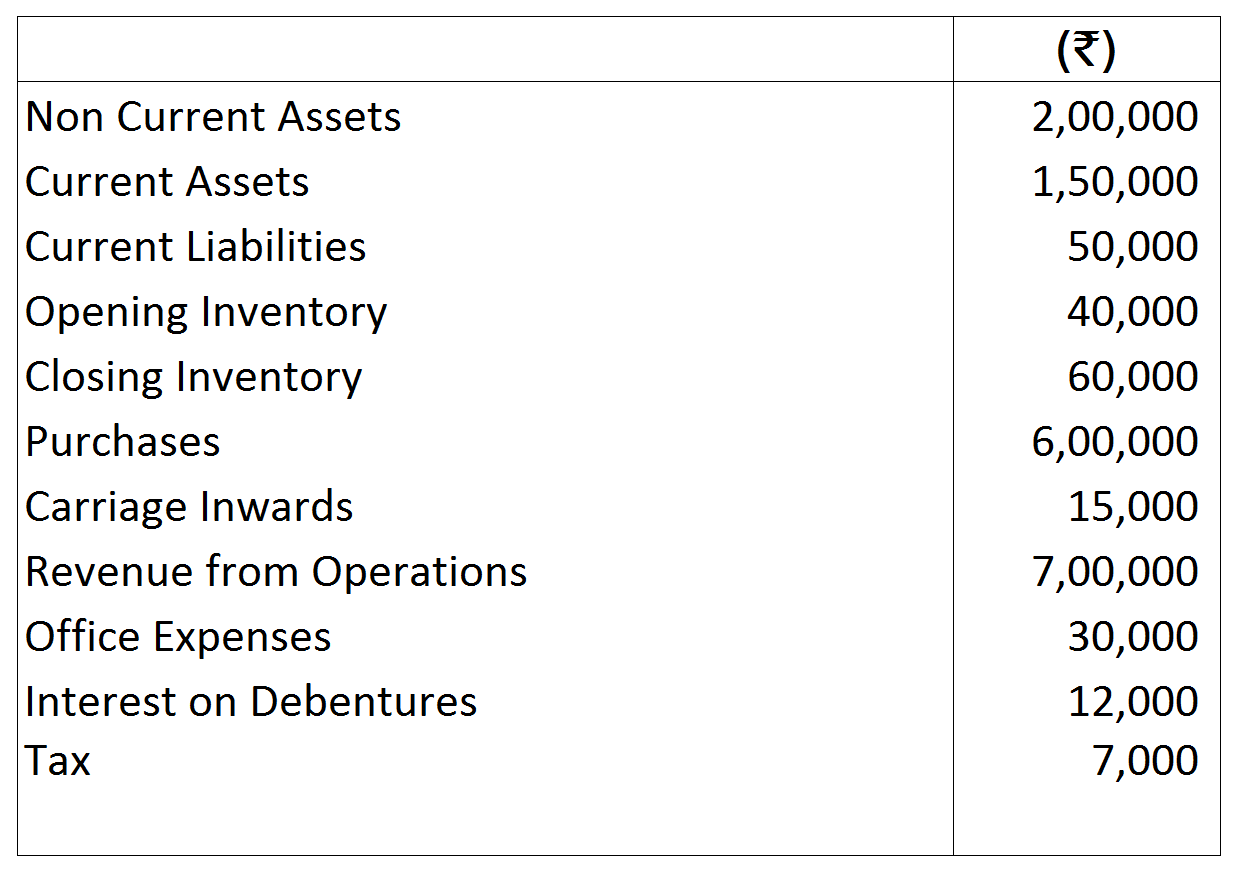

Question 16 Marks

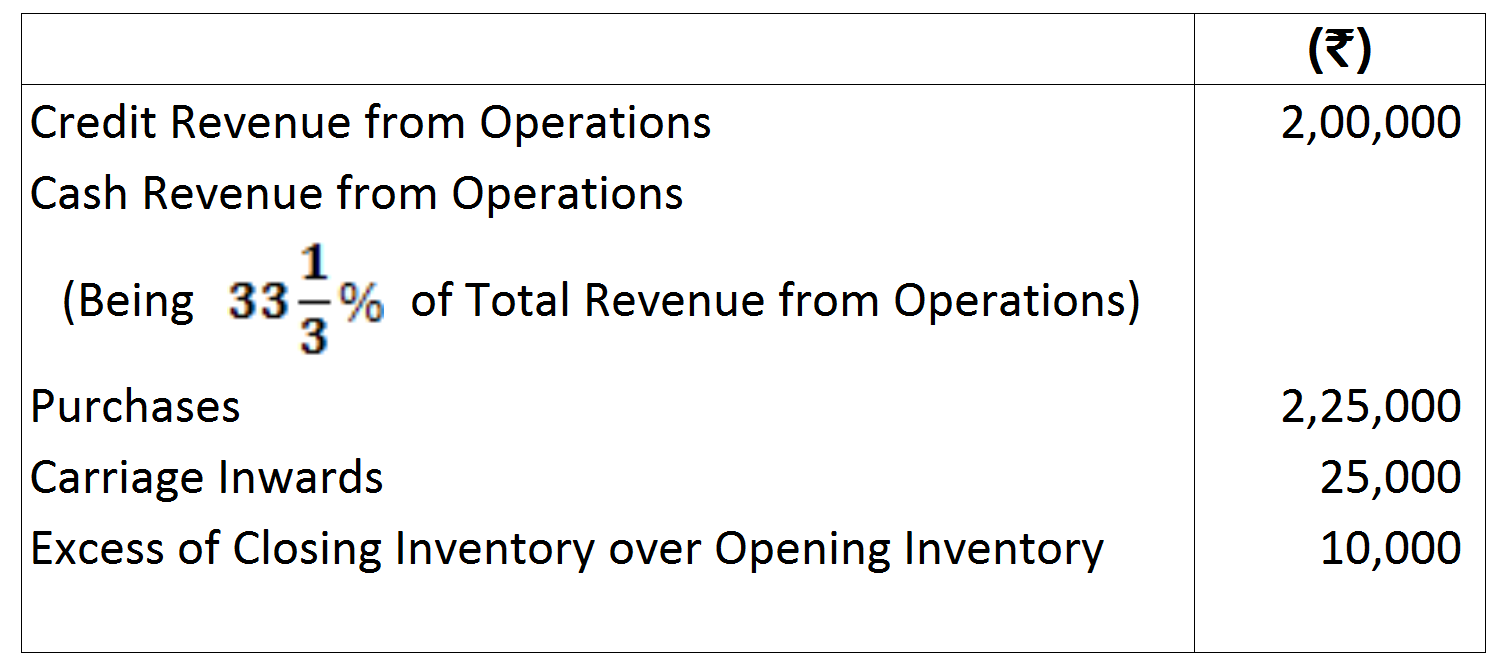

Calculate Gross Profit Ratio from the following data:

Answer

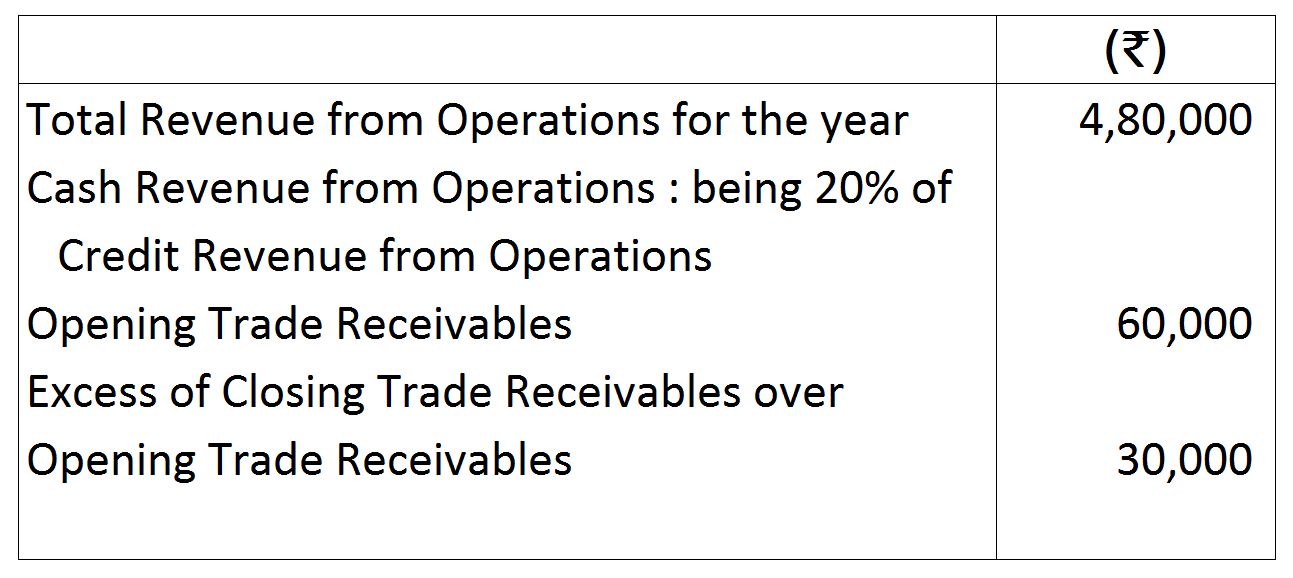

View full question & answer→If Total Revenue from Operations is ₹ 100, Cash Revenue from Operations will be $₹\ 33 \frac{1}{3}$ and Credit Revenue from Operations $₹\ 66 \frac{2}{3}$

Hence,

If Credit Revenue from Operations is $₹\ 66 \frac{2}{3}$ Total Revenue from Operations will be= ₹ 100

If Credit Revenue from Operations is ₹ 2,00,000

Total Revenue from Operations will be $=\frac{100}{66\frac{2}{3}}\times ₹\ 2,00,000$

$=100\times\frac{2}{200}\times ₹\ 2,00,000$

$=₹\ 3,00,000$

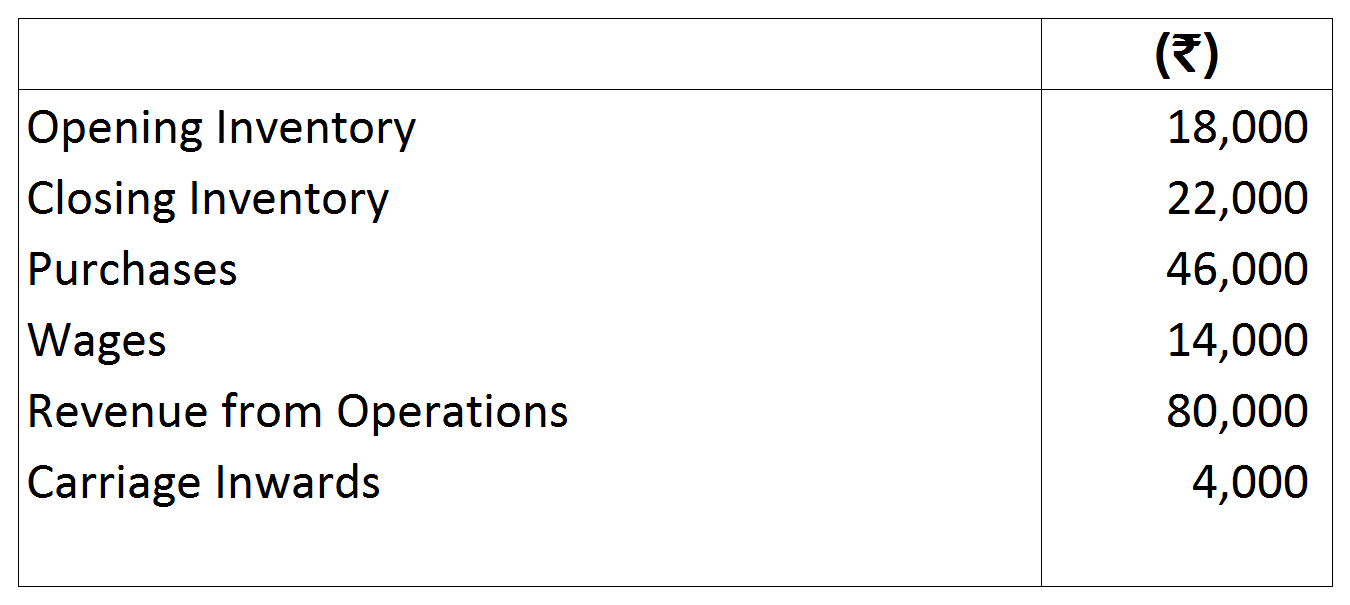

Cost of Revenue from Operations = Purchases + Carriage Inwards - Excess of Closing Inventory over Opening Inventory

= ₹ 2,25,000 + ₹ 25,000 - ₹ 10,000

= ₹ 2,40,000

Gross Profit = Total Revenue from Operations - Cost of Revenue from Operations

= ₹ 3,00,000 - ₹ 2,40,000 = ₹ 60,000

Gross Profit Ratio $=\frac{\text{Gross Profit}}{\text{Net Revenue from Operations x}}\times100$

$=\frac{₹\ 60,000}{₹\ 3,00,000}\times100= 20 \%$

Hence,

If Credit Revenue from Operations is $₹\ 66 \frac{2}{3}$ Total Revenue from Operations will be= ₹ 100

If Credit Revenue from Operations is ₹ 2,00,000

Total Revenue from Operations will be $=\frac{100}{66\frac{2}{3}}\times ₹\ 2,00,000$

$=100\times\frac{2}{200}\times ₹\ 2,00,000$

$=₹\ 3,00,000$

Cost of Revenue from Operations = Purchases + Carriage Inwards - Excess of Closing Inventory over Opening Inventory

= ₹ 2,25,000 + ₹ 25,000 - ₹ 10,000

= ₹ 2,40,000

Gross Profit = Total Revenue from Operations - Cost of Revenue from Operations

= ₹ 3,00,000 - ₹ 2,40,000 = ₹ 60,000

Gross Profit Ratio $=\frac{\text{Gross Profit}}{\text{Net Revenue from Operations x}}\times100$

$=\frac{₹\ 60,000}{₹\ 3,00,000}\times100= 20 \%$

Note:

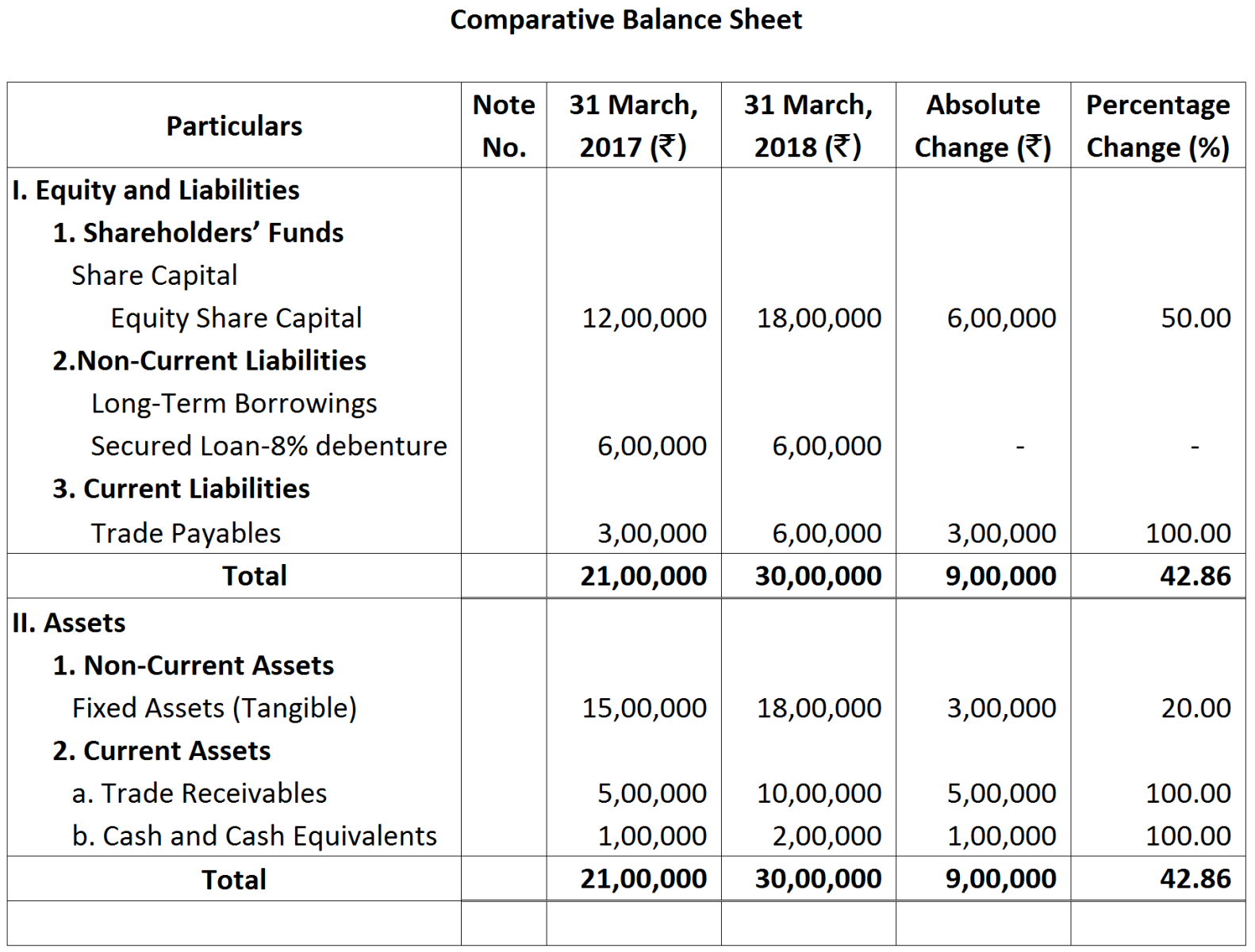

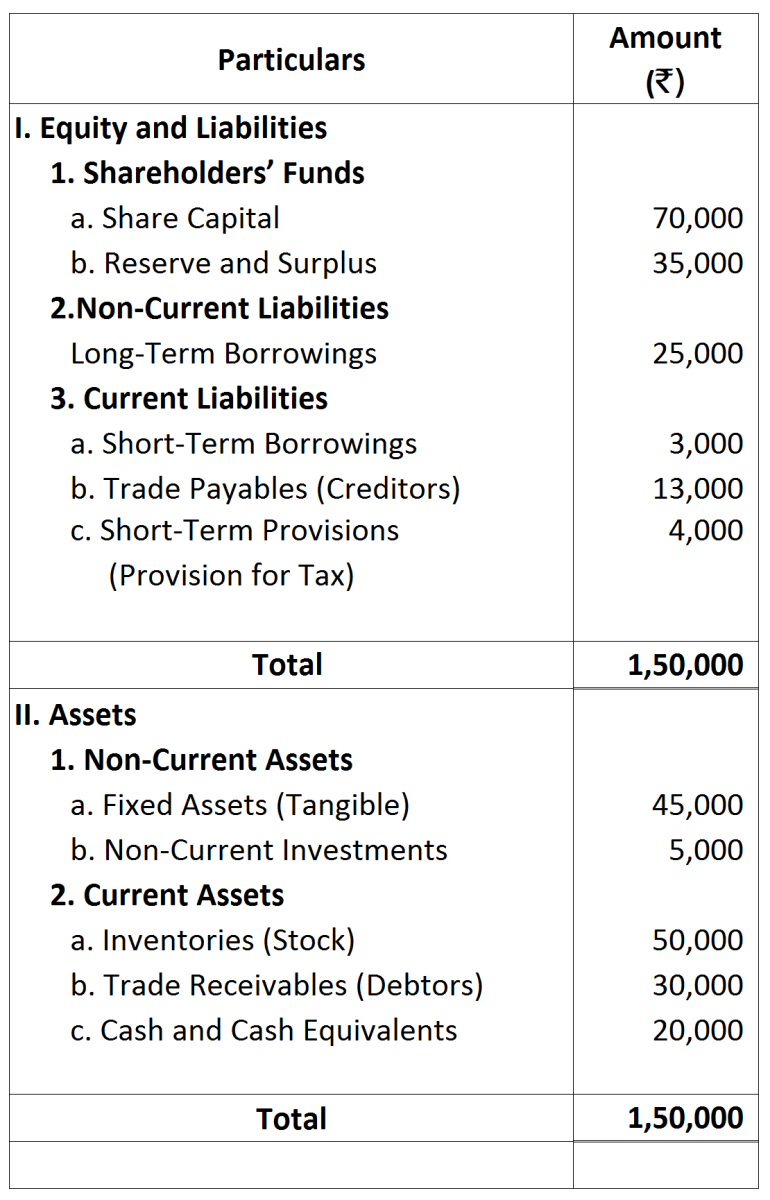

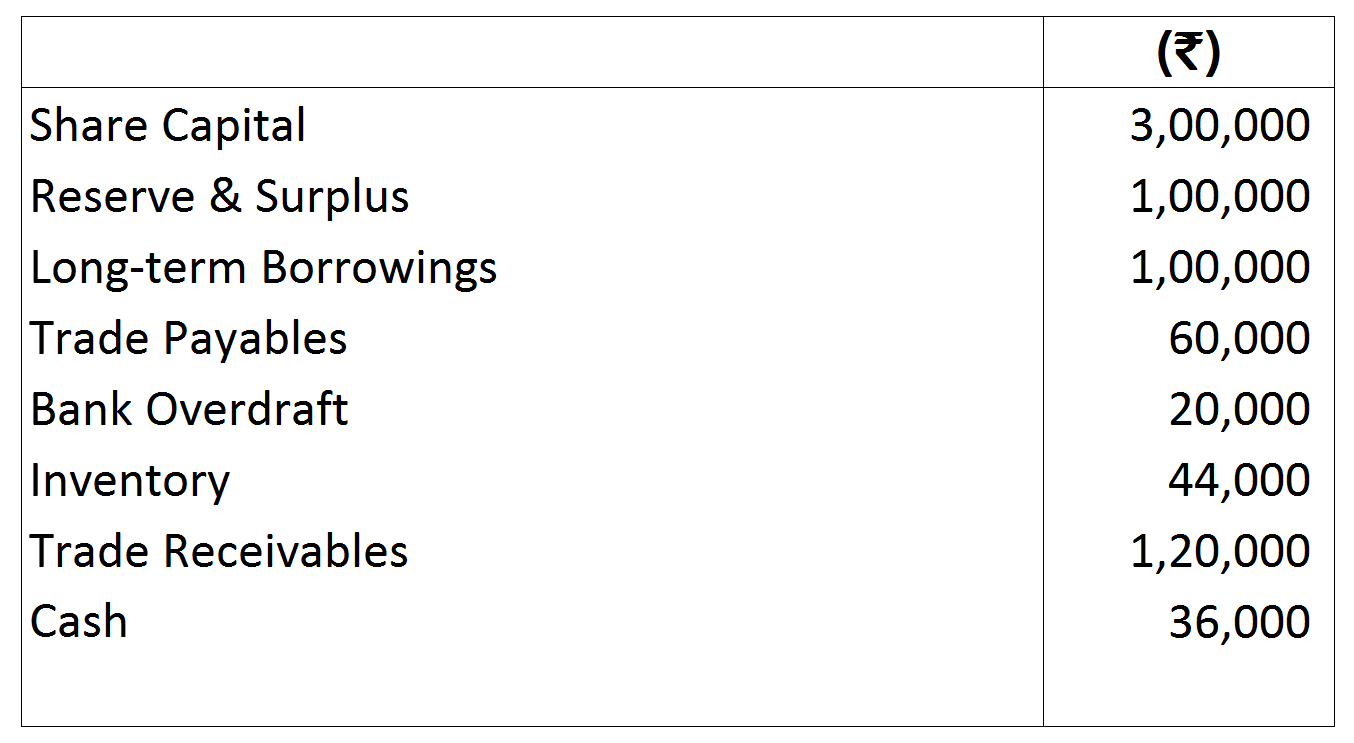

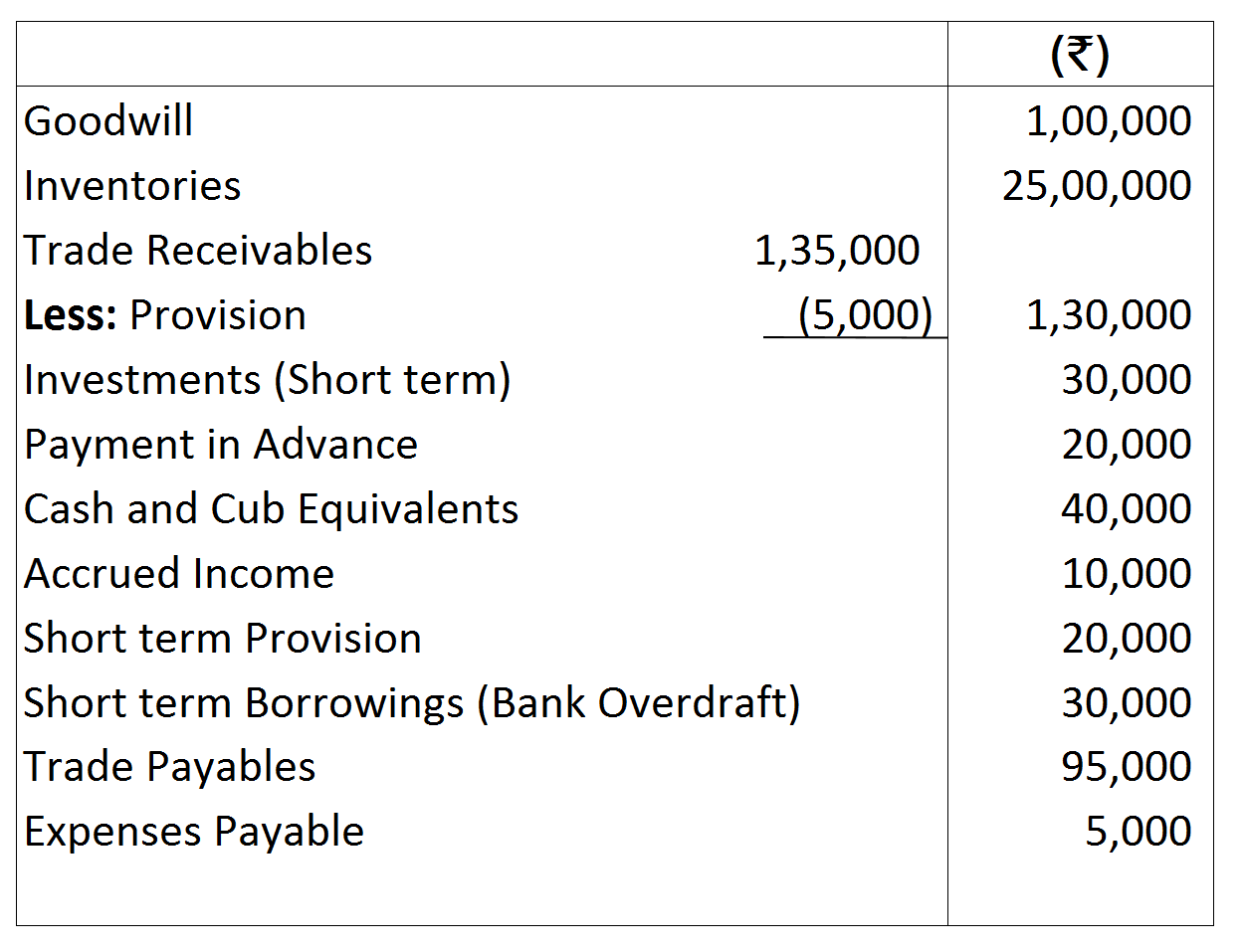

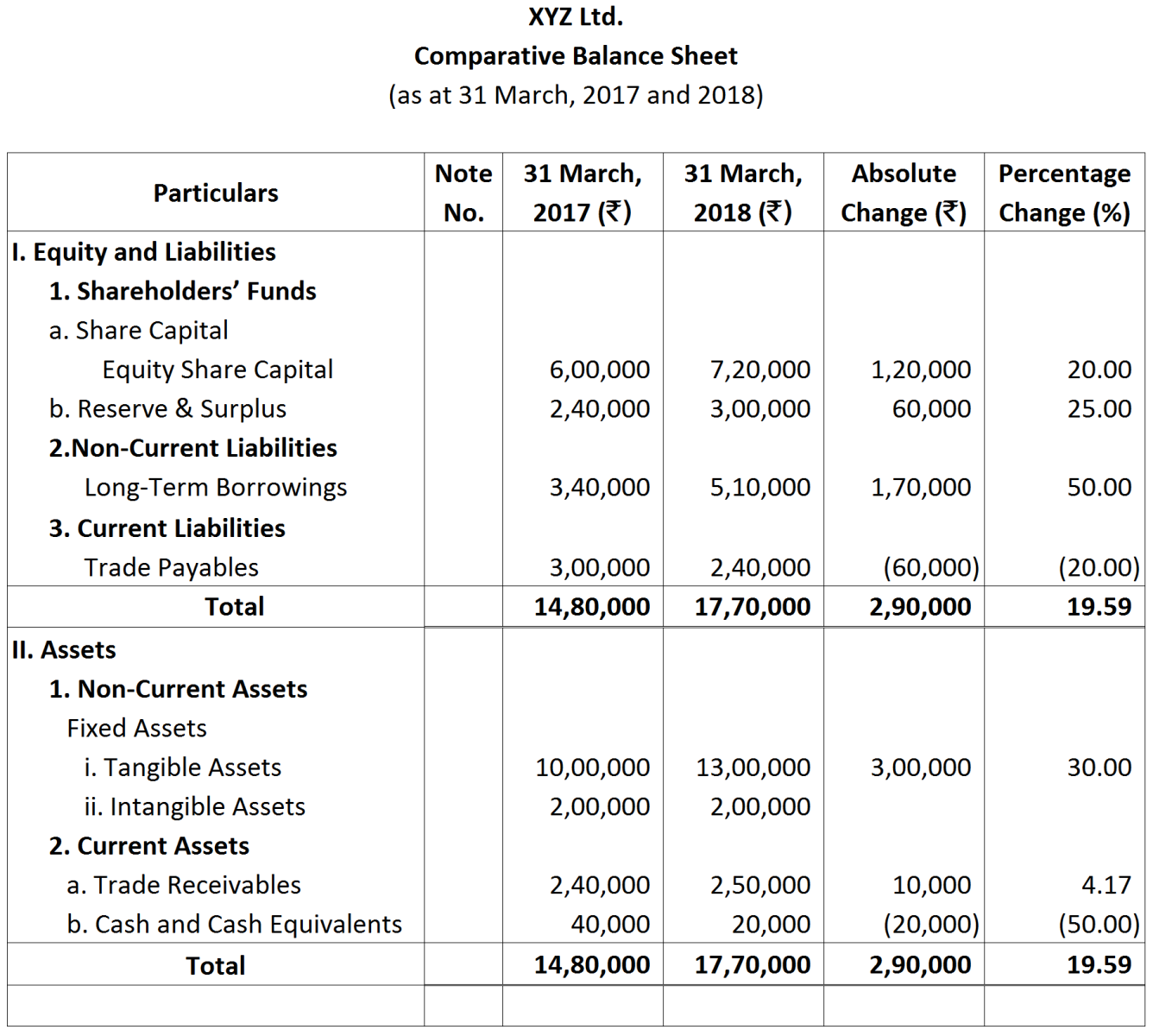

Note: Throw light on the short-term financial position of the Company with the help of suitable ratios.

Throw light on the short-term financial position of the Company with the help of suitable ratios.

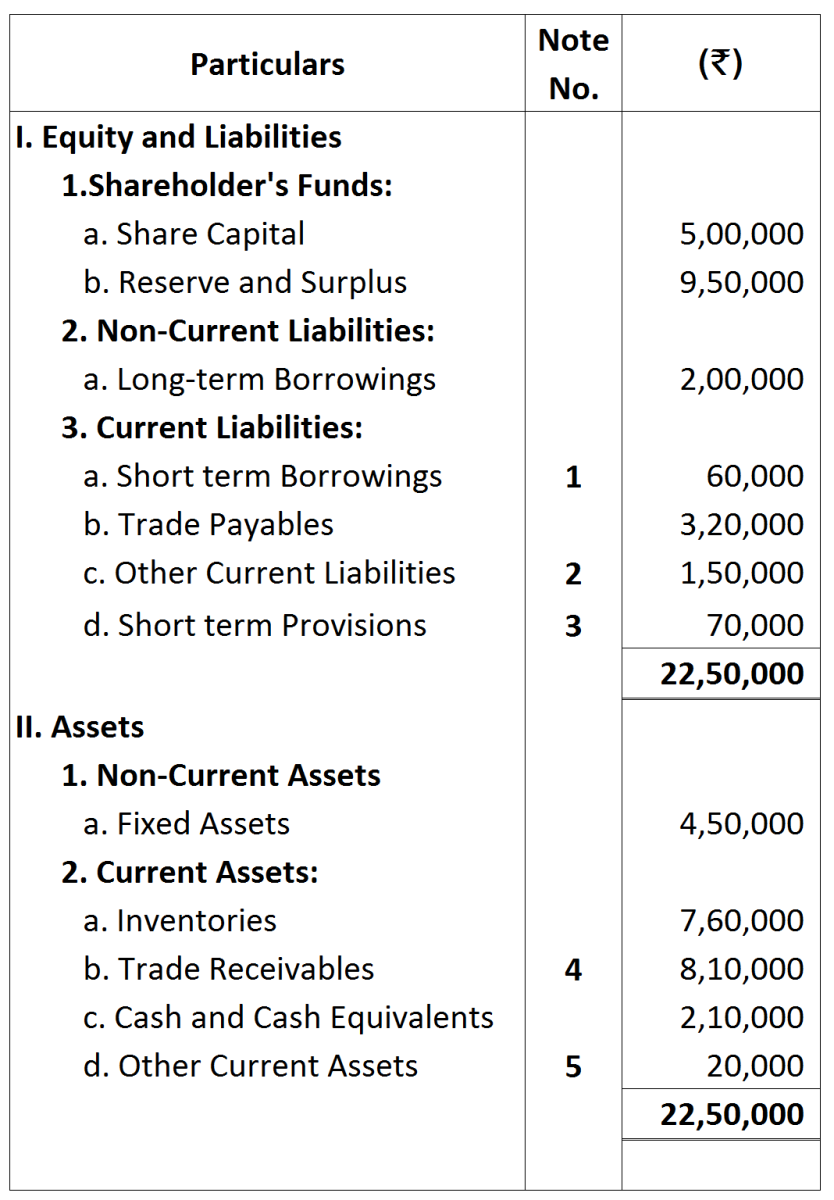

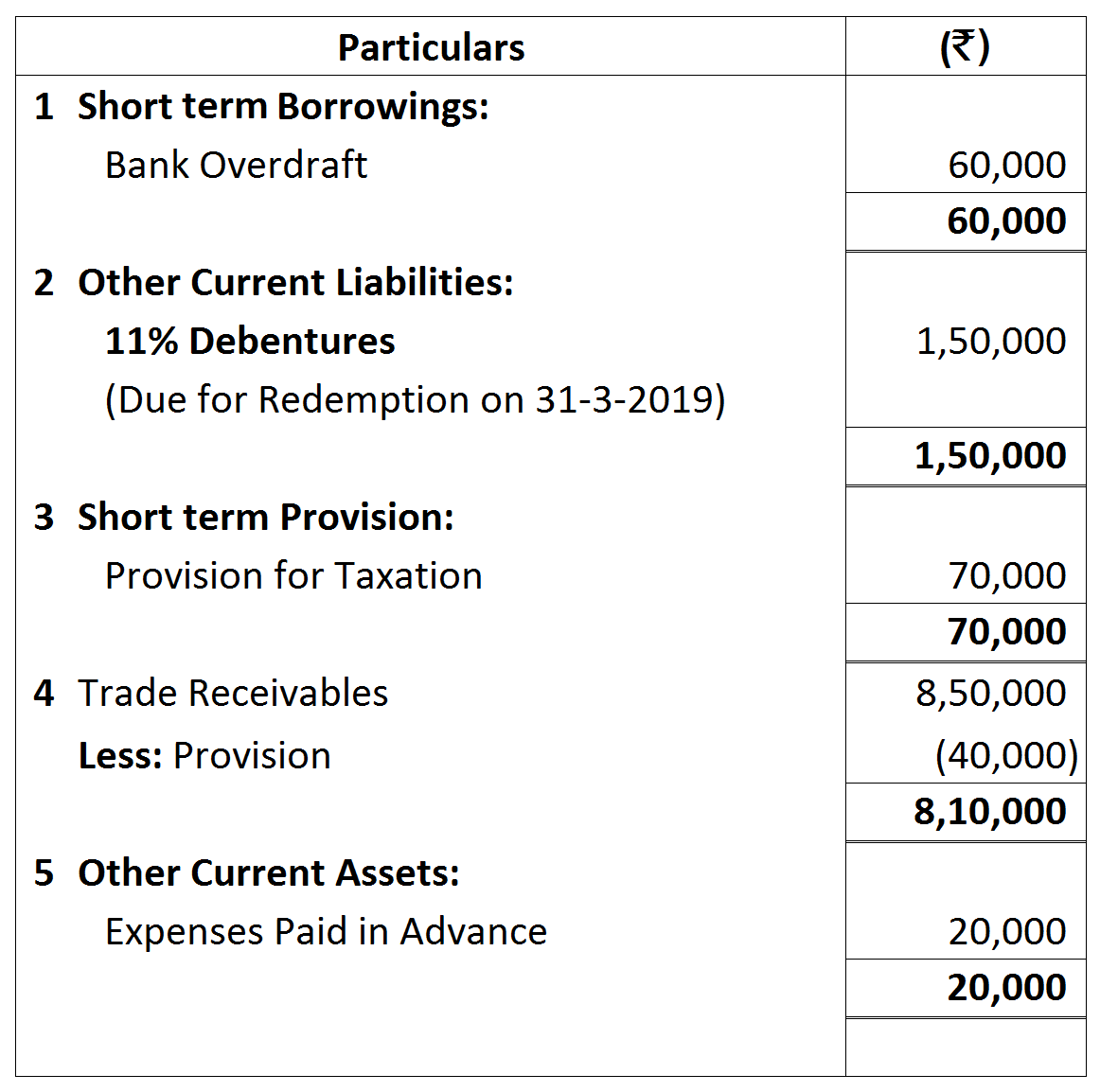

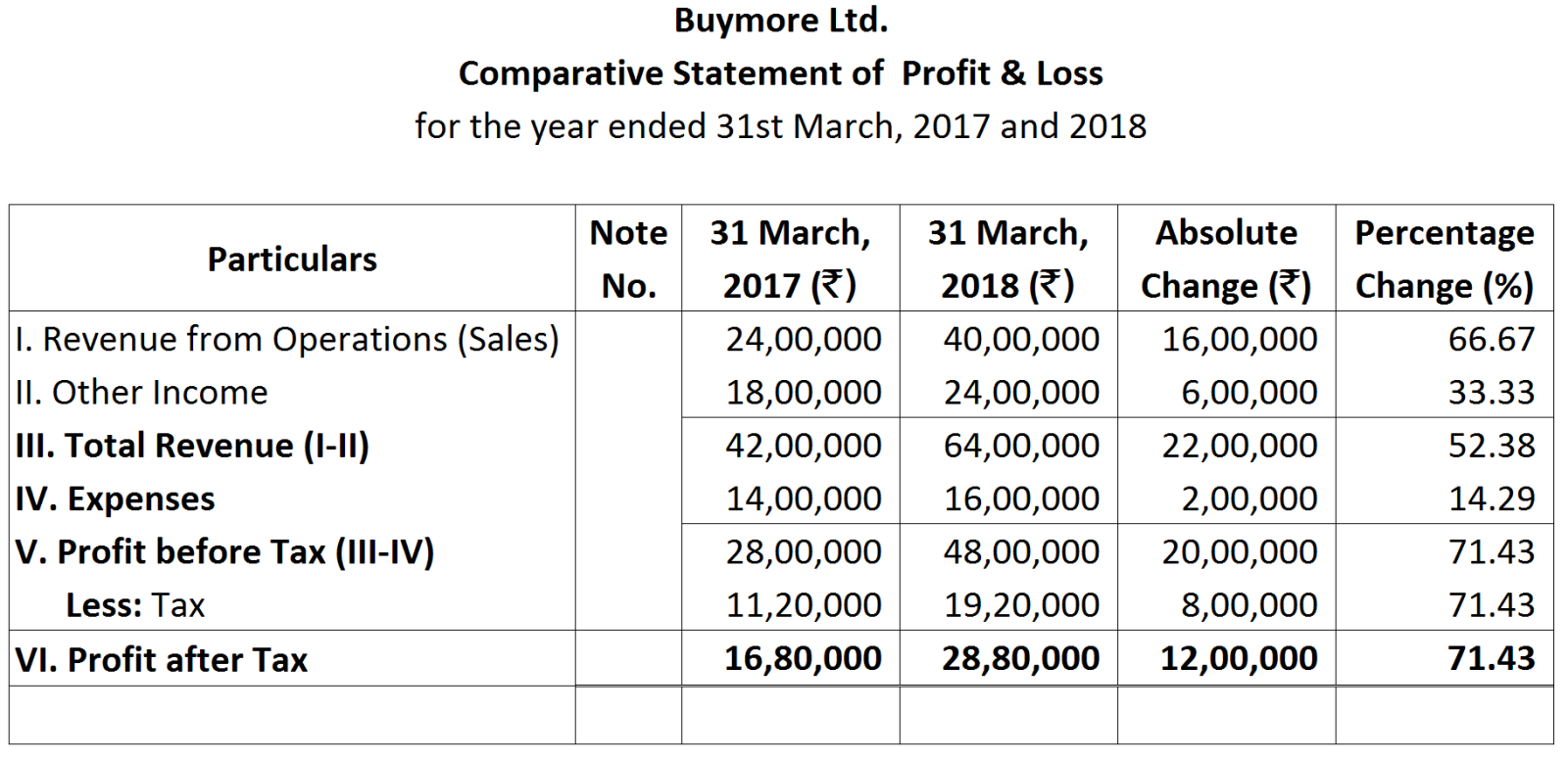

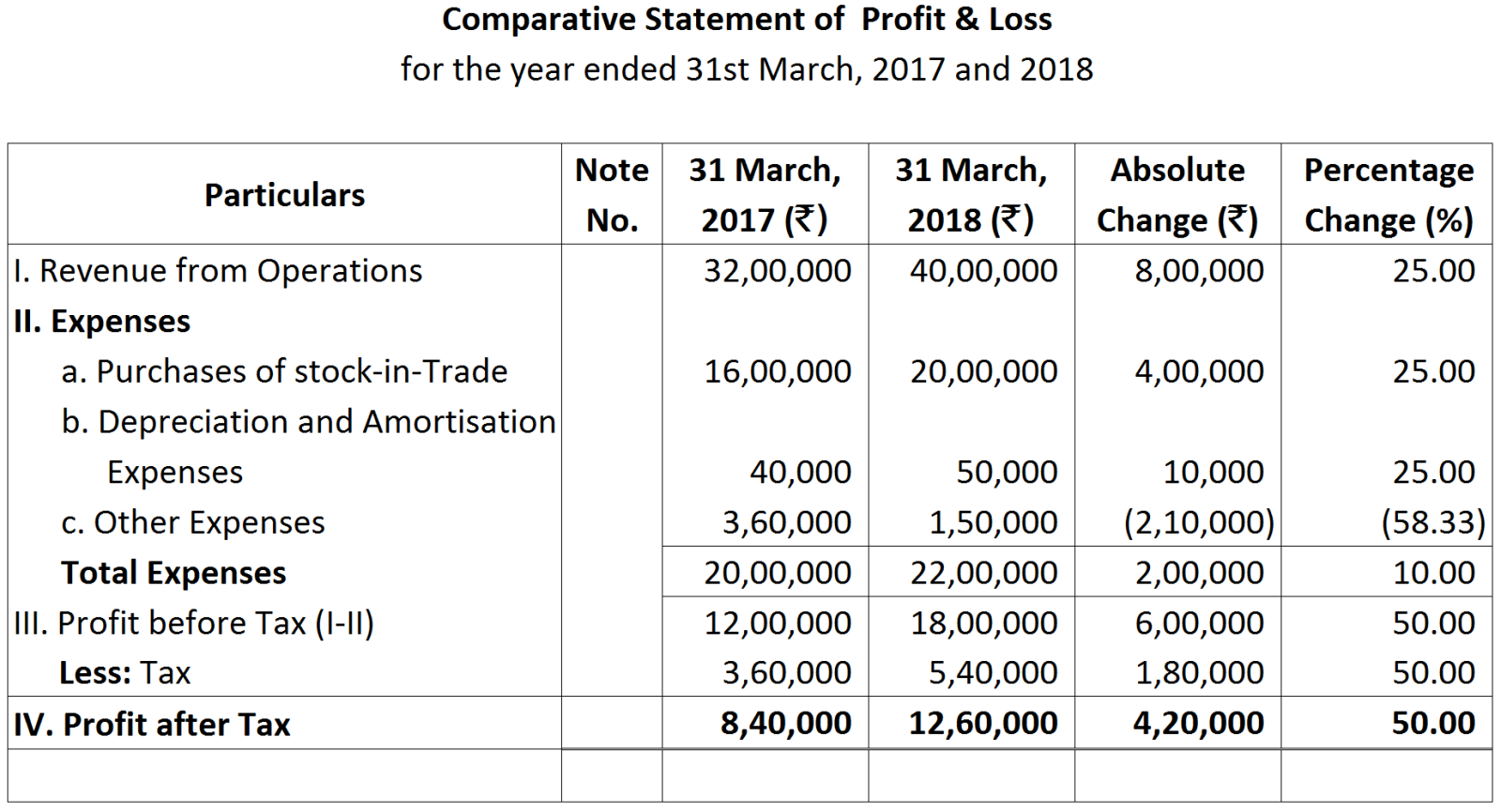

From the above Comparative Statement of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Net Profit ratio.

From the above Comparative Statement of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Net Profit ratio. From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Operating ratio.

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Operating ratio. From the above Common-size Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.

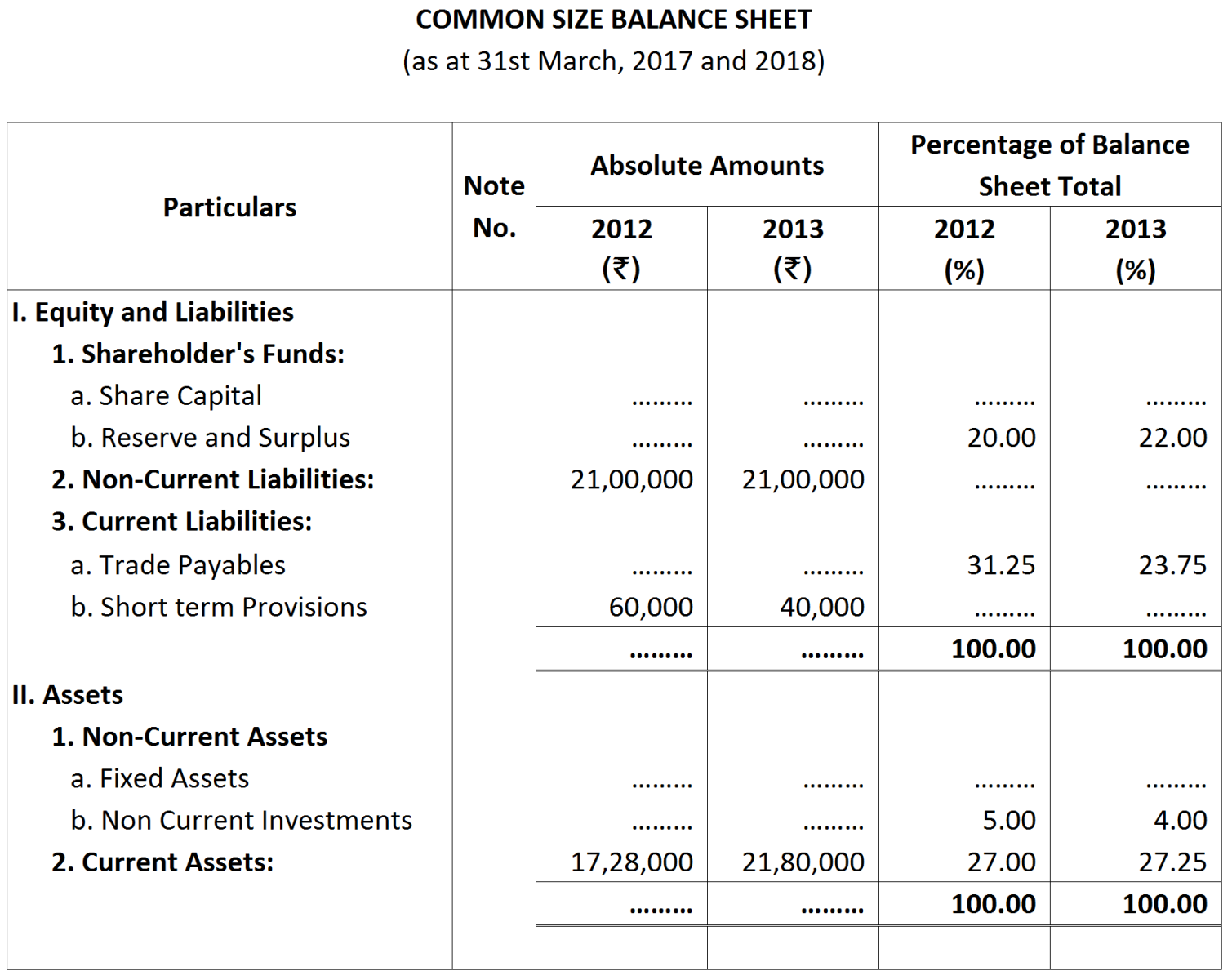

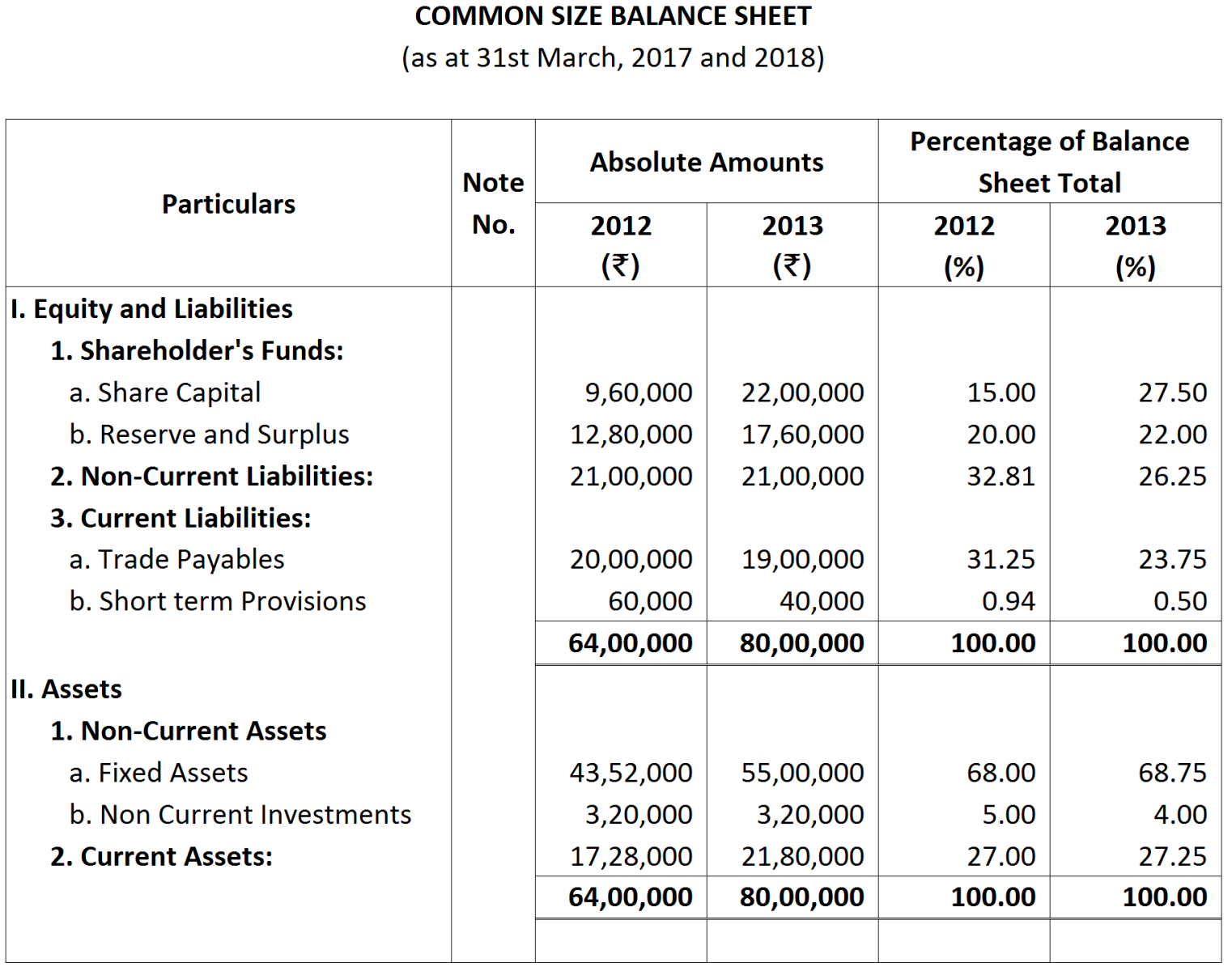

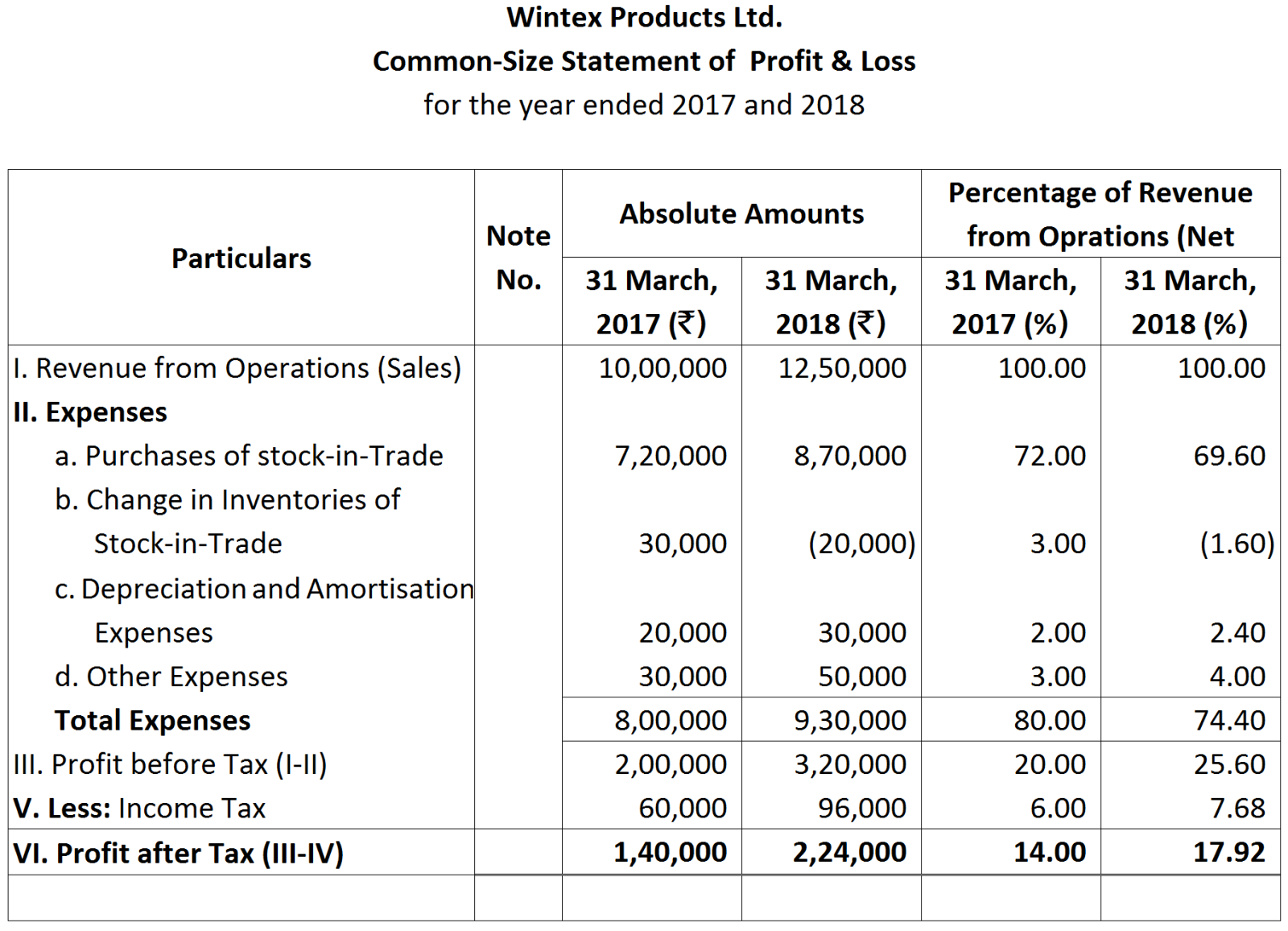

From the above Common-size Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.

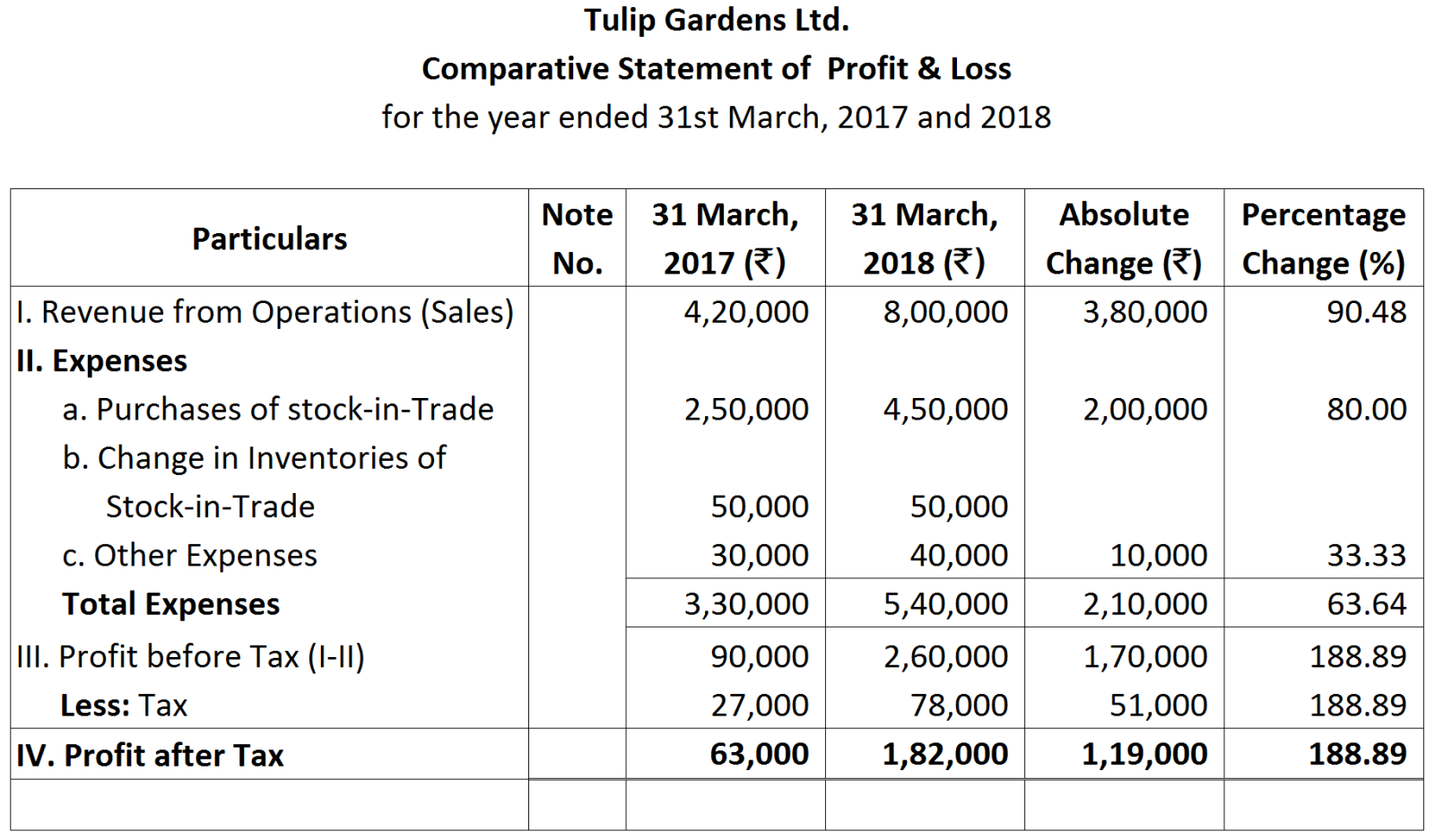

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.

From the above Comparative Statment of Profit and loss for the year ended 31st March, 2017 and 31st March, 2018, compute Gross Profit ratio.