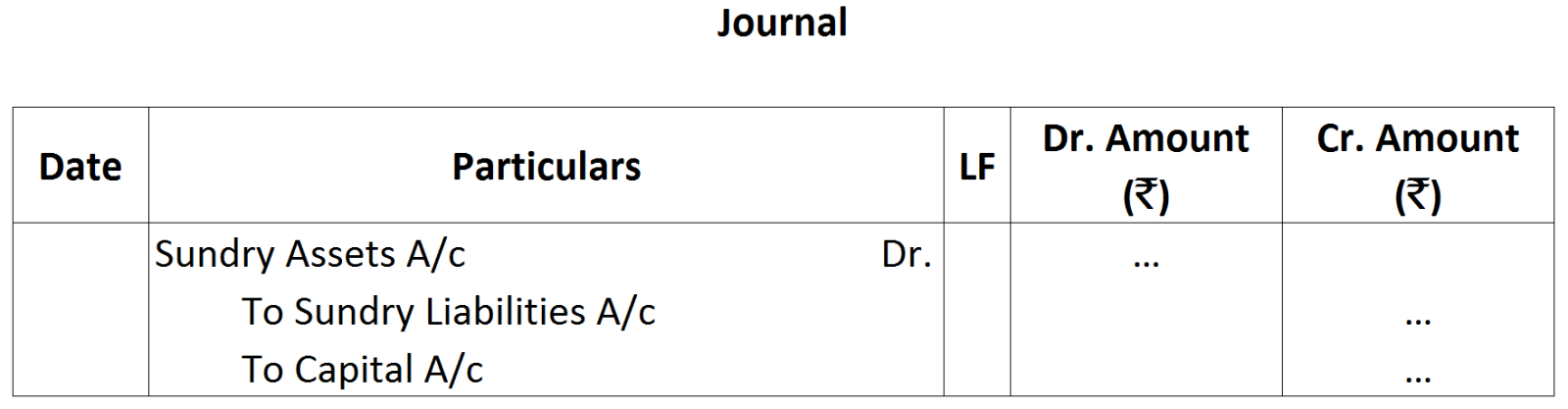

Question

Why opening entries are passed?

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

a.

|

Business started with cash

|

₹ 1,75,000

|

|

b.

|

Purchased goods from Rohit

|

₹ 50,000

|

|

c.

|

Sales goods on credit to Manish (Costing ₹ 17,500)

|

₹ 20,000

|

|

d.

|

Purchased furniture for office use

|

₹ 10,000

|

|

e.

|

Cash paid to Rohit in full settlement

|

₹ 48,500

|

|

f.

|

Cash received from Manish

|

₹ 20,000

|

|

g.

|

Rent paid

|

₹ 1,000

|

|

h.

|

Cash withdrew for personal use

|

₹ 3,000

|

|

2019

|

Particular

|

₹

|

| Jan-1 | Bought Computer Mouse (4 Nos.) vide Cash Memo No. 338* | 6,000 |

| Jan-8 | Wages paid for the month of December, 2018 | 10,000 |

| Jan-12 | Purchased two Desktop Computers from M/s Computech for cash vide Cash Memo No. 170 | 32,500 |

| Jan-25 | Paid cash to Hari & Sons vide receipt No. 102 for repairs | 1,000 |

| Jan-28 | Paid postage | 200 |

| Jan-30 | Cash withdrawn from bank | 10,000 |

|

|

Date of the Bills

|

Period

|

|

I.

|

29th May, 2017 | 4 months |

|

II.

|

31st March, 2017 | 1 month |

|

III.

|

21st July, 2017 | 60 days |

|

IV.

|

14th May, 2017 | 90 days |

|

V.

|

28th January, 2016 | 1 month |

|

VI.

|

31st January, 2016 | 1 month |

|

Emergency holiday 22nd September

|

|

Dec. 2017

|

|

₹

|

|

1

|

Started business with cash

|

2,00,000

|

|

2

|

Bought office furniture

|

30,000

|

|

3

|

Paid into bank to open an current account

|

1,00,000

|

|

5

|

Purchased a computer and paid by cheque

|

2,50,000

|

|

6

|

Bought goods on credit from Ritika

|

60,000

|

|

8

|

Cash sales

|

30,000

|

|

9

|

Sold goods to Karishna on credit

|

25,000

|

|

12

|

Cash paid to Mansi on account

|

30,000

|

|

14

|

Goods returned to Ritika

|

2,000

|

|

15

|

Stationery purchased for cash

|

3,000

|

|

16

|

Paid wages

|

1,000

|

|

18

|

Goods returned by Karishna

|

2,000

|

|

20

|

Cheque given to Ritika

|

28,000

|

|

22

|

Cash received from Karishna on account

|

15,000

|

|

24

|

Insurance premium paid by cheque

|

4,000

|

|

26

|

Cheque received from Karishna

|

8,000

|

|

28

|

Rent paid by cheque

|

3,000

|

|

29

|

Purchased goods on credit from Meena Traders

|

20,000

|

|

30

|

Cash sales

|

14,000

|

|

2019

|

|

₹

|

|

March 1

|

Manohar Lal & Sons started business with cash

|

60,000

|

|

March 2

|

Purchased furniture for cash

|

10,000

|

|

March 4

|

Purchased goods for cash

|

25,000

|

|

March 5

|

Bought goods from Kamlesh

|

15,000

|

|

March 10

|

Paid cash to Kamlesh

|

15,000

|

|

March 16

|

Purchased goods from Sohan

|

6,000

|

|

March 18

|

Purchased goods from Sohan for cash

|

8,000

|

|

March 20

|

Paid rent for the office

|

1,000

|

|

1.

|

Bought goods from Nanak Bros. for ₹ 4,00,000 at 10% trade discount and 3% cash discount on purchase price. 25% of the amount paid at the time of purchase.

|

|

2.

|

Sold goods to Kumar & Sons. for ₹ 2,00,000 at 20% trade discount and 5% cash discount on sale price. 60% of the amount received by Cheque.

|

|

3.

|

Received from Gopi Chand ₹ 38,000 by Cheque after deducting 5% cash discount.

|

|

4.

|

Paid ₹ 20,000 for rent by Cheque.

|

|

5.

|

Paid ₹ 50,000 for salaries by Cheque.

|

|

6.

|

Goods worth ₹ 10,000 distributed as free samples.

|

|

7.

|

₹ 5,000 due from Chanderkant are bad-debts.

|

|

8.

|

Sold household furniture for ₹ 15,000 and the proceeds were invested into business.

|