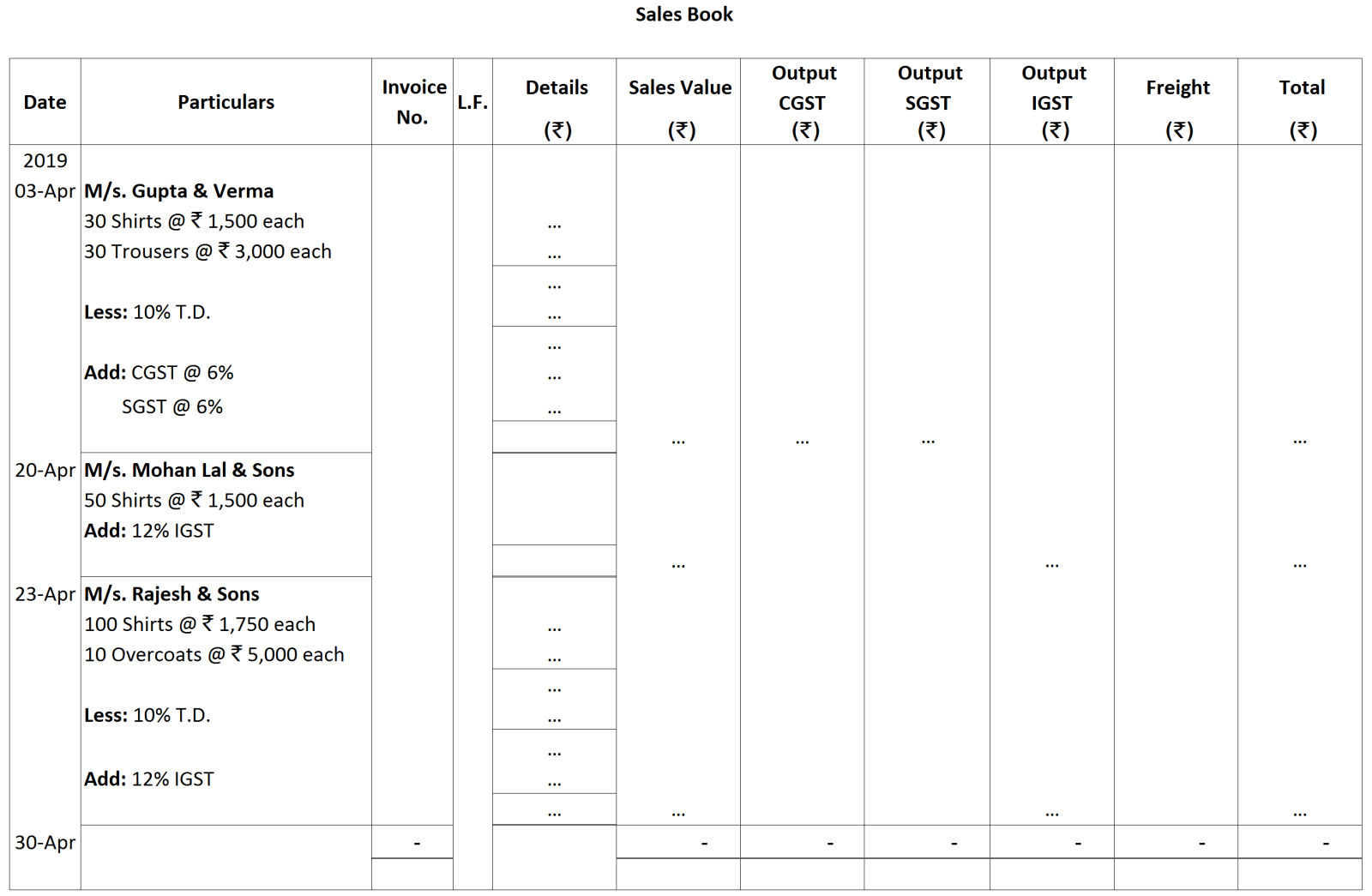

Question

In the following Sales Book, determine the missing information:

Get the step-by-step solution for this question inside the Vidyadip app.

Get the answer in the appGenerate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

2018

|

|

₹

|

|

October 1

|

Purchased goods from Anil for Cash |

40,000

|

| October 3 | Purchased goods from Atul |

75,000

|

|

October 6

|

Returned goods to Atul |

3,000

|

| October 8 | Paid cash to Atul |

50,000

|

| October 10 | Sold goods to Charu |

1,00,000

|

| October 12 | Charu returned 20% of goods |

|

| October 15 | Paid rent |

2,000

|

| October 20 | Sahil withdrew for personal use |

10,000

|

|

2017

|

|

(₹)

|

|

Jan. 1

|

Cash in hand

|

6,000

|

|

Bank Balance (Cr)

|

3,000

|

|

|

Jan. 3

|

Deposited into Bank

|

2,000

|

|

Jan. 5

|

Received from Mohan

|

400

|

|

Discount allowed

|

10

|

|

|

Jan. 7

|

Received a cheque from Hari and sent it to bank

|

600

|

|

Jan. 9

|

Received a cheque from Prem Mohan

|

1,600

|

|

Discount allowed

|

25

|

|

|

Jan. 12

|

Withdrew from bank for office use

|

300

|

|

Jan. 13

|

Bought goods for cash

|

600

|

|

Jan. 14

|

Sold goods for cash

|

1,200

|

|

Jan. 16

|

Paid to Ganesh by cheque

|

494

|

|

Discount received

|

6

|

|

|

Jan. 18

|

Prem Mohan's cheque deposited in the bank

|

|

|

Jan. 20

|

Sold goods to Gopal for ₹ 1,500 for which he gave cash ₹ 800 and a cheque of ₹ 700

|

|

|

Jan. 22

|

Deposited into bank (including Gopal's cheque)

|

900

|

|

Jan. 24

|

Paid rent by cheque

|

150

|

|

Jan. 25

|

Withdrew from bank for personal use

|

200

|

|

Jan. 28

|

Bank notifies that Prem Mohan's cheque was dishonoured

|

|

|

Jan. 30

|

Received from Anil ₹ 270 in cash and ₹ 540 by cheque

|

|

|

Discount Allowed ₹ 90

|

|

|

|

The cheque was deposited into bank.

|

|

|

|

Jan. 31

|

Bank charges as shown in Pass Book

|

5

|

|

Paid Salary

|

500

|

|

2019

|

|

₹

|

|

April 1

|

Suresh paid into bank as Capital*

|

60,000

|

|

April 2

|

He bought goods and paid by cheque

|

24,000

|

|

April 3

|

Sold goods to Mukand & Co., Delhi

|

6,700

|

|

April 4

|

Sold goods for cash

|

10,900

|

|

April 5

|

Paid sundry expenses in cash*

|

3,000

|

|

April 8

|

Paid for office furniture and fittings by cheque

|

4,000

|

|

April 9

|

Bought goods from Ramesh & Bros., Faridabad (Haryana)

|

10,600

|

|

April 11

|

Returned goods to Ramesh & Bros.

|

1,500

|

|

April 12

|

Issued cheque to Ramesh & Bros. in full settlement*

|

9,500

|

|

April 30

|

Bank charged interest*

|

200

|

|

April 30

|

Borrowed from Ridhi @ 10% per annum interest*

|

50,000

|

|

April 30

|

Received from Mahendra on account*

|

6,000

|

|

April 30

|

Sold household furniture and paid the amount into business*

|

2,000

|

|

April 30

|

Sold goods costing ₹ 5,000 to Anita for cash at a profit of 20% on cost, less 20% trade discount

|

|

|

April 30

|

Sold goods costing ₹ 20,000 to Sunil at a profit of 20% on sale less 20% Trade Discount and paid cartage ₹ 150 (to be charged from customer).

|