Question

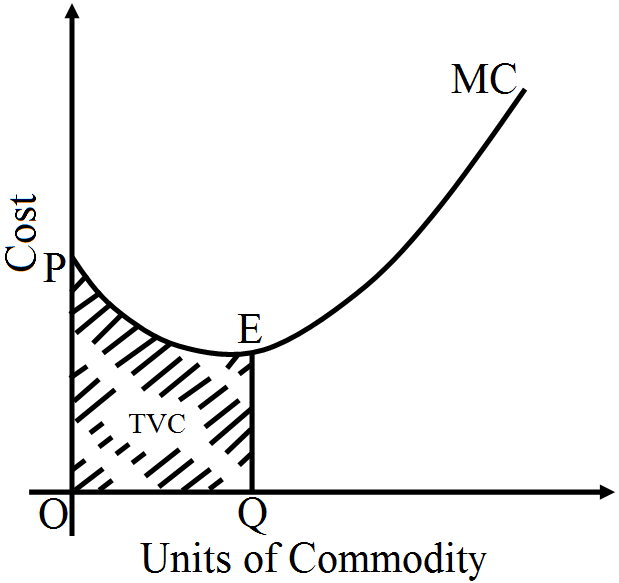

Explain that area under marginal bar cost (MC) is total variable cost (TVC).

|

Units of Commodity

|

MC

|

$\text{TVC}=\sum\text{MC}$

|

|

0

|

0

|

0

|

|

1

|

30

|

30

|

|

2

|

10

|

40

|

|

3

|

15

|

55

|

|

4

|

30

|

85

|

|

5

|

35

|

120

|

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| Units of Variable Input (Units) |

Total Physical Product |

| 1 | 10 |

| 2 | 22 |

| 3 | 30 |

| 4 | 35 |

| 5 | 30 |

|

Output(Units)

|

1

|

2

|

3

|

4

|

5

|

6

|

7

|

|

Price (Rs.)

|

24

|

24

|

24

|

24

|

24

|

24

|

24

|

|

Total Cost (Rs.)

|

26

|

50

|

72

|

92

|

115

|

139

|

165

|