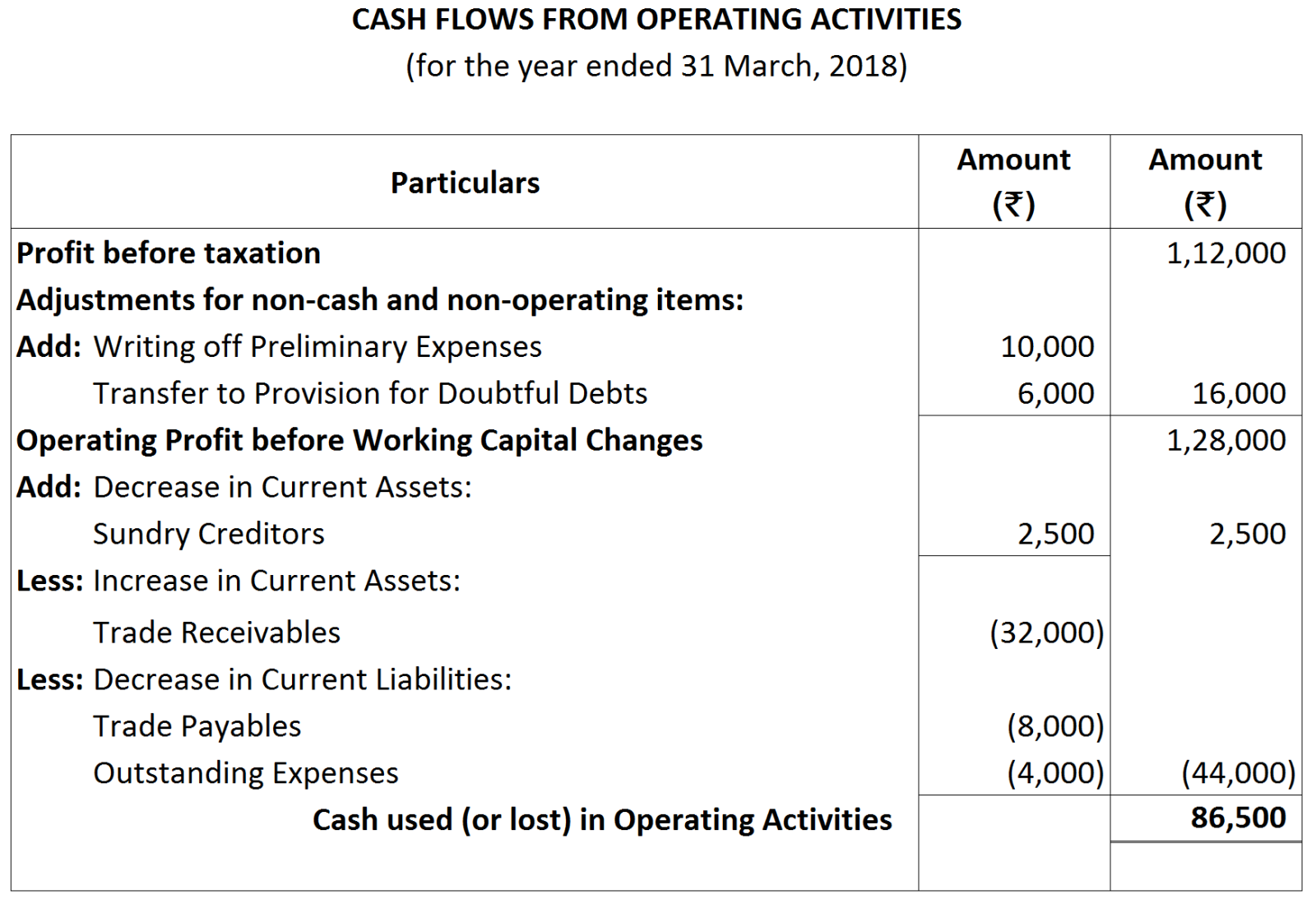

1,12,000

|

Working Notes:

Working Notes:

Ascertain the net cash (cash flow) from operating activities.

Ascertain the net cash (cash flow) from operating activities. Hints:

Hints:

Net Profit before Tax ₹ 1,60,000; Cash Flow from Operating Activities ₹ 1,50,000; Cash using in Investing Activities ₹ 2,70,000; and Cash flows from Financing Activities ₹ 1,30,000.

Net Profit before Tax ₹ 1,60,000; Cash Flow from Operating Activities ₹ 1,50,000; Cash using in Investing Activities ₹ 2,70,000; and Cash flows from Financing Activities ₹ 1,30,000.

Notes:

Notes:

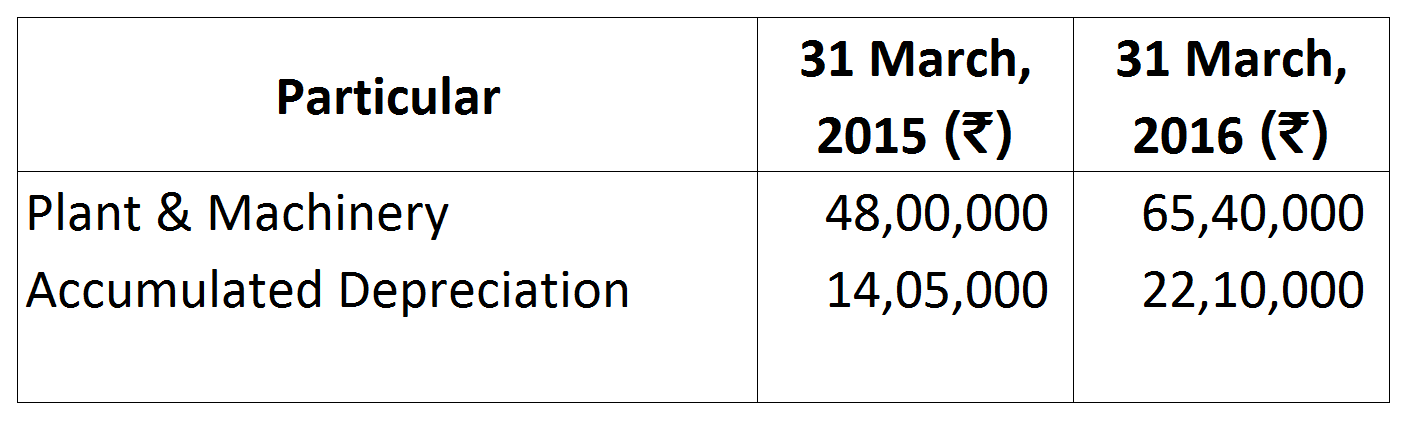

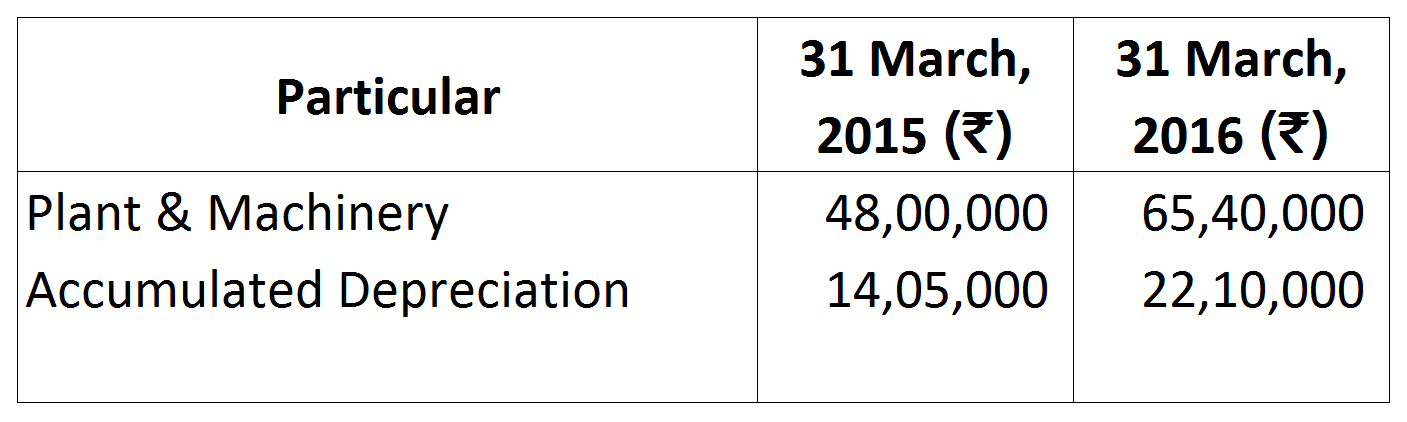

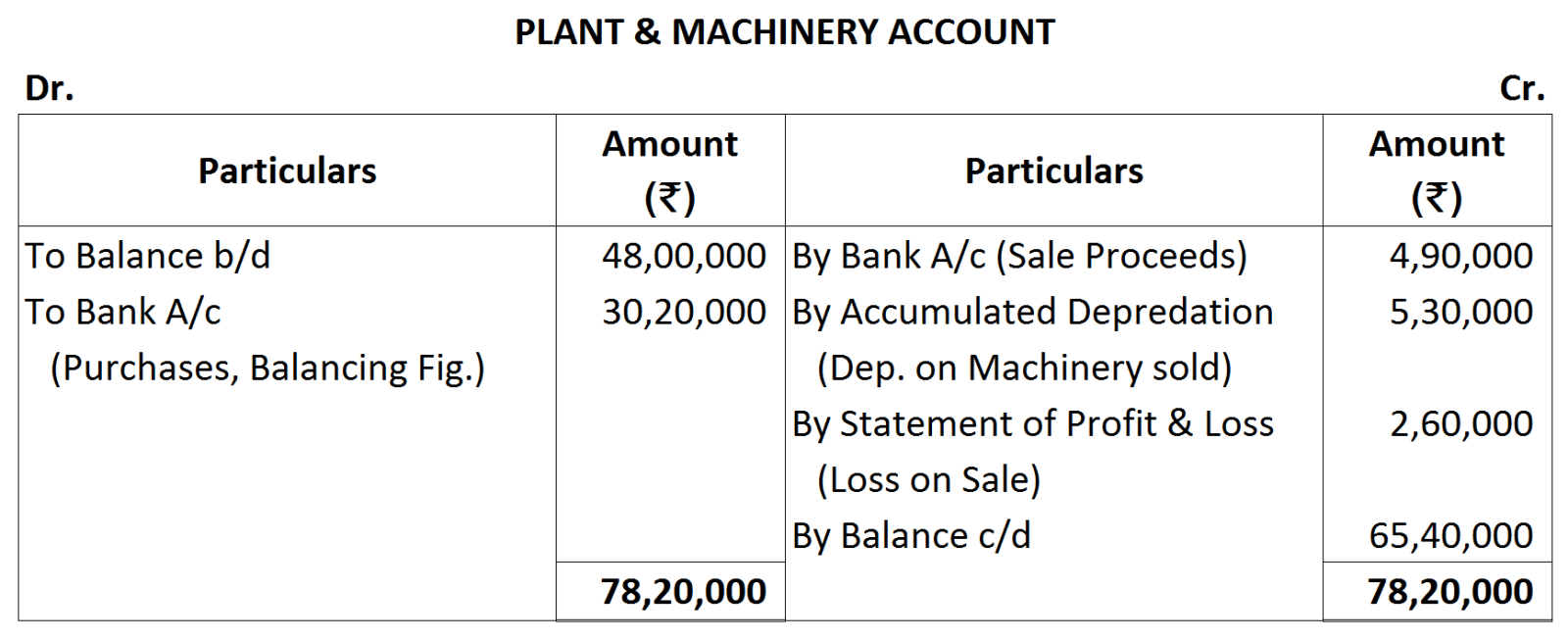

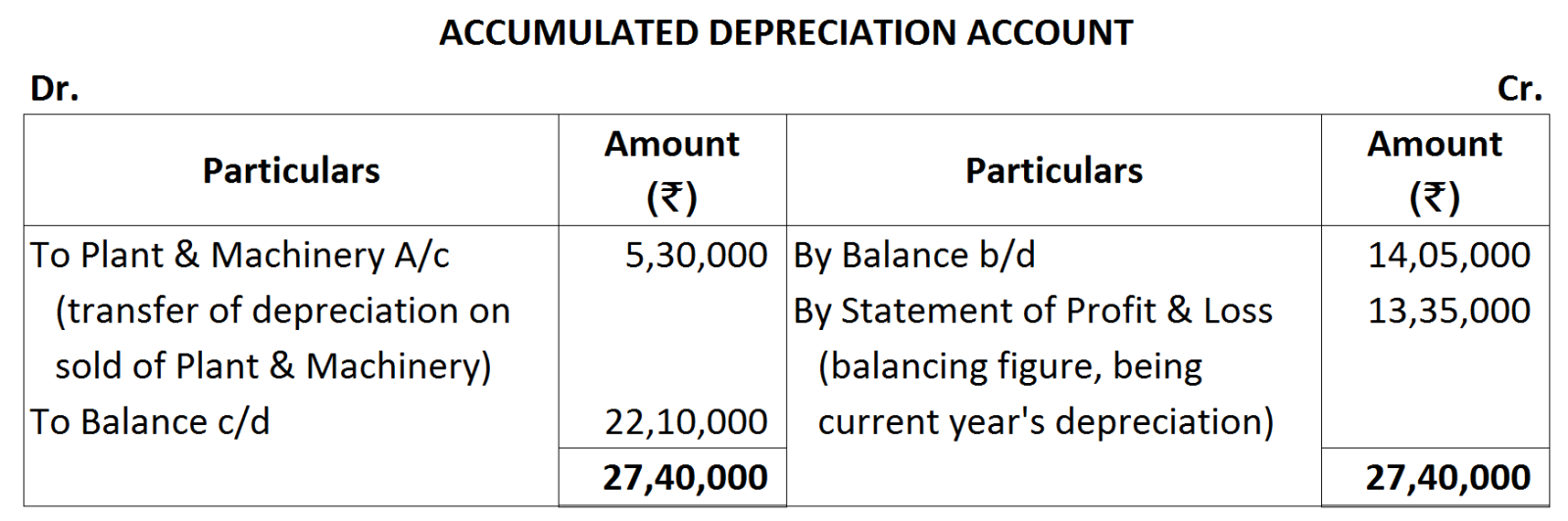

|

|

|

₹

|

|

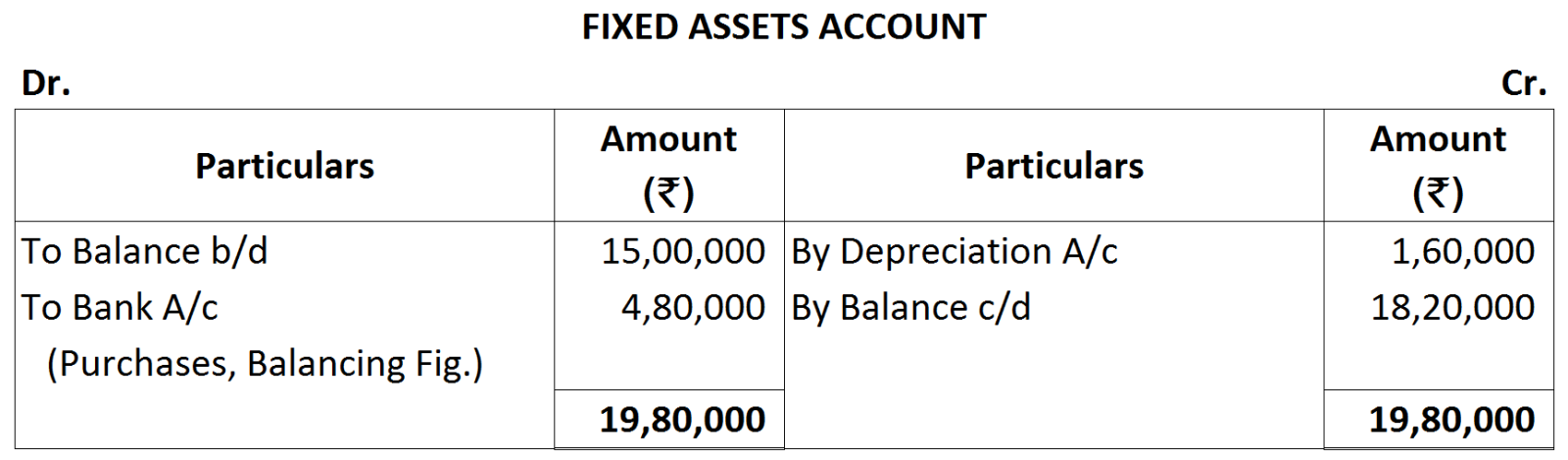

Cost of Plant and Machinery sold

|

=

|

12,80,000

|

|

Less: Accumulated Depreciation thereon

|

=

|

(5,30,000)

|

|

Written down value of Machinery sold

|

=

|

7,50,000

|

|

Less: Loss on sale of Machinery

|

=

|

(2,60,000)

|

|

Sale Proceeds of Machinery

|

|

4,90,000

|

|

Transaction

|

Effect on Cash or Cash Equivalents

|

Reason

|

|

1.

|

No effect

|

Cash is not affected.

|

|

2.

|

Inflow

|

Cash is increased by ₹ 15,000.

|

|

3.

|

No effect

|

Cash is not affected.

|

|

4.

|

No effect

|

Cash is not affected.

|

|

5.

|

Inflow

|

Cash is increased by ₹ 10,000.

|

|

6.

|

Inflow

|

Cash is increased by ₹ 20,000.

|

|

7.

|

No effect

|

Cash is not affected.

|

|

8.

|

No effect

|

Cash is not affected.

|

|

9.

|

Outflow

|

Cash is decreased by ₹ 18,000.

|

|

10.

|

No effect

|

Cash includes bank deposits also.

|

|

11.

|

No effect

|

It is merely a conversion of cash equivalents into cash.

|

|

12.

|

Inflow

|

Cash is increased.

|

|

13.

|

No effect

|

Cash is not affected.

|

|

14.

|

No effect

|

Cash is not affected.

|

|

15.

|

Outflow

|

Cash is decreased.

|

|

16.

|

Inflow

|

Cash is increased.

|

|

17.

|

Inflow

|

Cash is increased.

|

Notes:

Notes: