Question

Discuss the advantages of computerised accounting system over the manual accounting system.

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

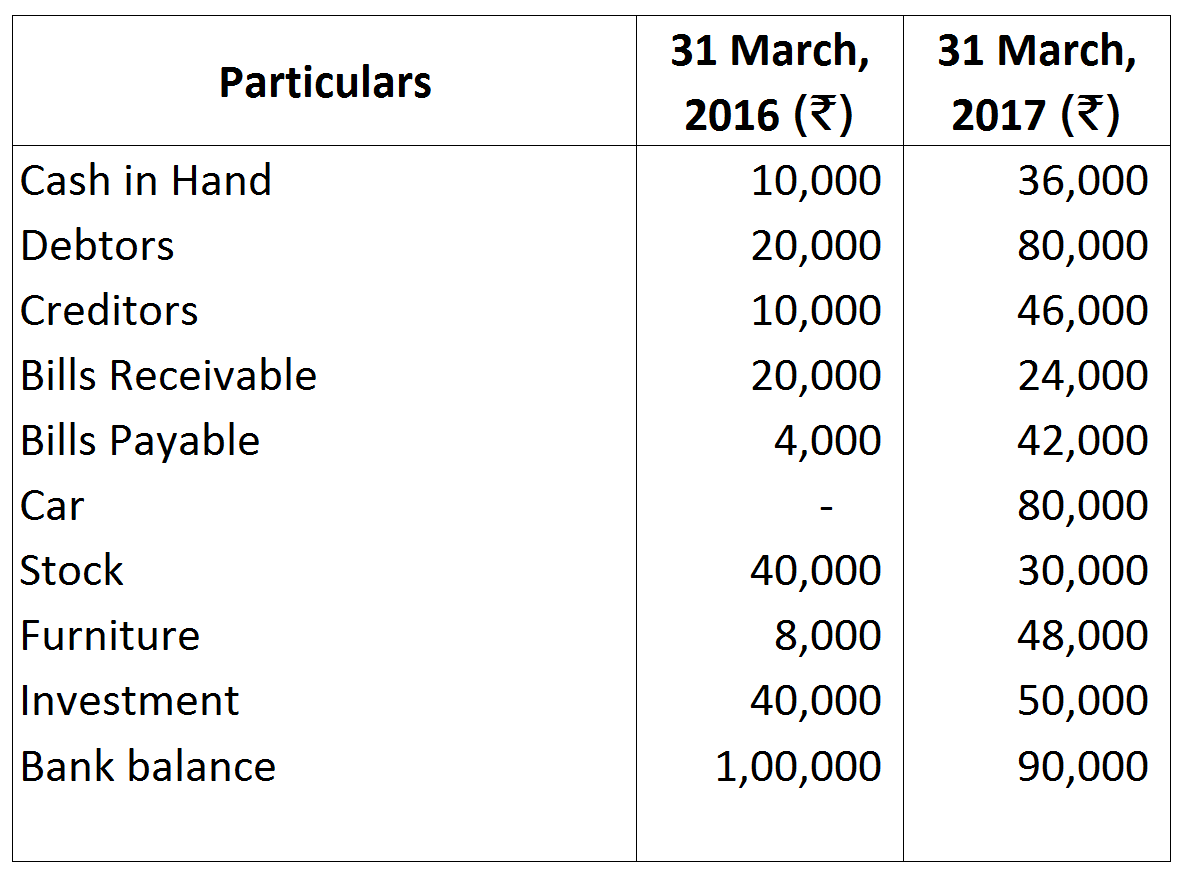

Closing Stock was valued at ₹ 35,000. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2017 and Balance Sheet as at that date.

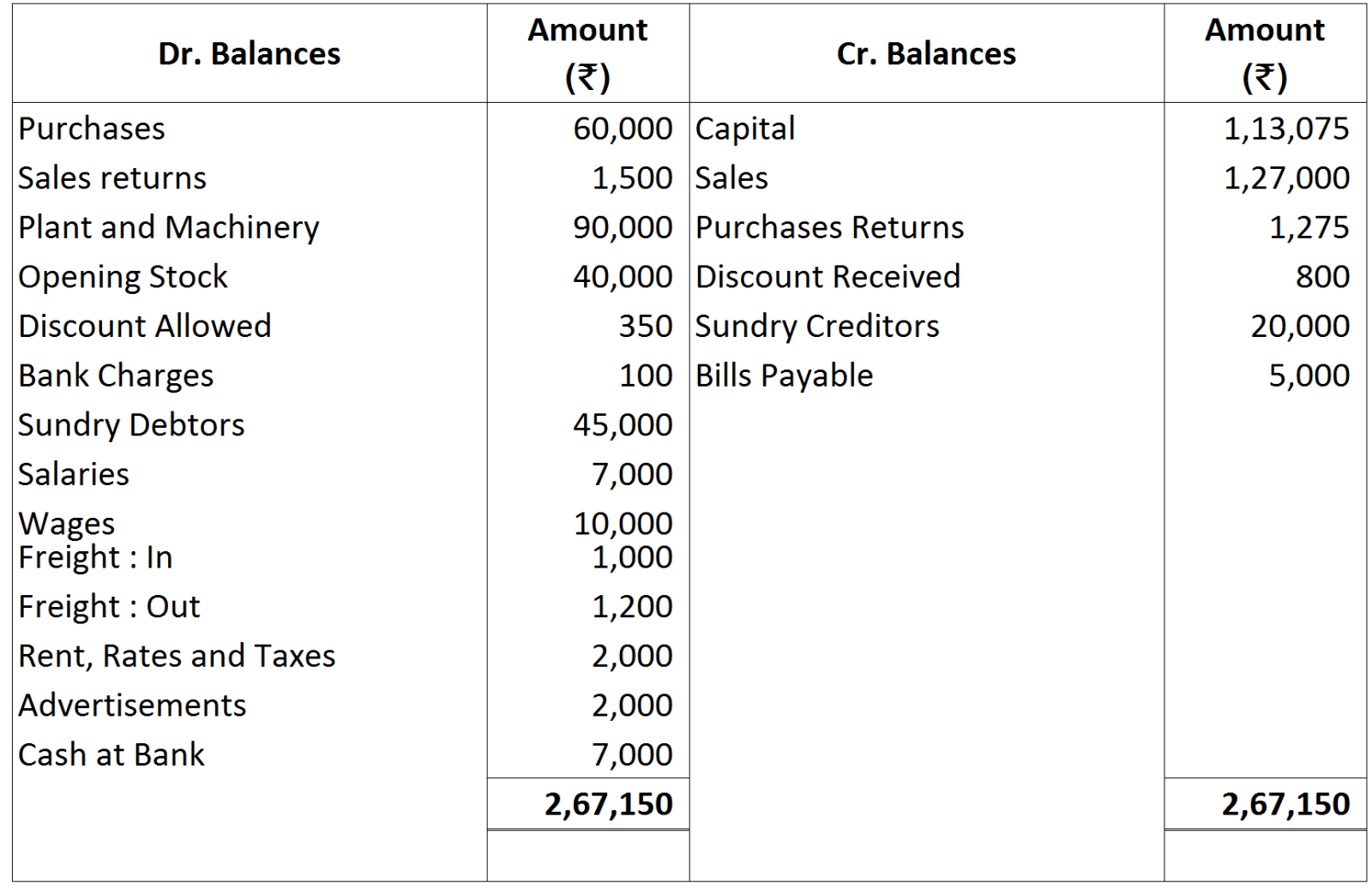

Closing Stock was valued at ₹ 35,000. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2017 and Balance Sheet as at that date.

|

|

|

₹

|

|

(i)

|

Bank overdraft as per the Cash Book.

|

80,000

|

|

(ii)

|

Cheques deposited as per the bank statement but not entered in the Cash Book.

|

3,000

|

|

(iii)

|

Cheques recorded for collection but not sent to the bank.

|

10,000

|

|

(iv)

|

Credit side of bank column casted short.

|

1,000

|

|

(v)

|

Bank charges recorded twice in the Cash Book.

|

100

|

|

(vi)

|

Customer's cheque returned as per the Bank Statement.

|

4,000

|

|

(vii)

|

Cheques issued but dishonoured on technical grounds.

|

3,000

|

|

(viii)

|

Bills collected by bank directly.

|

20,000

|

|

(ix)

|

Cheque received entered twice in the Cash Book.

|

5,000

|