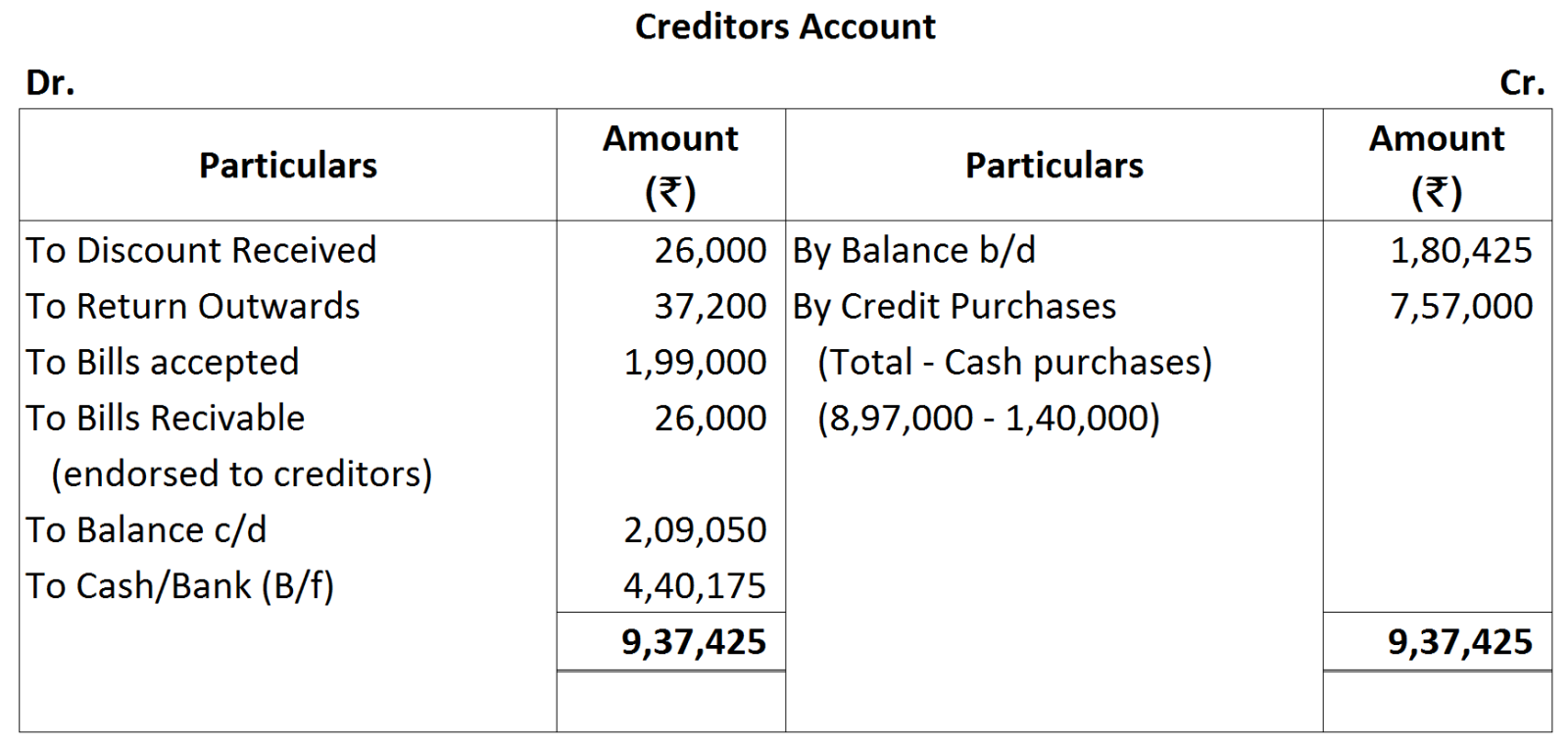

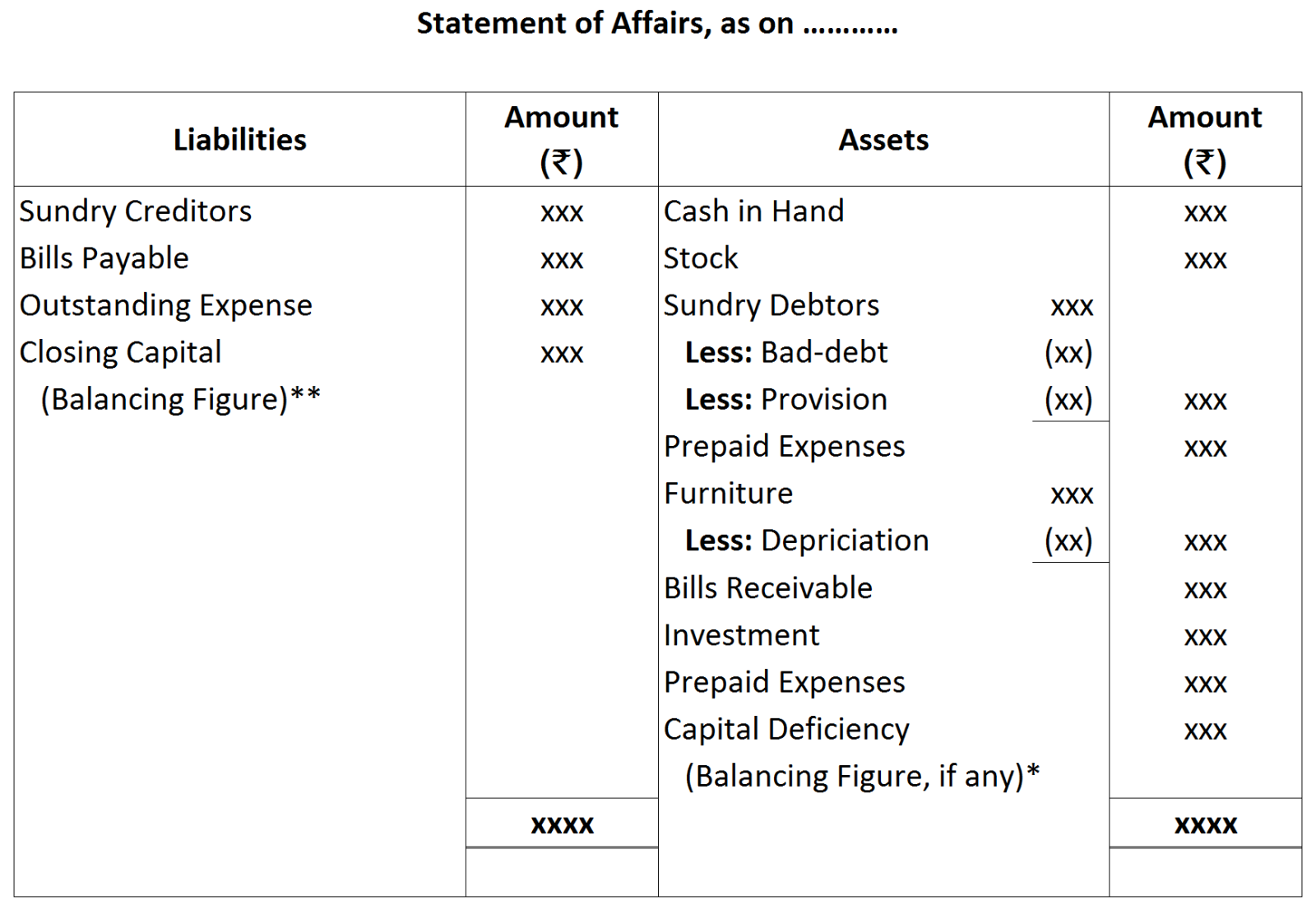

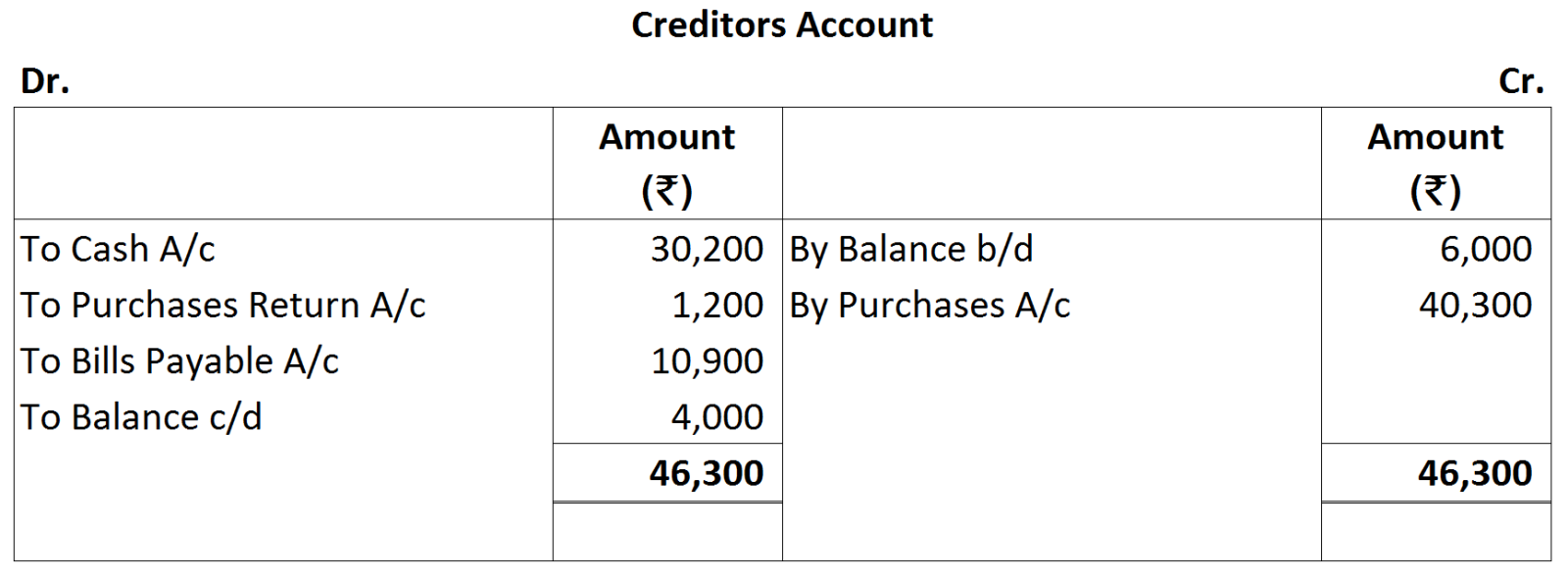

Question 14 Marks

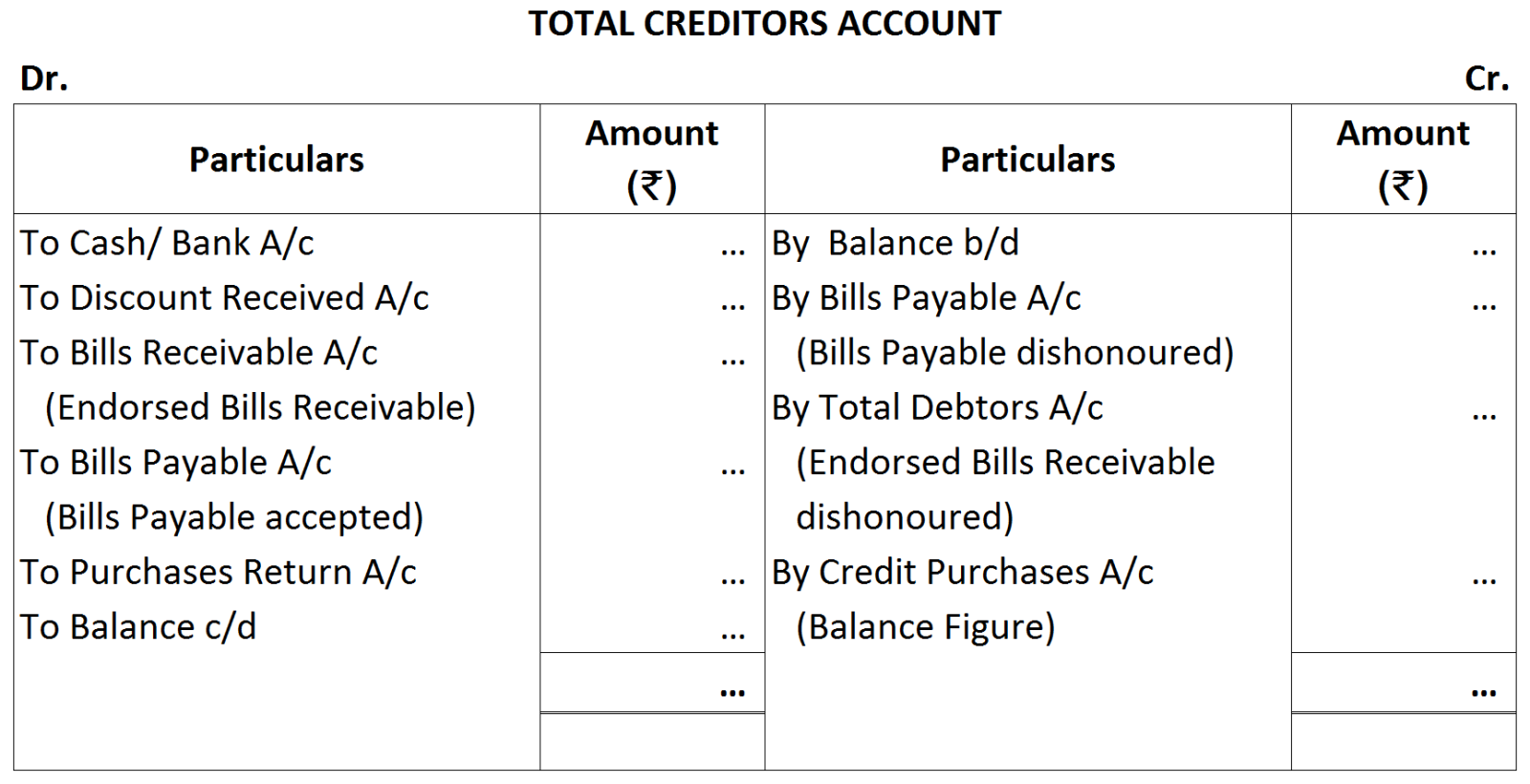

Prepare a ‘Total Creditors Account with imaginary figures.

Answer

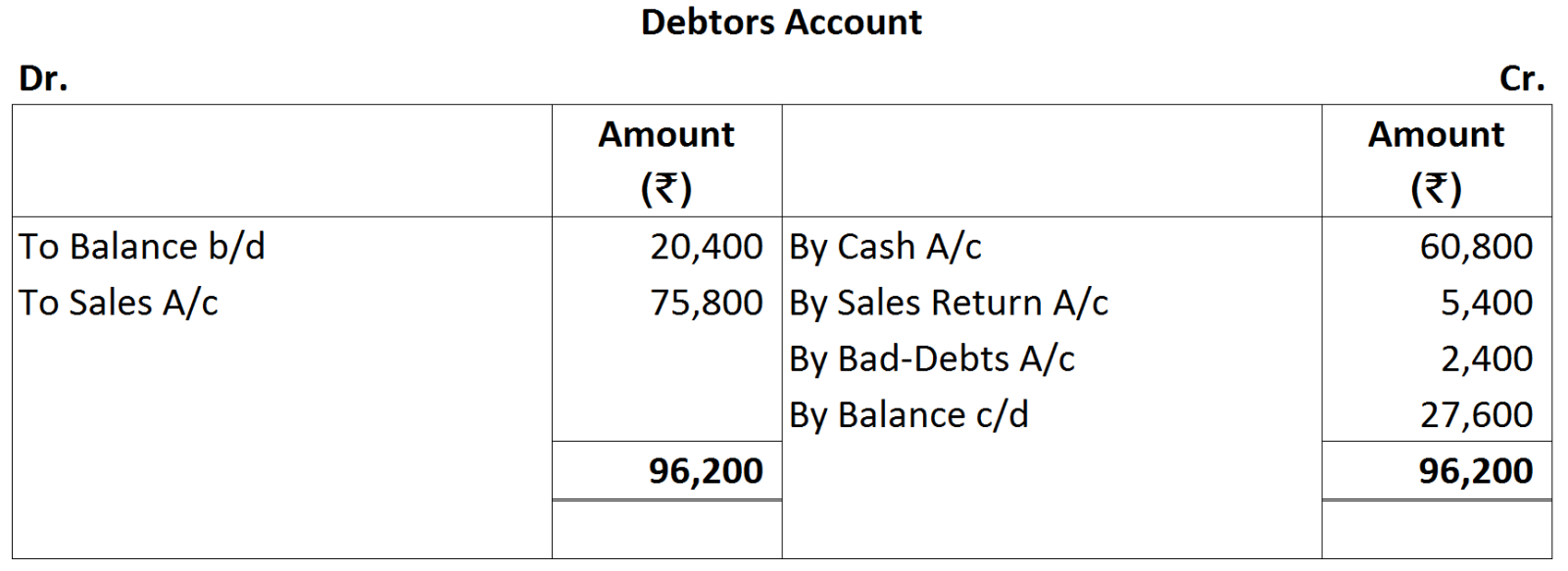

View full question & answer→Prepare Total Creditors Account: Total Creditors Account is prepared in the same manner as Total Debtors Account to find the missing value (figure) of credit purchases or closing balance of creditors or cash paid to creditors or opening balance of creditors as given below:

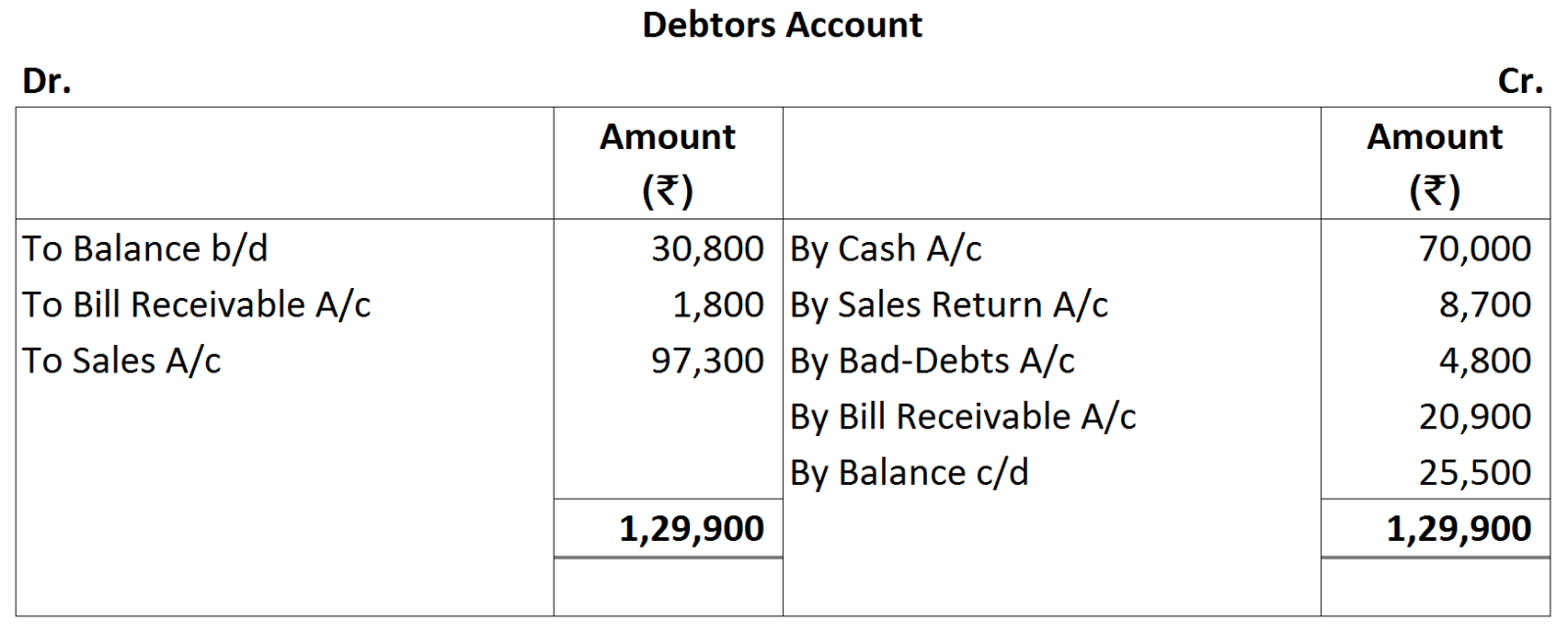

Total Sales = Cash Sales + Credit Sales

Total Sales = Cash Sales + Credit Sales

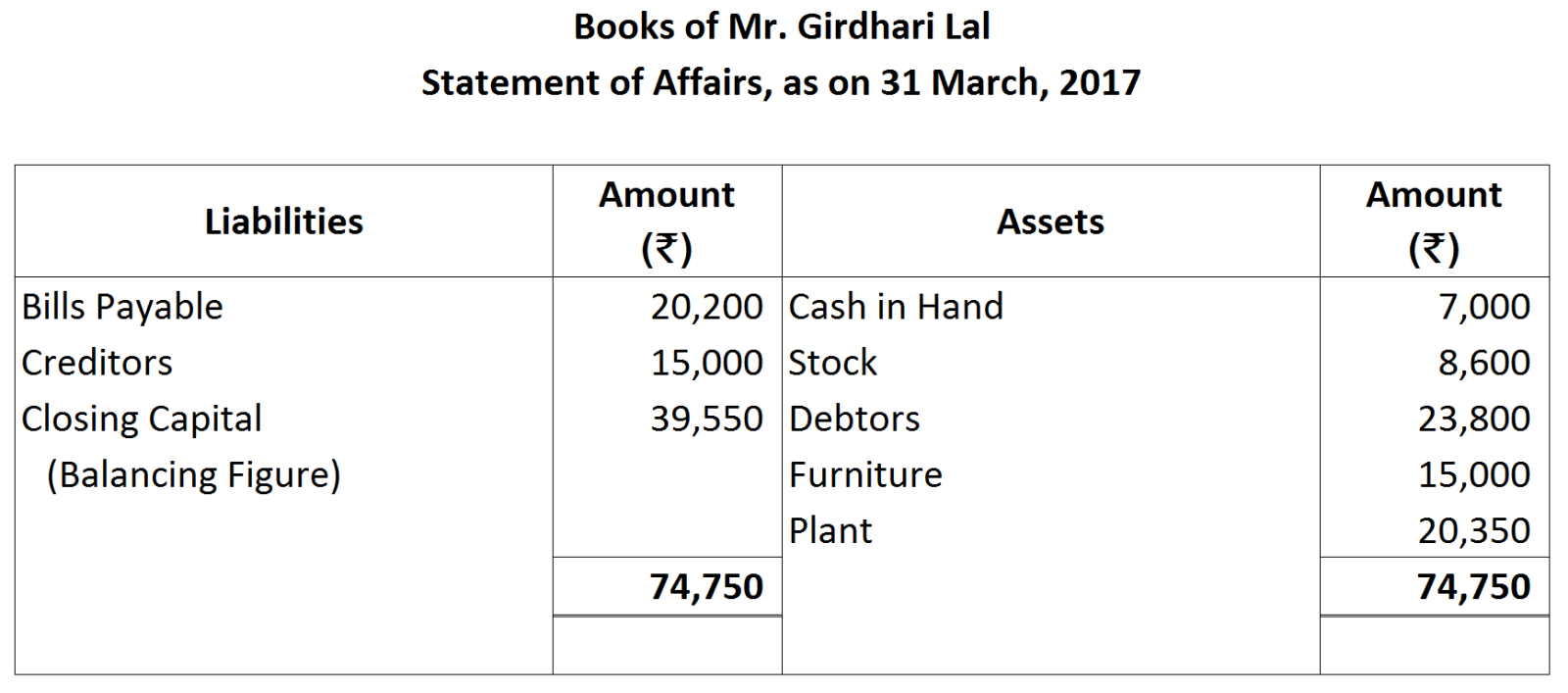

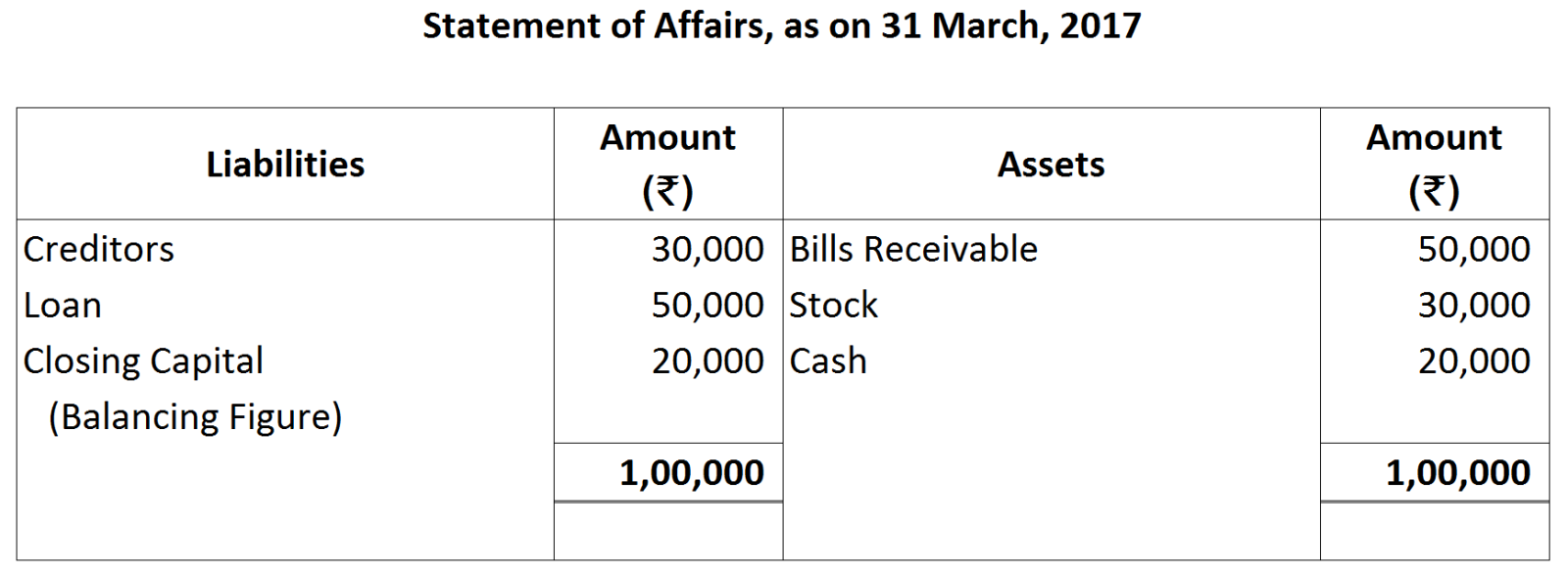

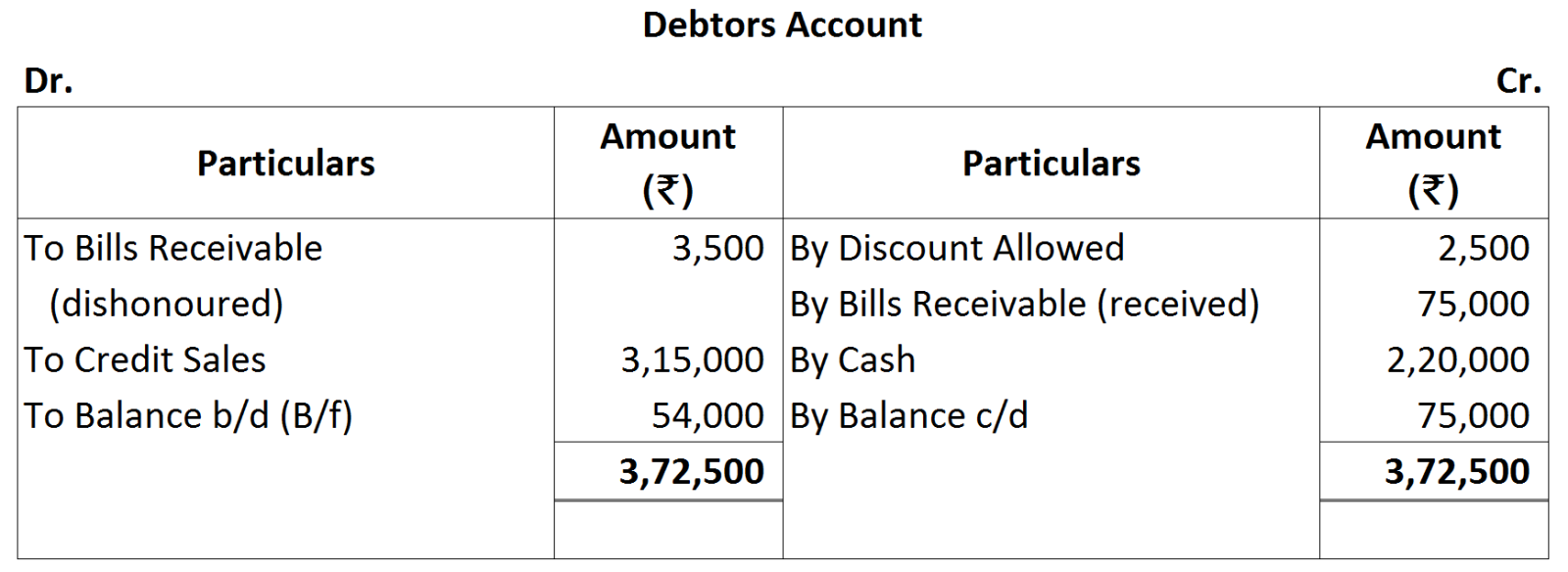

Capital on March 31, 2017 (Closing) is ₹ 20,000

Capital on March 31, 2017 (Closing) is ₹ 20,000

Total Sales = Cash Sales + Credit Sales

Total Sales = Cash Sales + Credit Sales

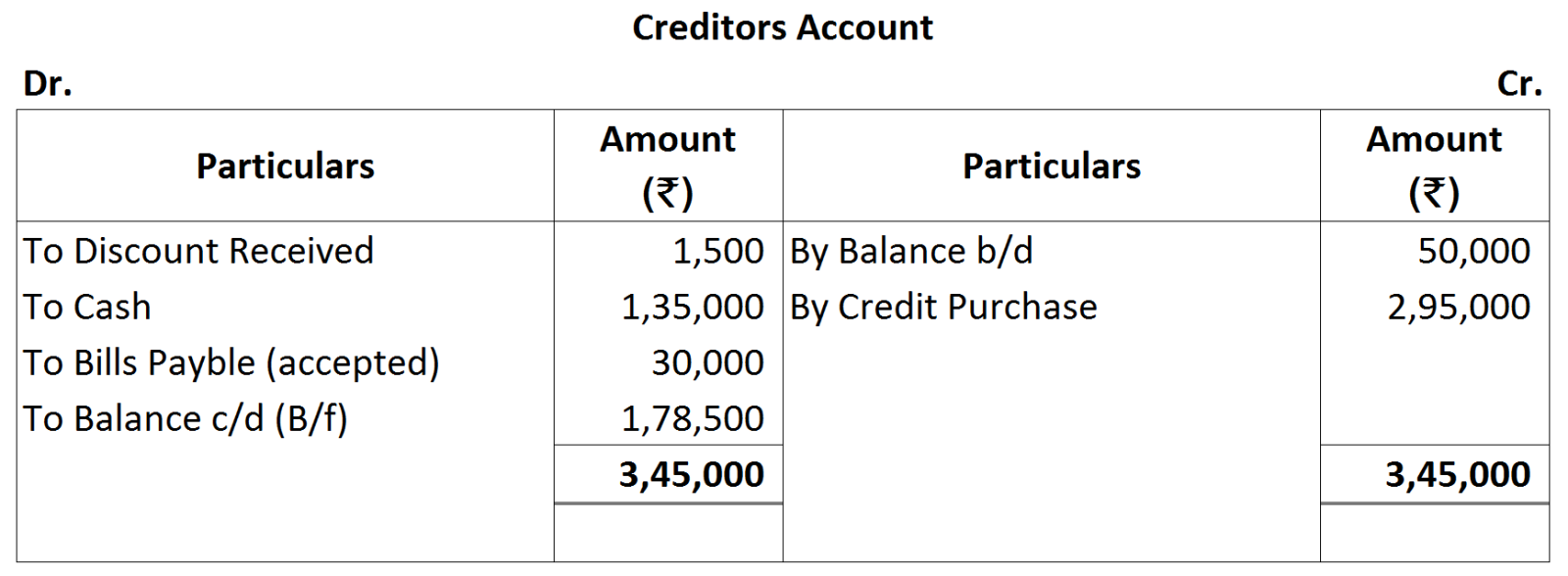

Total Purchases = Cash Purchases + Credit Purchases

Total Purchases = Cash Purchases + Credit Purchases