Question

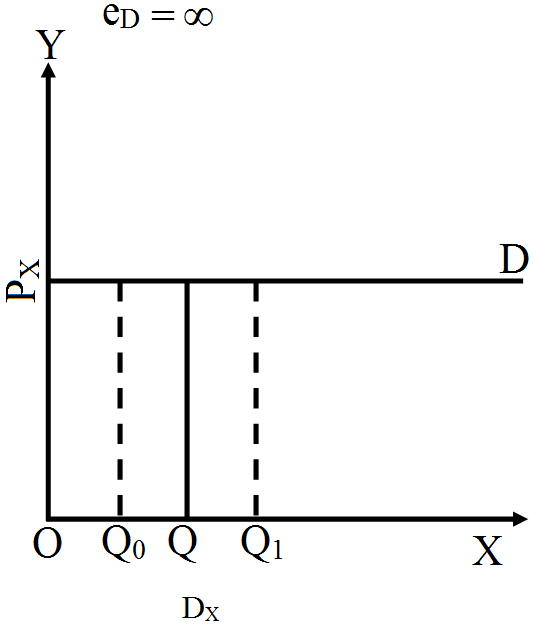

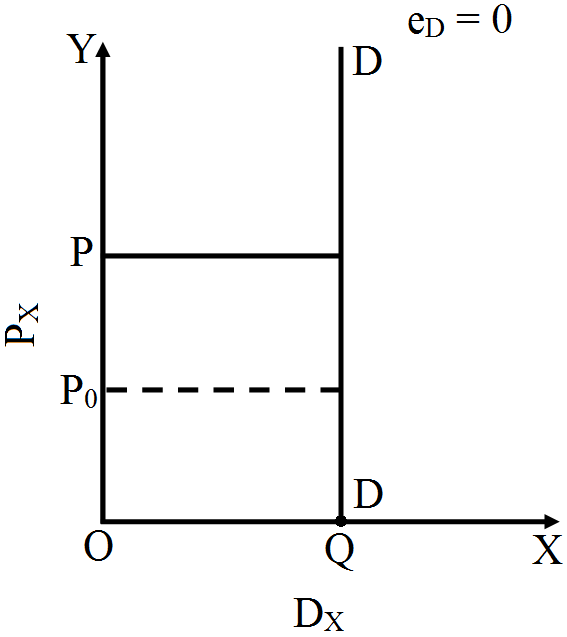

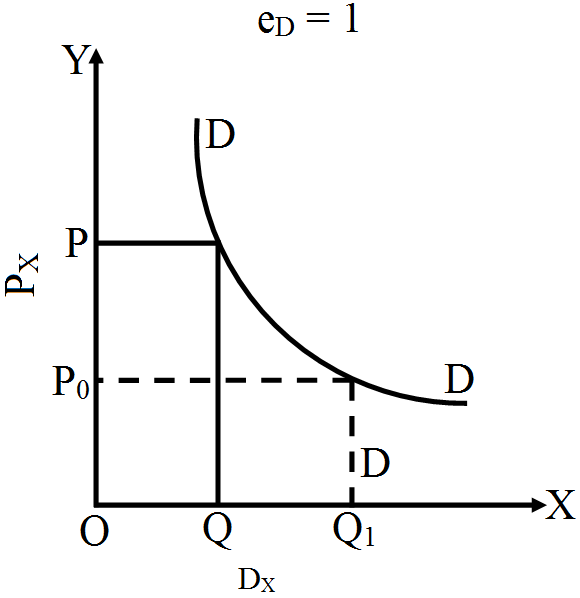

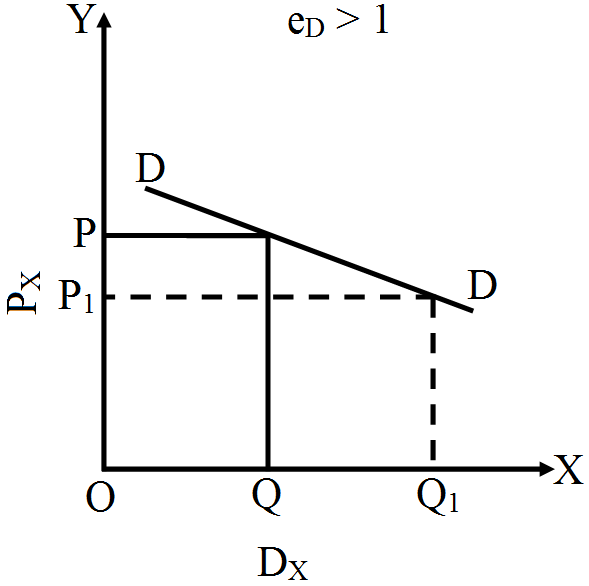

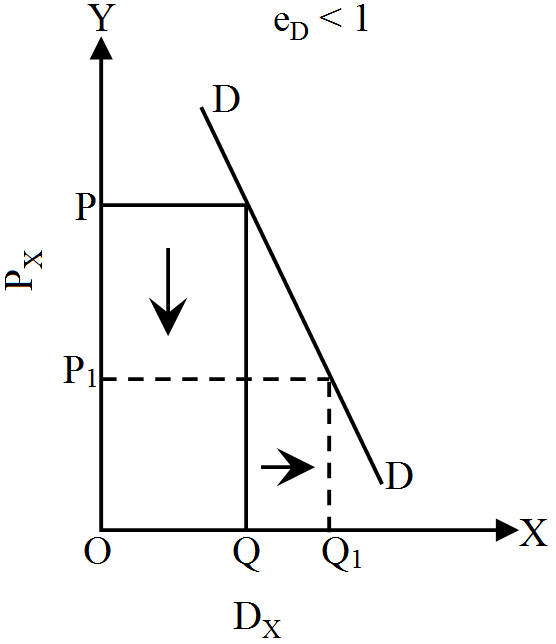

Define price elasticity of demand. Explain its various degrees. Use diagrams.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| Output (Units) | Average Revenue(₹) | Total Cost(₹) |

| 1 | 7 | 7 |

| 2 | 7 | 15 |

| 3 | 7 | 22 |

| 4 | 7 | 28 |

| 5 | 7 | 33 |

| 6 | 7 | 40 |

| 7 | 7 | 48 |

| Price per unit(Rs.) | Output(units) | Total cost(Rs.) |

| 8 | 1 | 6 |

| 7 | 2 | 11 |

| 6 | 3 | 15 |

| 5 | 4 | 18 |

| 4 | 5 | 23 |

| Output (units) ₹ | 1 | 2 | 3 | 4 | 5 |

| Total Cost ₹ | 9 | 17 | 24 | 29 | 36 |

| Total Revenue | 11 | 20 | 27 | 32 | 35 |