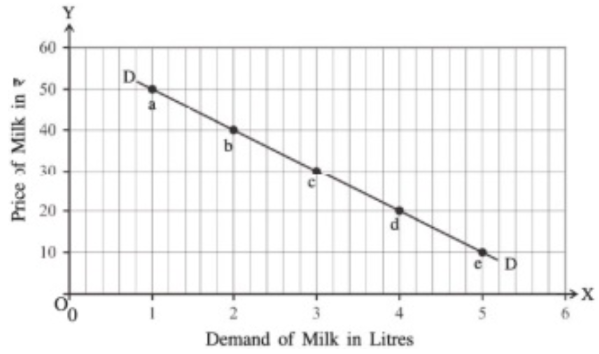

Answer the questions based on the figure provided below.

(1) What is the price when the demand for milk is 1 liter?

(2) What is the demand for milk when the price is 30 rupees?

(3) What is the relationship between the demand for milk and its price?

(4) If the price is increased from 50 rupees to 40 rupees, how much will the demand for milk change?

(5) If the demand for milk is reduced from 5 liters to 3 liters, how much will the price change?