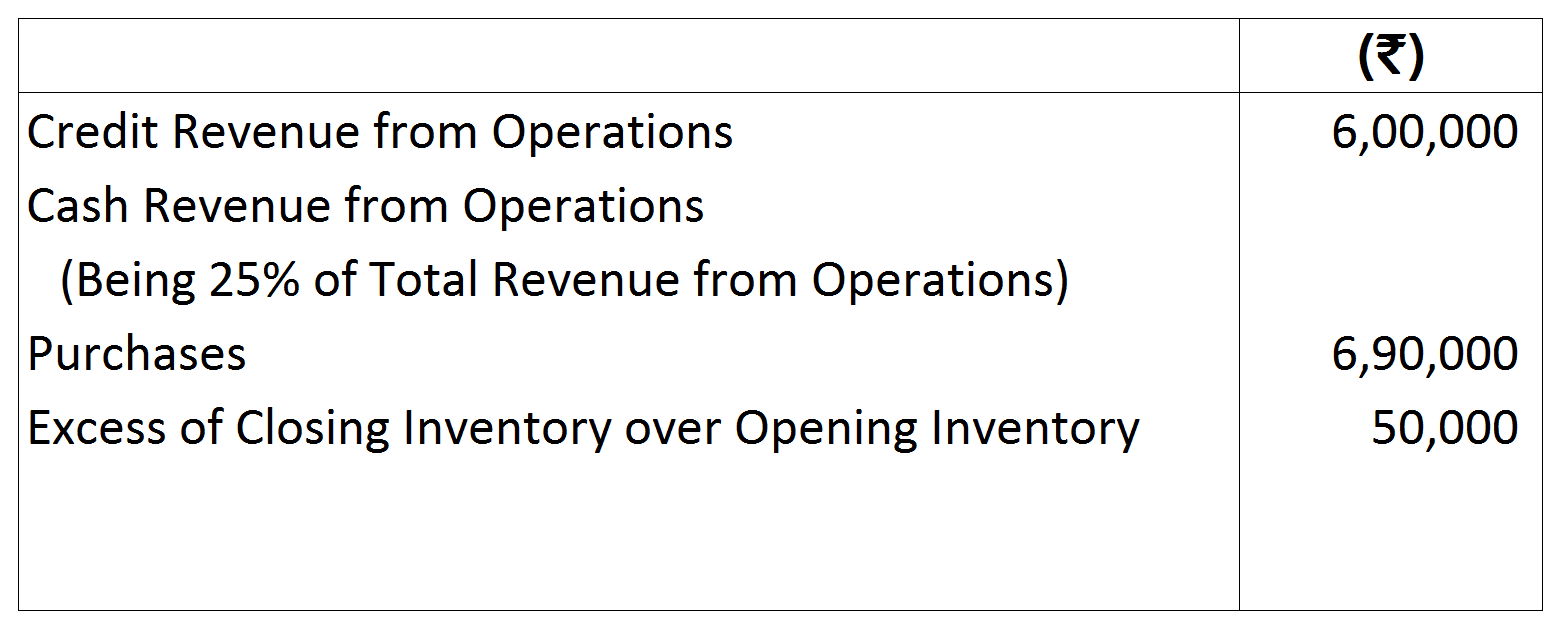

Question

Calculate G.P. Ratio from the following:

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

2,00,000 divided into 20,000 shares of

2,00,000 divided into 20,000 shares of ₹ 10 each. 6,000 of these shares were issued to the vendor for building purchased. 8,000 shares were issued to the public and

₹ 10 each. 6,000 of these shares were issued to the vendor for building purchased. 8,000 shares were issued to the public and  ₹ 5 per share were called up as follows:

₹ 5 per share were called up as follows:

₹ 2 per share

₹ 2 per share ₹ 1 per share

₹ 1 per share 3 per share

3 per share ₹ 2 per share

₹ 2 per share ₹ 2 per share were received.

₹ 2 per share were received.| On application and allotment | - | ₹ 4 per share, |

| On first Call | - | ₹ 3 per share, |

| On second and final Call | - | balance. |

| On application and allotment | ₹ 50 per share, |

| On first call | ₹ 25 per share, |

| On second and final call | ₹ 25 per share. |