The rationale behind preparing financial statements is to present a summarised version of all financial activities in such a manner that all users can interpret and understand the information easily, appropriately and also take decisions accordingly.

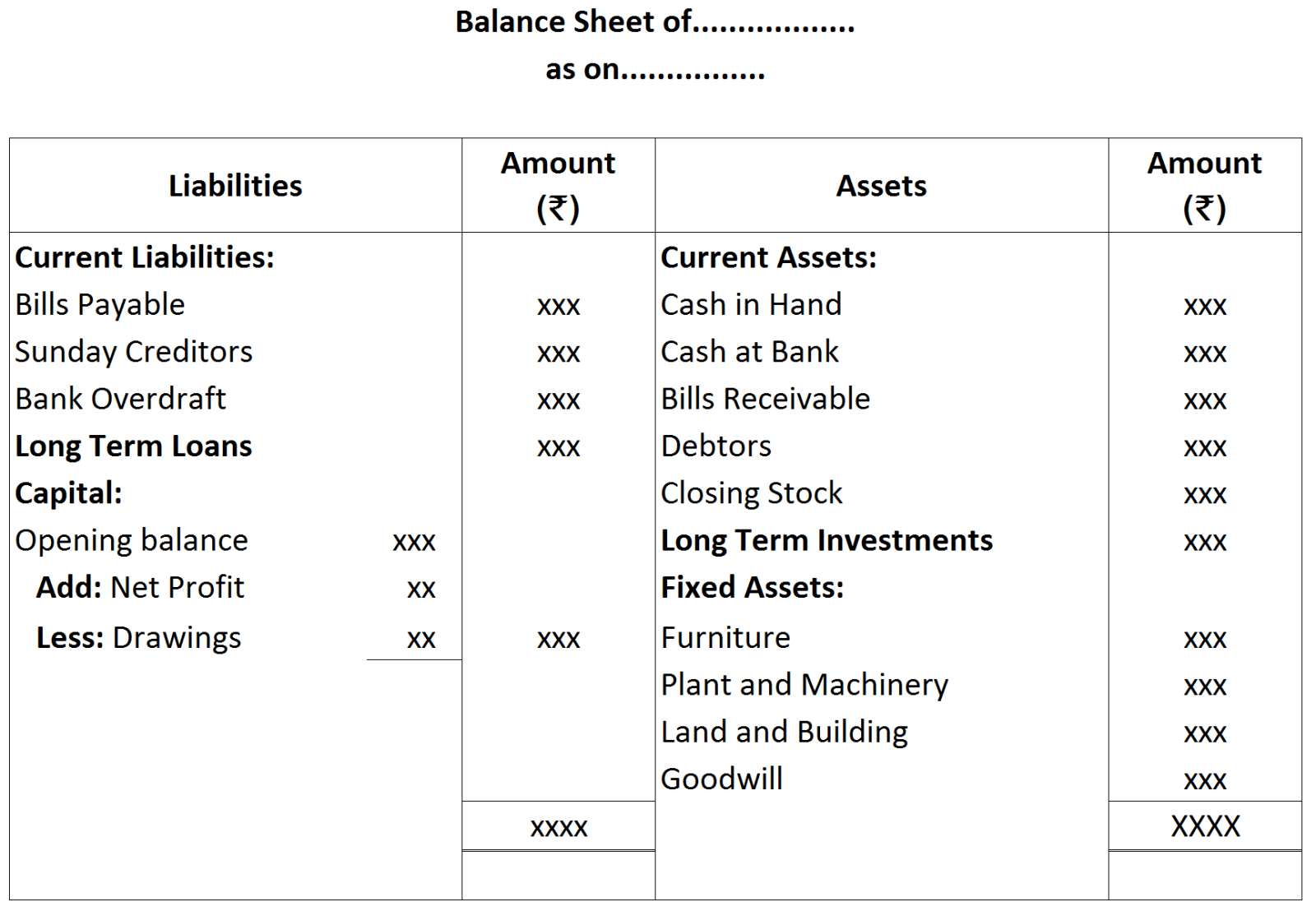

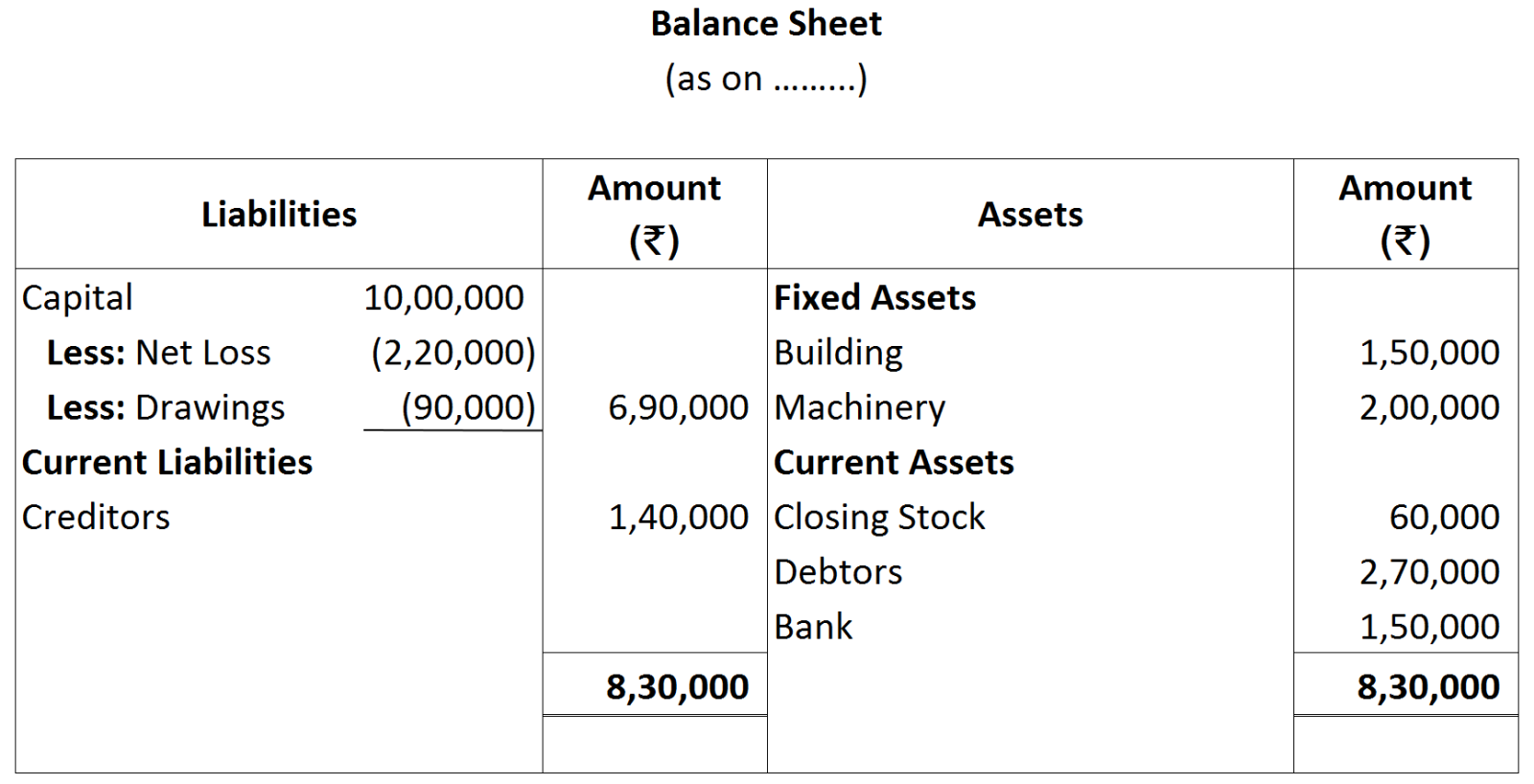

Grouping of assets and liabilities: Grouping means showing similar assets and liabilities under a single head. For example, all assets that can be used for more than a year are clubbed together under the heading ‘fixed assets’, for example, building, furniture, machinery, etc.

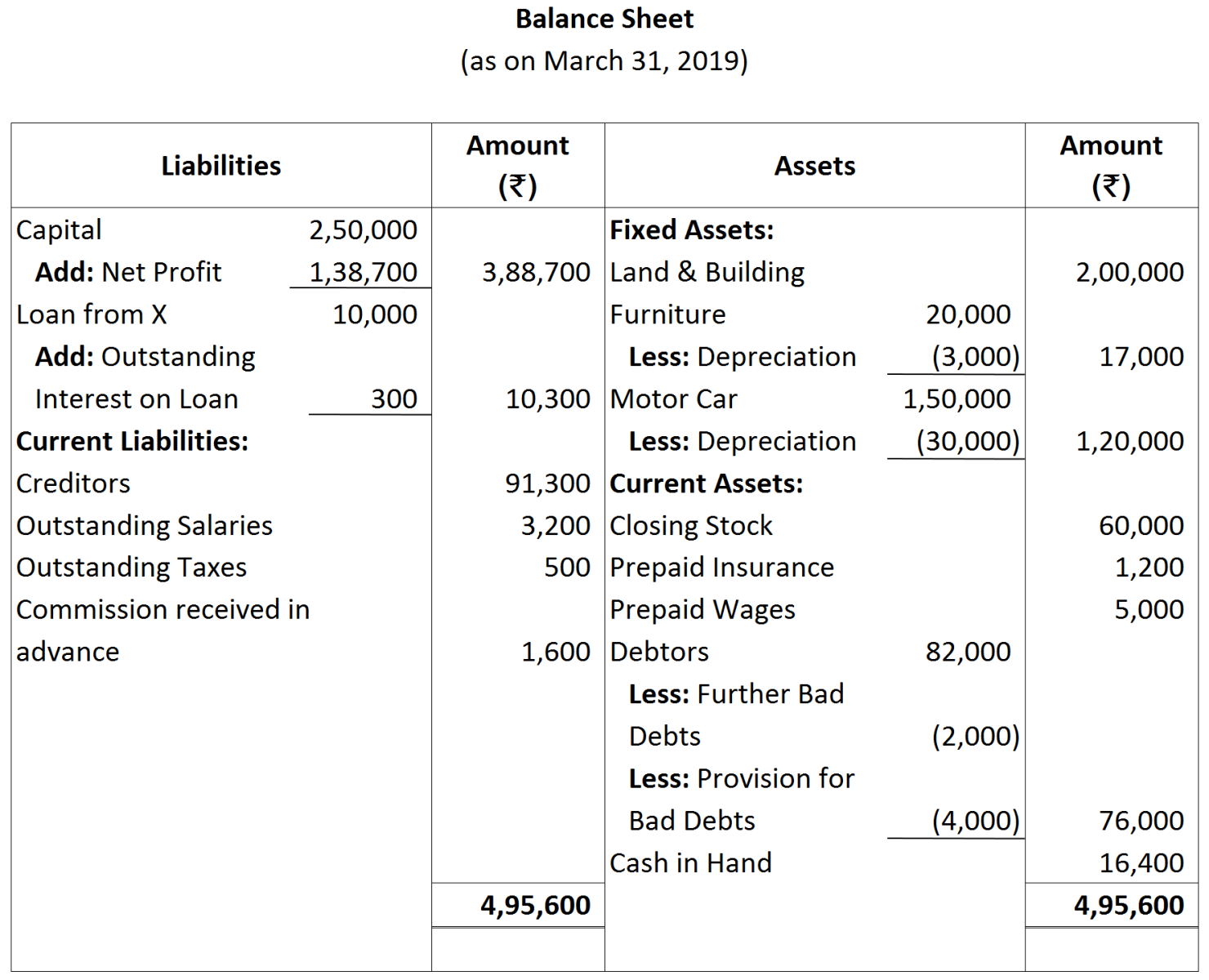

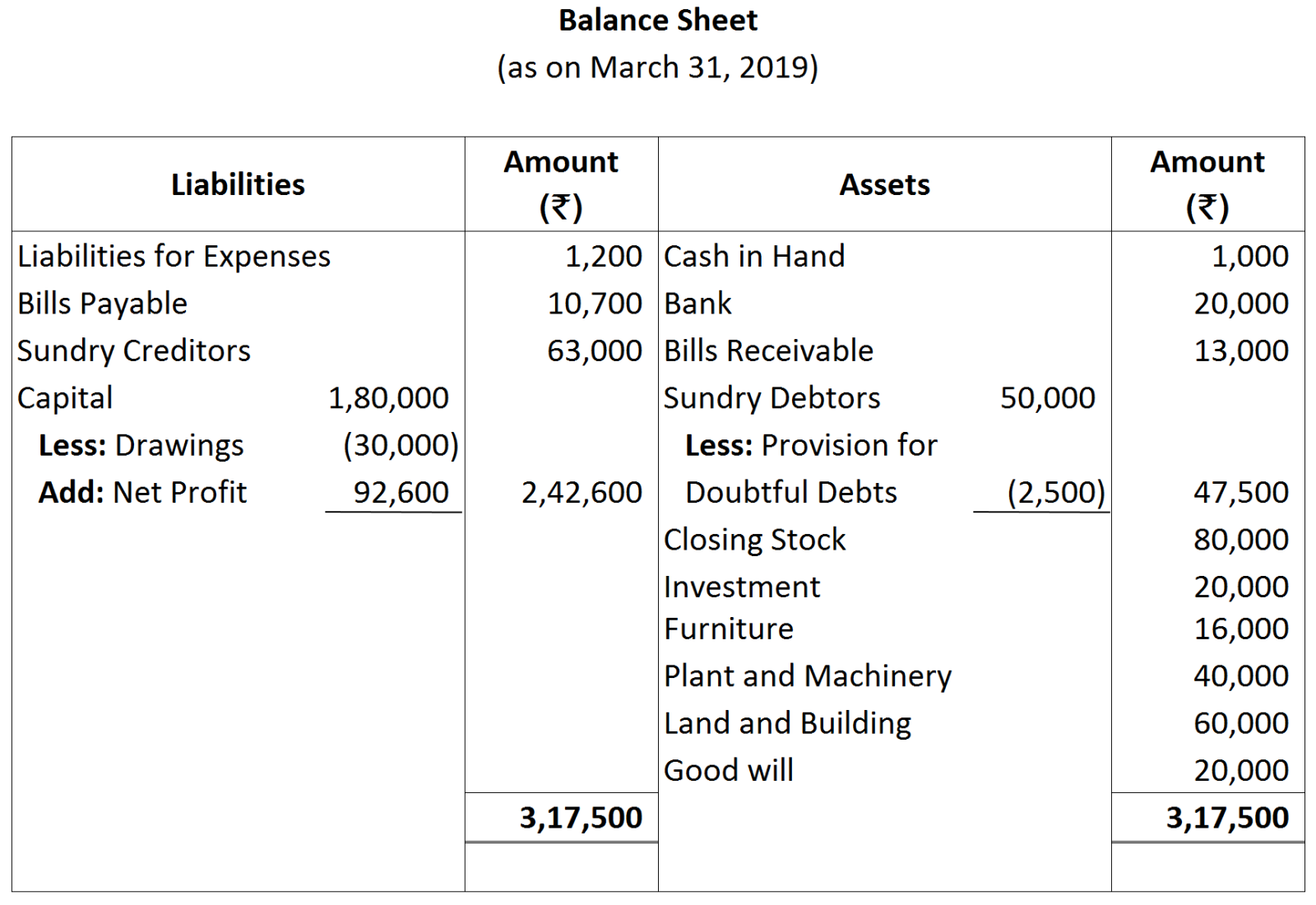

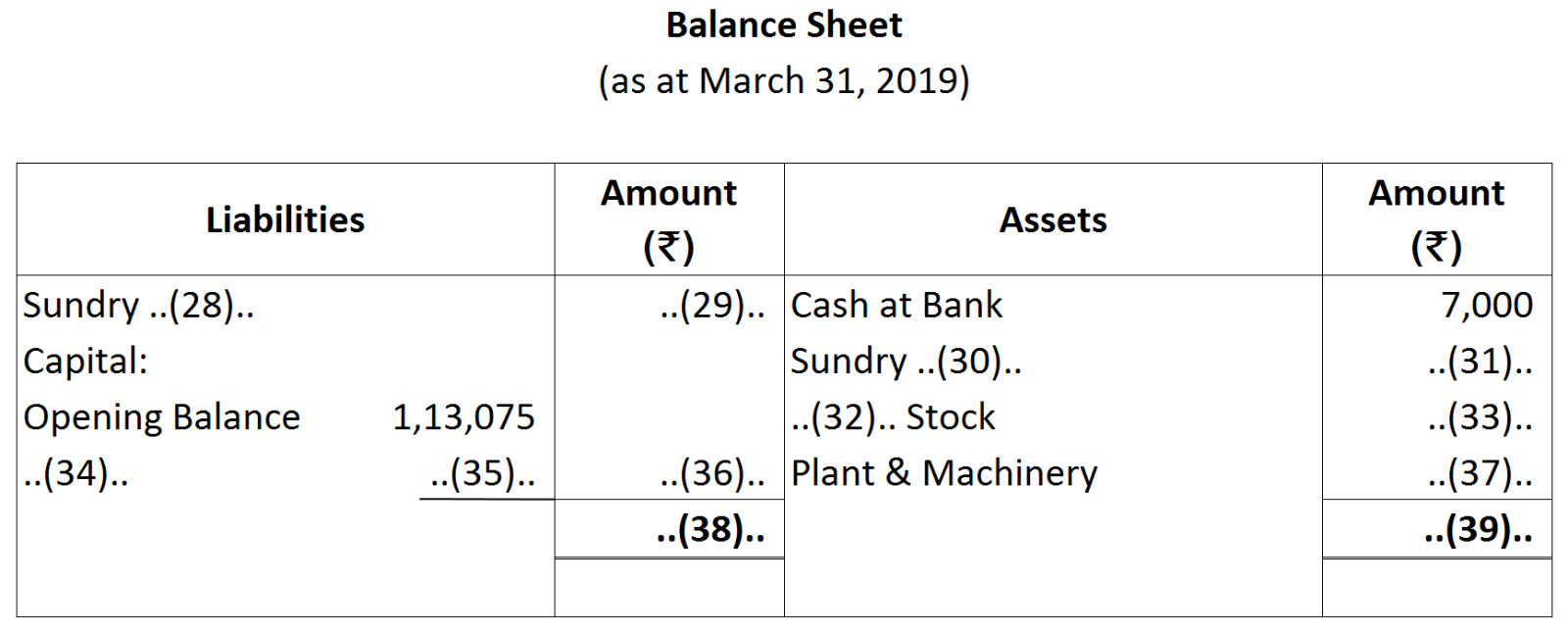

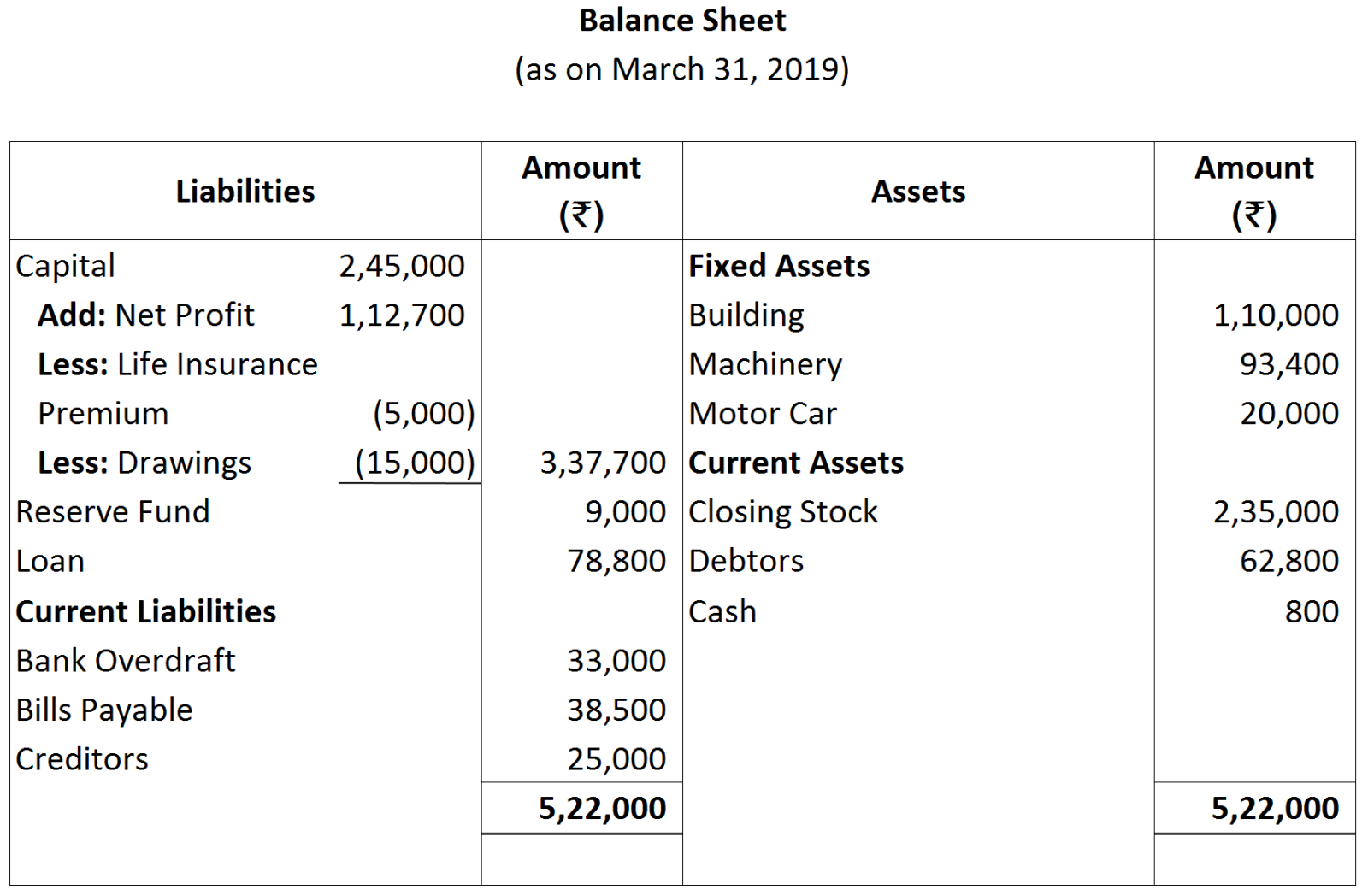

Marshalling of asset and liabilities: When assets and liabilities are shown in a particular order of liquidity or permanence, they are said to be marshalled.

- In order of liquidity: Liquidity means convertibility into cash. Assets that can be converted into cash in least possible time, i.e., more liquid assets are recorded first, followed by the lesser liquid assets. In a balance sheet, cash in hand is recorded at first and goodwill at last. In the same way, liabilities that are to be paid first, i.e., high priority liabilities are recorded first, followed by the lower priority ones. In a balance sheet, current liabilities are recorded first and then the long term liabilities and capital at the last.

- In order of permanence: It is just the reverse of the above method. In this, assets and liabilities are arranged in their reducing level of permanence. The assets with higher degree of permanence are recorded first, followed by the assets with lower degree of permanence. For example, goodwill, land and building have the highest degree of permanence and hence are recorded at the top, whereas, cash at bank and cash in hand are recorded at the bottom. In the same way, liabilities are shown according to their life in the business. Liabilities with higher level of permanence like, capital is recorded at the top and other liabilities with lower permanence are recorded at the bottom.

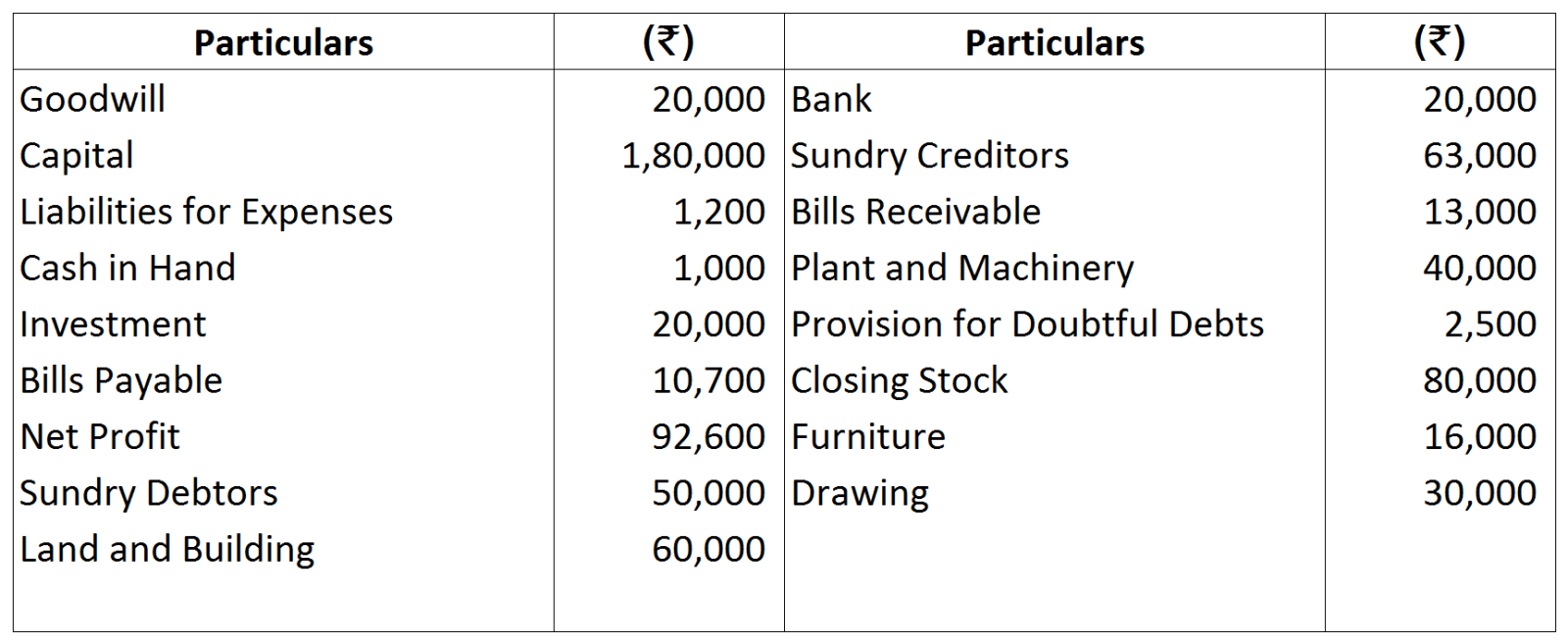

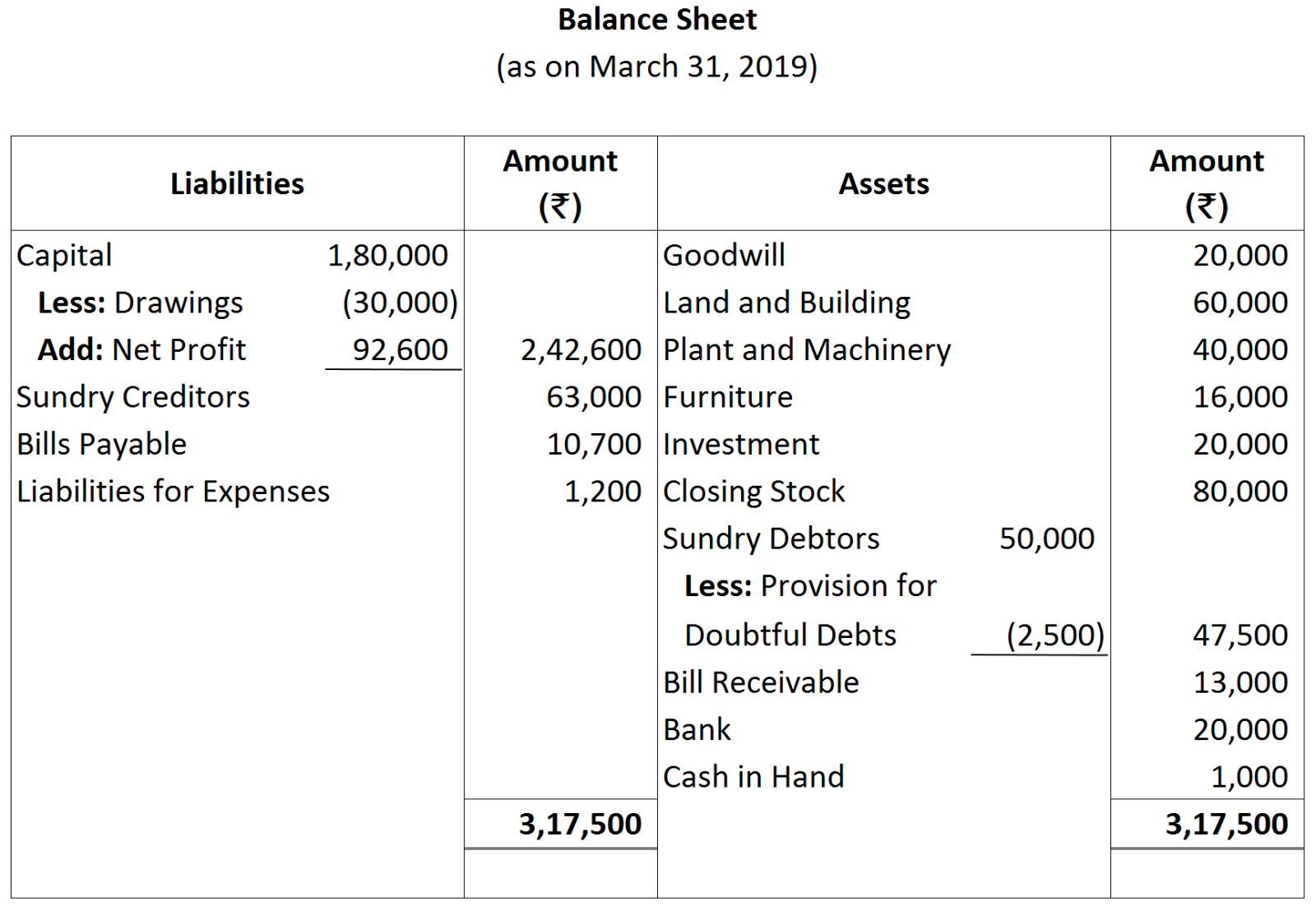

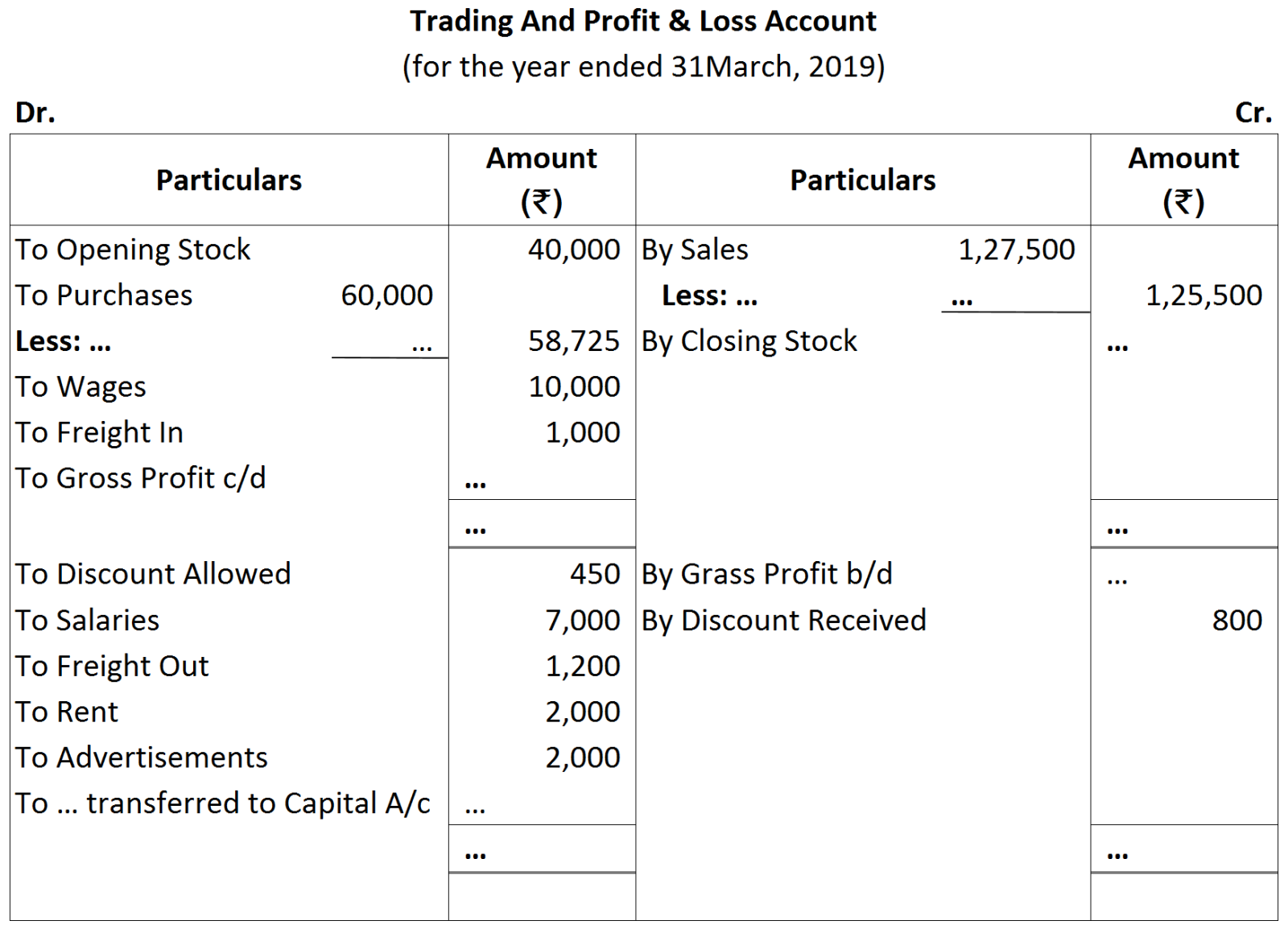

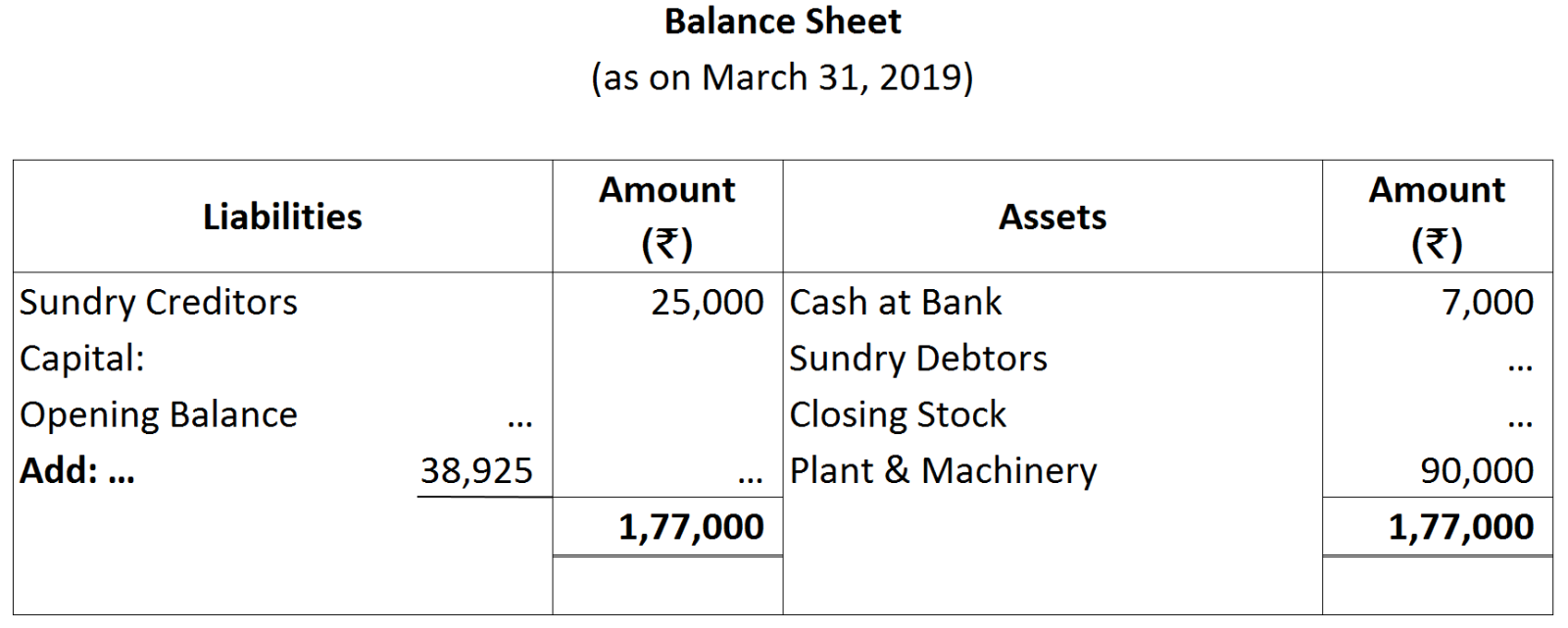

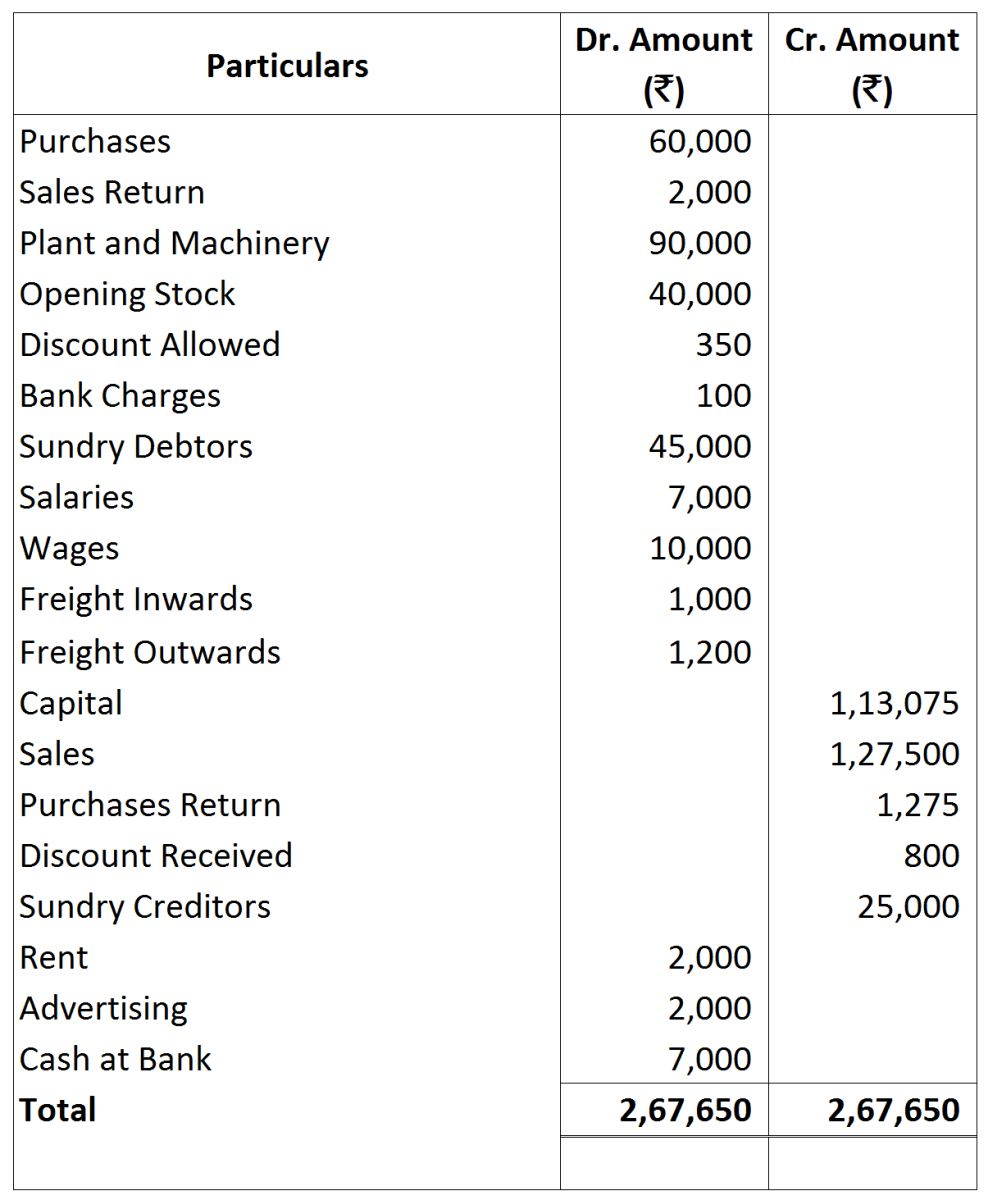

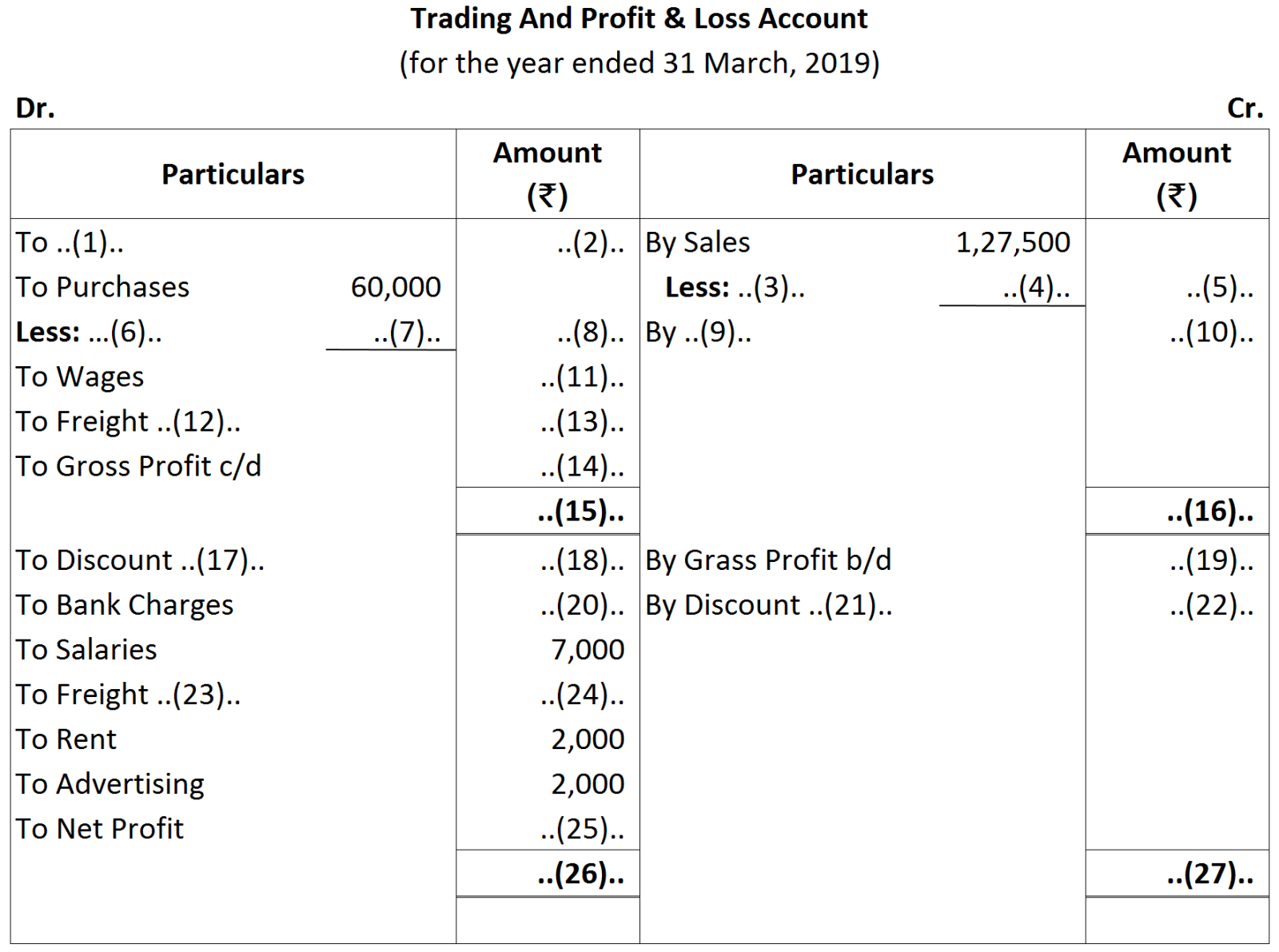

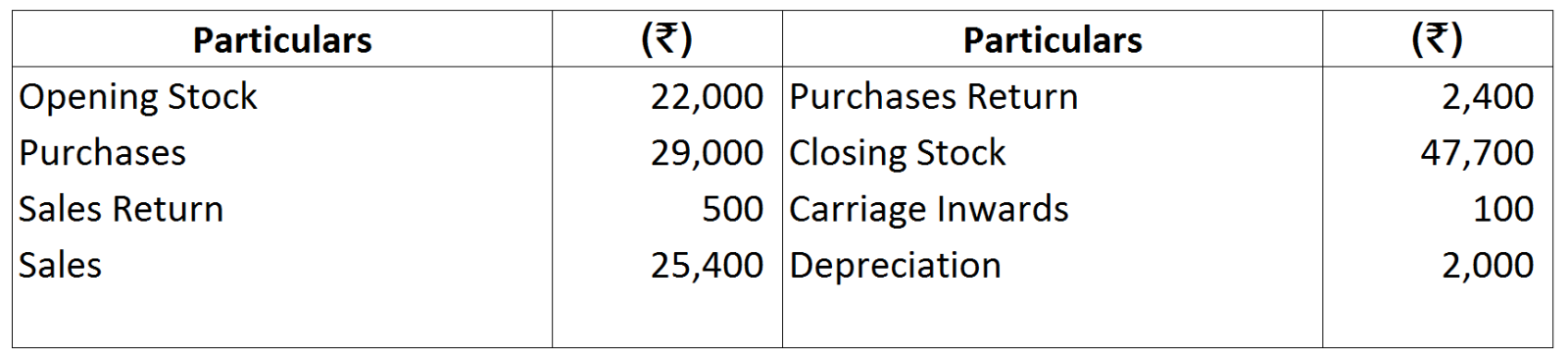

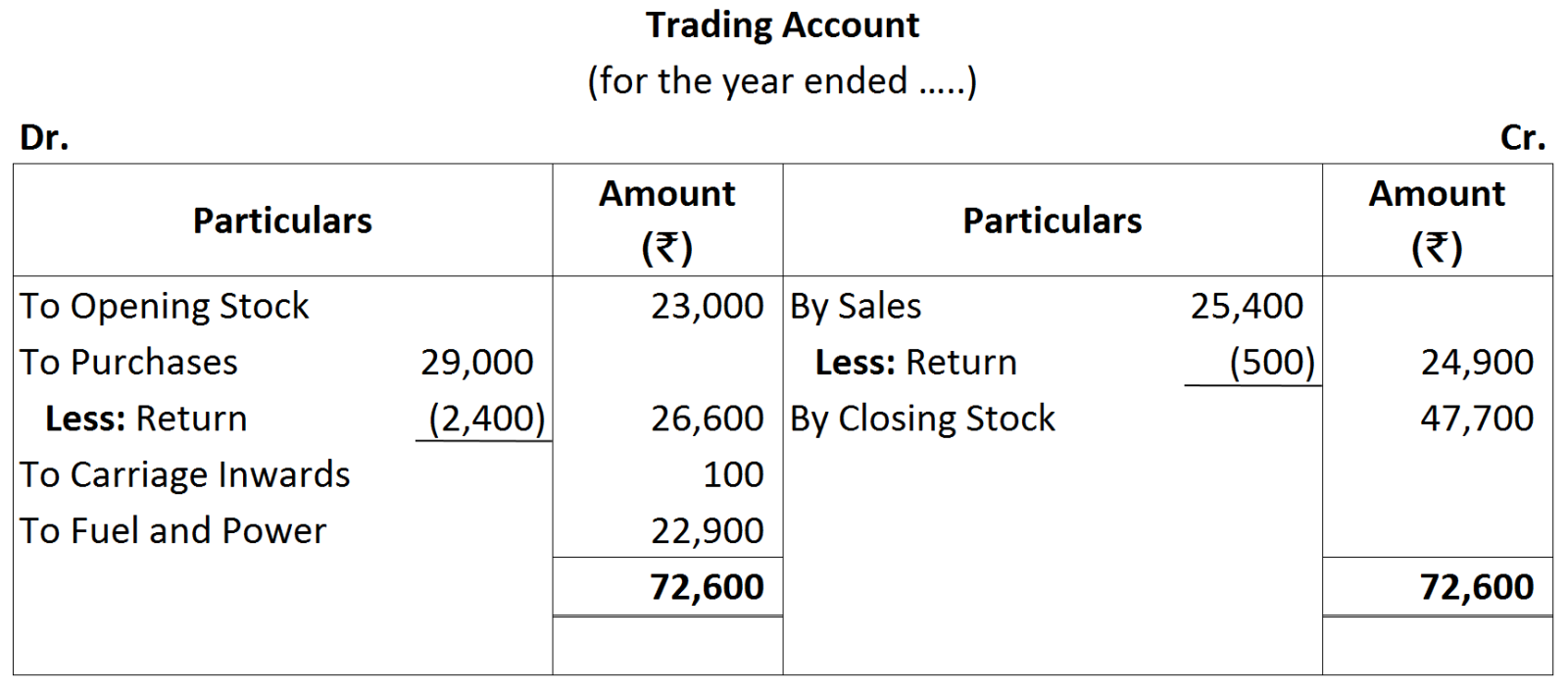

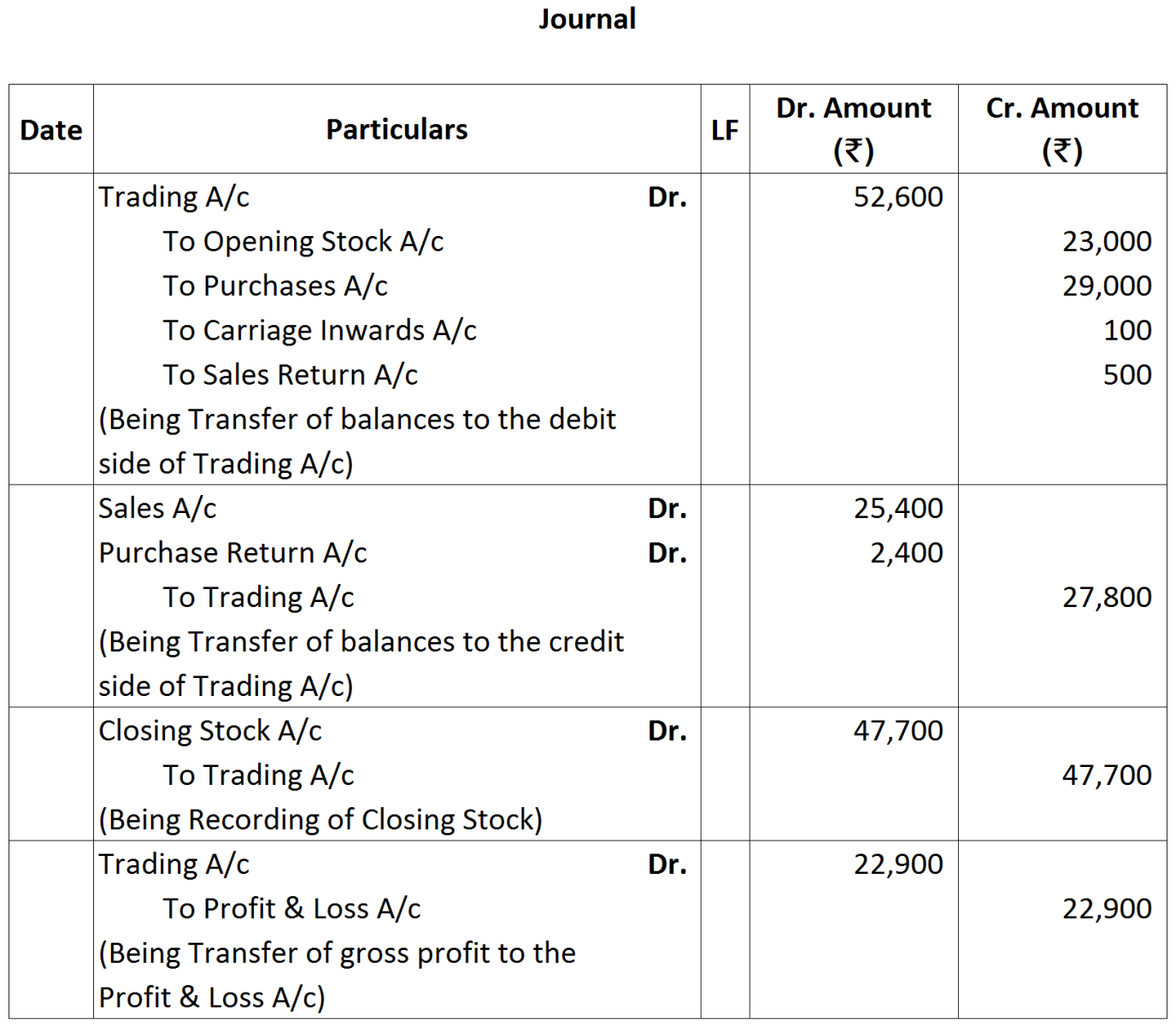

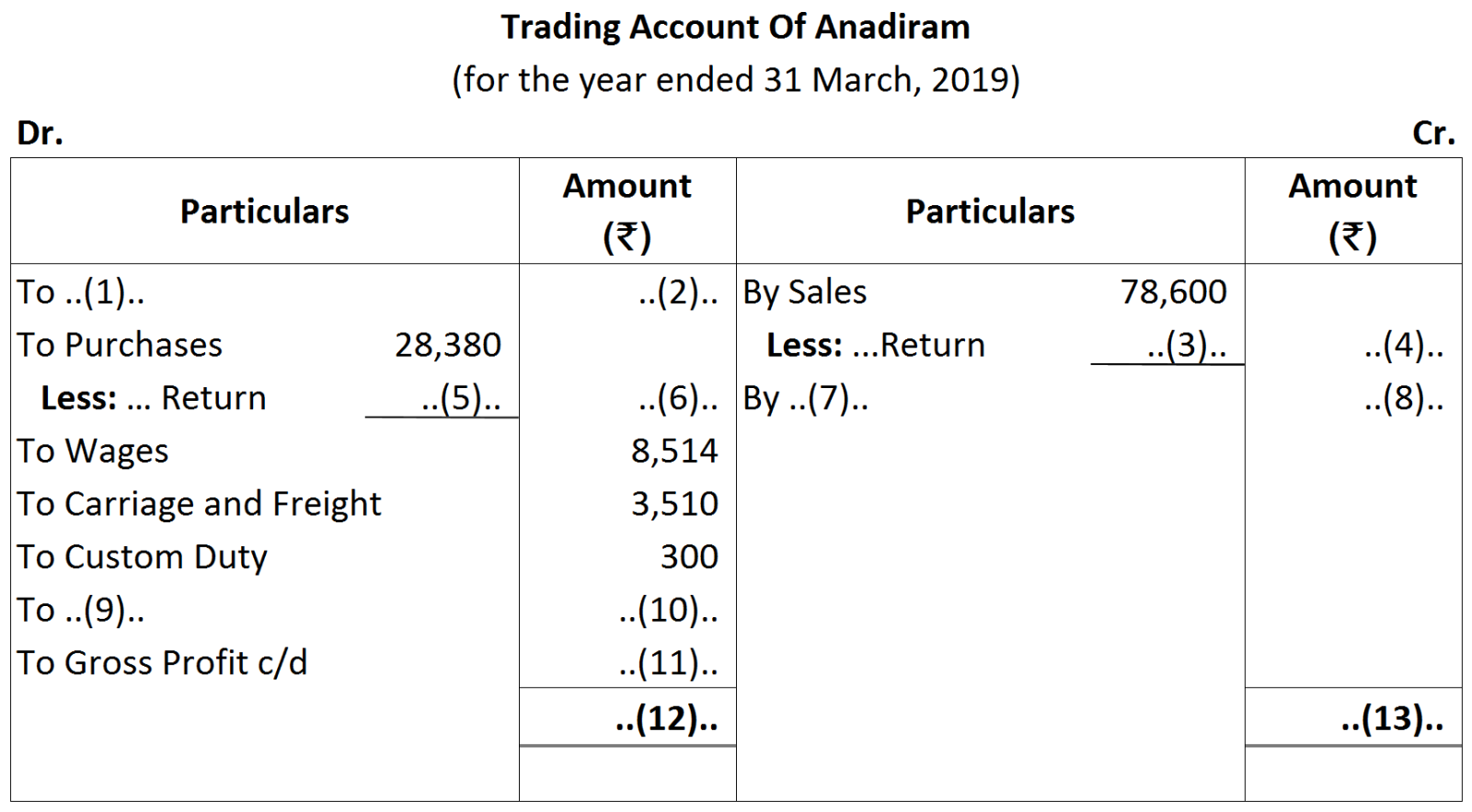

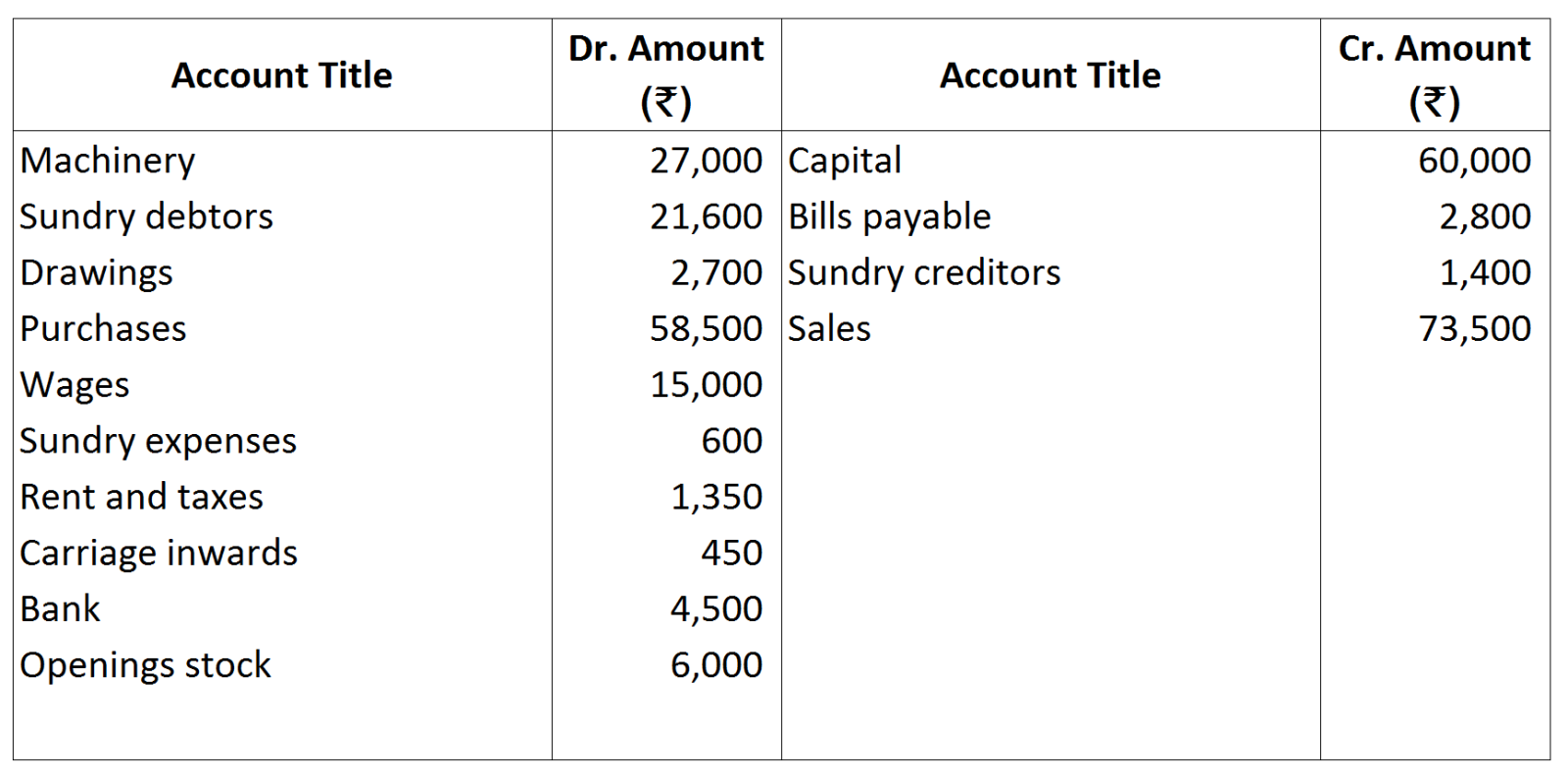

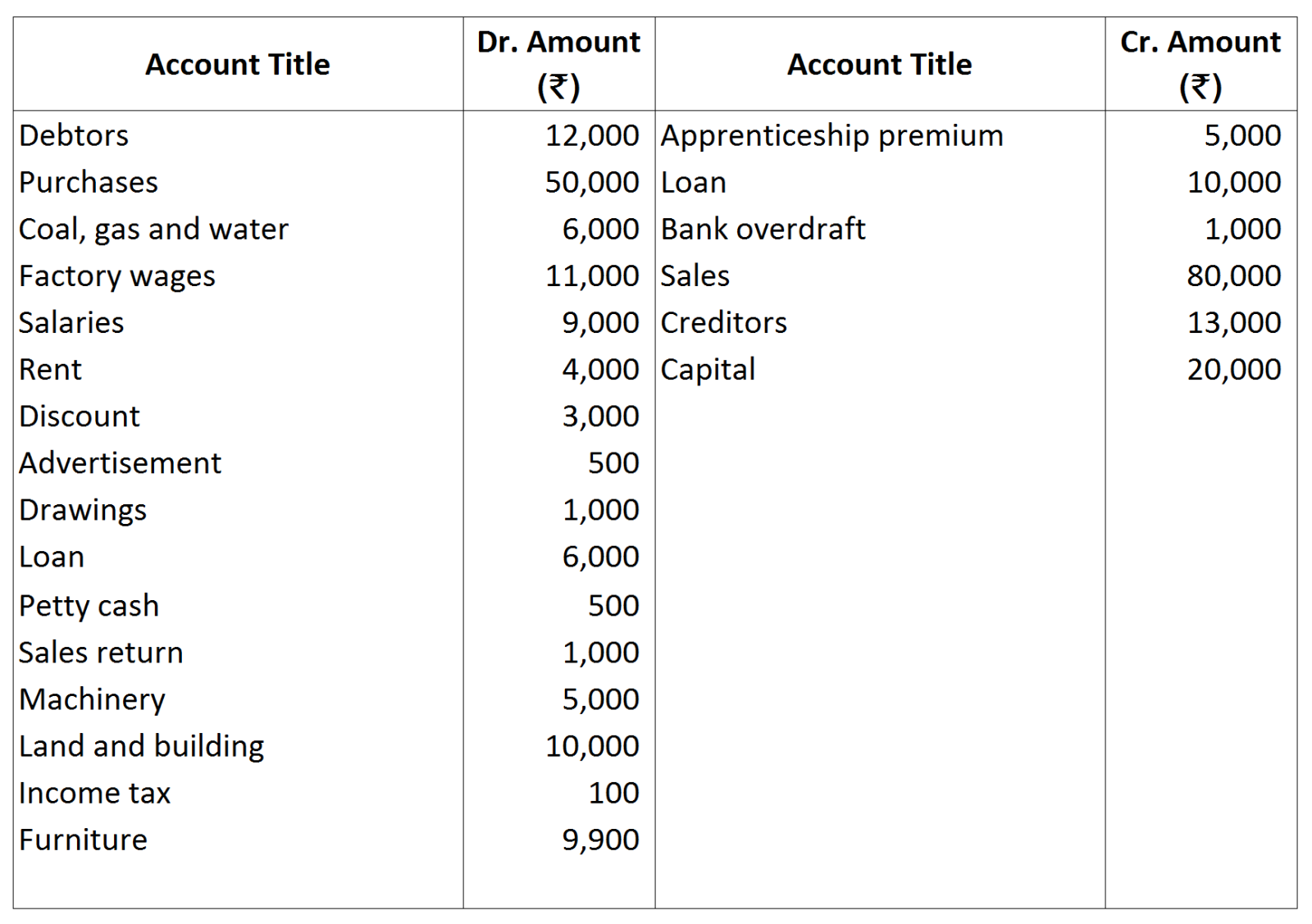

Also pass the Journal entries.

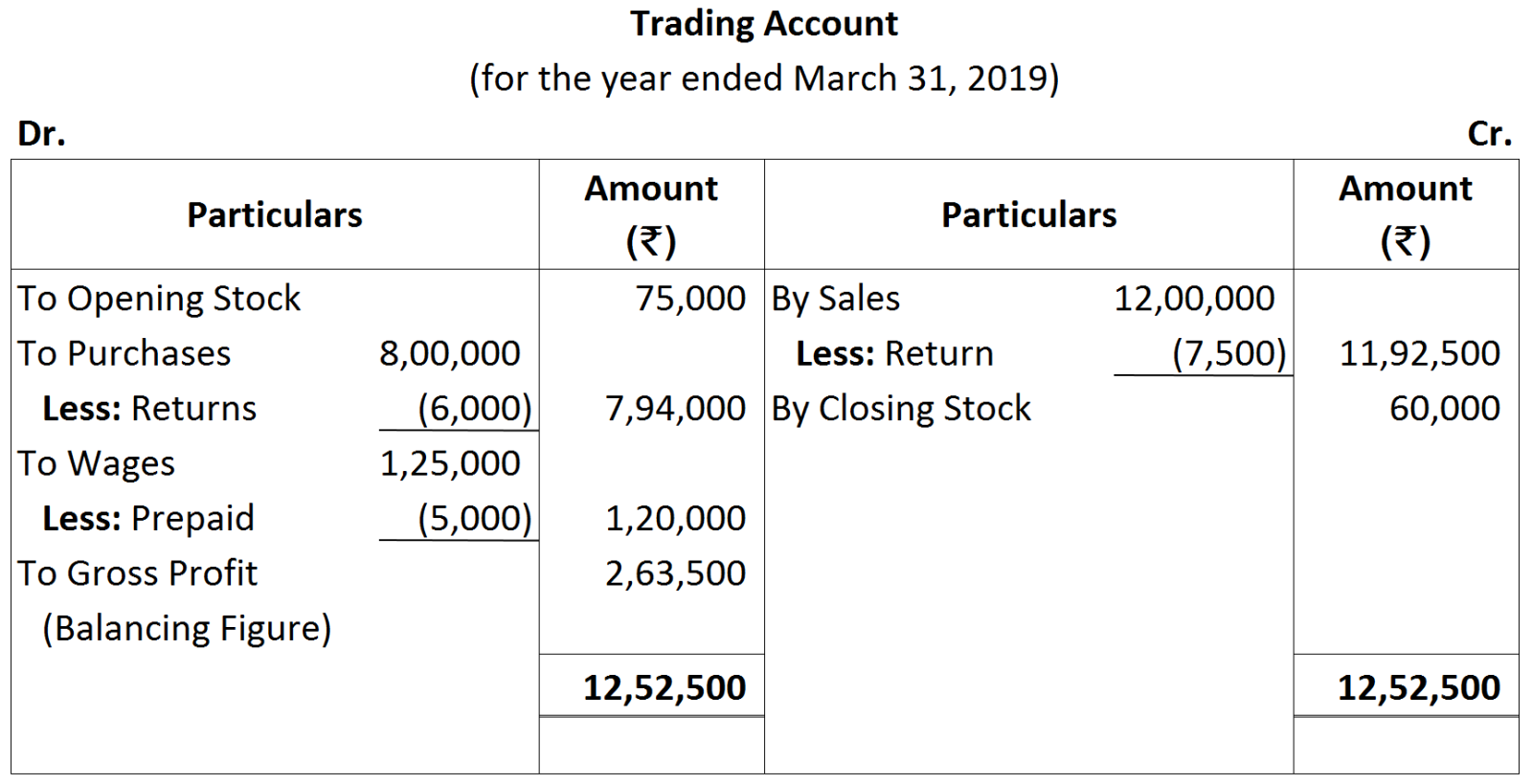

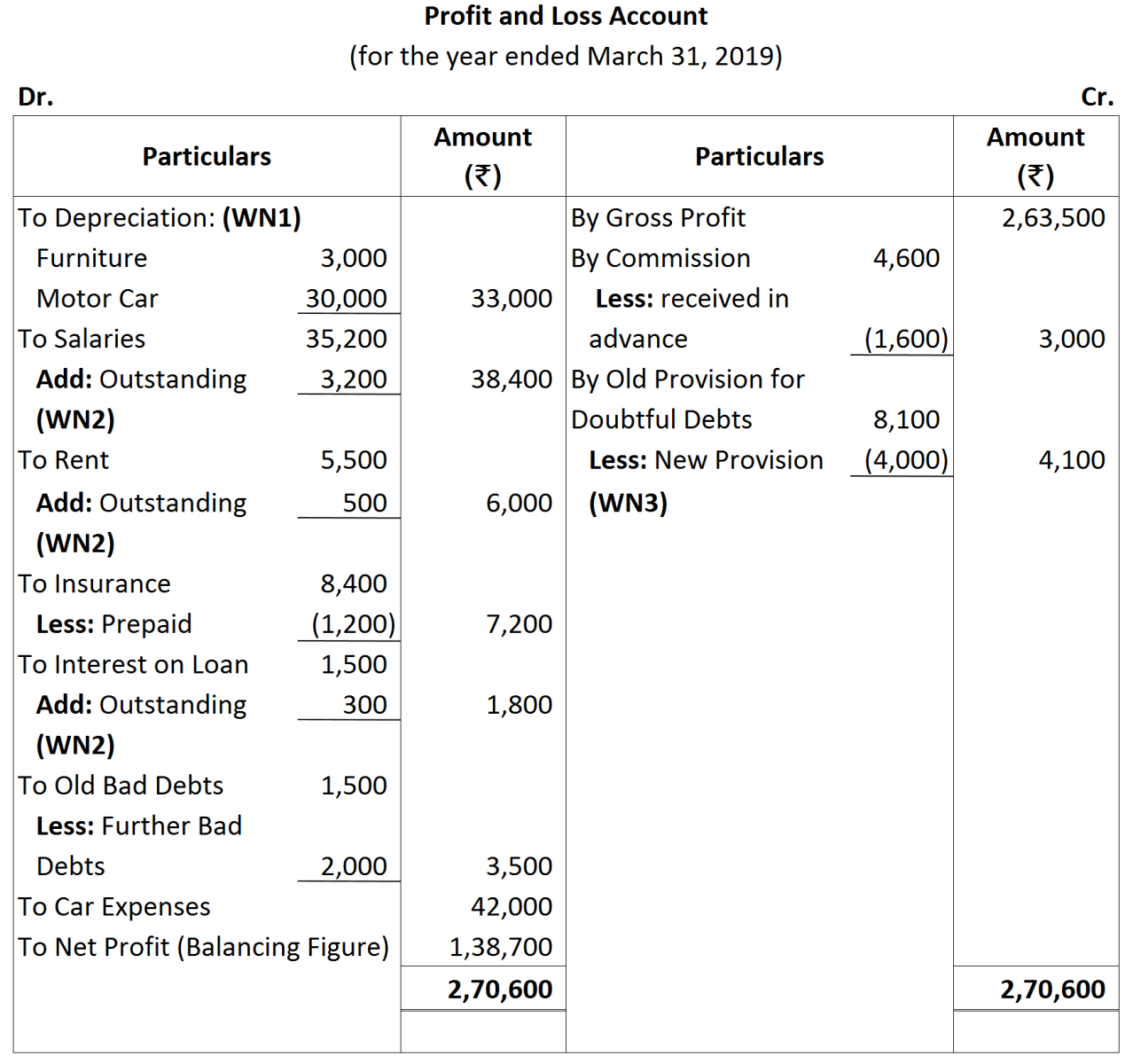

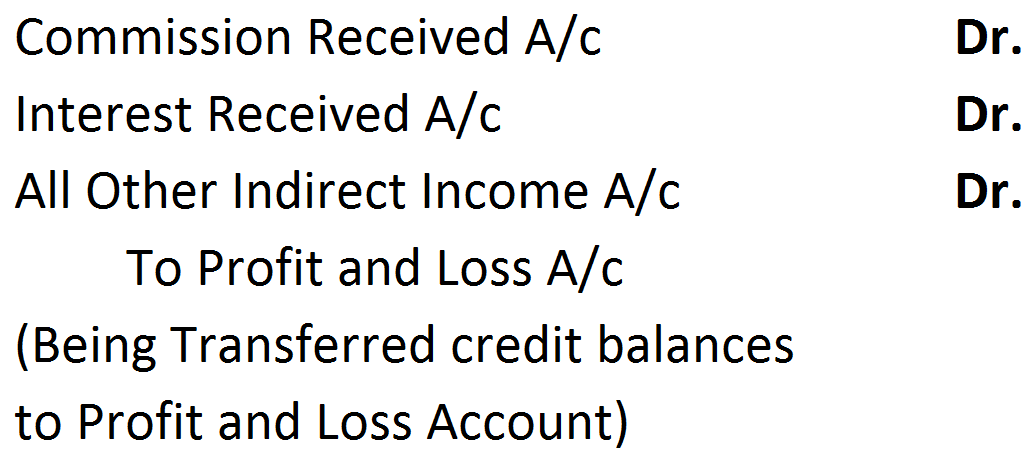

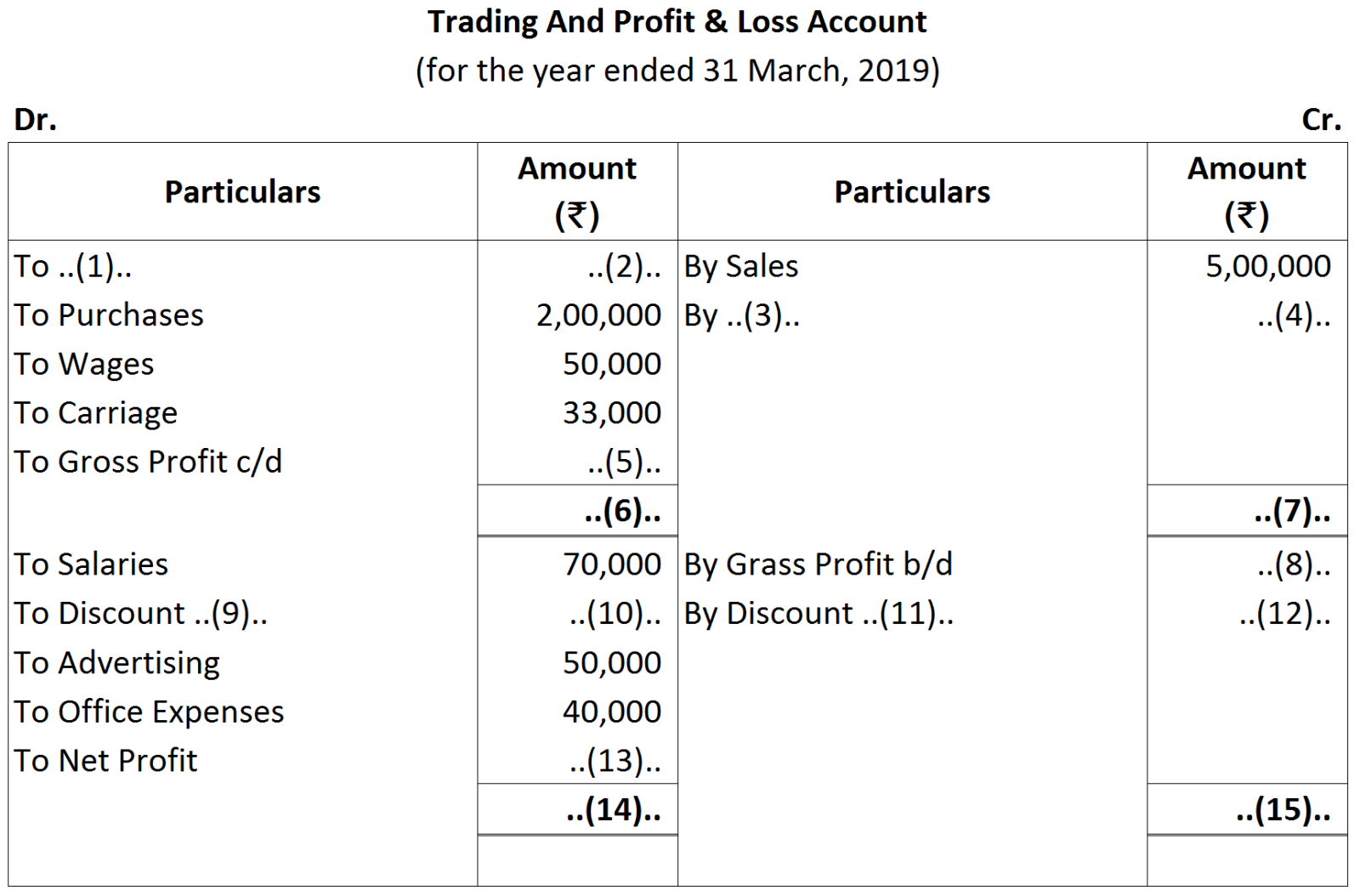

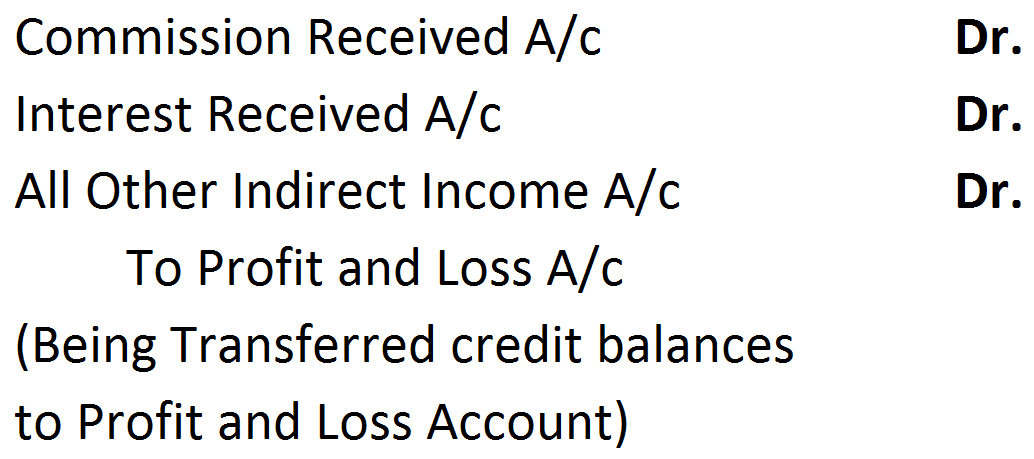

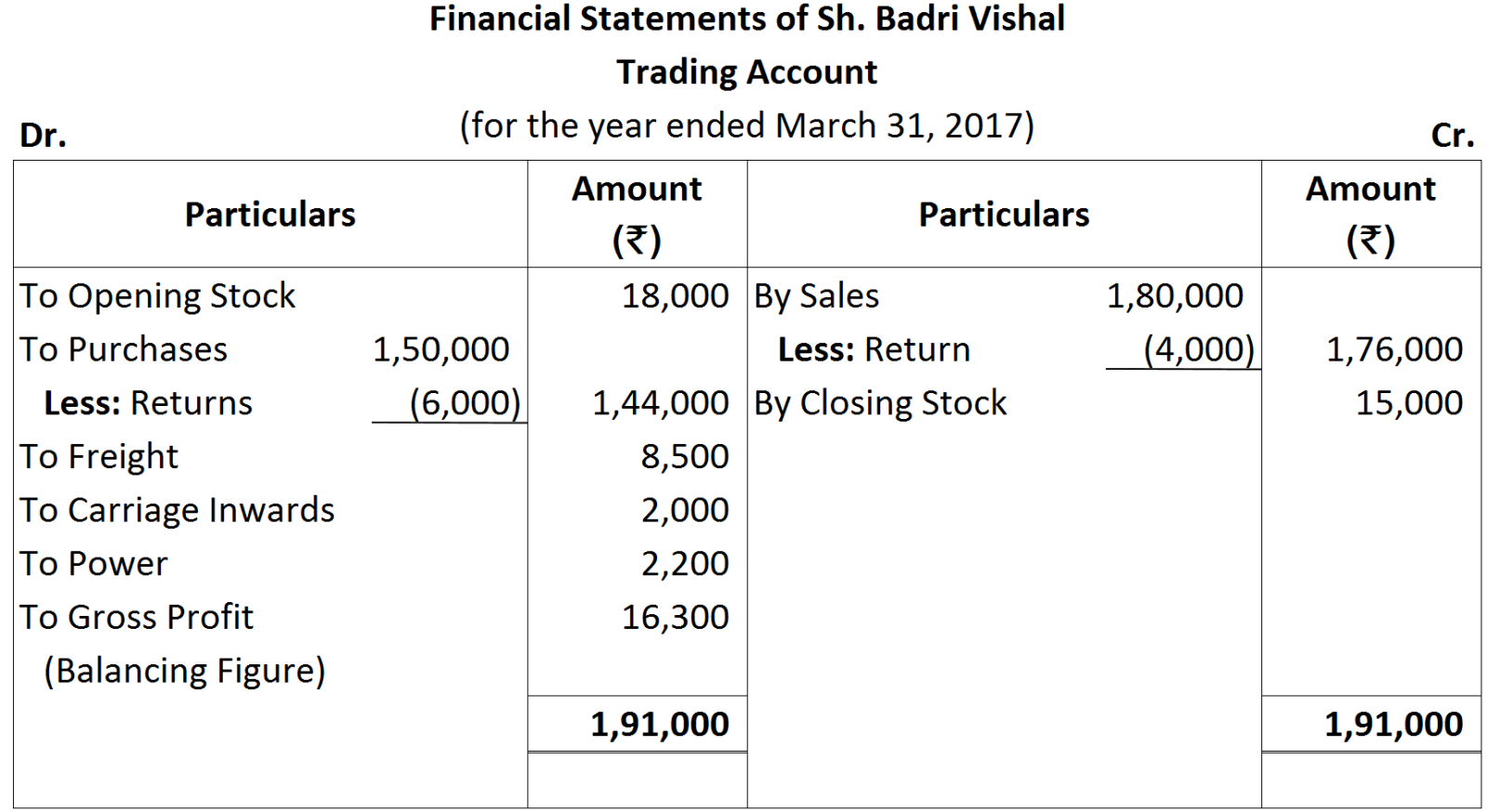

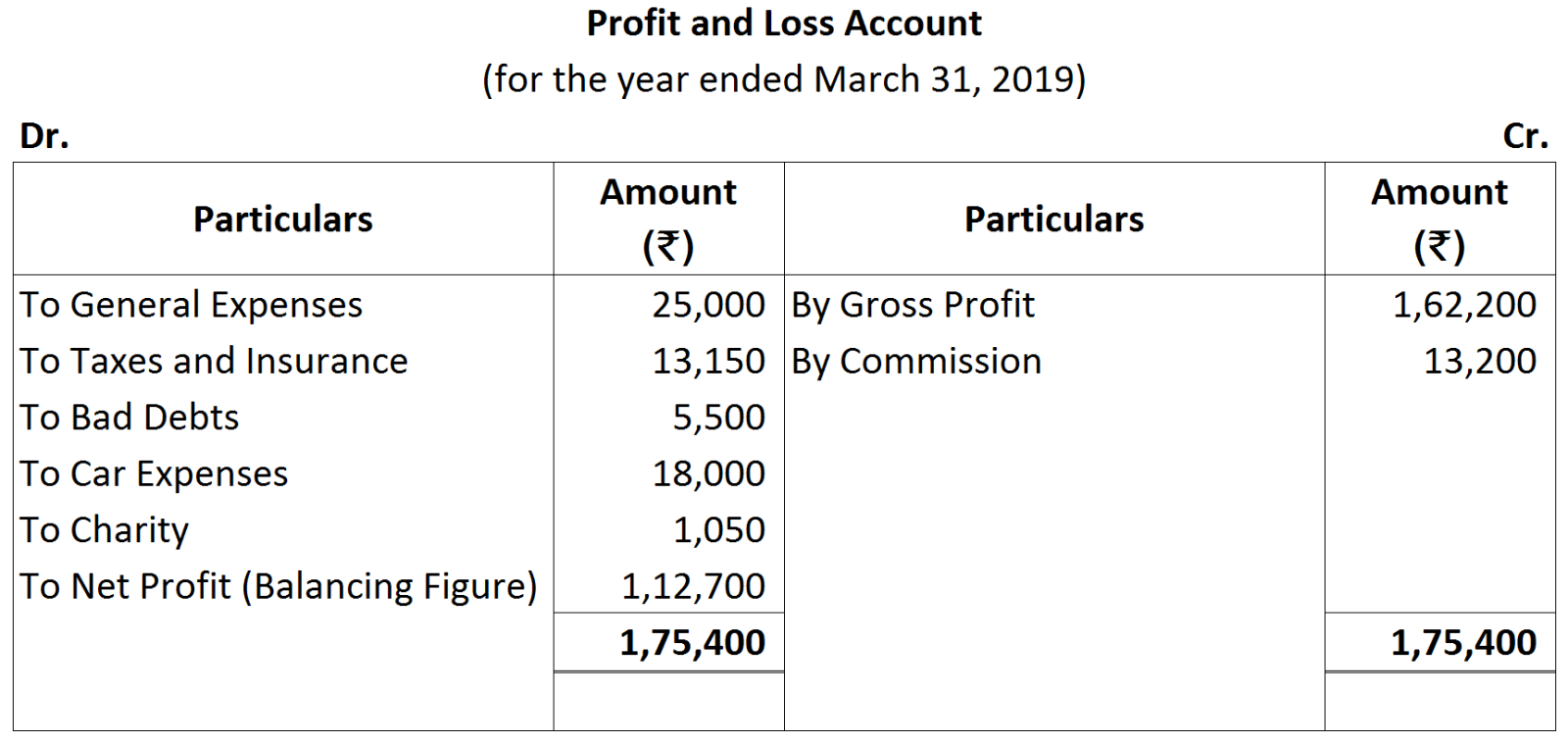

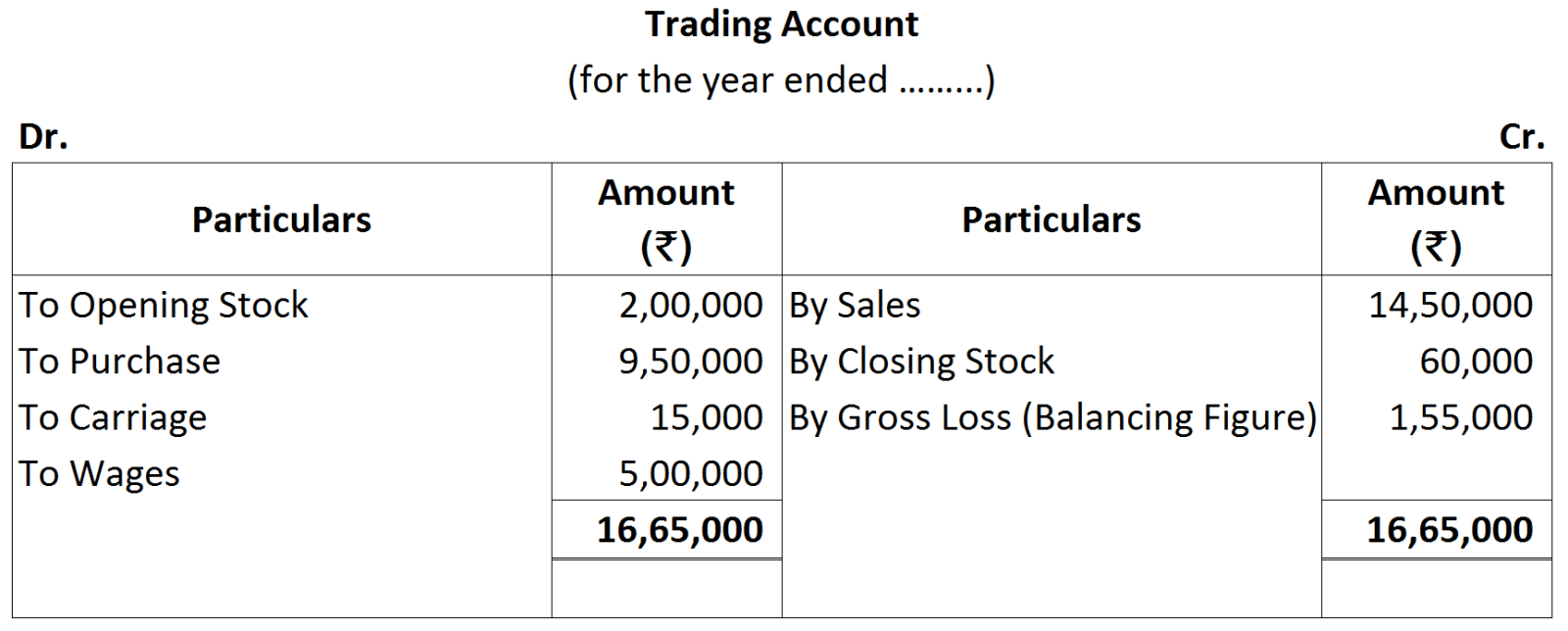

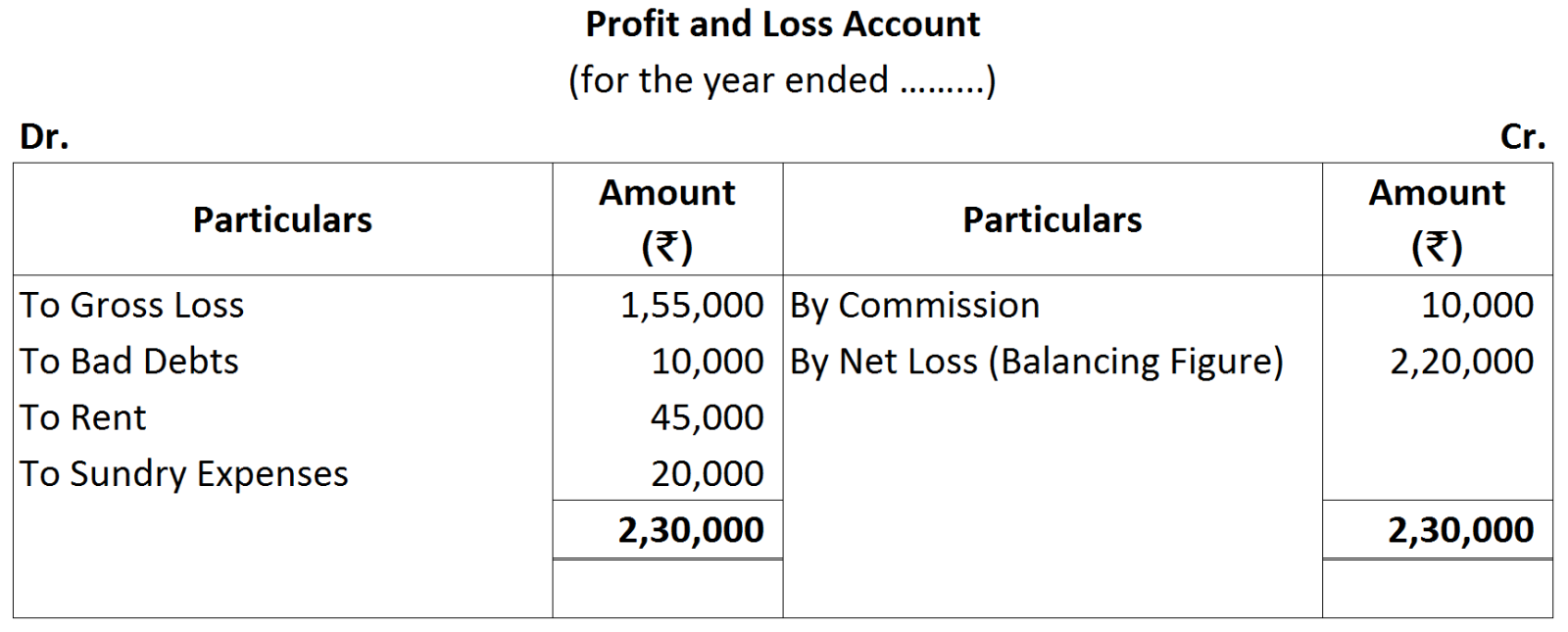

Also pass the Journal entries. Note: Depreciation is an Indirect Expense, therefore it is not shown in the Trading Account.

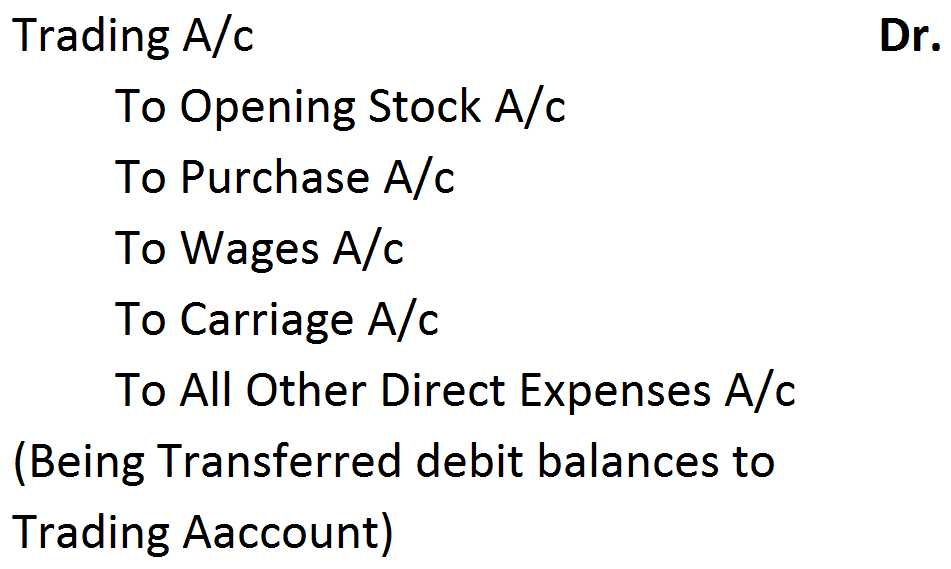

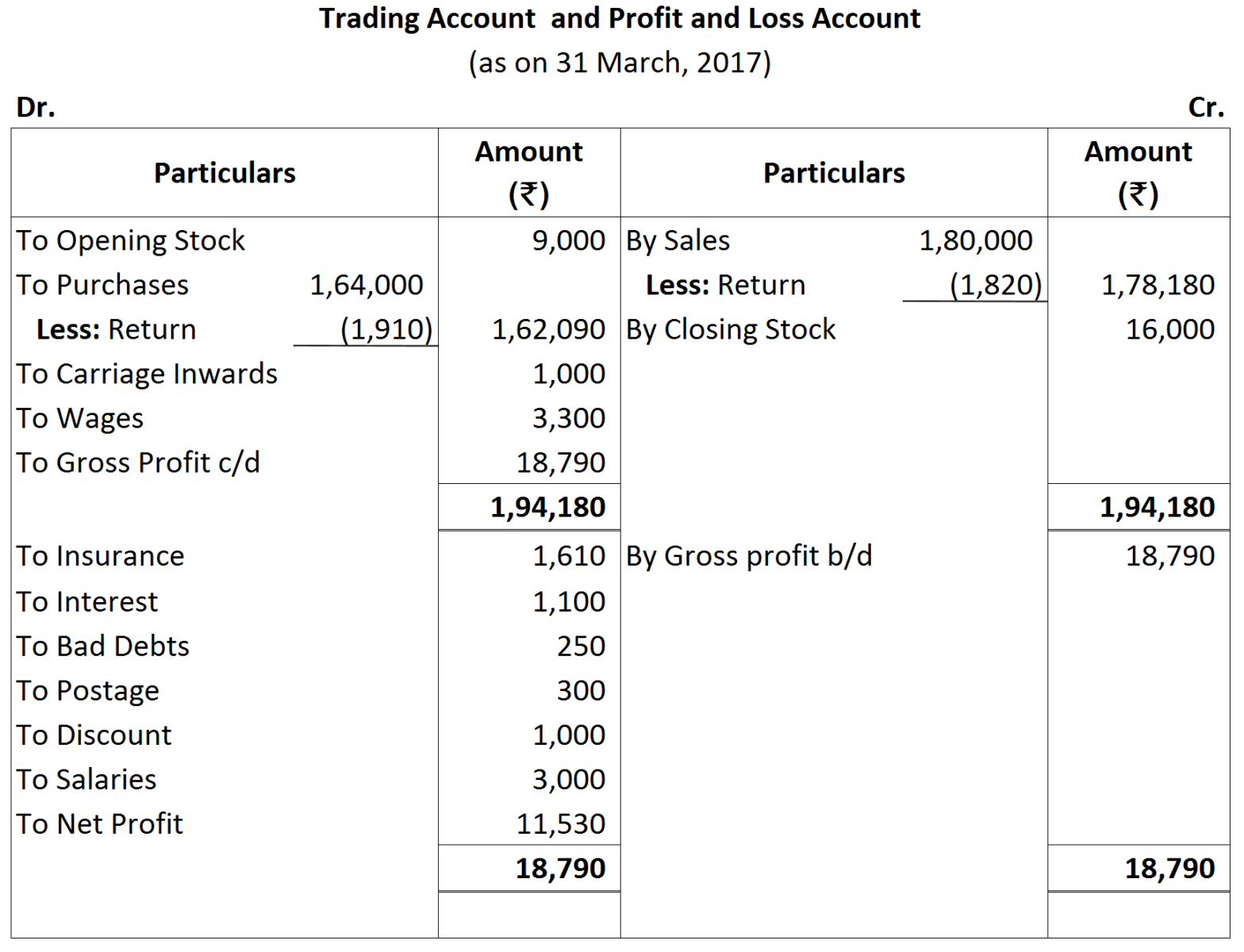

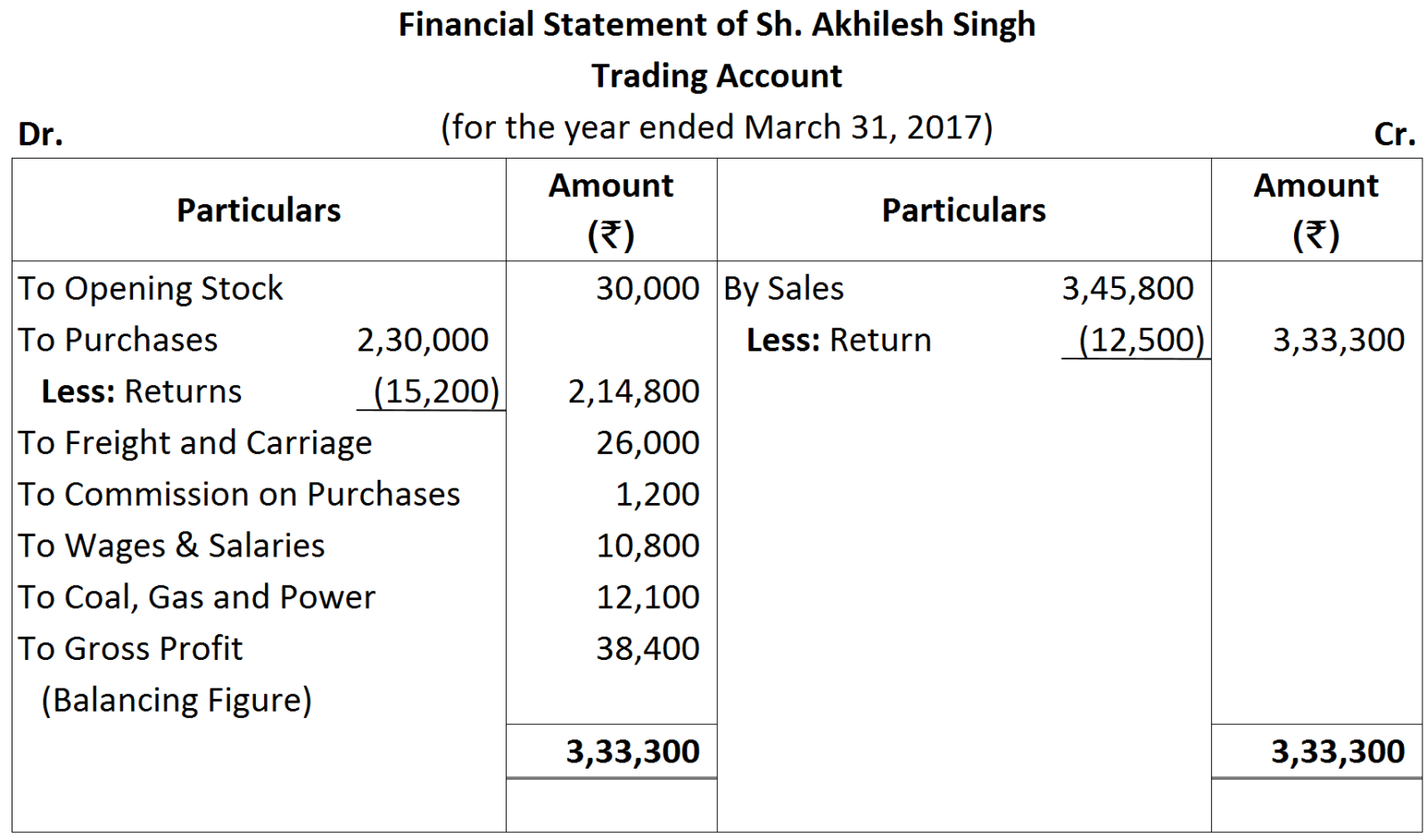

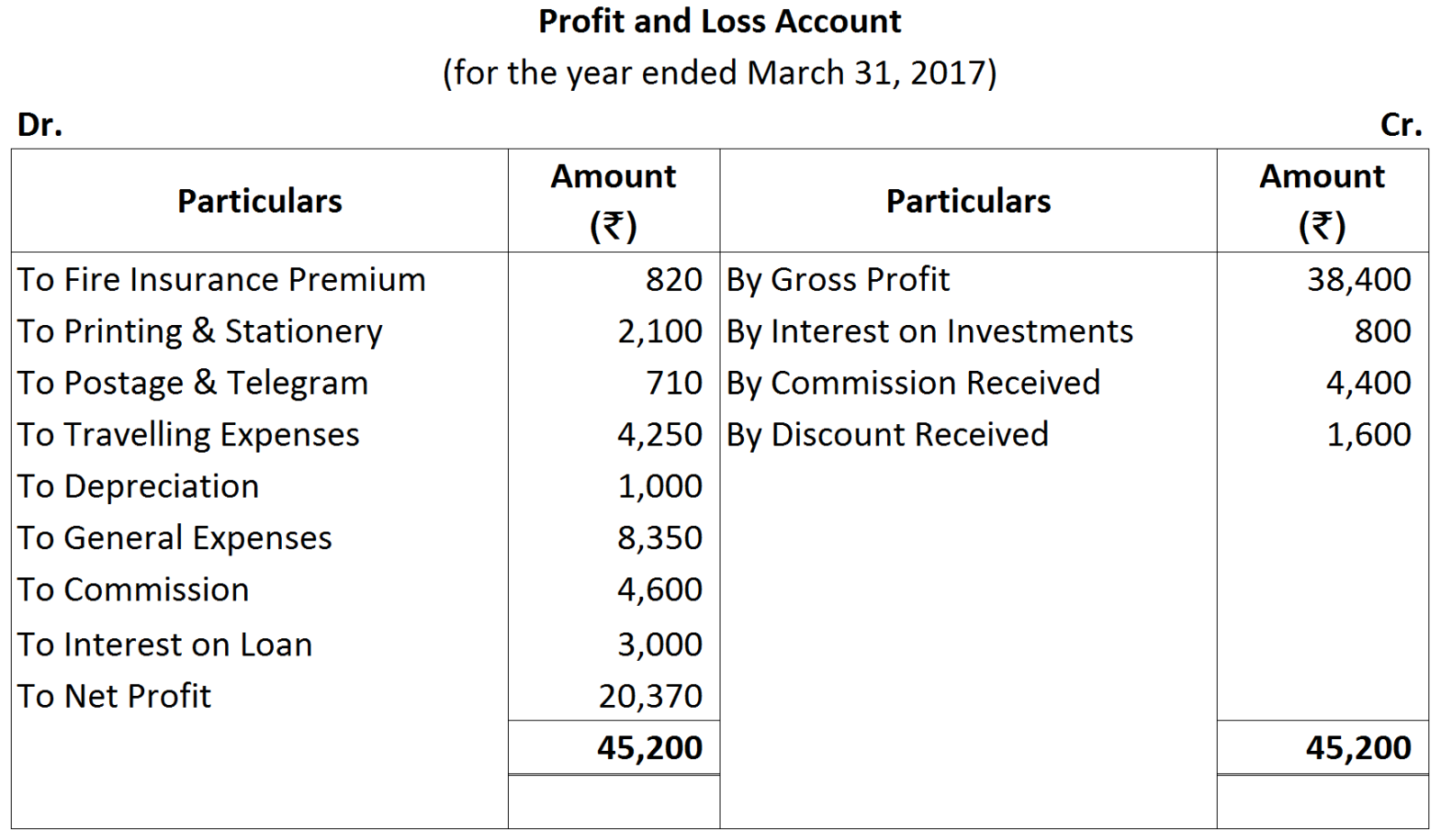

Note: Depreciation is an Indirect Expense, therefore it is not shown in the Trading Account.

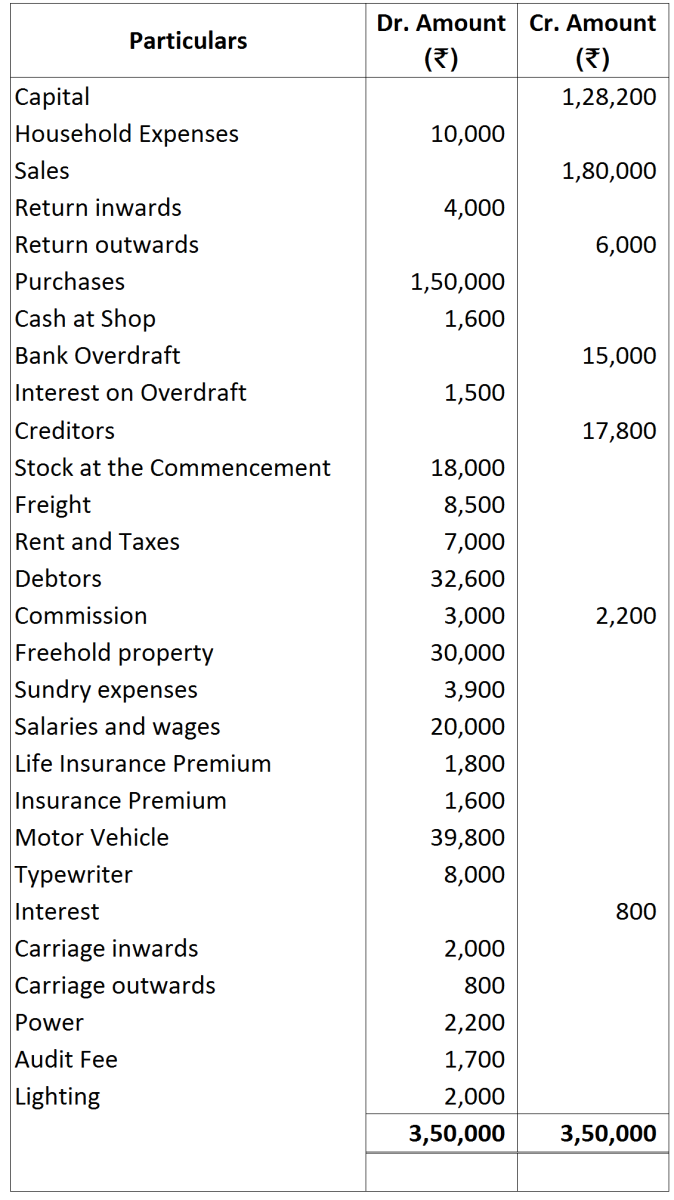

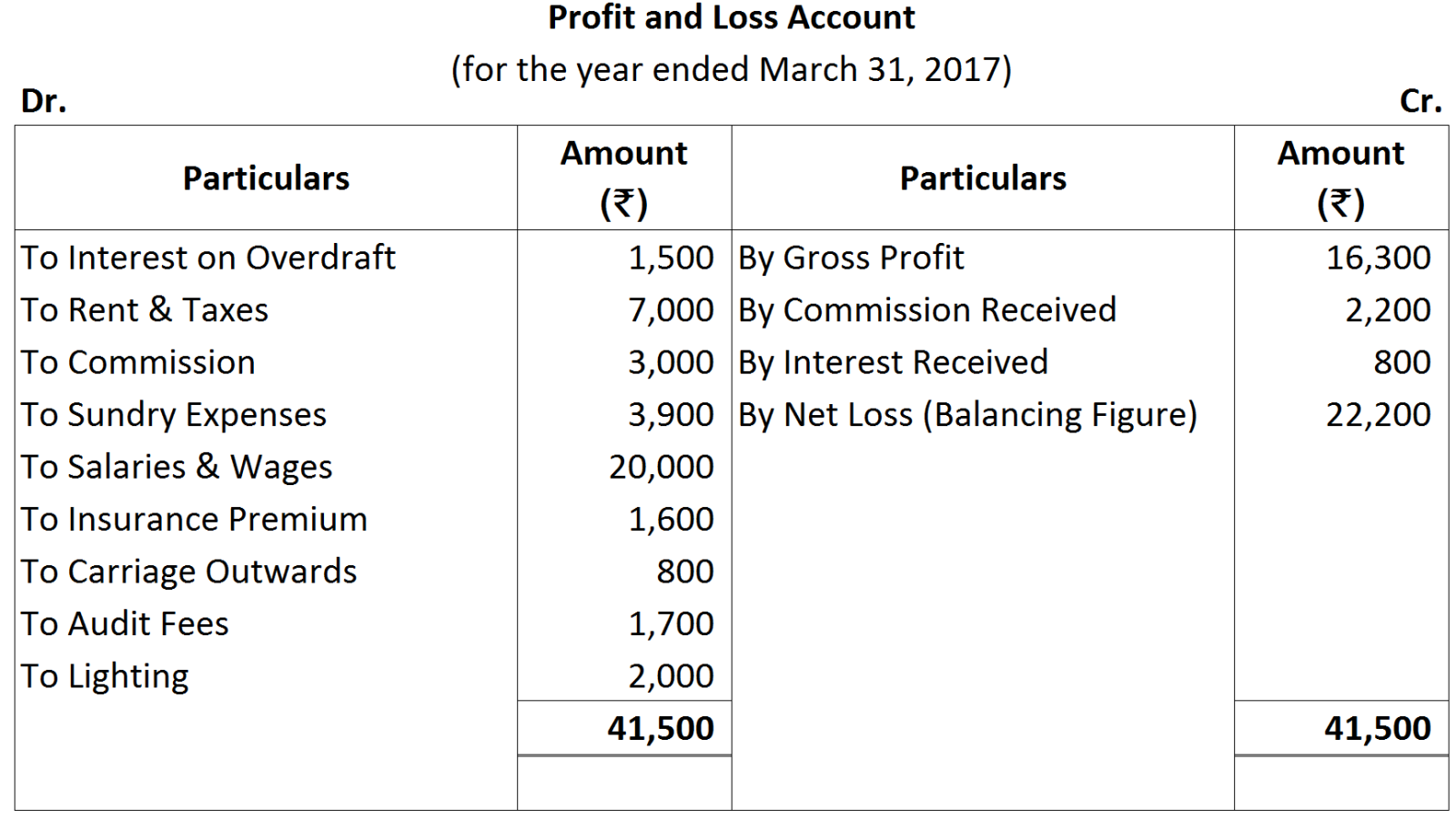

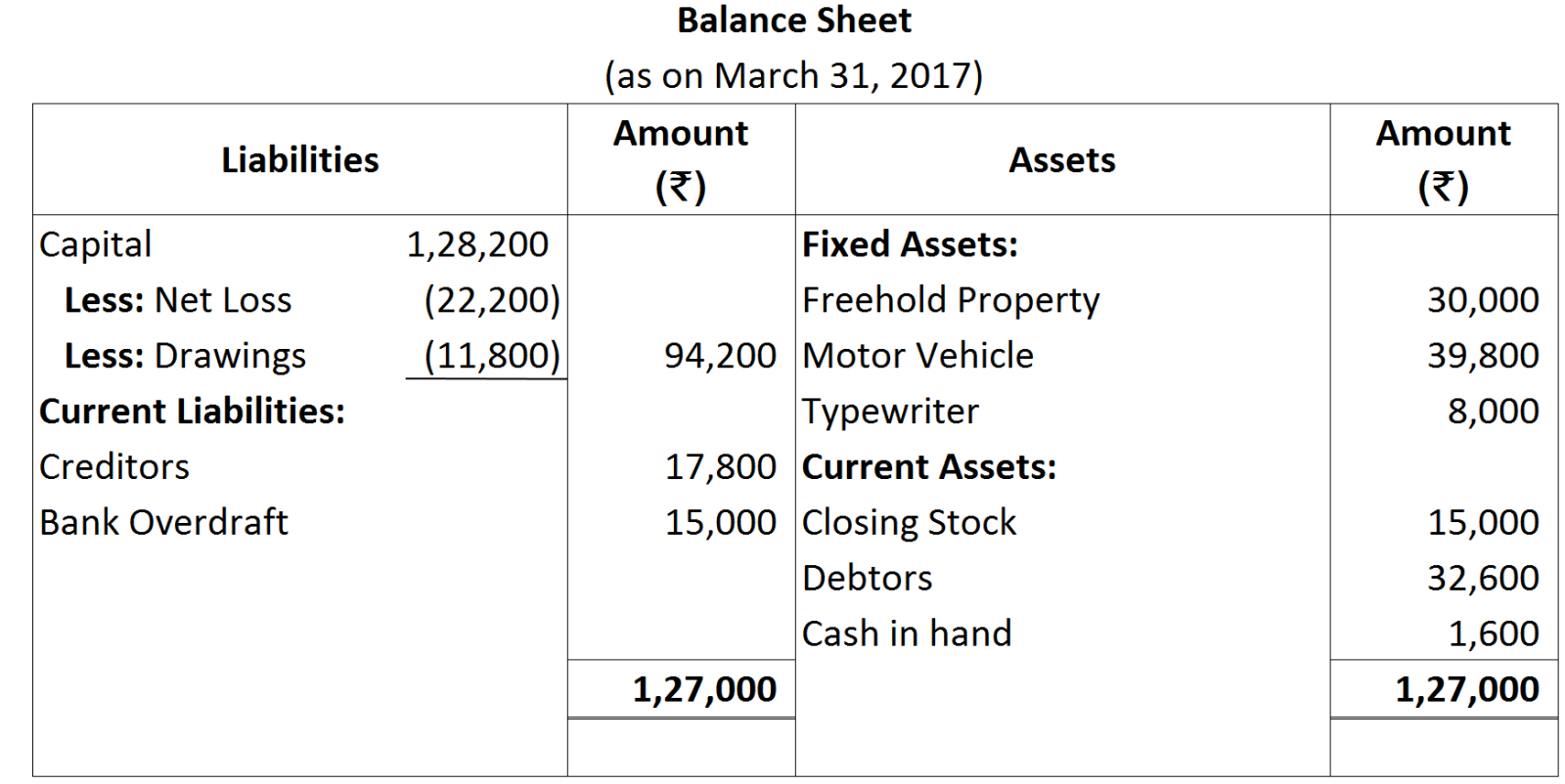

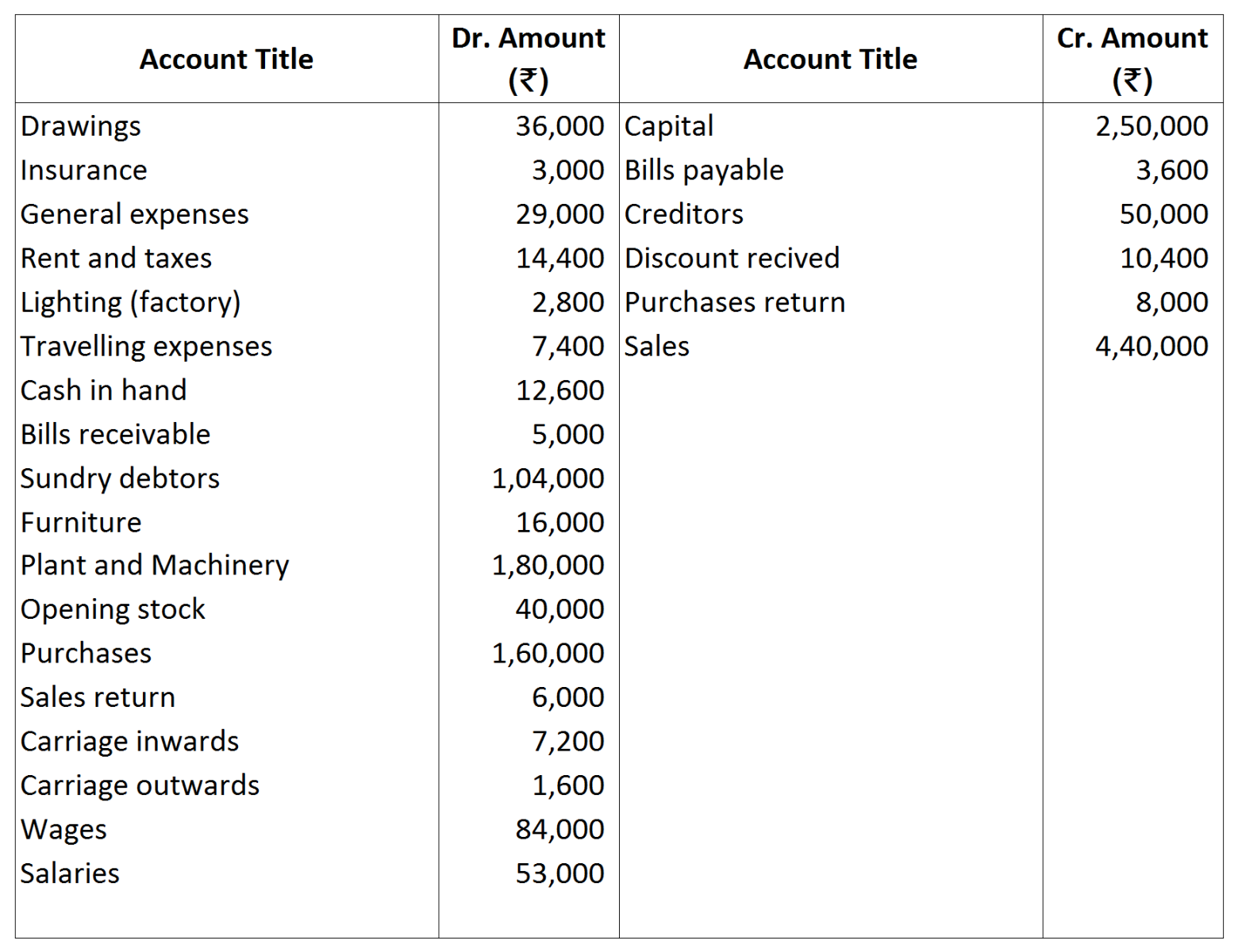

*Drawings = Household Expenses + Life Insurance Premium = 10,000 + 1,800 = ₹ 11,800.

*Drawings = Household Expenses + Life Insurance Premium = 10,000 + 1,800 = ₹ 11,800.

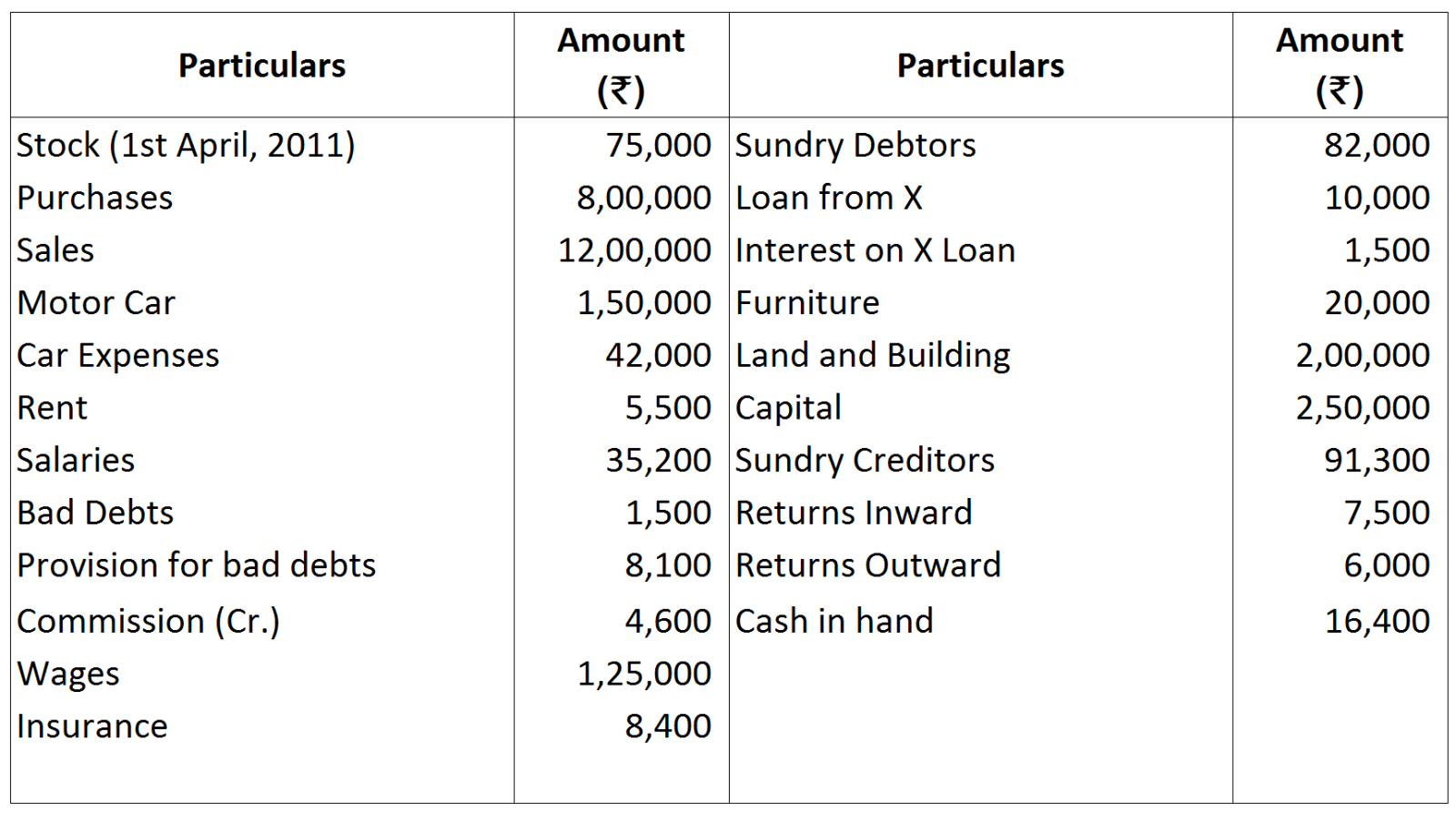

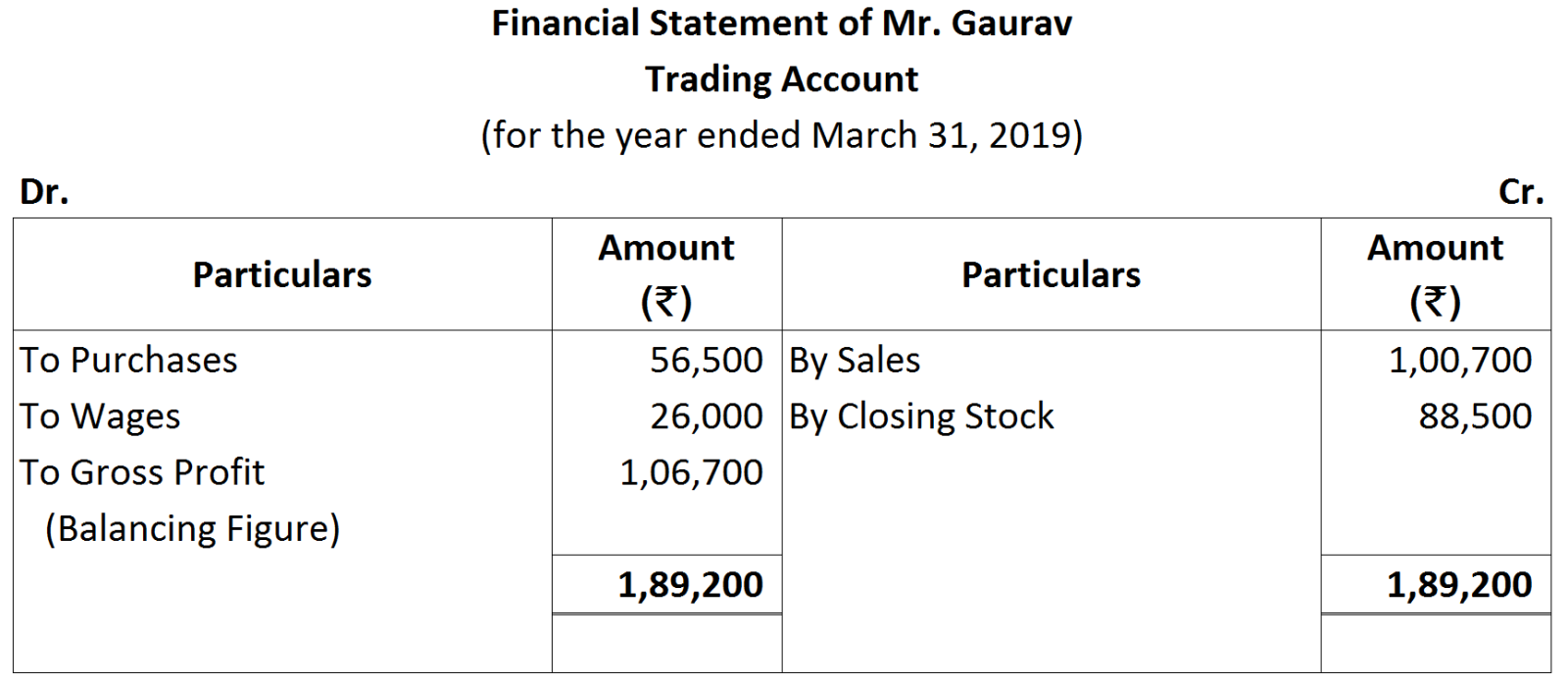

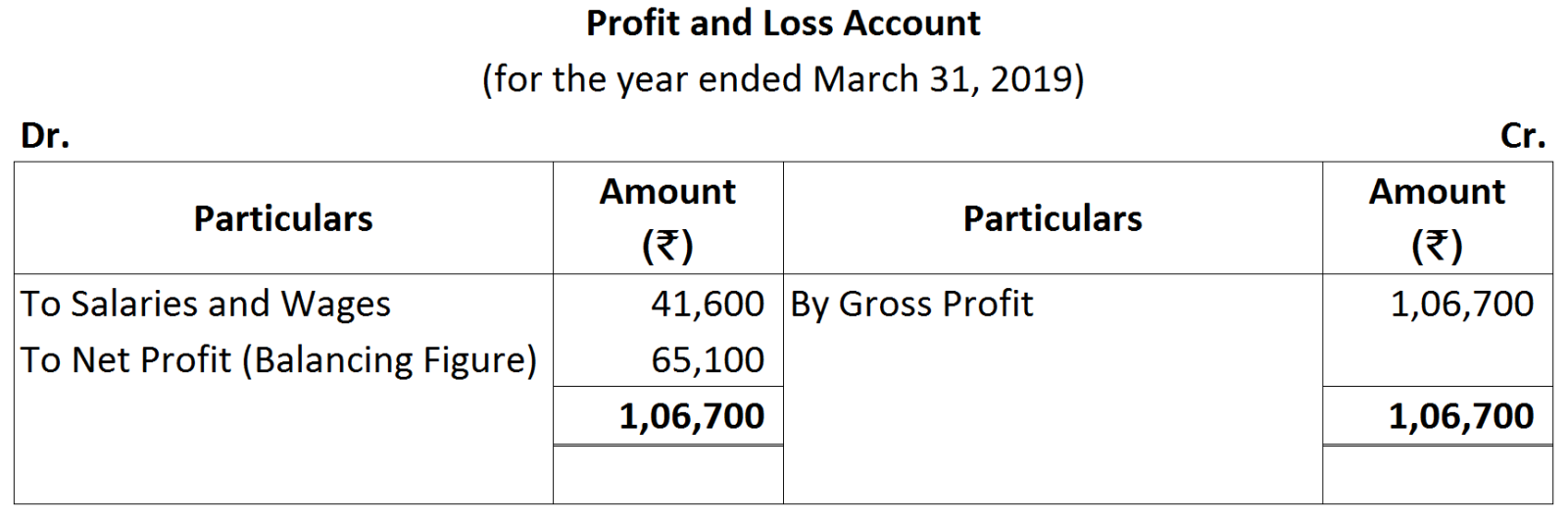

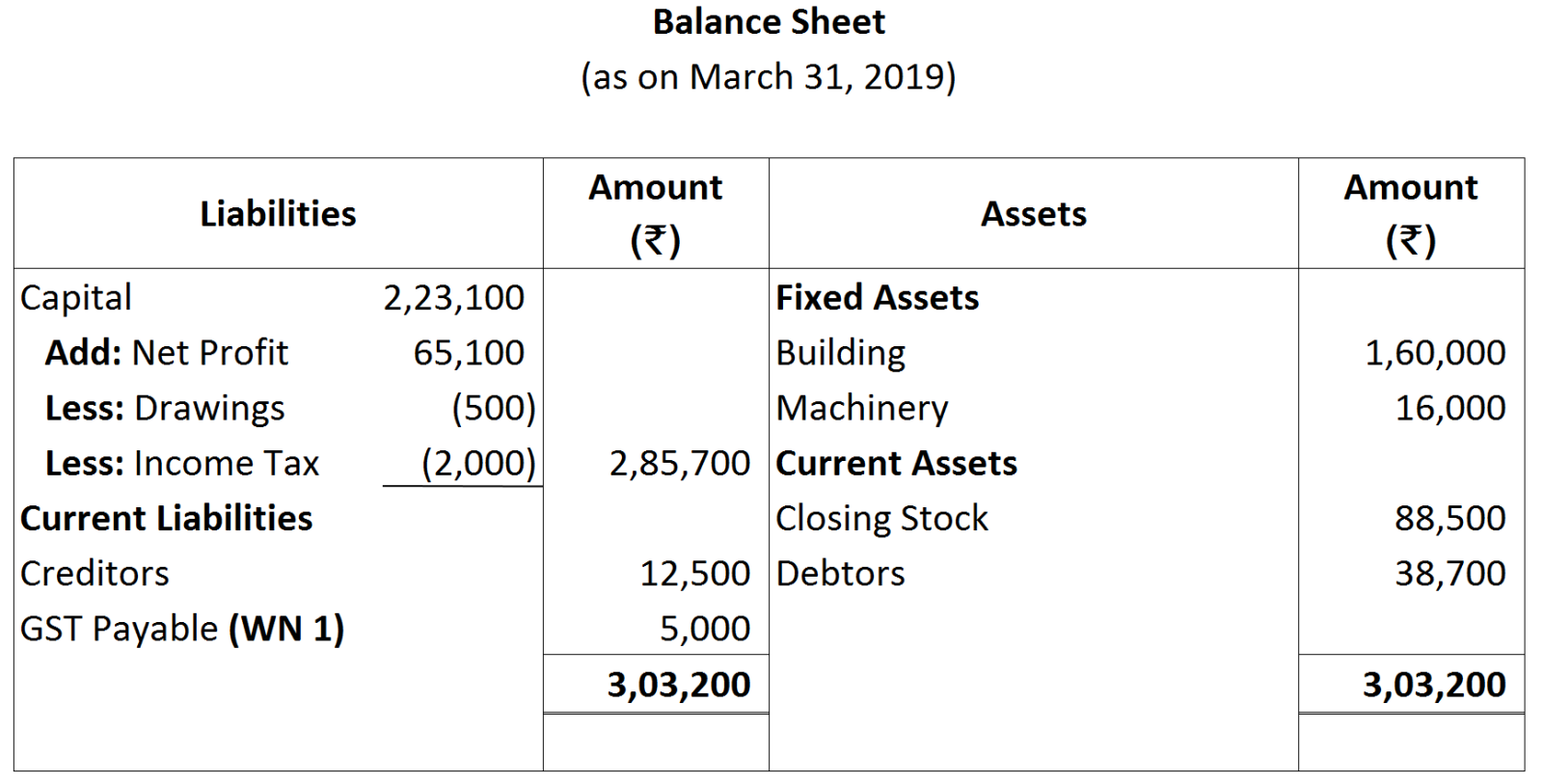

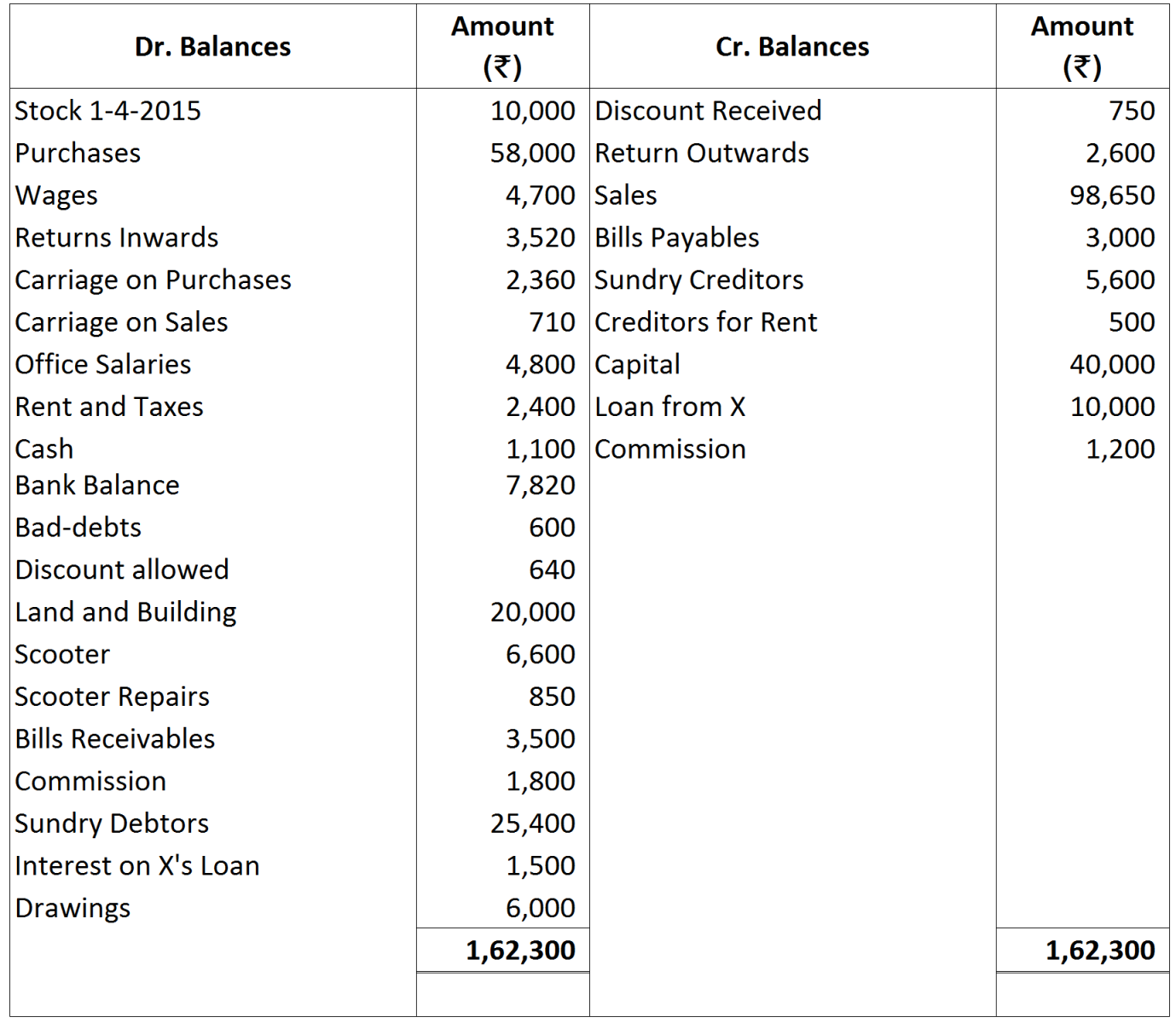

Working Note:

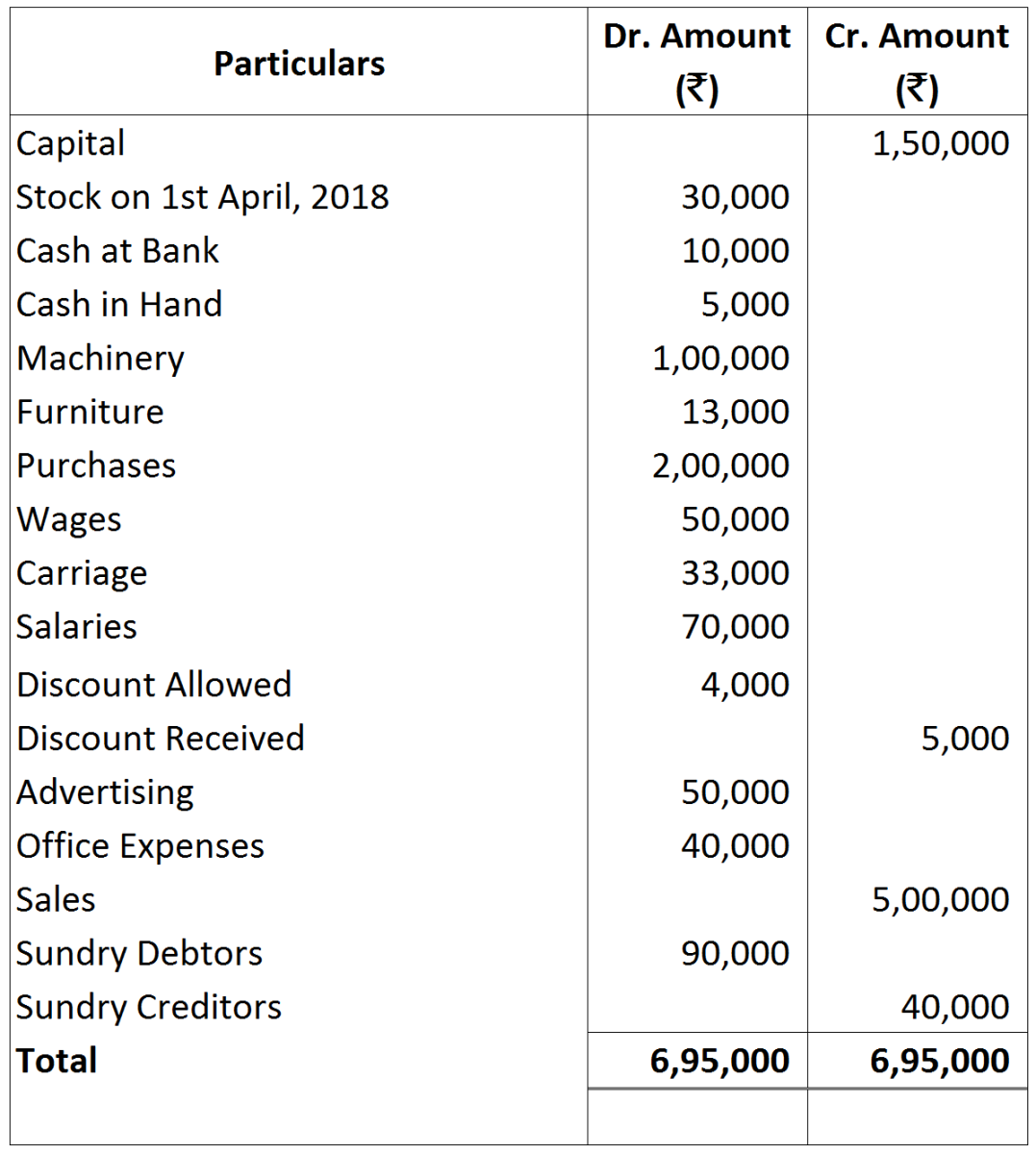

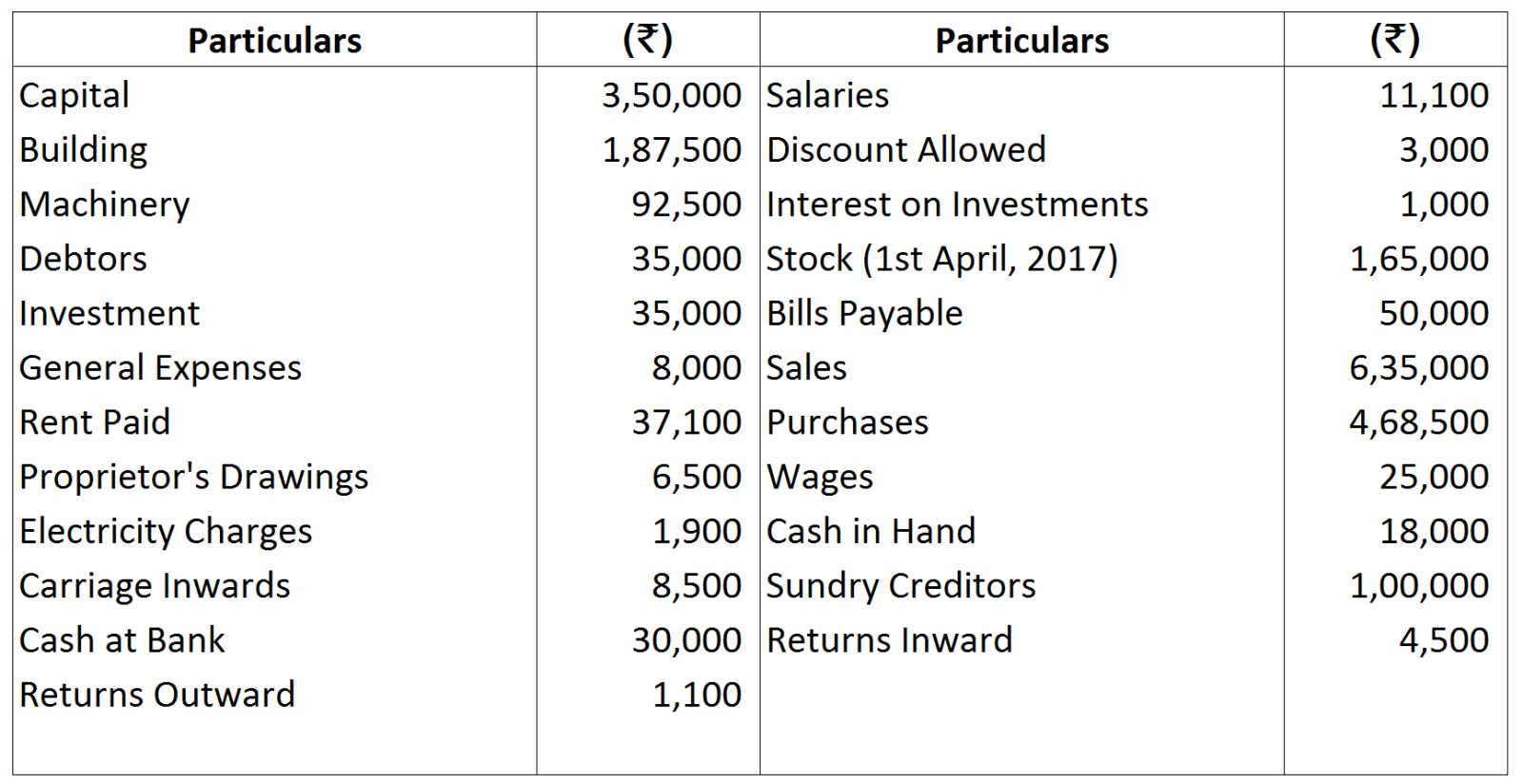

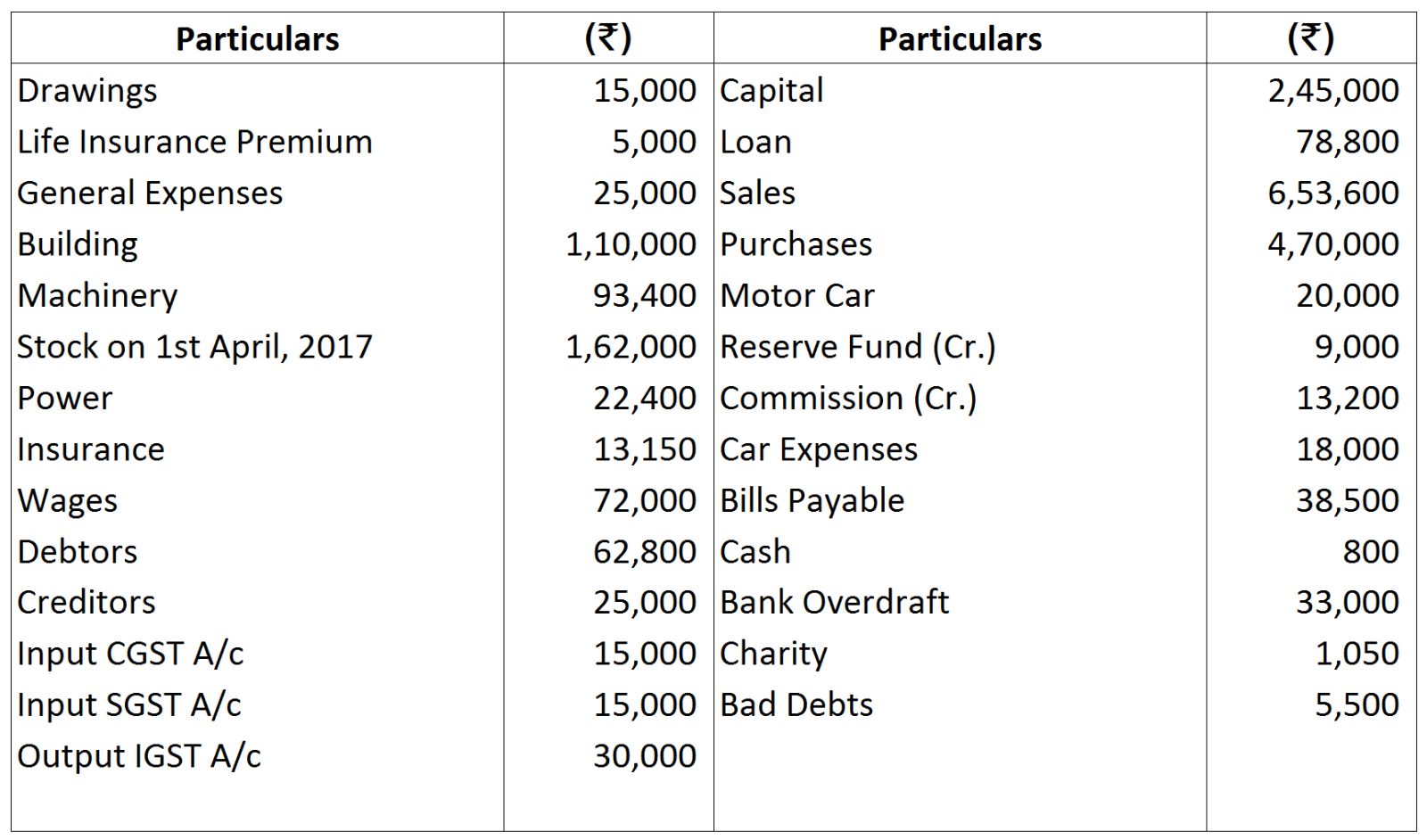

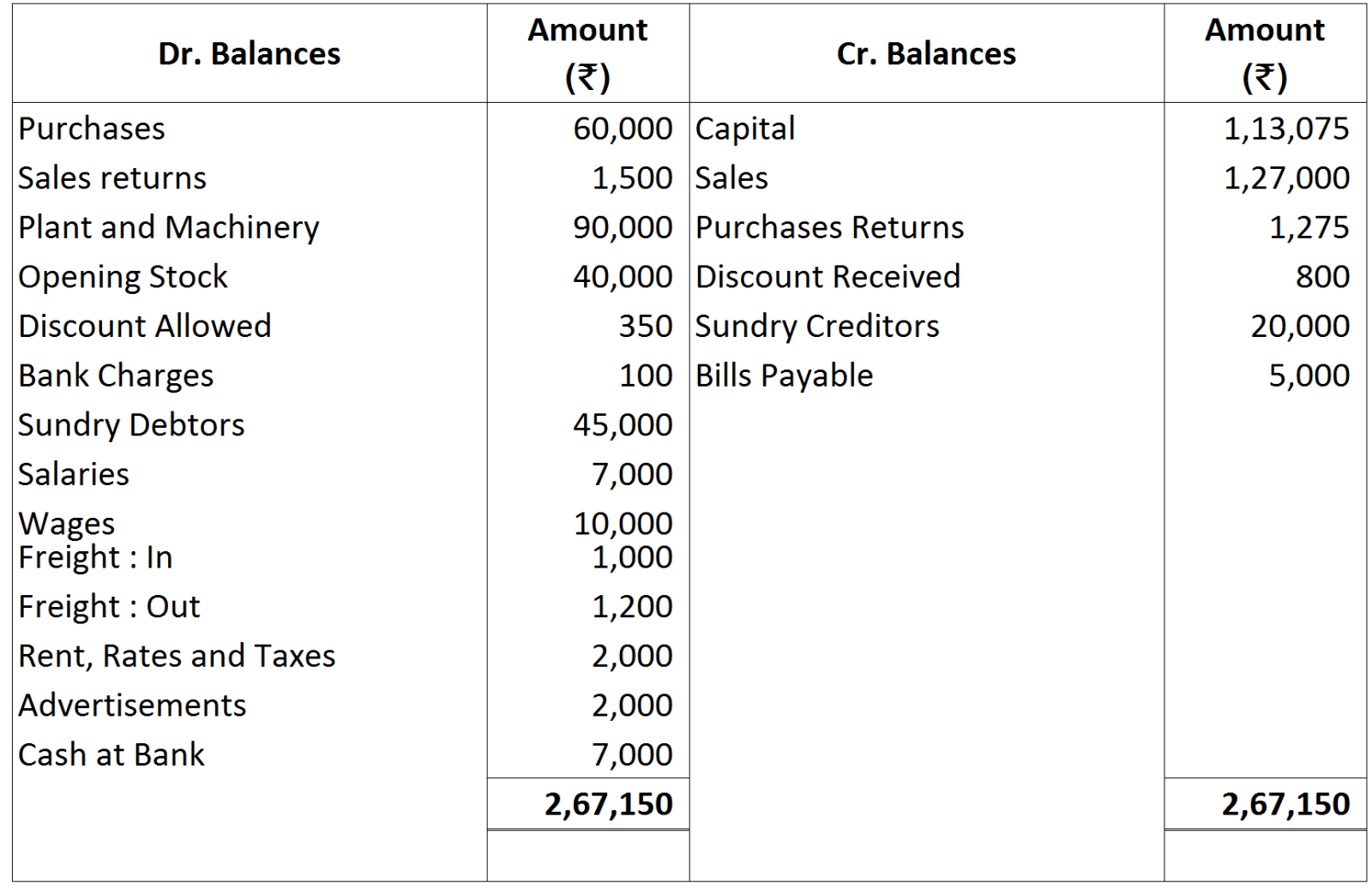

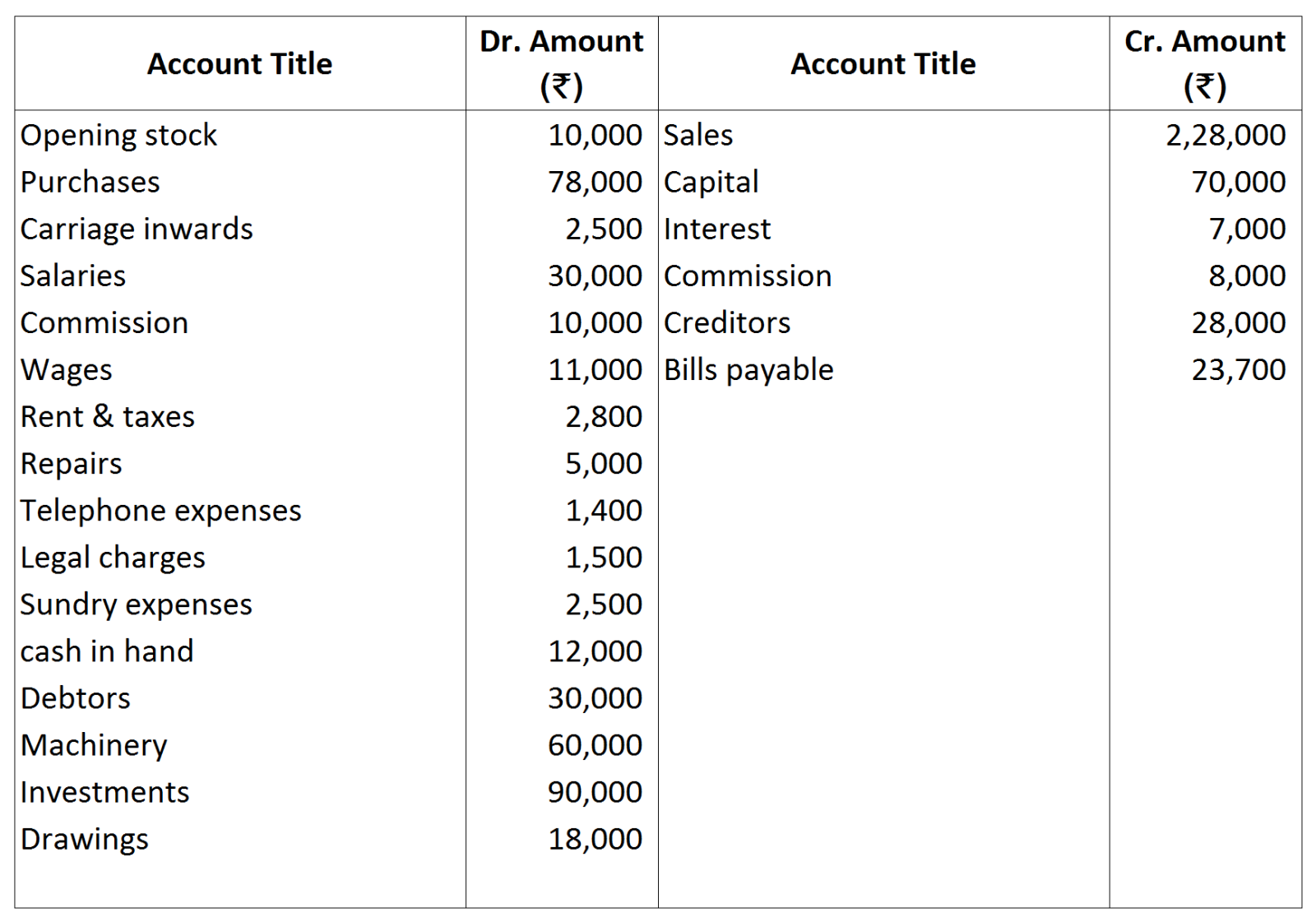

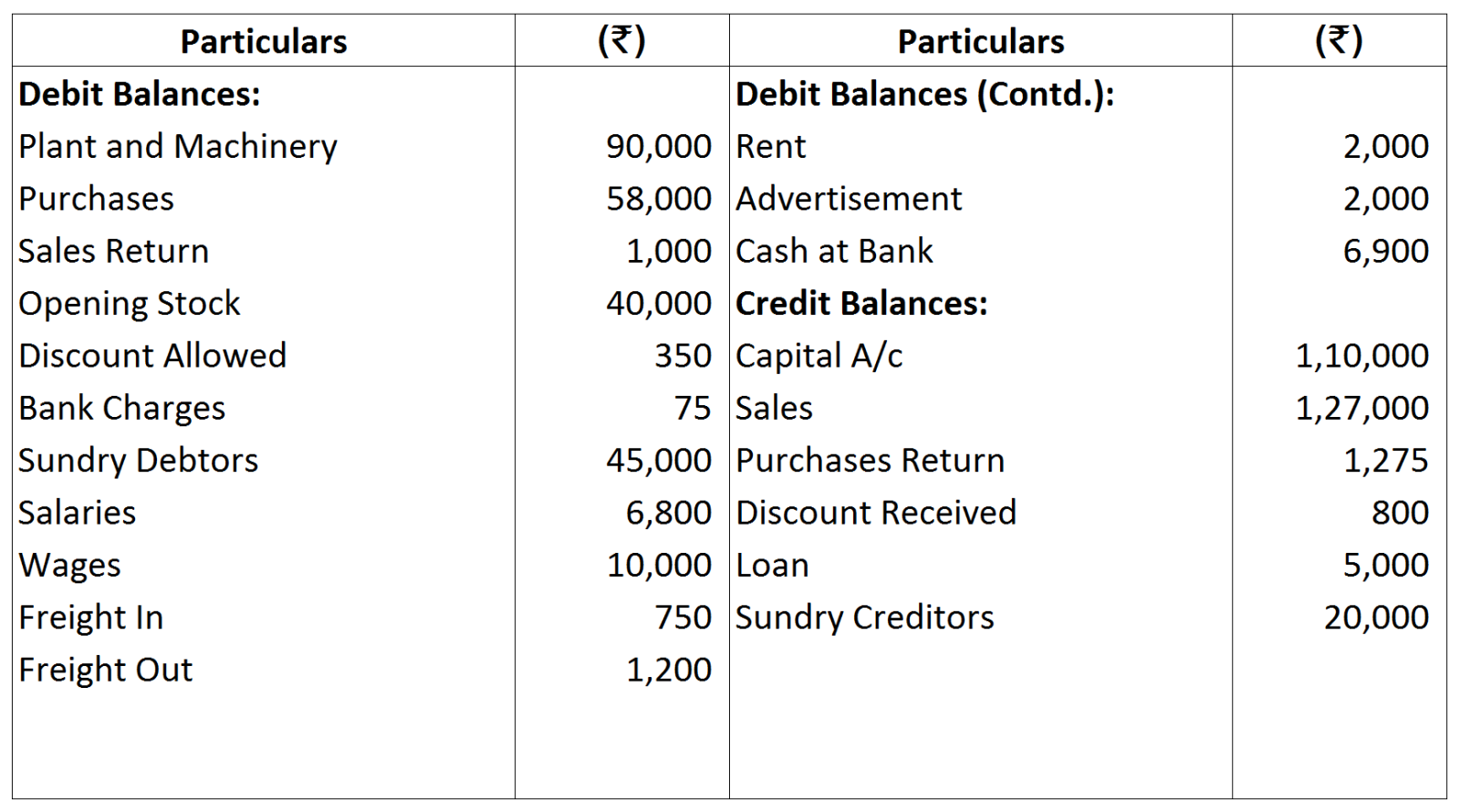

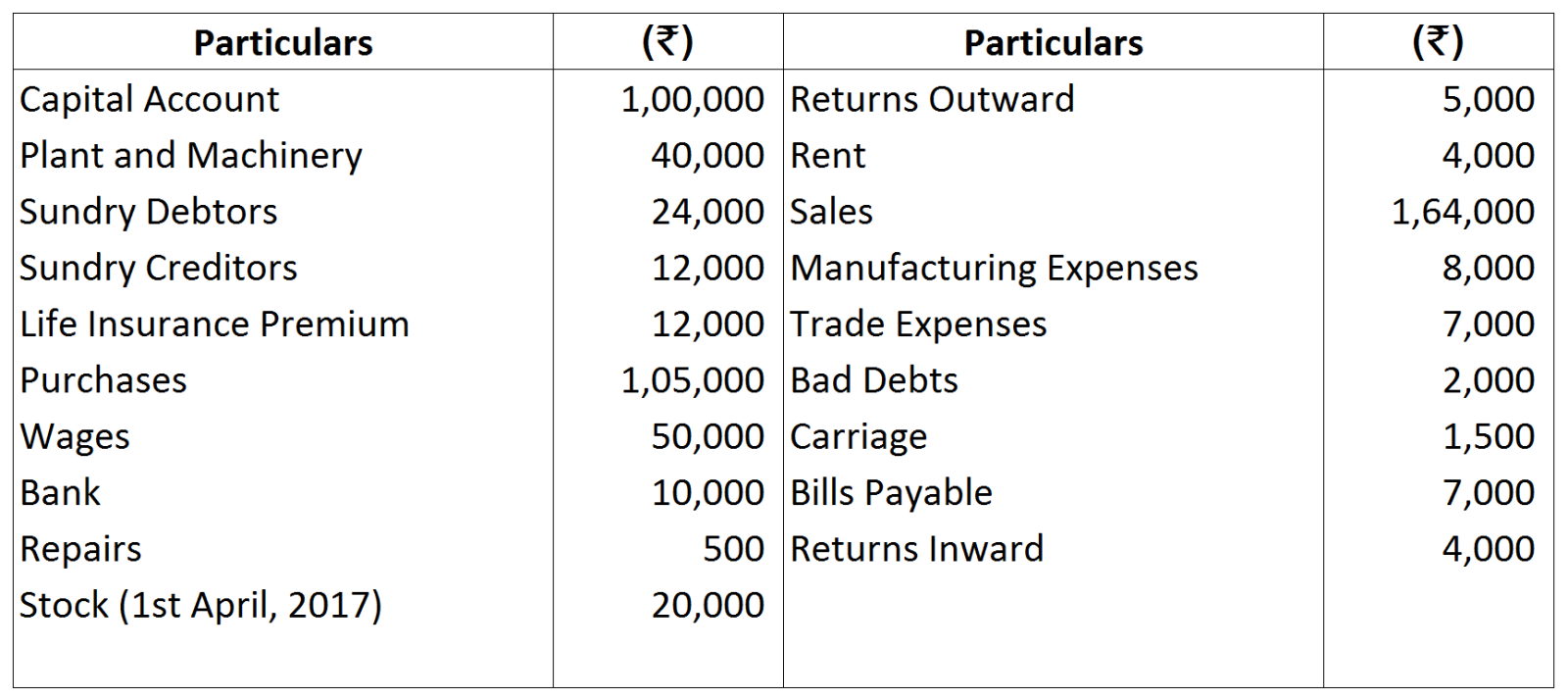

Working Note: Closing Stock was valued at ₹ 35,000. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2017 and Balance Sheet as at that date.

Closing Stock was valued at ₹ 35,000. Prepare Trading and Profit and Loss Account for the year ended 31st March, 2017 and Balance Sheet as at that date.

Working Notes:

Working Notes:

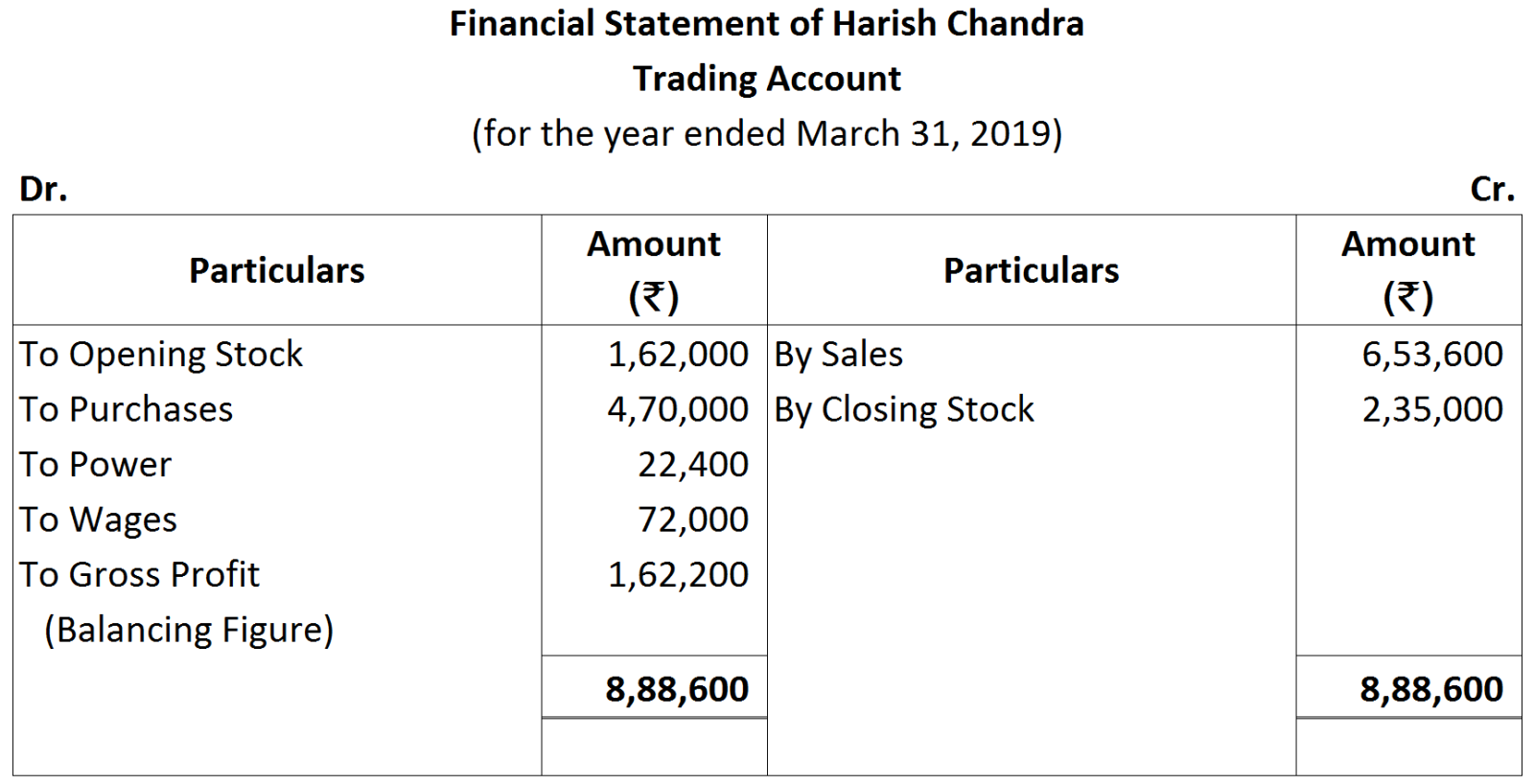

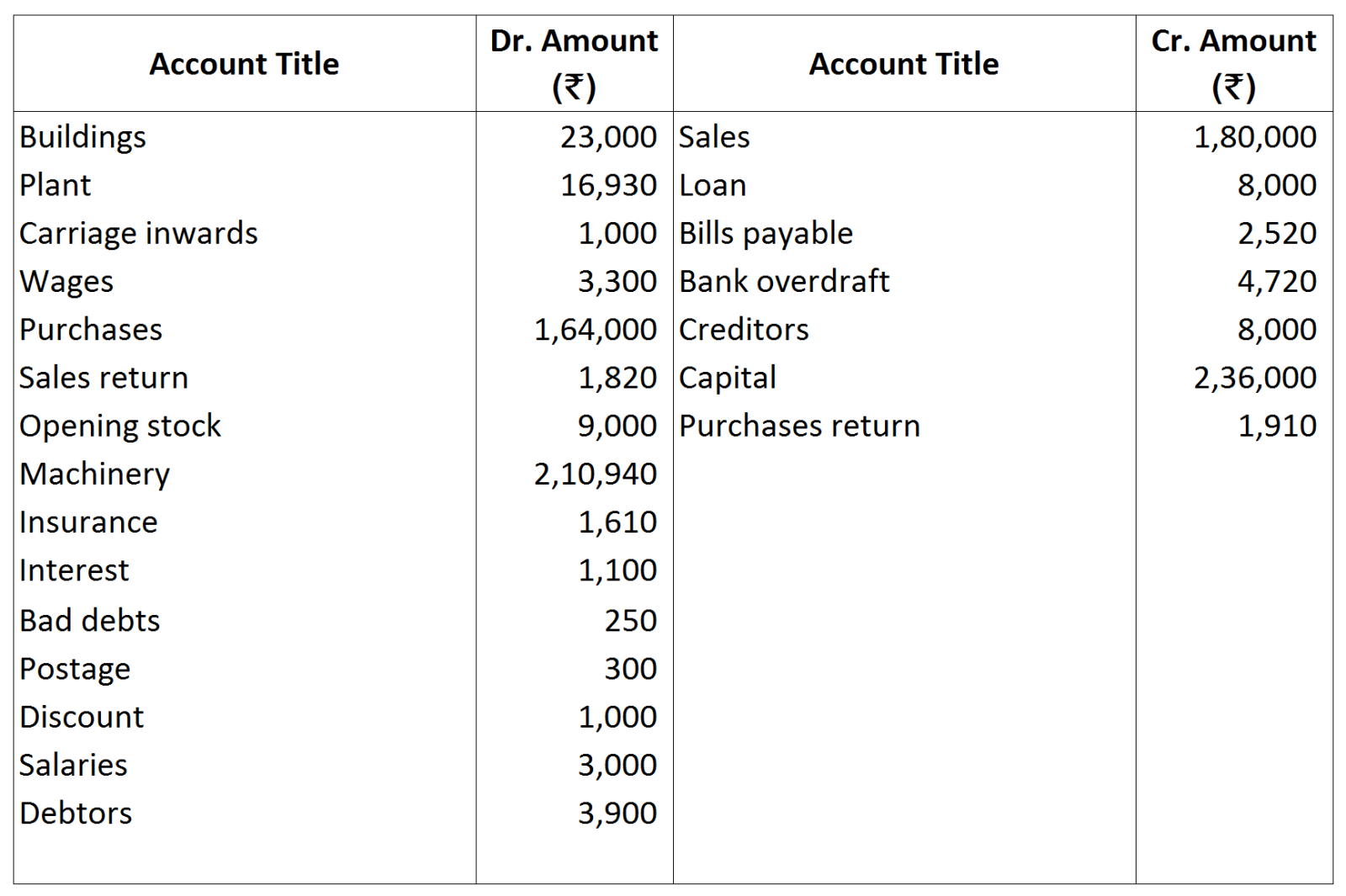

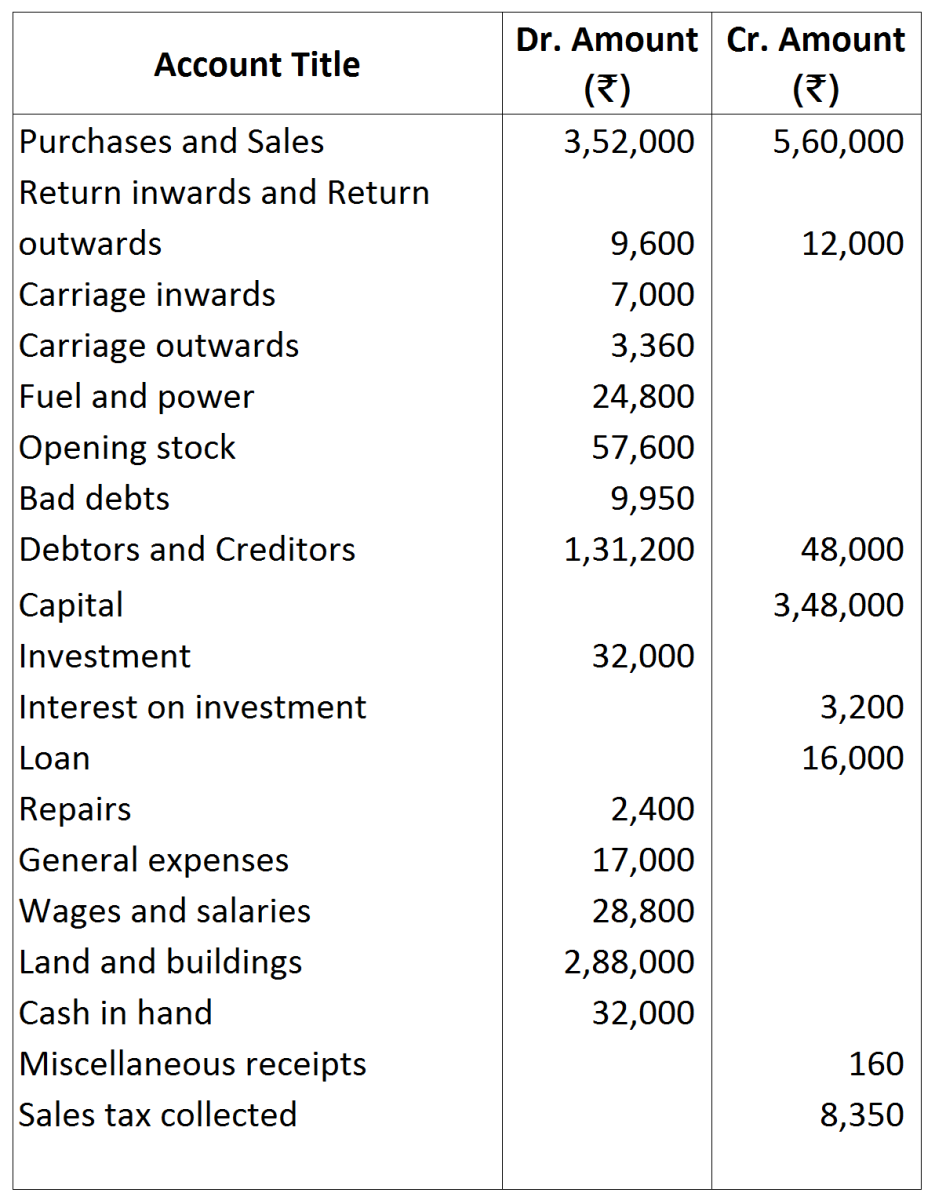

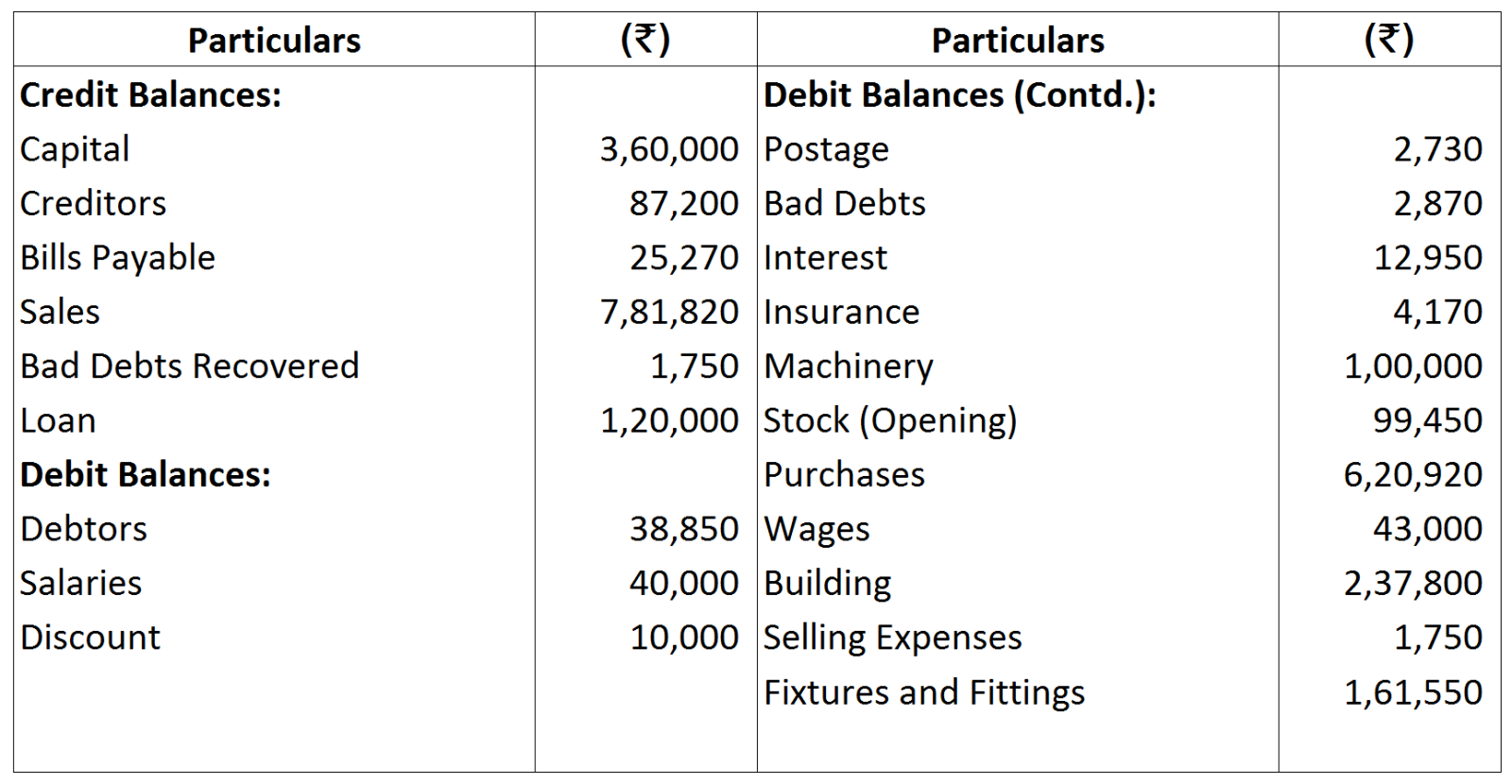

Value of Closing Stock was ₹ 36,500 on 31st March, 2017.

Value of Closing Stock was ₹ 36,500 on 31st March, 2017.

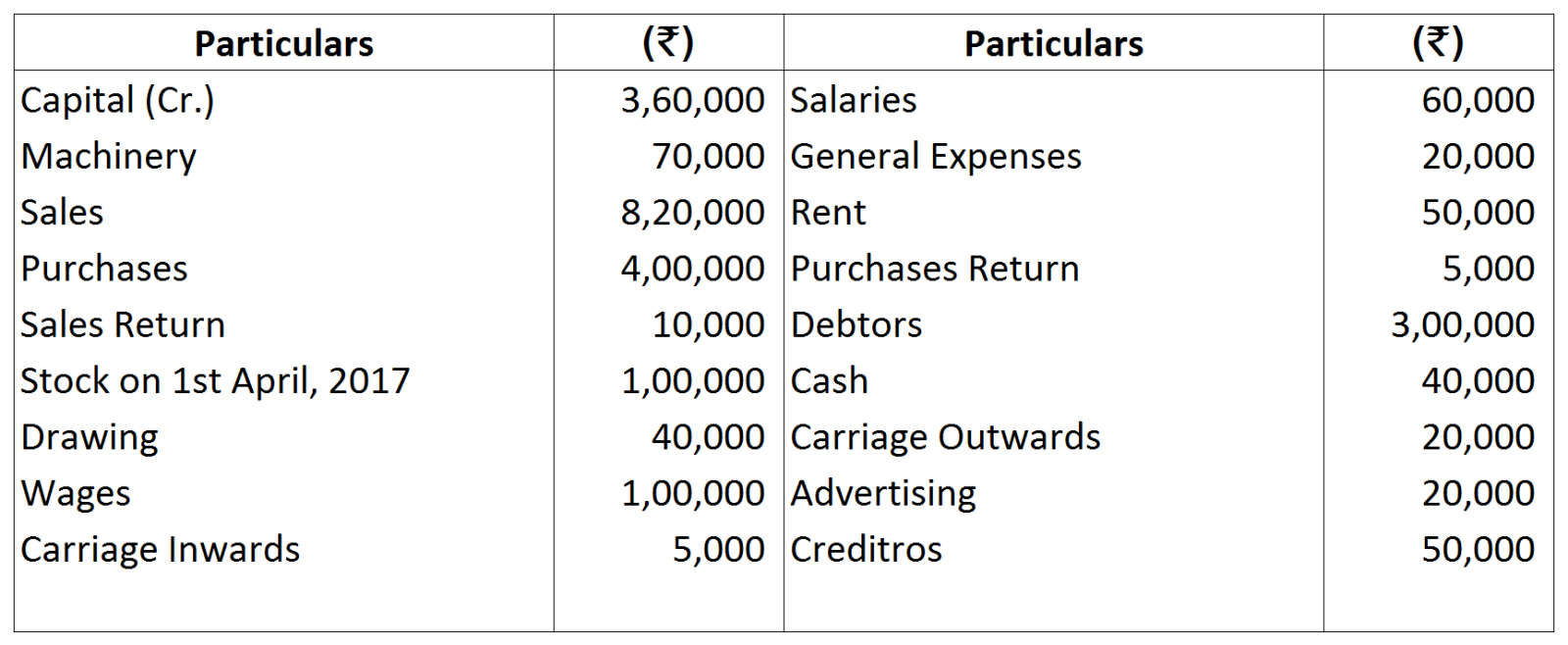

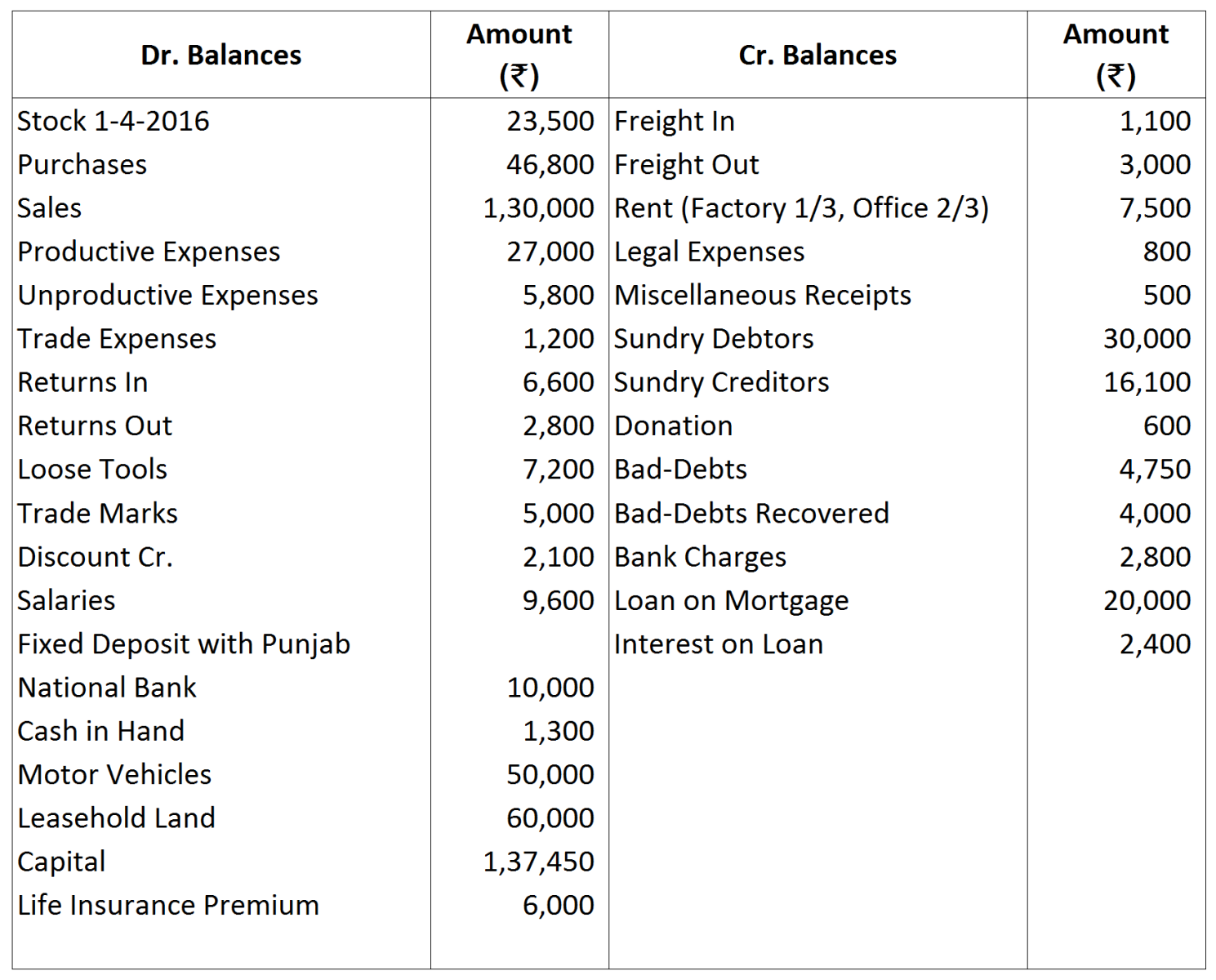

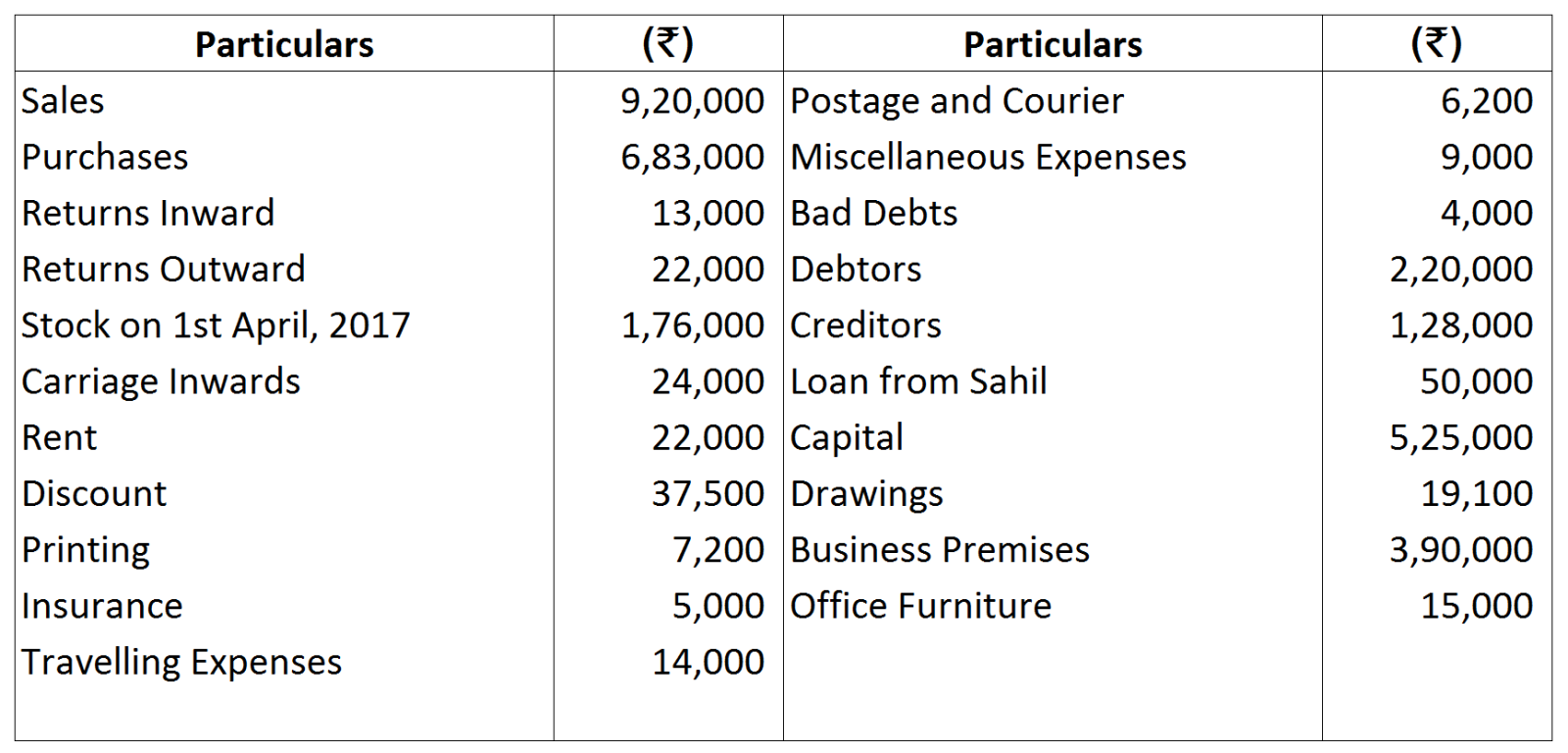

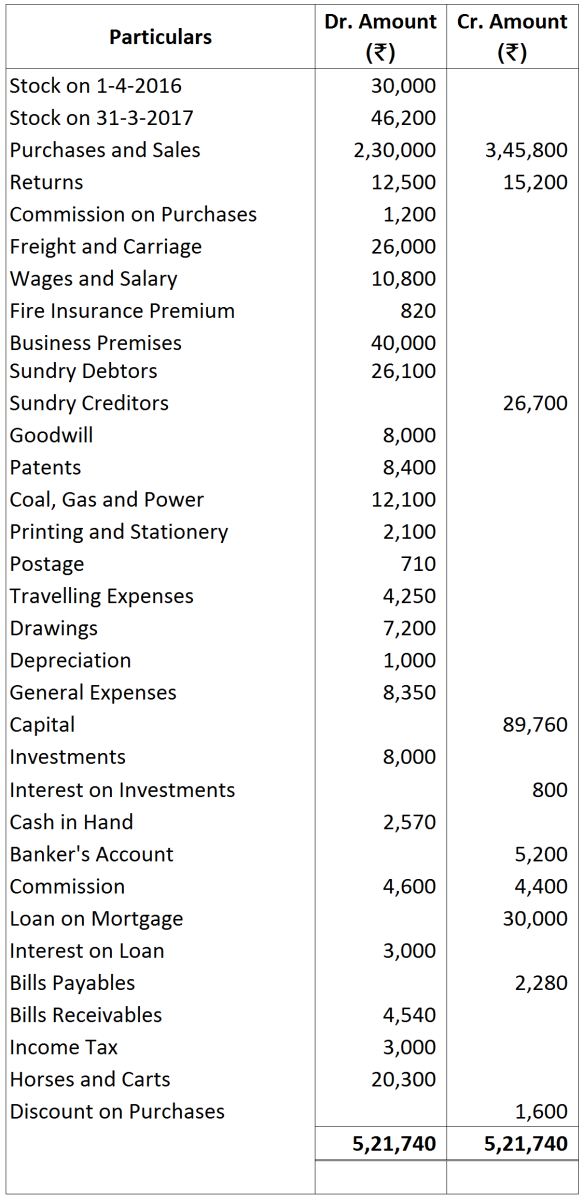

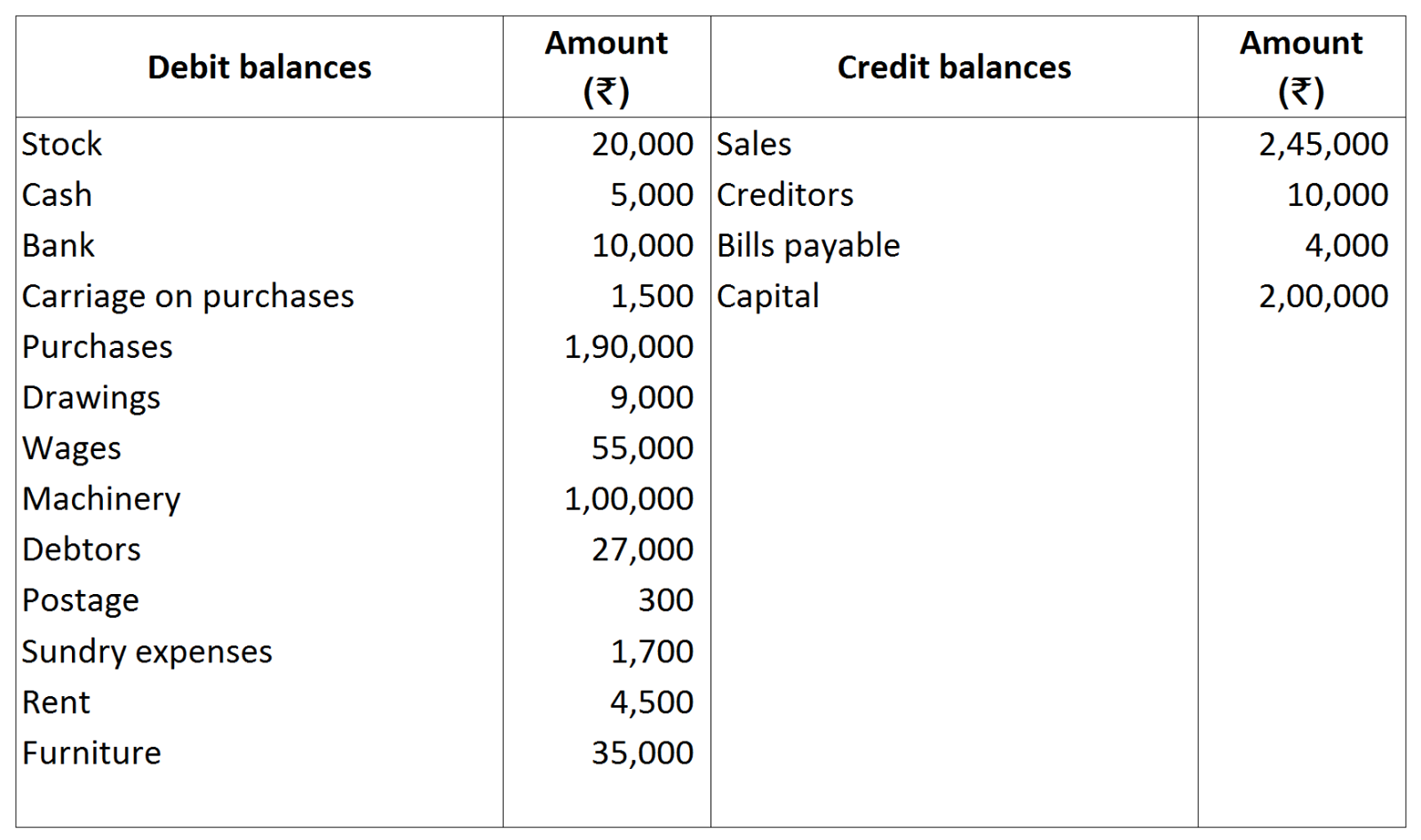

Prepare a Trading and Profit and Loss Account for the year ended on 31-3-2016 and the Balance Sheet as at that date. The Stock on 31st March, 2016 was ₹ 22,000.

Prepare a Trading and Profit and Loss Account for the year ended on 31-3-2016 and the Balance Sheet as at that date. The Stock on 31st March, 2016 was ₹ 22,000.

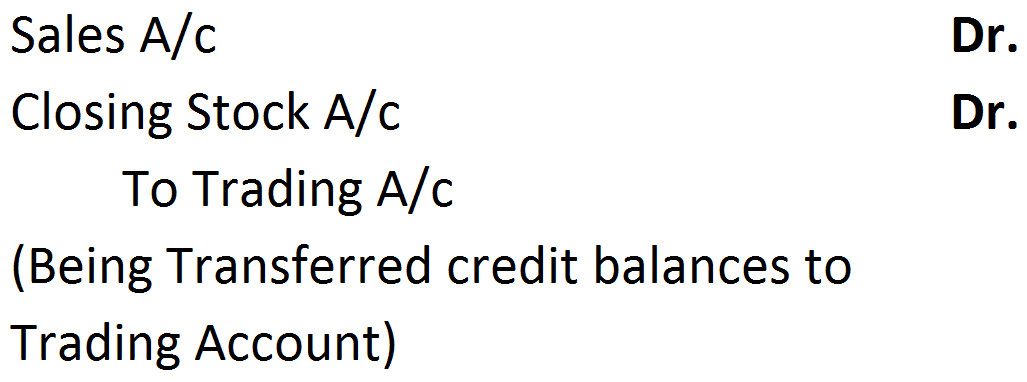

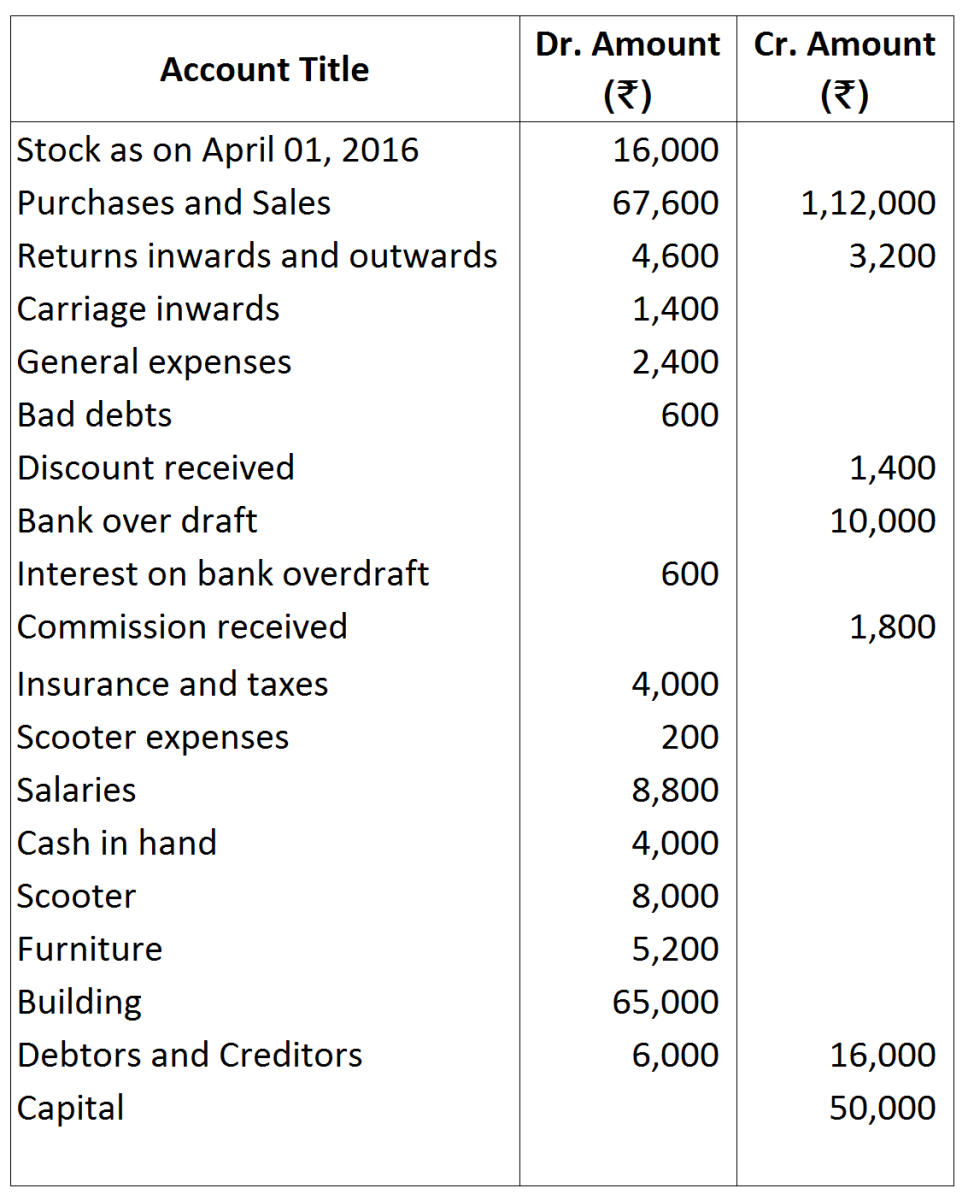

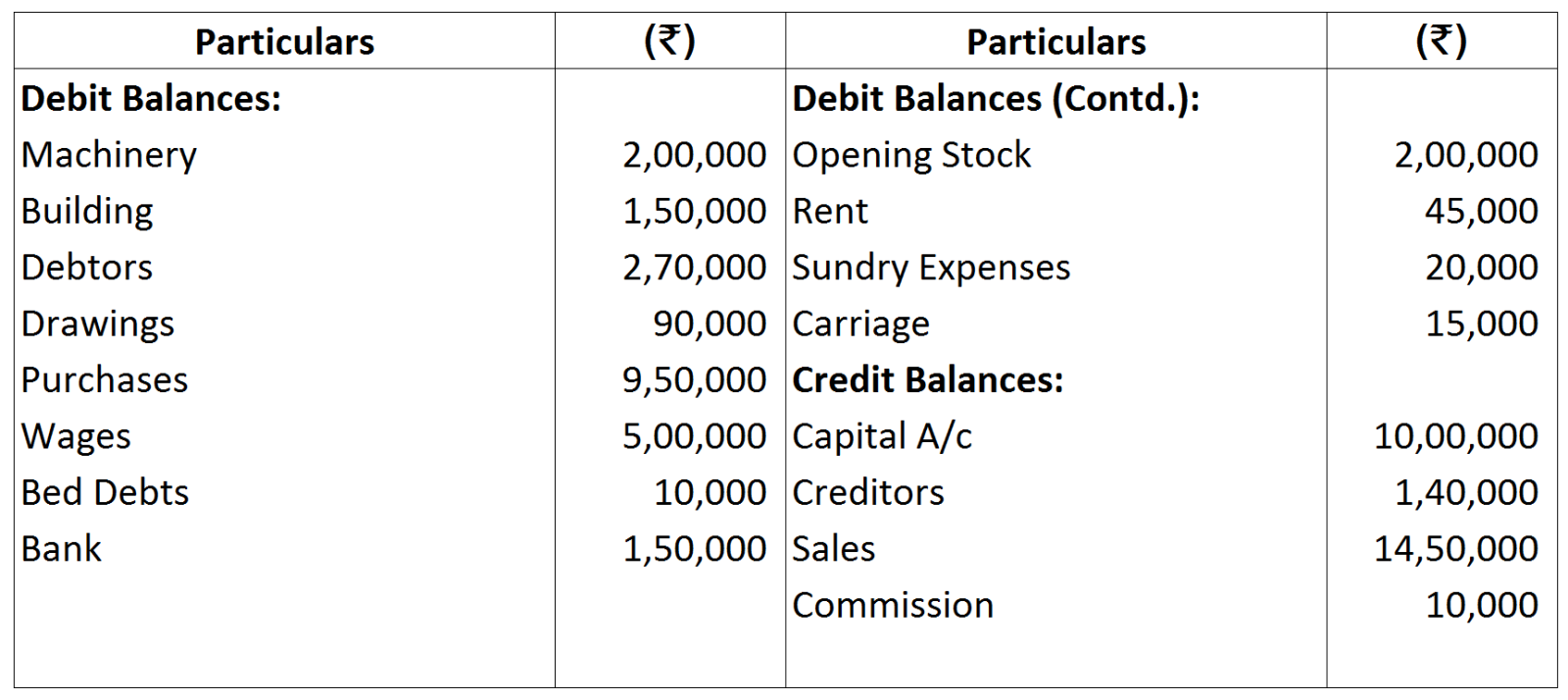

Note: Closing Stock is recorded at cost price or market price which is lower.

Note: Closing Stock is recorded at cost price or market price which is lower.