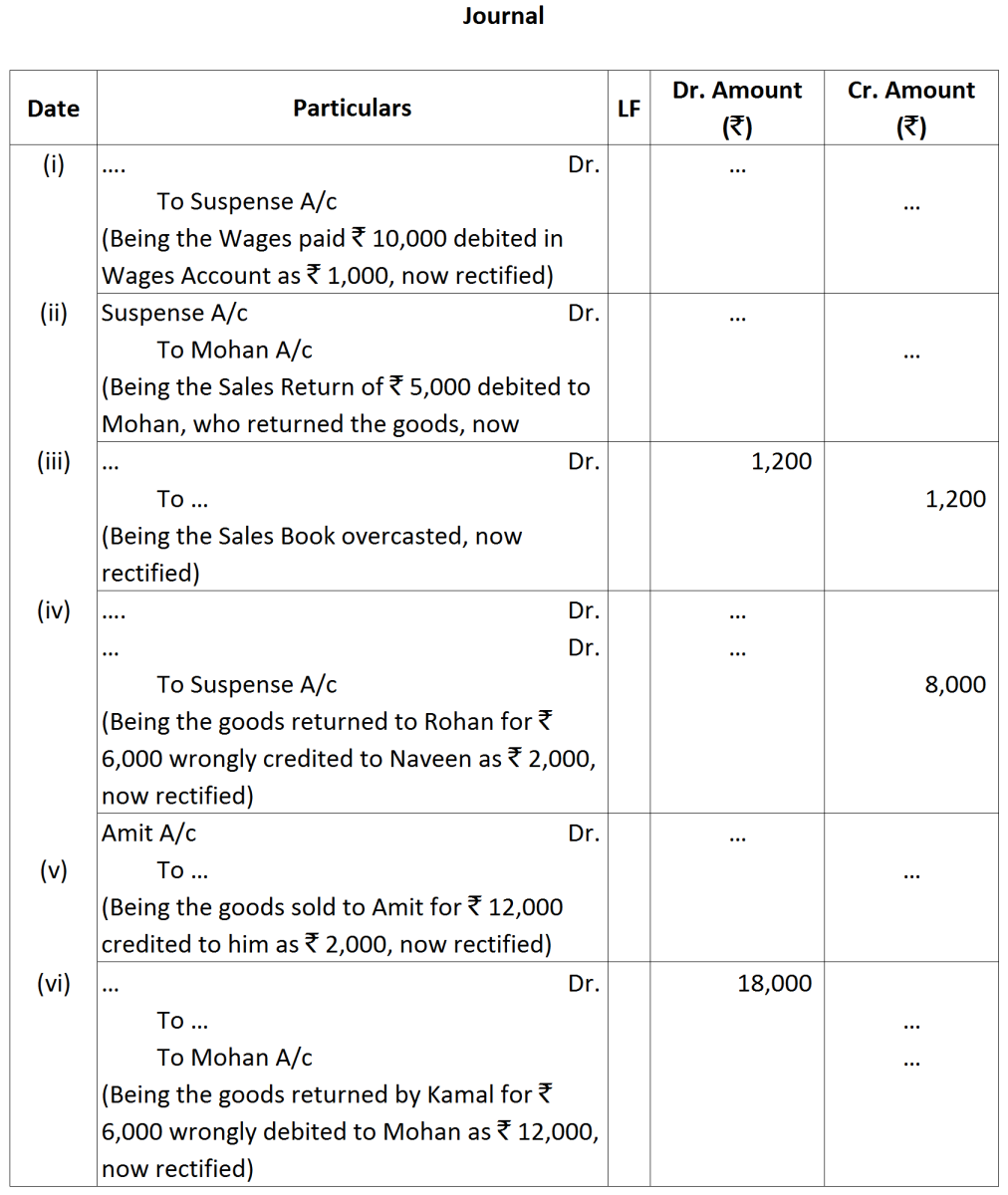

Question

Fill in the missing information in the following Rectifying Journal Entries:

Get the step-by-step solution for this question inside the Vidyadip app.

Get the answer in the appGenerate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

| April 01, 2016 | March 31, 2017 | |

| ₹ | ₹ | |

| Sundry creditors | 45,000 | 93,000 |

| Loan from wife | 66,000 | 57,000 |

| Sundry debtors | 22,500 | — |

| Land and Building | 89,600 | 90,000 |

| Cash in hand | 7,500 | 8,700 |

| Bank overdraft | 25,000 | — |

| Furniture | 1,300 | 1,300 |

| Stock | 34,000 | 25,000 |

|

|

|

₹

|

|

(i)

|

Bank balance as per Pass Book.

|

10,000

|

|

(ii)

|

Cheque deposited into the Bank, but no entry was passed in the Cash Book.

|

500

|

|

(iii)

|

Cheque received and entered in the Cash Book but not sent to bank.

|

1,200

|

|

(iv)

|

Credit side of the Cash Book bank column cast short.

|

200

|

|

(v)

|

Insurance premium paid directly by the bank under the standing advice.

|

600

|

|

(vi)

|

Bank charges entered twice in the Cash Book.

|

20

|

|

(vii)

|

Cheque issued but not presented to the bank for payment.

|

500

|

|

(viii)

|

Cheque received entered twice in the Cash Book.

|

1,000

|

|

(ix)

|

Bill discounted dishonoured not recorded in the Cash Book.

|

5,000

|

|

(x)

|

Bank had wrongly allowed interest of ₹ 5,000, which was reversed by it on 5th April, 2019

|

| 2019 | ₹ | |||

| April 1 | Opening Balance of Cash in Hand | 1,00,000 | ||

| Opening Balance of Bank Overdraft | 5,00,000 | |||

| April 2 | Sold goods for cash, including CGST and SGST @ 6% each | 4,48,000 | ||

| April 3 | Sold goods including CGST and SGST @ 6% each against cheque and paid into bank the same day | 3,36,000 | ||

| April 5 | Sold goods to Reema, including IGST @ 12% | 1,12,000 | ||

| April 6 | Ram paid by cheque | 78,000 | ||

| Discount allowed | 2,000 | |||

| April 7 | Bought goods from Rahul, Gurugram for ₹ 40,000 plus CGST and SGST @ 6% each and paid him by cheque | 44,800 | ||

| Salary paid to staff by cheque | 2,20,000 | |||

| April 10 | Deposited into bank | 3,10,000 | ||

| April 11 | Received a cheque from Suresh and paid into bank | 1,28,500 | ||

| Discount allowed | 1,500 | |||

| April 15 | Received from R. Kumar a cheque for a full settlement of his account for ₹ 1,95,000 | 1,87,500 | ||

| April 18 | Paid wages in cash | 30,000 | ||

| April 20 | Bank charges, including CGST and SGST @ 6% each | 5,600 | ||

| April 22 | Withdrew from bank for office use | 1,00,000 | ||

| Withdrew from Bank for personal use | 1,20,000 | |||

| April 25 | Paid electricity bill by cheque | 31,500 | ||

| Issued a cheque in favour of Sudha as advance for purchase of house of Gaurav | 2,00,000 | |||

| April 26 | Received a cheque from Amar | 58,200 | ||

| Allowed discount to him | 1,800 | |||

| April 28 | Cheque received from Amar sent to bank | |||

| April 30 | Bank collected interest received on investments | 15,000 | ||

| Paid rent for the month of May, 2019, including CGST and SGST @ 6% each | 22,400 | |||

|

|

|

₹

|

|

(i)

|

Bank overdraft as per the Cash Book.

|

80,000

|

|

(ii)

|

Cheques deposited as per the bank statement but not entered in the Cash Book.

|

3,000

|

|

(iii)

|

Cheques recorded for collection but not sent to the bank.

|

10,000

|

|

(iv)

|

Credit side of bank column casted short.

|

1,000

|

|

(v)

|

Bank charges recorded twice in the Cash Book.

|

100

|

|

(vi)

|

Customer's cheque returned as per the Bank Statement.

|

4,000

|

|

(vii)

|

Cheques issued but dishonoured on technical grounds.

|

3,000

|

|

(viii)

|

Bills collected by bank directly.

|

20,000

|

|

(ix)

|

Cheque received entered twice in the Cash Book.

|

5,000

|