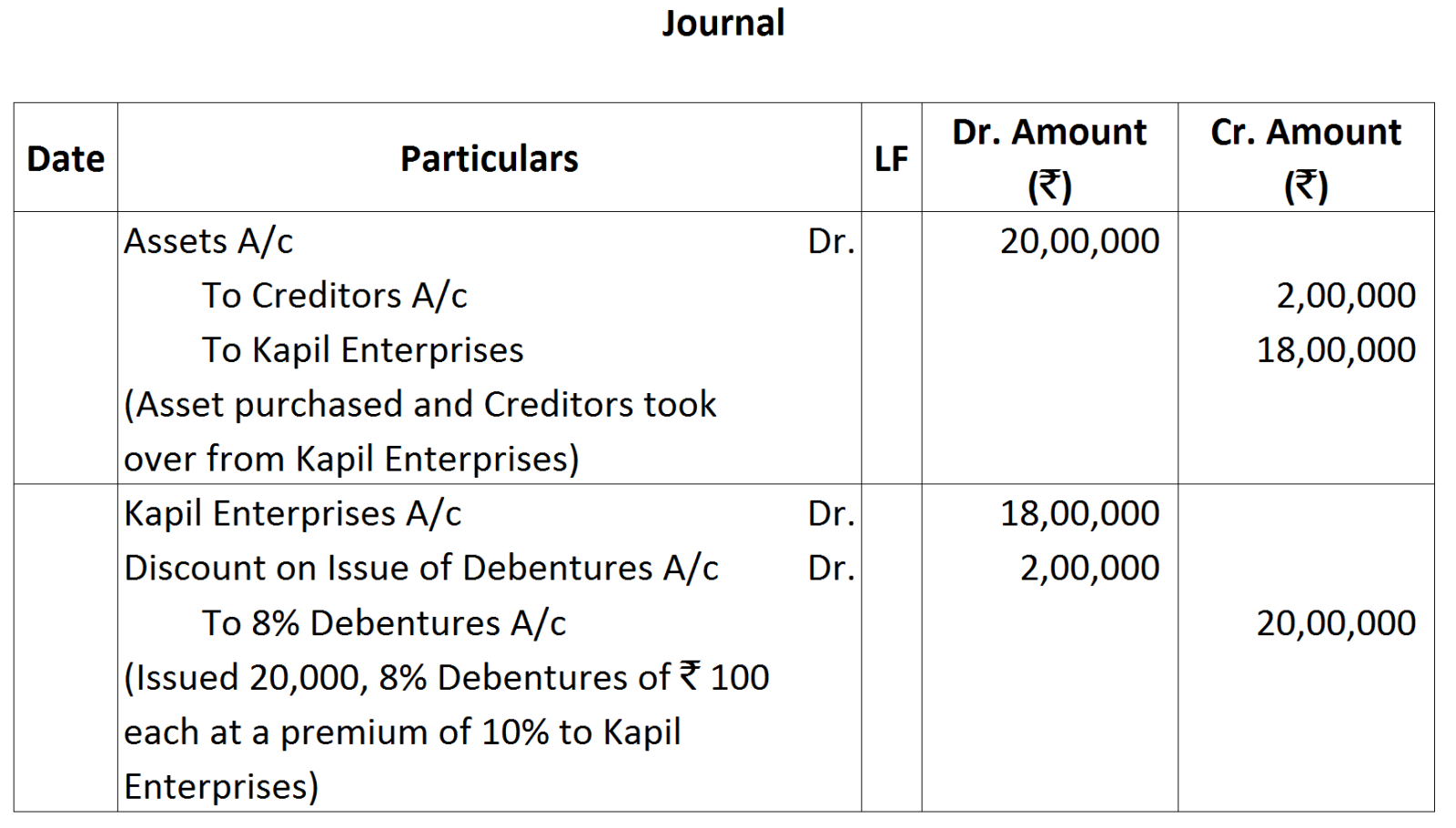

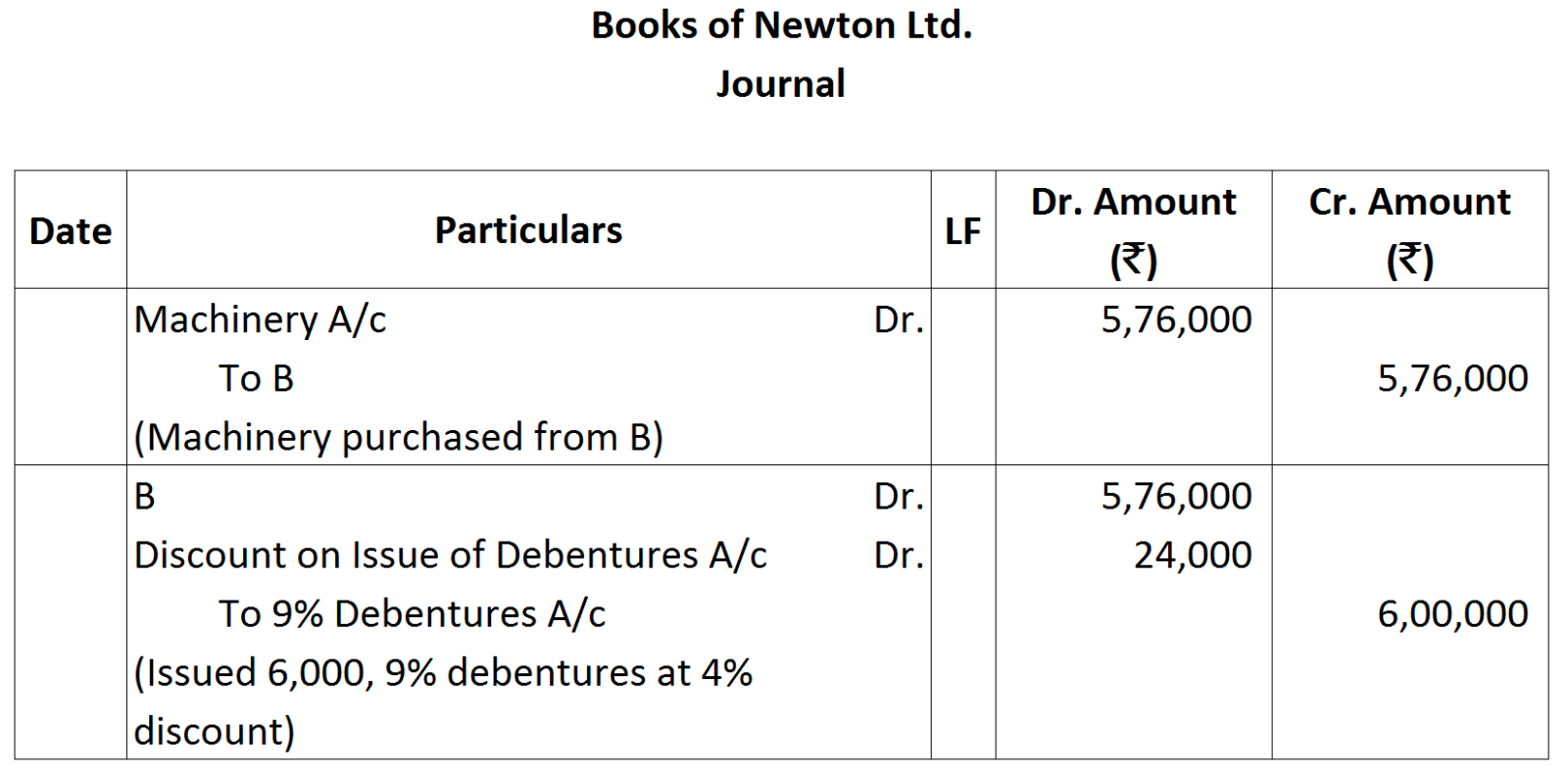

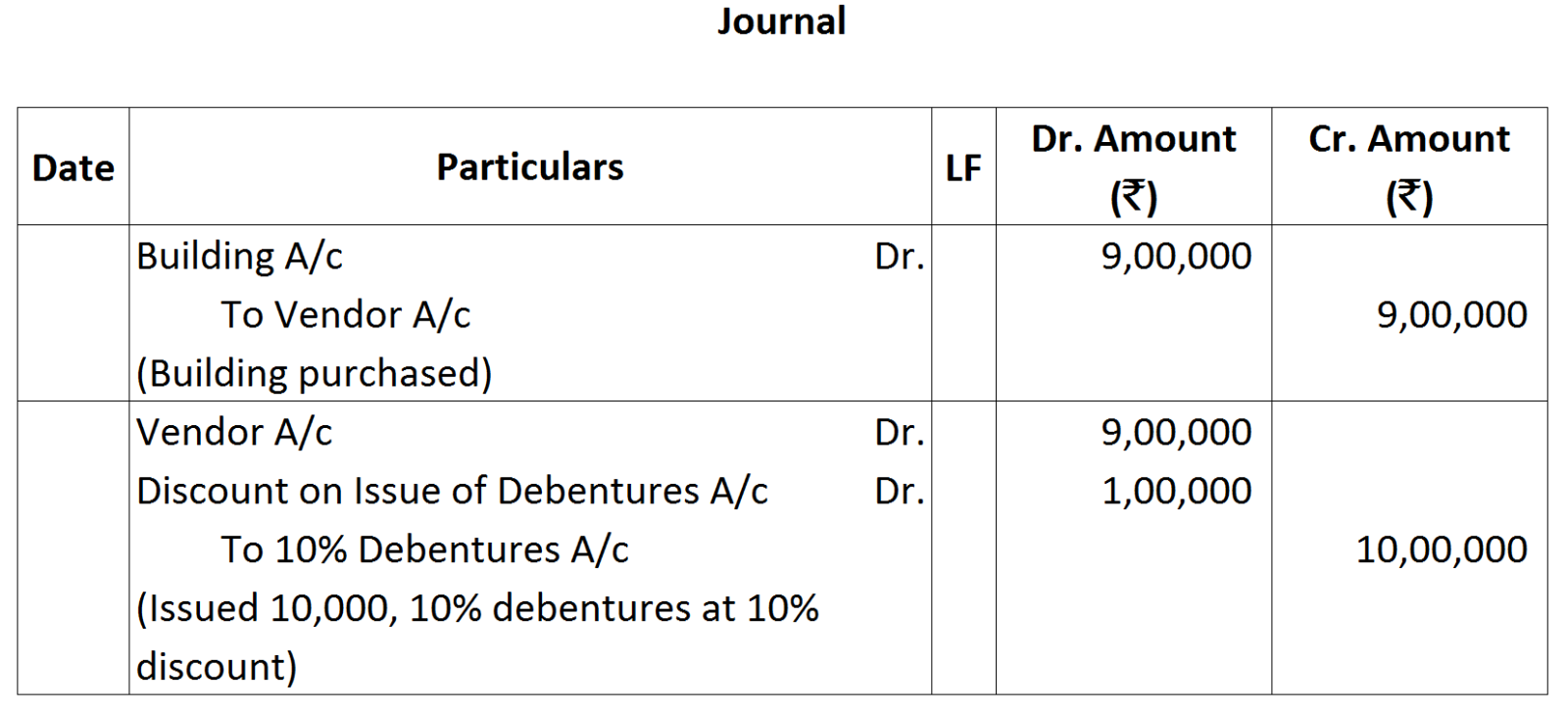

Question 13 Marks

Pass journal entries in the following cases:

A Co.Ltd. issued ₹ 40,000; 12% Debentures at a premium of 5% redeemable at par.

A Co.Ltd. issued ₹ 40,000; 12% Debentures at a premium of 5% redeemable at par.

37 questions · timed · auto-graded

|

Year end

|

2nd

|

3rd

|

4th

|

5th

|

|

Nominal value of Debentures to be Redeemed.

|

10%

|

20%

|

30%

|

40%

|

| At the end of | Outstanding Balance | Weight | Discount Written-off |

| Year I | 10,00,000 | 10 | $15,000\Big(\frac{10}{40}\times60,000\Big)$ |

| Year II | 10,00,000 | 10 | $15,000\Big(\frac{10}{40}\times60,000\Big)$ |

| Year III | 9,00,000 | 9 | $13,500\Big(\frac{9}{40}\times60,000\Big)$ |

| Year IV | 7,00,000 | 7 | $10,500\Big(\frac{7}{40}\times60,000\Big)$ |

| Year V | 4,00,000 | 4 | $6,000\Big(\frac{4}{40}\times60,000\Big)$ |

| 40 |

Note:

Note: Note:

Note:

Note:

Note: Note:

Note:

|

|

Basis

|

Debenture

|

Share

|

|

1

|

Ownership

|

Debenture means debt taken by the company. Therefore, a debentureholder is a lender.

|

Share means capital. Hence, a shereholder is the Owner.

|

|

2

|

Return.

|

Debentureholder gets interest at the stated rate whether the company earns profit or not.

|

A shareholder gets dividend on investment.

|

|

3

|

Repayment.

|

Debenture are issued for a specified period. Hence, the amount of debentures is repaid on the due date.

|

Normally, the amount of share is not repaid during the lifetime of the company. However, preference share have a specified life and are redeemed on due date.

|

|

4

|

Issue at Discount.

|

Debenture can be issued at discount.

|

Share cannot be issued at discount except Sweat Equity shares.

|

|

5

|

Security.

|

Debentures may or may not be secured by a change on the assets of the company.

|

Share are not secured.

|

| Year-end | Amount (Face Value) (₹) |

| 2 | 1,00,000 |

| 3 | 2,00,000 |

| 4 | 3,00,000 |

| 5 | 4,00,000 |

| Year end | Outstanding Amount (₹) | Ratio | Discount |

| 1 | 10,00,000 | 10 | $80,000\times\frac{10}{40}\times20,000$ |

| 2 | 10,00,000 | 10 | $80,000\times\frac{10}{40}\times20,000$ |

| 3 | 9,00,000 | 9 | $80,000\times\frac{9}{40}\times18,000$ |

| 4 | 7,00,000 | 7 | $80,000\times\frac{7}{40}\times14,000$ |

| 5 | 4,00,000 | 4 | $80,000\times\frac{4}{40}\times8,000$ |

| Total | 40 | 80,000 |

Working Note:

Working Note: Note:

Note: Note:

Note: Note:

Note: