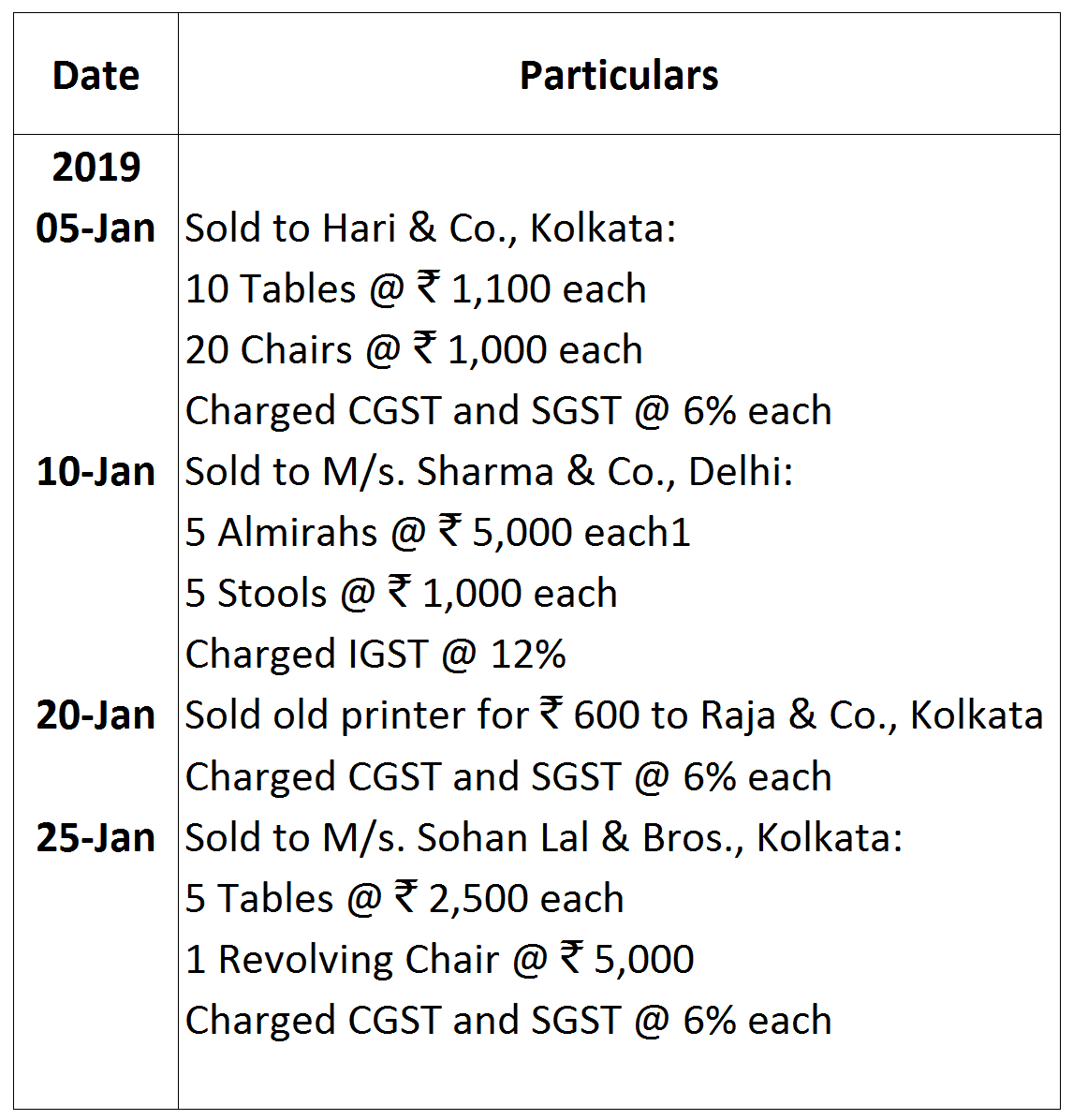

Question

Distinguish between a Balance Sheet and Trial Balance. (Any five points)

|

|

Basis

|

Balance Sheet

|

Trial Balance

|

|

1.

|

Purpose

|

The purpose is protray finacial position.

|

The purpose is to establish arithmetical accuracy of the books of account.

|

|

2.

|

Information about Profit

|

It provides information as to prolitablity and finacial position of the firm.

|

No such information is possible from Trial Balance.

|

|

3.

|

Necessity

|

It is essential to prepare Balance Sheet to complete the accounting process.

|

Though desirable, it may be possible to dipense with its preparation.

|

|

4.

|

Headlings

|

The two sides are headed as assets and liabilities.

|

The two columns are headed as debit and credit.

|

|

5.

|

Coverage

|

Only personal and real accounts appear in the Balance Sheet.

|

In the Trial Balance all accounts must be written, no account can be left out.

|

|

6.

|

Closing Stock

|

This account appears in the Balance Sheet.

|

Normally, a closing stock does not appear in the Trial Balance.

|

|

7.

|

Period

|

Normally, it is prepared only at the end of the accounting period.

|

A Trial Balance can be prepared at any time, even monthly or whenever required.

|

|

8.

|

Adjustment

|

A Balance Sheet cannot be prepared without making adjustments for outstanding and prepaid items and without taking into account all events and transaction for the year.

|

A Trial Balance can be prepared at any stage, without even making adjustments.

|

|

9.

|

Accounts

|

Only Asset, Liability and Capital Account are shown.

|

All account i.e., Asset, Liability, Capital, Income and Expense Account are shown.

|

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| 2019 | ₹ | |||

| April 1 | Cash balance ₹ 2,000, bank balance ₹ 24,500 | |||

| April 2 | Cash sales ₹ 60,000 plus CGST and SGST @ 6% each | |||

| April 5 | Deposited in Bank | 50,000 | ||

| April 7 | Issued cheque to Sohan | 10,000 | ||

| April 9 | Sold goods for cash ₹ 10,000 plus CGST and SGST @ 6% each | |||

| April 12 | Received a cheque from National Insurance Co. Ltd. against claim lodged last year | 19,800 | ||

| April 14 | Sold goods to Niraj of ₹ 25,000 plus CGST and SGST @ 6% each, received cash ₹ 10,000 and balance by cheque. Allowed him discount ₹ 500 | |||

| April 16 | Purchased furniture for ₹ 10,000 plus CGST and SGST @ 6% each, paid for furniture by cheque | |||

| April 18 | Sold old furniture for ₹ 10,000 plus CGST and SGST @ 6% each and received cash | |||

| April 20 | Paid into bank cheque of Niraj and cash | 2,500 | ||

| April 22 | Paid to Suman by cheque | 2,500 | ||

| April 26 | Suman's cheque returned on technical ground and paid cash for equal amount | |||

| April 28 | Bank charged its commission of ₹ 300 plus CGST and SGST @ 6% each | |||

| April 29 | Bank paid insurance premium as per standing instructions | 2,500 | ||

| April 30 | Nigam paid into bank directly, intimation received on the same day | 5,000 | ||

Debit Balances | ₹ | Credit Balances | ₹ |

Stock on $1^{s t}$ April, 2022 | 50,000 | Capital | 3,20,000 |

Furniture | 16,000 | Creditors | 80,000 |

Building | 1,60,000 | Purchases Return | 2,000 |

Debtors | 60,000 | Commission | 6,000 |

Drawings | 20,000 | Sales | 4,65,600 |

Plant and Machinery | 1,40,000 | Bad Debts Recovered | 1,400 |

Wages | 24,000 |

|

|

Salaries | 40,000 |

|

|

Bad Debts | 2,000 |

|

|

Purchases | 2,40,000 |

|

|

Electricity Charges | 12,000 |

|

|

Telephone Charges | 4,800 |

|

|

Sales Return | 1,800 |

|

|

Insurance Premium | 3,000 |

|

|

Cash in Hand | 6,400 |

|

|

Cash at Bank | 95,000 |

|

|

| 8,75,000 |

| 8,75,000 |