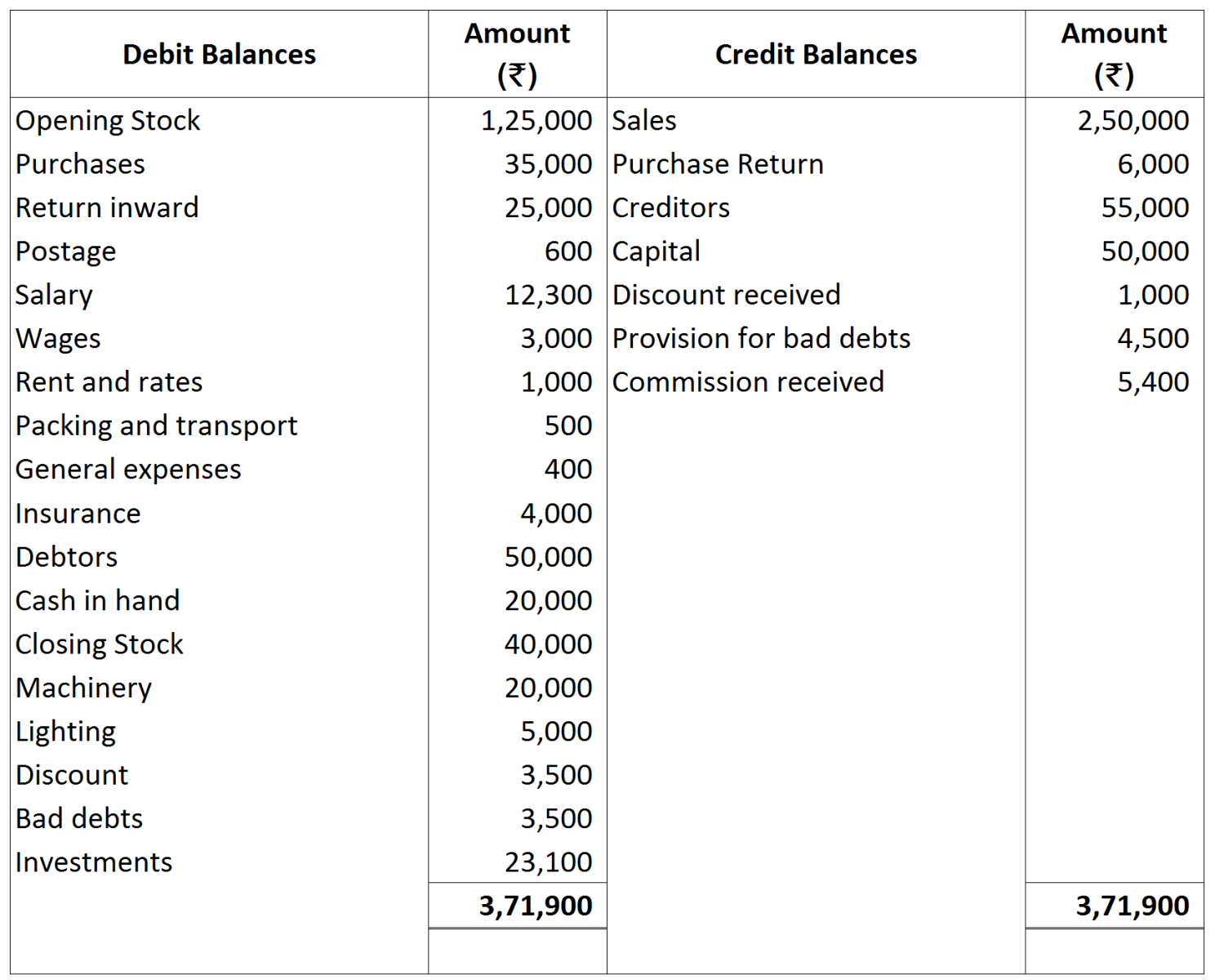

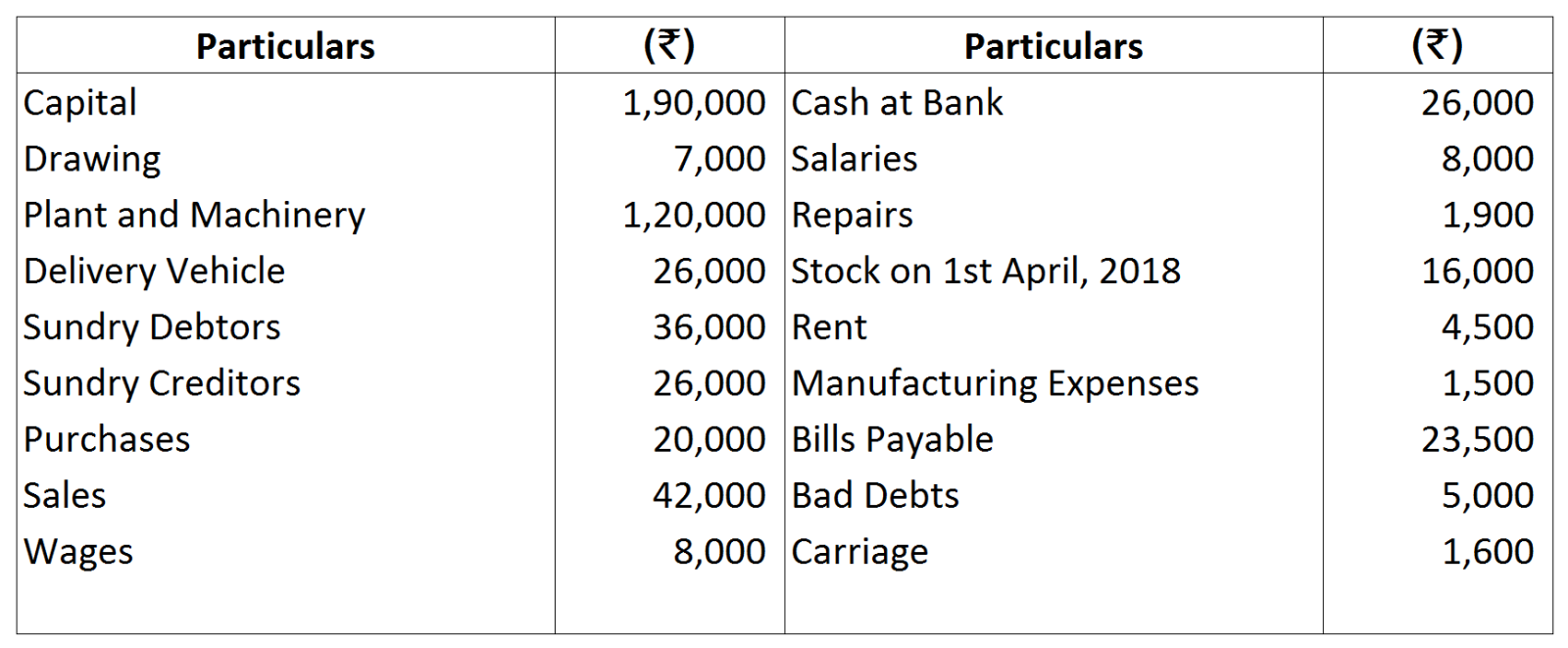

Question

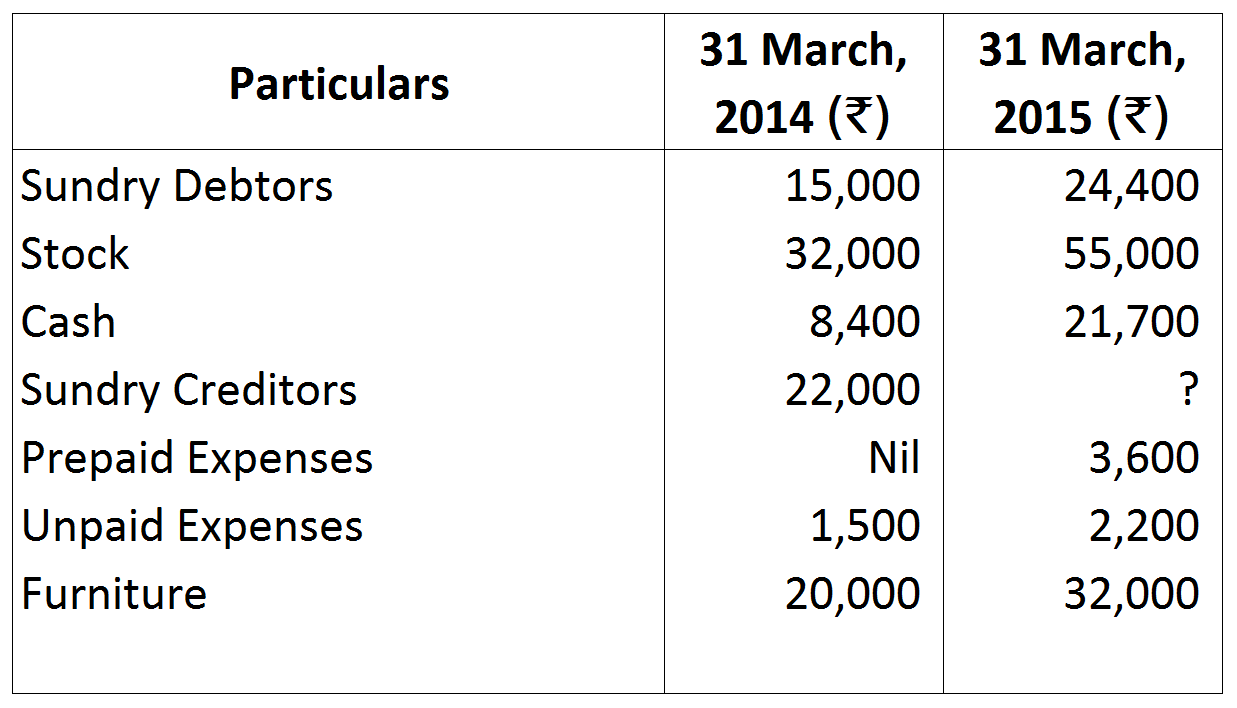

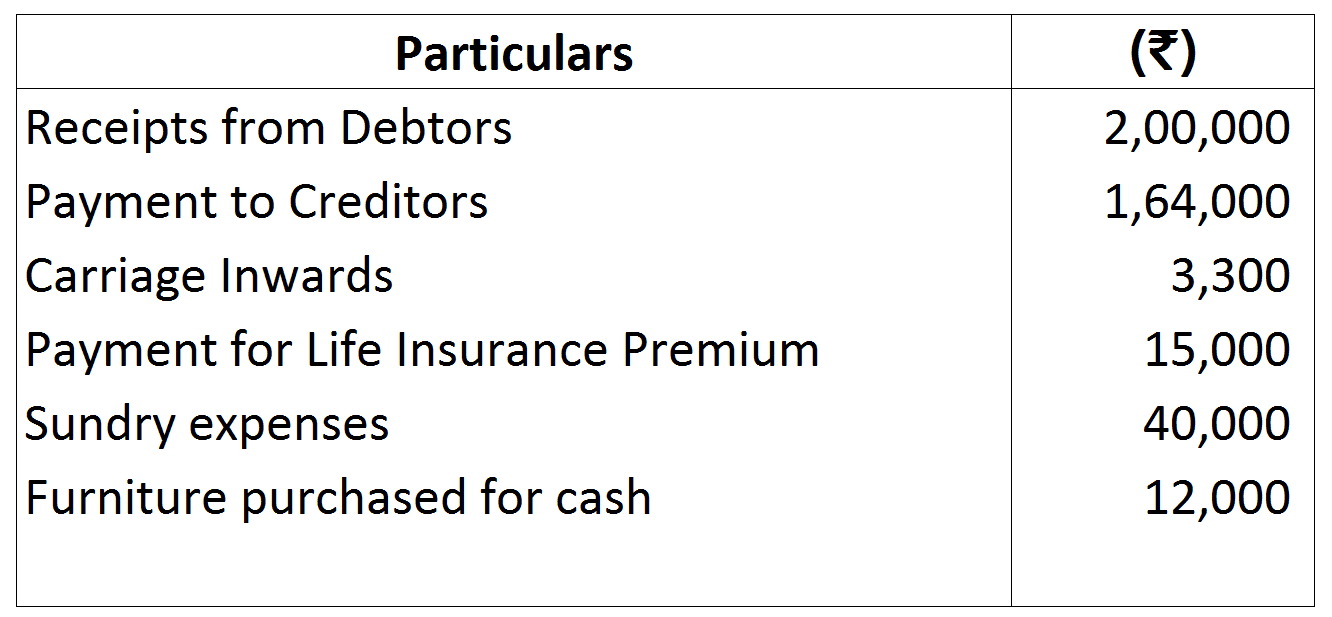

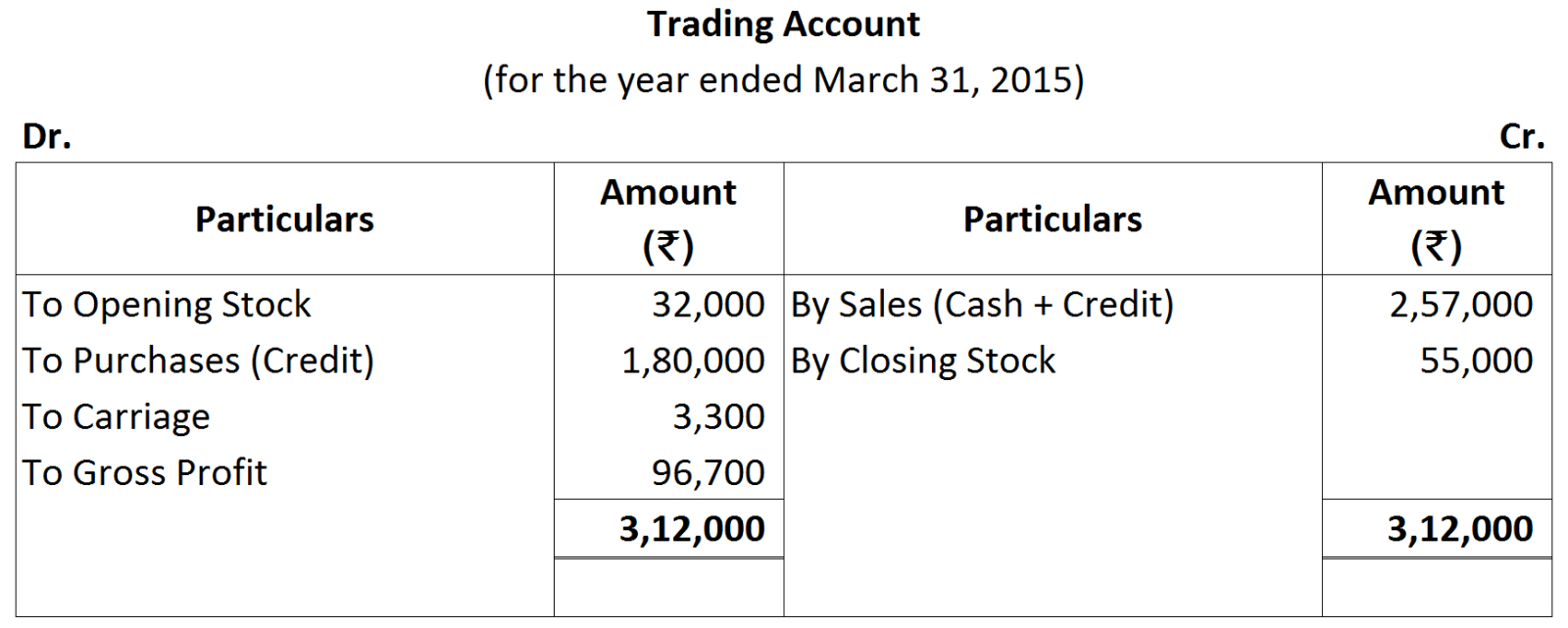

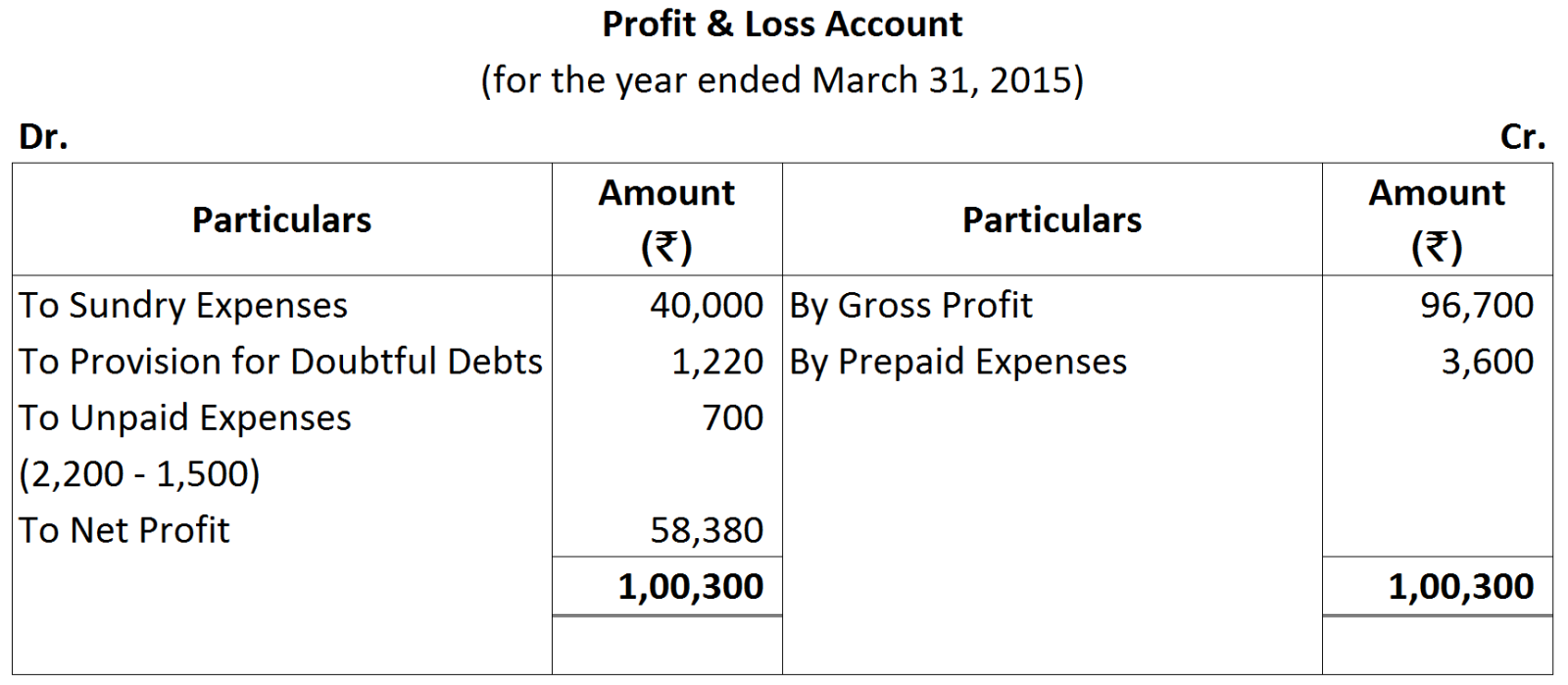

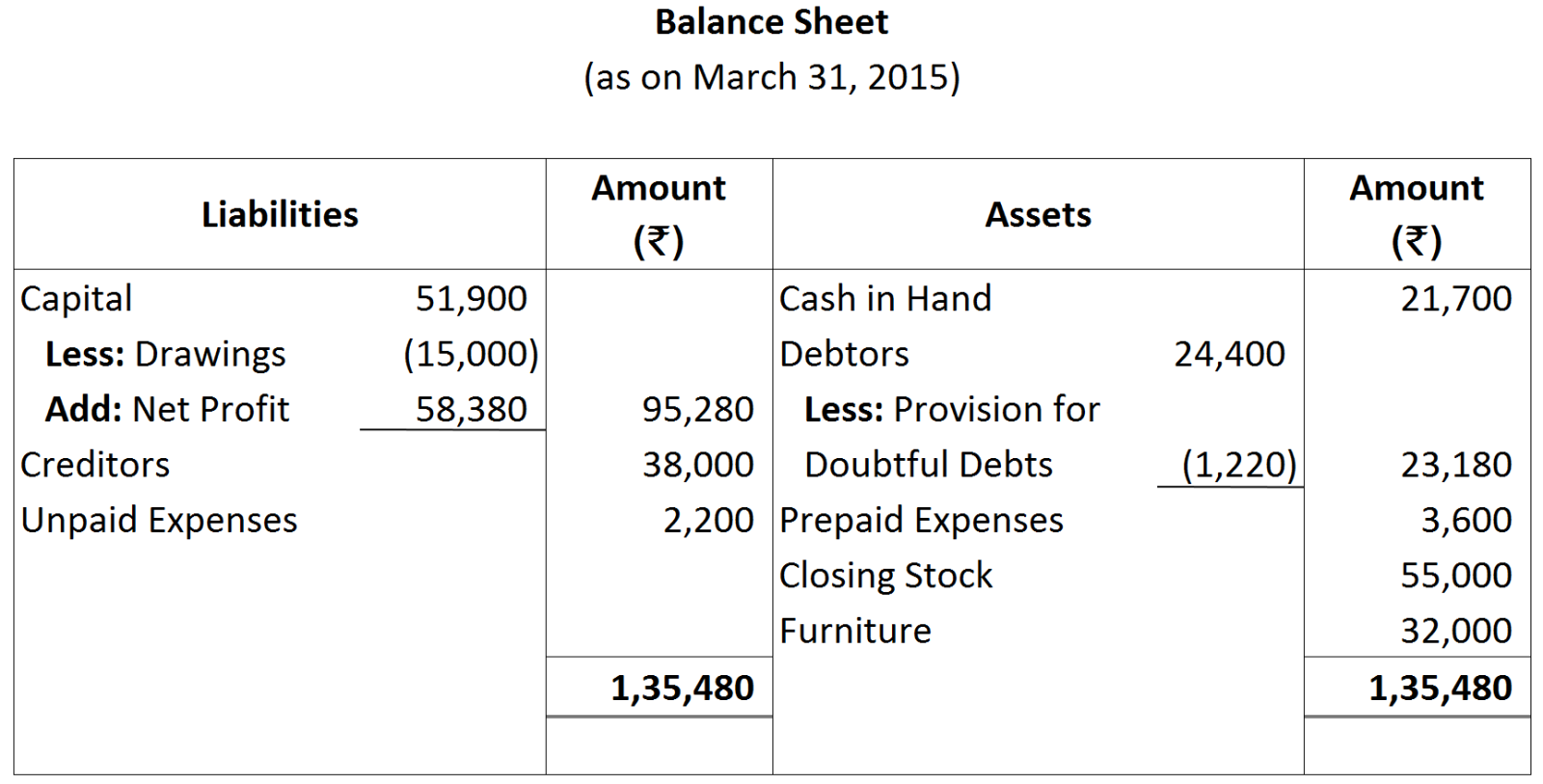

Lalit Mohan keeps incomplete records. From the following information provided by him, prepare a Trading and Profit & Loss Account for the year ended $31^{st}$ March, $2015$ and a Balance Sheet as at that date:

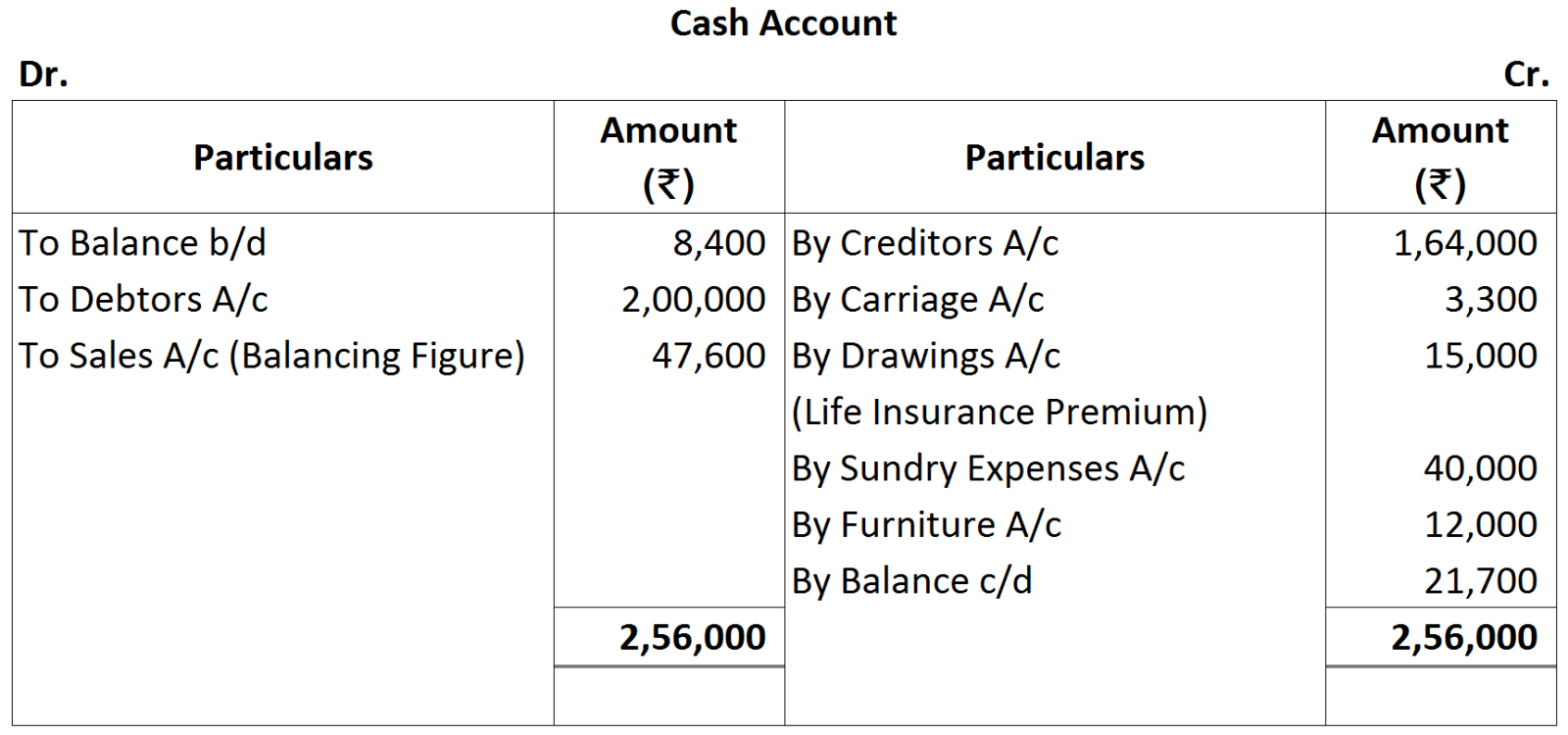

Summary of cash transactions during the year:

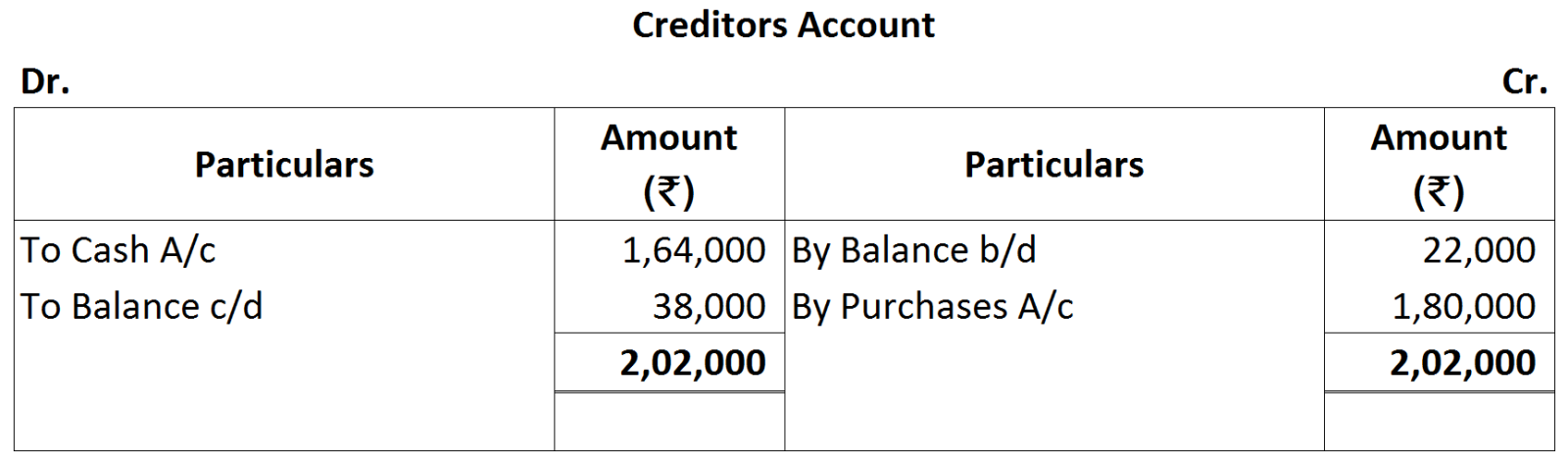

You are informed that there were considerable amount of cash sales during the year. Credit purchases during the year amounted to ₹ $1,80,000$. Provide $5\%$ for doubtful debts on debtors.

Summary of cash transactions during the year:

You are informed that there were considerable amount of cash sales during the year. Credit purchases during the year amounted to ₹ $1,80,000$. Provide $5\%$ for doubtful debts on debtors.

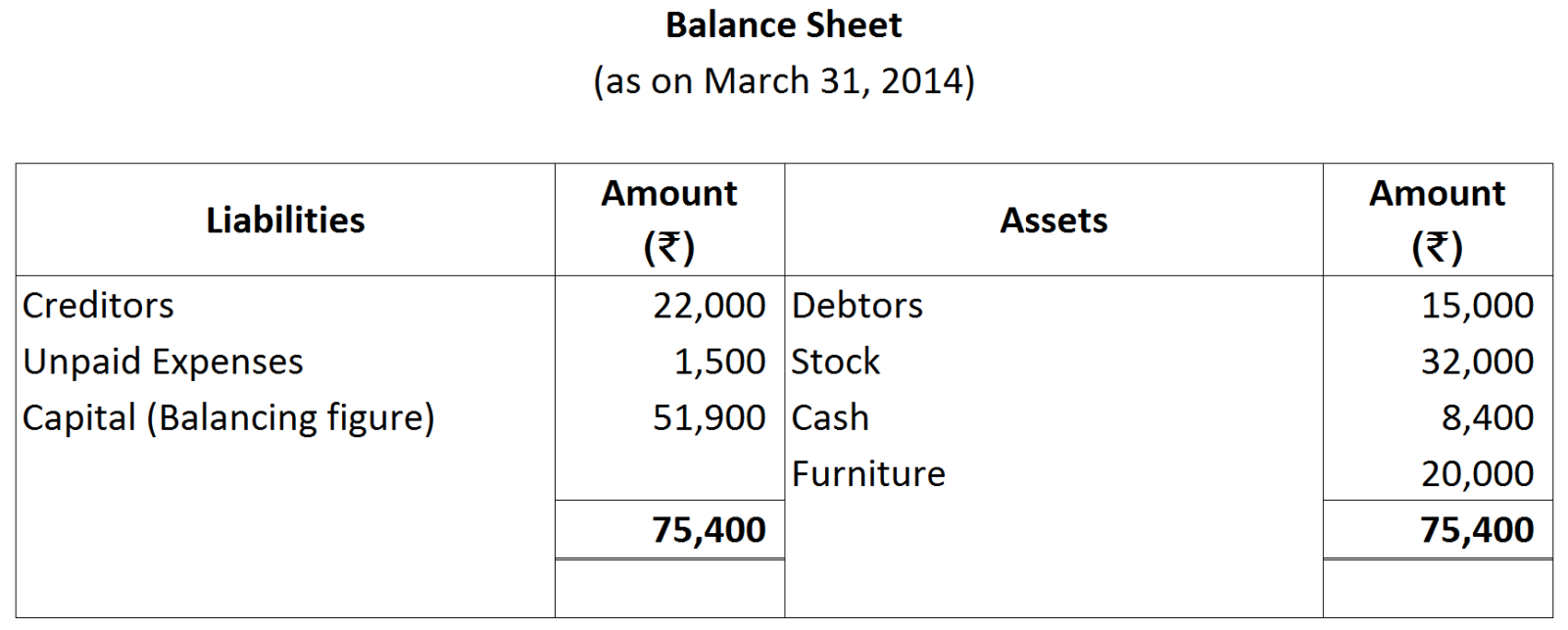

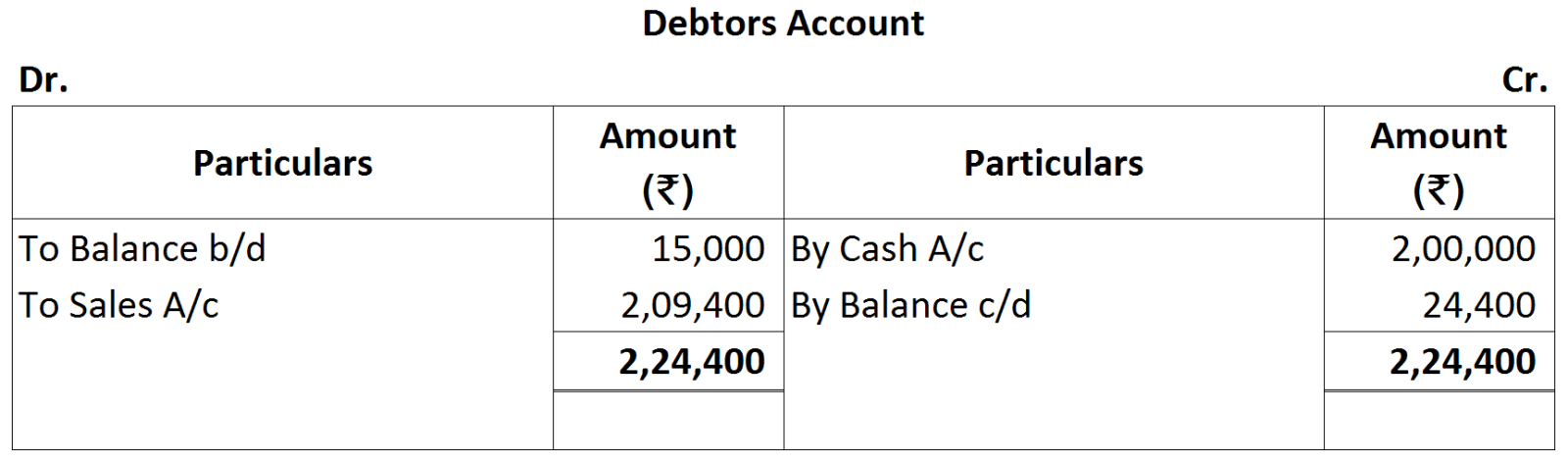

Working Notes:

Working Notes: