Question

State three points of difference between Single Entry and Double Entry System. Difference between Double Entry System and Single Entry System?

|

S.No.

|

Basis

|

Double Entry System

|

Single Entry System

|

|

1.

|

Aspect of a Transaction

|

Under this system, both aspect of a transaction are recorded.

|

Under this system, both aspect of transaction may not be recorded. In fact, for some transaction both the aspect, for some others one aspect and yet for others no aspect at all are recorded.

|

|

2.

|

Accounts Maintained

|

Under this system, personal, real and nominal etc.., all the accounts are maintained. Thus, it is a complete and scientificsystem of accounting.

|

Under this system, only personal accounts and Cash Book and maintained. Hence, it reamin an incomplete record of accounts.

|

|

3.

|

Trial Balance

|

Under this system, Trial Balance is prepared and thus, the arithmetical accuracy of all books of account is verified.

|

Under this system, Trial Balance cannot be prepared due to incomplete system of accounting. Therefore, arithmetical accuracy of the accounting cannot be verified.

|

|

4.

|

Profit or Loss

|

Under this system, after a certain period, net profit or net loss can be ascertained by preparing the Profit and Loss Account.

|

Under this system, Profit and Loss Account is not prepared to ascertain the net profit or loss. Method for ascertaining the profit or loss is not adequate.

|

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

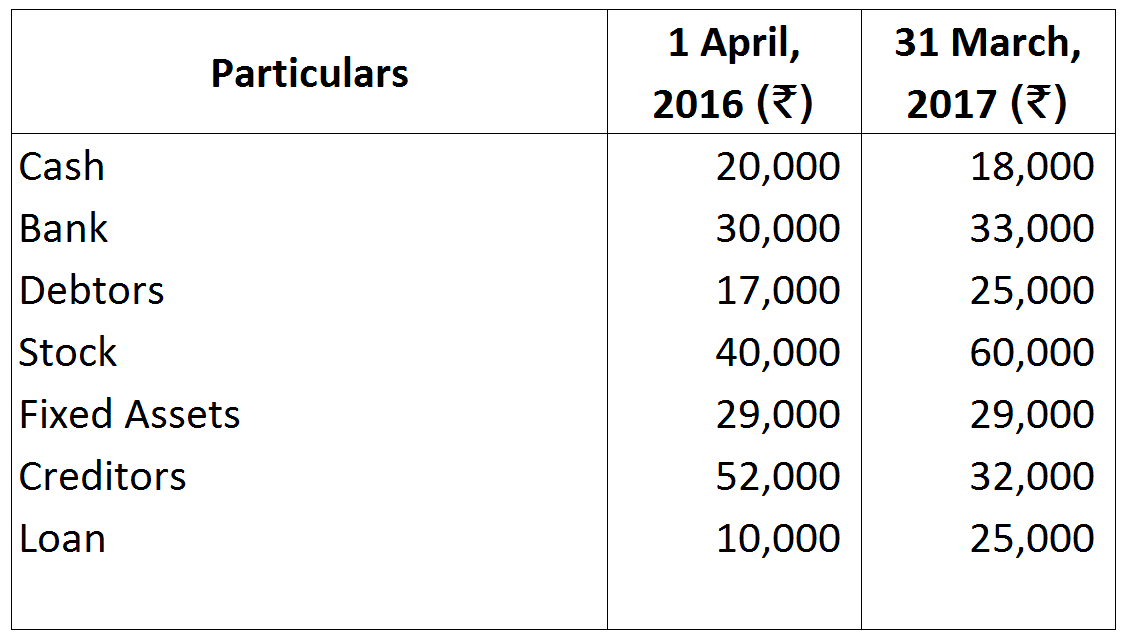

| $1^{\text {st }}$ April, 2022 (₹) | $31^{\text {st }}$ March, 2023 (₹) |

Stock-in-Trade | 16,700 | 18,100 |

Sundry Creditors | 15,400 | 19,200 |

Sundry Debtors | 27,200 | 15,600 |

Cash in Hand | 250 | 1,400 |

Bank Overdraft | 19,200 | Nil |

Fixtures and Fittings | 1,500 | 1,500 |

Motor Van | 1,900 | Nil |

Bank Balance | Nil | 2,900 |

Drawings during the year amounted to ₹ 2,400 . Depreciate Fixtures and Fittings by $10 \%$. ₹ 600 is irrecoverable from Debtors. Provide ₹ 700 for Doubtful Debts.