Production and cost — Economics STD 11 Commerce — Question

CBSE BoardEnglish MediumSTD 11 CommerceEconomicsProduction and cost6 Marks

Question

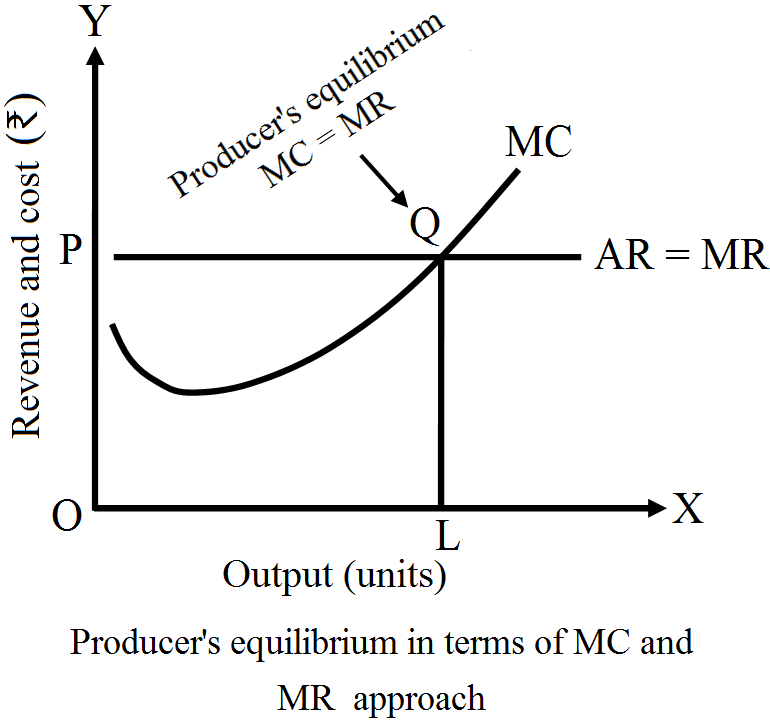

Explain producer's equilibrium with the help of a diagram.

✓

Answer

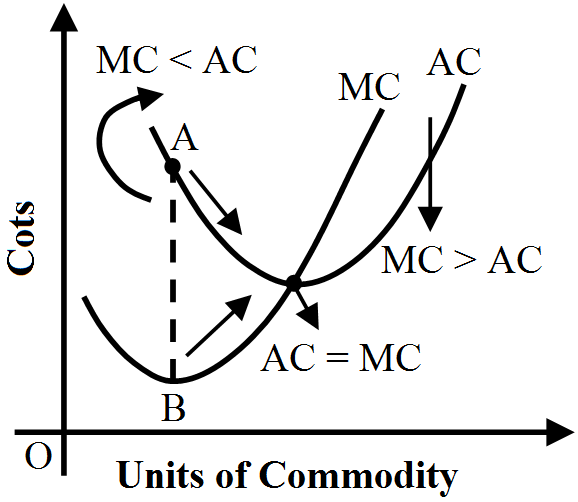

Producer's equilibrium refers to a situation of profit maximisation or cost minimisation. To study producer's equilibrium, two approaches are used

Total Revenue and Total Cost approach: Under this approach, a producer is deemed to be in equilibrium, on the fulfillment of the following two conditions

The difference between TR and TC is the maximum.

Total profits are falling after this level of output.

Marginal Revenue and Marginal Cost approach Under this approach, a producer attains equilibrium on the fulfillment of the following two conditions:

MR = MC

MC is rising after the point of equilibrium.

Need a full question paper?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.