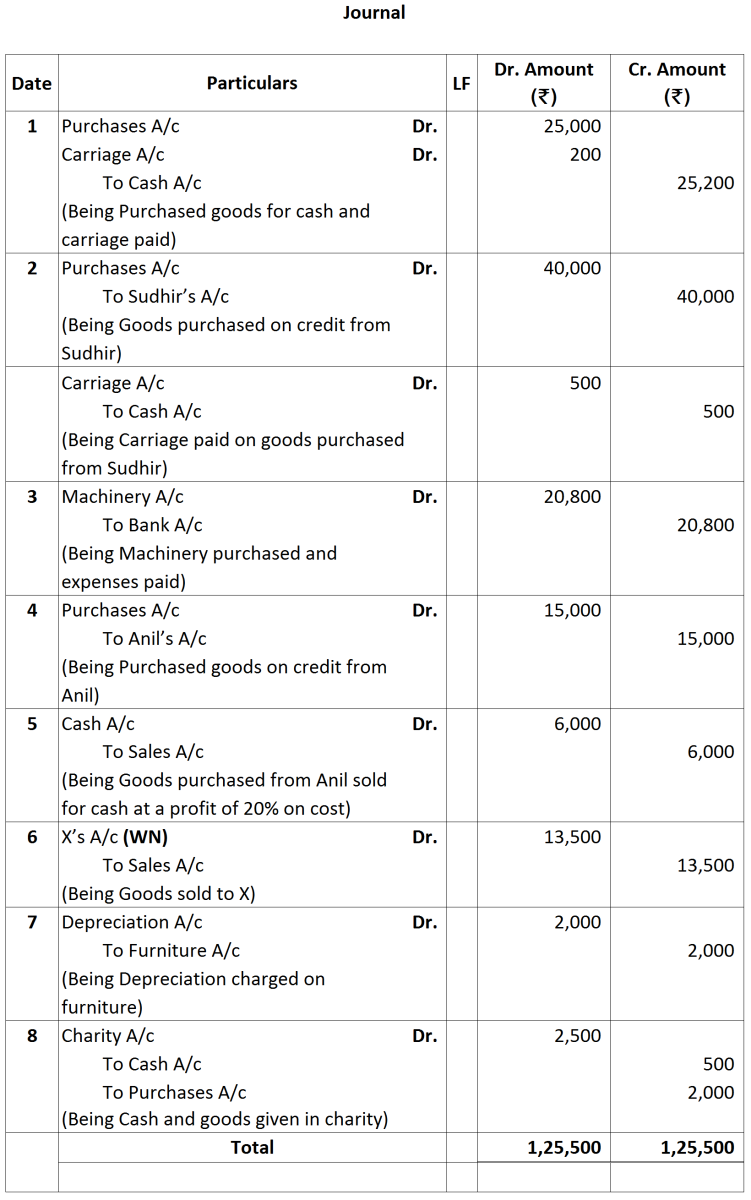

Question 13 Marks

Journalise the following in the books of Som Nath & Sons:

| 2019 | |

| May 1 | Purchased a Machinery for ₹ 1,00,000 and the payment was made by issuing a cheque from Proprietor's saving bank account. |

| May 4 | Received an order from Chakravarti for goods of ₹ 4,00,000 alongwith a cheque of 10% of the order as advance. |

| May 8 | Paid cash ₹ 8,000 to Dushyant and discount allowed by him ₹ 800. |

| May 10 | Goods stolen by an employee (Sale Price ₹ 20,000; Cost ₹ 15,000). |

| May 15 | Purchased stationery worth ₹ 8,000 for office use and ₹ 2,000 for personal use. |

| May 20 | Manoj pays us ₹ 5,400 after deducting 10% for prompt payment. |

| May 28 | Sold goods to Kuber costing ₹ 2,00,000 at 25% above cost less trade discount of 10% and cash discount of 5%. Kuber did not avail the cash discount. |

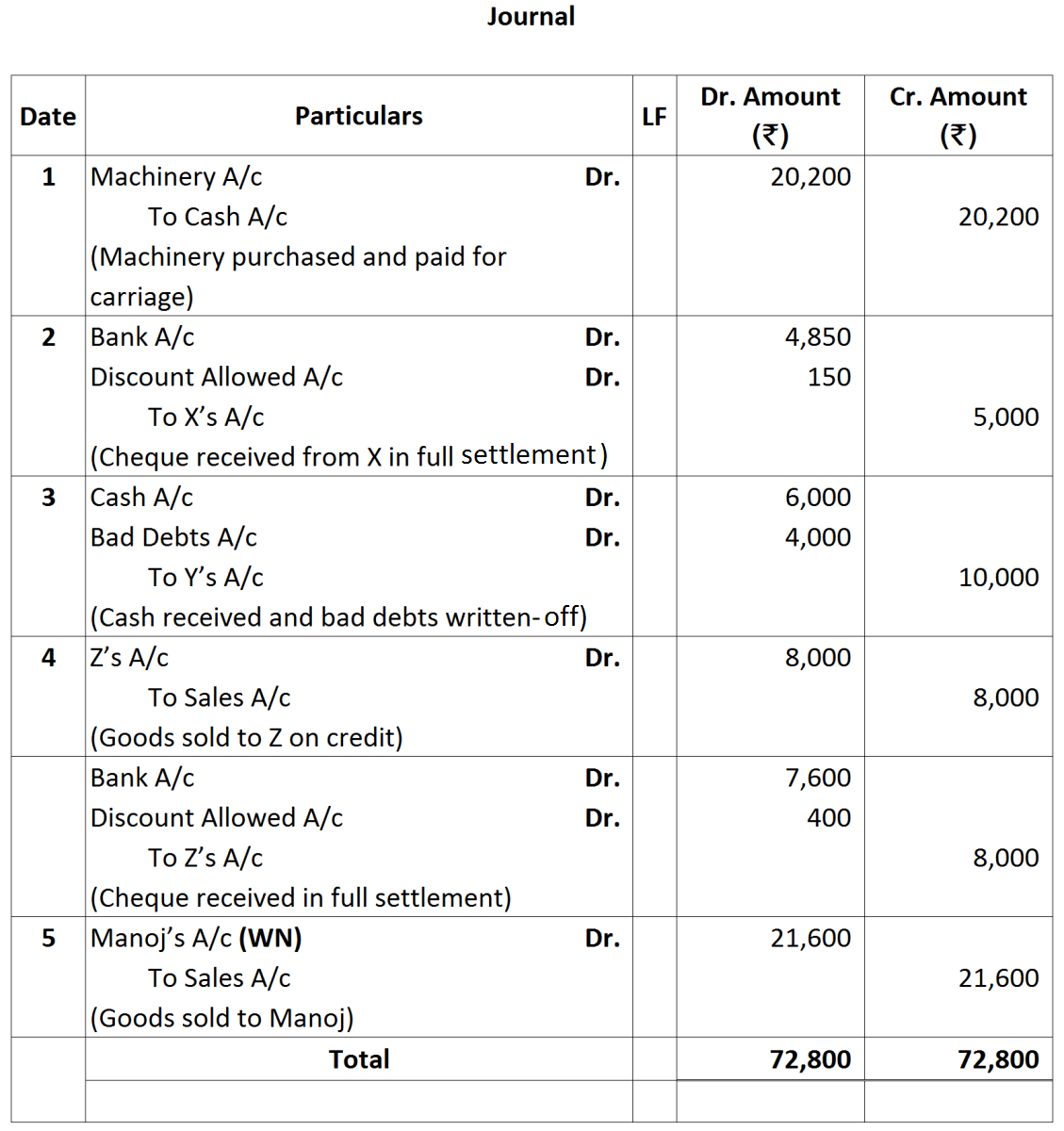

Working Notes: Calculation of amount of goods sold to Manoj.

Working Notes: Calculation of amount of goods sold to Manoj.

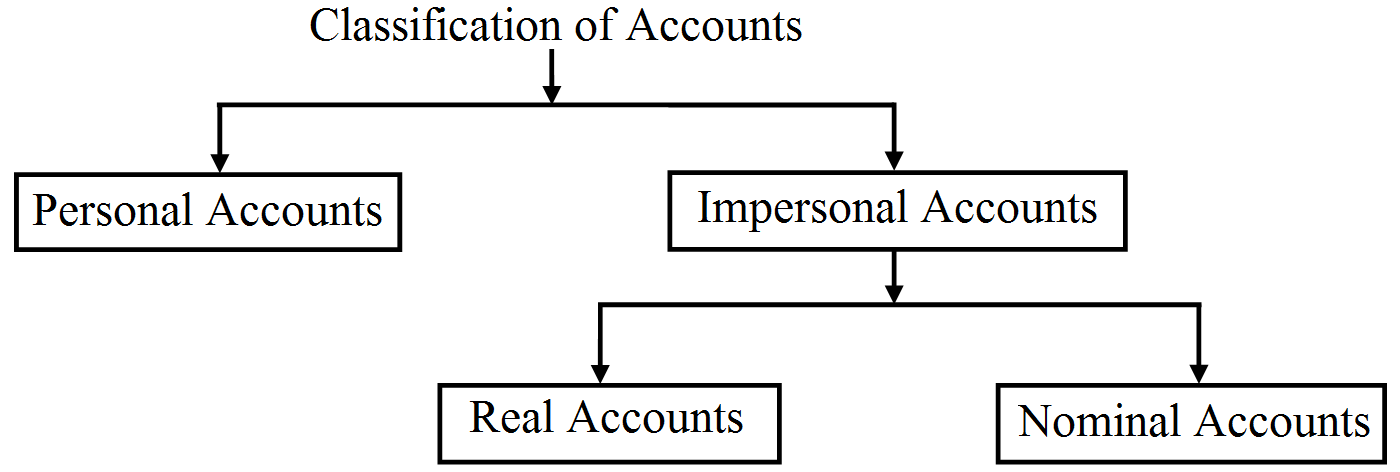

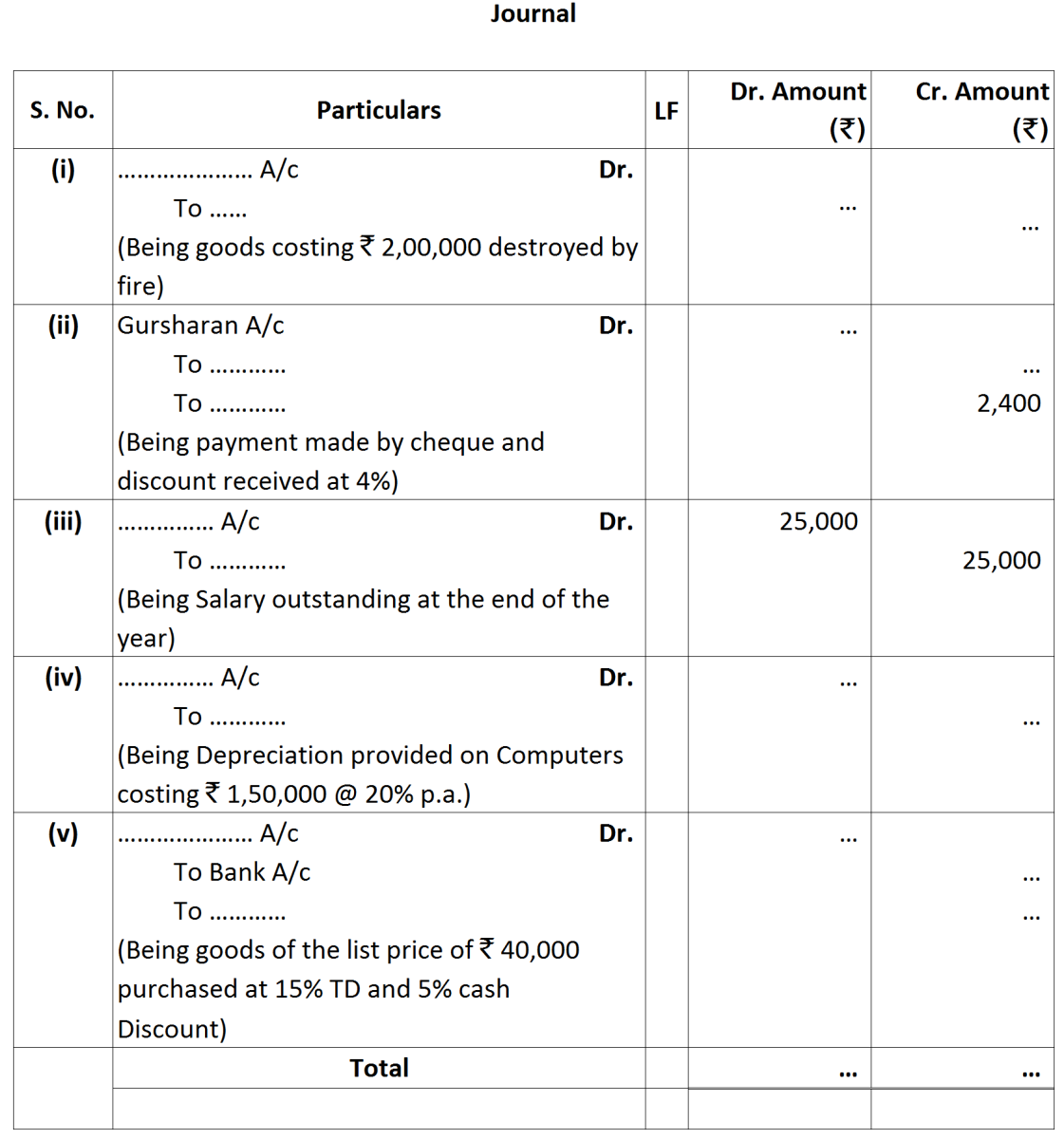

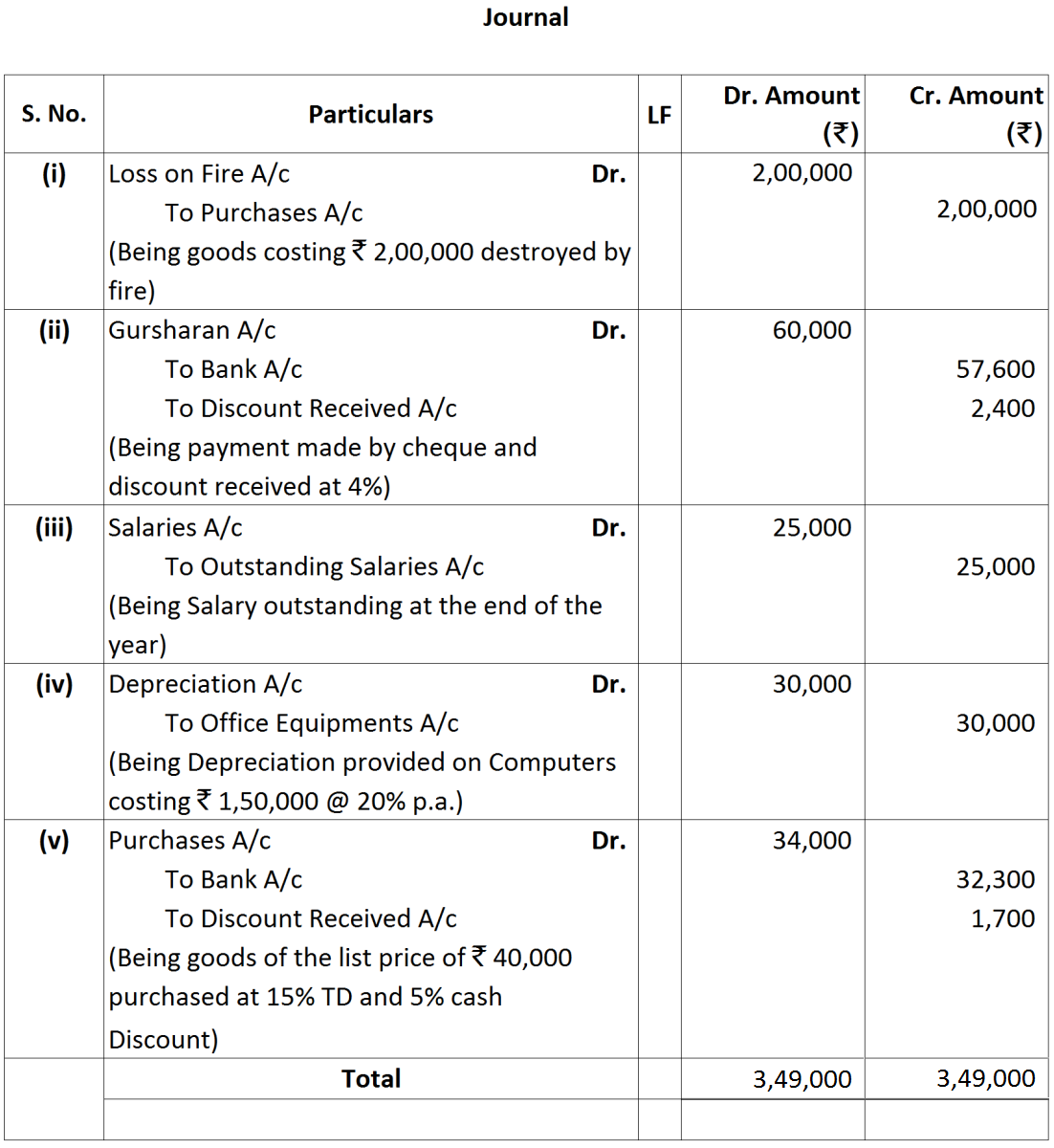

Date: Date of transaction is recorded in the order of their occurrence. Particulars: Details of business transactions like, name of the parties involved and the name of related accounts, are recorded. L.F.: Page number of ledger account when entry is posted. Debit Amount: Amount of debit account is written. Credit Amount: Amount of credit account is written. Recording of a Journal Entry

Date: Date of transaction is recorded in the order of their occurrence. Particulars: Details of business transactions like, name of the parties involved and the name of related accounts, are recorded. L.F.: Page number of ledger account when entry is posted. Debit Amount: Amount of debit account is written. Credit Amount: Amount of credit account is written. Recording of a Journal Entry

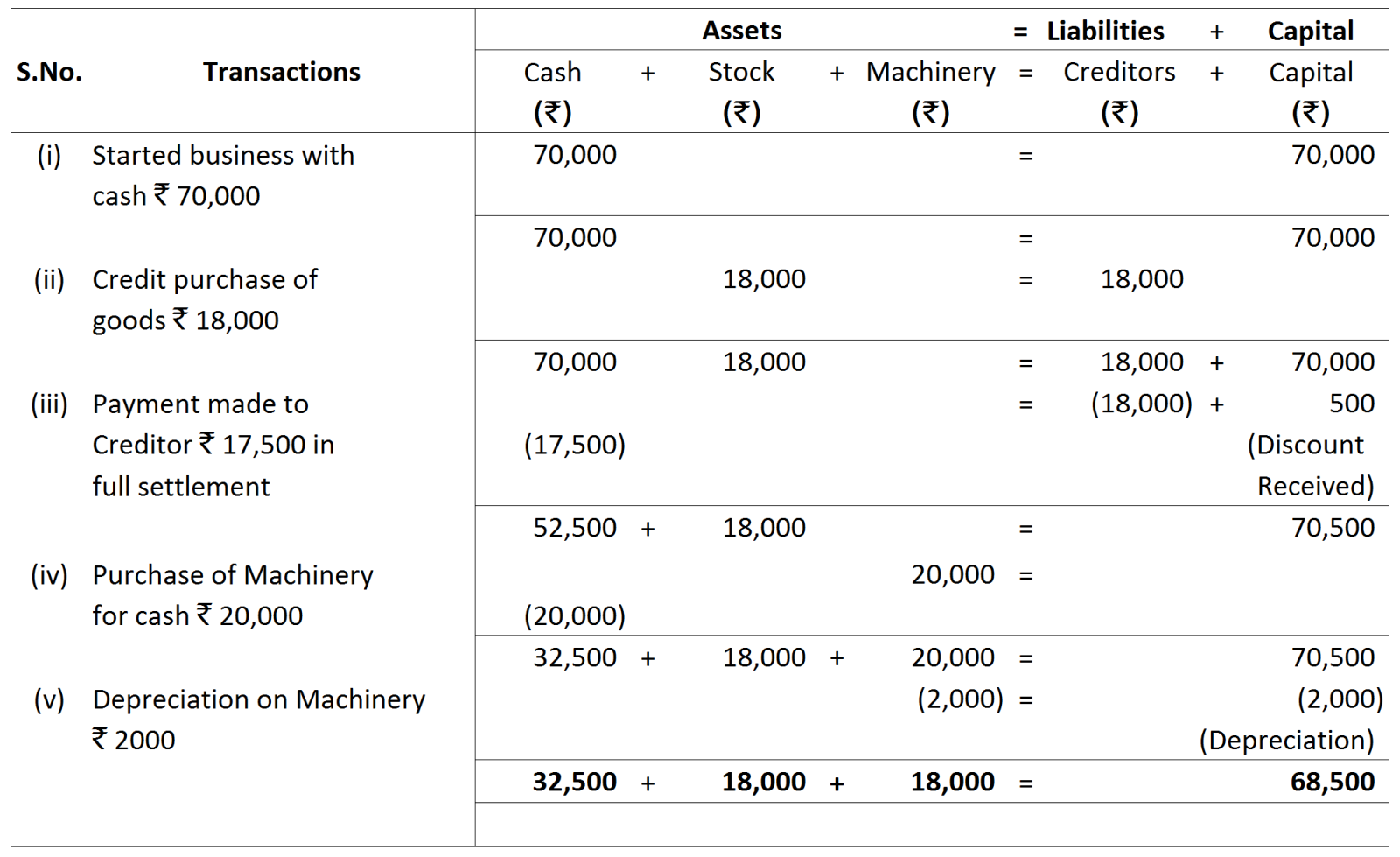

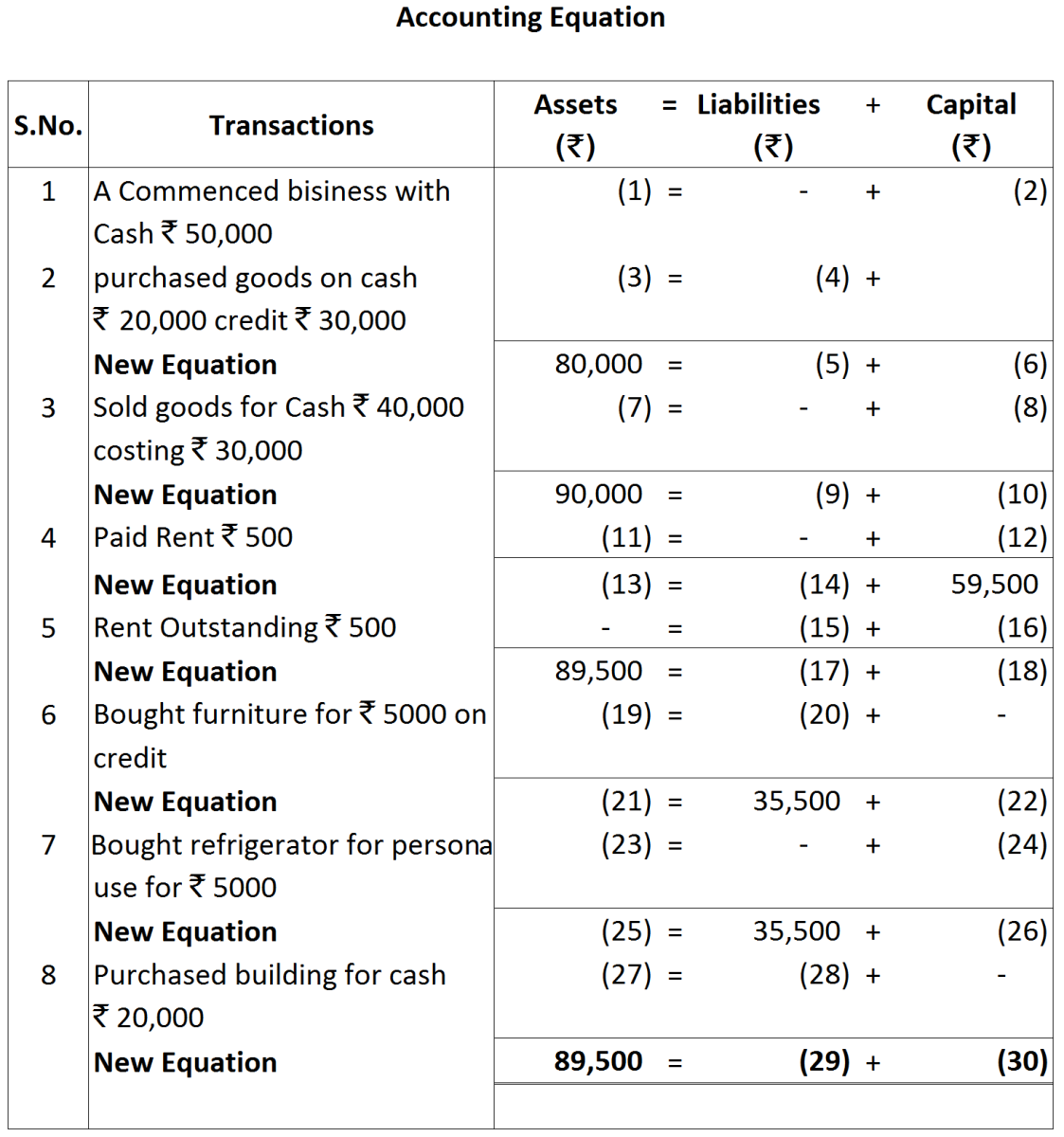

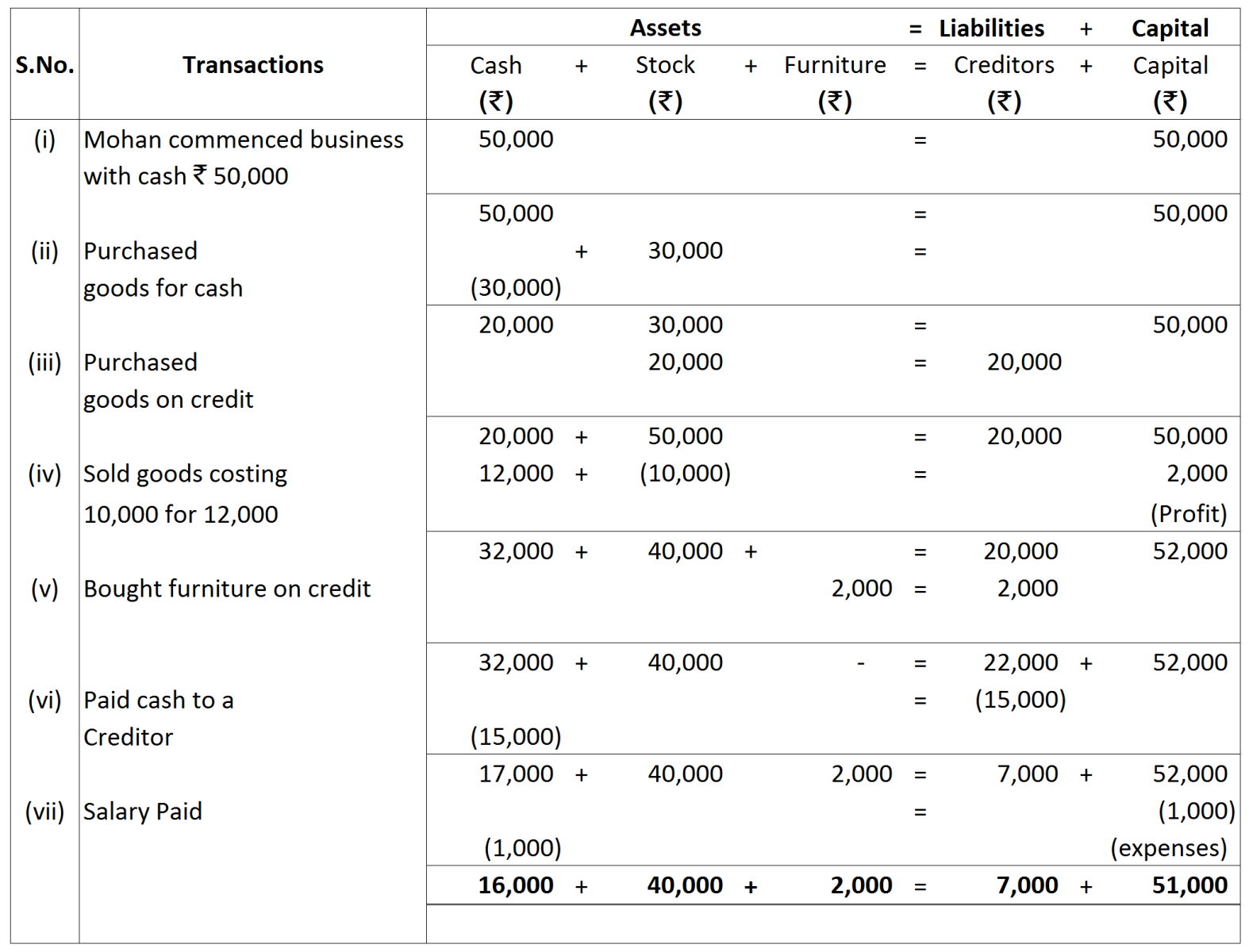

Assets = 32,500 + 18,000 + 18,000 = ₹ 68,500

Assets = 32,500 + 18,000 + 18,000 = ₹ 68,500

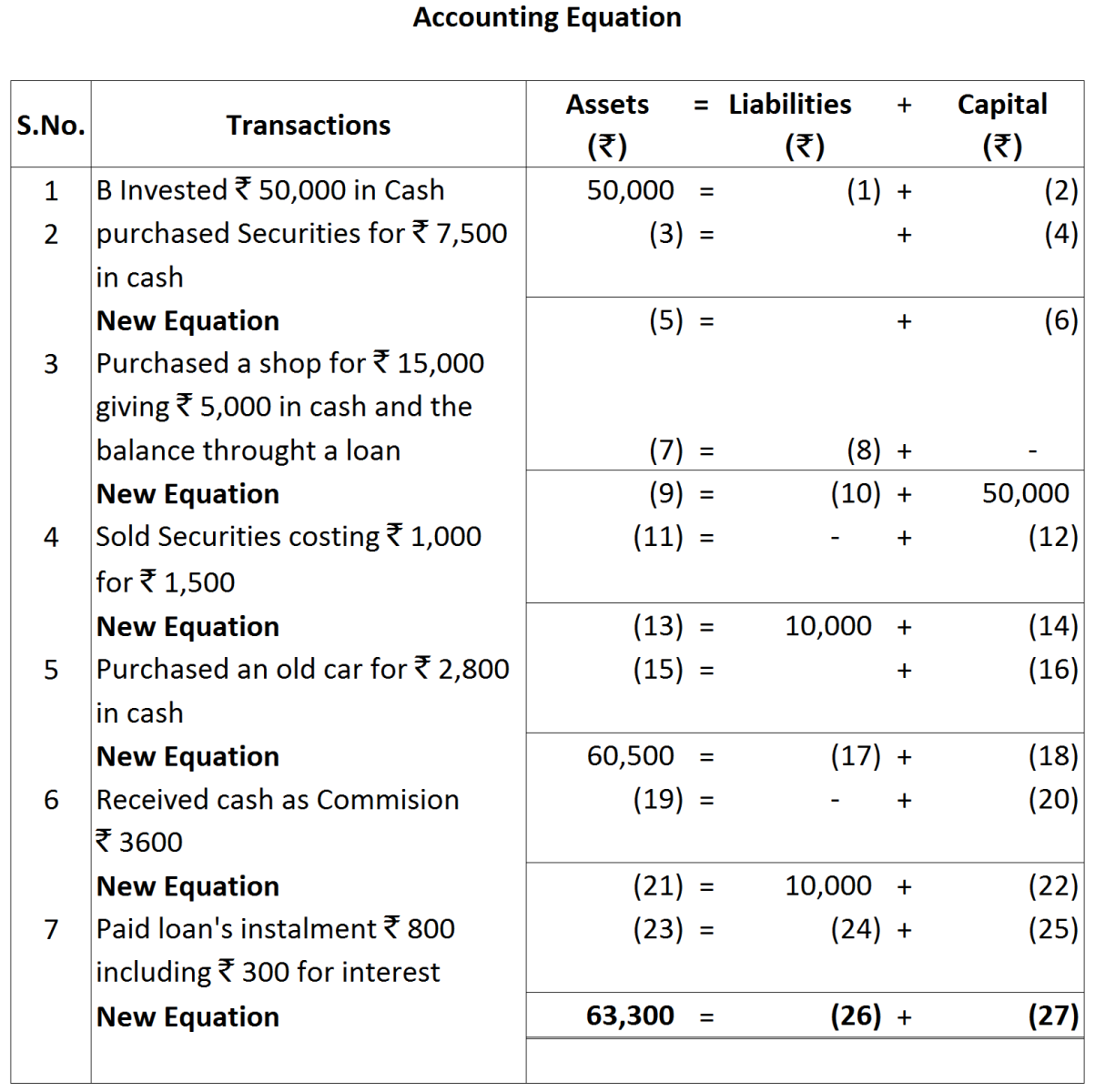

Working Note:

Working Note:

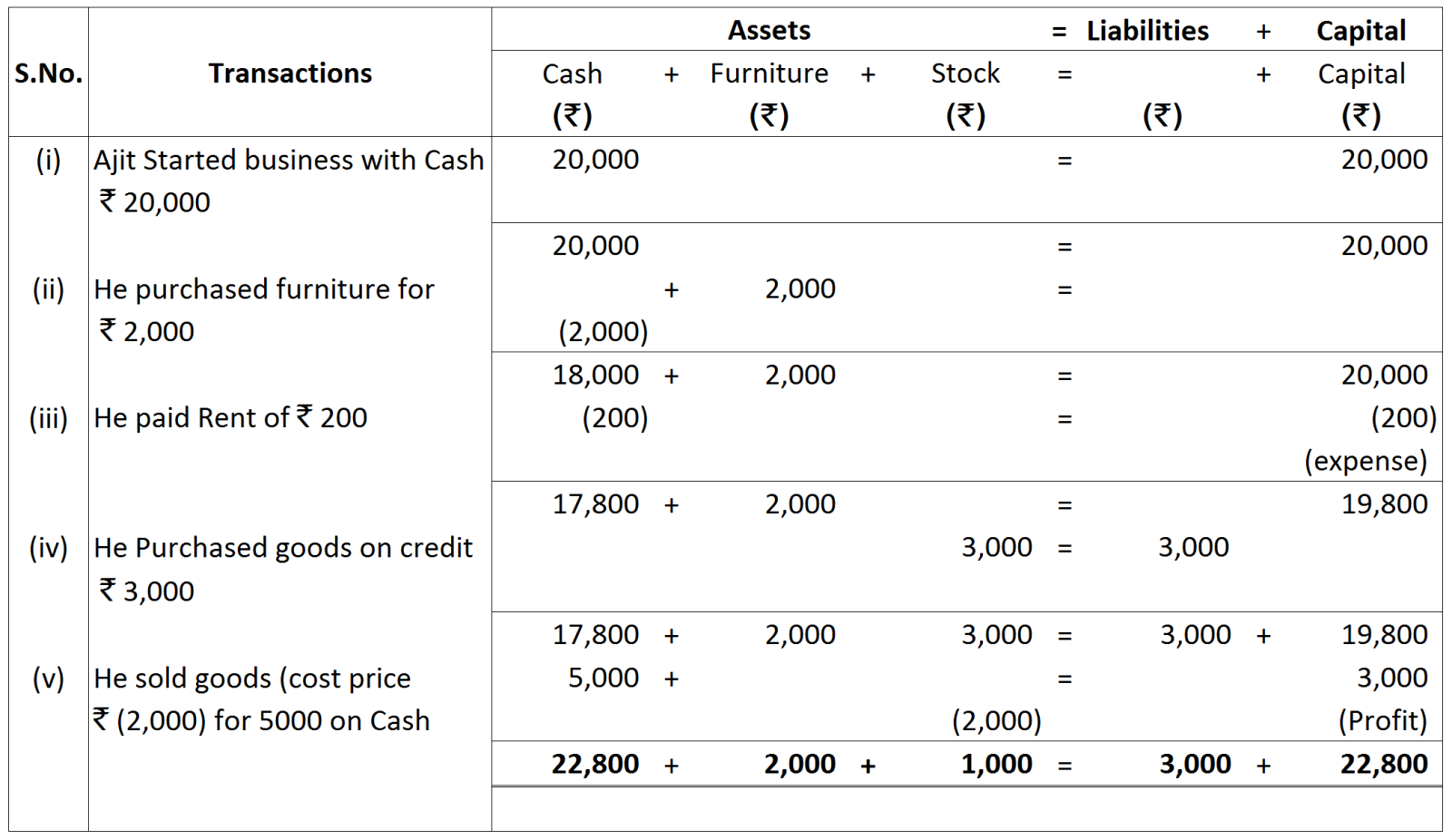

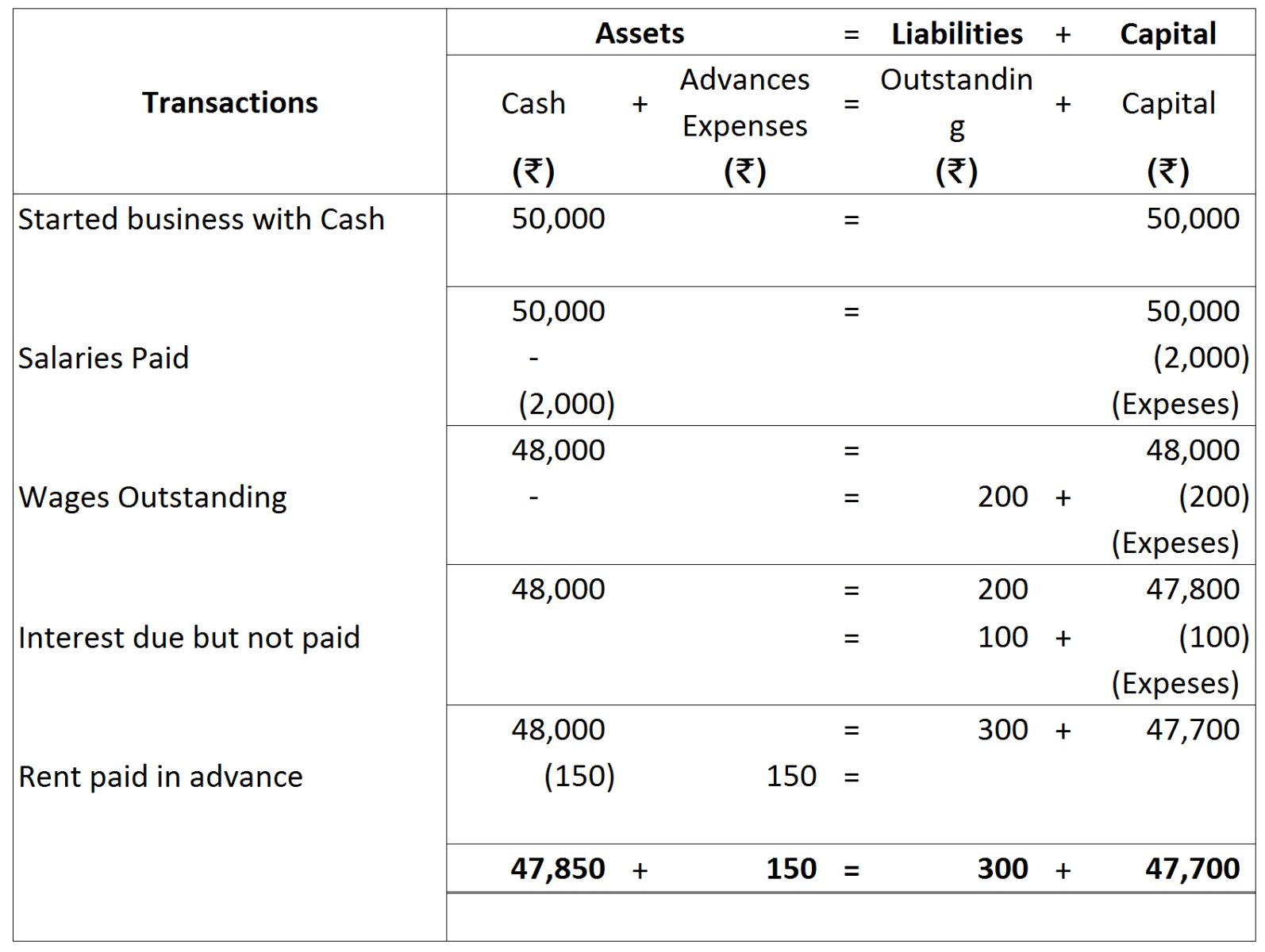

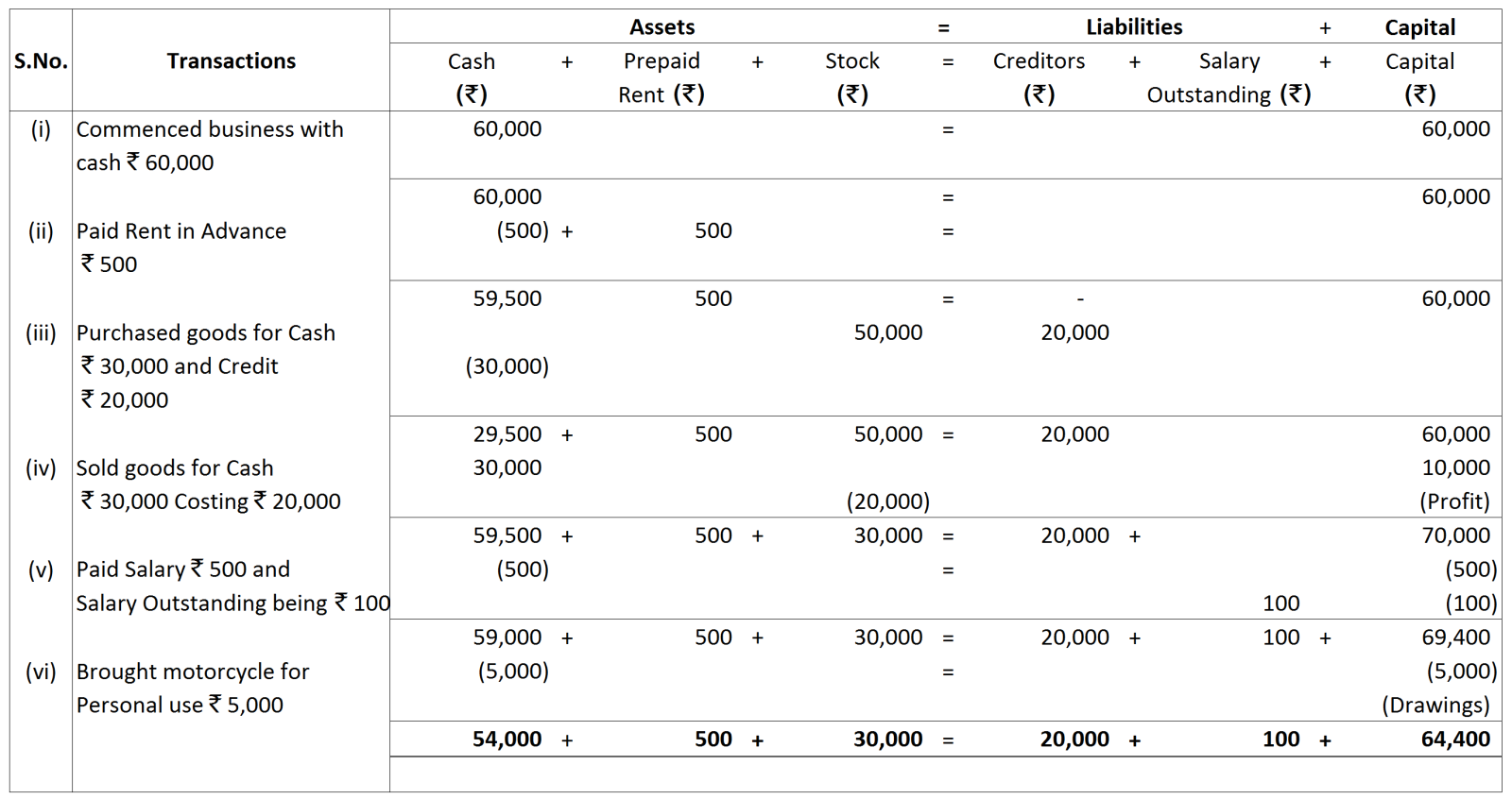

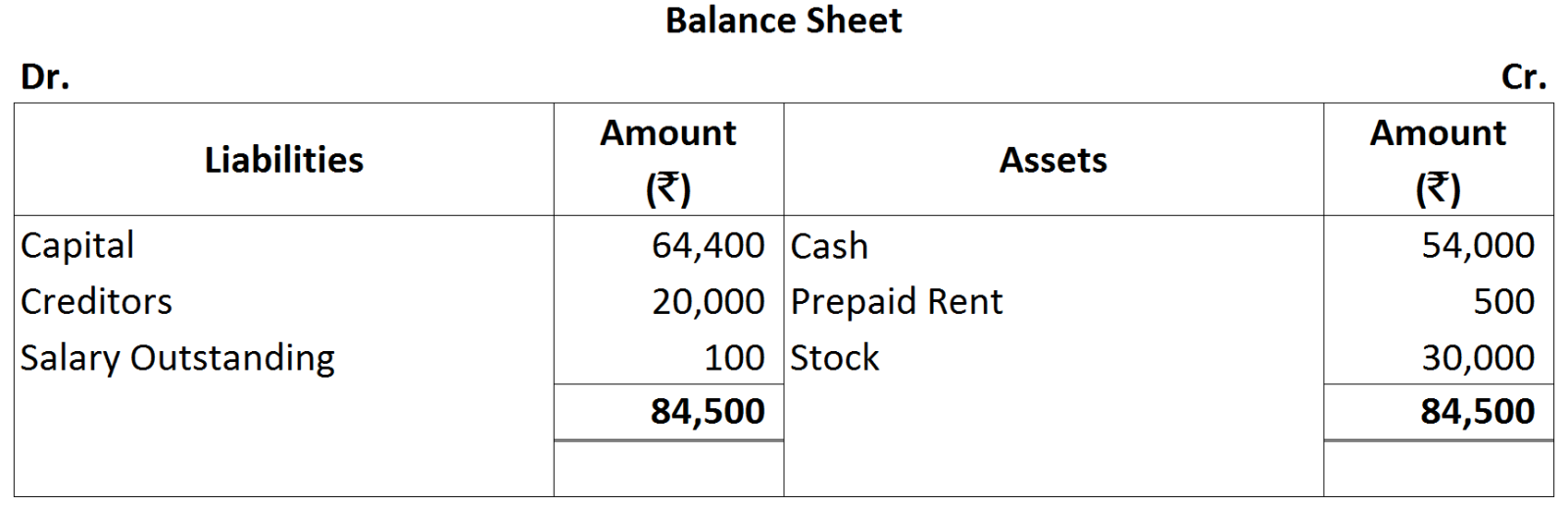

Assets = 54,000 + 500 + 30,000 = ₹ 84,500

Assets = 54,000 + 500 + 30,000 = ₹ 84,500

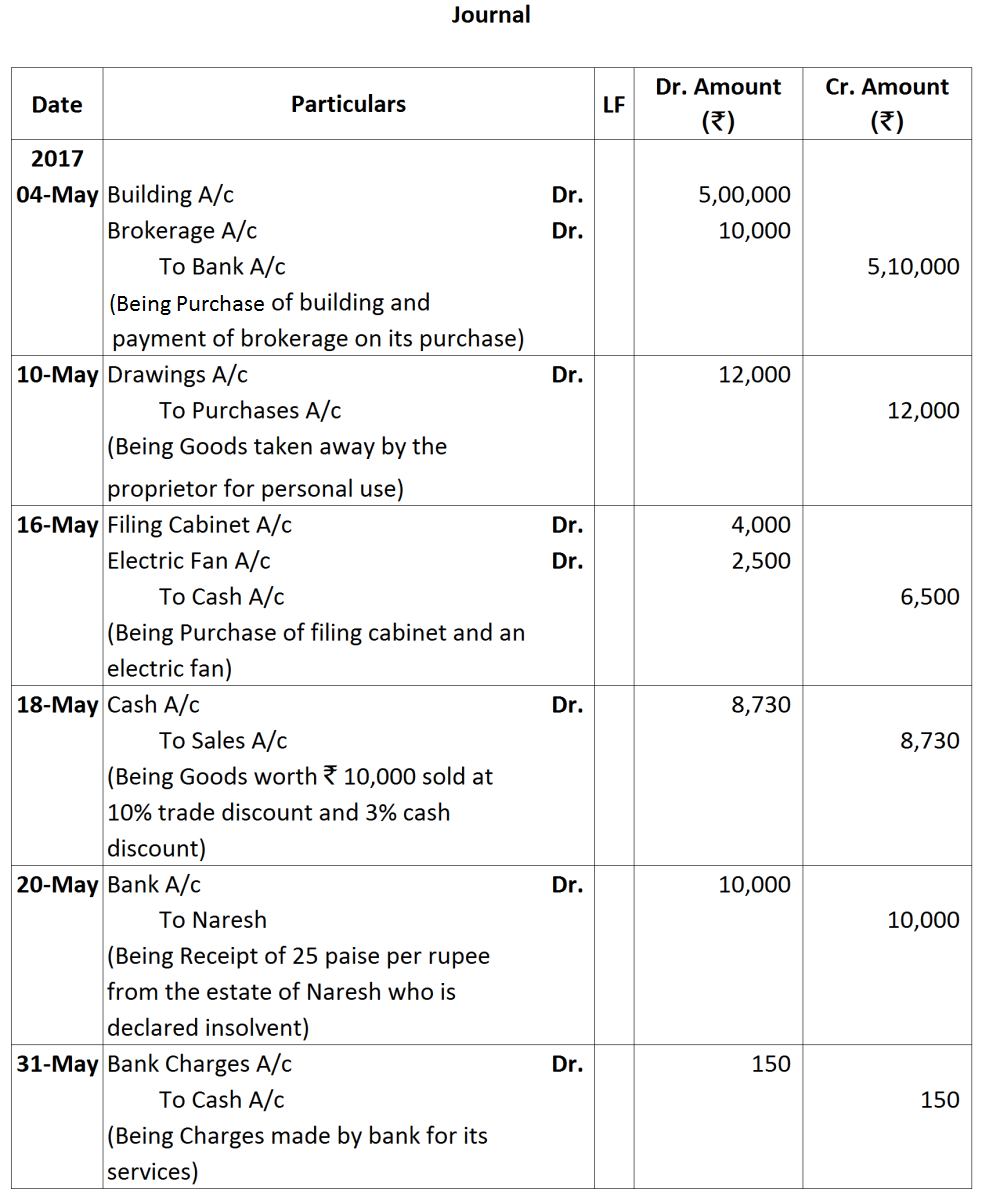

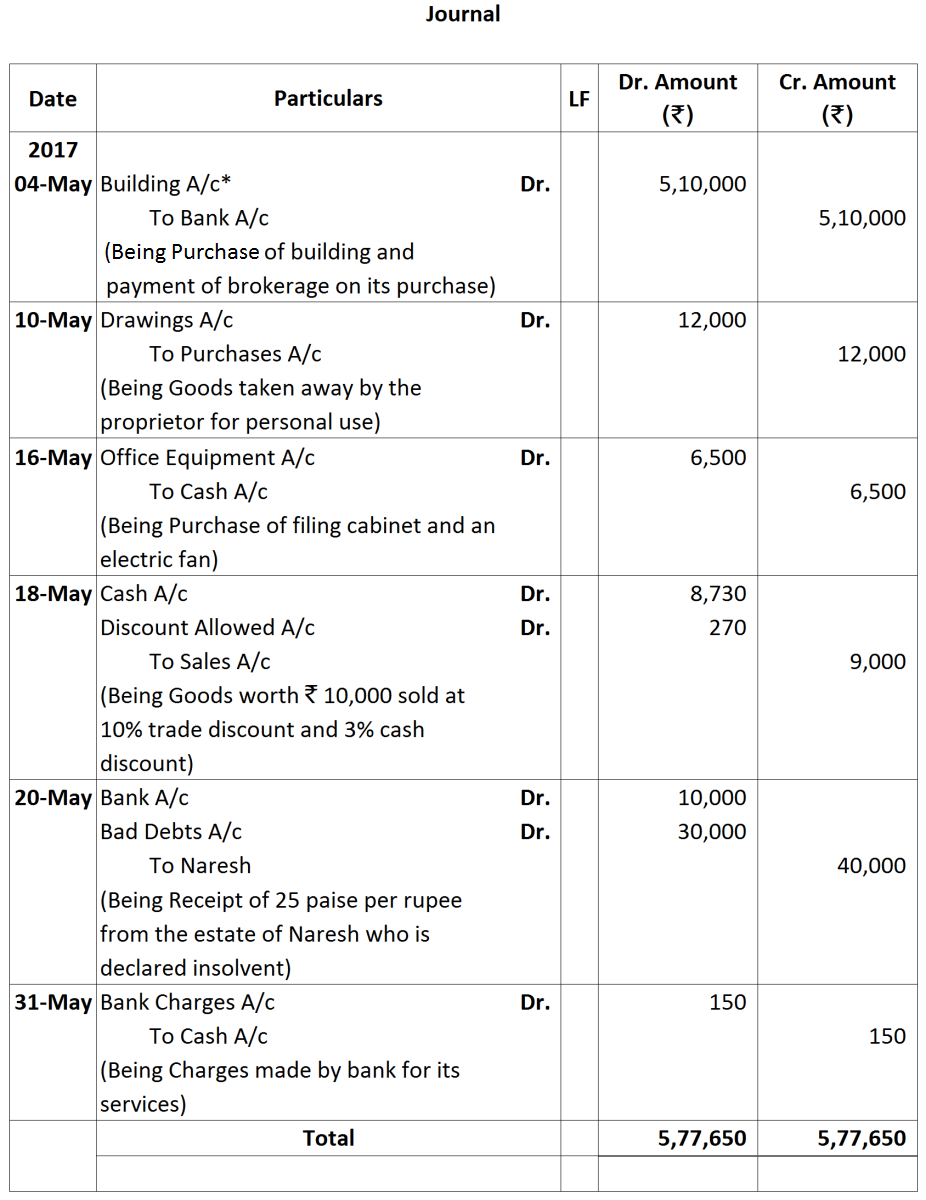

*Payment of brokerage will be included in cost of the building as it is incurred at time of purchase of building.

*Payment of brokerage will be included in cost of the building as it is incurred at time of purchase of building.