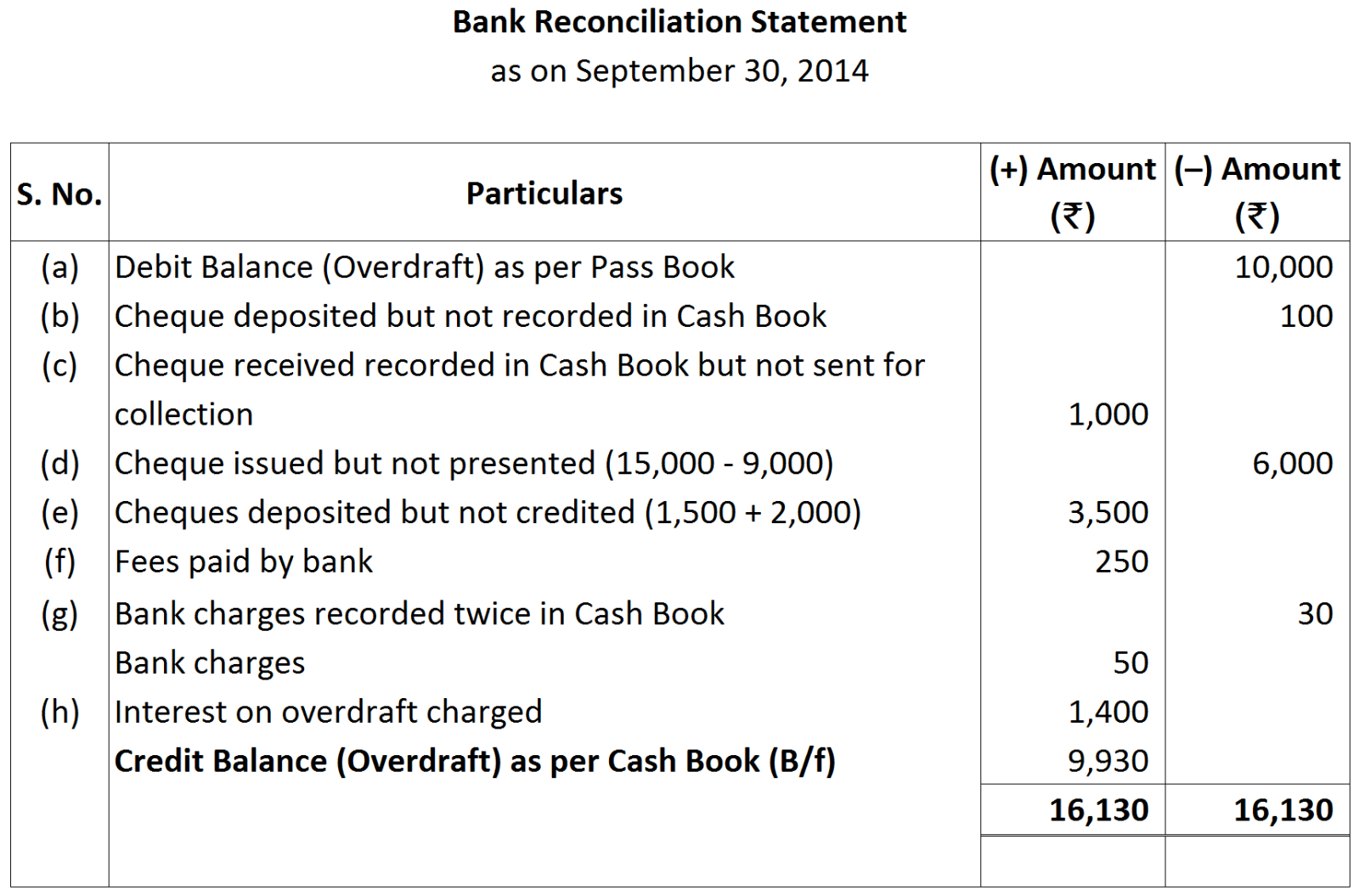

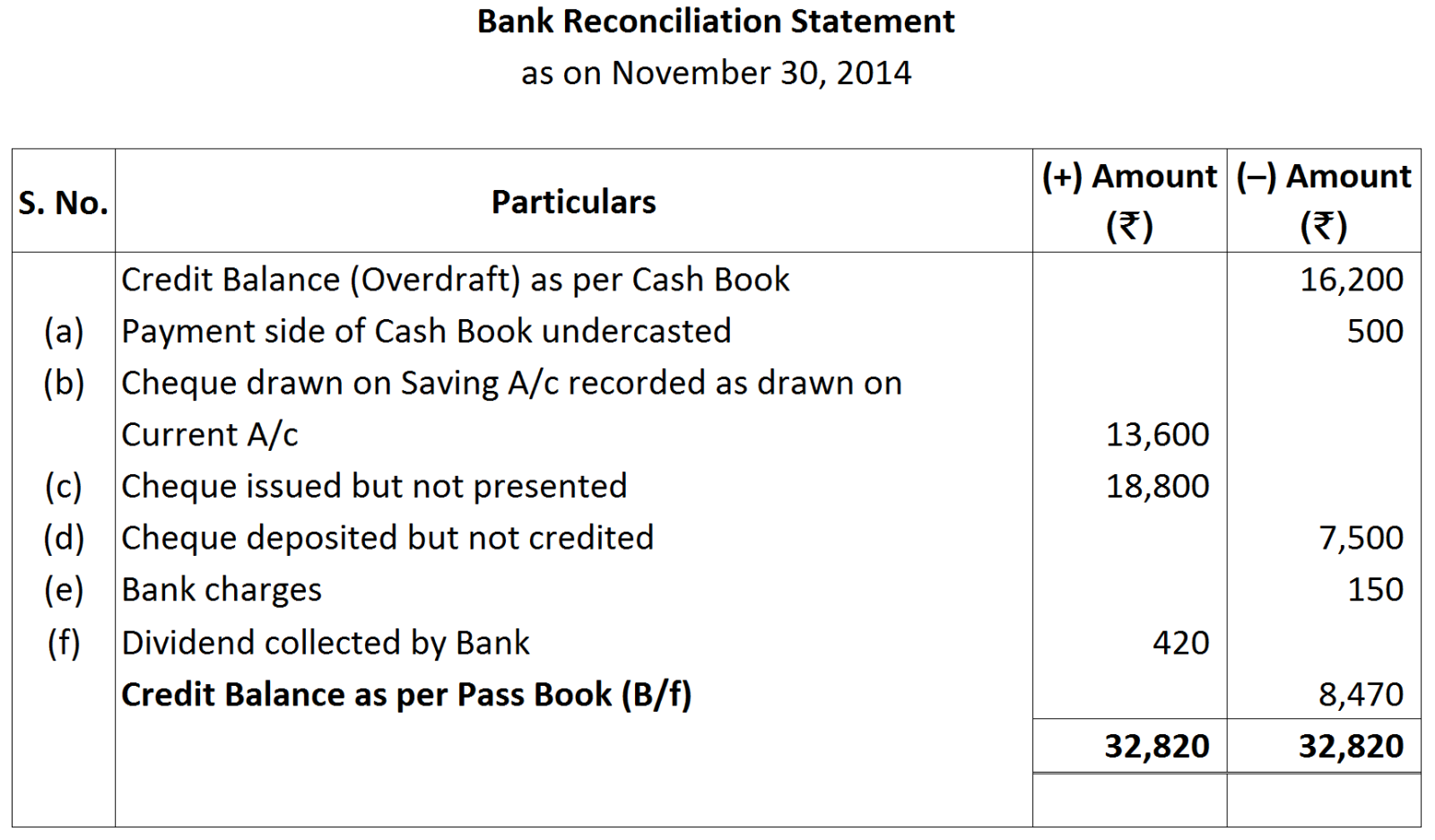

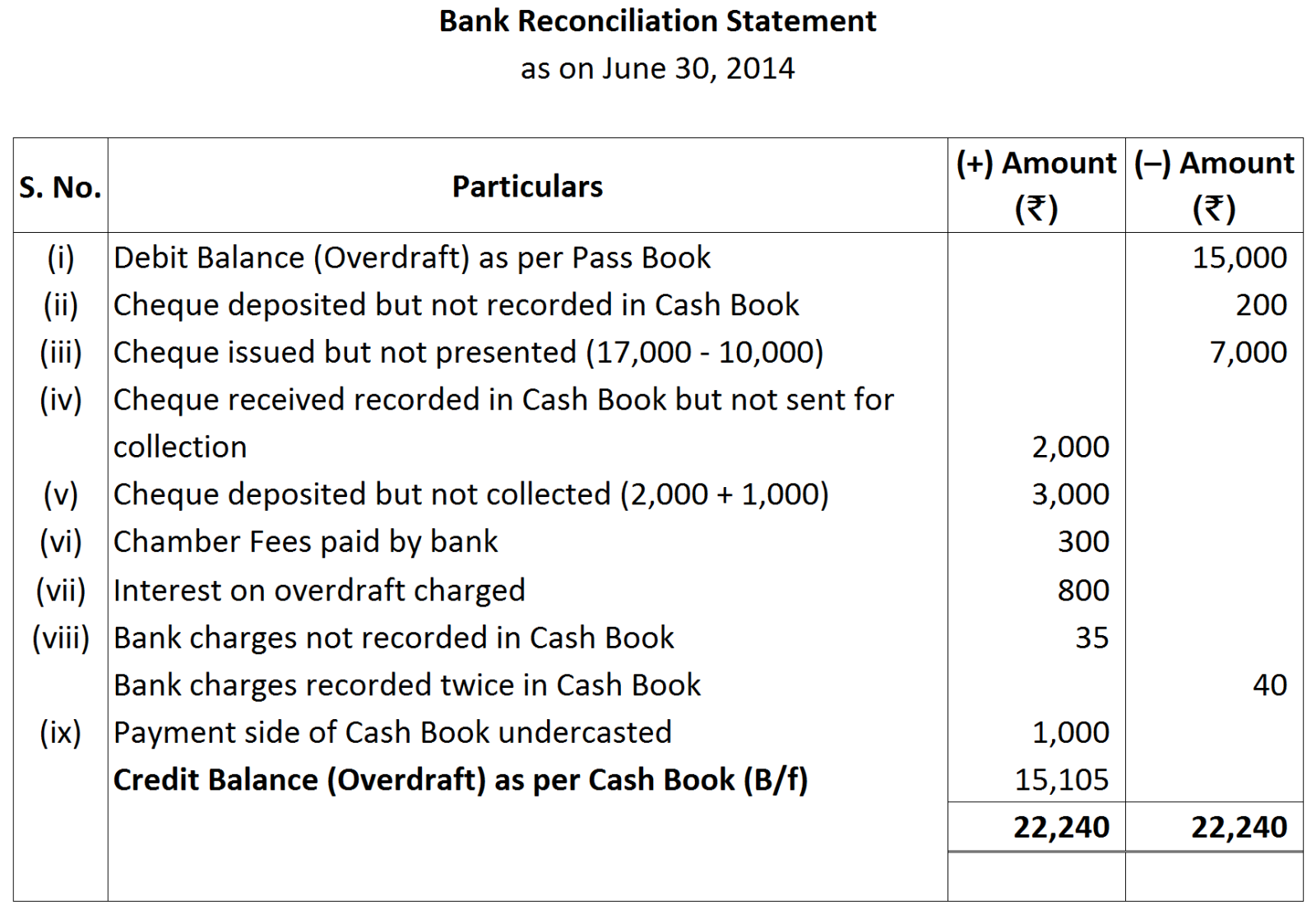

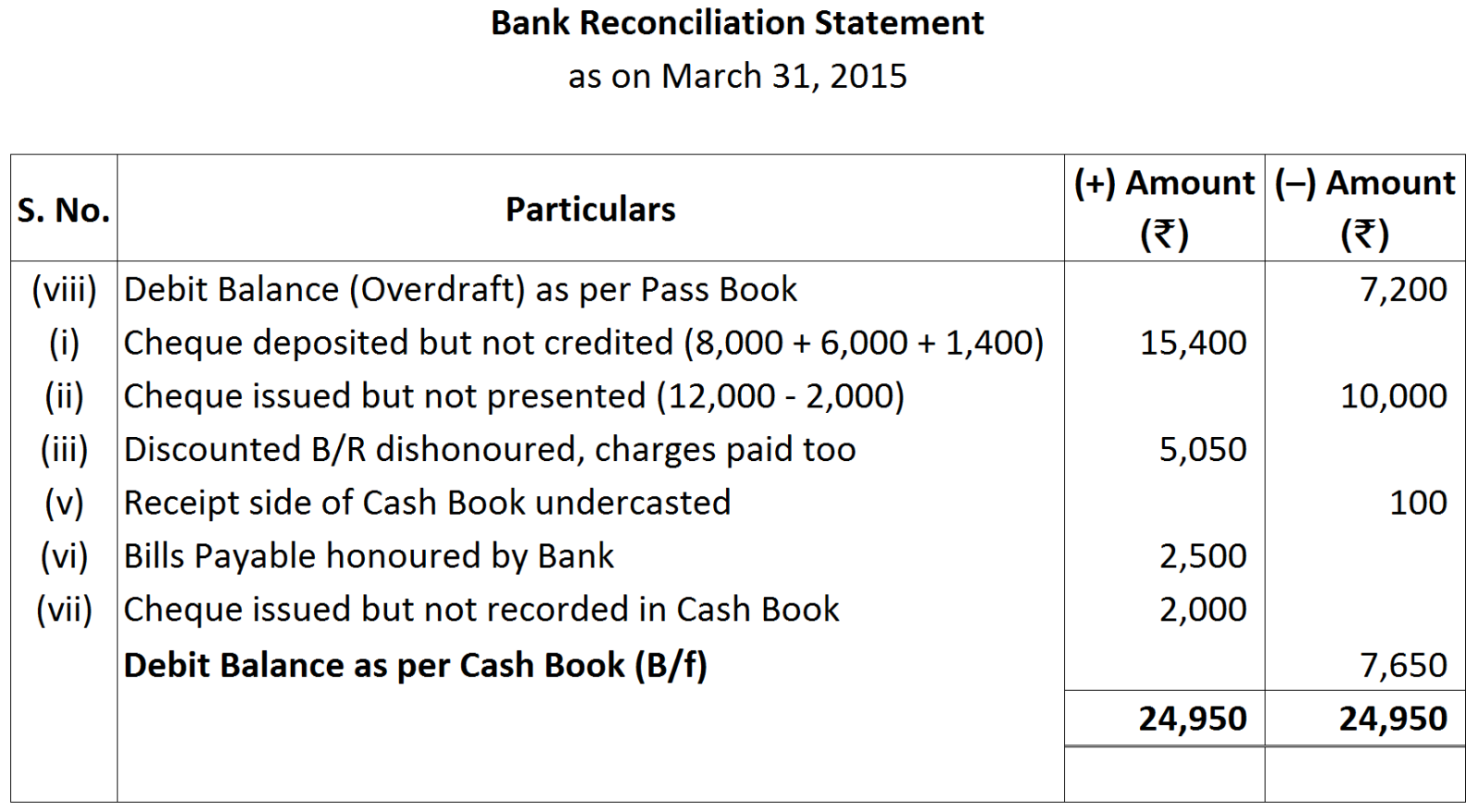

Question 16 Marks

The bank statement of Mr. James Flint showed an overdraft to the tune of ₹ 60,400 as on 31-12-2014. Cash Book showed a debit balance of ₹ 2,00,120 as on the same date. The following further facts are available:

Prepare a Bank Reconciliation Statement of Mr. James Flint as on 31-12-2014.

|

|

|

₹

|

|

(a)

|

Cheque issued to Tax Consultants was not cashed till 31-12-2014.

|

12,000

|

|

(b)

|

Cheque issued to Management Consultancy Services was cashed on 14-1-2015.

|

20,000

|

|

(c)

|

Cheque received from M/s General Studies and deposited into the bank was credited in the account on 3-1-2015.

|

2,20,000

|

|

(d)

|

Dividend warrant deposited on 29-12-2014 was not credited by the bank till 31-12-2014.

|

74,400

|

|

(e)

|

Bank charge not adjusted in books of Mr. Flint till 31-12-2014

|

680

|

|

(f)

|

Interest credited by the bank and not adjusted in the books till 31-12-2014

|

2,560

|

Note:

Note: