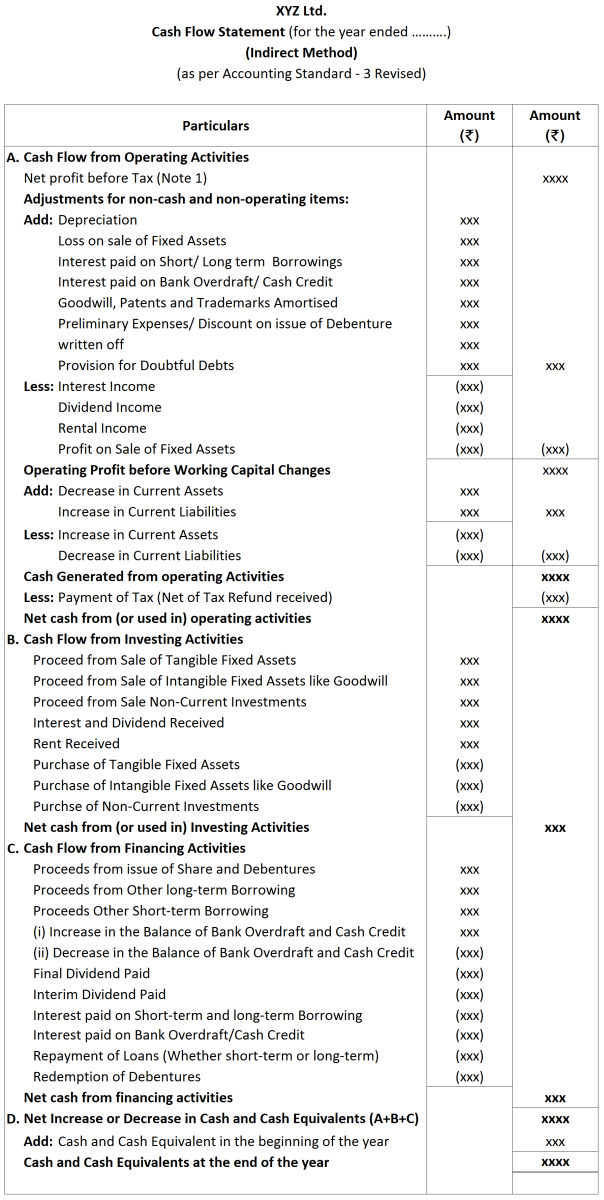

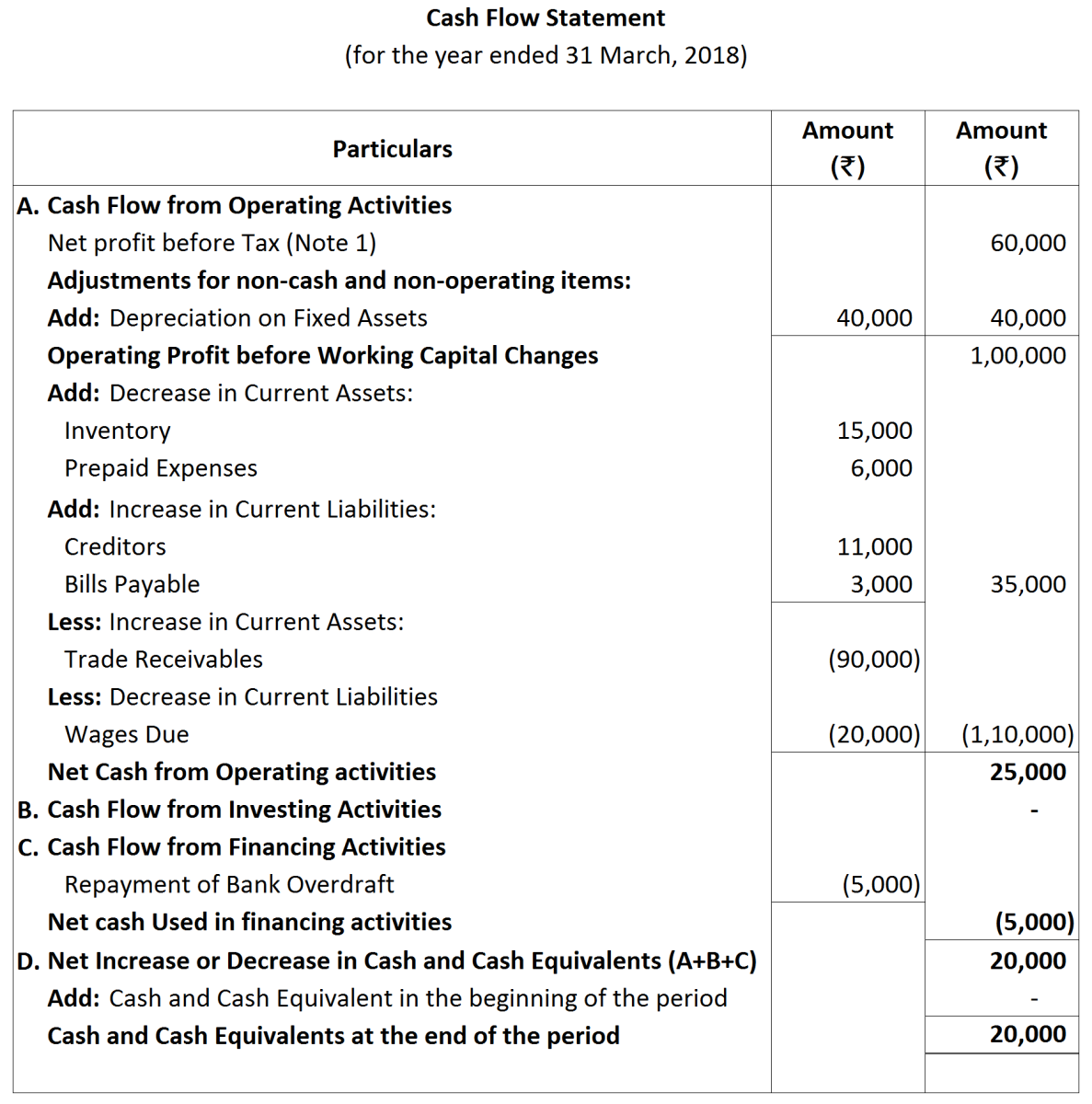

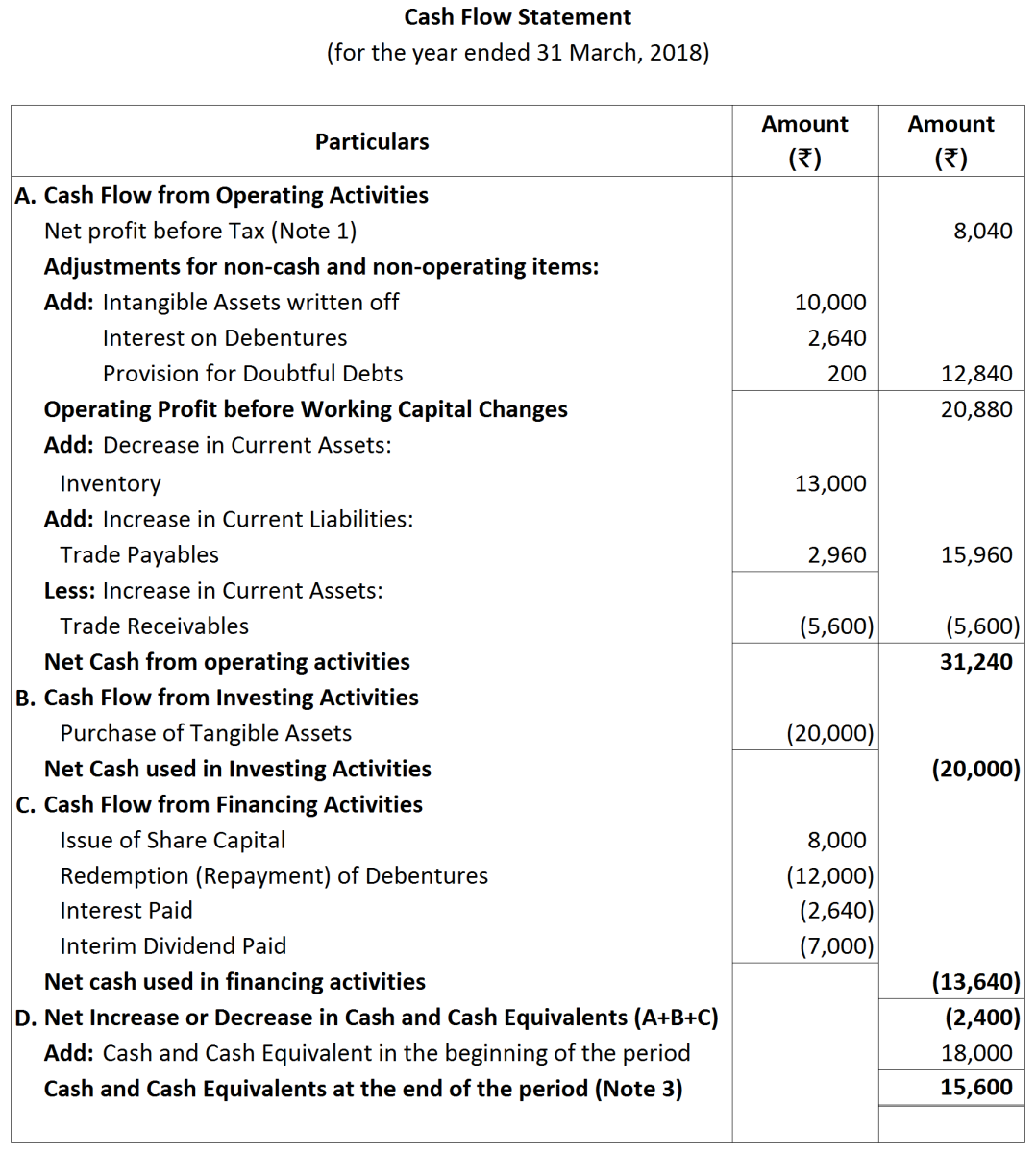

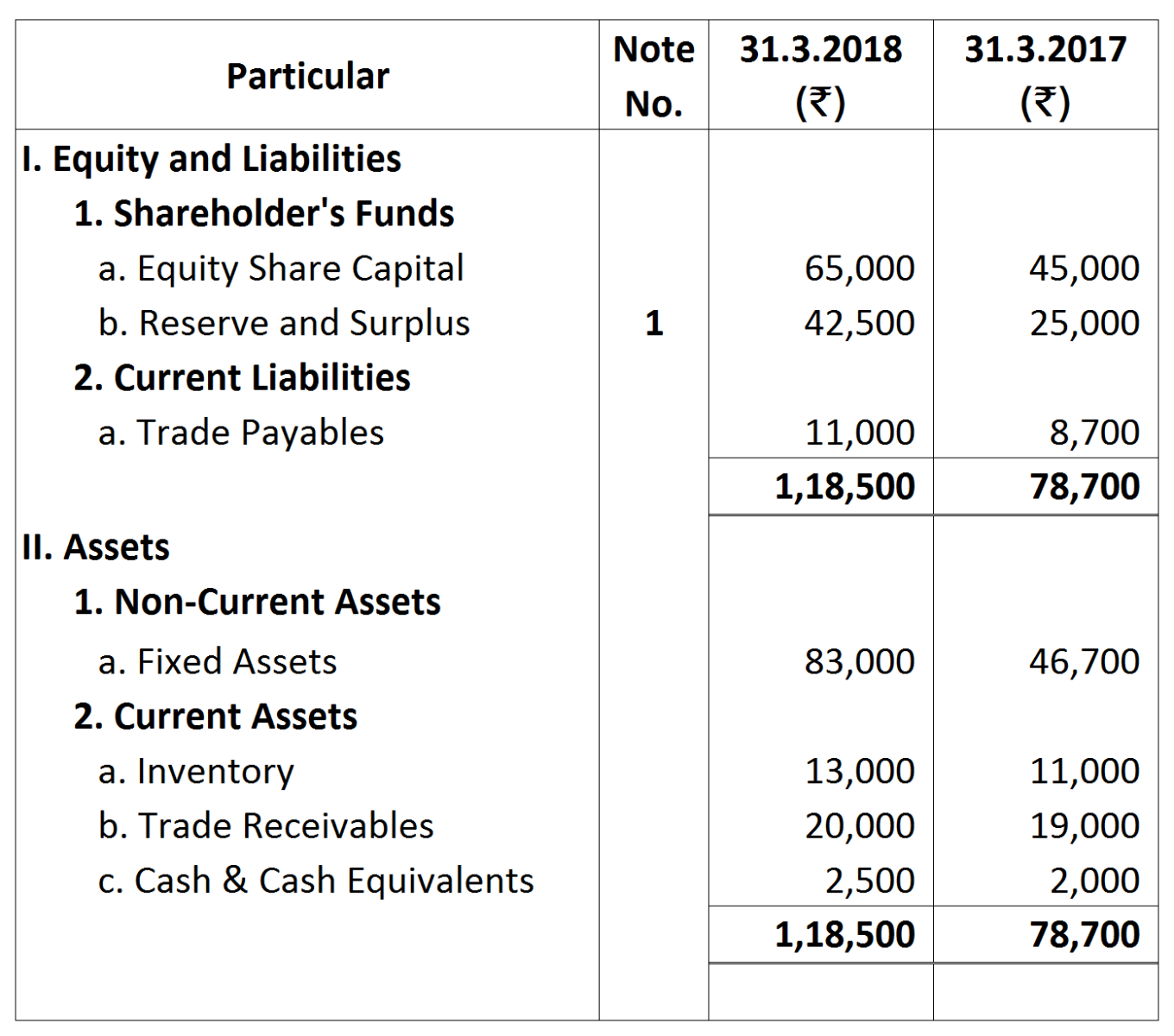

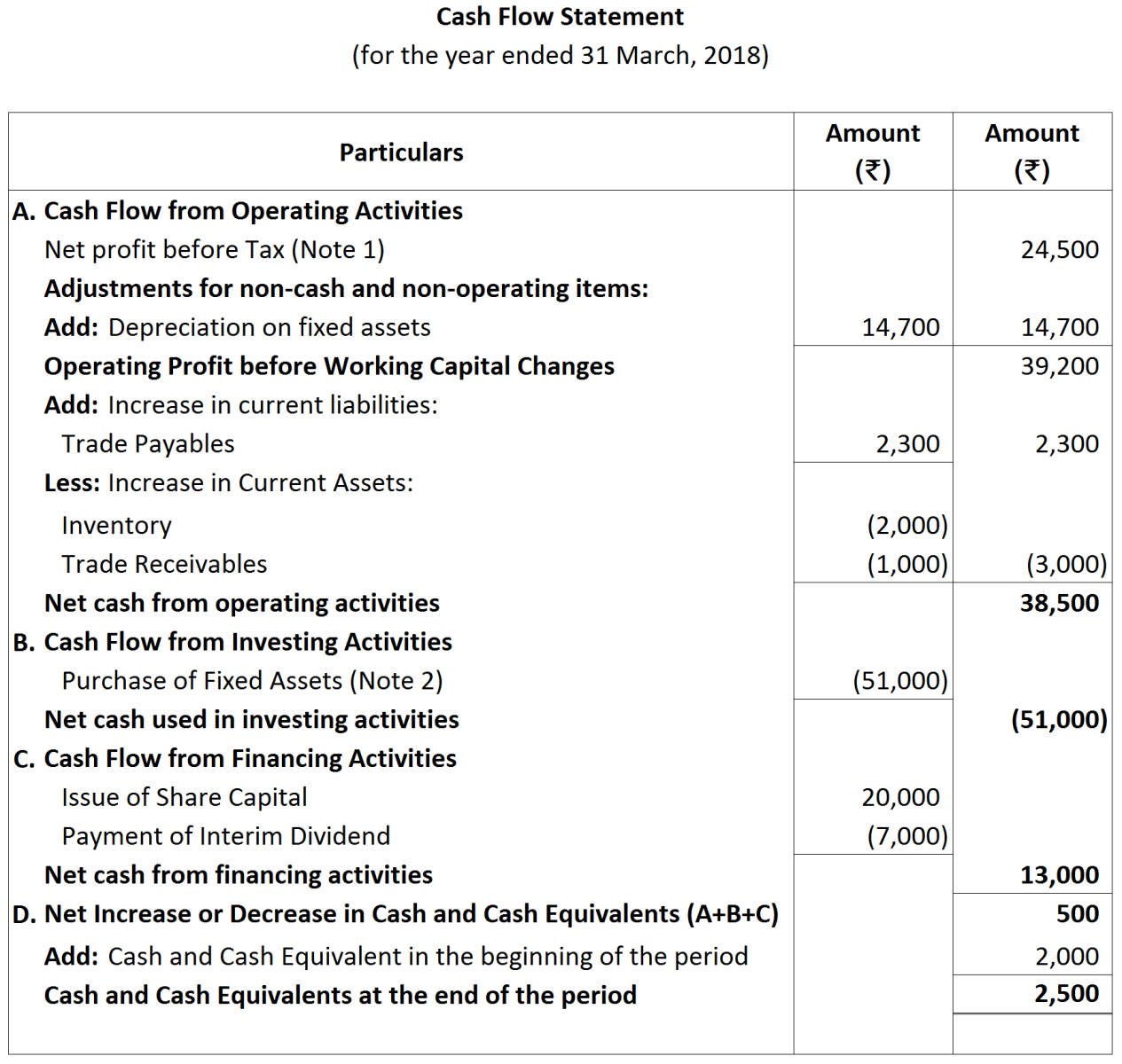

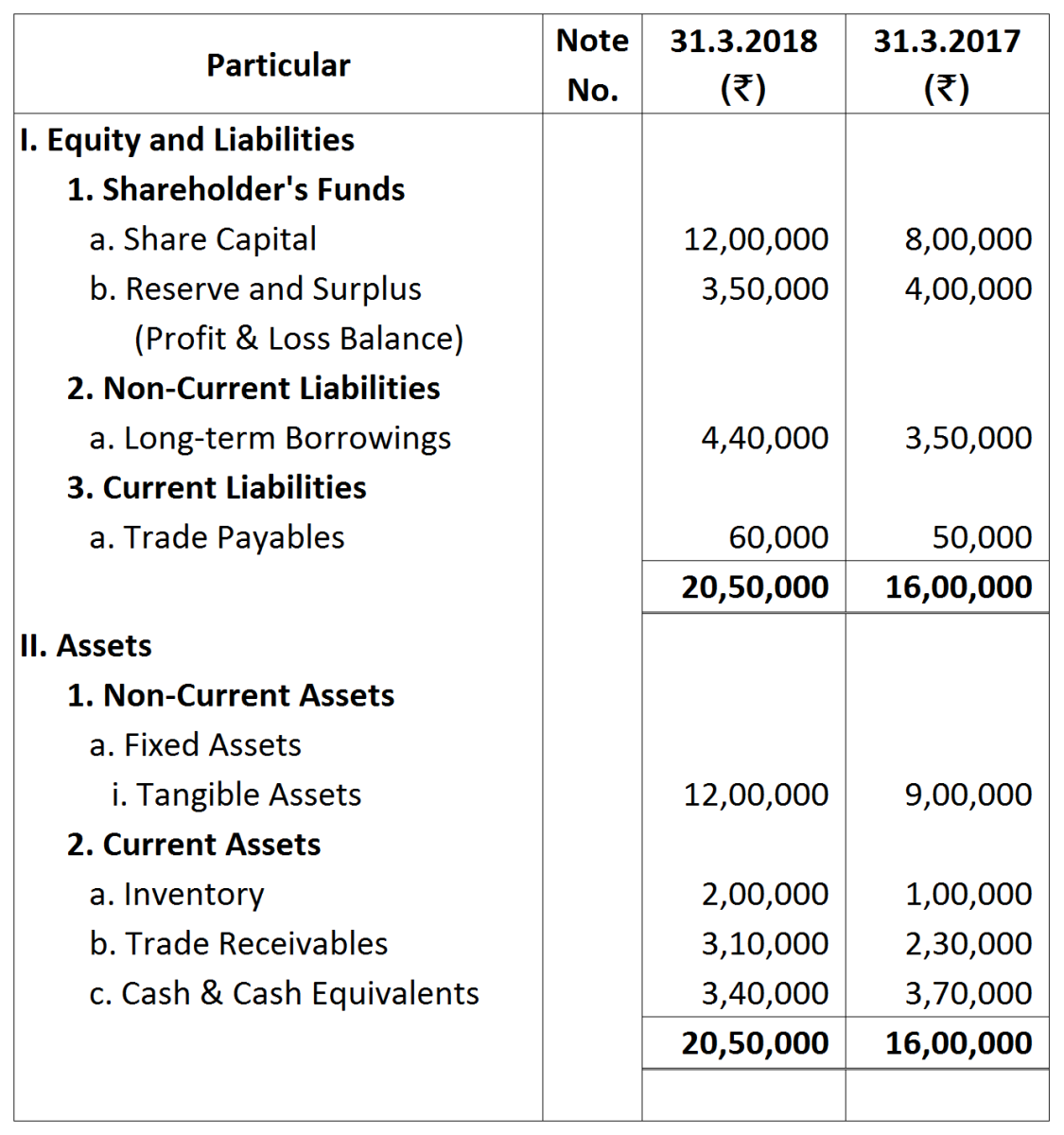

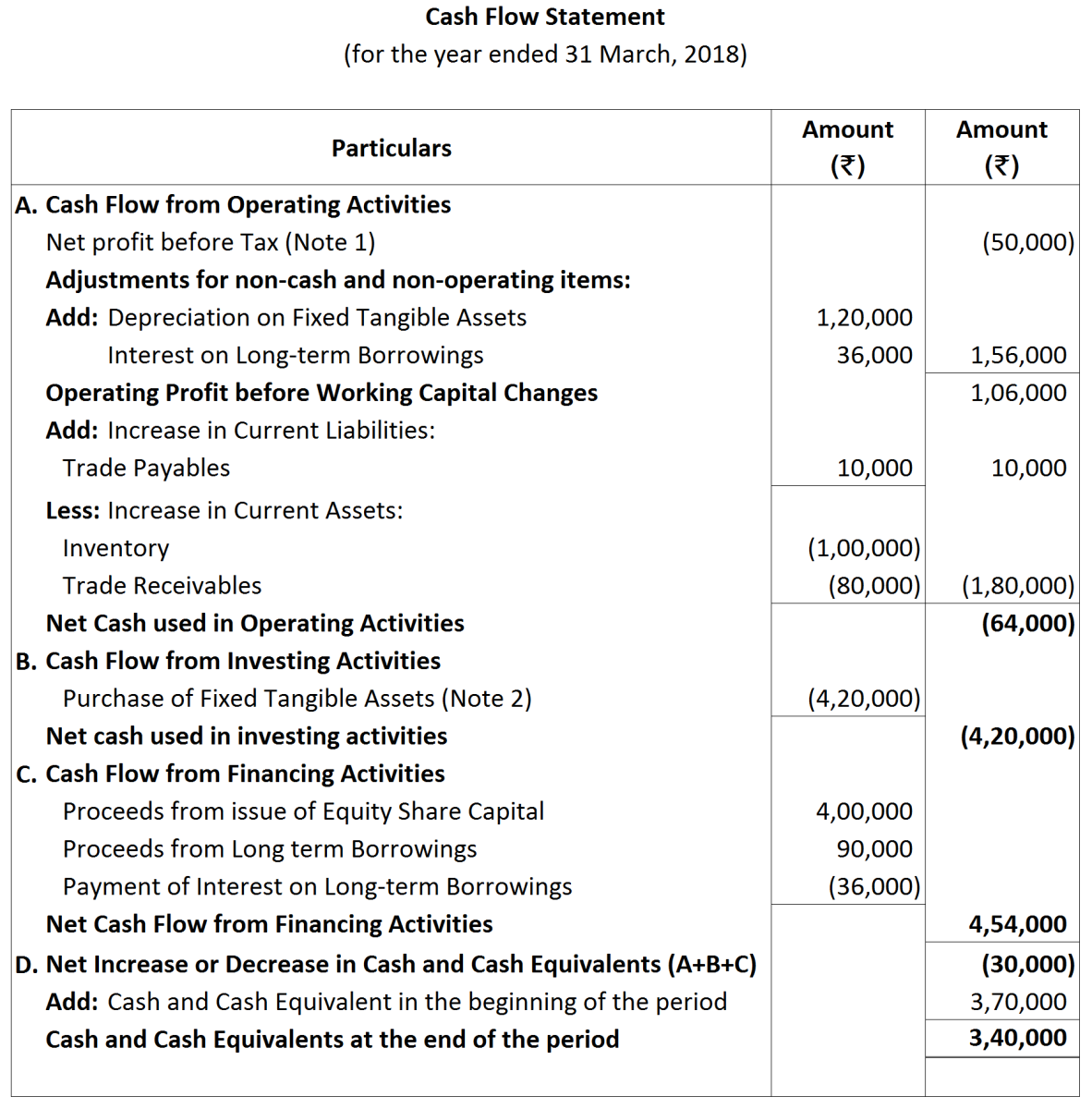

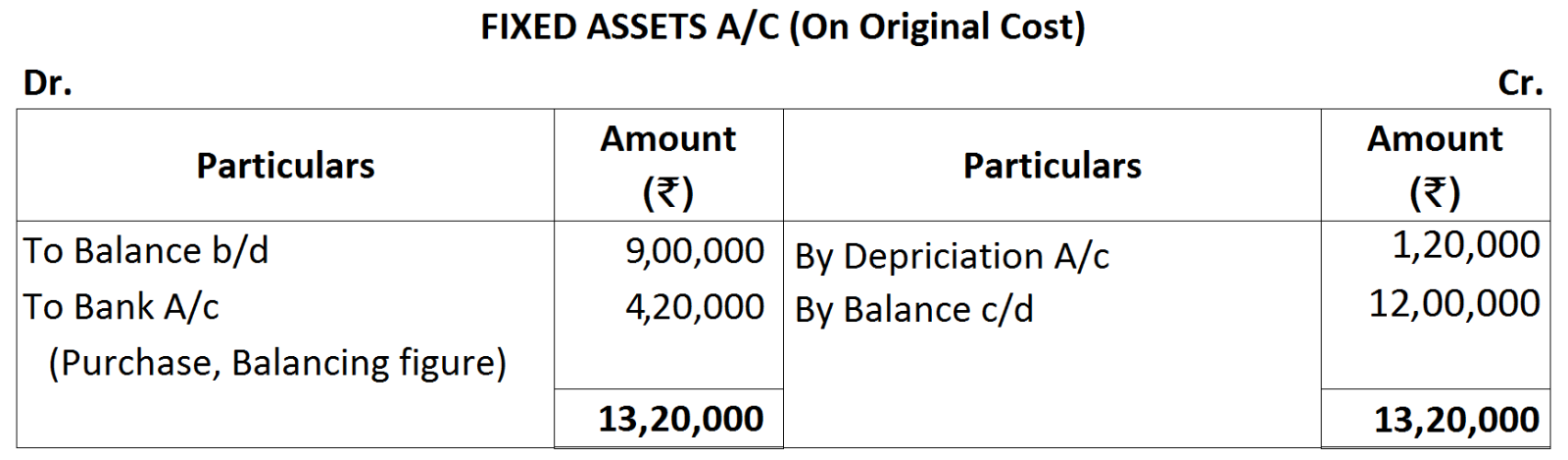

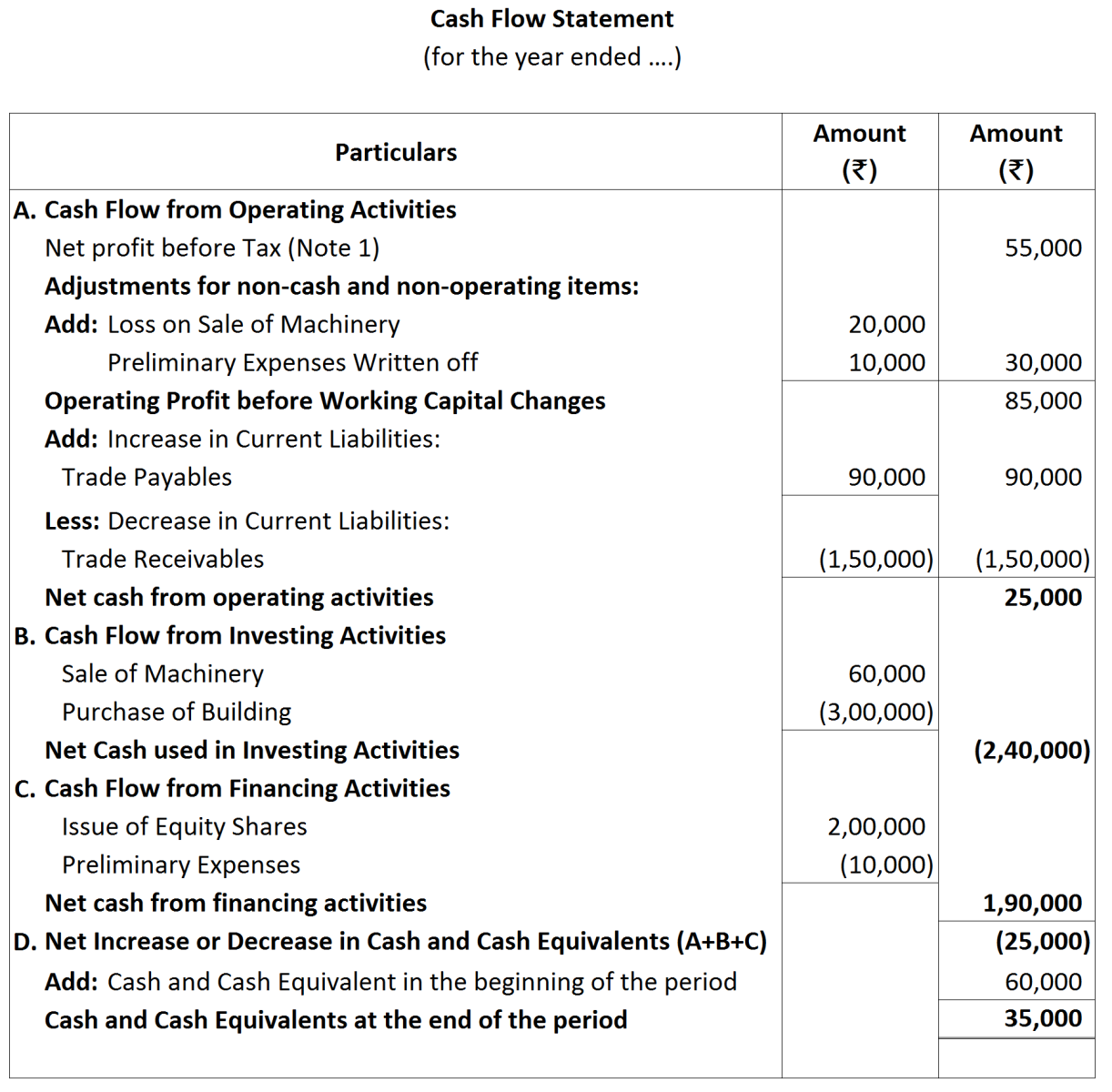

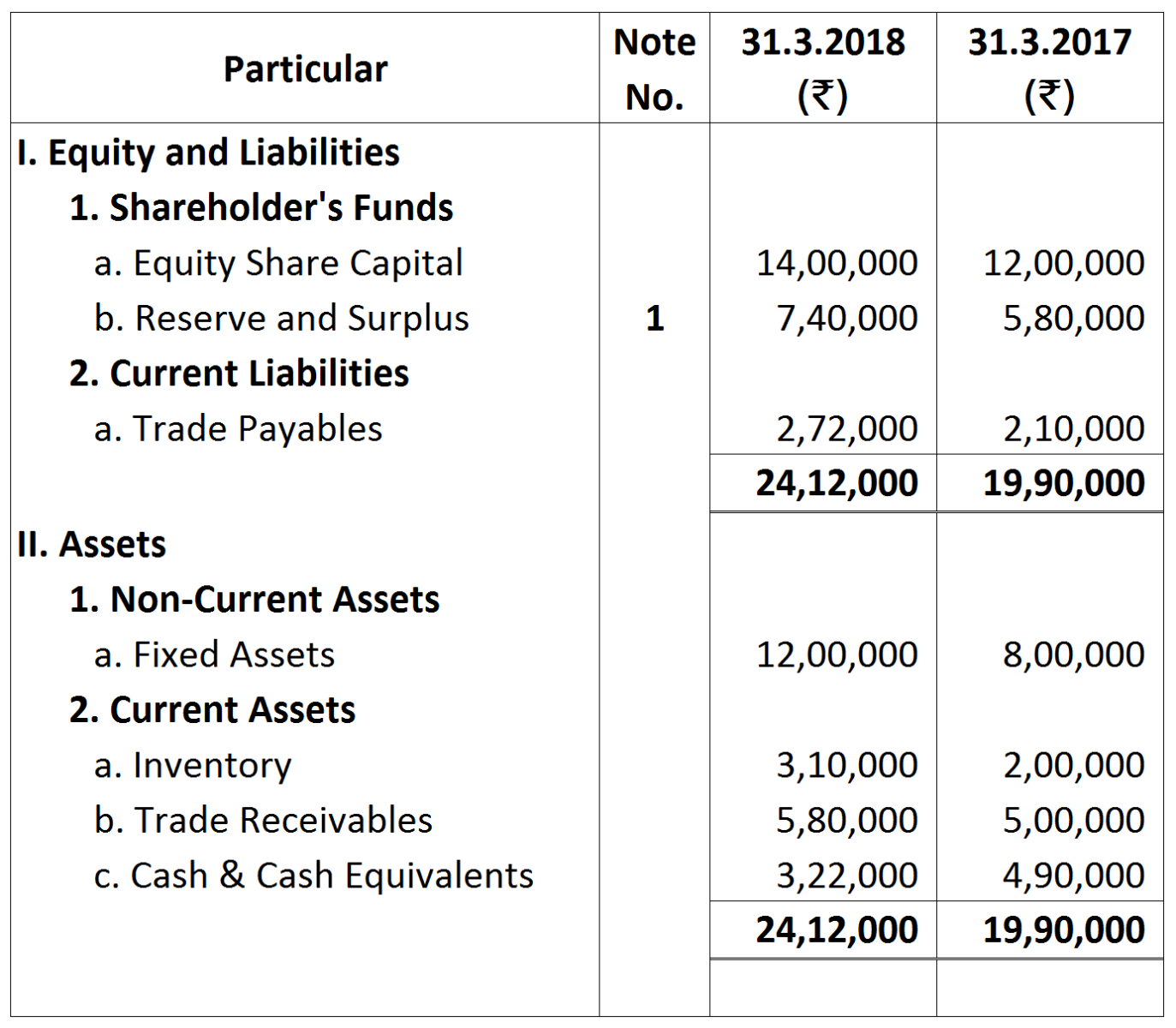

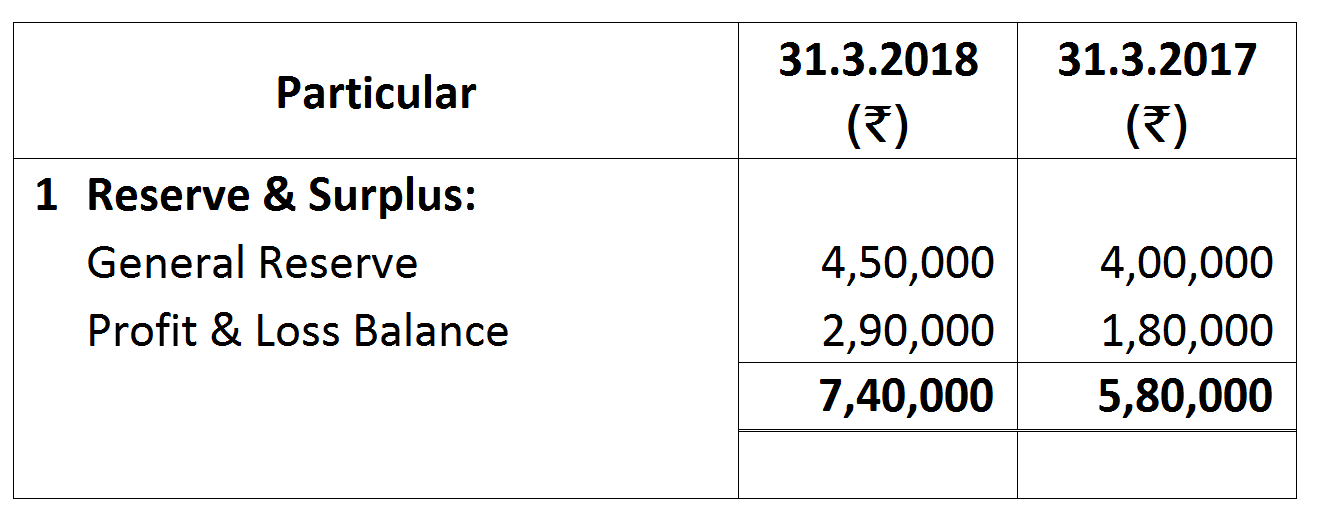

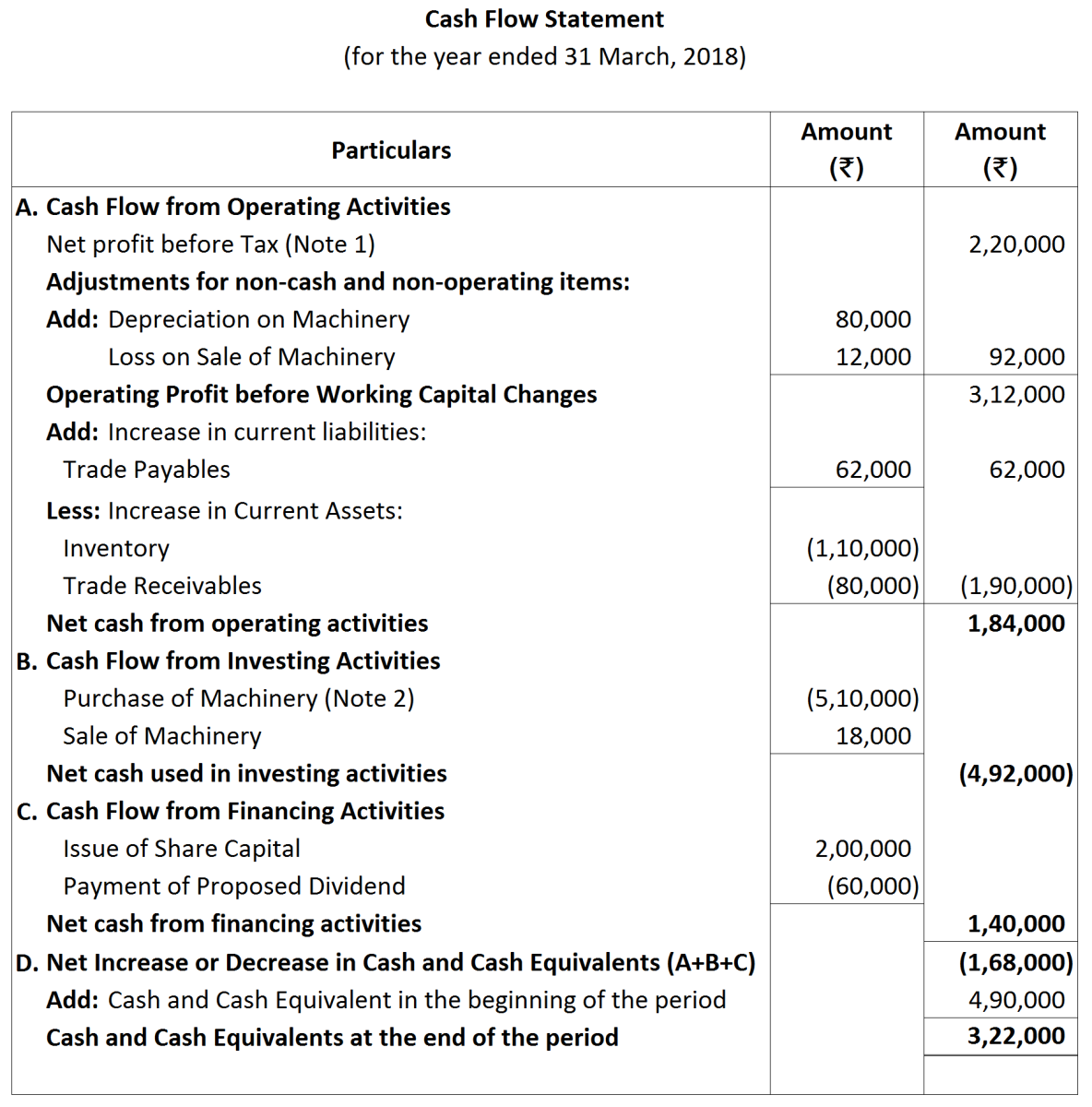

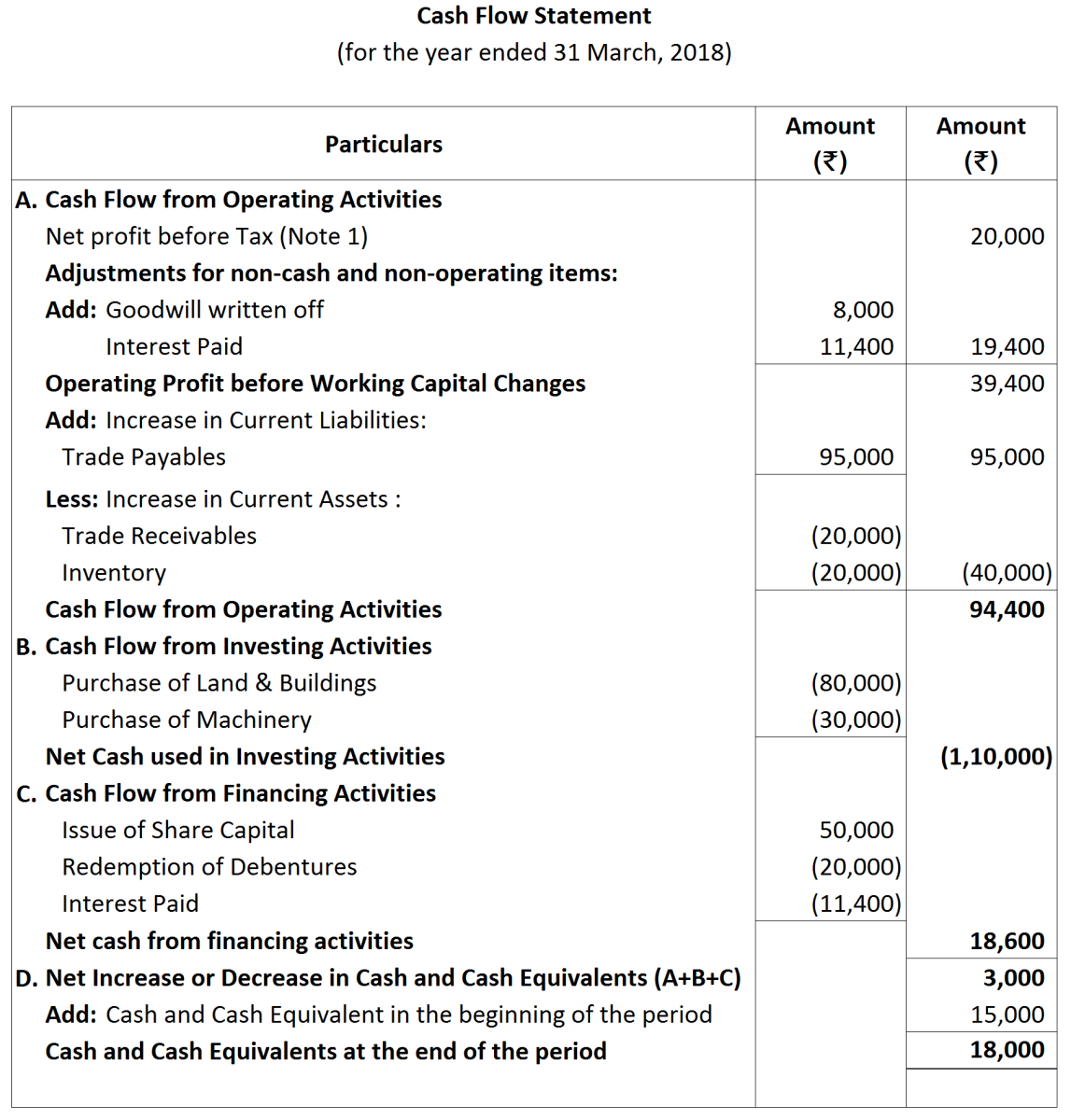

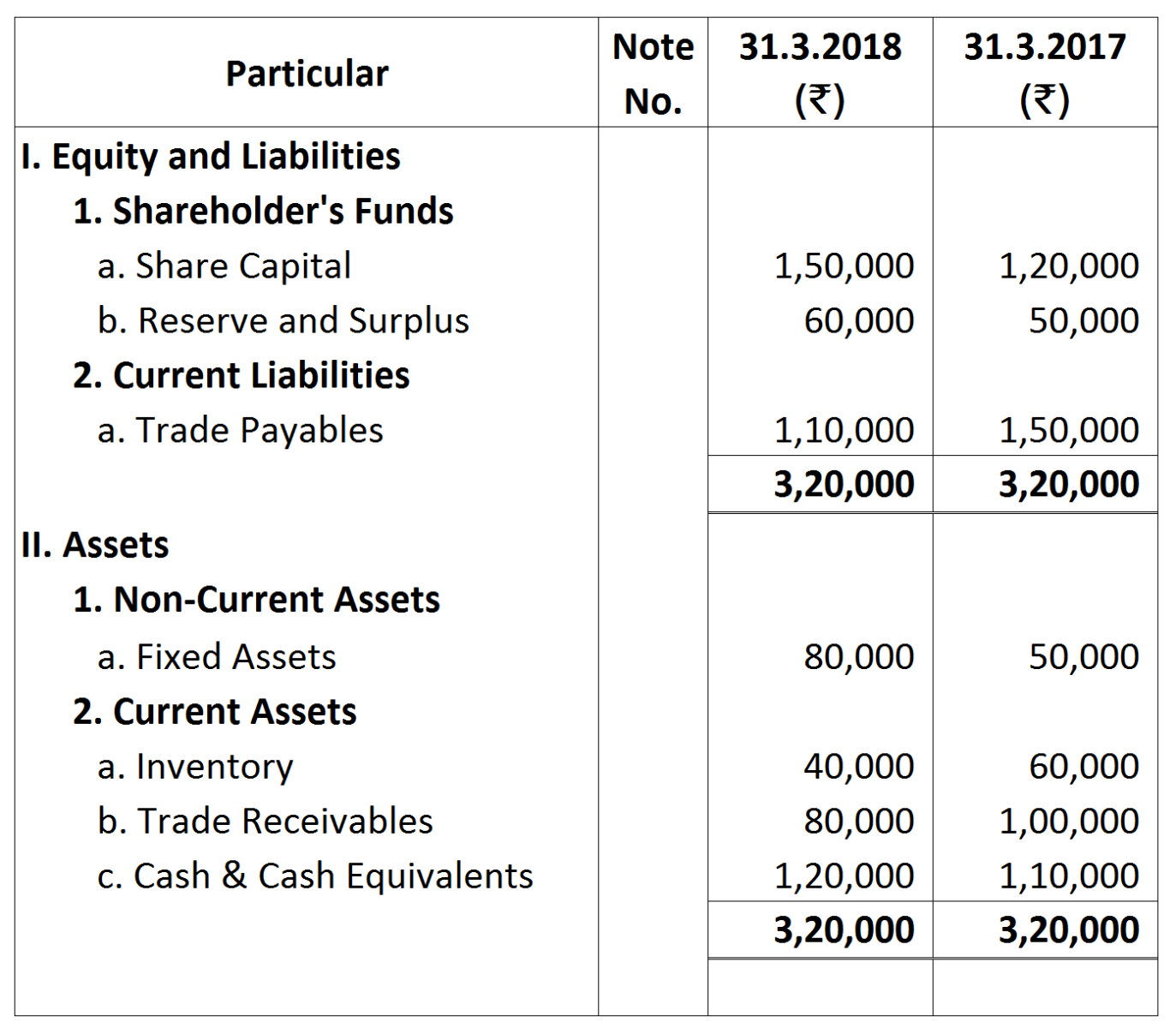

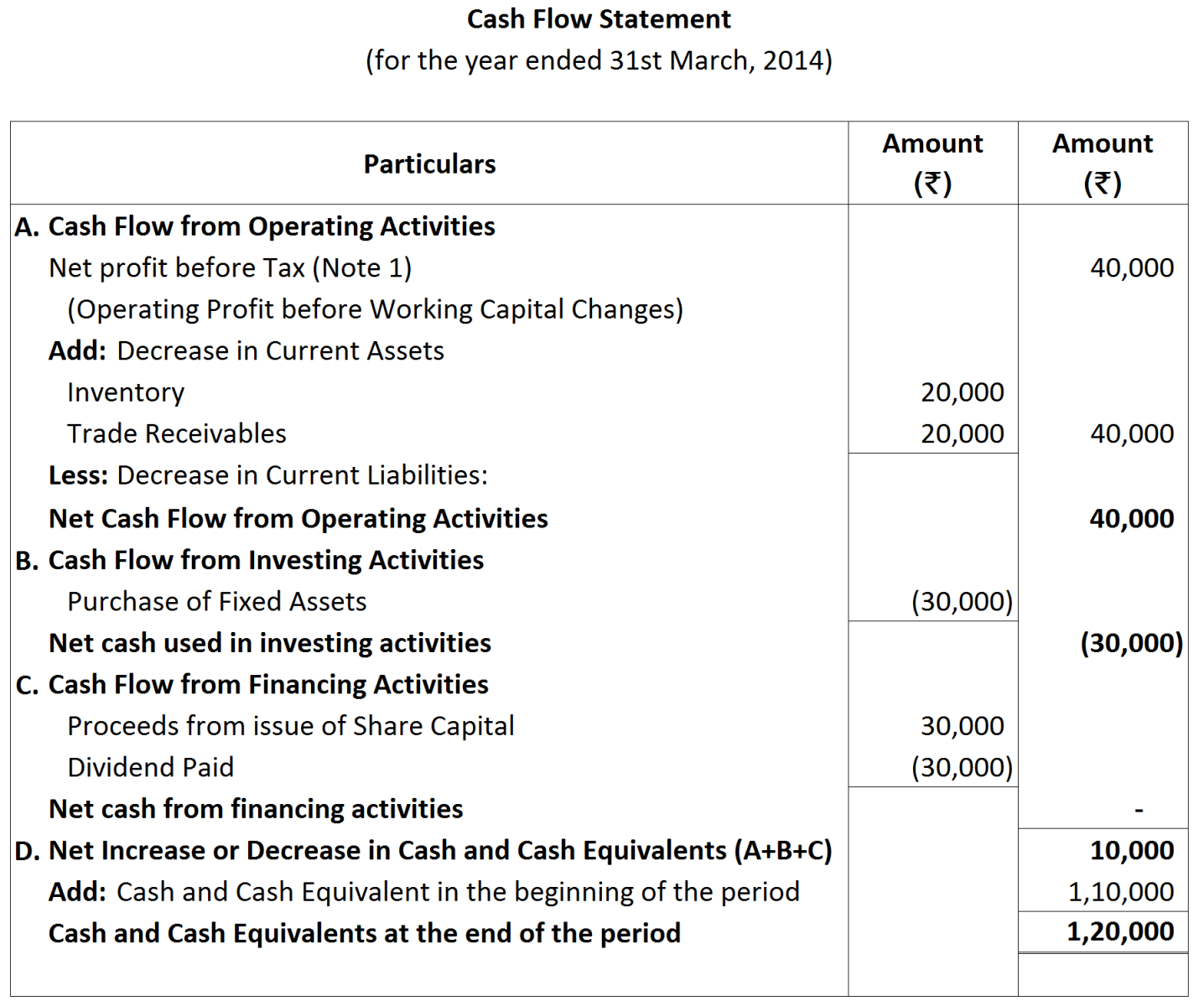

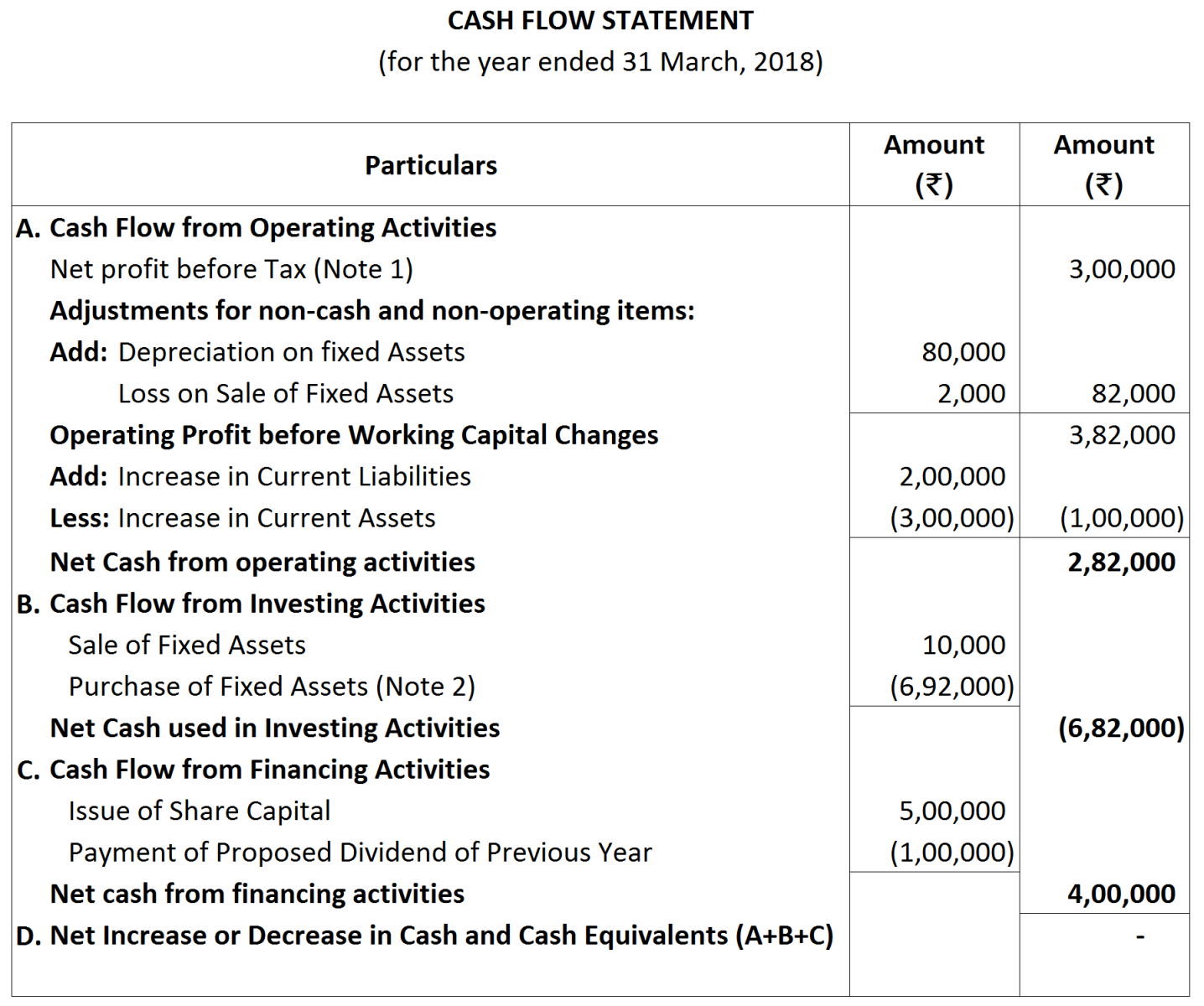

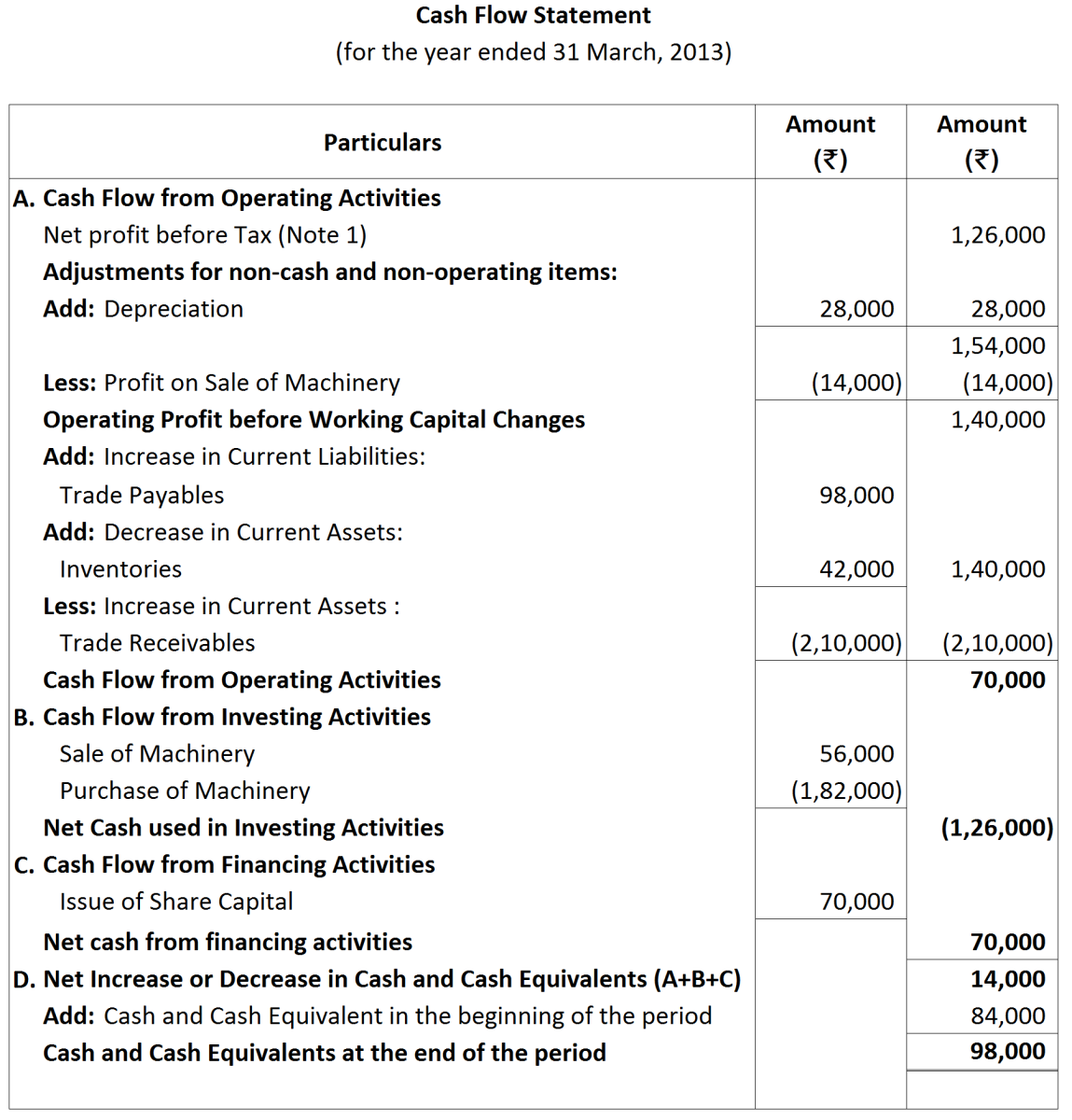

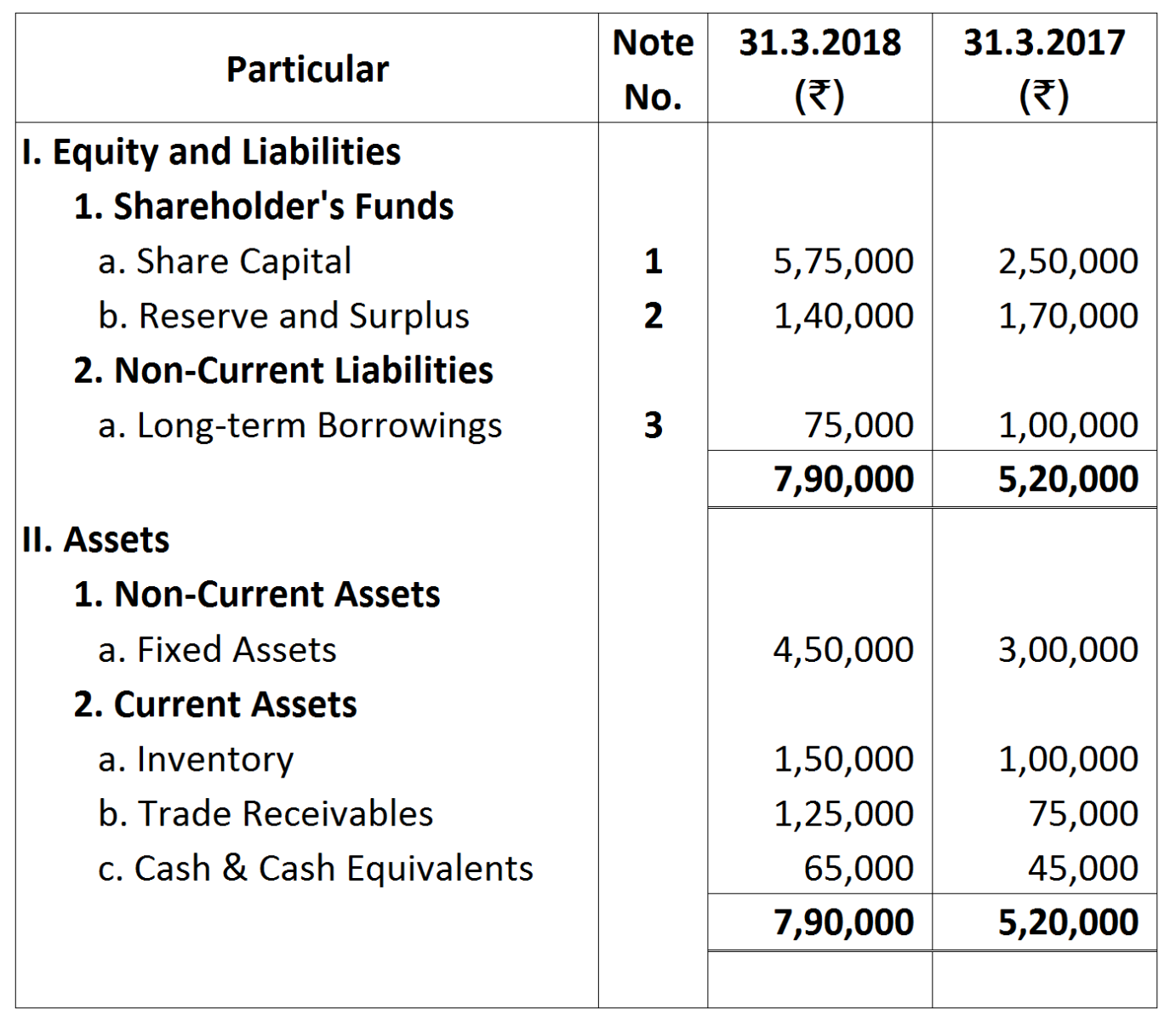

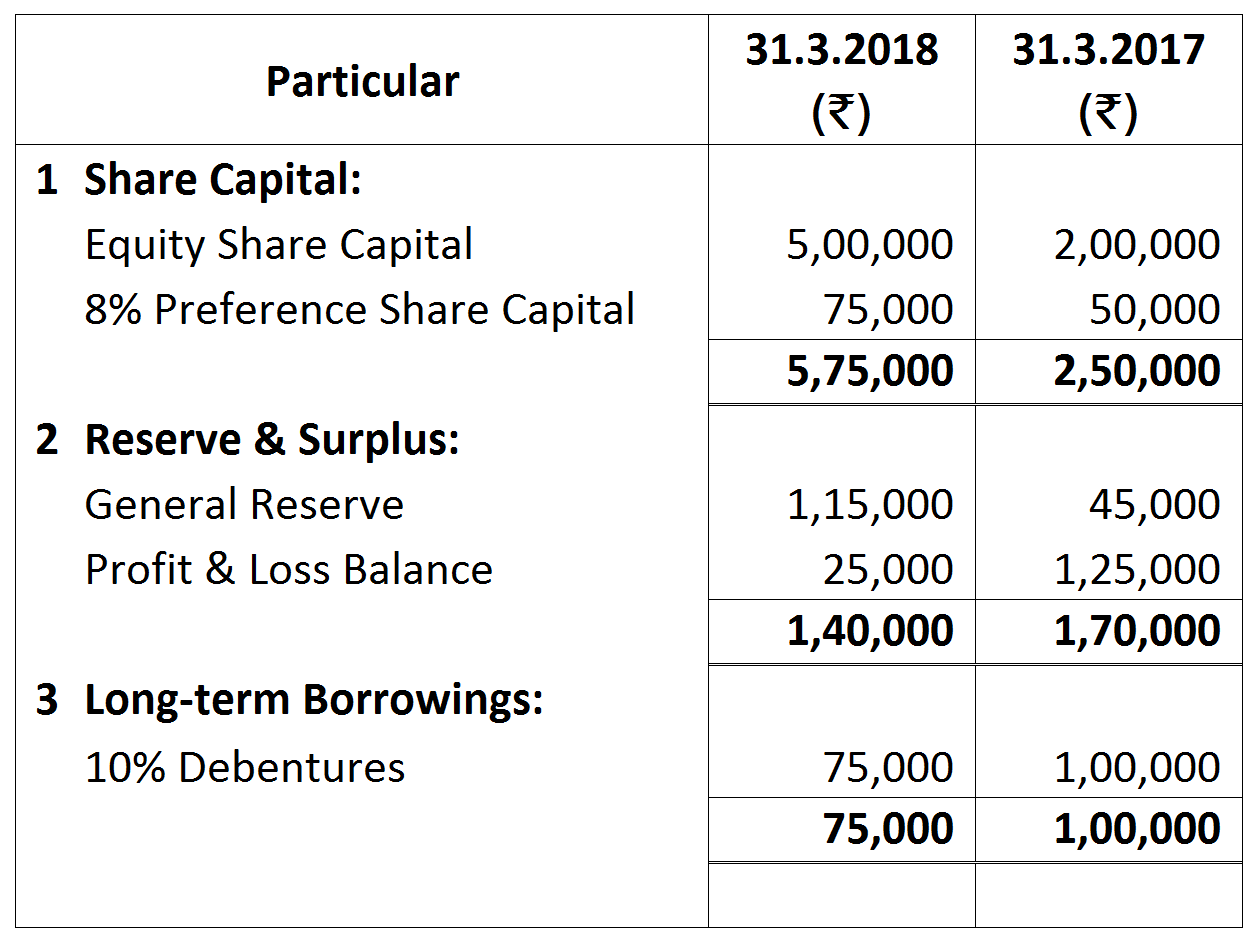

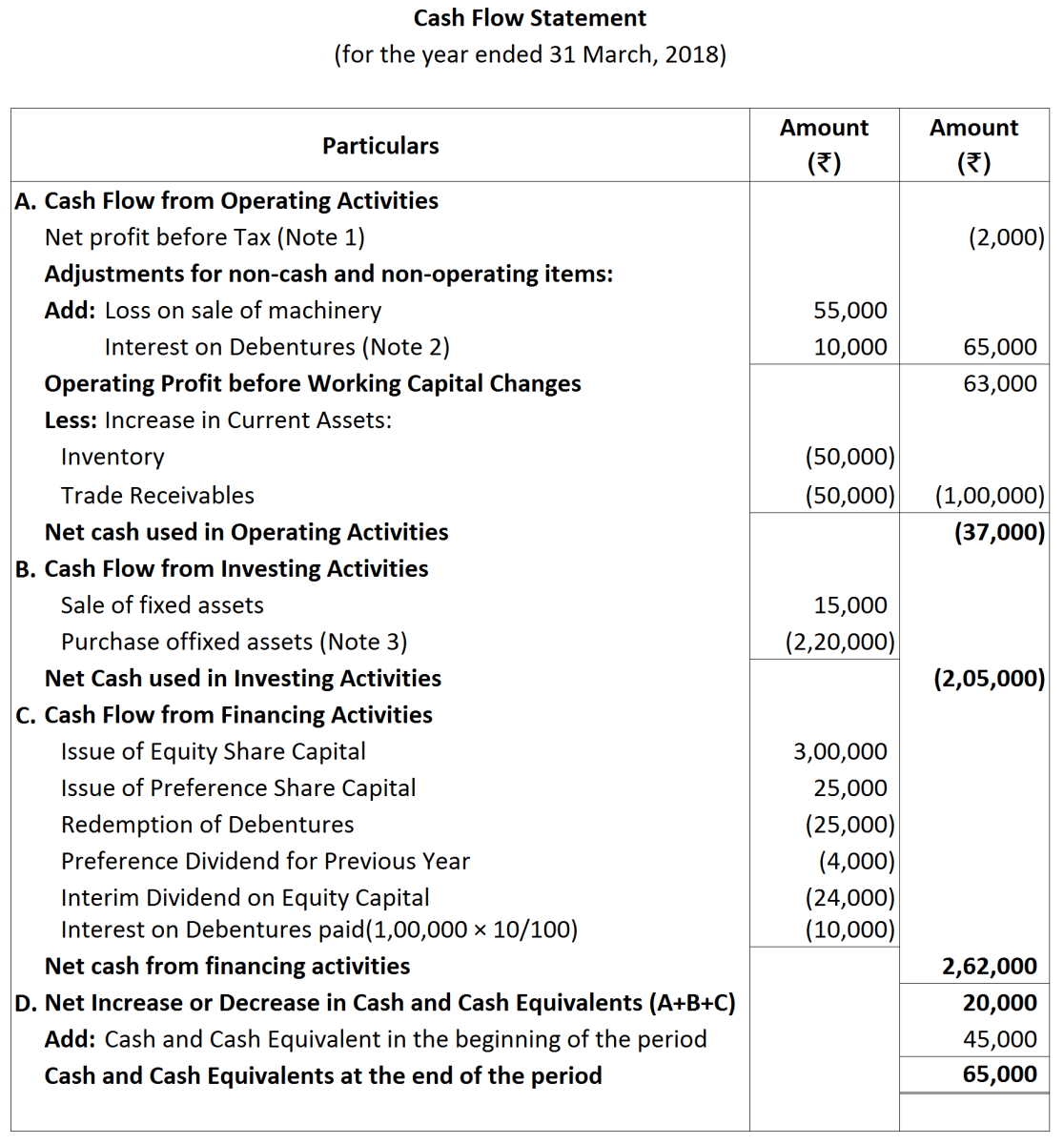

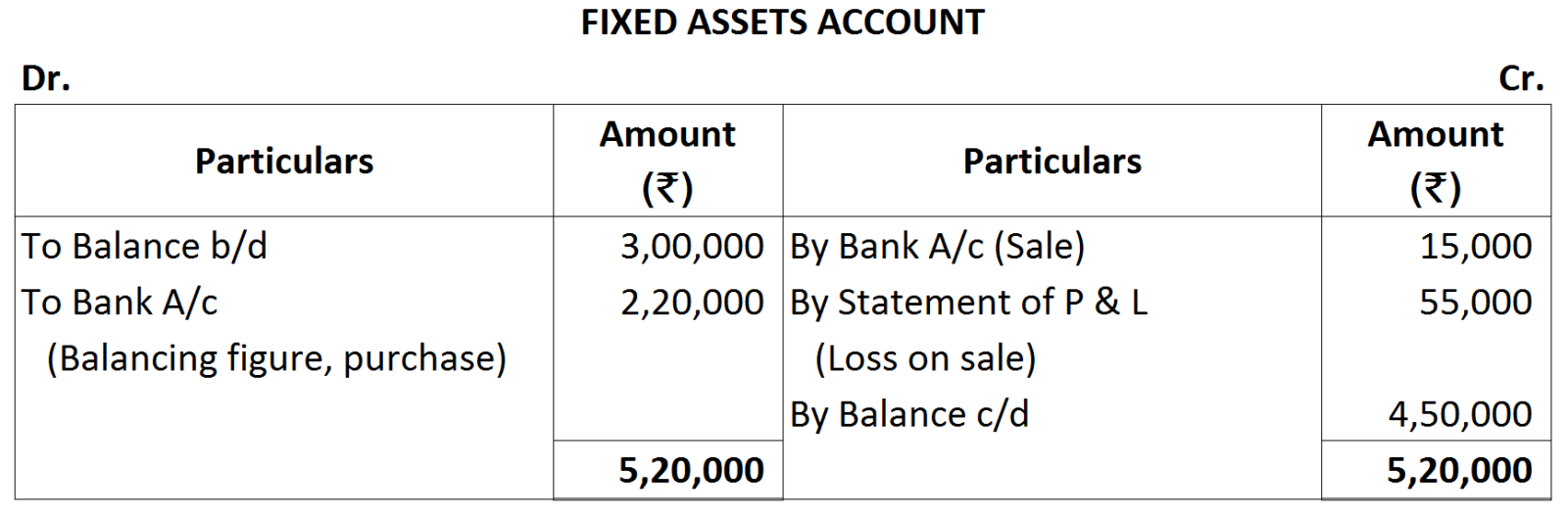

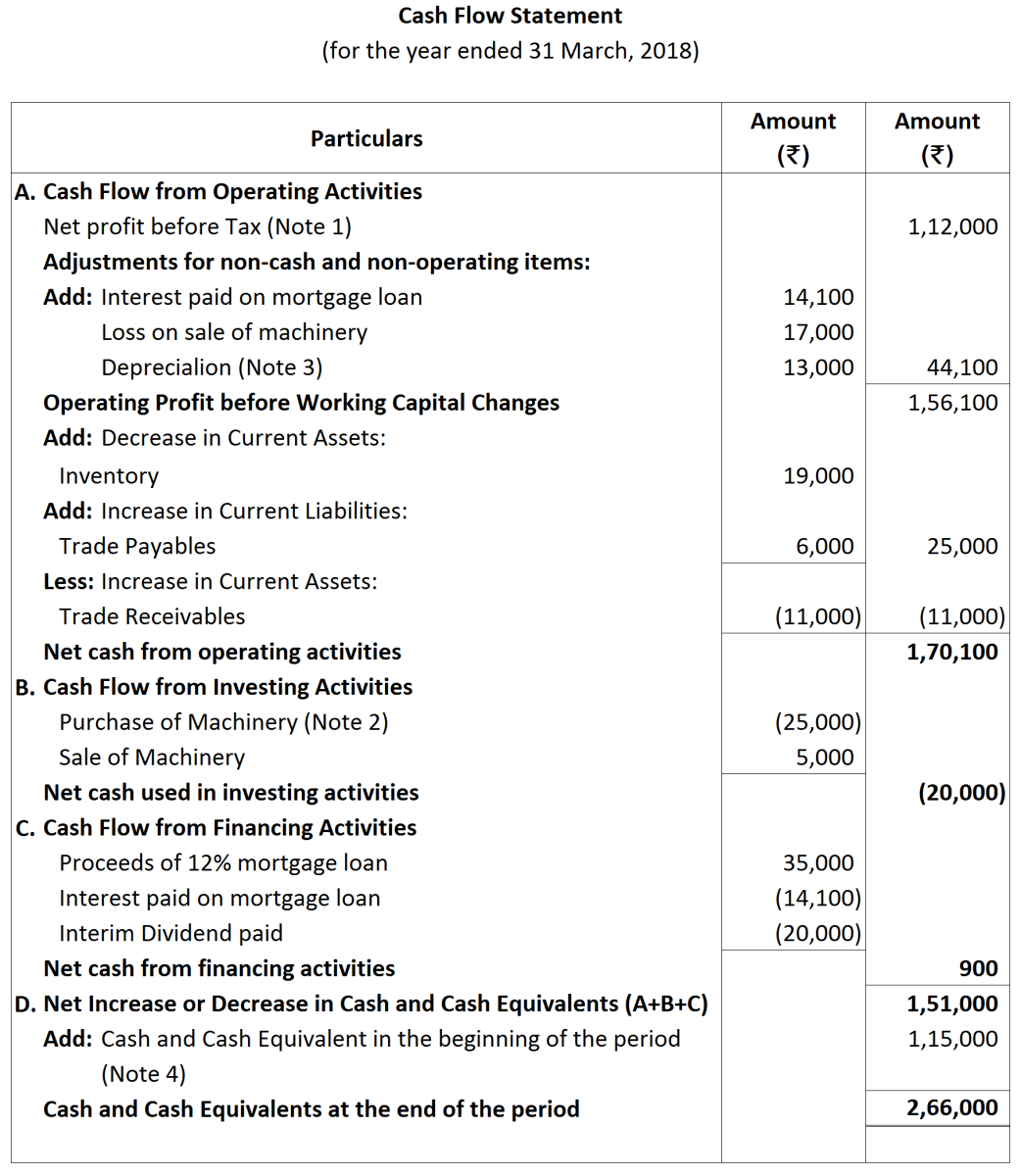

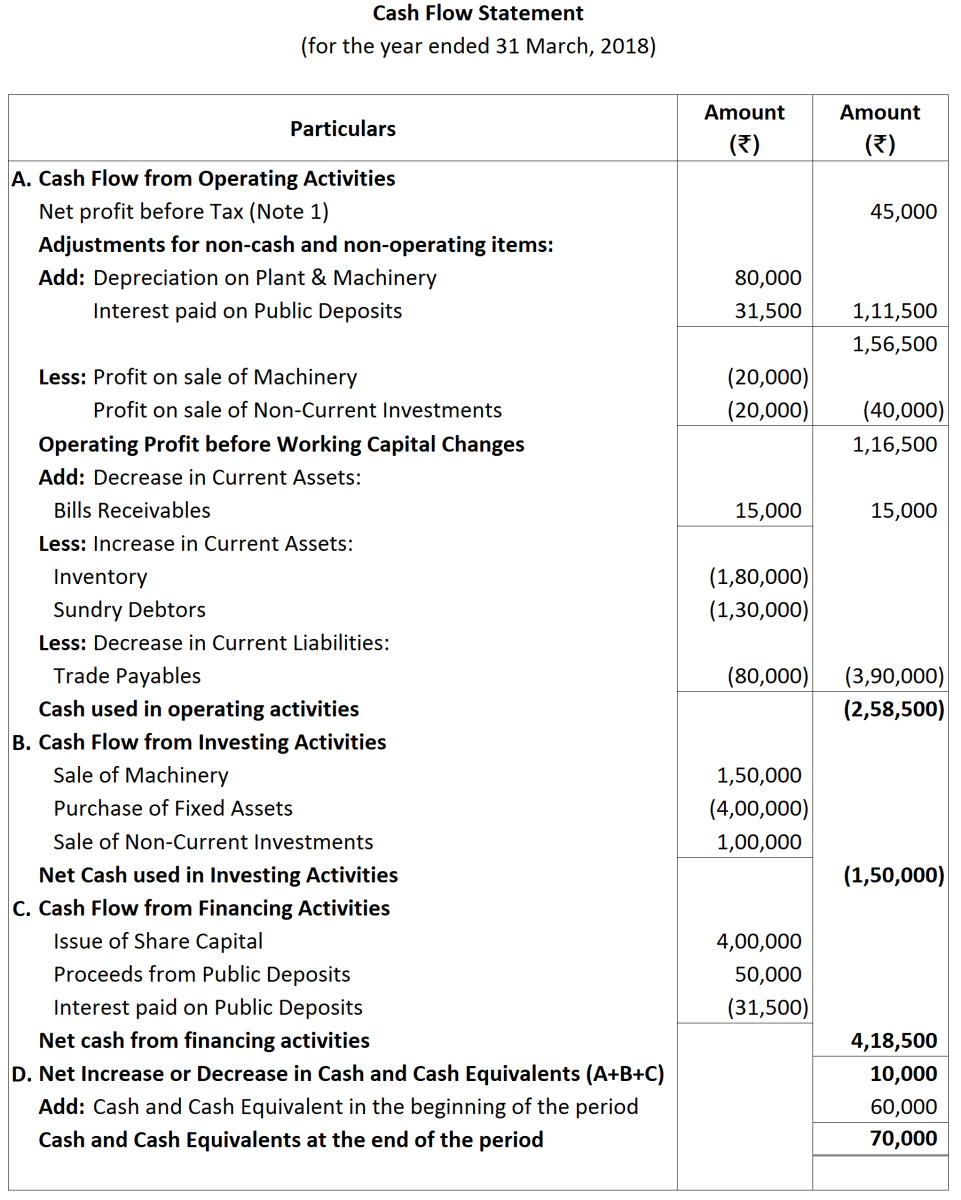

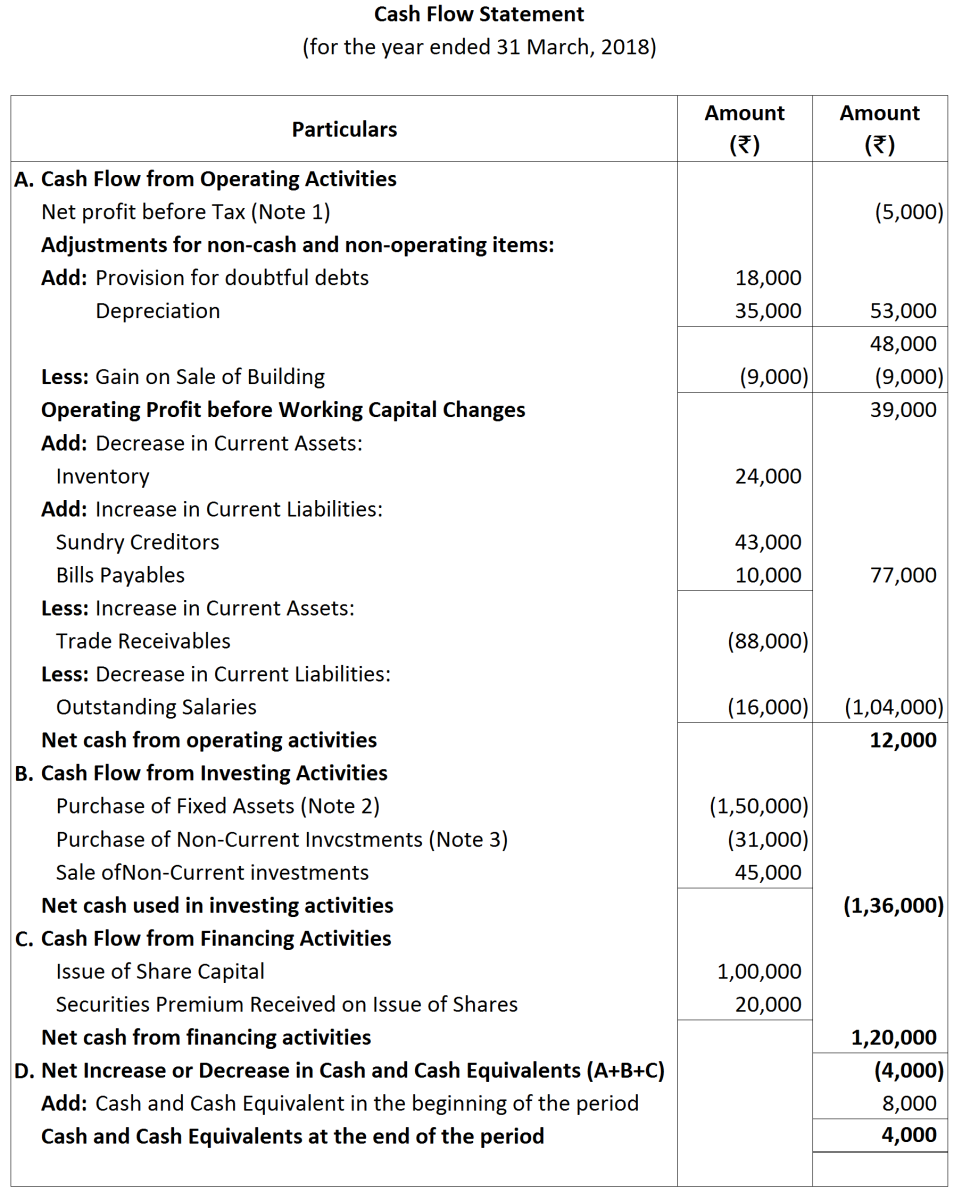

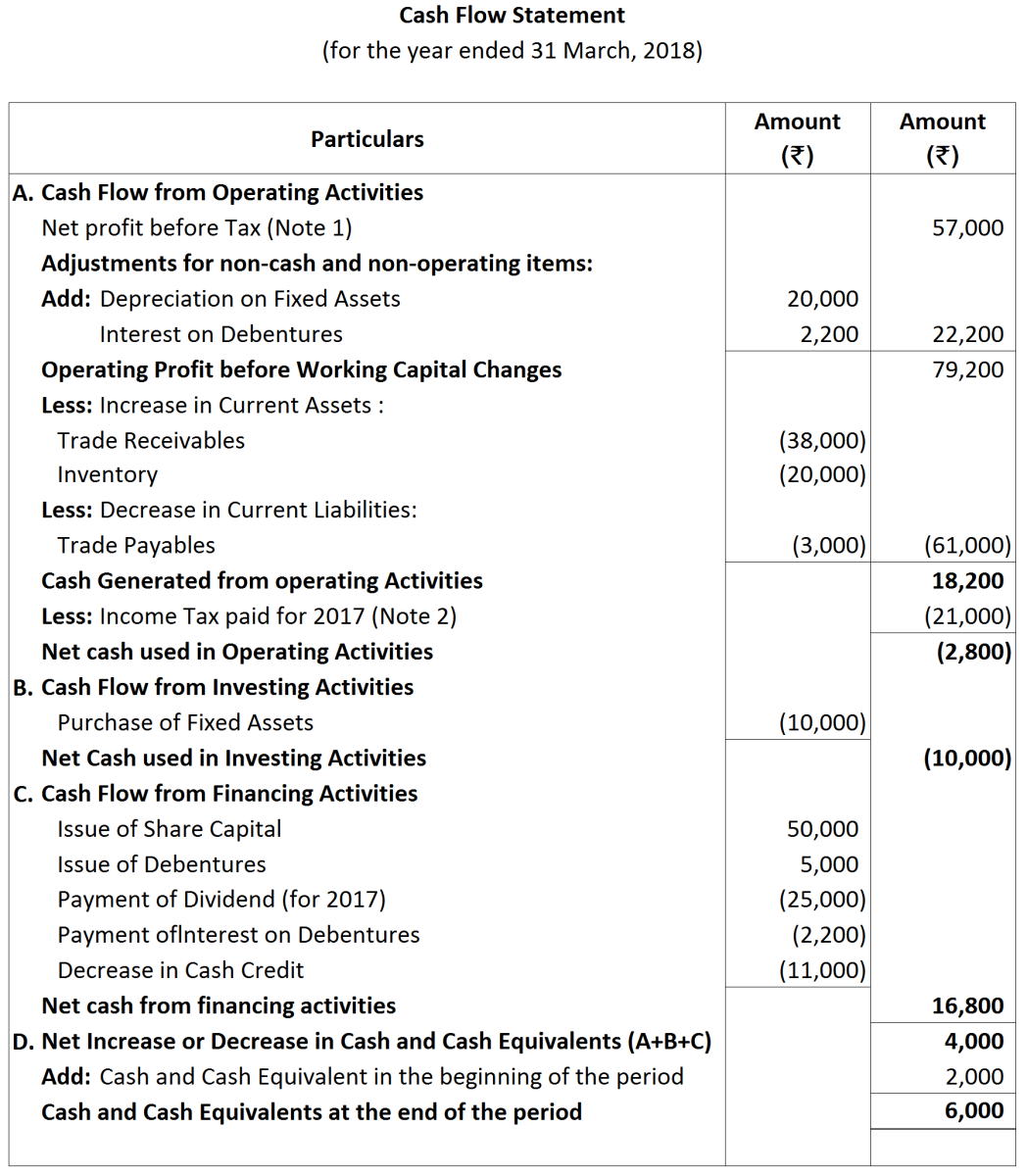

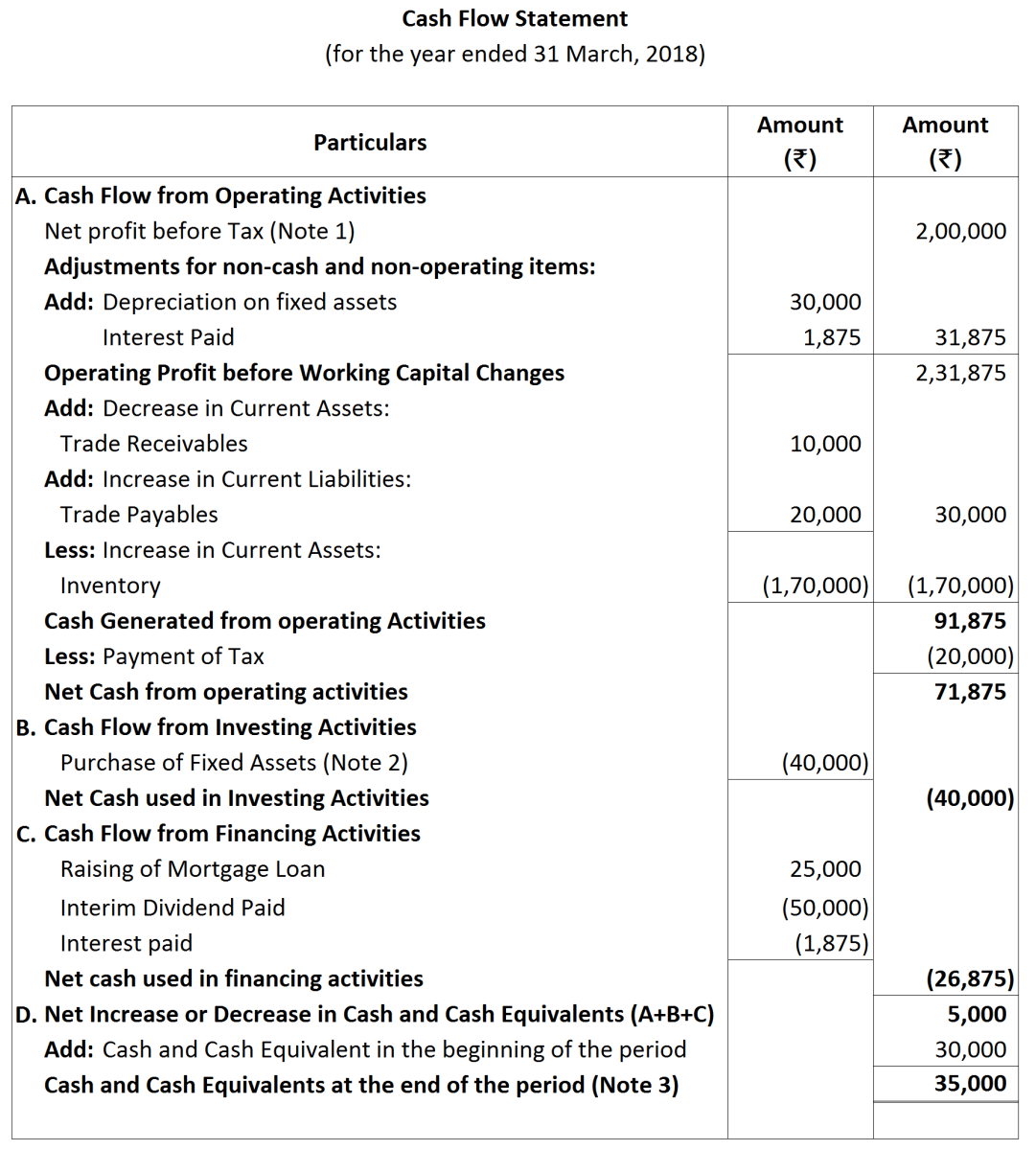

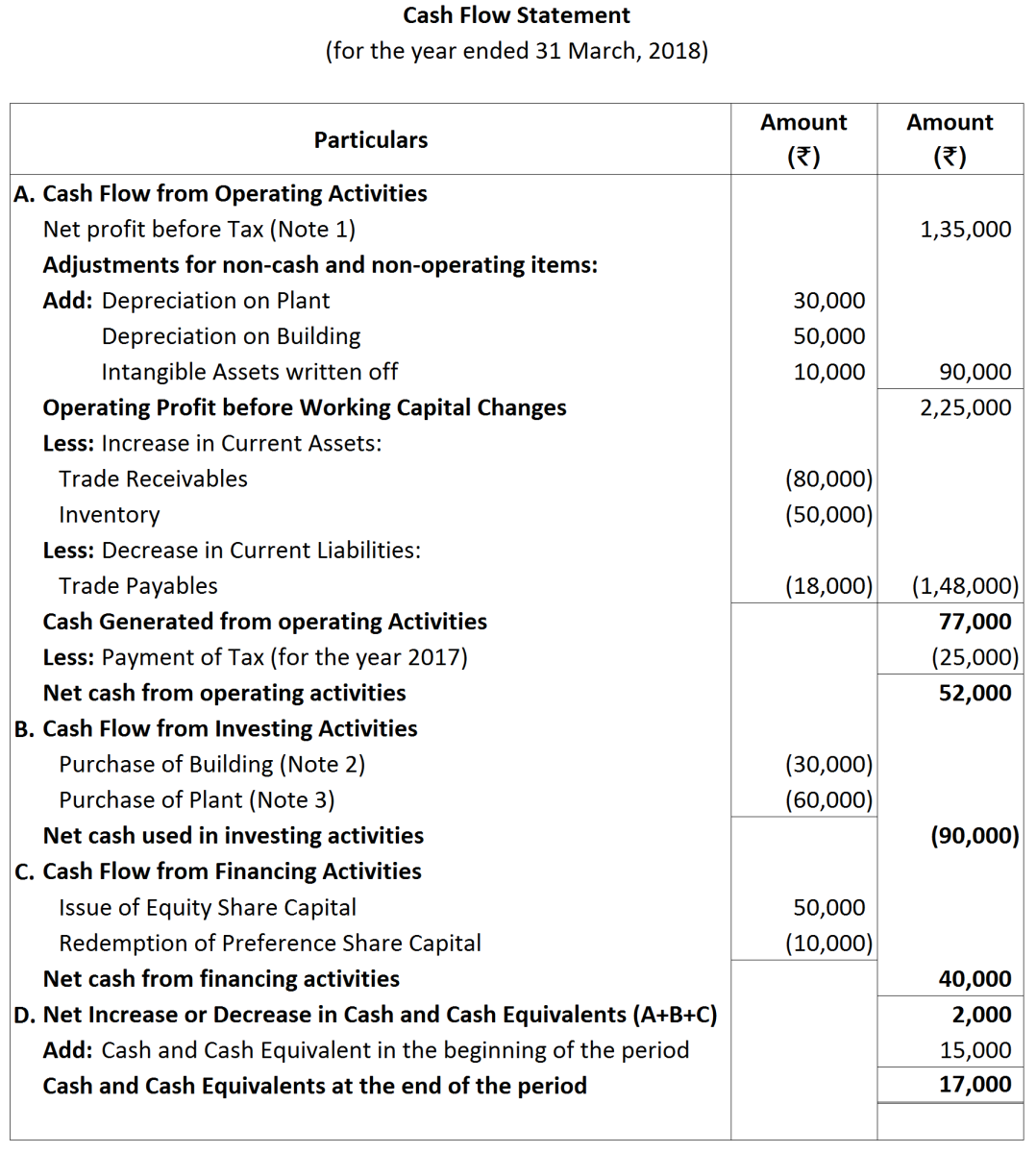

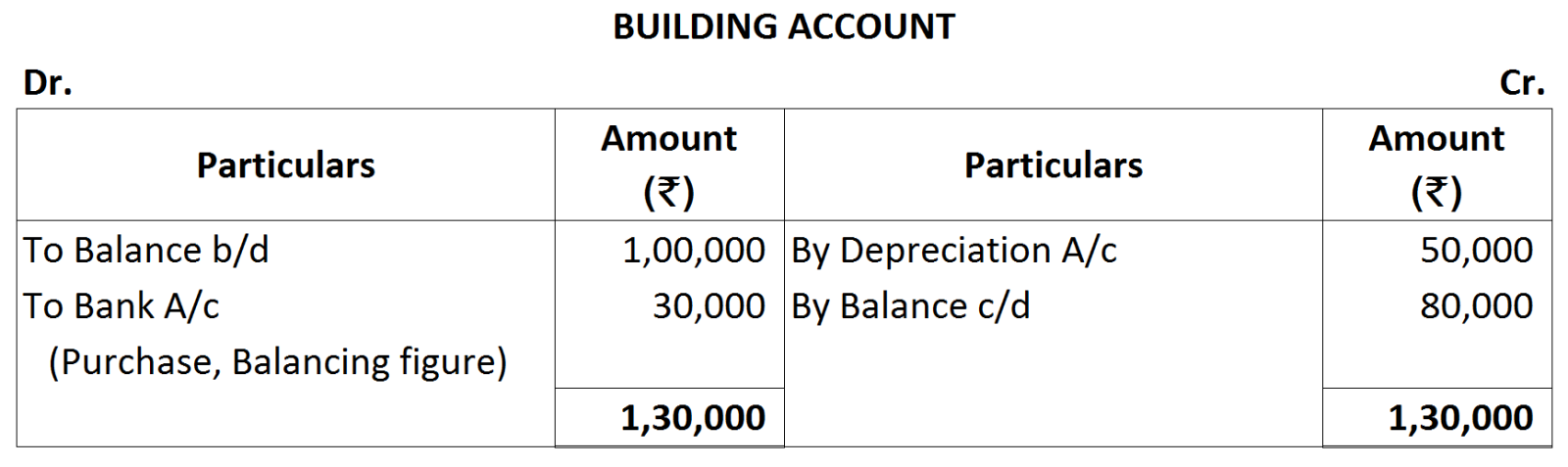

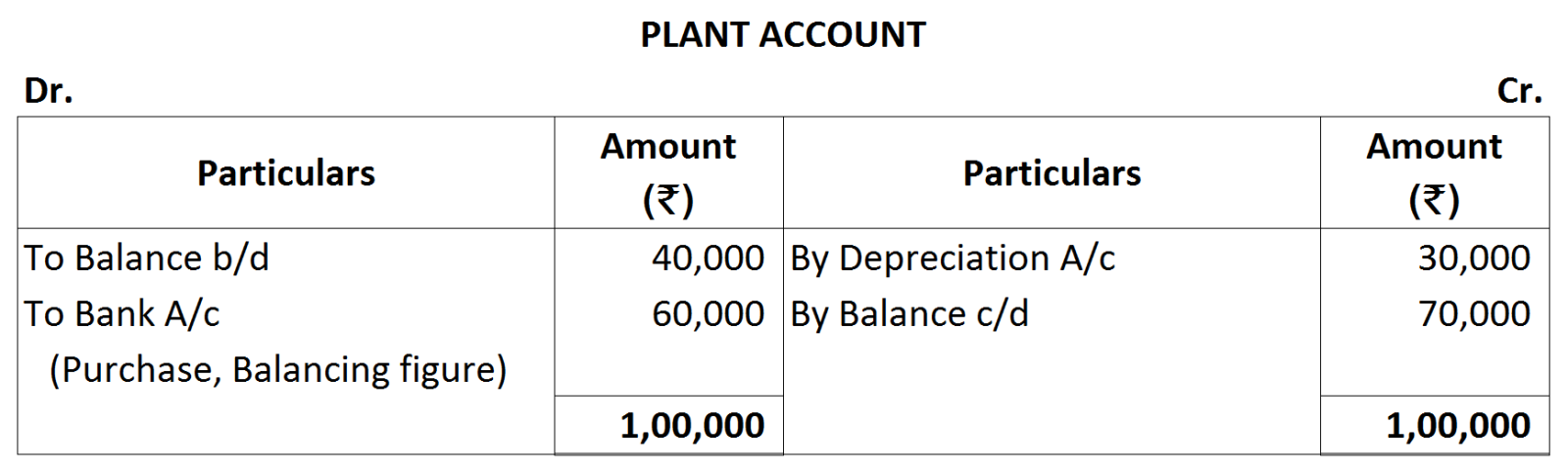

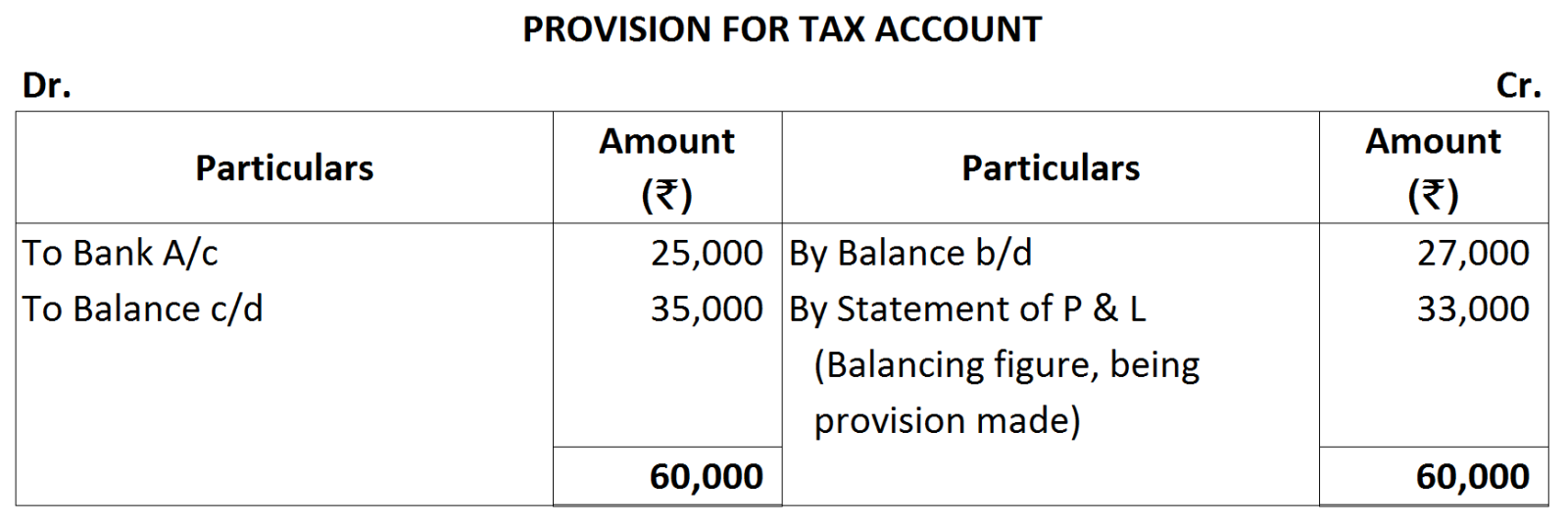

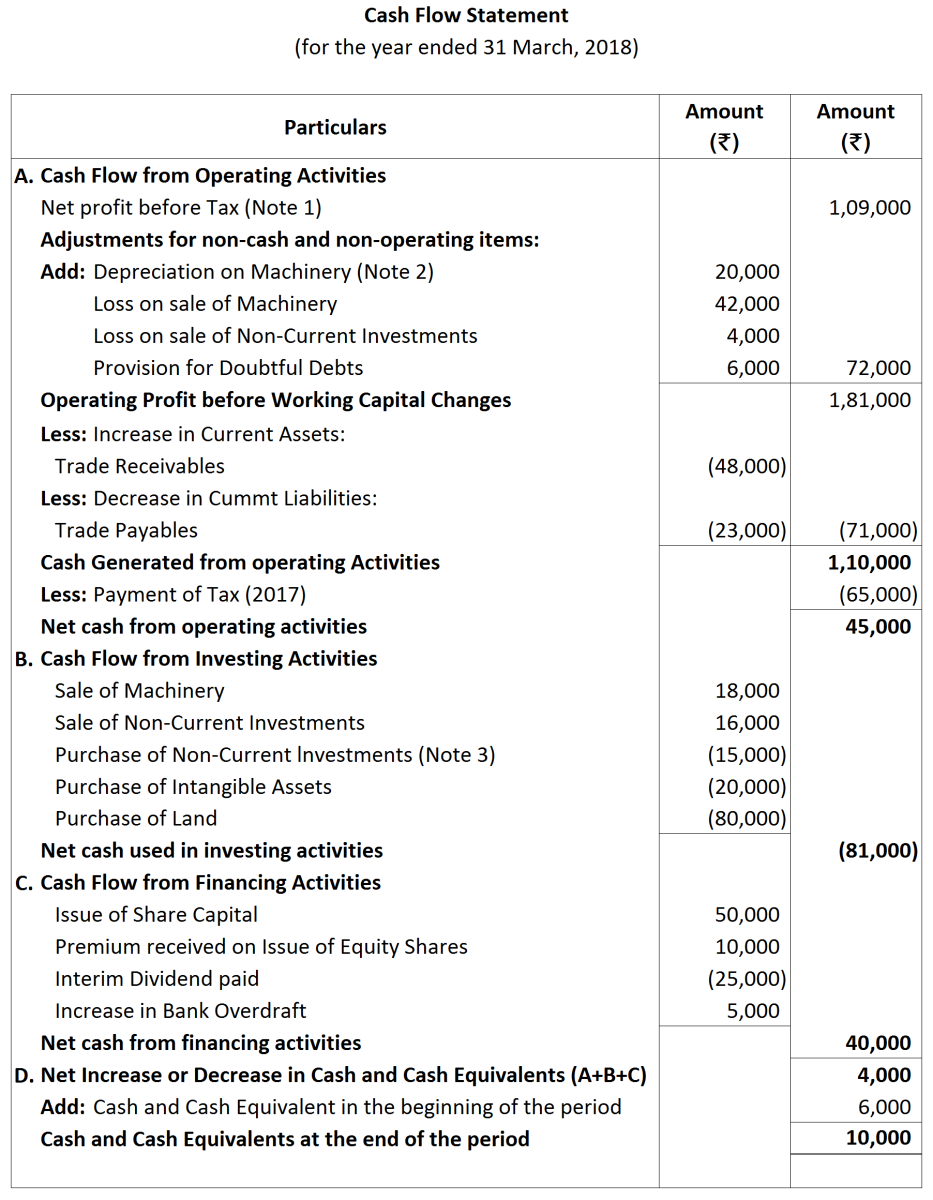

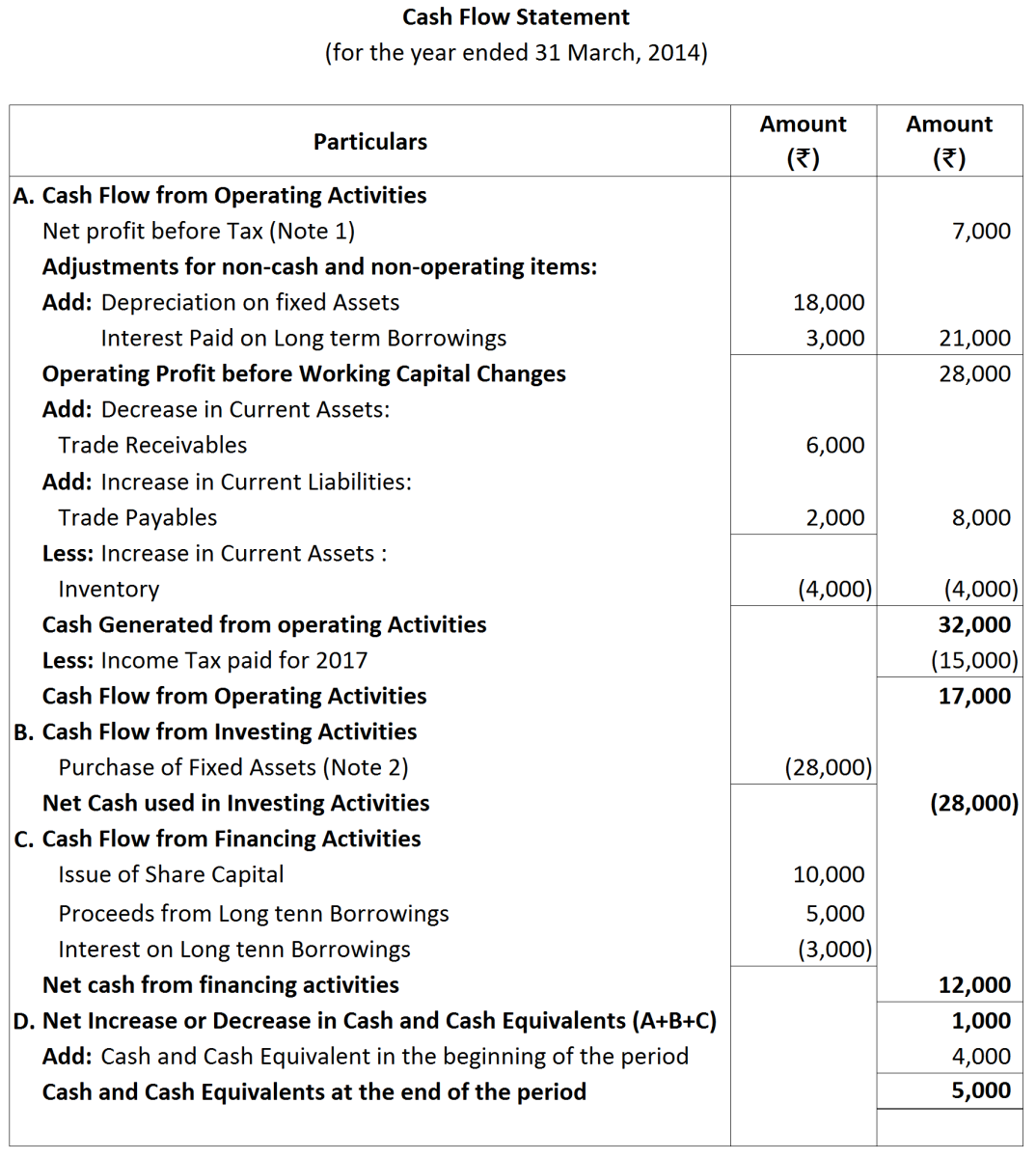

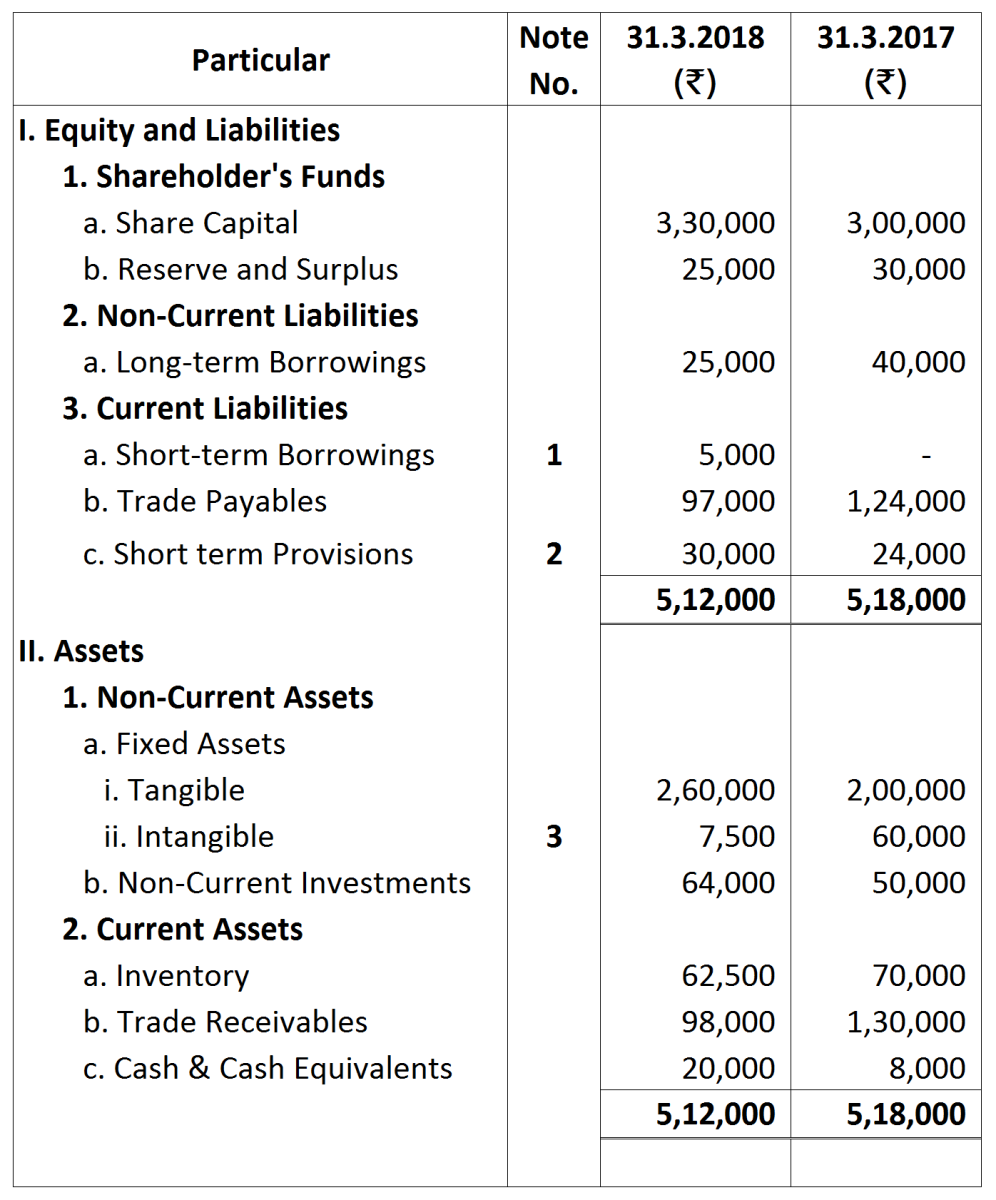

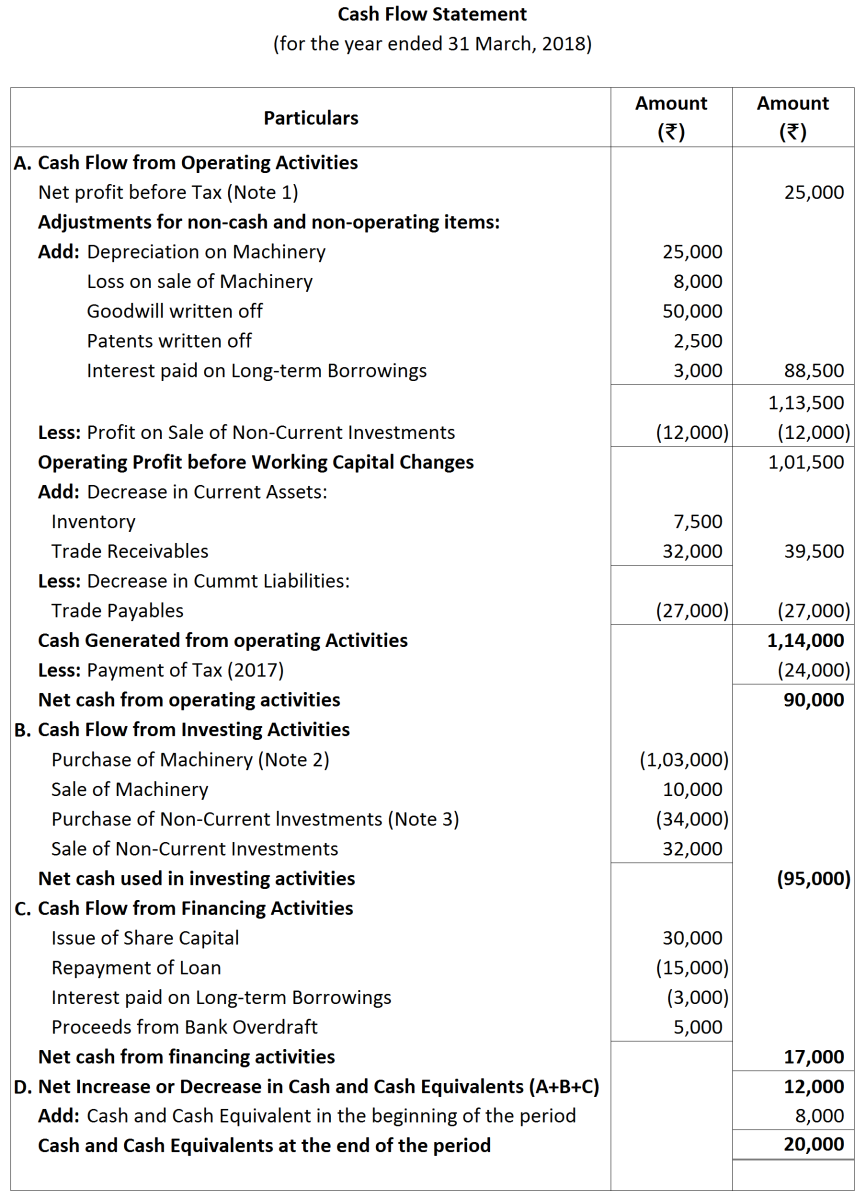

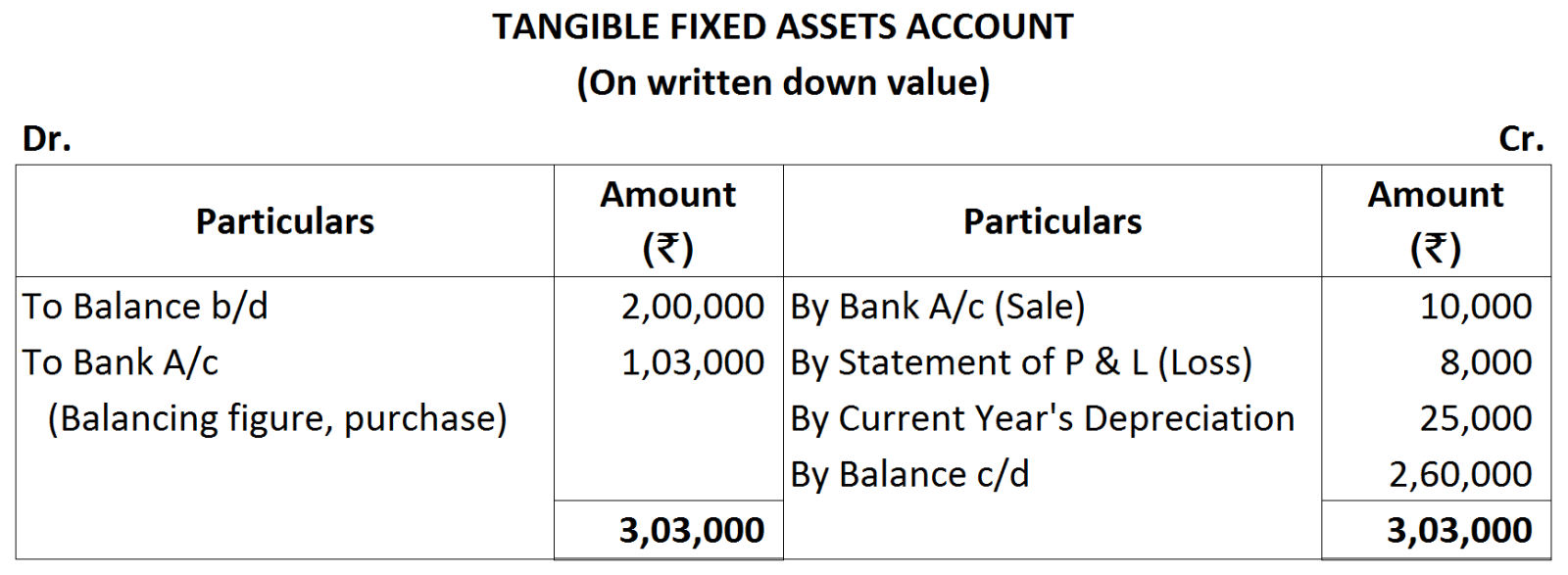

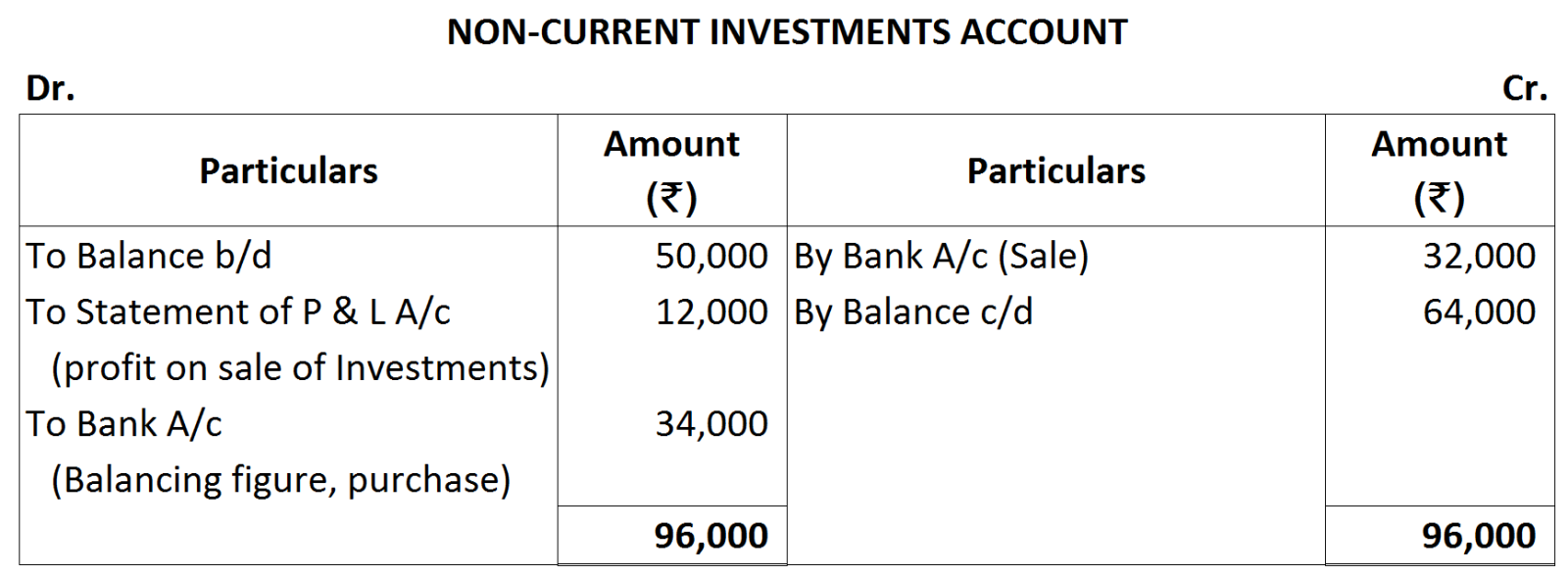

Question 16 Marks

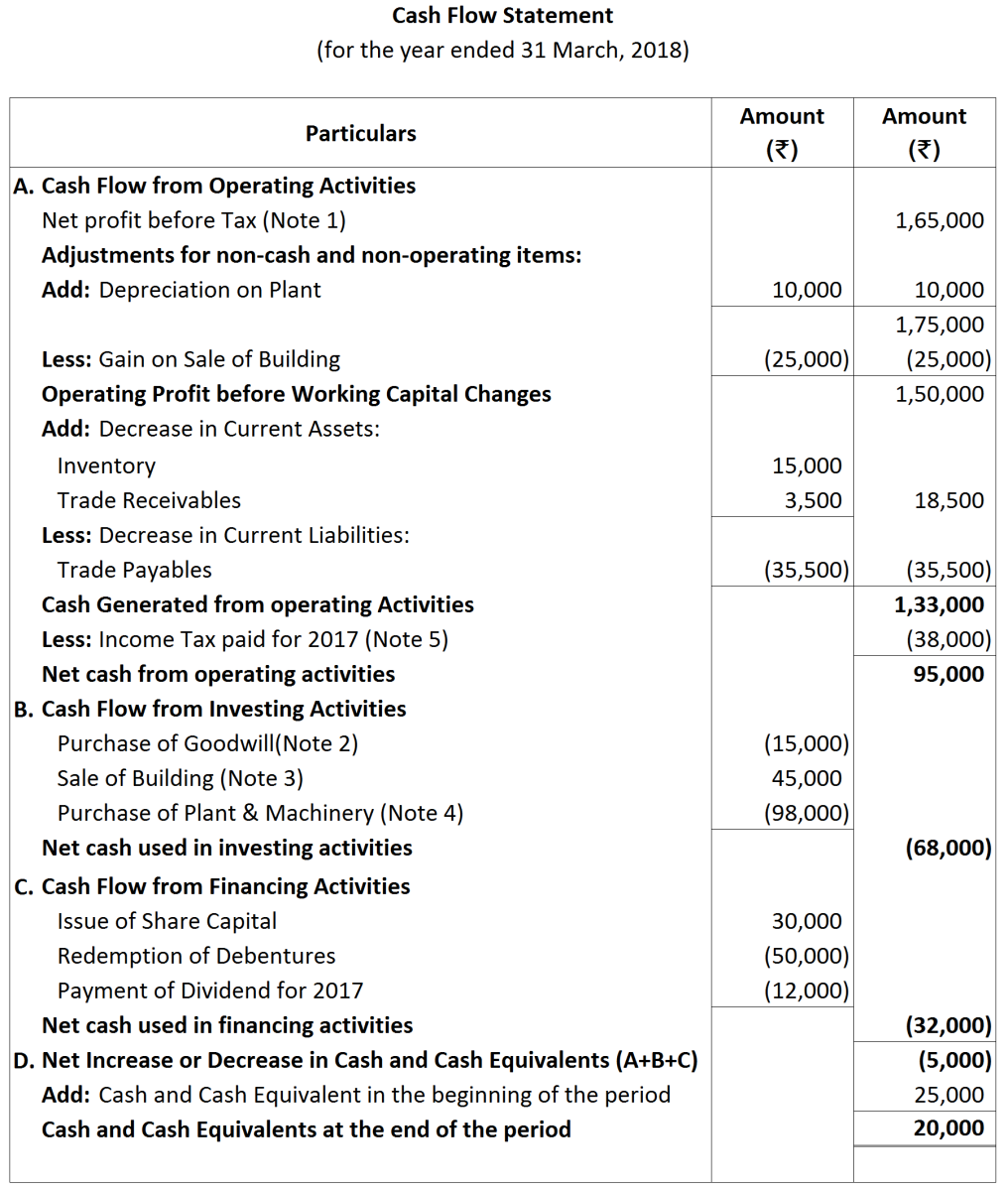

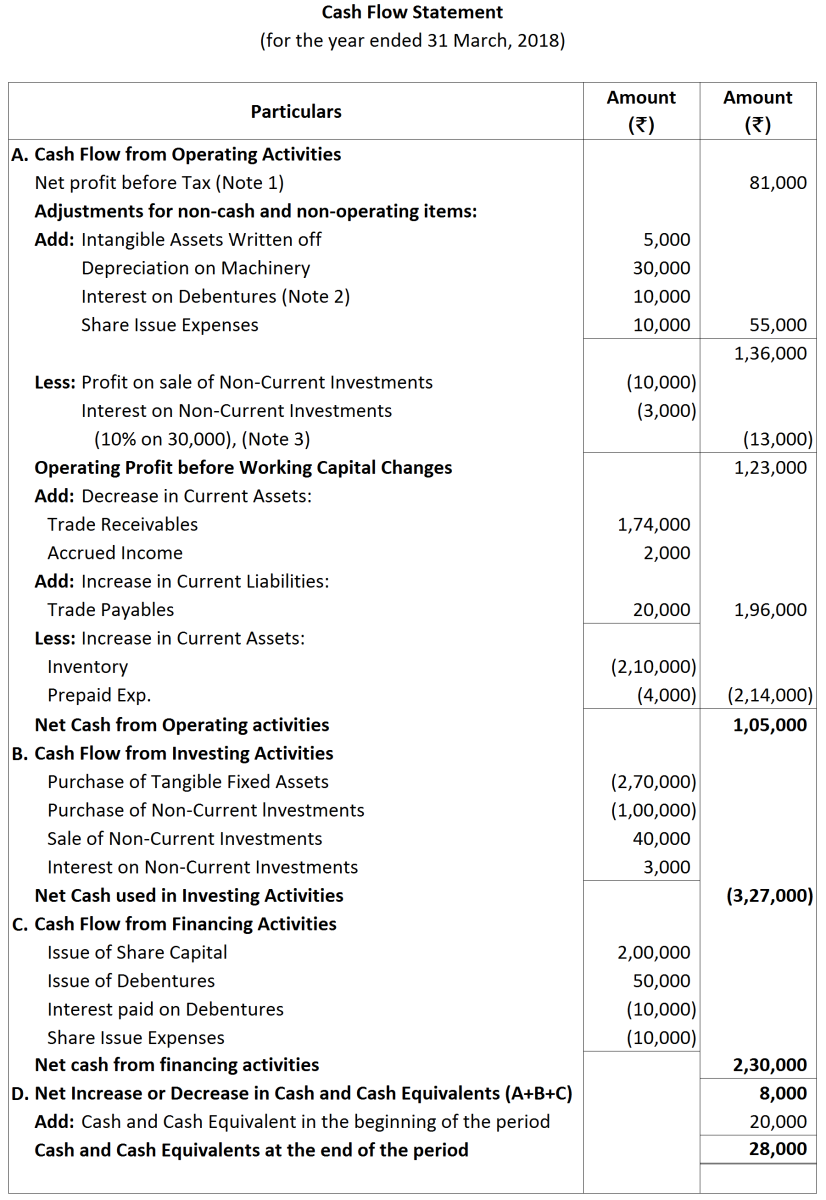

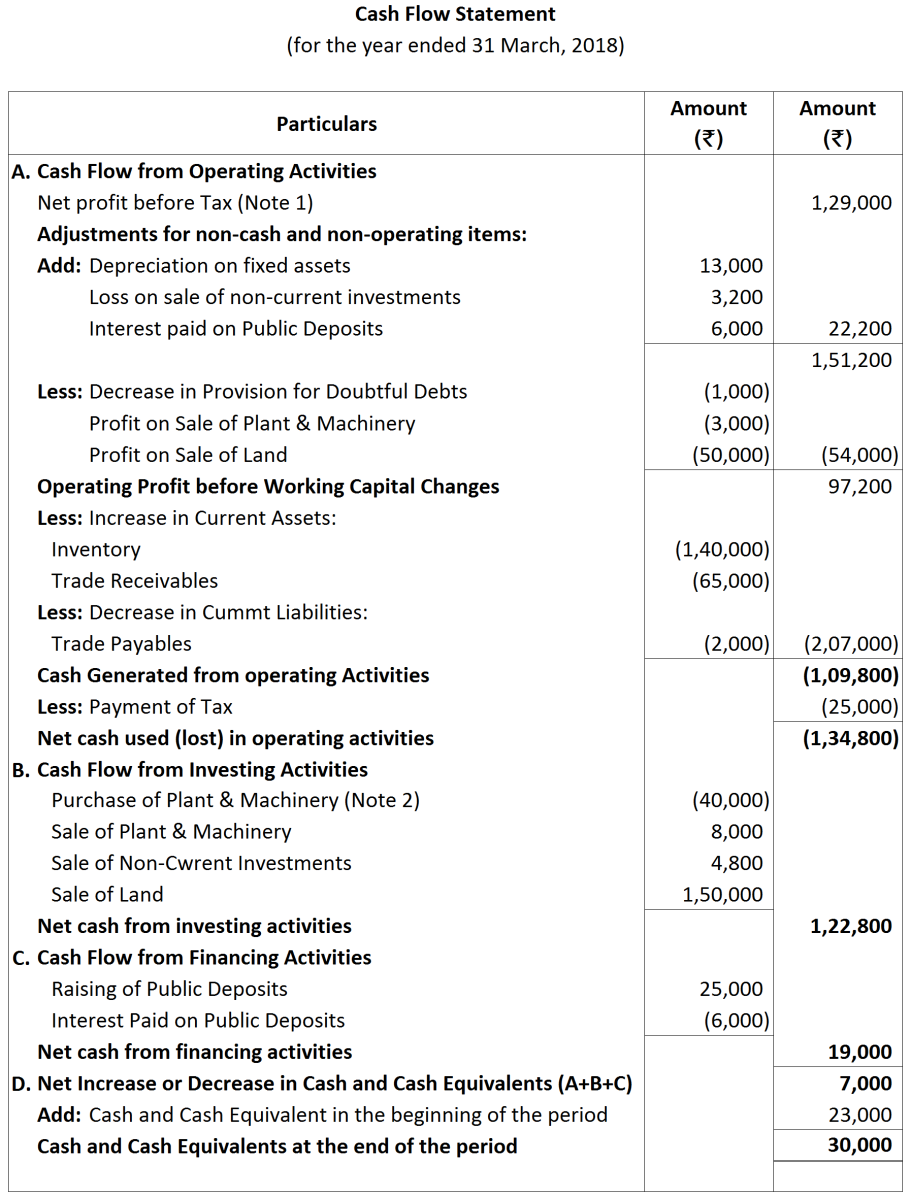

Prepare a format of 'cash flow statment' under indirect method.

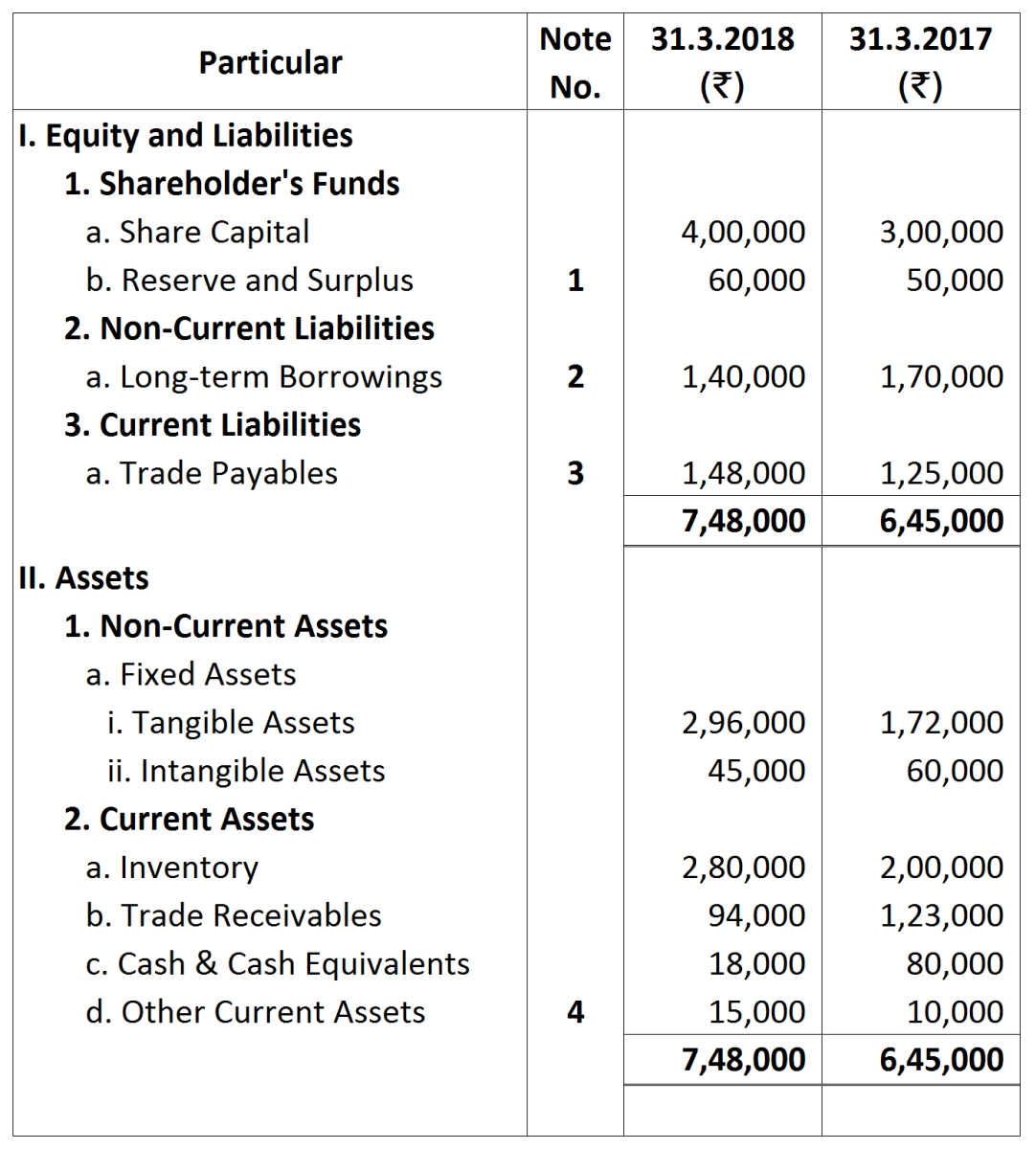

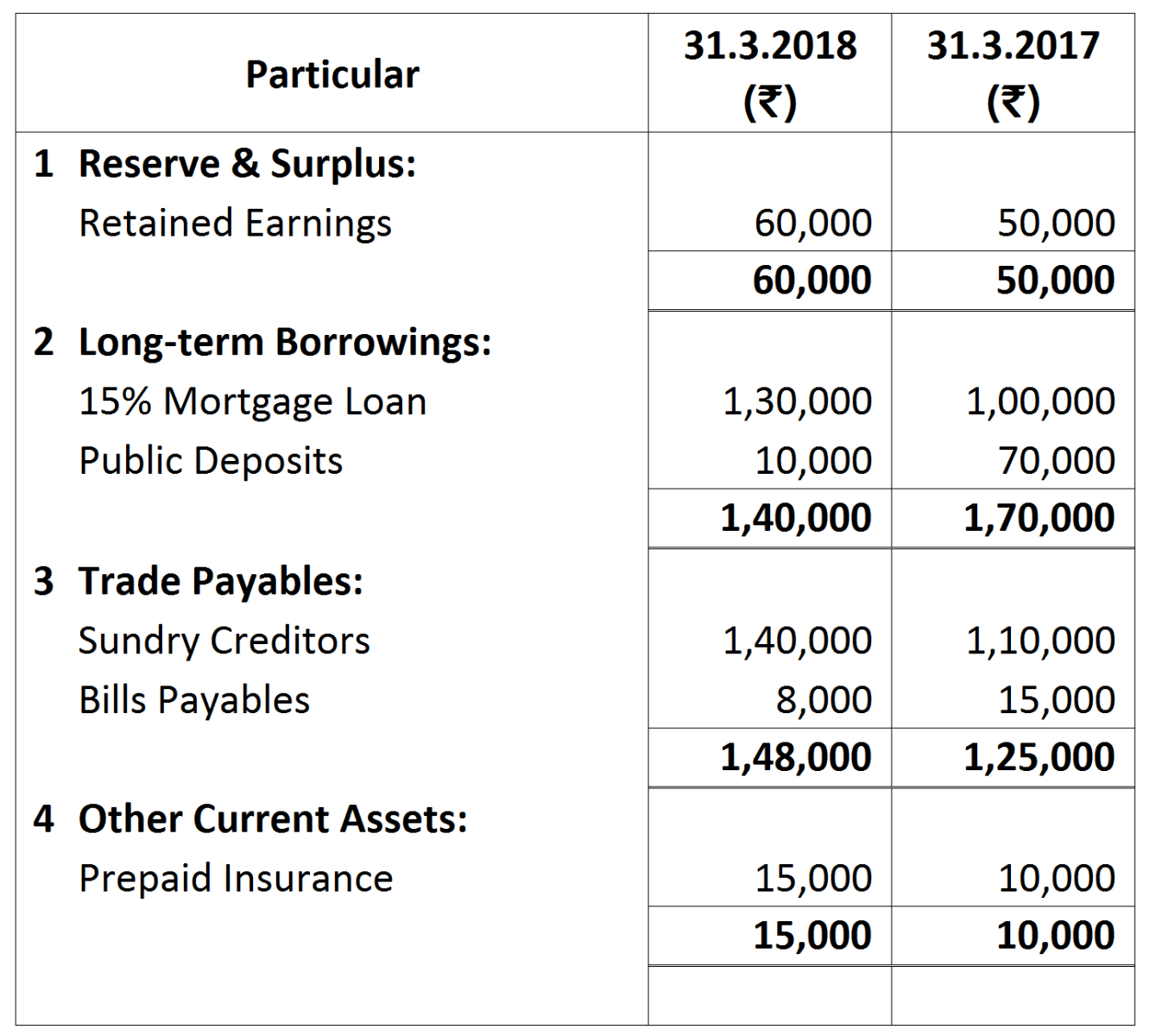

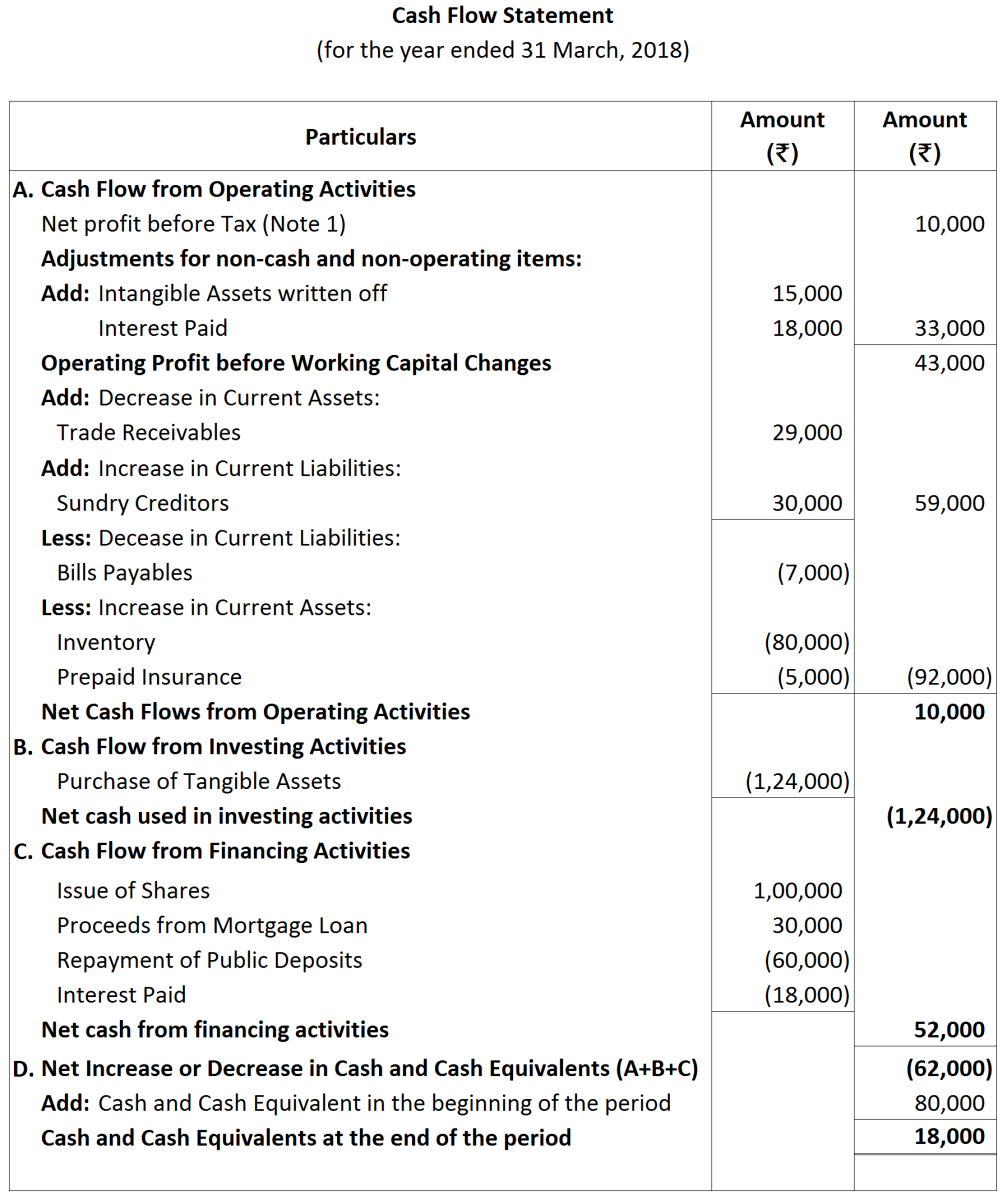

Answer

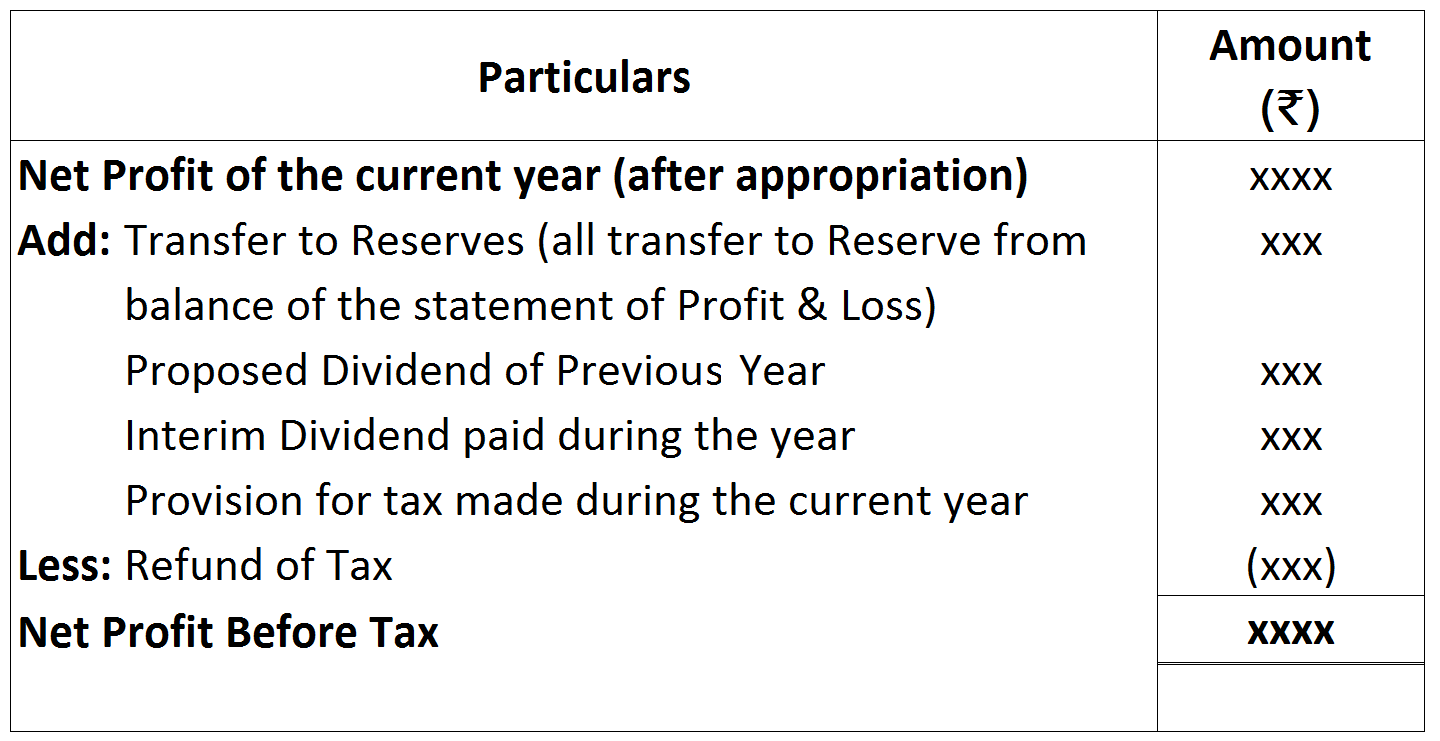

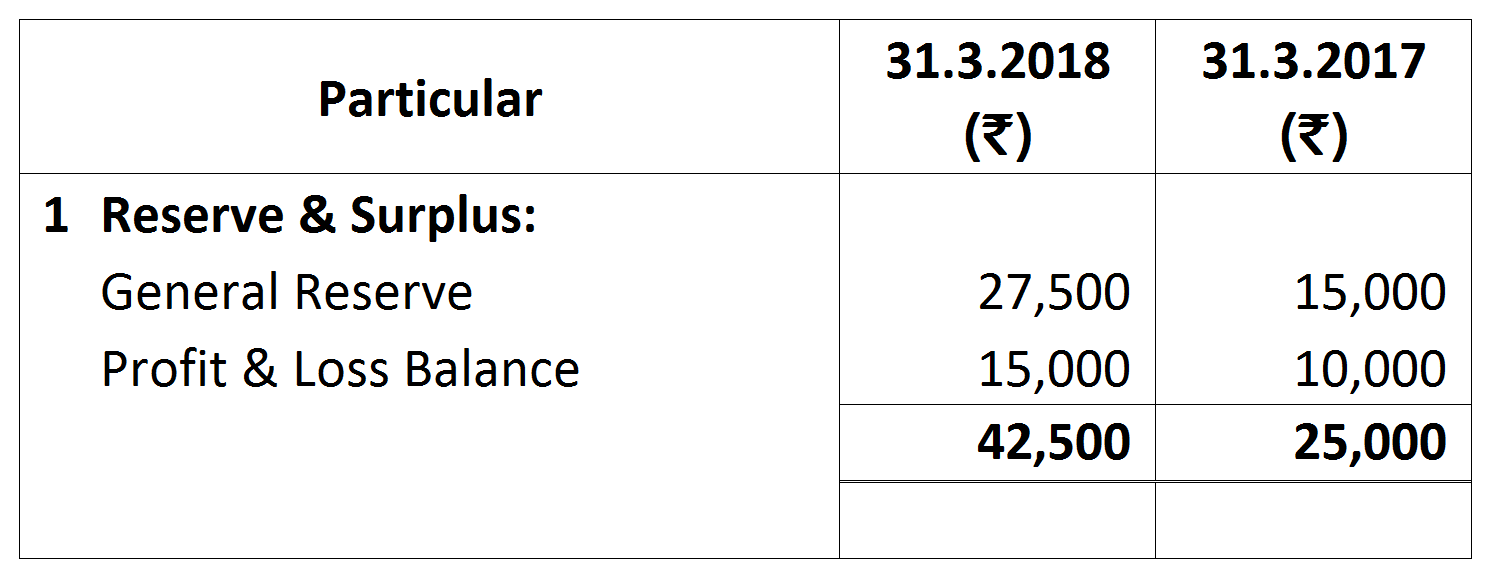

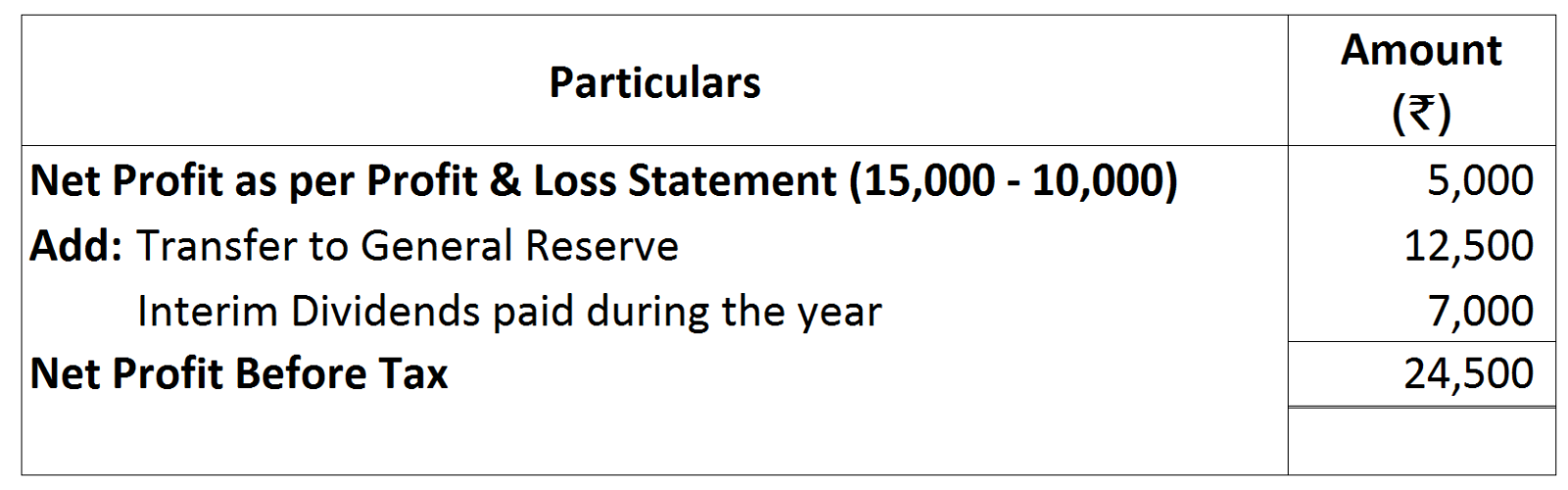

Note No. 1: Calculation of Net Profit before Tax:

Note No. 1: Calculation of Net Profit before Tax:

View full question & answer→Note No. 1: Calculation of Net Profit before Tax:46 questions · timed · auto-graded

Note No. 1: Calculation of Net Profit before Tax: Additional Information:

Additional Information:

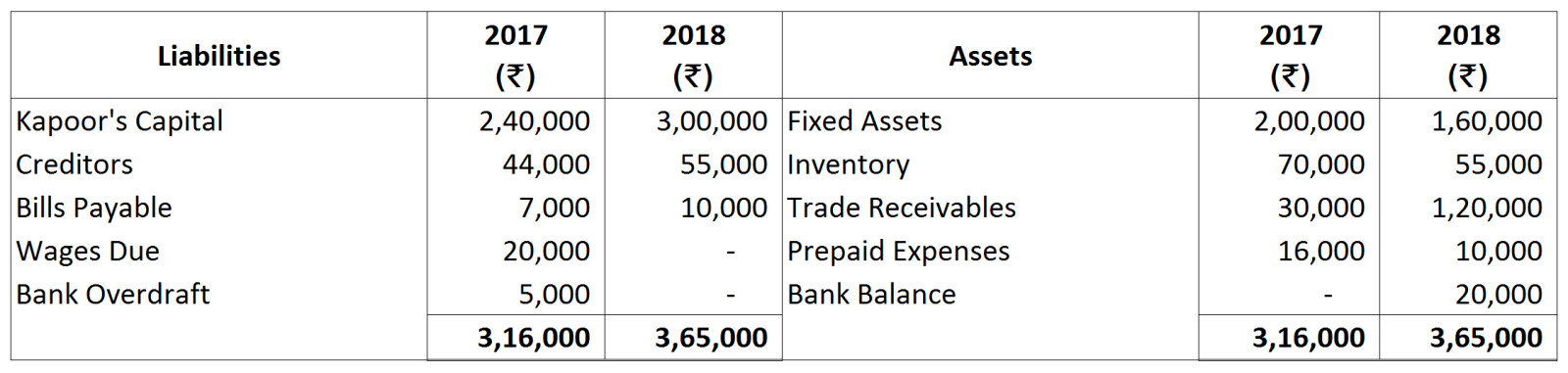

Note: No information is given in the question about the amount of net profit or net loss incurred during the year. As such, increase in proprietor's capital will be treated as net profit:

Note: No information is given in the question about the amount of net profit or net loss incurred during the year. As such, increase in proprietor's capital will be treated as net profit:

|

|

₹

|

|

Opening Capital

|

2,40,000

|

|

Less: Closing Capital

|

(3,00,000)

|

|

Net Profit

|

60,000

|

Debentures were redeemed on 1st April, 2017

Debentures were redeemed on 1st April, 2017 Notes:

Notes:

|

1.

|

Calculation of Net Profit before Tax:

|

₹

|

|

|

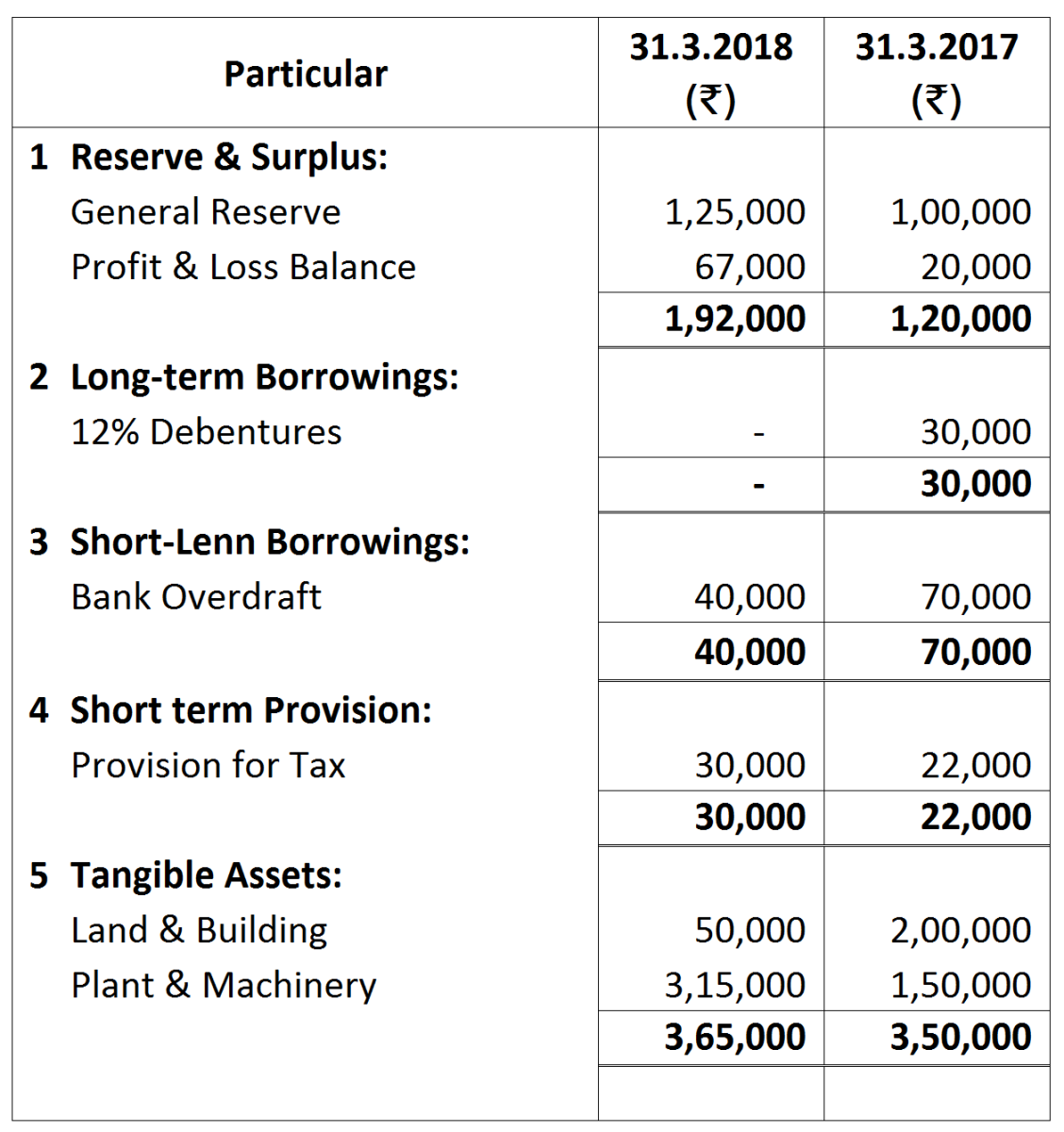

Profit & Loss Balance on 31st March, 2018

|

67,000

|

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(20,000)

|

|

|

|

47,000

|

|

|

Add: Transfer to General Reserve

|

25,000

|

|

|

Provision for Tax made during the Current year

|

30,000

|

|

|

Net Profit before Tax

|

1,02,000

|

|

2.

|

Decrease in the amount of Land & Building is treated as sale.

|

|

|

|

|

₹

|

|

1.

|

Interim Dividends paid during the year

|

7,000

|

|

2.

|

Plant Purchased

|

20,000

|

|

3.

|

Intangible Assets written off during the year

|

10,000

|

|

4.

|

Debentures redeemed on 1st Feb. 2018

|

12,000

|

|

5.

|

Interest on debentures has been paid up-to date

|

|

Note:

Note:

|

Calculation of Net Profit before Tax:

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2018

|

21,120

|

|

Less: Reserve & Surplus Balance on 31st March, 2017

|

(20,080)

|

|

|

1,040

|

|

Add: Dividend Paid

|

7,000

|

|

|

8,040

|

Notes:

Notes:

Note:

Note:

|

Retained Earnings on 31st March, 2018

|

60,000

|

|

Less: Retained Earnings on 31st March, 2017

|

(50,000)

|

|

Net profit before tax

|

10,000

|

Working note:

Working note:

Working Note:

Working Note:

Additional Information:

Additional Information:

Note:

Note:

|

Calculation of Net Profit before Tax:

|

₹

|

|

Profit & Loss Balance on 31st March, 2014

|

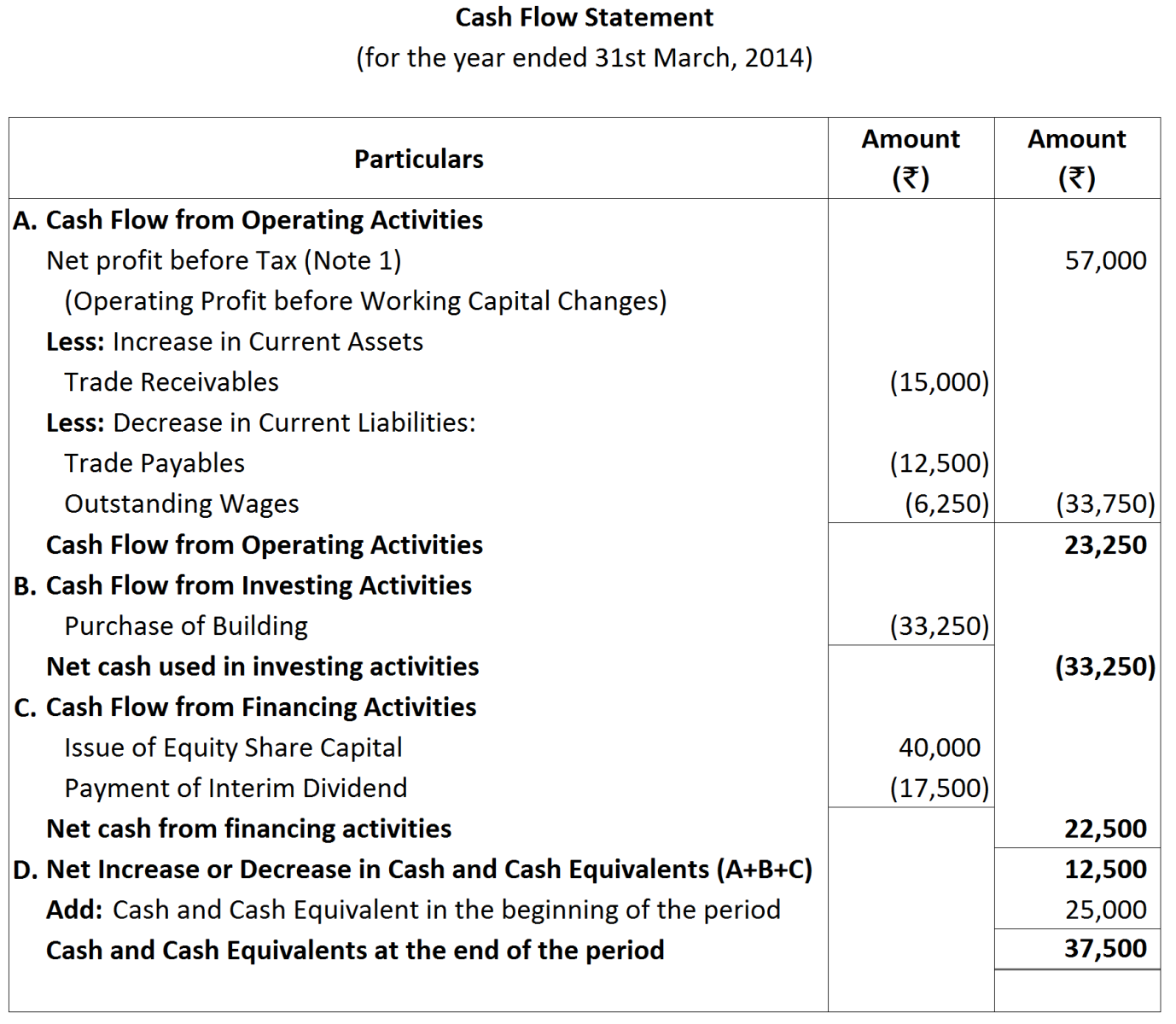

79,500

|

|

Less: Profit & Loss Balance on 31st March, 2013

|

(42,000)

|

|

|

37,500

|

|

Add: Transfer to General Reserve

|

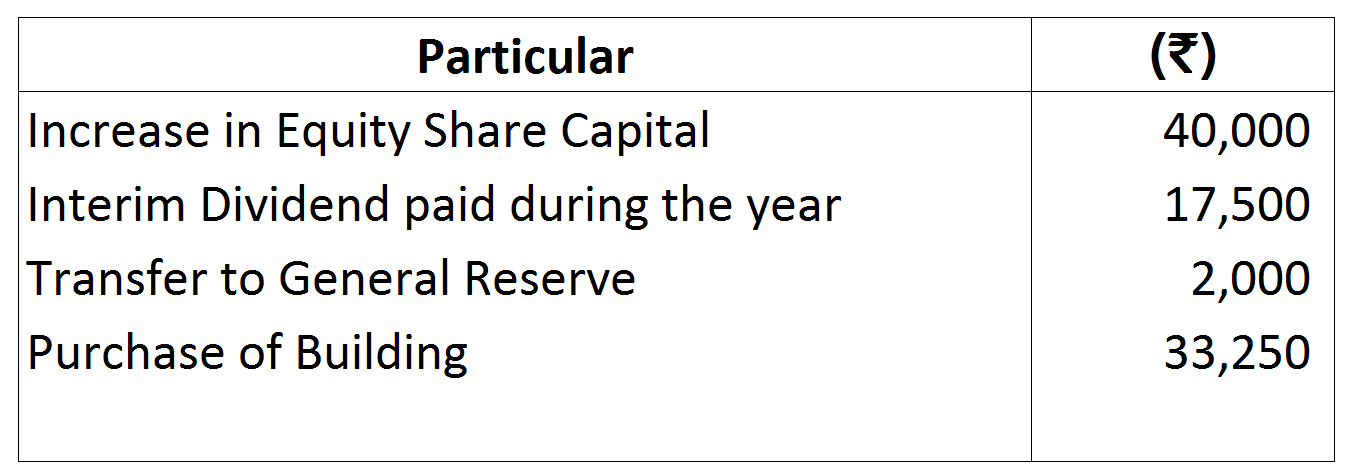

2,000

|

|

Dividend Paid

|

17,500

|

|

|

57,000

|

Working notes:

Working notes:

Note:

Note:

|

Net Profit for the year

|

40,000

|

|

Add: Transfer to General Reserve

|

15,000

|

|

Net Profit before Tax

|

55,000

|

|

1.

|

Contingent Liability:

|

31.3.2018

|

31.3.2017

|

|

|

|

₹

|

₹

|

|

|

Proposed Dividend

|

72,000

|

60,000

|

|

2.

|

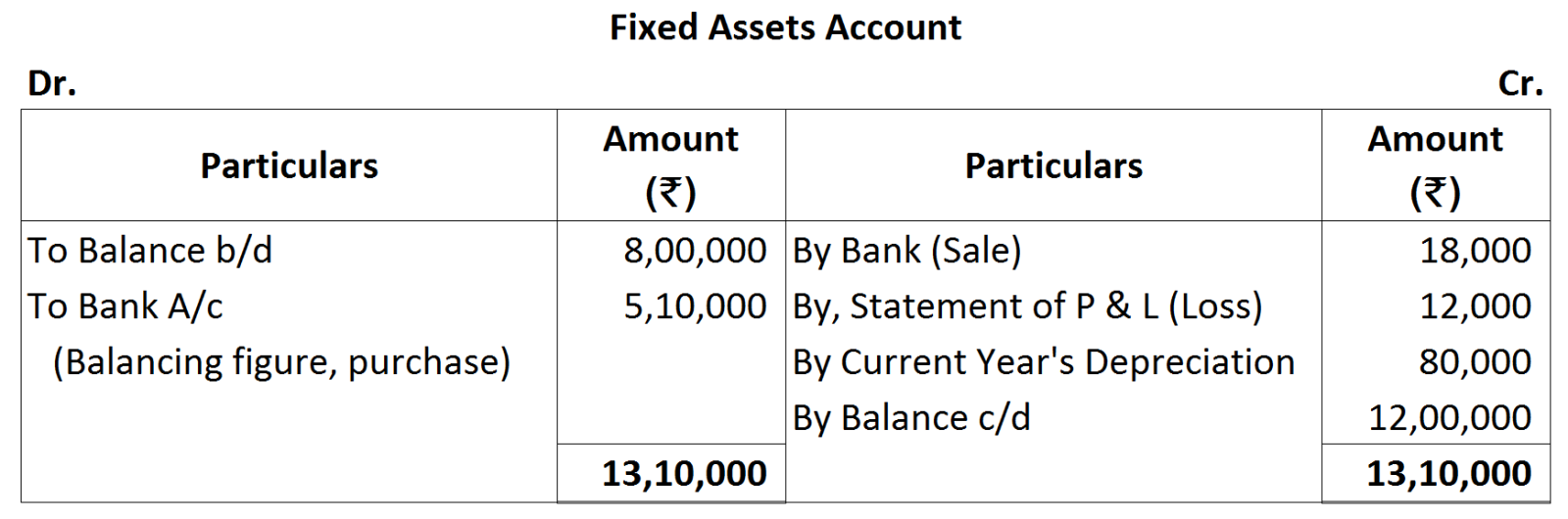

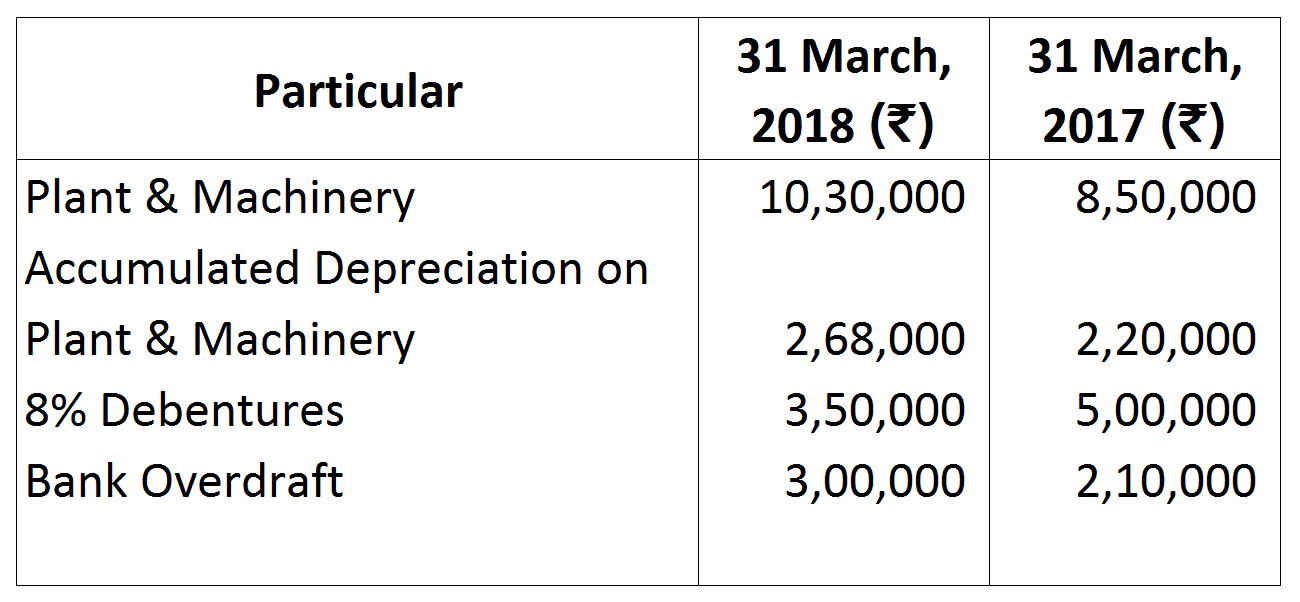

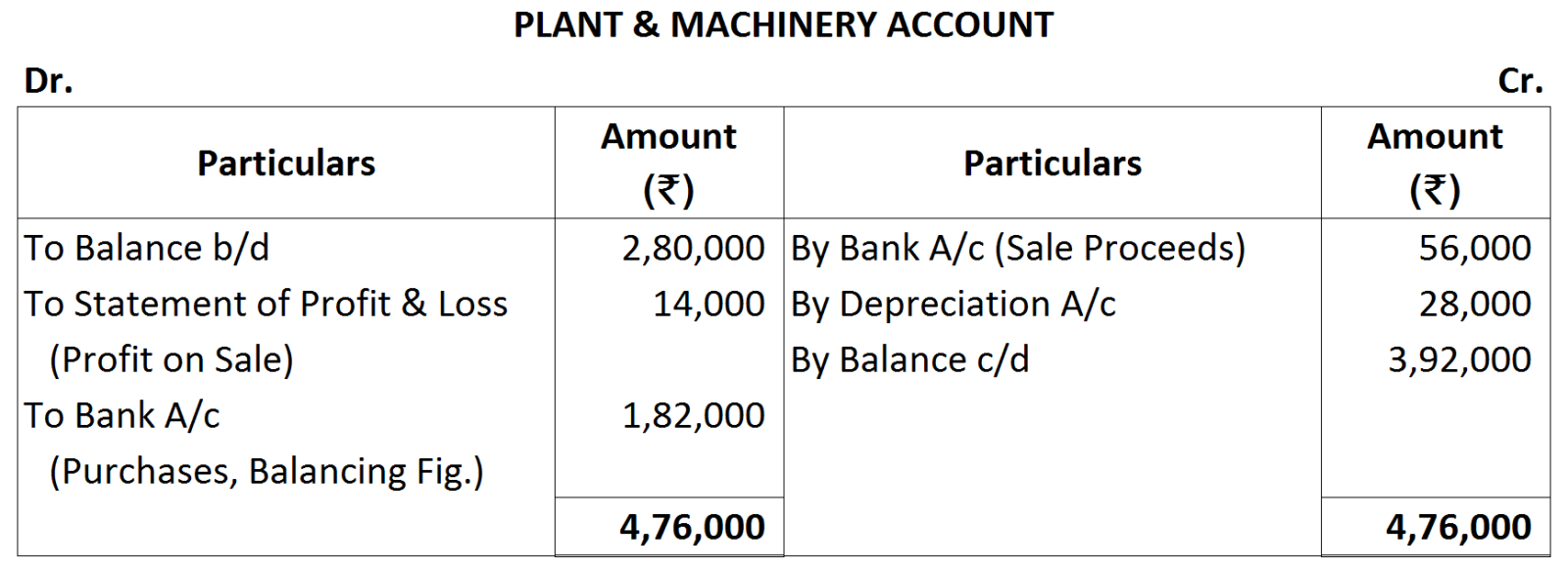

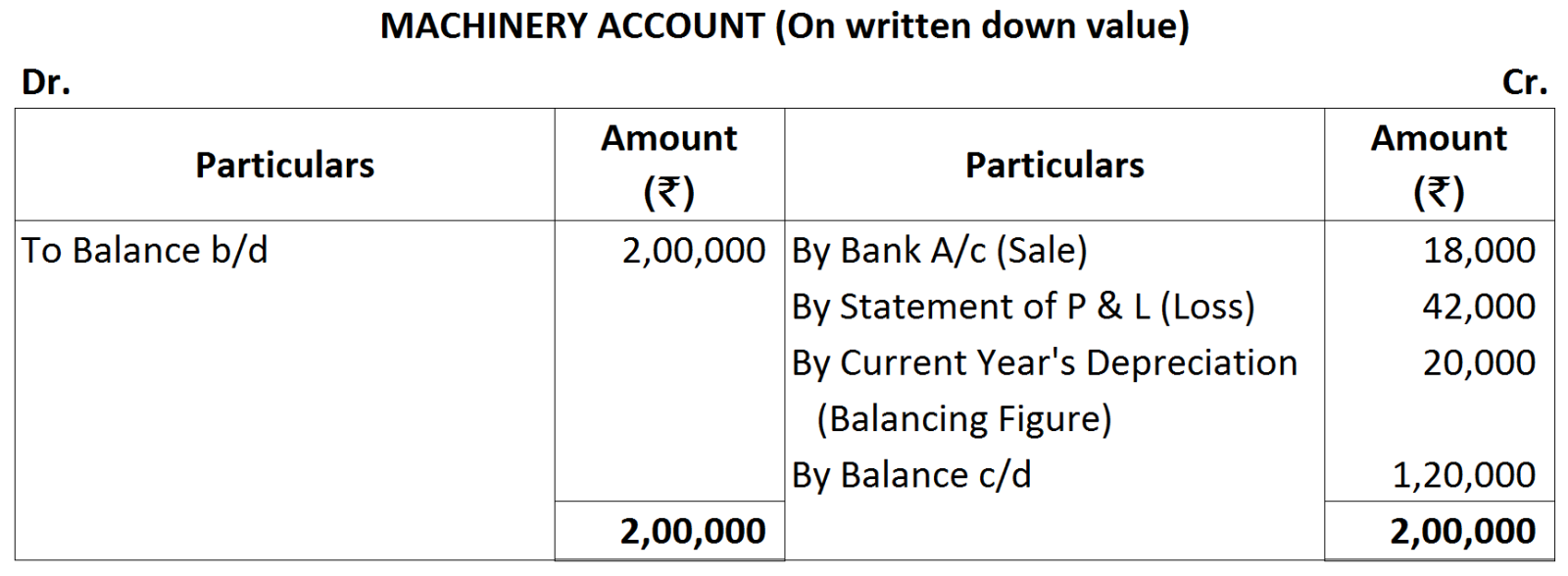

Depreciation charged during the year on Plant & Machinery amounted to ₹ 80,000.

|

||

|

3.

|

Machinery costing ₹ 80,000 (book value ₹ 30,000) was sold at a loss of 40% on book value.

|

||

Notes:

Notes:

|

|

₹

|

|

Profit & Loss Balance on 31 st March, 2018

|

2,90,000

|

|

Less: Profit & Loss Balance on 31st March, 20 I 7

|

(1,80,000)

|

|

|

1,10,000

|

|

Add: Transfer to General Reserve

|

50,000

|

|

Proposed Dividend for Previous year

|

60,000

|

|

|

2,20,000

|

Working Notes:

Working Notes:

|

|

₹

|

|

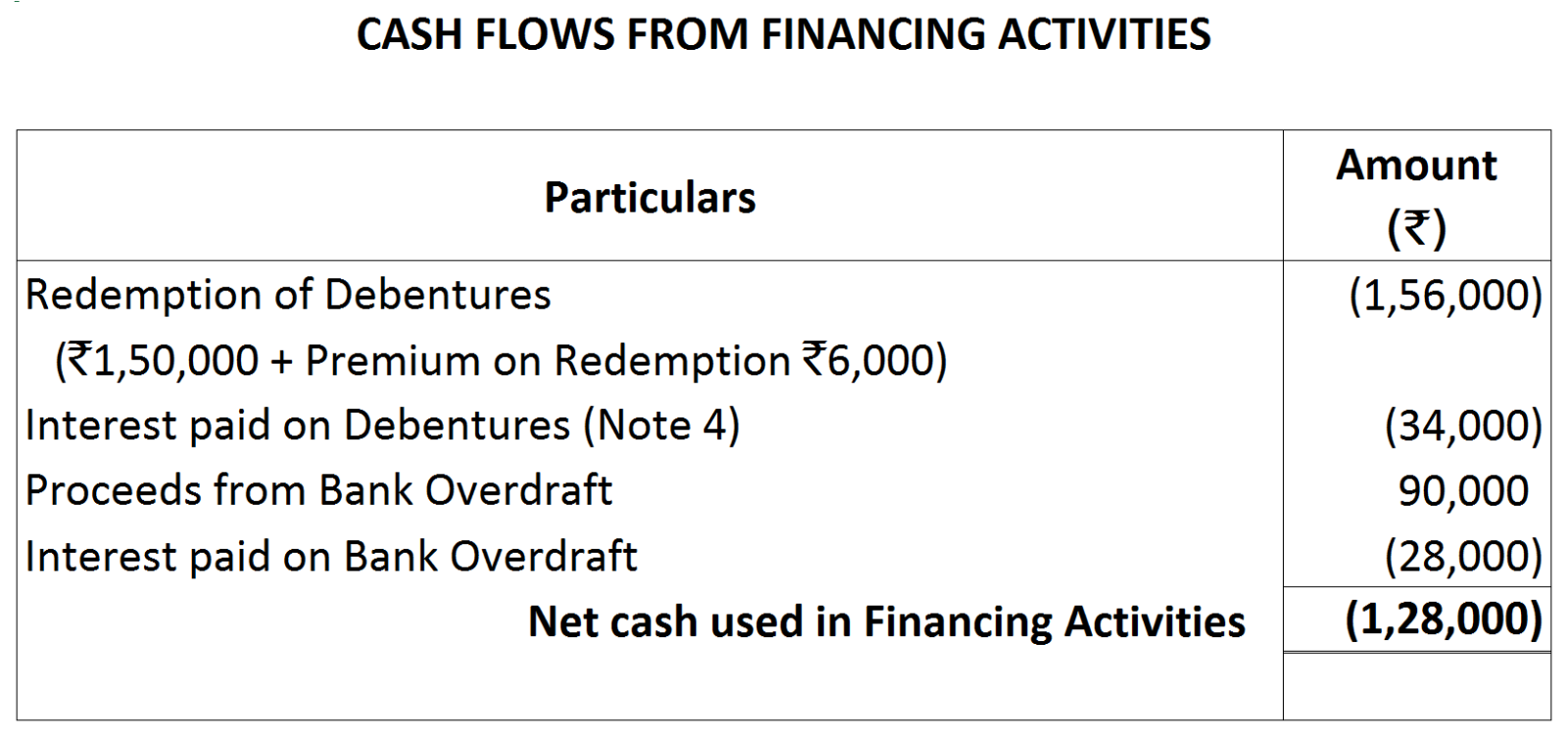

8% on ₹ 5,00,000 for six months

|

20,000

|

|

8% on ₹ 3,50,000 for six months

|

14,000

|

|

|

34,000

|

Note:

Note:

|

Calculation of Net Profit before Tax:

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2018

|

70,000

|

|

Less: Reserve & Surplus Balance on 31st March, 2017

|

50,000

|

|

|

20,000

|

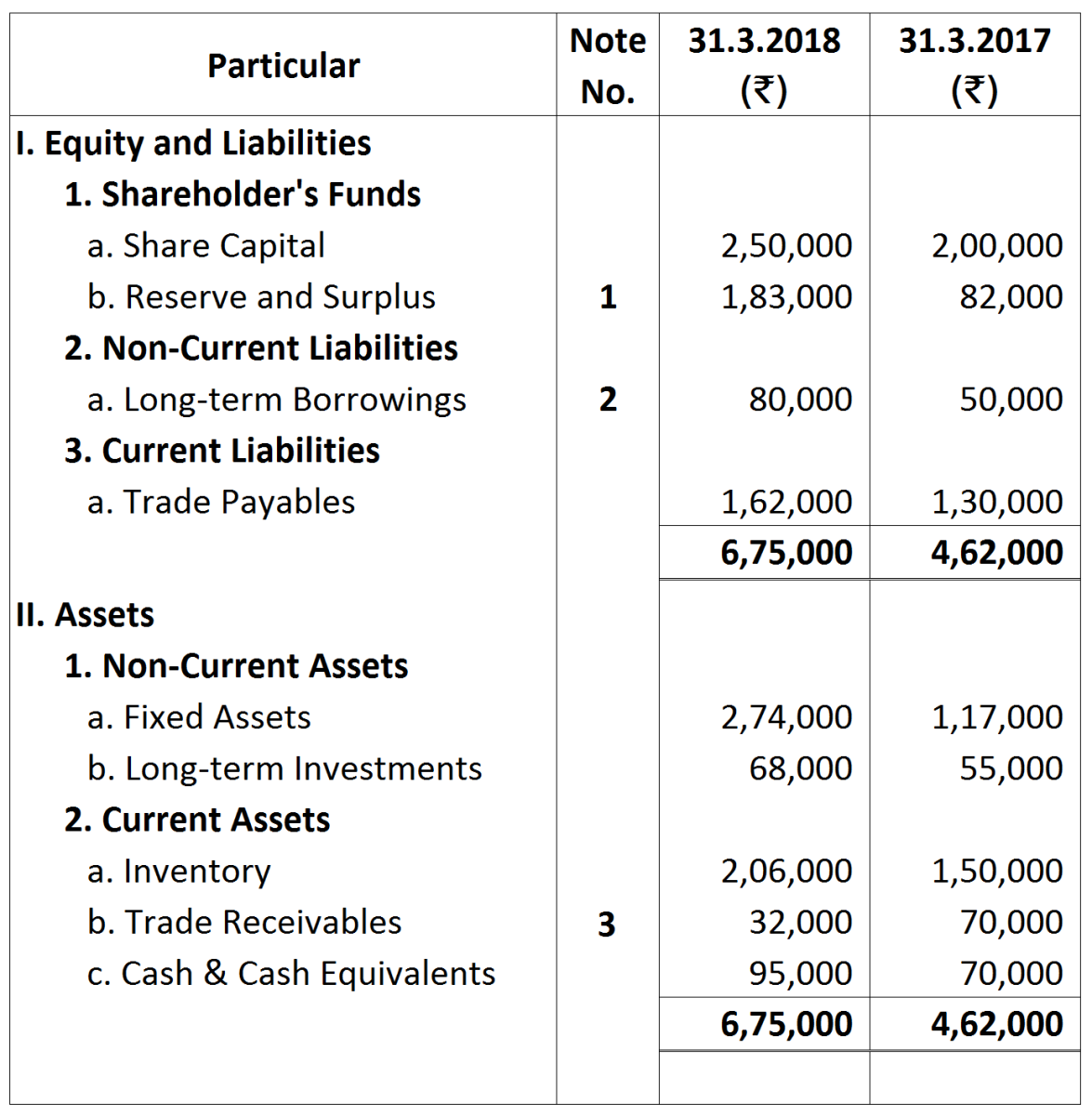

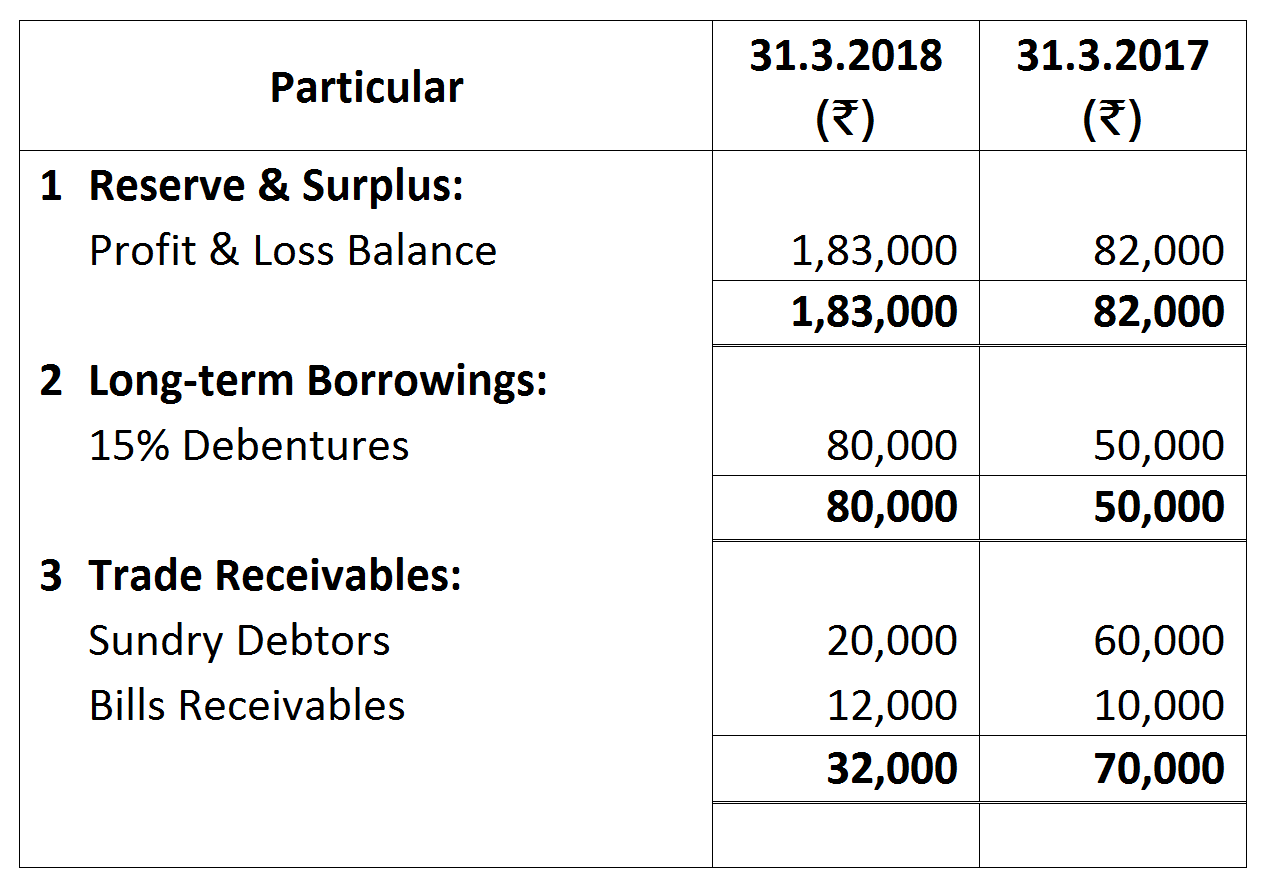

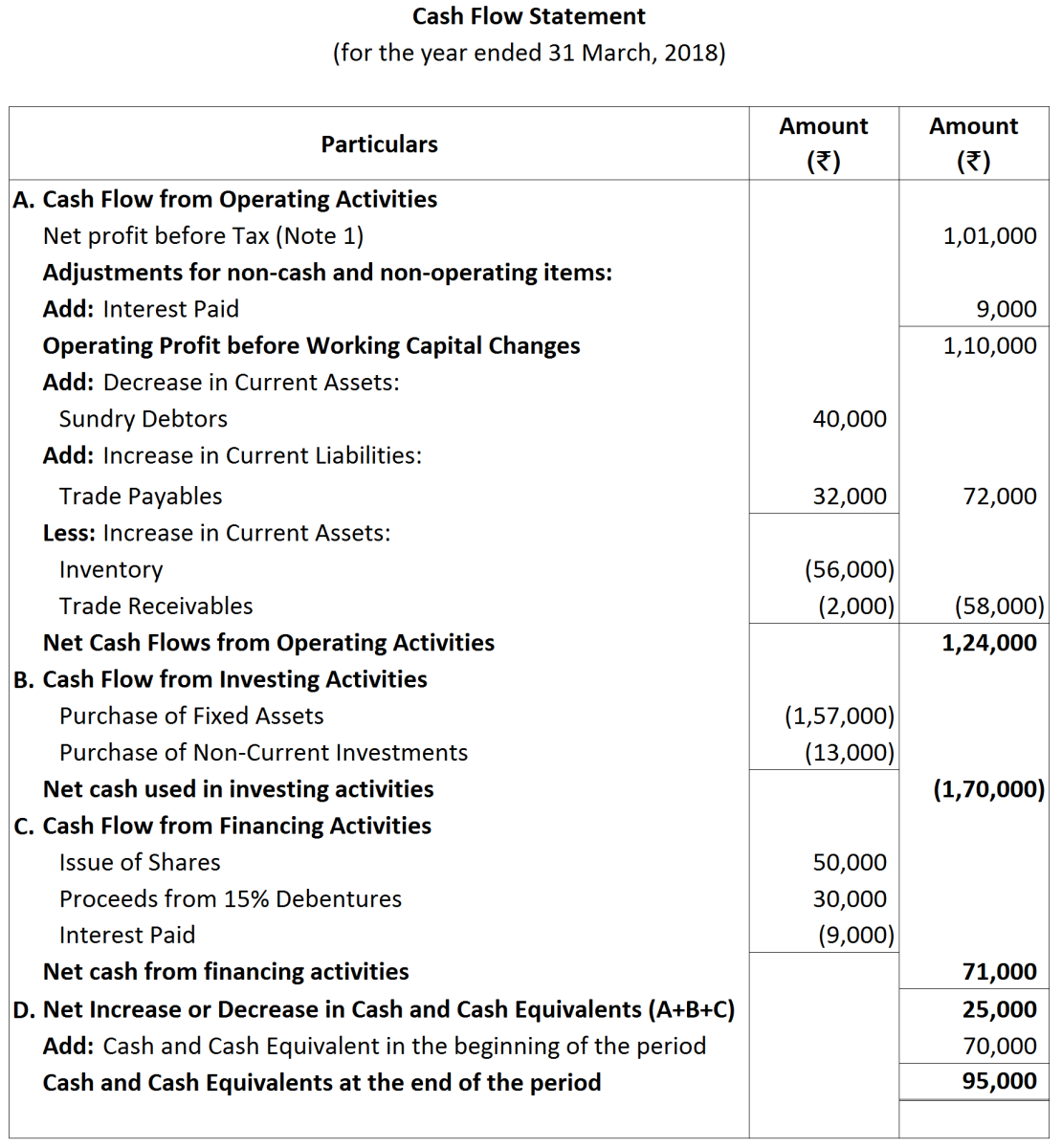

Interest paid on debentures amounted to ₹ 9,000.

Interest paid on debentures amounted to ₹ 9,000. Note:

Note:

|

|

₹

|

|

Profit & Loss Balance on 31.3.2018

|

1,83,000

|

|

Less: Profit & Loss Balance on 31.3.2017

|

(82,000)

|

|

Net Profit before Tax

|

1,01,000

|

Additional Information:

Additional Information:

|

Contingent Liability:

|

31.3.2018

|

31.3.2017

|

|

|

₹

|

₹

|

|

Proposed Dividend

|

20,200

|

11,200

|

Note:

Note:

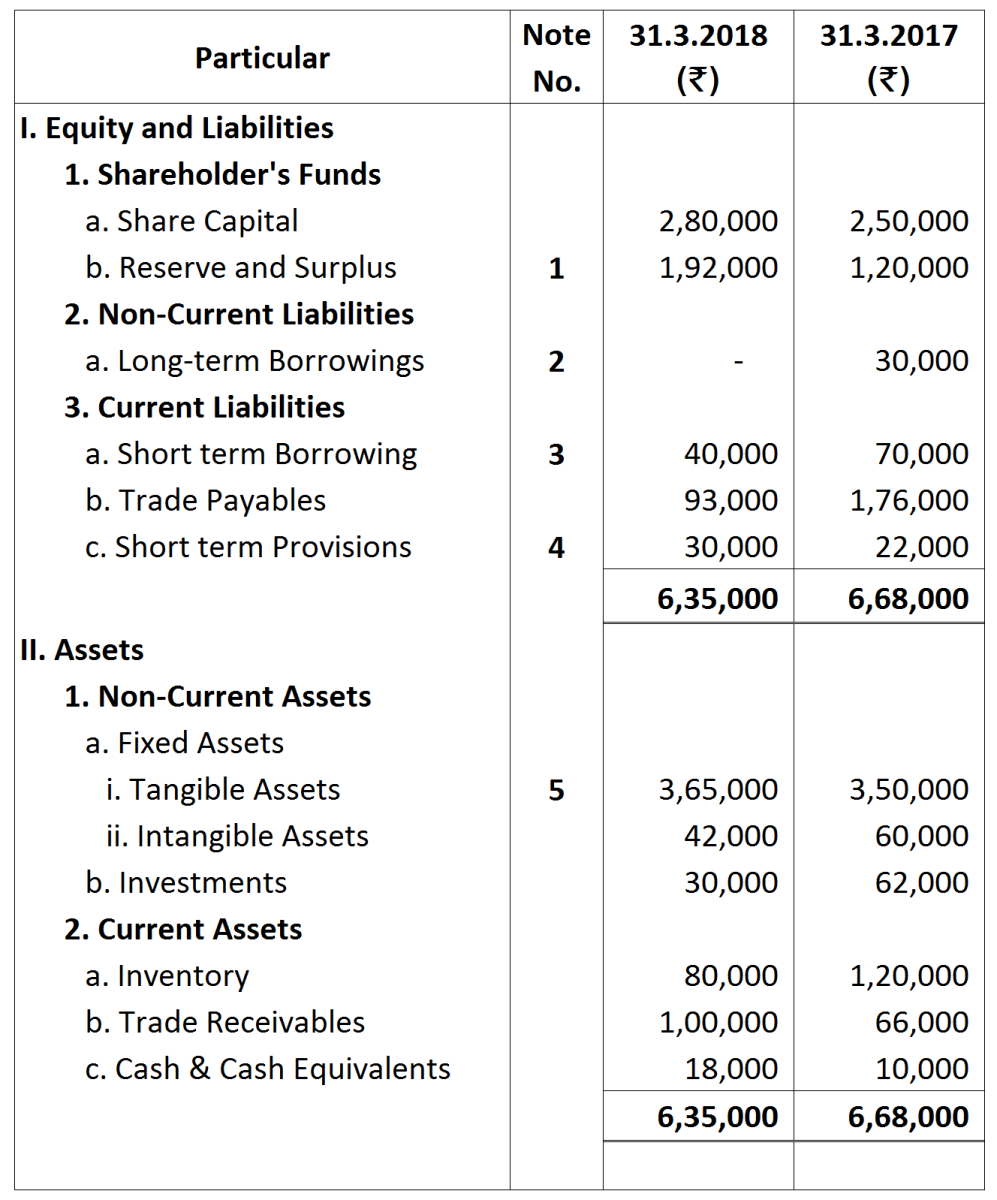

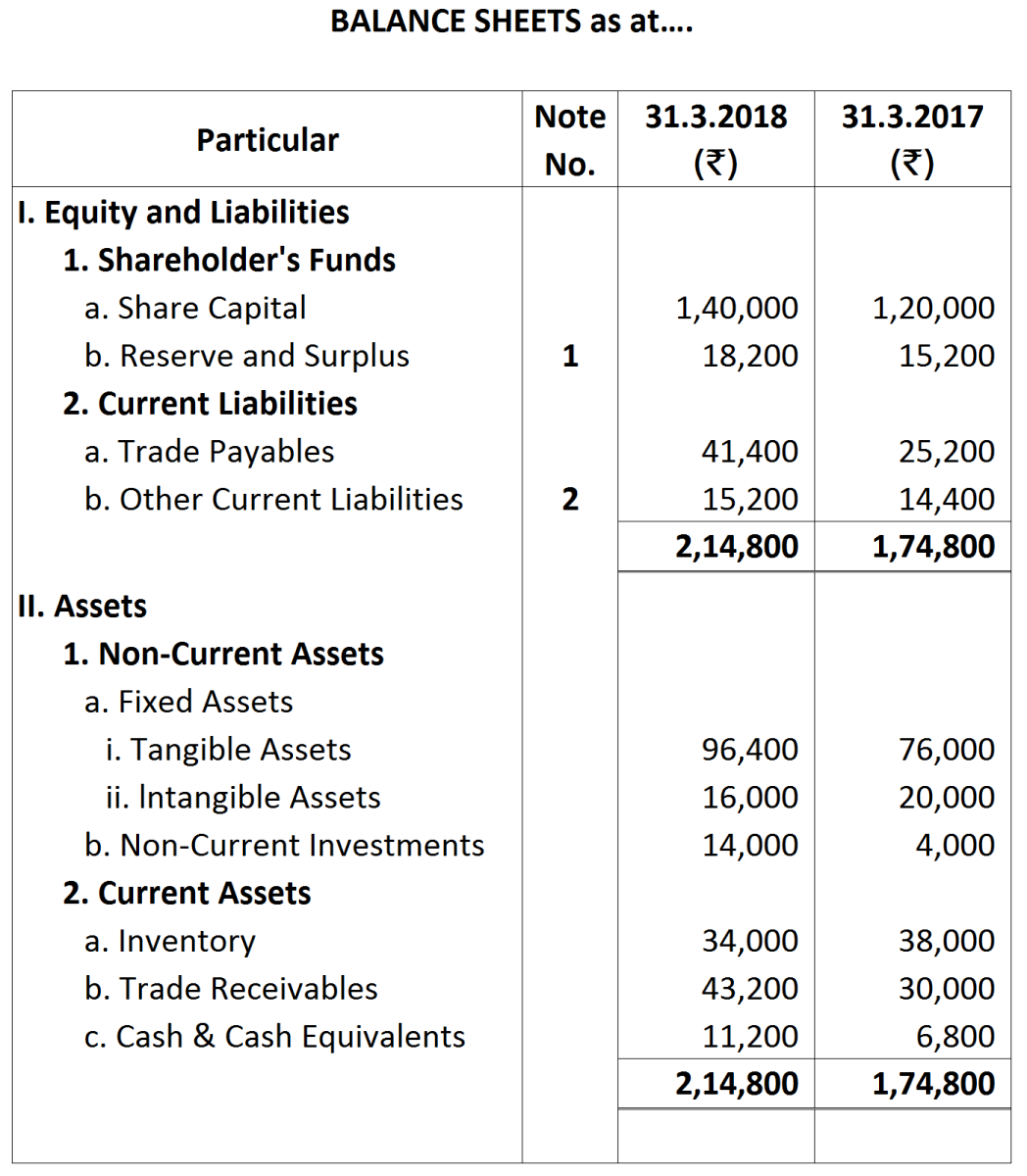

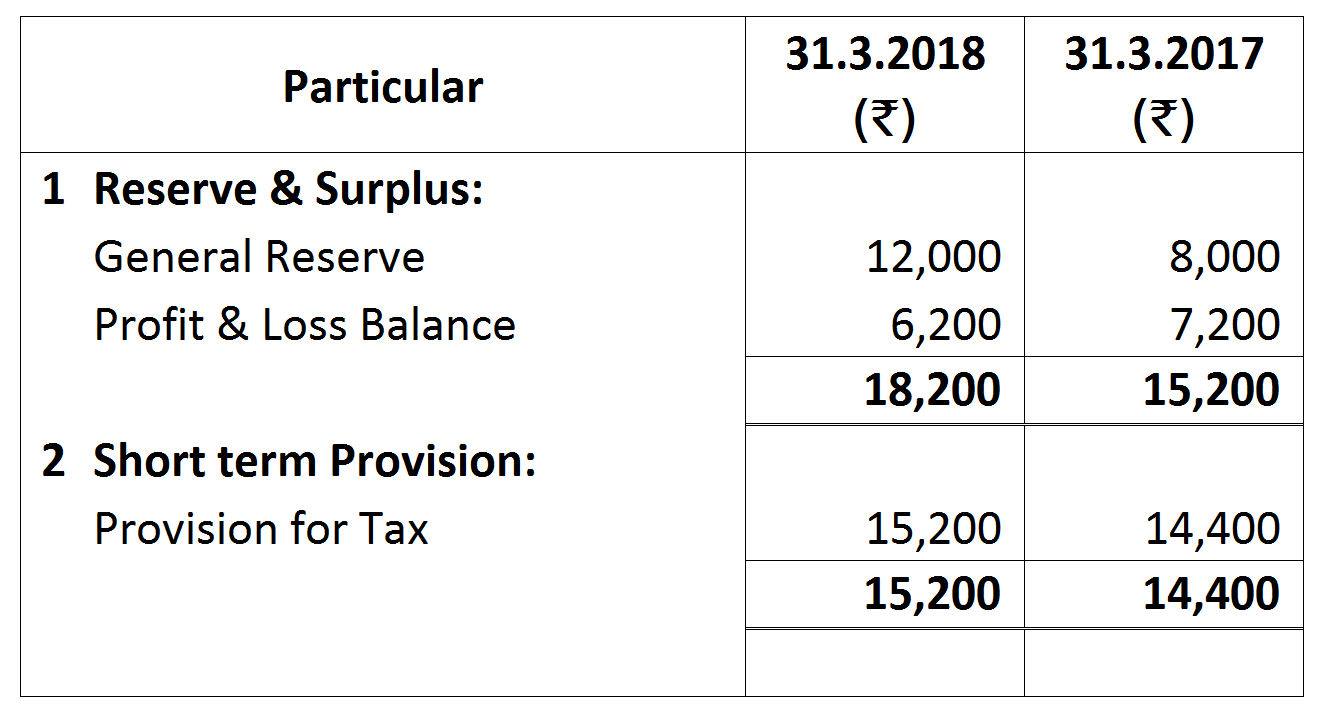

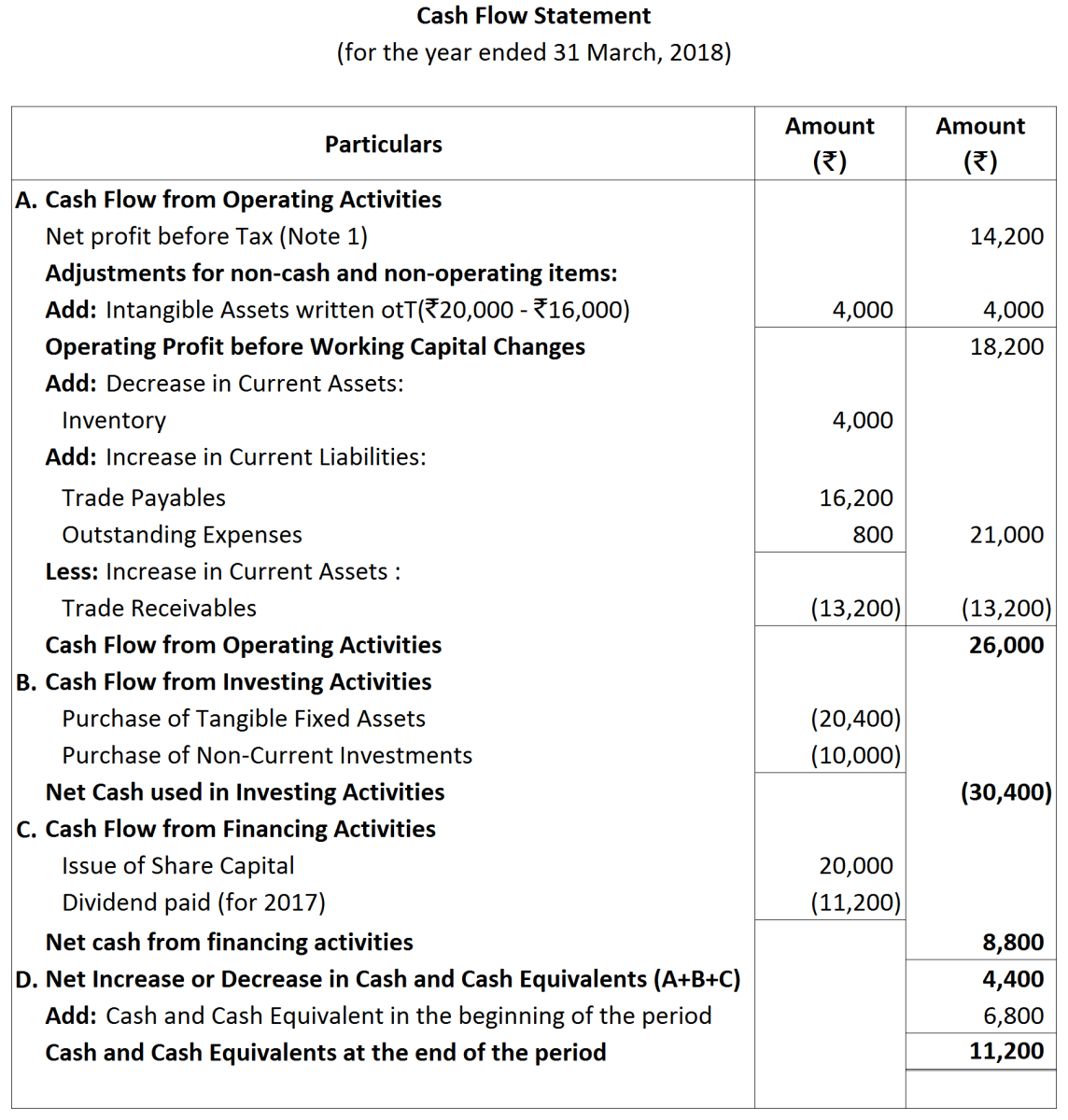

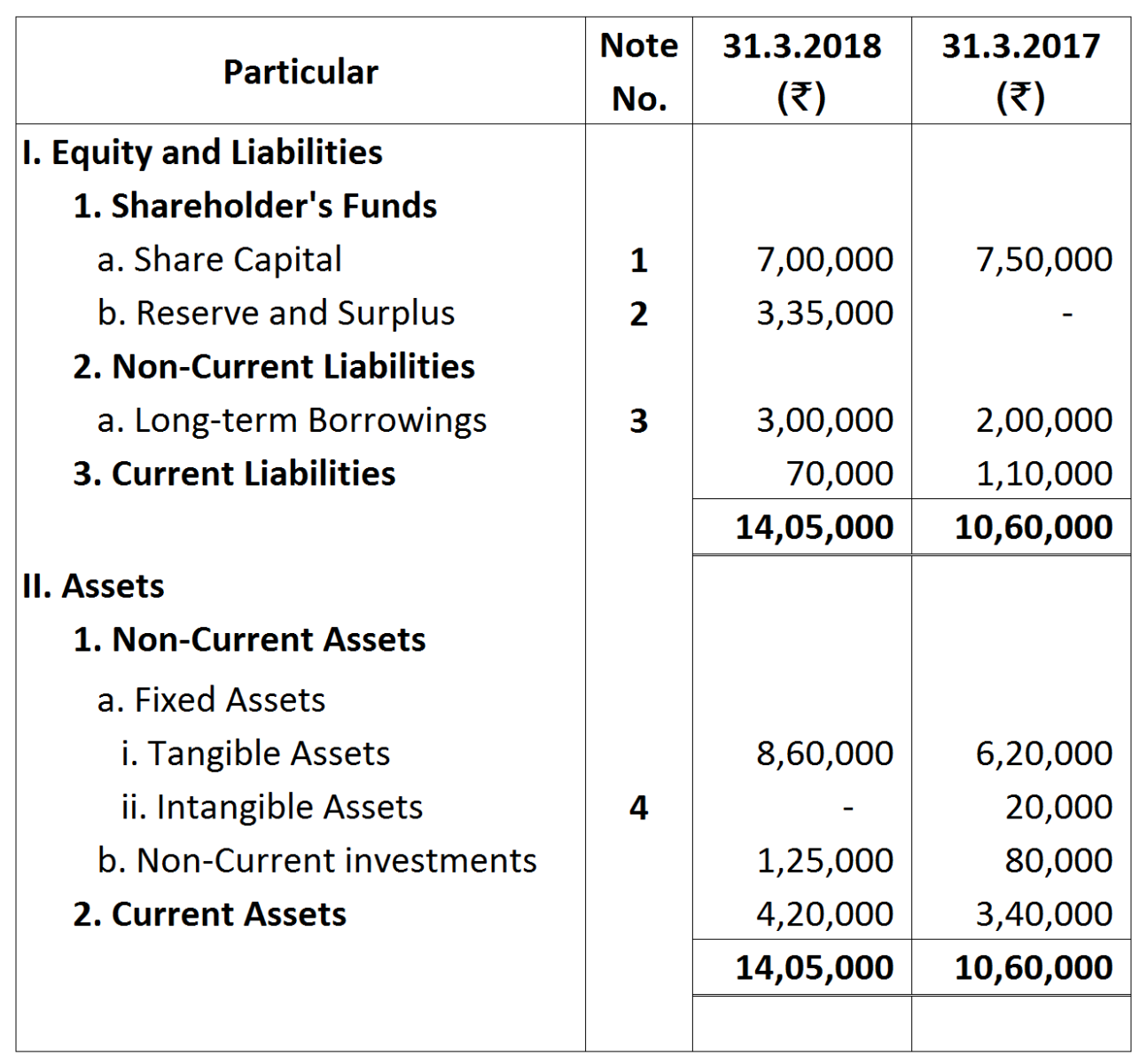

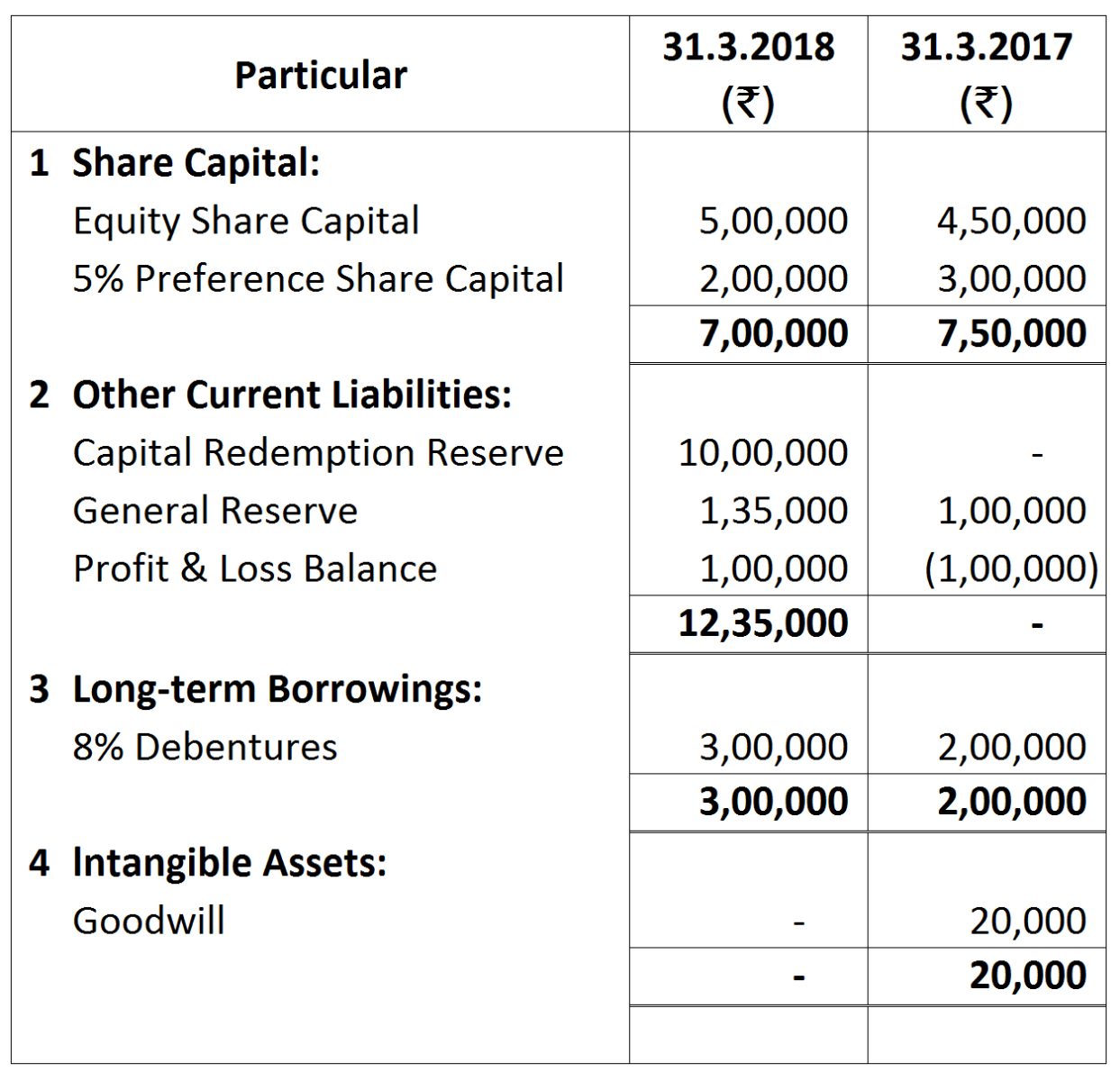

| Calculation of Net Profit before Tax: | ₹ |

| Profit & Loss Balance on 31st March, 2018 | 6,200 |

| Less: Profit & Loss Balance on 31st March, 2017 | (7,200) |

| 1,000 | |

| Add: Transfer to General Reserve (₹ 12,000 - ₹ 8,000) | 4,000 |

| Proposed Dividend for Previous year | 11,200 |

| Net Profit before Tax | 14,200 |

Working Note:

Working Note:

|

Calculation of Net Profit before Tax

|

₹

|

₹

|

|

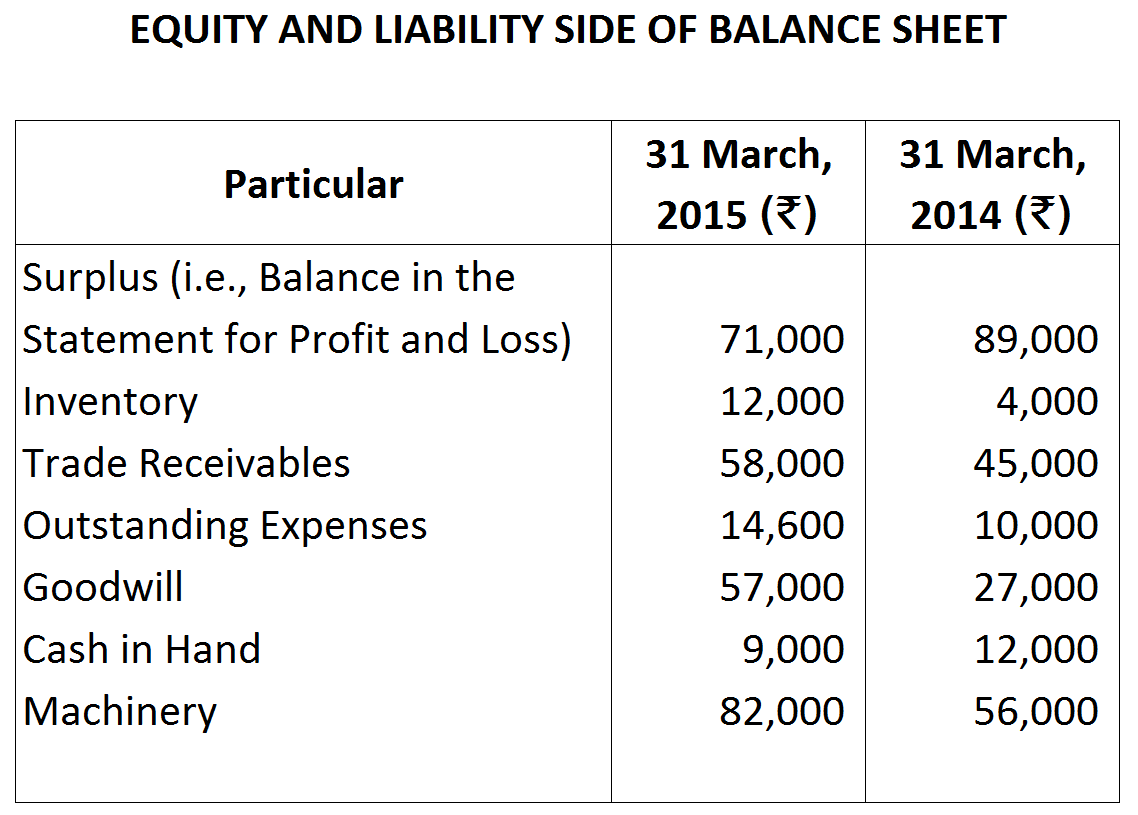

Surplus (i.e., Balance in the Statement of Profit and Loss as on 31st March, 2015)

|

|

71,000

|

|

Surplus (i.e., Balance in the Statement of Profit and Loss as on 31st March, 2014)

|

|

89,000

|

|

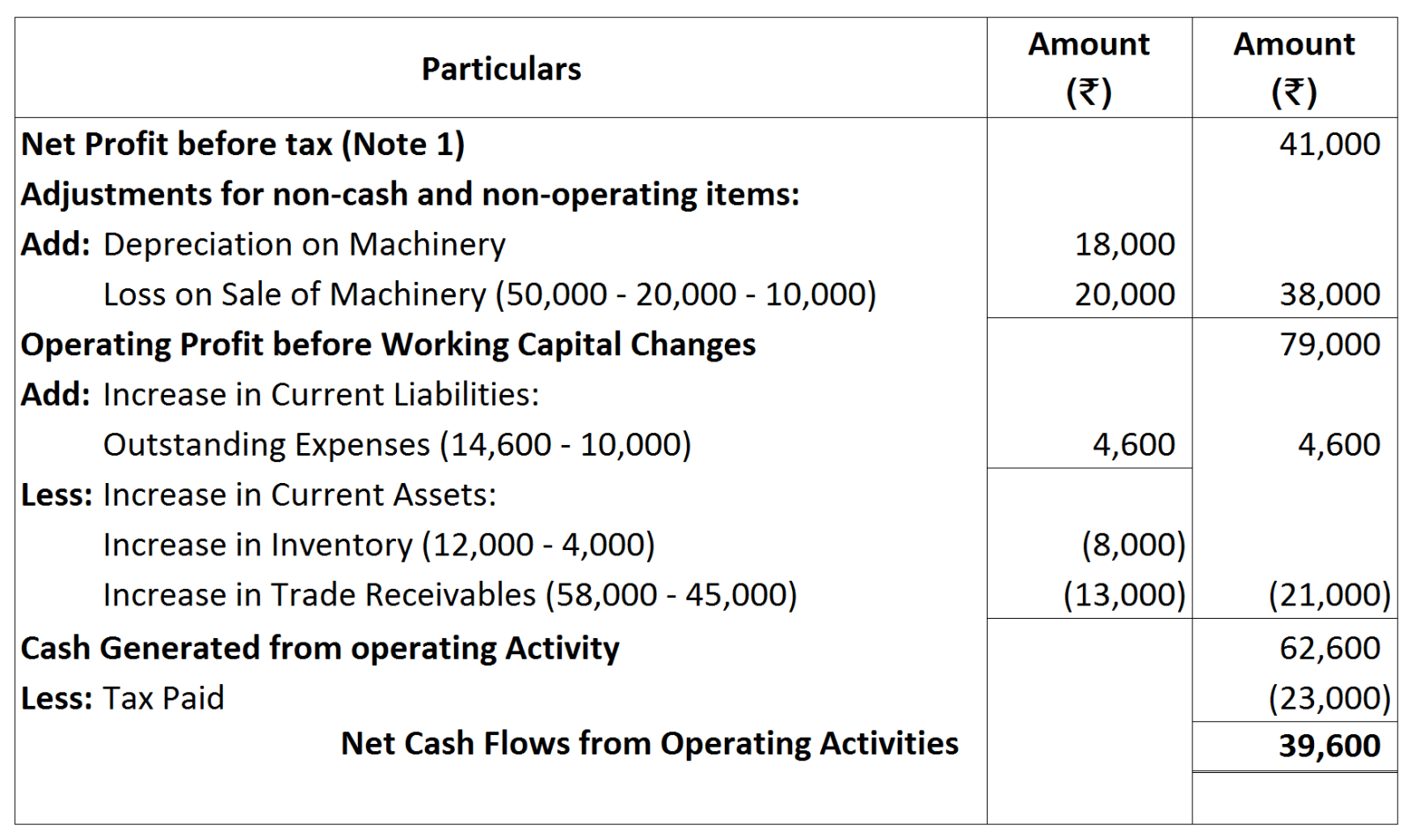

Net Loss during the year

|

|

18,000

|

|

Add: Tax Paid

|

23,000

|

|

|

Interim Dividend Paid

|

36,000

|

59,000

|

|

Net Profit before Tax

|

|

41,000

|

|

|

₹

|

|

Profit & Loss Balance on 31st March, 2018

|

1,60,000

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(85,000)

|

|

|

75,000

|

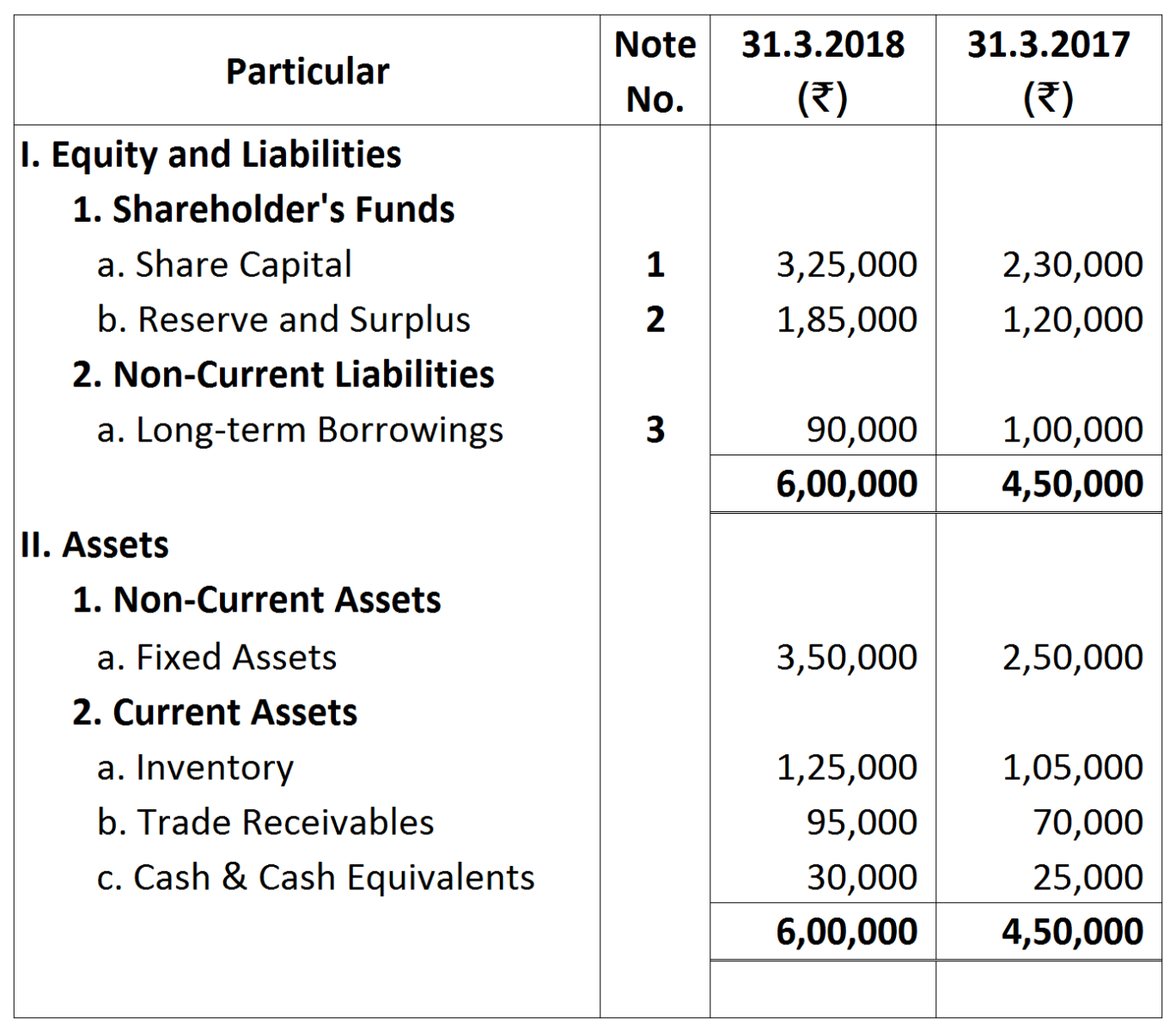

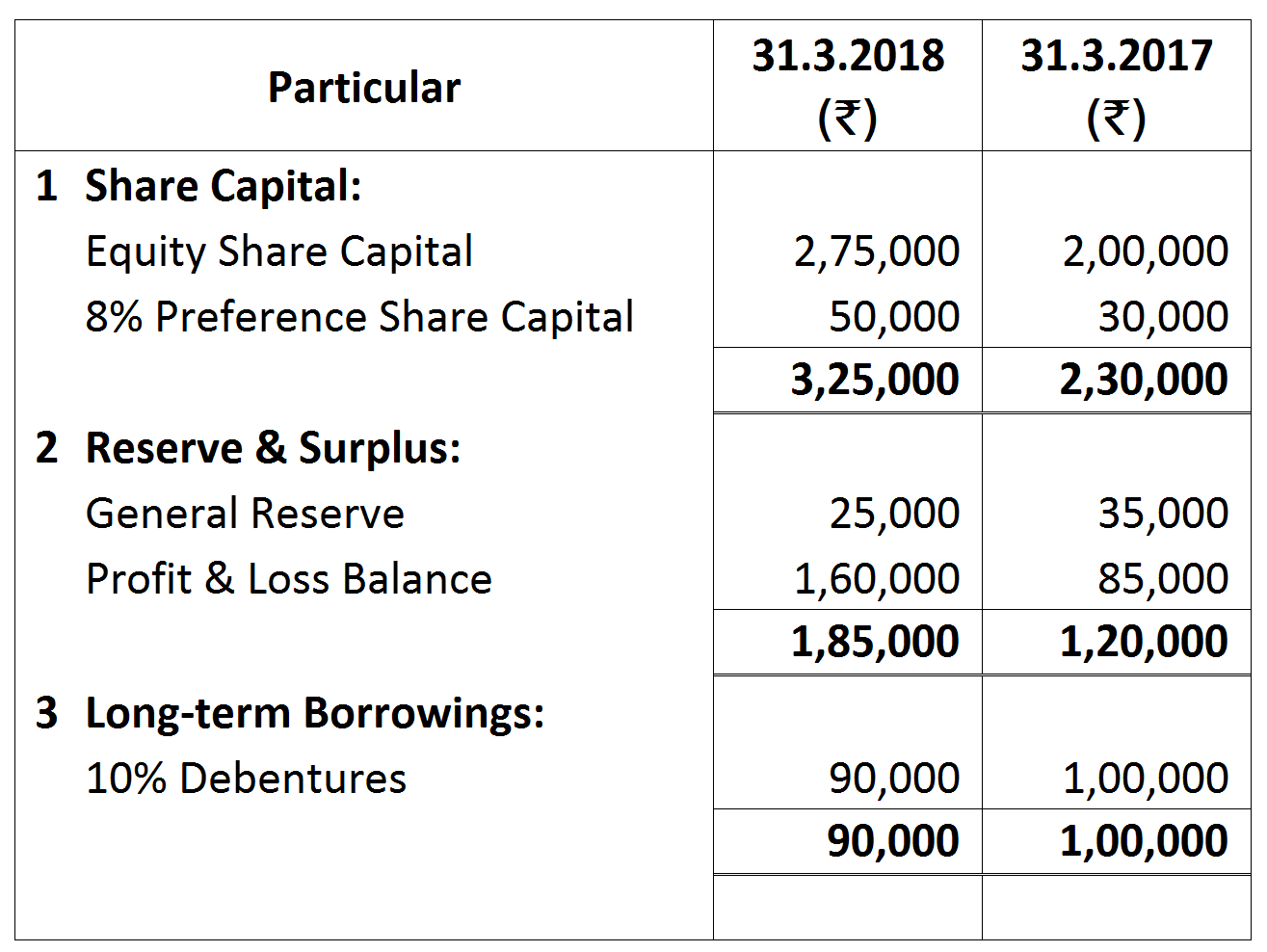

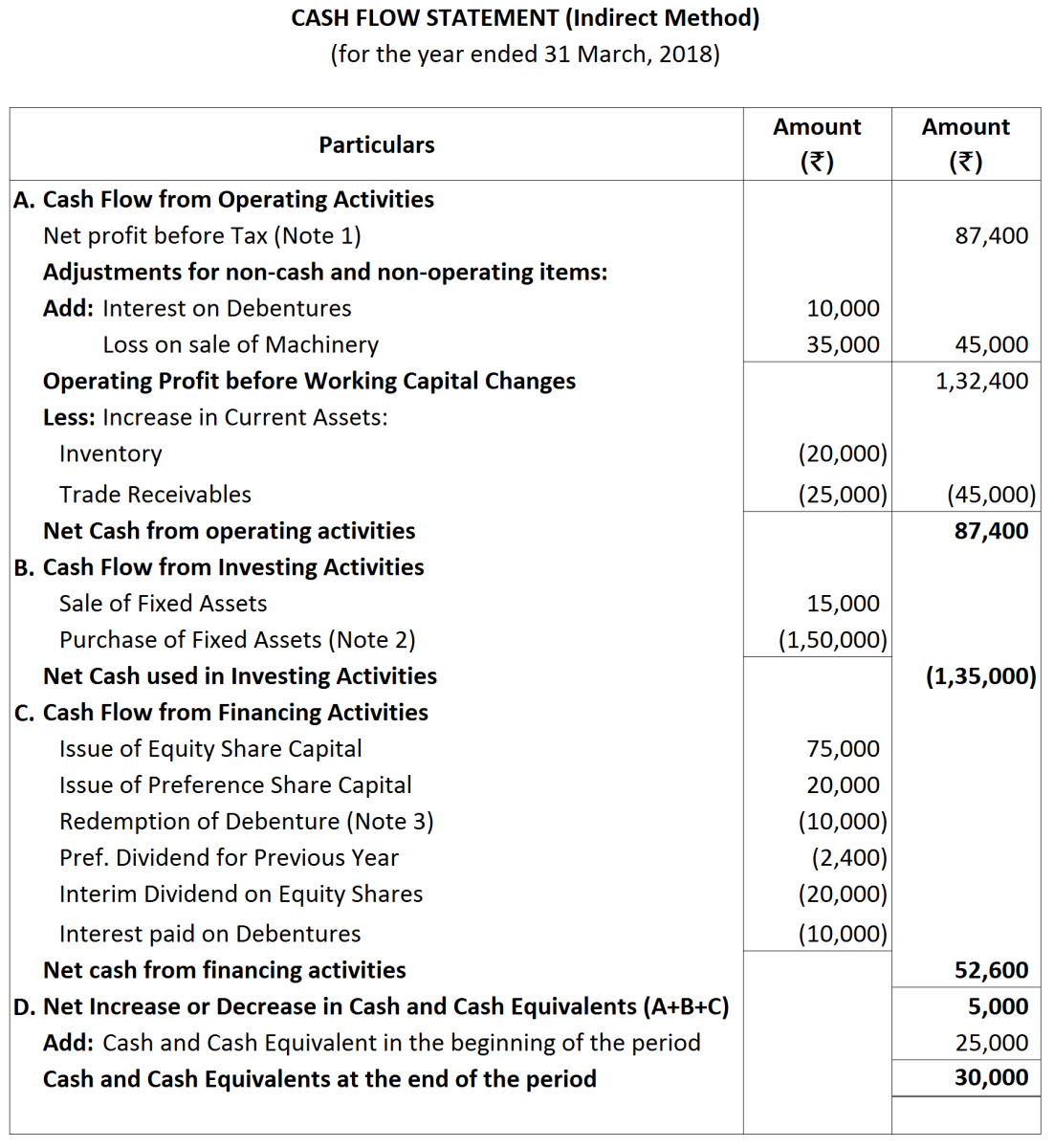

|

Add: Preference Dividend for Previous Year (8% on ₹ 30,000)*

|

2,400

|

|

Interim Dividend on Equity Capital

|

20,000

|

|

|

97,400

|

|

Less: Decrease in General Reserve (₹ 25,000 - ₹ 35,000)

|

(10,000)

|

|

Net Profit before Tax

|

87,400

|

|

1.

|

Contingent Liability

|

31st March, 2018

|

31st March, 2017 |

|

|

|

₹

|

₹

|

|

|

Proposed Dividend

|

28,000

|

20,000

|

|

2.

|

Interest paid on long-term borrowings amounted to ₹ 8,000.

|

||

|

Calculation of Net Profit before Tax:

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2018

|

1,25,000

|

|

Less: Reserve & Surplus Balance on 3 l st March, 2017

|

(20,000)

|

|

|

1,05,000

|

|

Add: Proposed Dividend for Previous year

|

20,000

|

|

Provision for Tax made during the Current year

|

15,000

|

|

Net Profit before Tax

|

1,40,000

|

|

|

₹

|

|

Profit & Loss Balance on 31st March, 2018

|

1,00,000

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(1,00,000)

|

|

|

2,00,000

|

|

Add: Transfer to Capital Redemption Reserve

|

1,00,000

|

|

Transfer to General Reserve

|

35,000

|

|

Proposed Dividend on Equity Shares (8% on ₹ 4,50,000)

|

36,000

|

|

Dividend on Preference Shares (5% on ₹ 3,00,000)

|

15,000

|

|

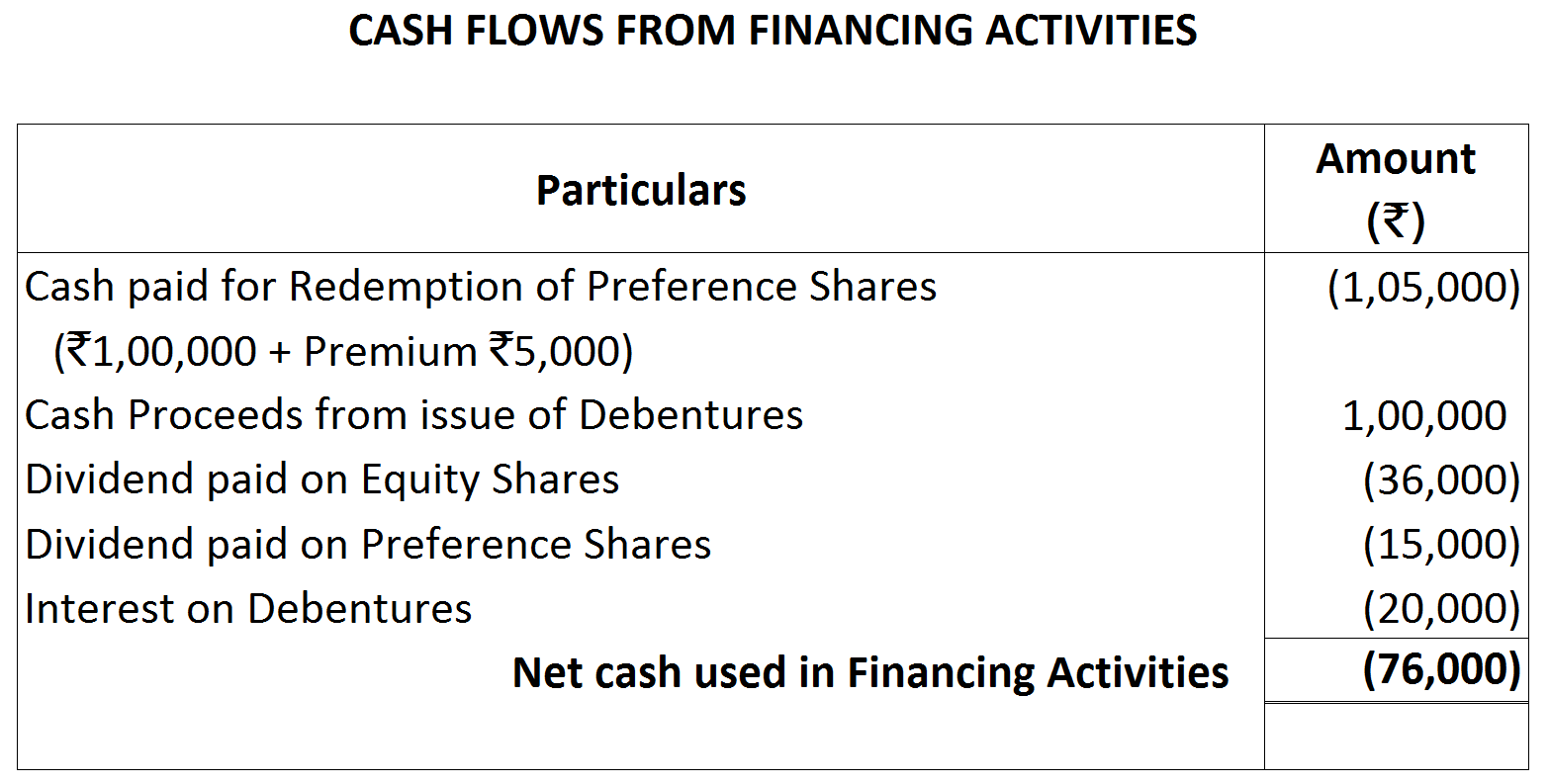

Net Profit before Tax

|

3,86,000

|

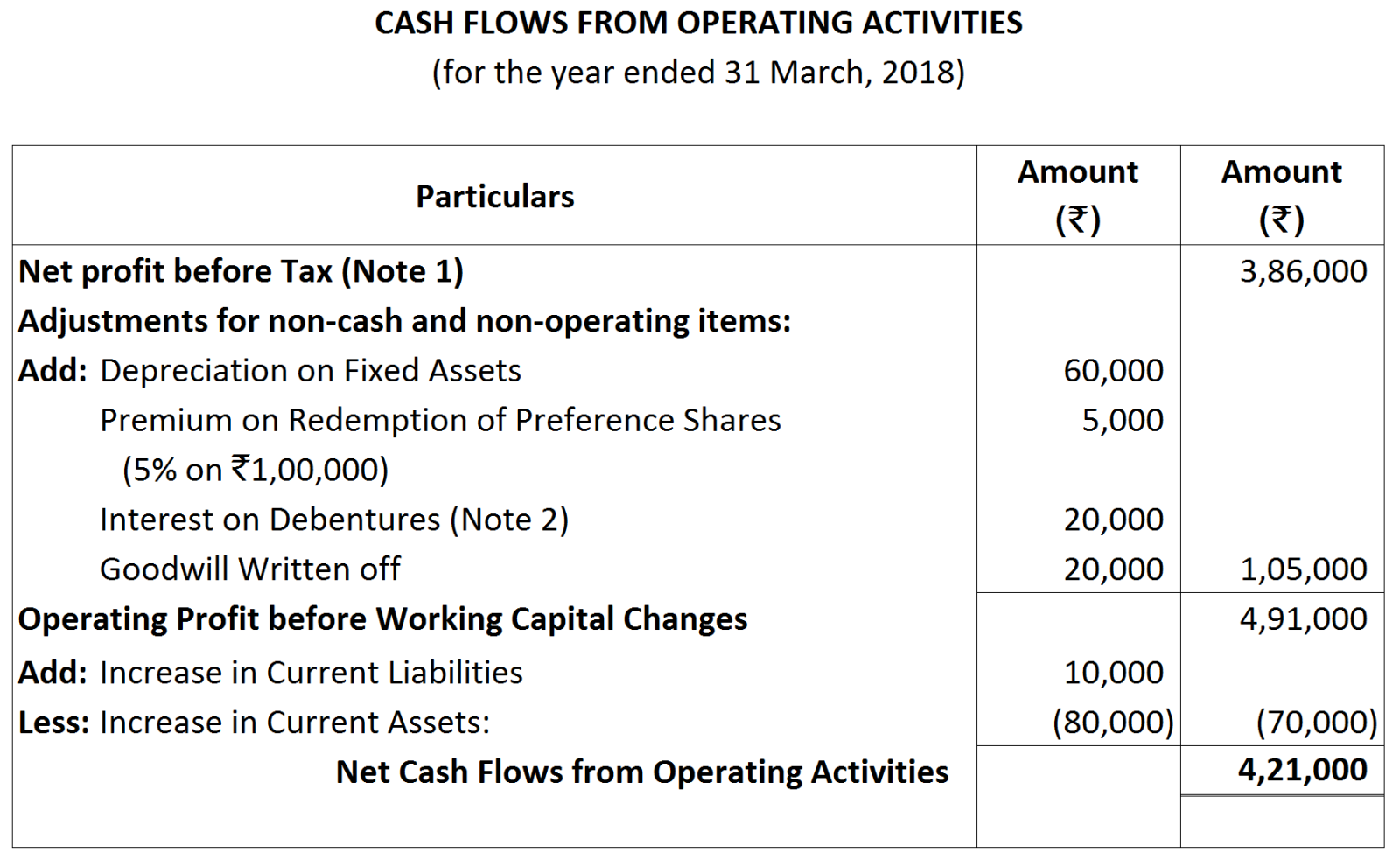

| ₹ | |

| 8% on ₹ 2,00,000 for 6 months | 8,000 |

| 8% on ₹ 3,00,000 for 6 months | 12,000 |

| 20,000 |

Note:

Note:

|

Calculation of Net Profit before Tax:

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2018

|

60,000

|

|

Less: Reserve & Surplus Balance on 31st March, 2017

|

(50,000)

|

|

|

10,000

|

|

Add: Dividend paid for Current year

|

30,000

|

|

|

40,000

|

|

1.

|

Contingent Liability:

|

31.3.2018

|

31.3.2017

|

|

|

|

₹

|

₹

|

|

|

Proposed Dividend

|

2,00,000

|

1,00,000

|

|

2.

|

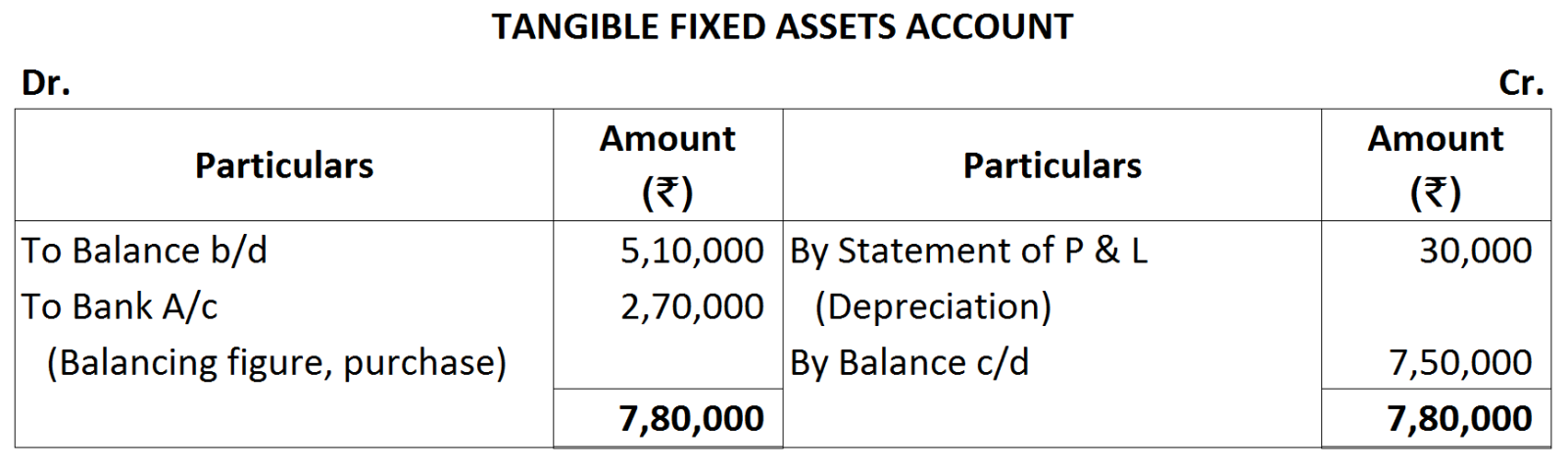

During the year ₹ 80,000 depreciation was charged on fixed tangible assets.

|

||

|

3.

|

A piece of machinery included in fixed tangible assets costing ₹ 20,000 on which depreciation charged was ₹ 8,000, was sold fort ₹ 10,000.

|

||

Notes:

Notes:

| ₹ | |

| Reserve & Surplus Balance on 31st March, 2018 | 4,00,000 |

| Less: Reserve & Surplus Balance on 31st March, 2017 | 2,00,000 |

| 2,00,000 | |

| Add: Proposed Dividend for Previous year | 1,00,000 |

| Net Profit before Tax | 3,00,000 |

Working Notes:

Working Notes:

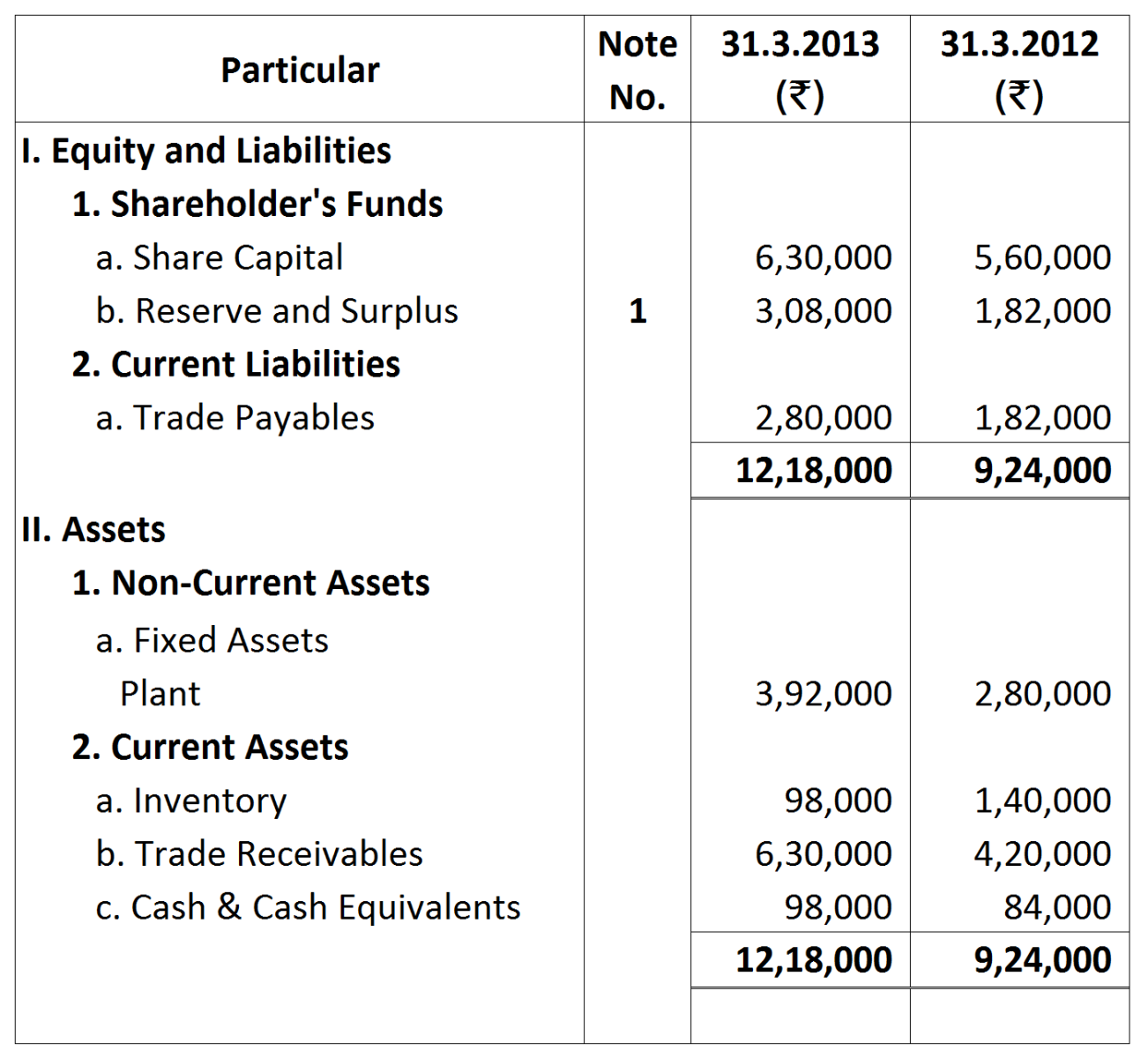

| ₹ | |

| Profit & Loss Balance on 31st March, 2013 | 3,08,000 |

| Less: Profit & Loss Balance on 31st March, 2012 | (1,82,000) |

| 1,26,000 |

Notes:

Notes:

|

1.

|

Reserve and Surplus on 31st March, 2018

|

|

23,000

|

|

|

Reserve and Surplus on 31st March, 2017

|

|

10,000

|

|

|

|

|

13,000

|

|

2.

|

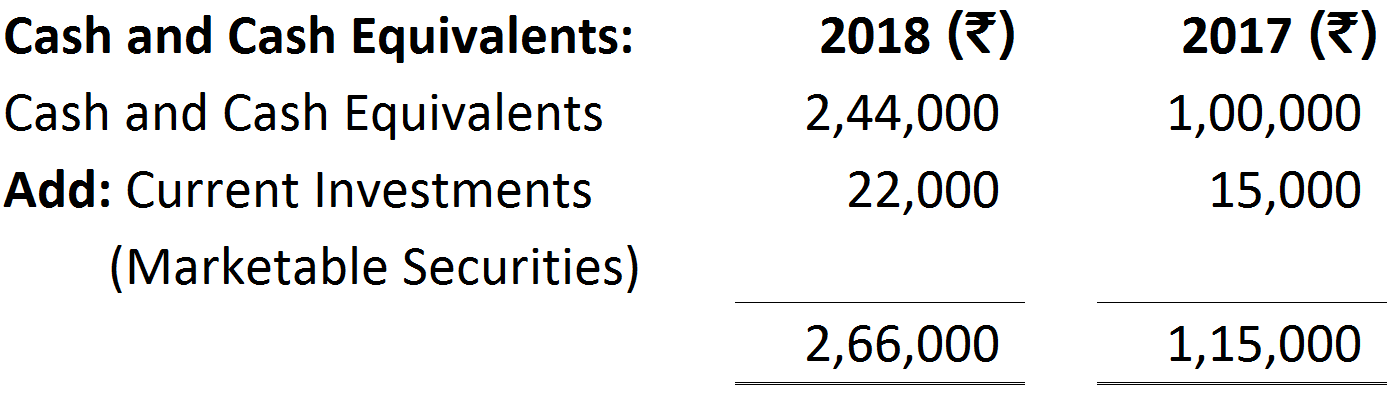

Cash & Cash Equivalents:

|

|

|

|

|

Cash & Cash Equivalents

|

47,000

|

30,000

|

|

|

Current Investments

|

8,000

|

10,000

|

|

|

|

55,000

|

40,000

|

Notes:

Notes:

|

|

₹

|

|

Profit & Loss Balance on 31st March, 2018

|

25,000

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(1,25,000)

|

|

|

1,00,000

|

|

Add: Transfer to General Reserve

|

70,000

|

|

Preference Dividend for previous year (8% on ₹ 50,000)

|

4,000

|

|

Interim Dividend on Equity Capital

|

24,000

|

|

|

2,000

|

Additlonal Information:

Additlonal Information:

Notes:

Notes:

|

|

₹

|

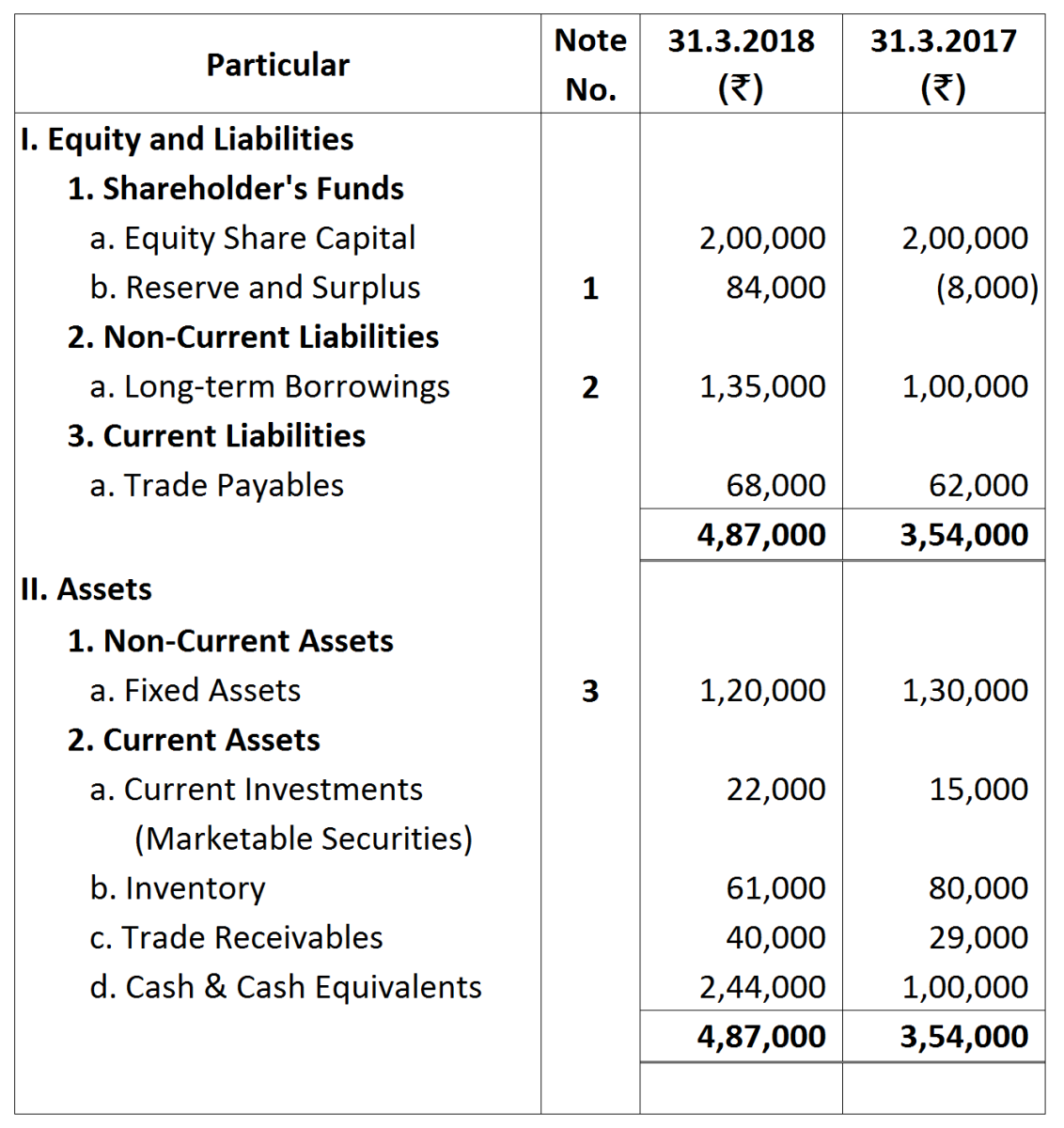

|

Profit & Loss Balance on 31st March, 2018

|

60,000

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(8,000)

|

|

|

68,000

|

|

Add: Transfer to General Reserve

|

24,000

|

|

Interim Dividend Paid

|

20,000

|

|

|

1,12,000

|

Additional Information:

Additional Information:

Notes:

Notes:

|

|

₹

|

|

Profit & Loss Balance (Net Loss) on 31.3.2018

|

(1,70,000)

|

|

Profit & Loss Balance (Net Loss) on 31.3.2017

|

(2,15,000)

|

|

Net Profit before Tax

|

45,000

|

|

|

|

₹

|

|

12% on ₹ 2,50,000 for 1 year

|

=

|

30,000

|

|

12% on ₹ 50,000 for 3 months

|

=

|

1,500

|

|

|

|

31,500

|

Notes:

Notes:

|

1.

|

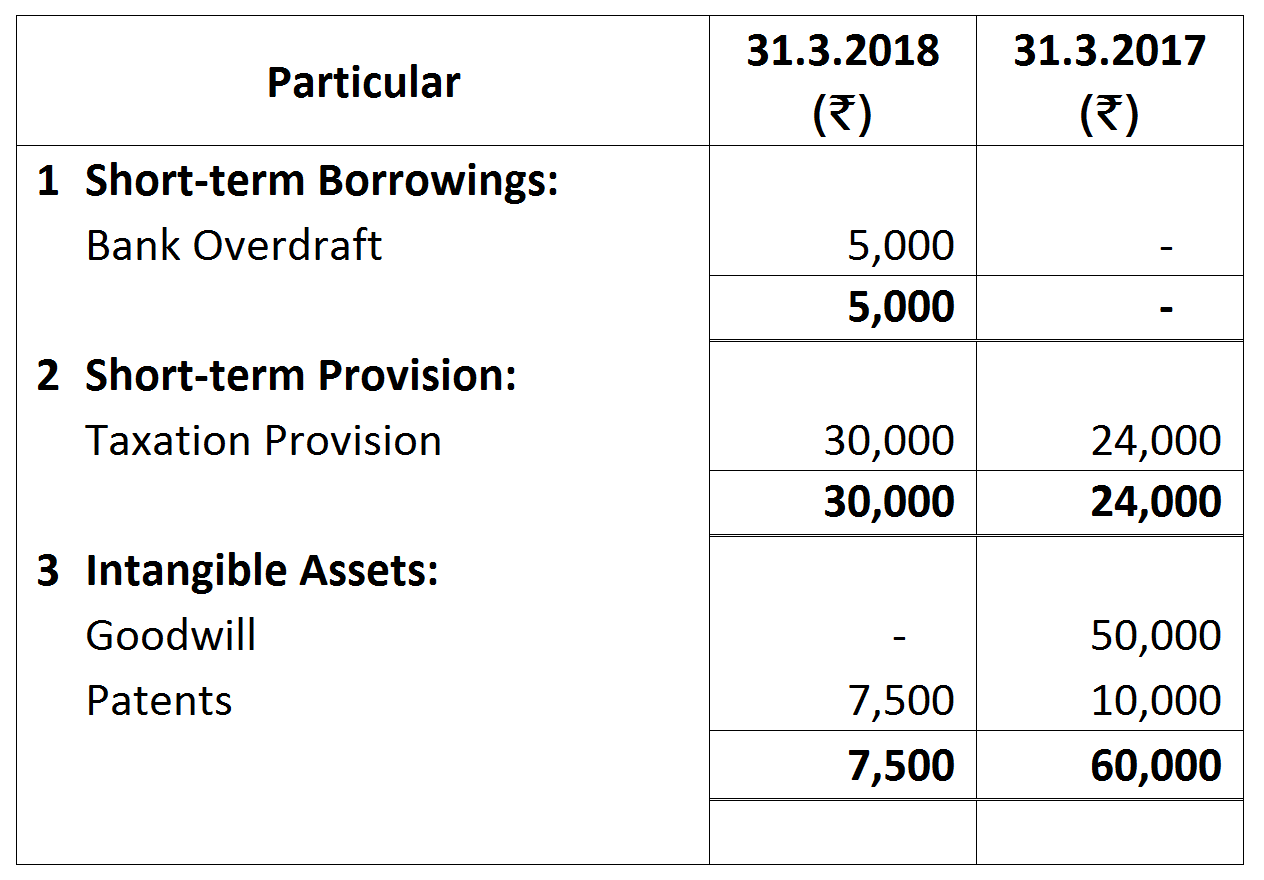

Short-term Borrowings:

|

31.3.2018

|

31.3.2017

|

|

|

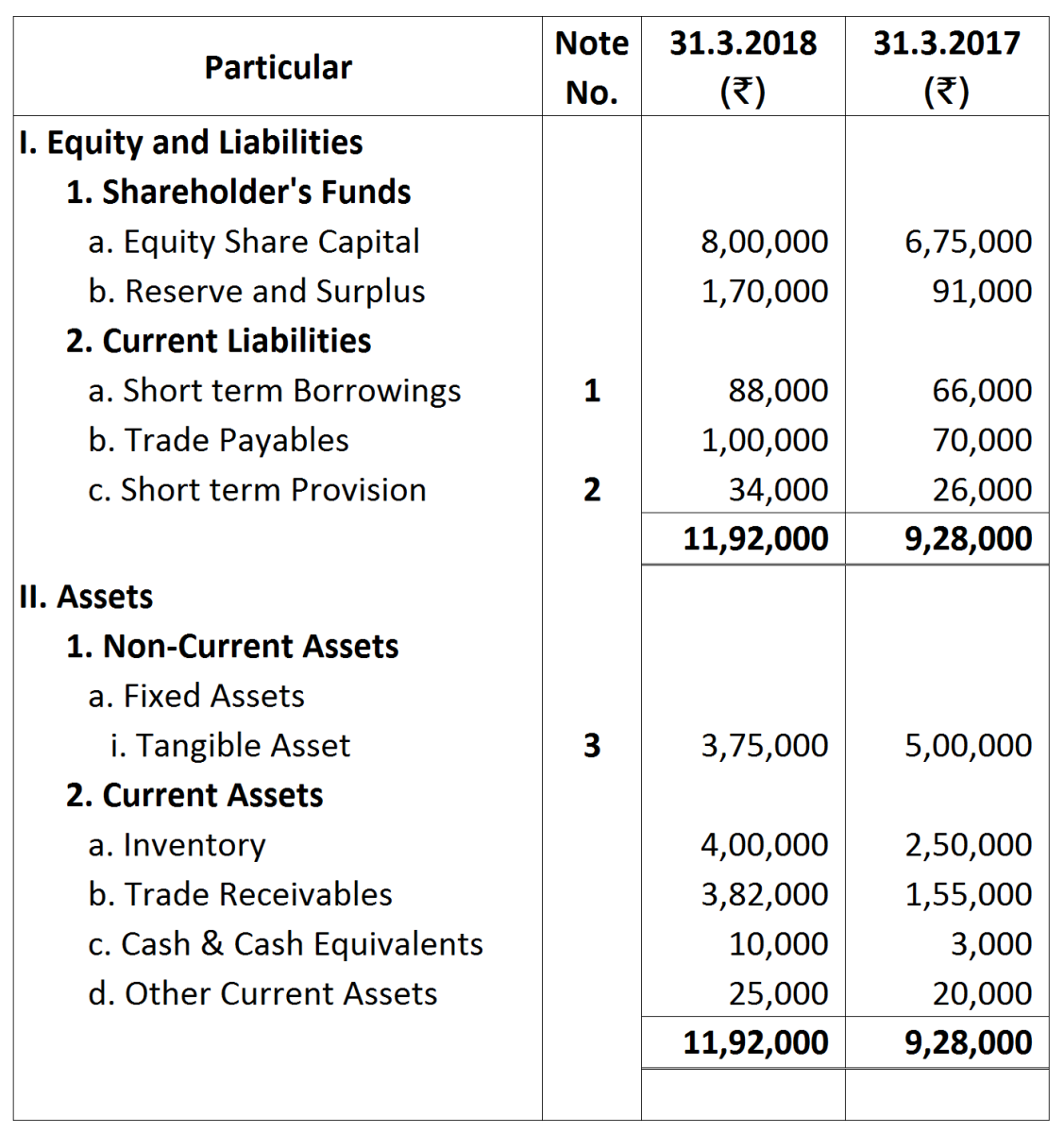

Bank Overdraft

|

88,000

|

66,000

|

|

2.

|

Short-term Provision

|

|

|

|

|

Taxation Provision

|

34,000

|

26,000

|

|

3

|

Tangible Assets:

|

|

|

|

|

Land

|

1,50,000

|

2,00,000

|

|

|

Plant

|

2,25,000

|

3,00,000

|

|

|

|

3,75,000

|

5,00,000

|

Notes:

Notes:

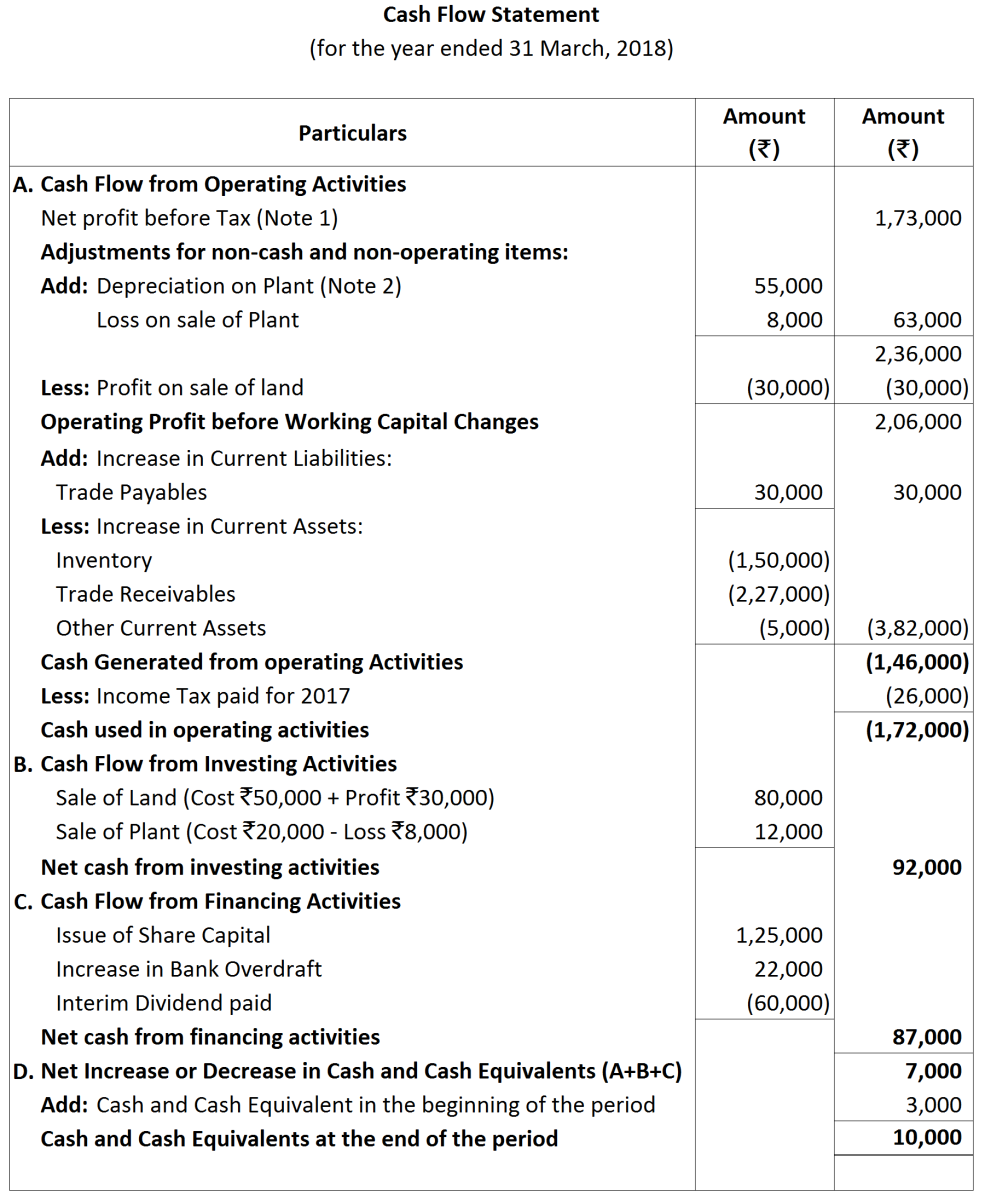

| ₹ | |

| Reserve & Surplus Balance on 31st March, 2018 | 1,70,000 |

| Less: Reserve & Surplus Balance on 31st March, 2017 | 91,000 |

| 79,000 | |

| Add: Interim Dividend Paid | 60,000 |

| Provision for Tax made during the Current year | 34,000 |

| 1,73,000 |

Notes:

Notes:

|

Profit and Loss Balance on 31st March, 2018

|

45,000

|

|

Less: Profit & Loss Balance on 31st March, 201 7

|

(50,000)

|

|

Net Loss during the year

|

5,000

|

Notes:

Notes:

|

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2017

|

72,000

|

|

less: Reserve & Surplus Balance on 31st March, 2016

|

(50,000)

|

|

|

22,000

|

|

Provision for Tax made during the Current year

|

24,000

|

|

Net Profit before Tax

|

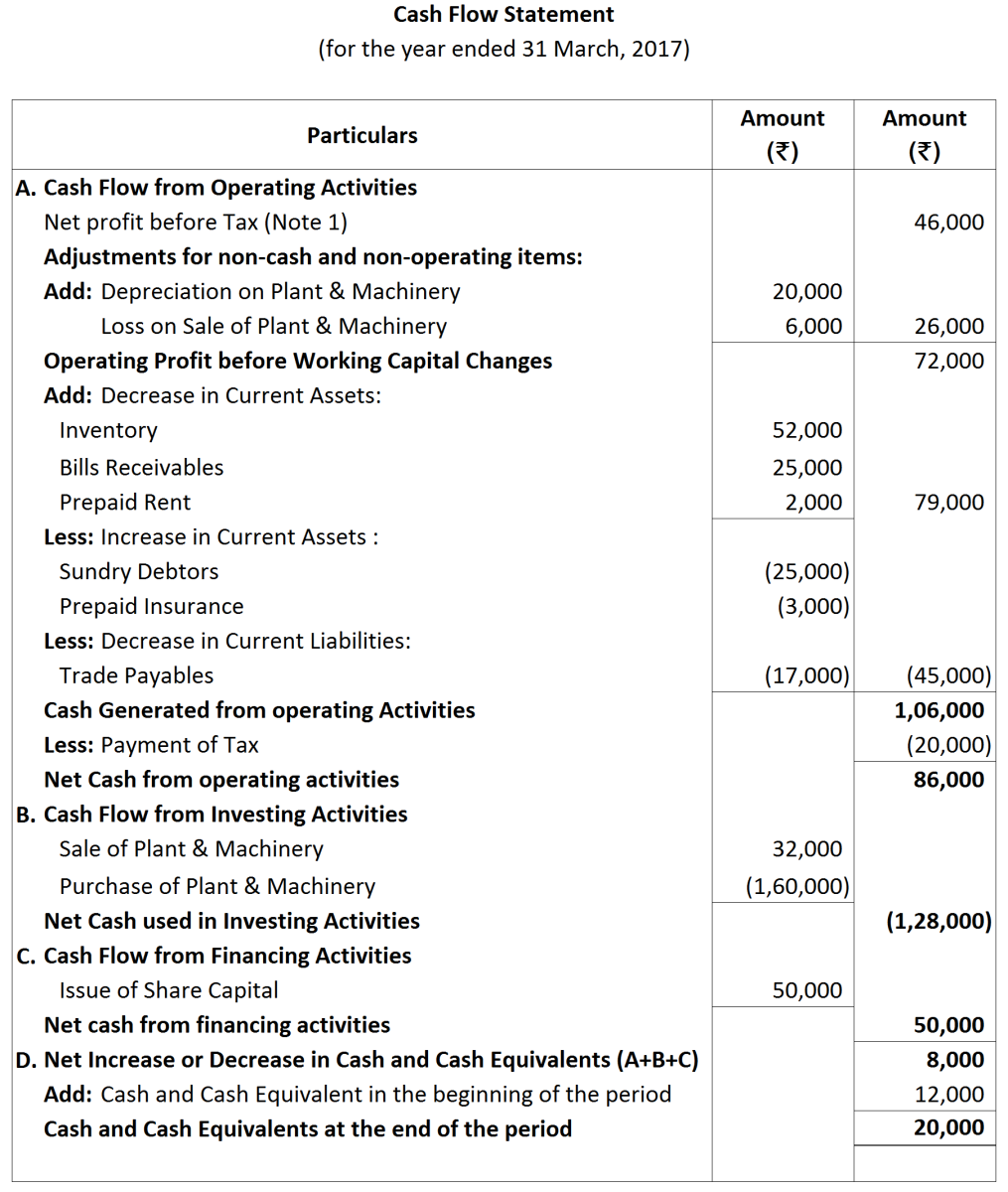

46,000

|

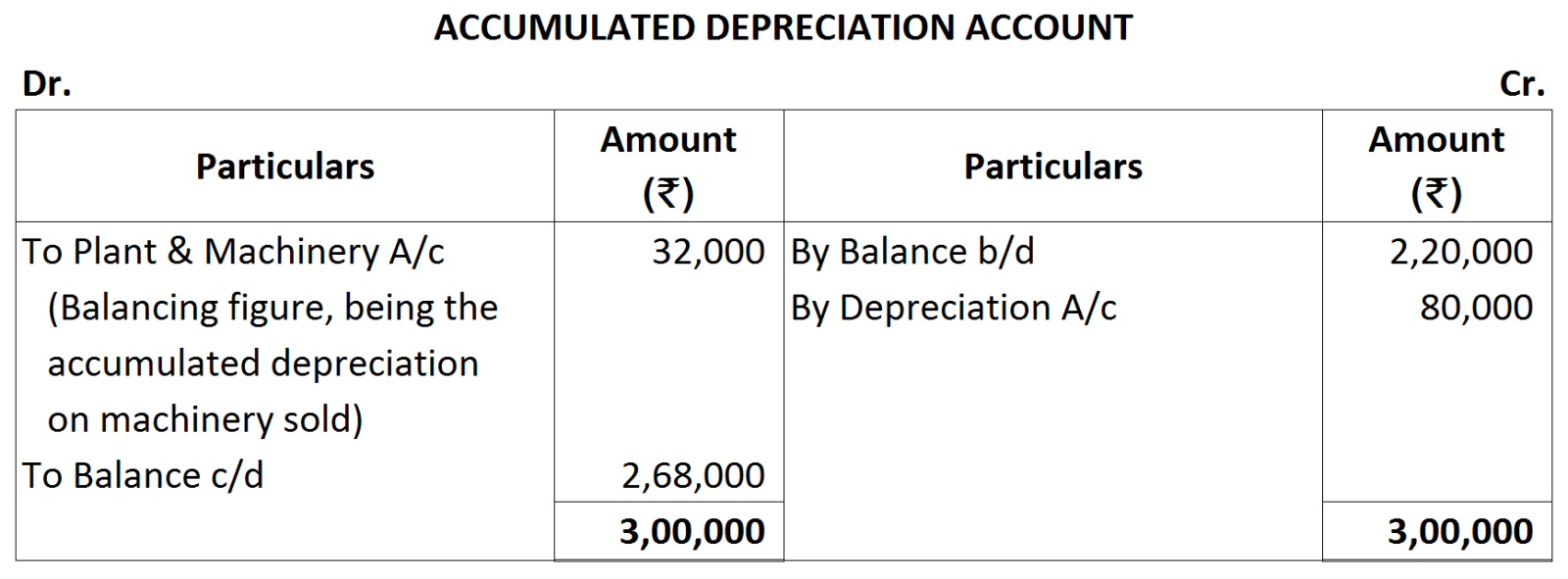

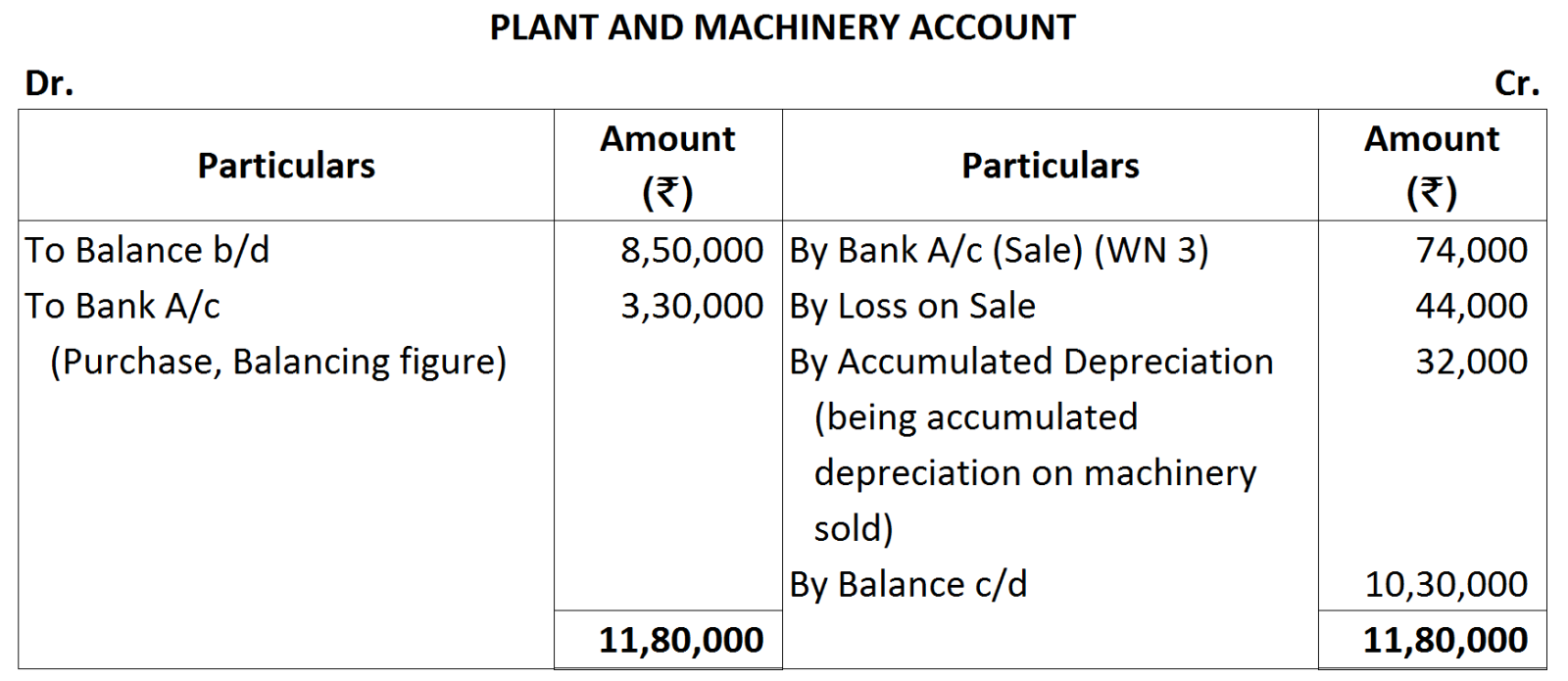

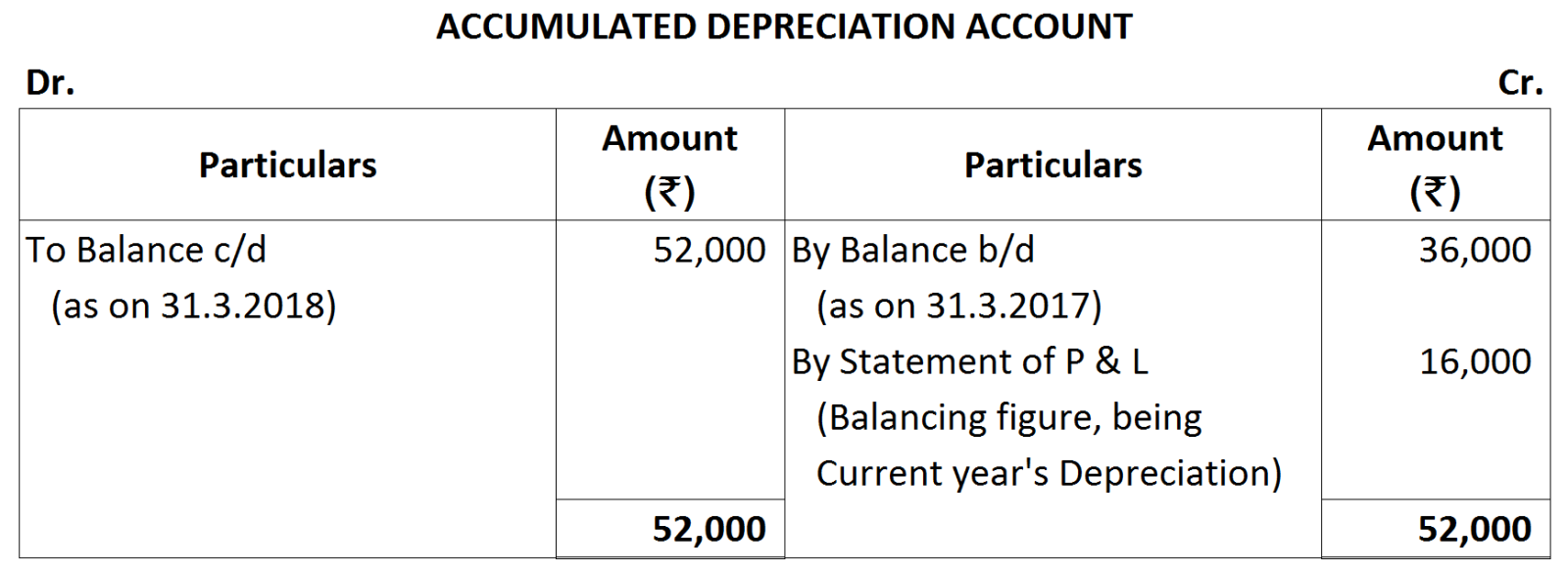

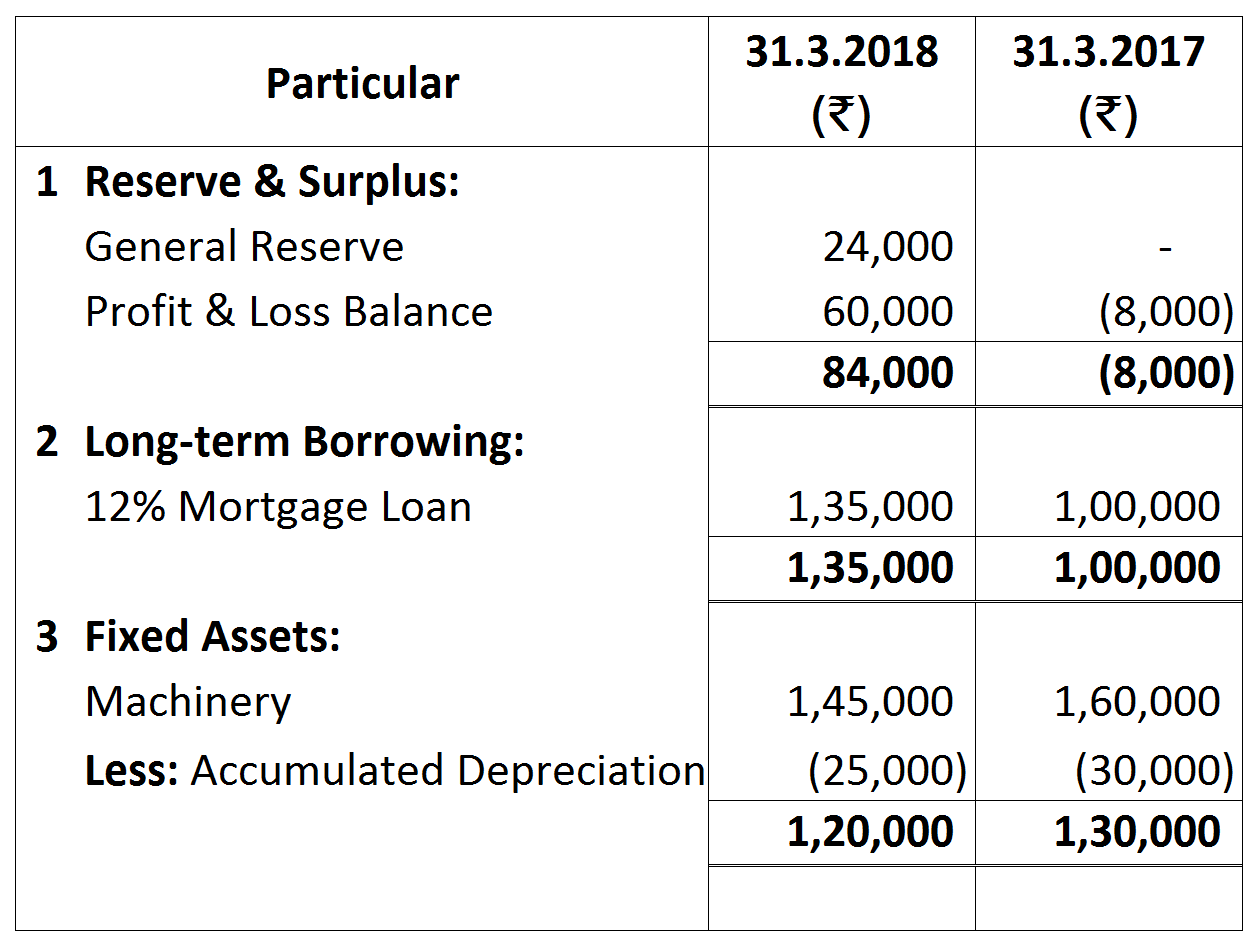

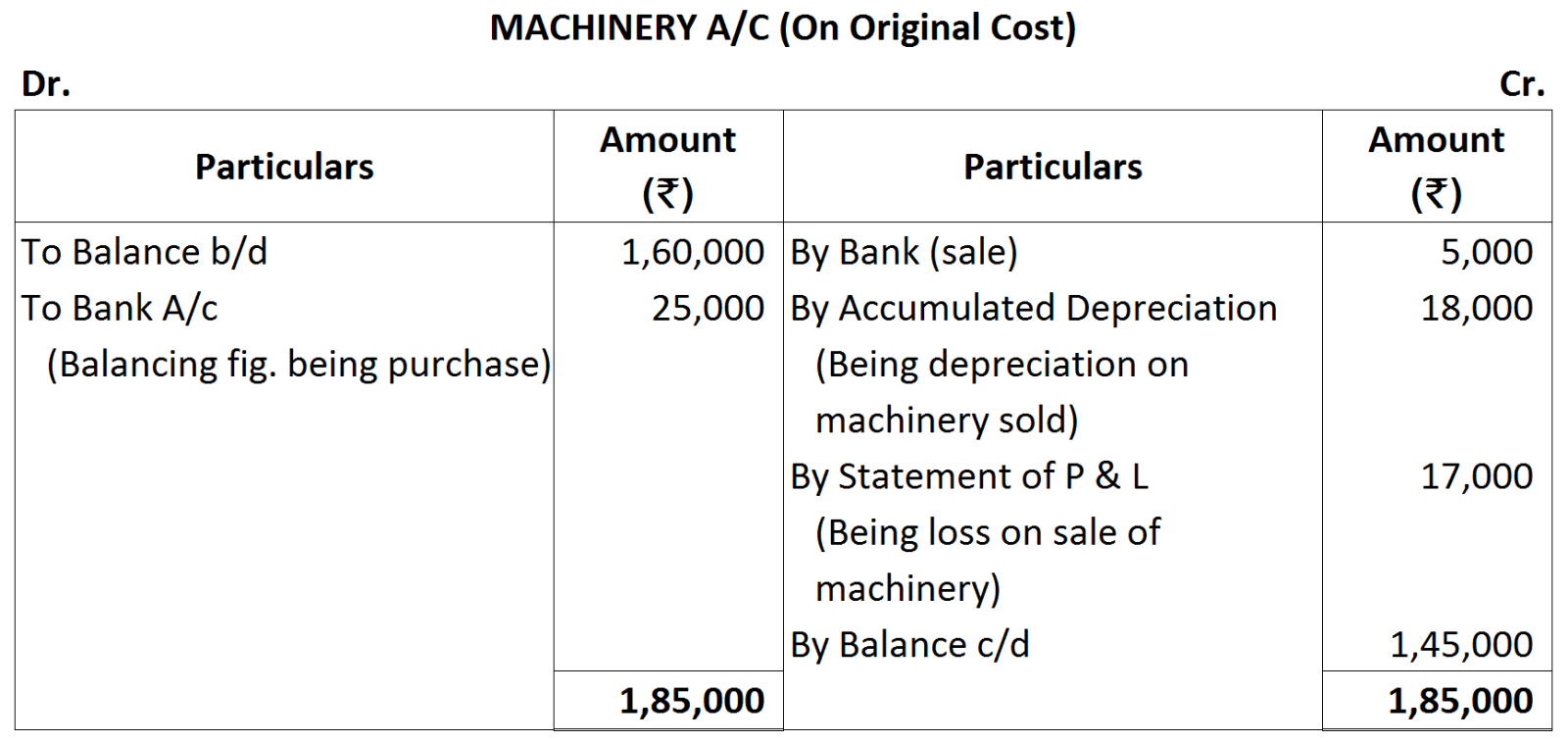

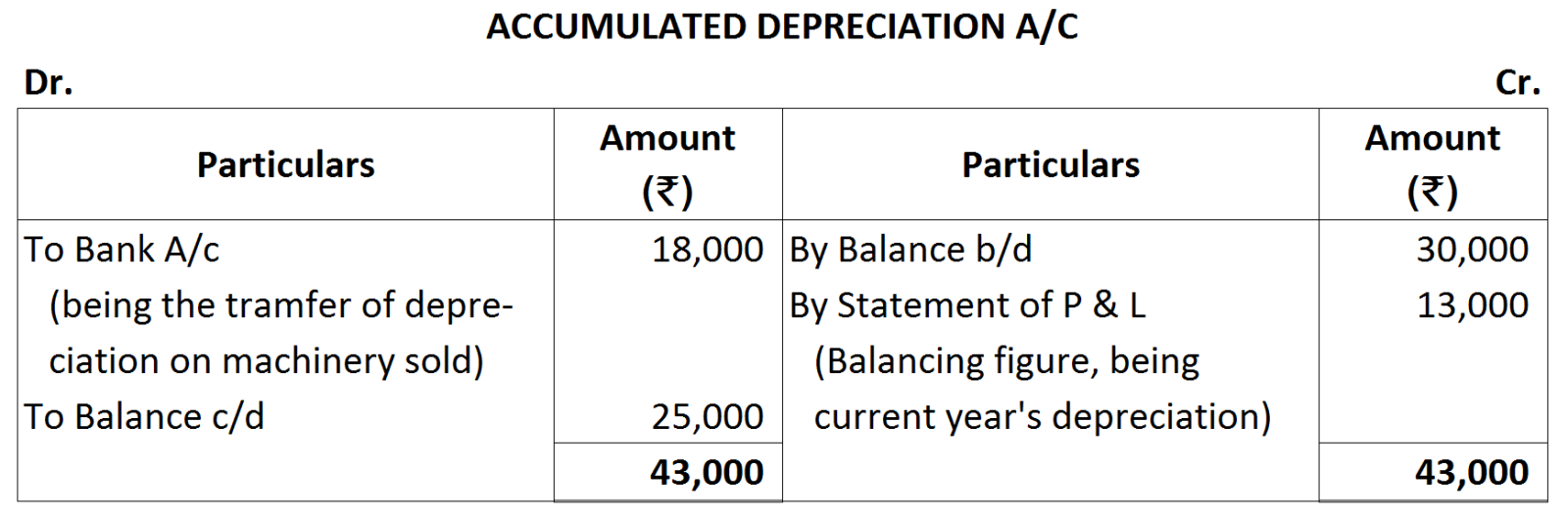

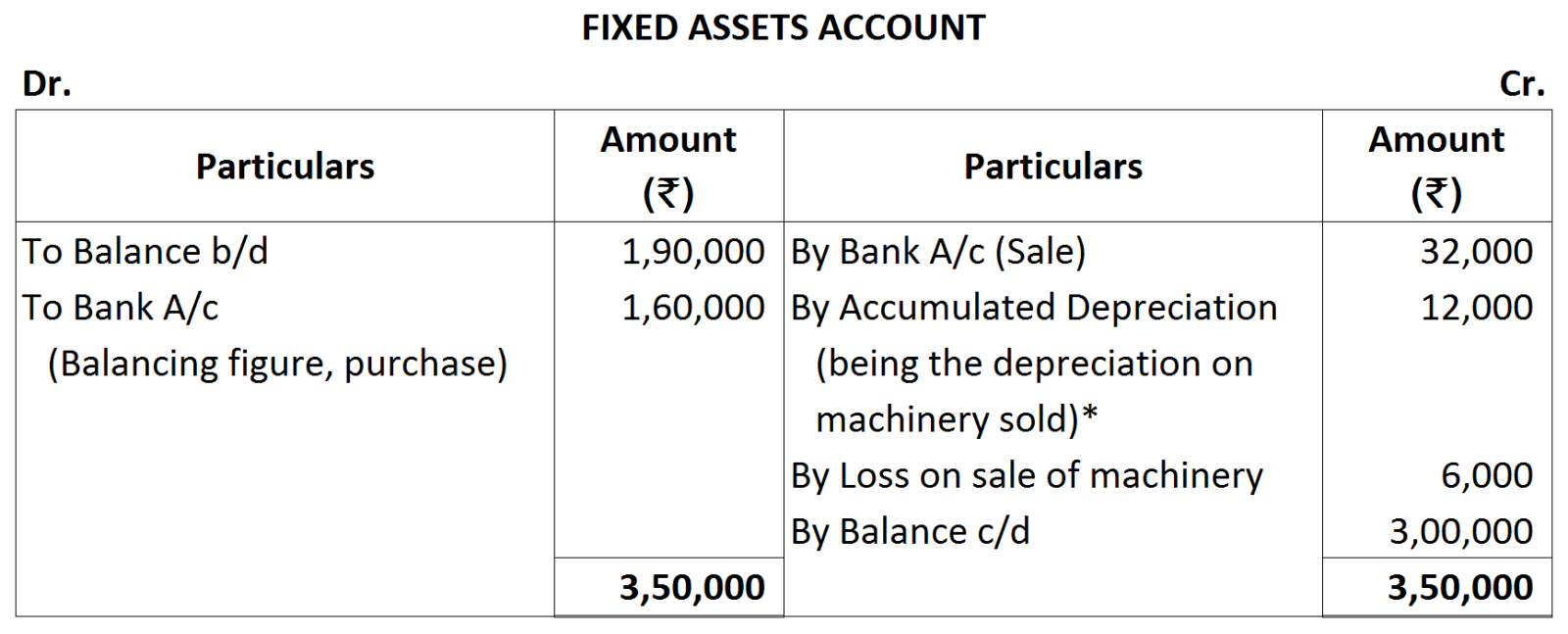

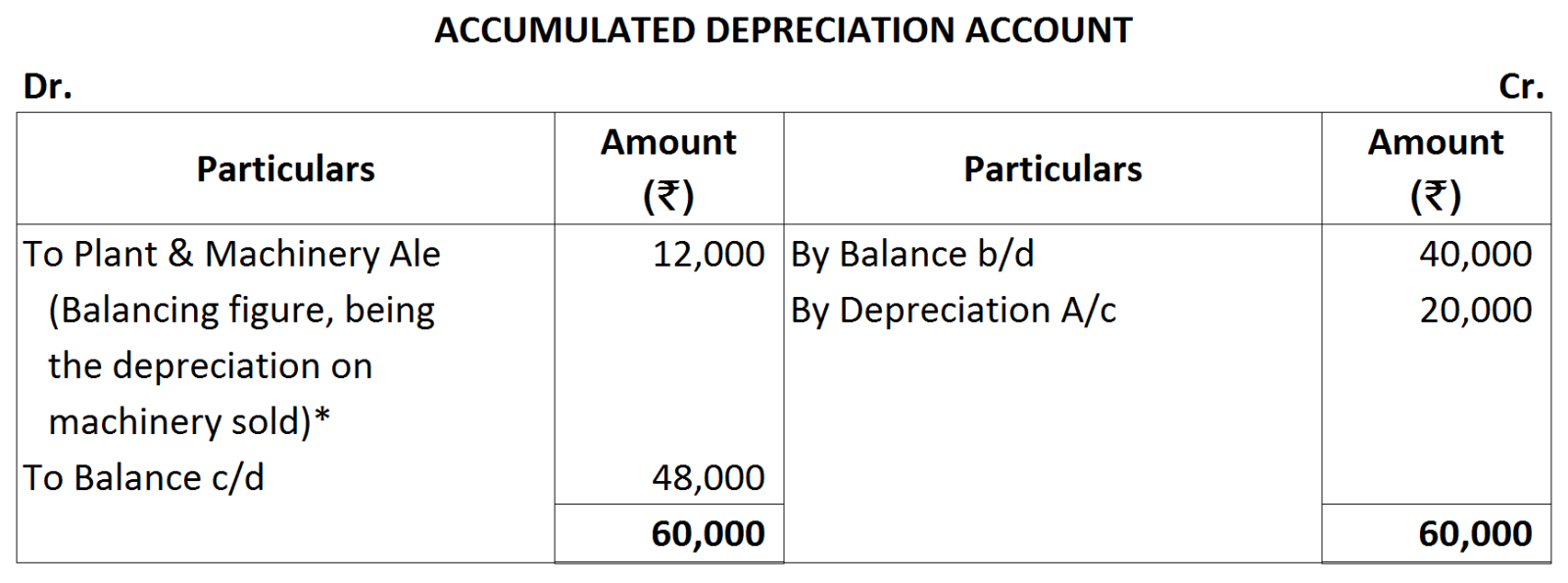

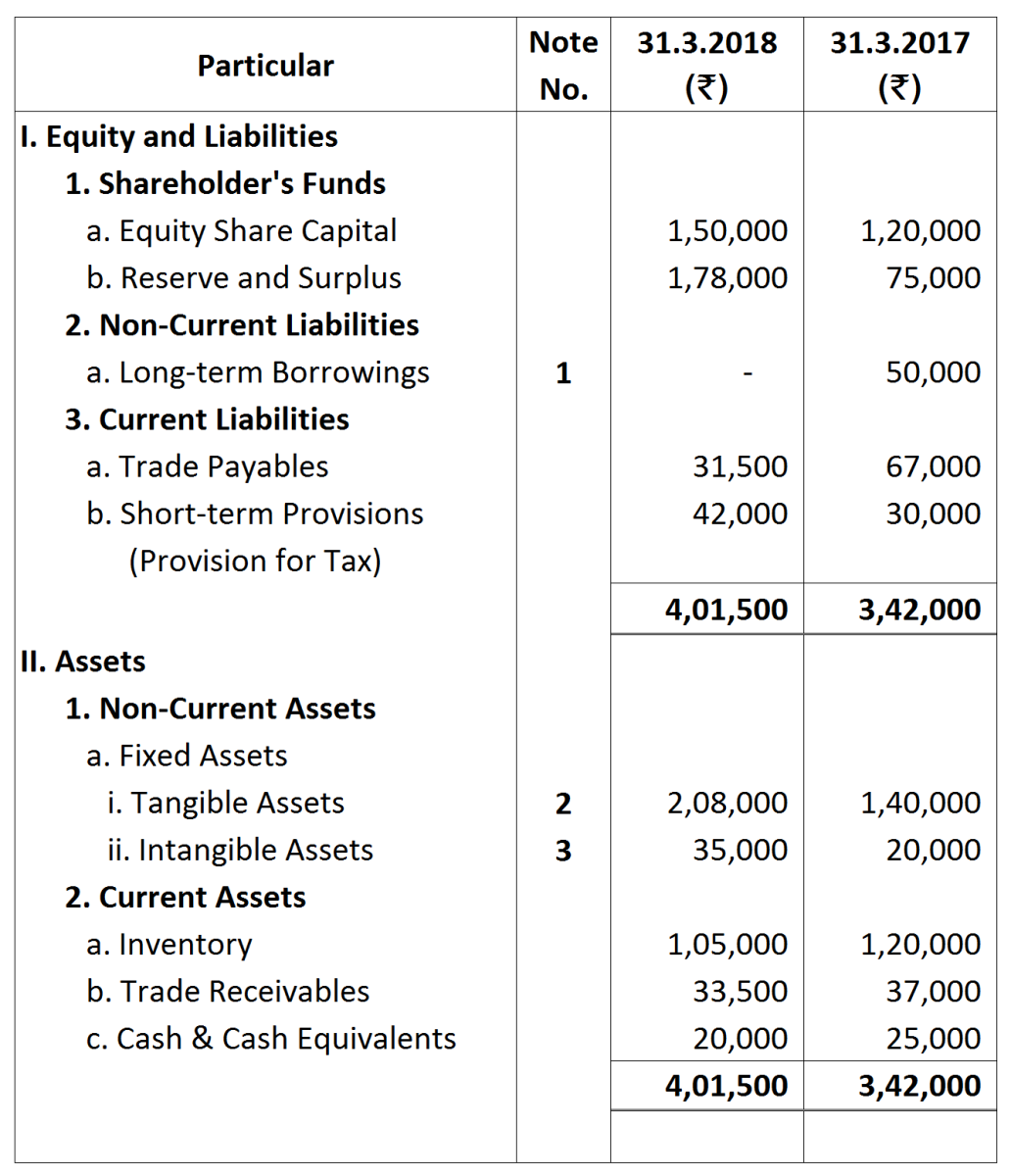

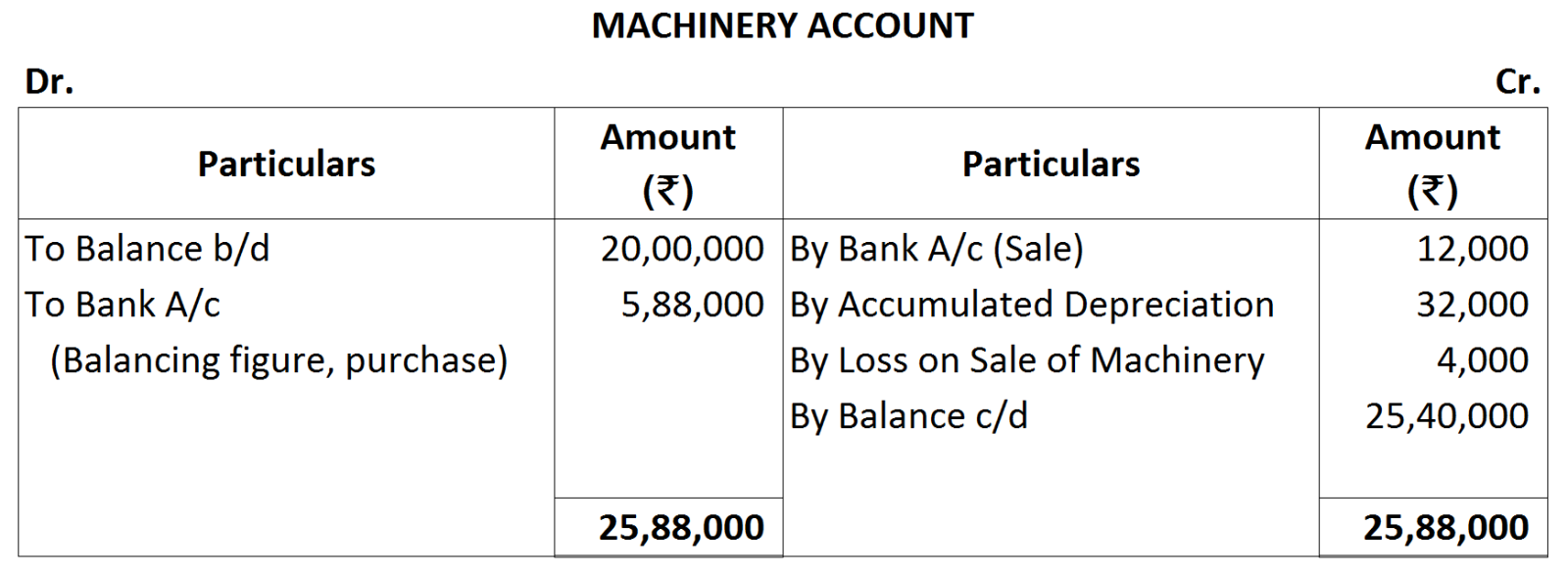

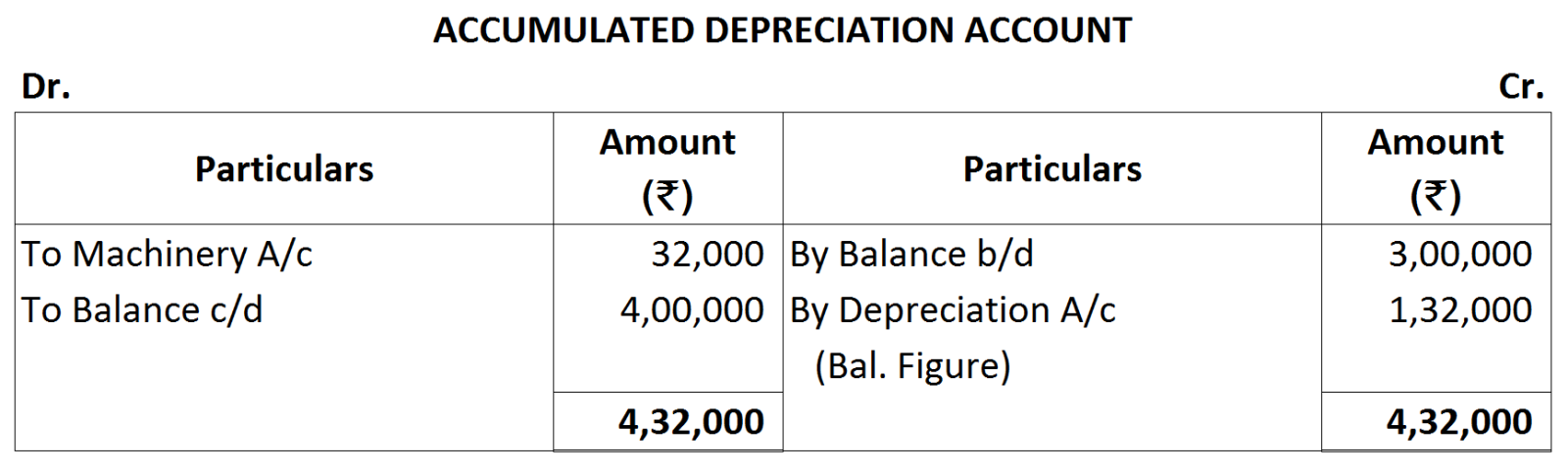

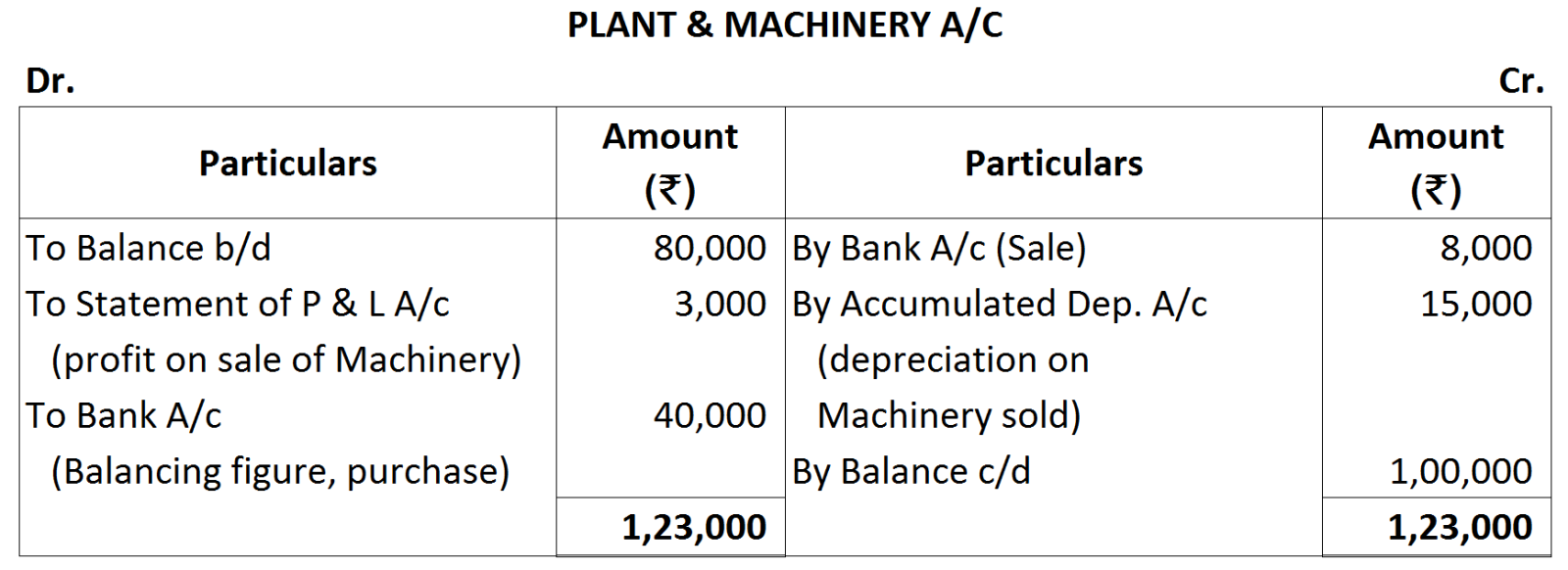

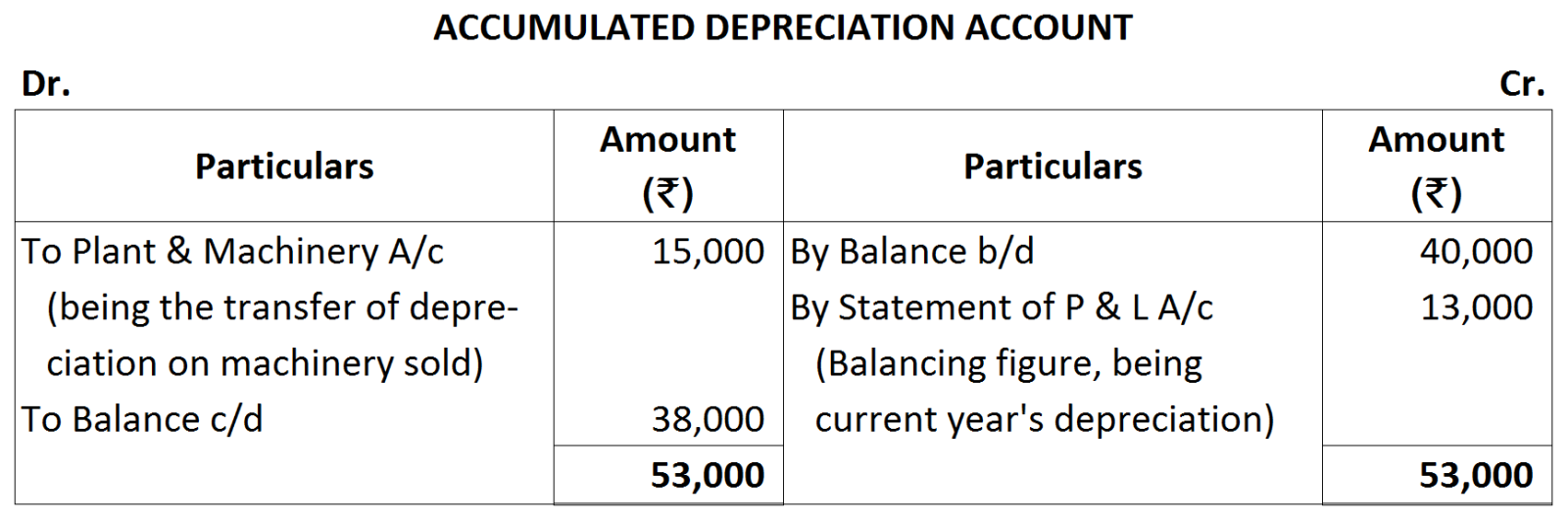

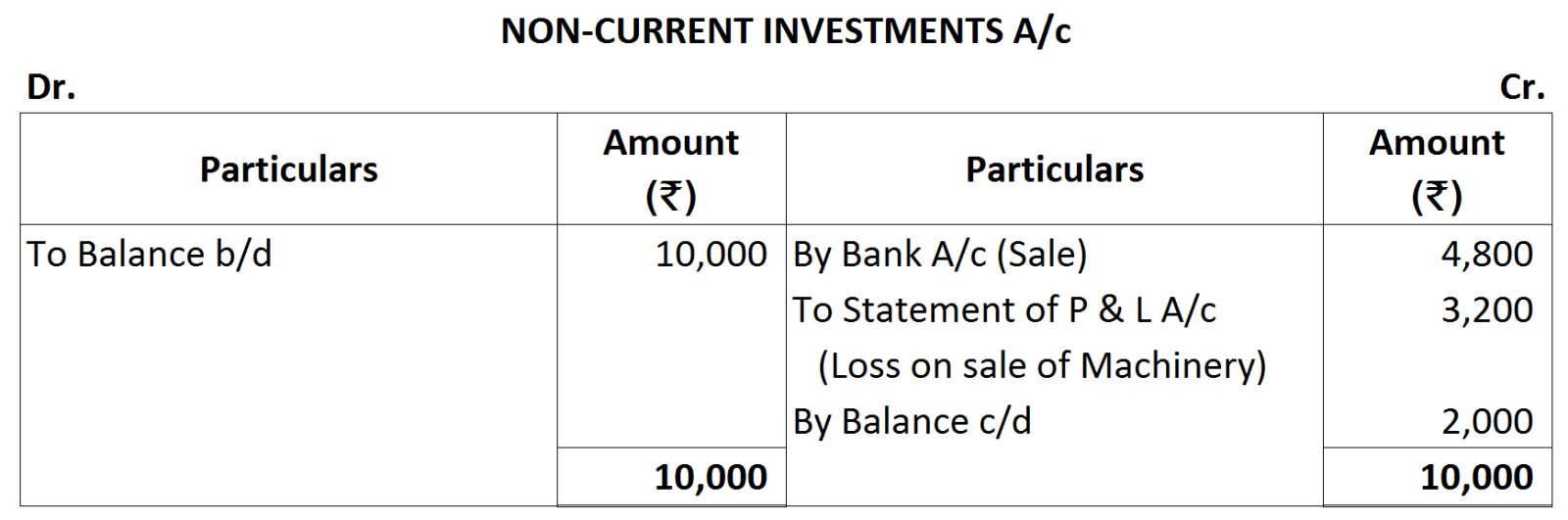

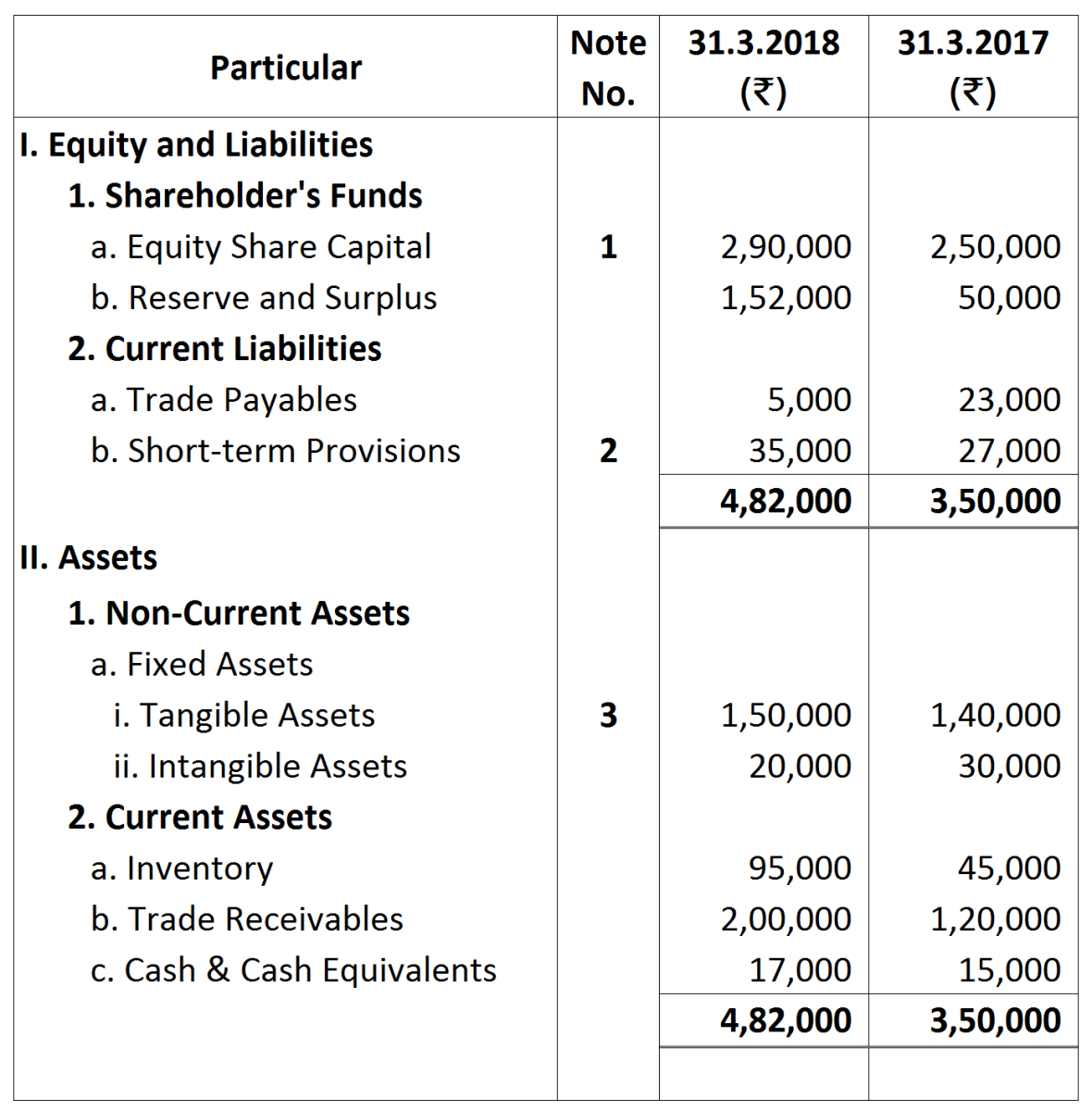

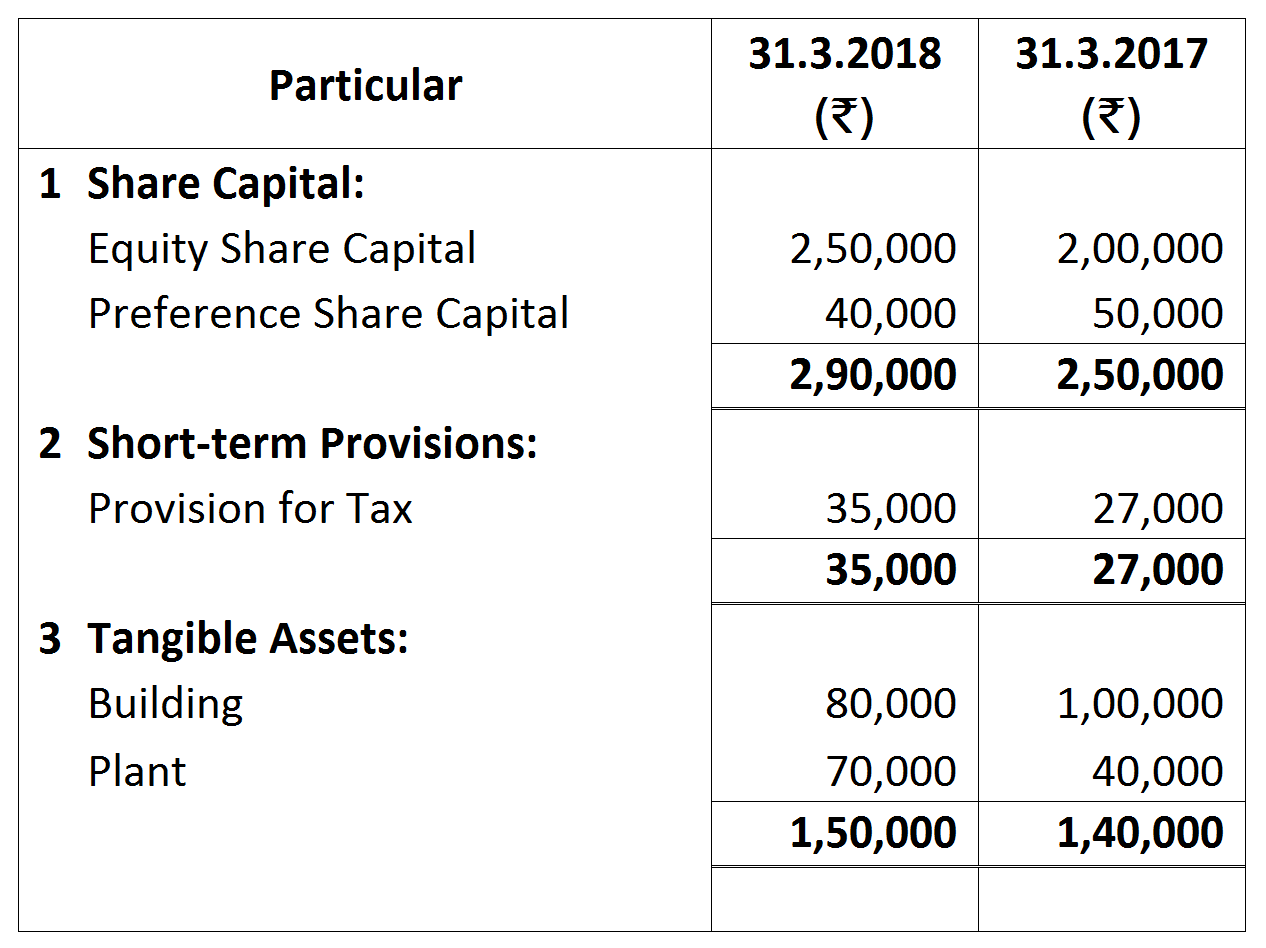

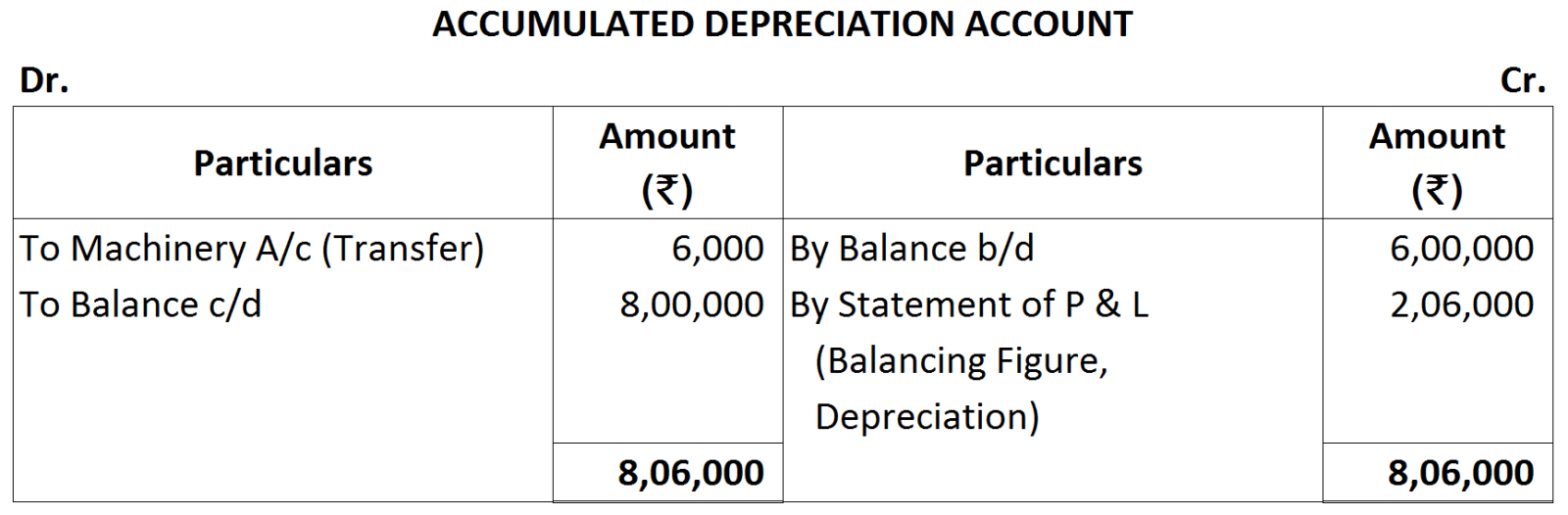

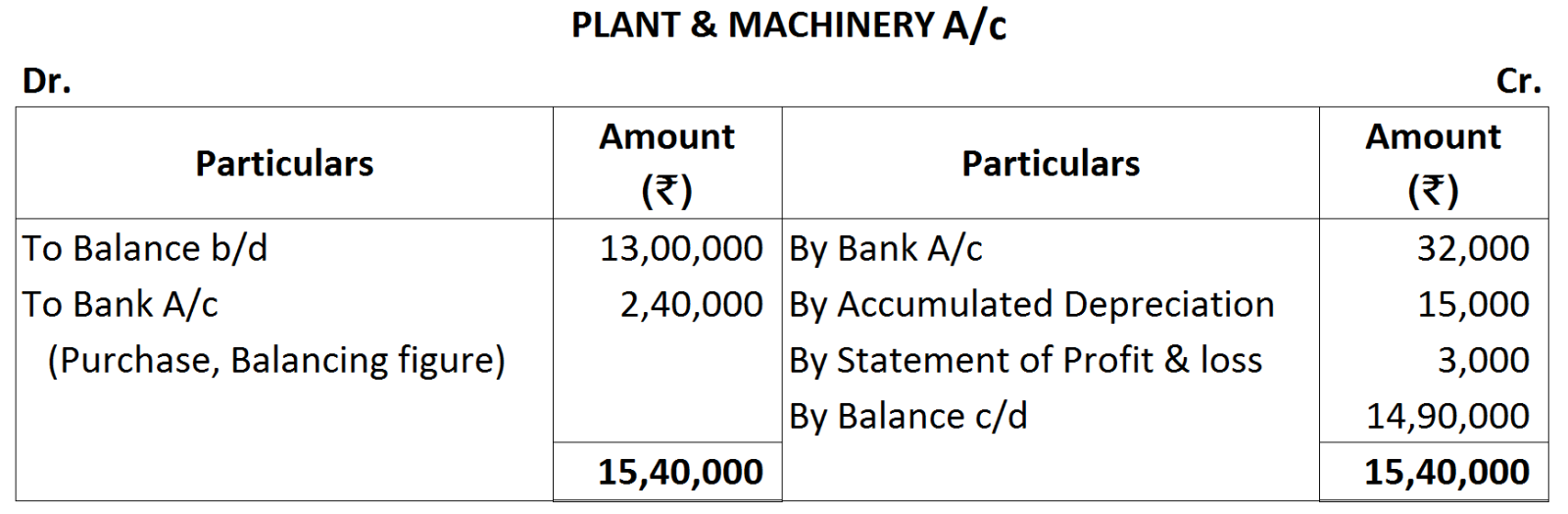

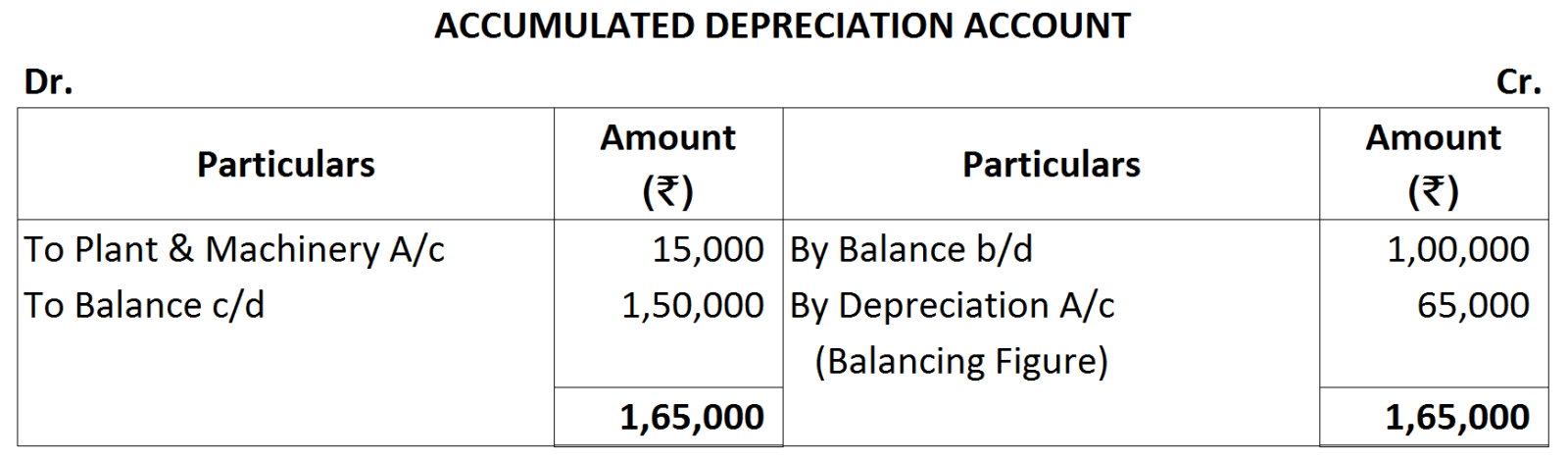

* Balancing figure of Accumulated Depreciation Ne ~ 12,000 will be transferred to the Cr. side of Plant & Machinery Account.

* Balancing figure of Accumulated Depreciation Ne ~ 12,000 will be transferred to the Cr. side of Plant & Machinery Account. Notes:

Notes:

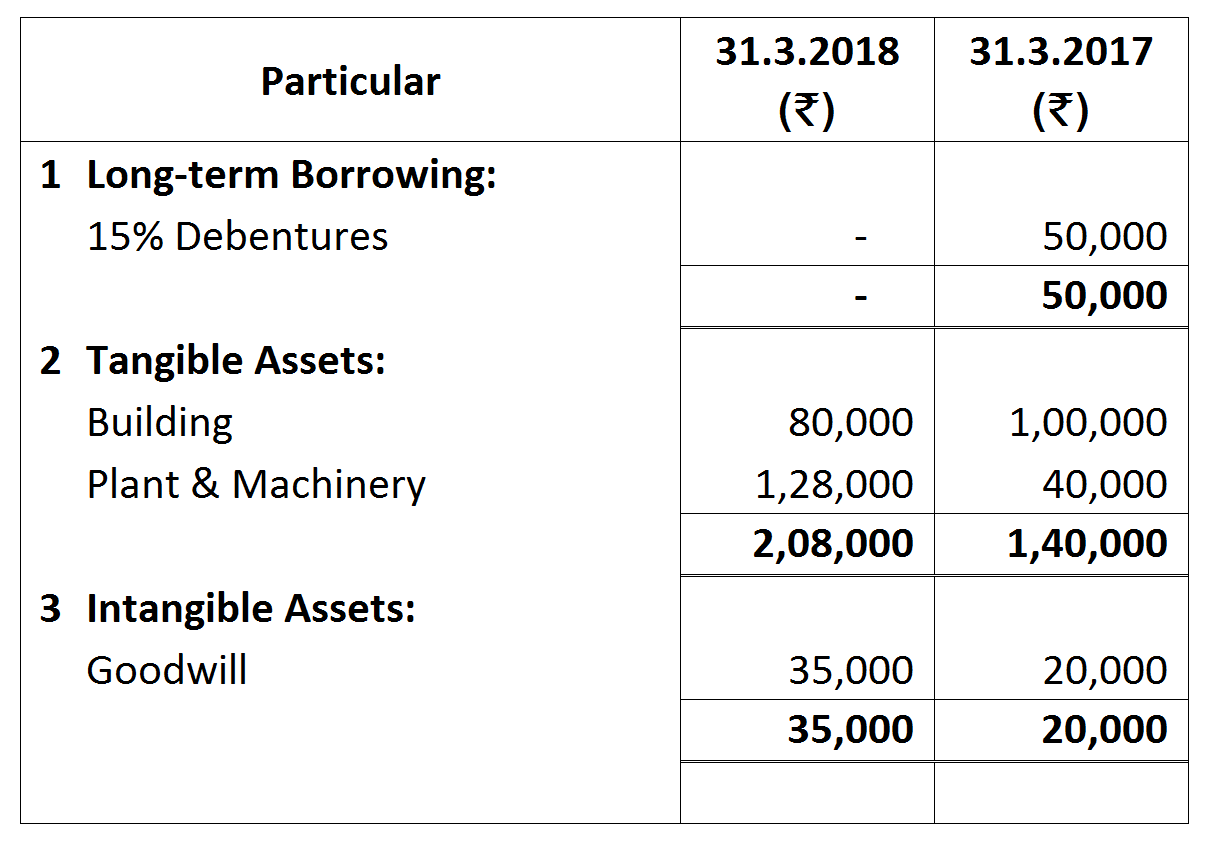

| 1. | Contingent Liability: | 31.3.2018 | 31.3.2017 |

| ₹ | ₹ | ||

| Proposed Dividend | 15,000 | 12,000 | |

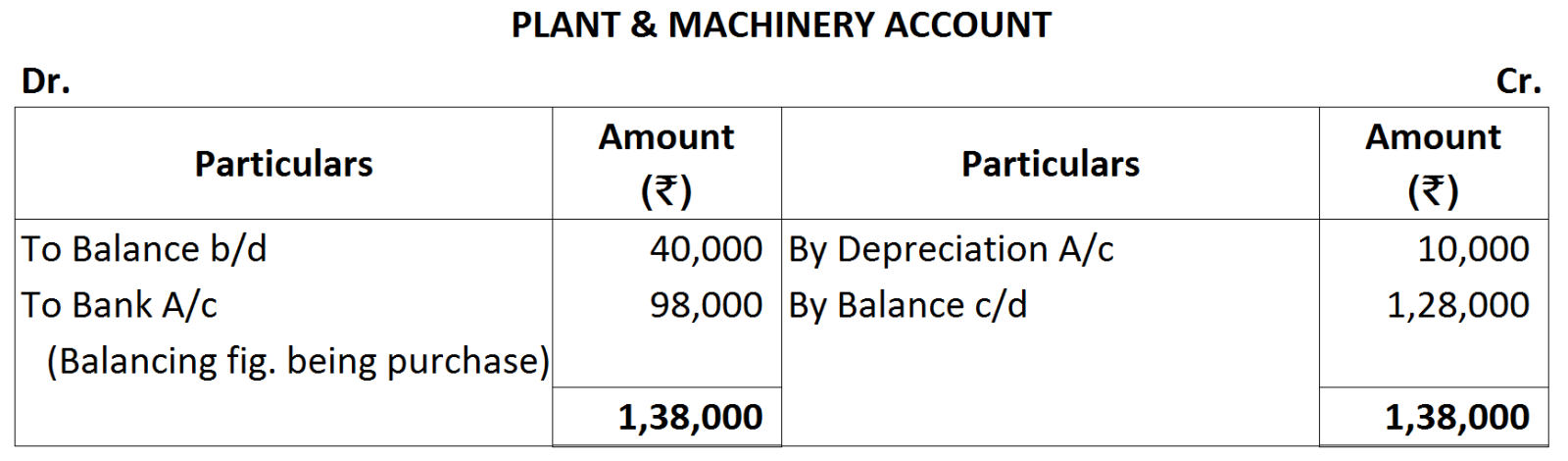

| 2. | Depreciation of ₹ 10,000 was provided on Plant & Machinery | ||

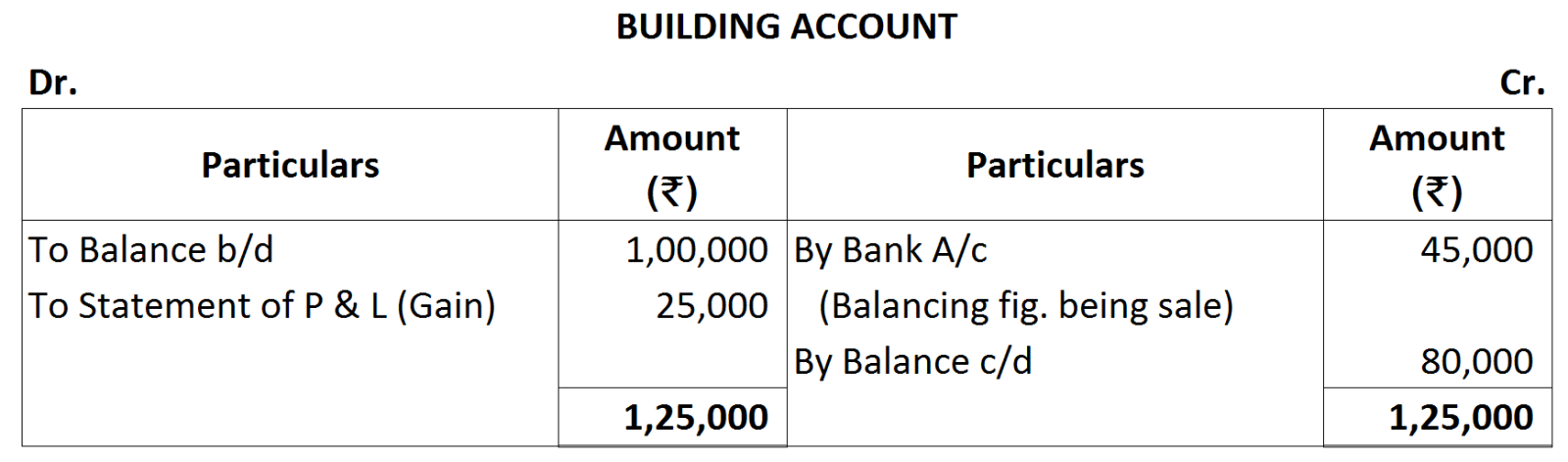

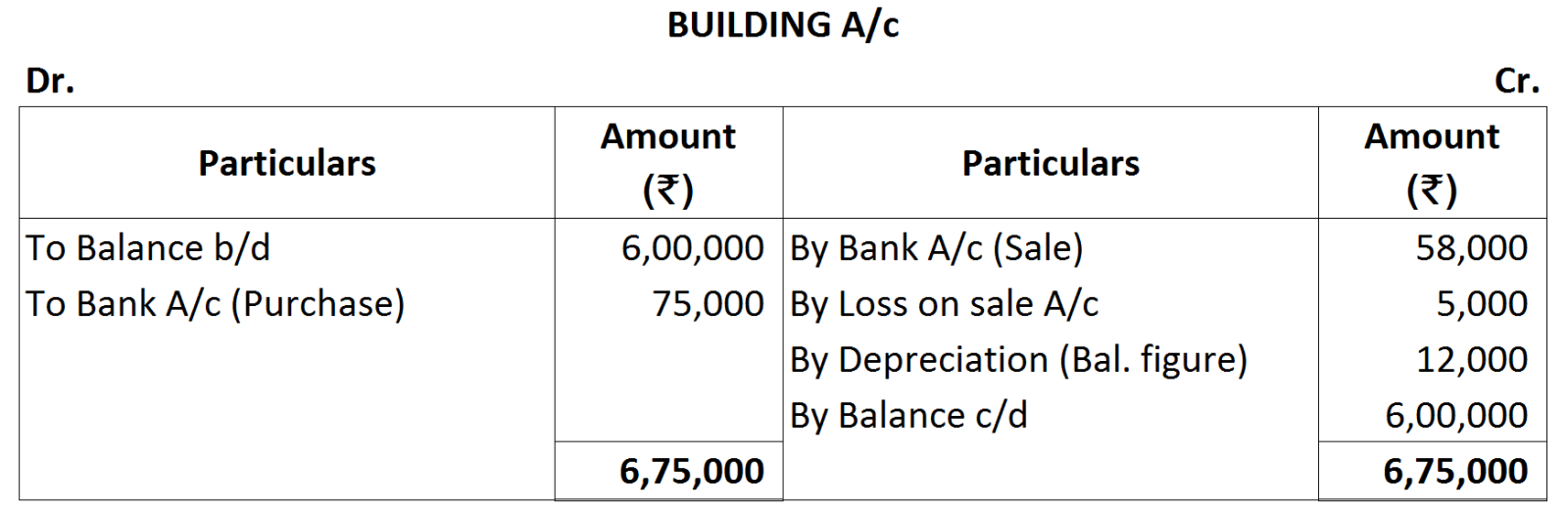

| 3. | Gain on sale of a part of Building ₹ 25,000 | ||

| 4. | Debentures were redeemed on 1st April, 2017 | ||

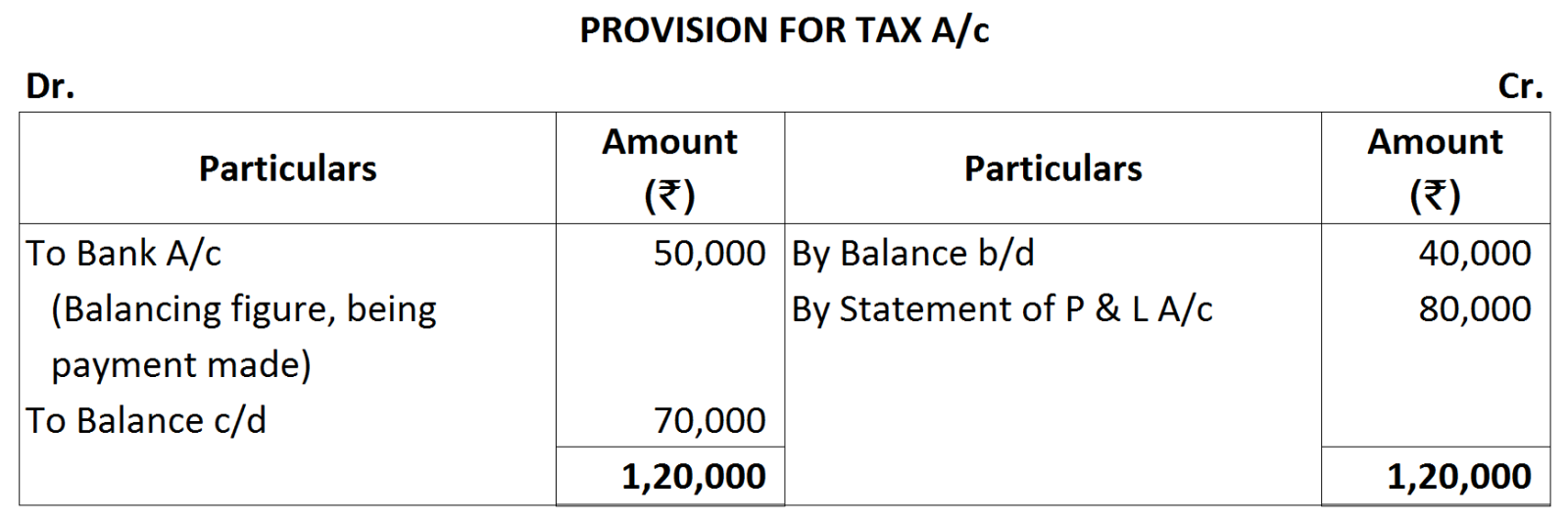

| 5. | Provision for Tax made during the year ₹ 50,000 | ||

Notes:

Notes:

|

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2018

|

1,78,000

|

|

Less: Reserve & Surplus Balance on 31st March, 2017

|

75,000

|

|

|

1,03,000

|

|

Add: Proposed Dividend for Previous year

|

12,000

|

|

Provision for Tax made during Current year

|

50,000

|

|

Net Profit before Tax

|

1,65,000

|

Notes:

Notes:

|

|

₹

|

|

Profit & Loss Balance on 31st March, 2018

|

1,20,000

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(1,59,000)

|

|

|

39,000

|

|

Add: Transfer to General Reserve

|

1,20,000

|

|

Net Profit before Tax

|

81,000

|

| ₹ | |

|

8% on 1,00,000 for 1 year

|

8,000

|

|

8% on 50,000 for 6 months

|

2,000

|

|

|

10,000

|

Notes:

Notes:  Additional Information:

Additional Information:

|

1.

|

Contingent Liability

|

31.3.2018

|

31.3.2017

|

|

|

|

₹

|

₹

|

|

|

Proposed Dividend

|

30,000

|

25,000

|

|

2.

|

Provision for tax made ₹ 30,000.

|

||

|

3.

|

Additional debentures amounting to ₹ 5,000 were issued on 1st Oct. 2017. Interest on debentures has been paid up-to date.

|

||

Working Notes:

Working Notes:

|

|

₹

|

|

Reserve & Surplus Balance (₹ 52,000 - ₹ 50,000)

|

2,000

|

|

Add: Provision for Tax for 2018

|

30,000

|

|

Proposed Dividend for 2017

|

25,000

|

|

|

57,000

|

Working Netes:

Working Netes:

|

|

₹

|

|

Statement of Profit & Loss (₹ 2,00,000 - ₹ 1,00,000)

|

1,00,000

|

|

Add: Proposed dividend for Previous Year (20% of ₹ 4,00,000)

|

80,000

|

|

Provision for Tax

|

80,000

|

|

Net Profit before Tax

|

2,60,000

|

Notes:

Notes:

|

|

₹

|

|

Profit & Loss Balance on 31st March, 2018

|

75,000

|

|

less: Profit & Loss Balance on 31st March, 2017

|

(30,000)

|

|

|

1,05,000

|

|

Add: Transfer to General Reserve

|

30,000

|

|

Dividend Paid (10% on ₹ 5,00,000)

|

50,000

|

|

Provision for Tax made during the Current year

|

15,000

|

|

Net Profit before Tax

|

2,00,000

|

Working Notes:

Working Notes:

|

|

₹

|

|

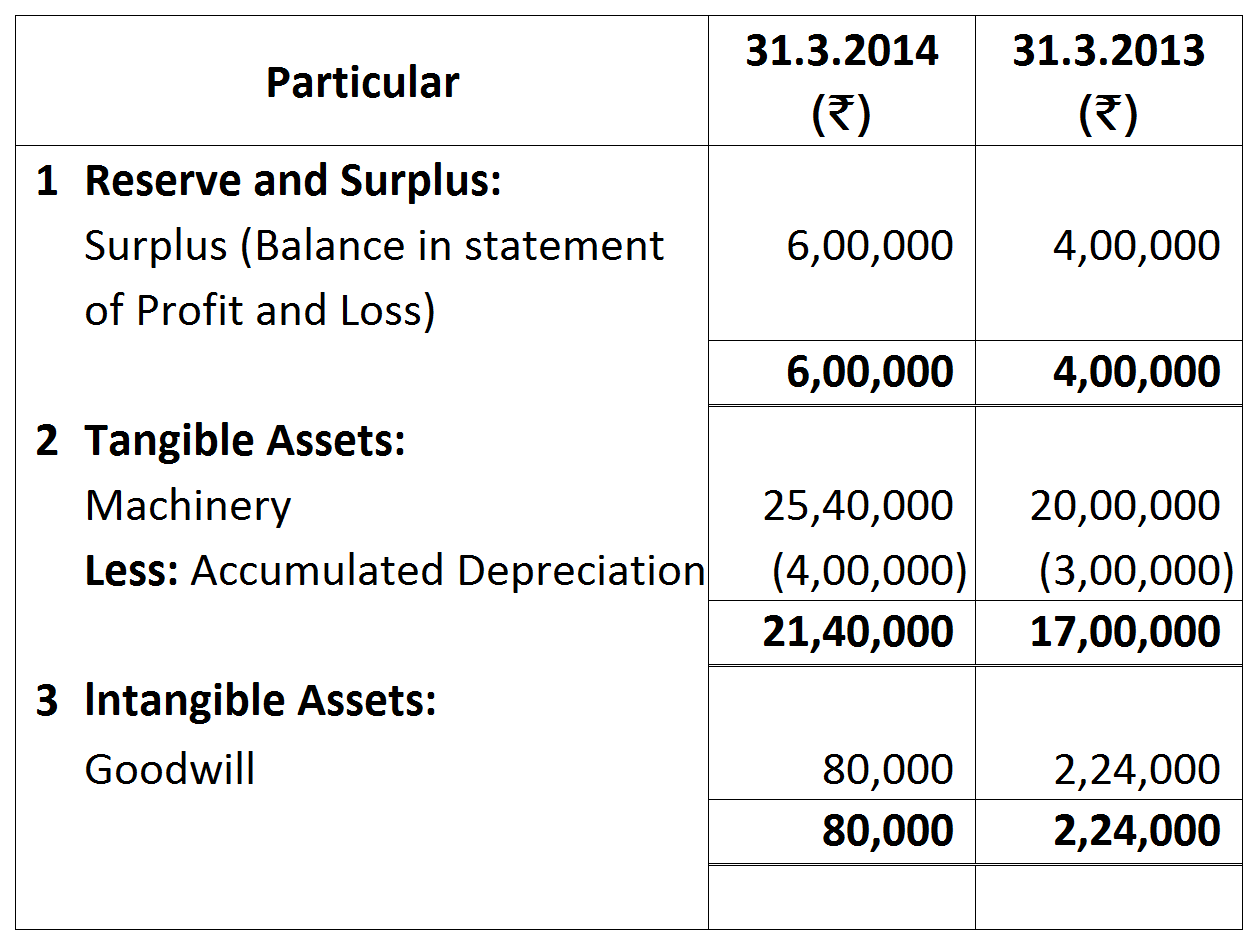

Surplus (Balance in Statement of Profit & Loss) on 31st March, 2014

|

6,00,000

|

|

less: Surplus (Balance in Statement of Profit & Loss) on 31st March, 2013

|

(4,00,000)

|

|

|

2,00,000

|

|

Add : Provision for Tax for Current Year

|

1,00,000

|

|

|

3,00,000

|

|

|

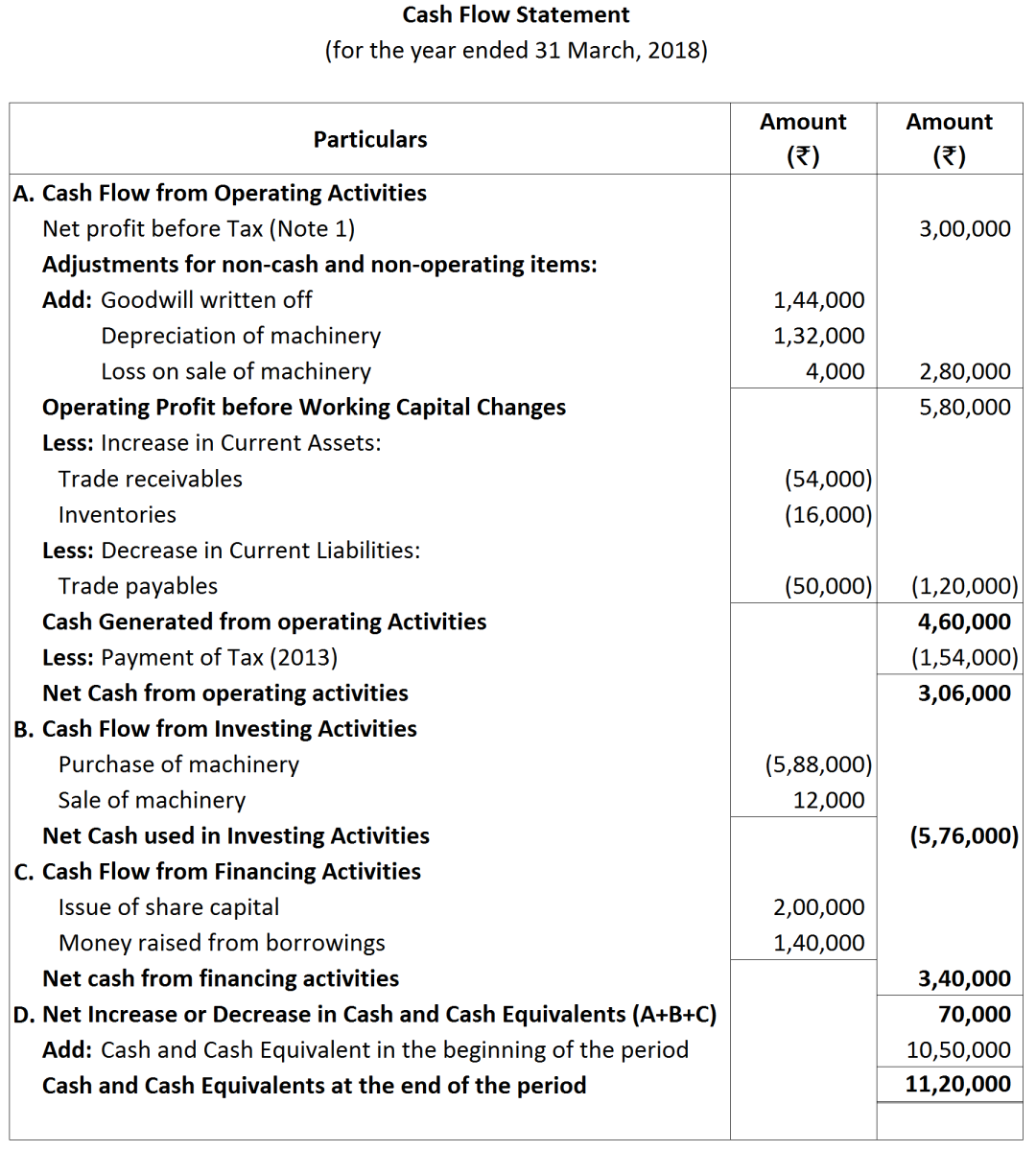

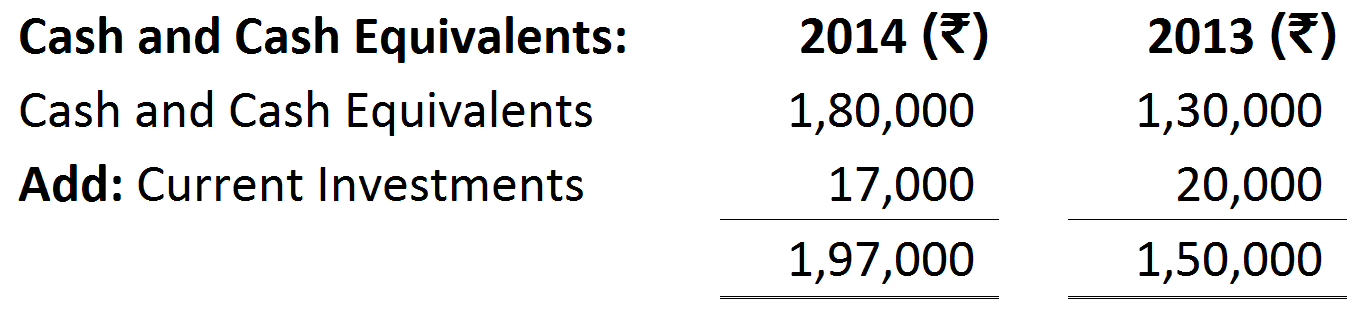

31.3.2014

|

31.3.2013

|

|

|

₹

|

₹

|

|

Cash and Bank

|

6,40,000

|

7,50,000

|

|

Current Investments

|

4,80,000

|

3,00,000

|

|

|

11,20,000

|

10,50,00

|

Notes:

Notes:

Note:

Note:

|

|

₹

|

|

Profit & Loss Balance on 31st March, 2018

|

50,000

|

|

Less: Profit & Loss Balance on 31st March, 2017

|

(37,000)

|

|

|

87,000

|

|

Add: Transfer to General Reserve

|

22,000

|

|

Provision for Tax made during the Current year

|

20,000

|

|

Net Profit before Tax

|

1,29,000

|

Notes:

Notes:

Notes:

Notes:

| ₹ | |

| Reserve and Surplus Balance on 31st March, 2018 | 1,52,000 |

| Less: Reserve and Surplus Balance on 31st March, 2017 | (50,000) |

| 1,02,000 | |

| Add: Provision for Tax made during the Current year | 33,000 |

| 1,35,000 |

Working Notes:

Working Notes:

|

|

₹

|

|

Surplus, i.e., Balance in Statement of Profit and Loss (₹ 5,00,000- ₹ 3,00,000)

|

2,00,000

|

|

Add: Provision for Tax

|

70,000

|

|

Net Profit before Tax

|

2,70,000

|

Working Notes:

Working Notes:

Notes:

Notes:

|

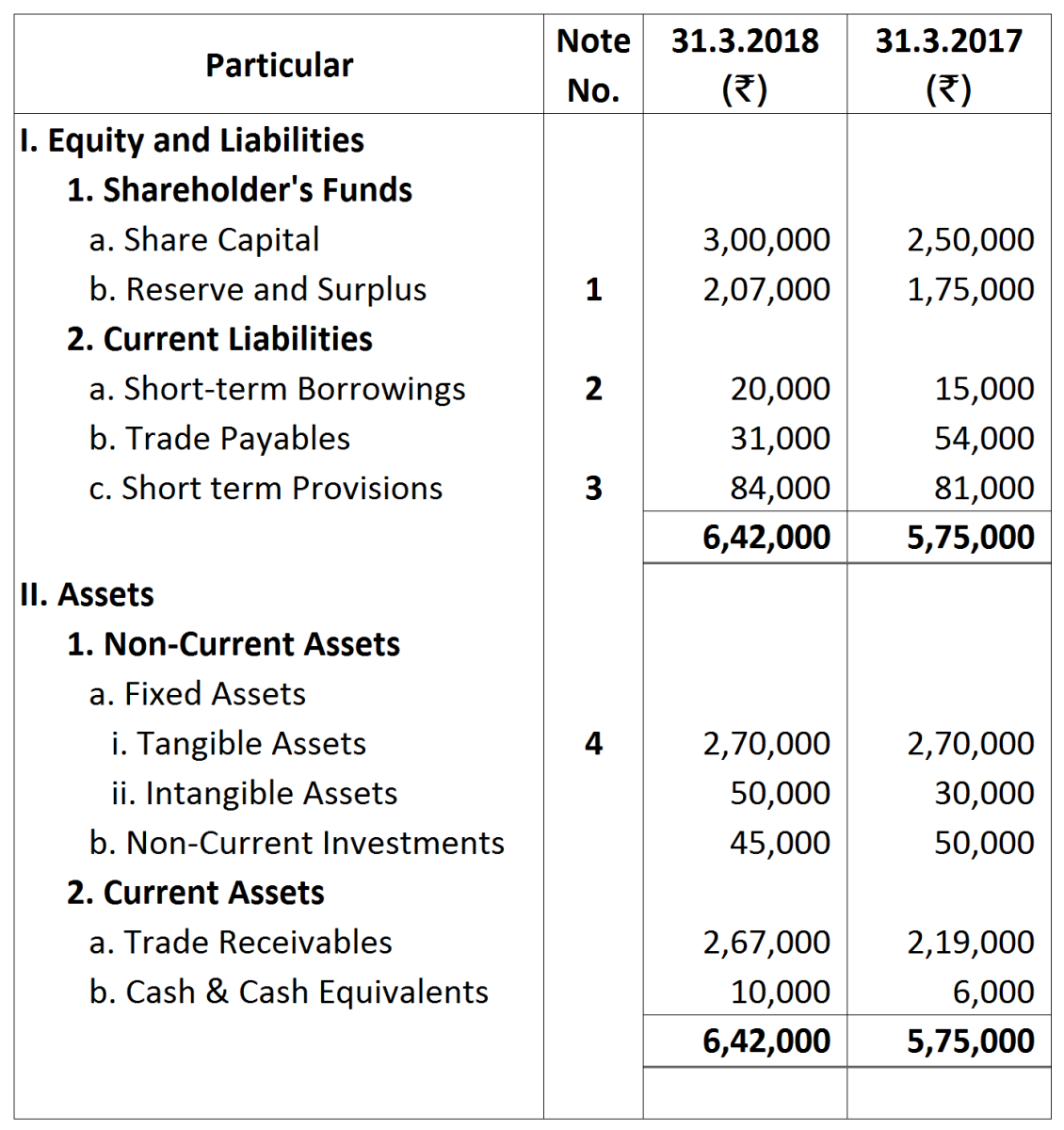

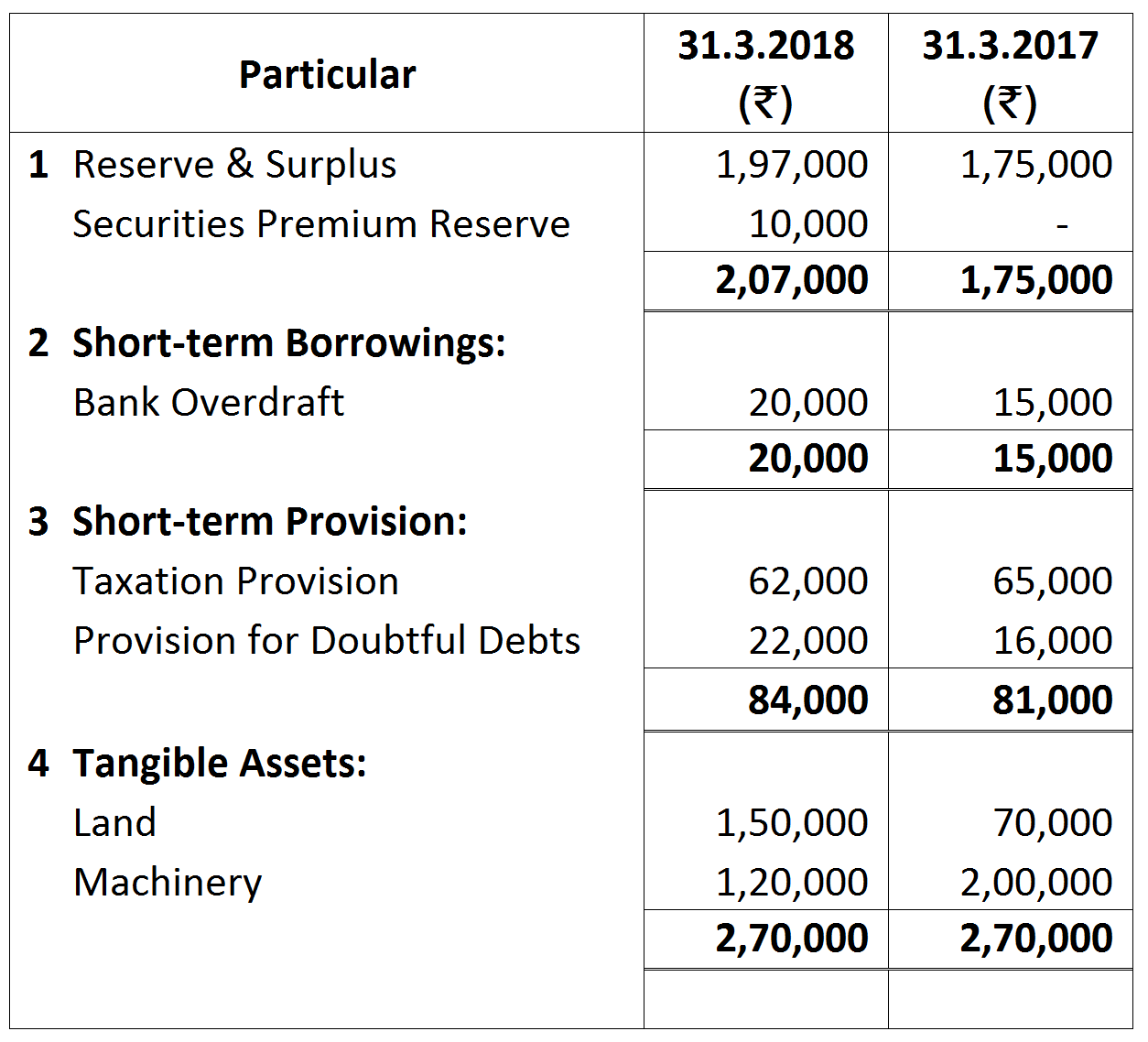

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2018

|

1,97,000

|

|

Less: Reserve & Surplus Balance on 31st March, 2017

|

(1,75,000)

|

|

|

22,000

|

|

Add: Interim Dividend Paid

|

25,000

|

|

Provision for Tax made during the Current year

|

62,000

|

|

Net Profit before Tax

|

1,09,000

|

|

|

|

₹

|

|

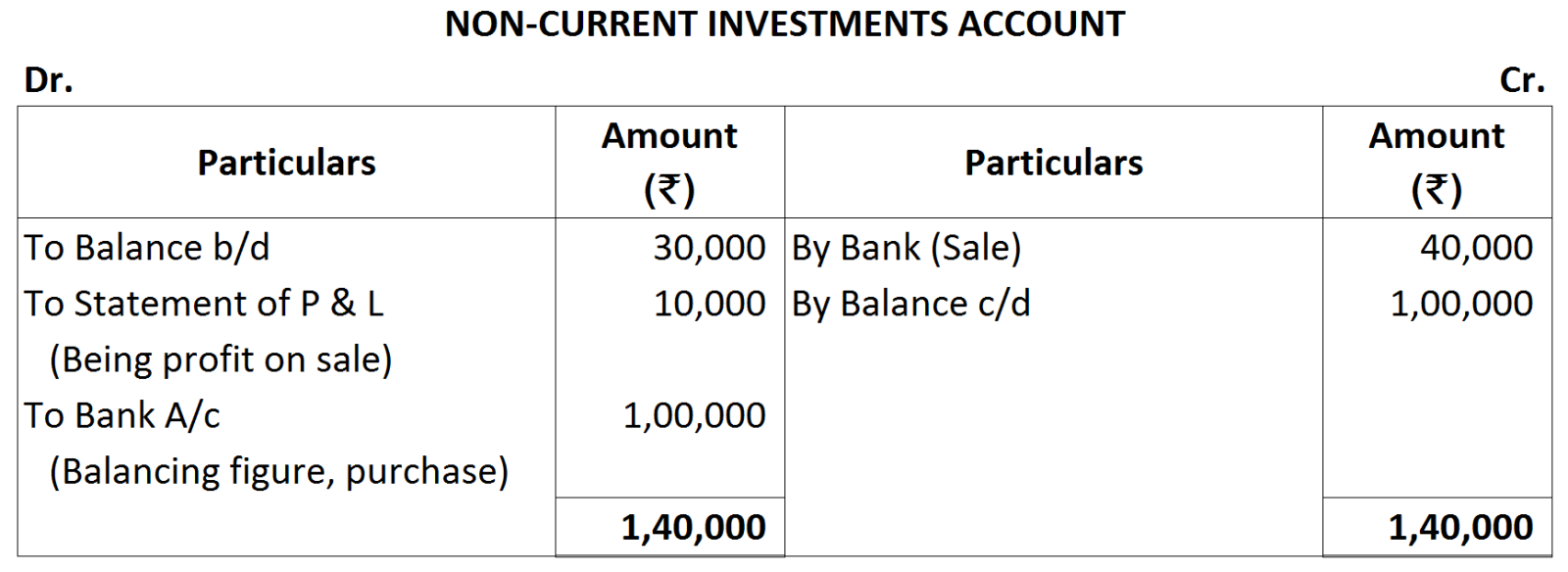

Book Value of Investments sold= 40% of ₹ 50,000

|

=

|

20,000

|

|

Loss on Sale = 20% of ₹ 20,000

|

=

|

(4,000)

|

|

Sale Price of Investments

|

|

16,000

|

Working Notes:

Working Notes:

|

|

₹

|

|

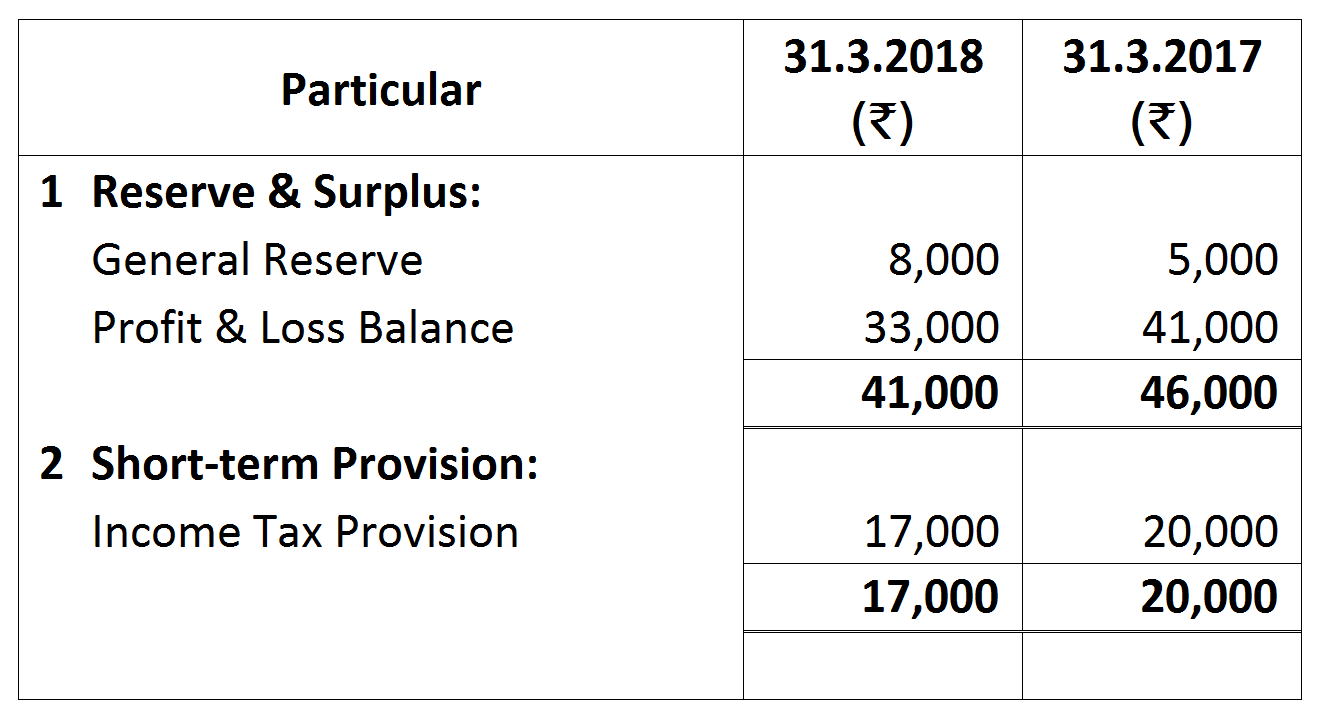

Loss for the year (₹ 33,000 - ₹ 41,000)

|

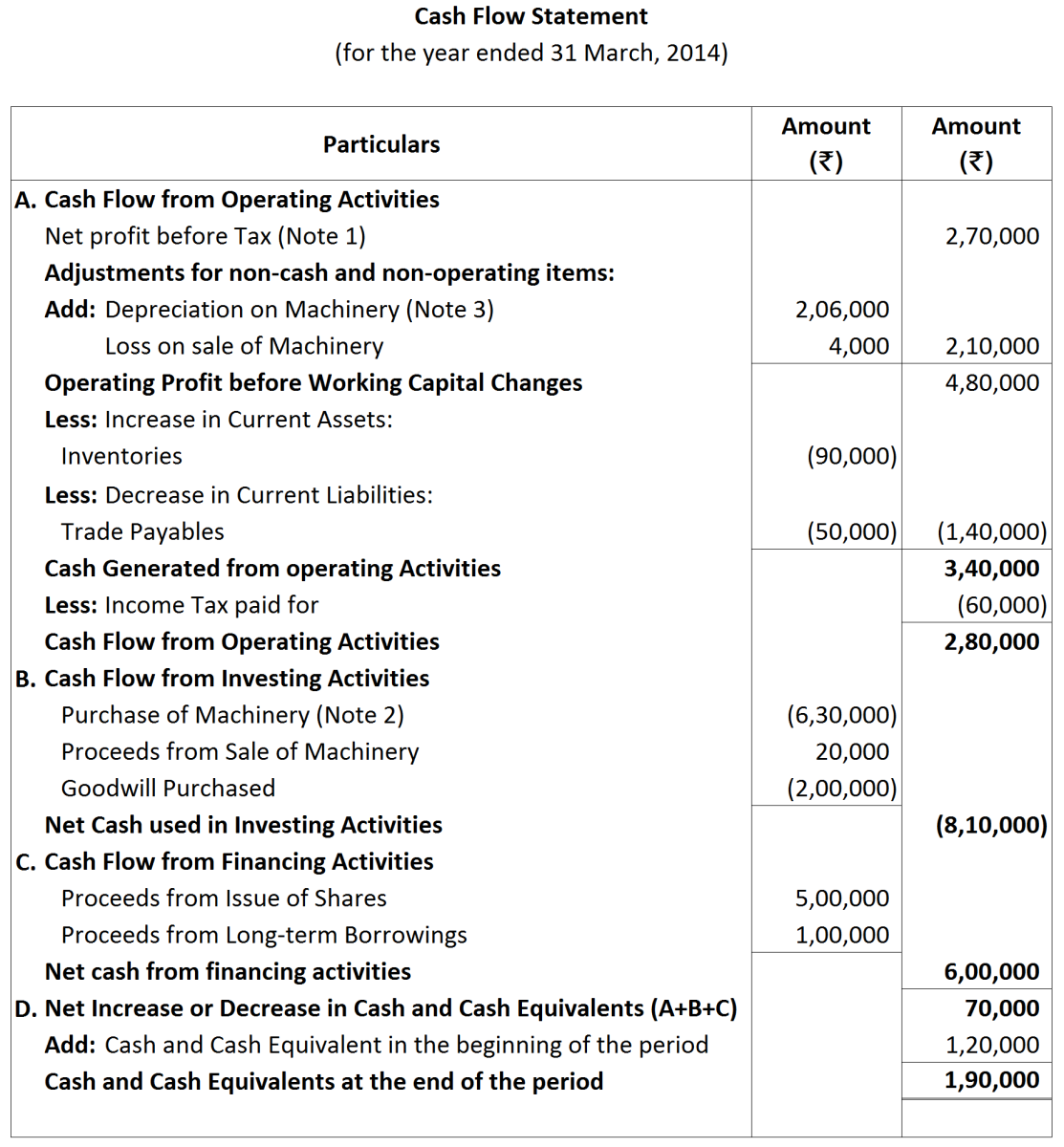

(8,000)

|

|

Add: Provision for Tax for 2018 (Note 3)

|

12,000

|

|

Transfer to General Reserve

|

3,000

|

|

Profit before Tax

|

7,000

|

Working Note:

Working Note:

| ₹ | |

| Profit for the year: | |

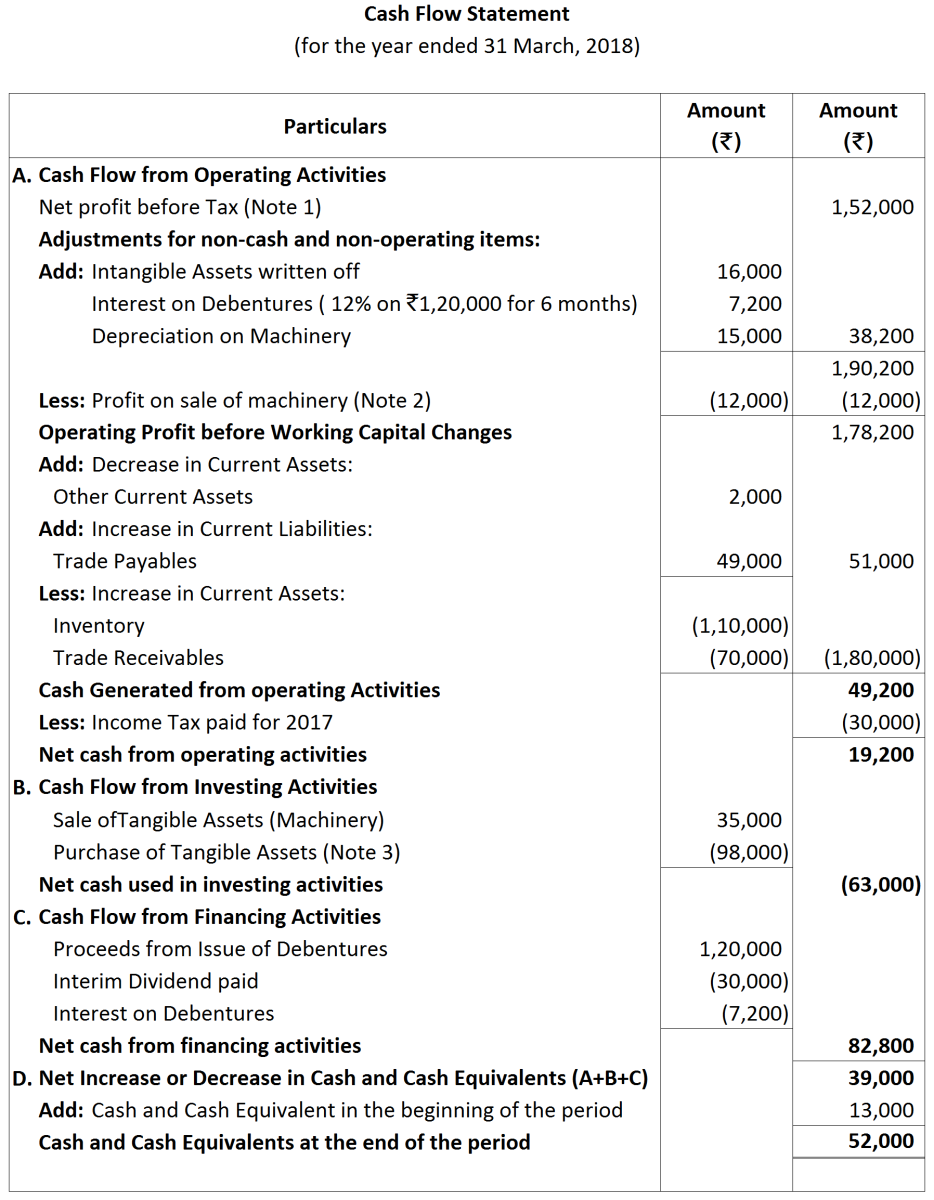

| Reserve and Surplus on 31st March, 2018 | 1,07,000 |

| (-) Reserve and Surplus on 31st March, 2017 | (25,000) |

| 82,000 | |

| Add: Provision for Taxation for 2018 | 40,000 |

| Interim Dividend paid ( 15% on ₹ 2,00,000) | 30,000 |

| 1,52,000 |

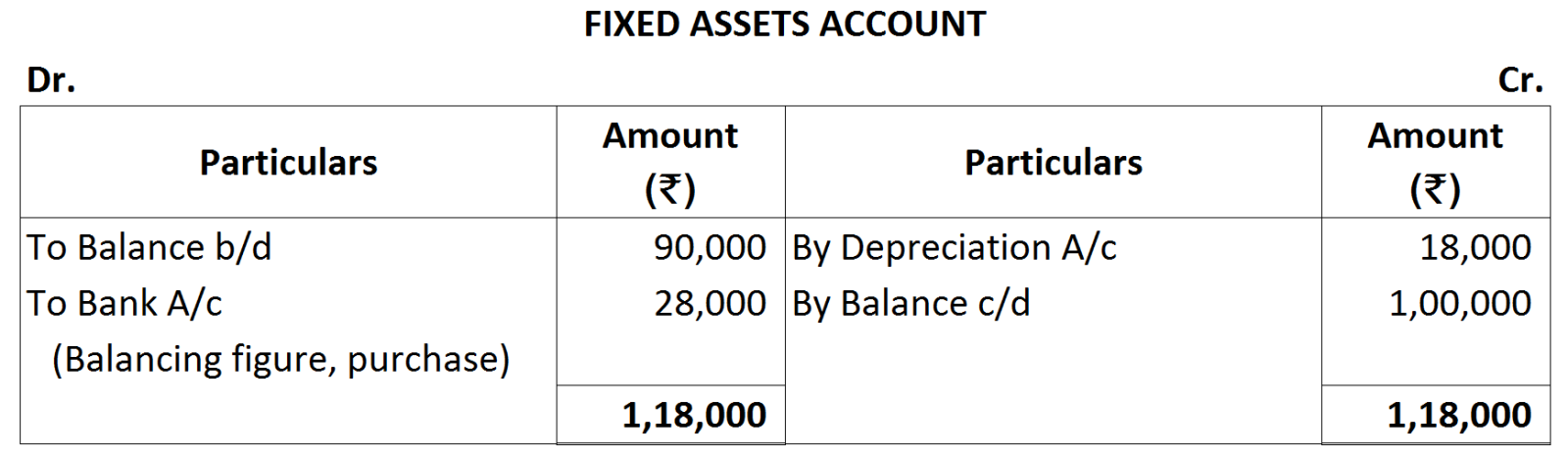

|

|

₹

|

|

Cost of Machine sold

|

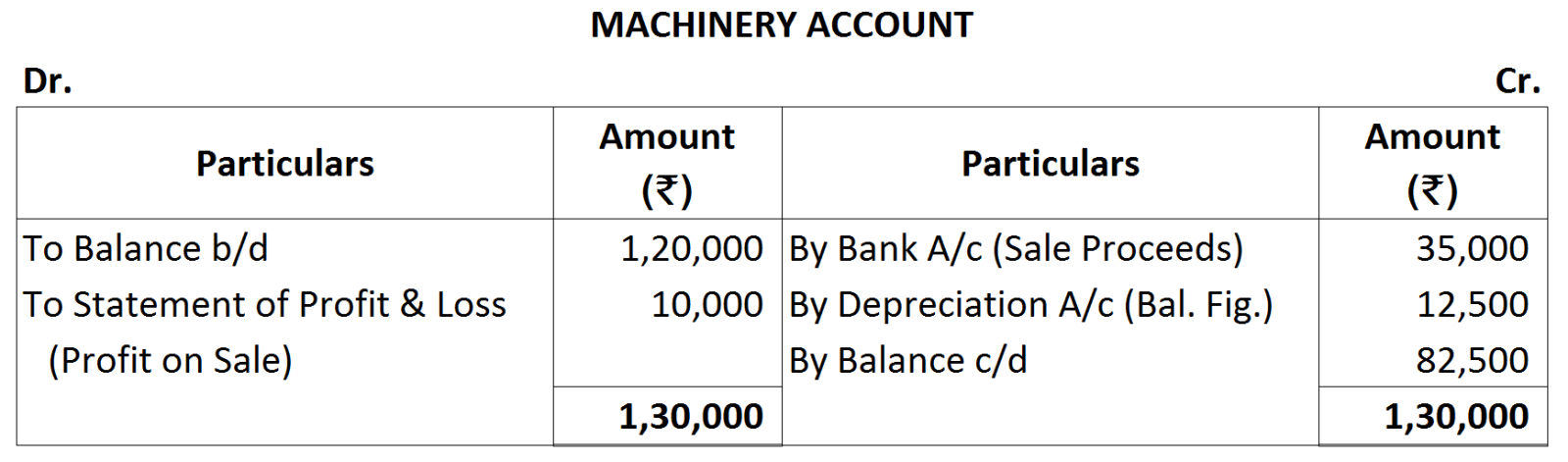

50,000

|

|

Less: Accumulated Depreciation thereon

|

(27,000)

|

|

Written down value of Machine sold

|

23,000

|

|

Sale amount of Machine

|

35,000

|

|

Profit on sale of Machine

|

12,000

|

Working Notes:

Working Notes:

|

|

₹

|

|

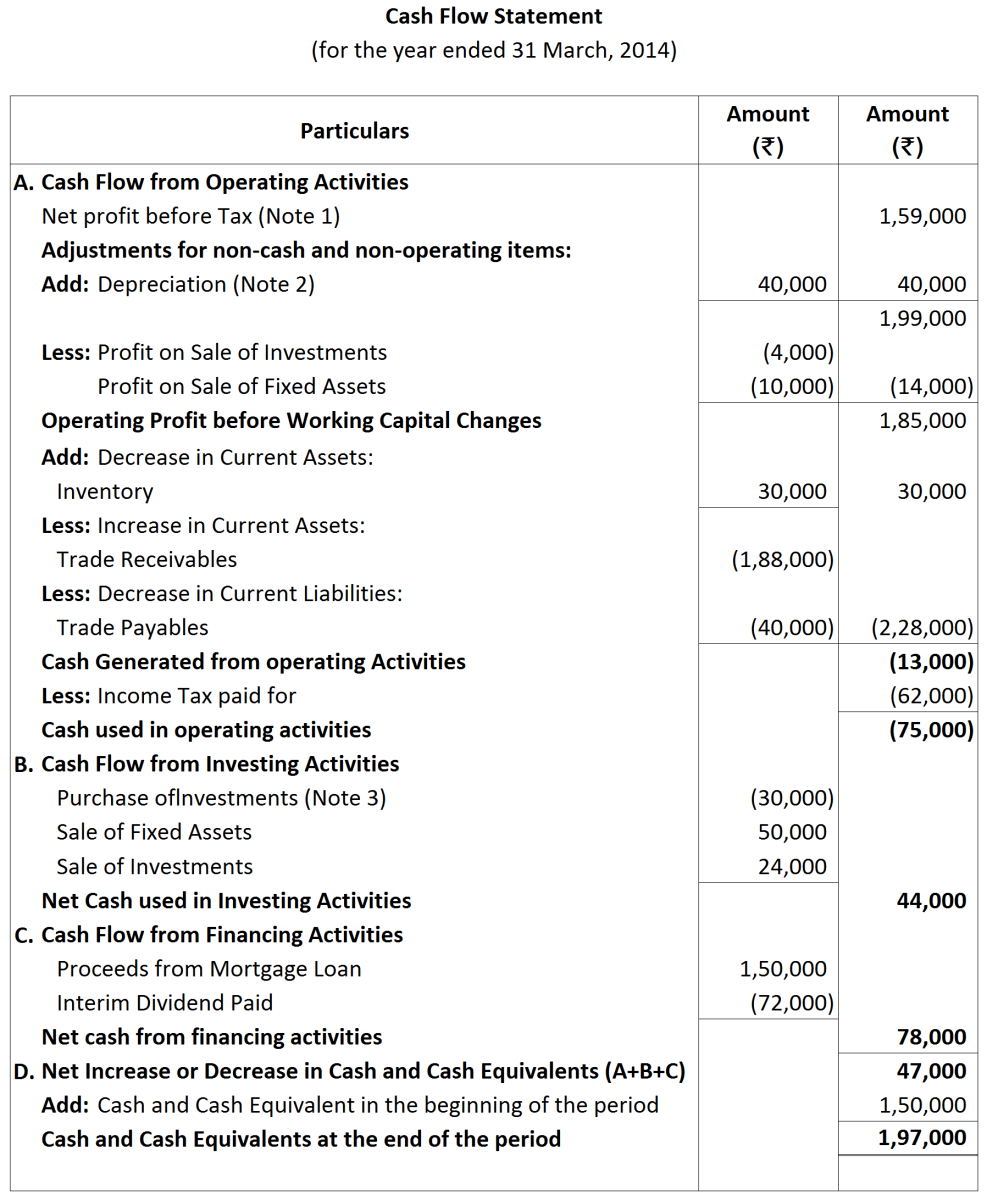

Profit & Loss Balance on 31st March, 2014

|

50,000

|

|

Less: Profit & Loss Balance on 31st March, 2013

|

(70,000)

|

|

|

20,000

|

|

Add: Increase in General Reserve

|

50,000

|

|

Interim Dividend paid (12% on ₹ 6,00,000)

|

72,000

|

|

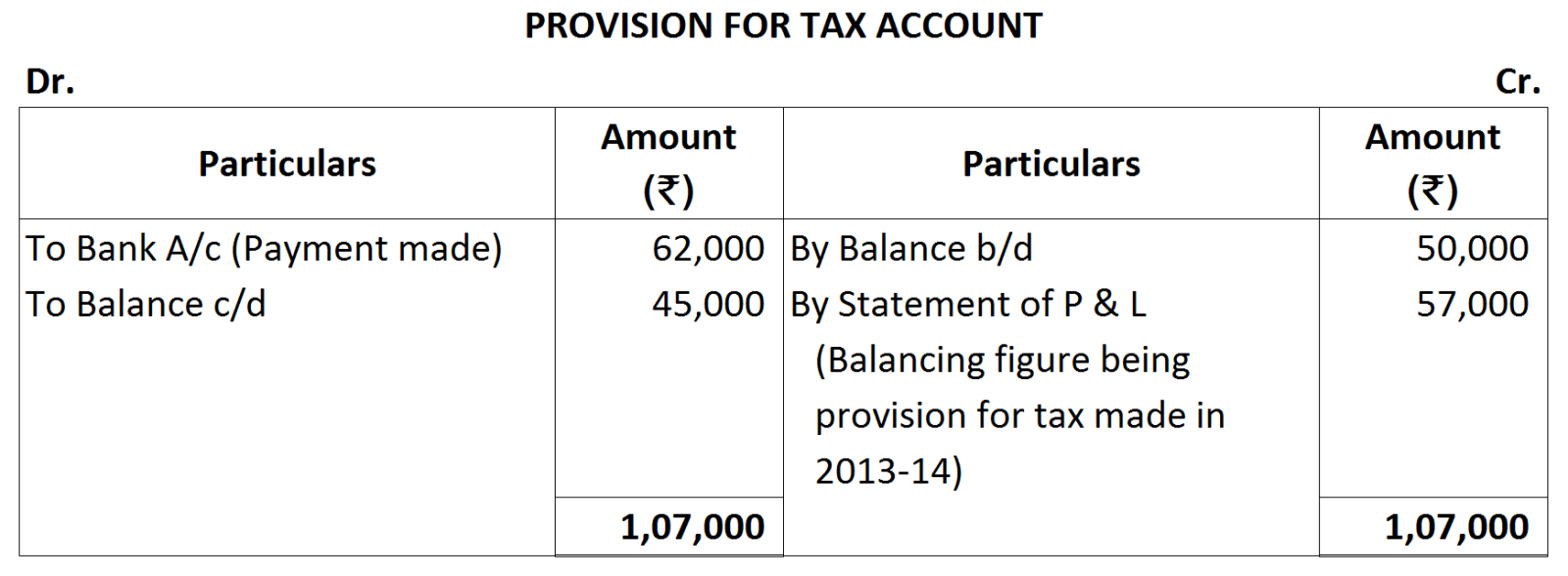

Provision for Tax made during current year (Note 4)

|

57,000

|

|

Net Profit before Tax

|

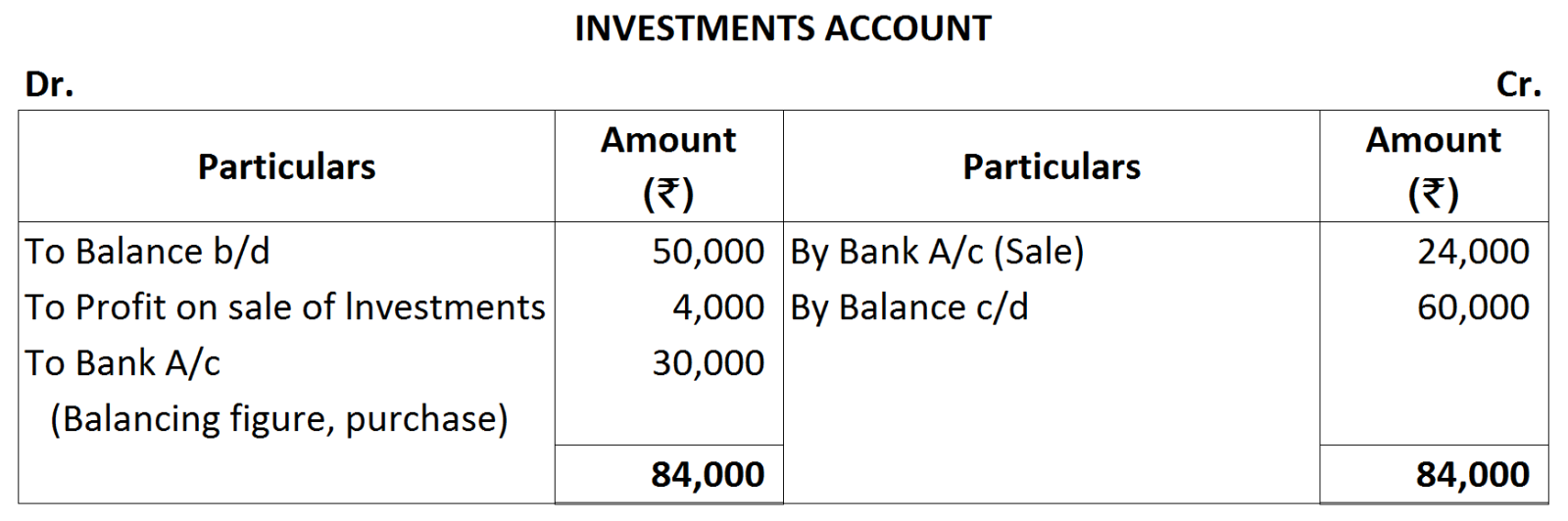

1,59,000

|

Notes:

Notes:

Notes:

Notes:

|

|

₹

|

|

Reserve & Surplus Balance on 31st March, 2018

|

25,000

|

|

Less: Reserve & Surplus Balance on 31st March, 2017

|

(30,000)

|

|

|

5,000

|

|

Add: Provision for Tax made during the Current year

|

30,000

|

|

|

25,000

|

Working Notes:

Working Notes:

Notes:

Notes: