Debit originated from the Italian word debito, which in turn is derived from the Latin word debeo, which means ‘owed to proprietor’ and credit comes from the Italian word credito, which is derived from the Latin word credo, which means belief, i.e., ‘owed by proprietor’.

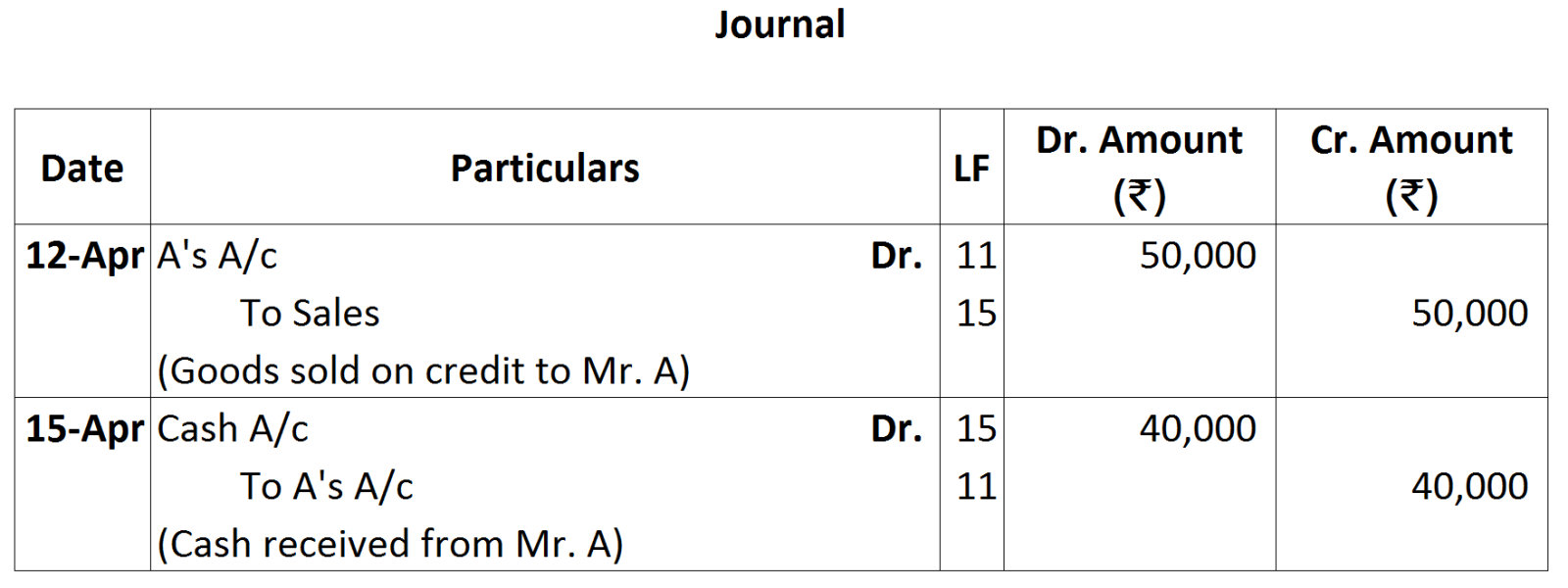

According to the dual aspect concept, all the business transactions that are recorded in the books of accounts, have two aspects- debit and credit. The dual aspect can be better understood by the help of an example; bought goods worth ₹ 500 on cash.

This transaction affects two accounts with the same amount simultaneously. As goods are brought in exchange of cash, so the cash balances in the business reduce by ₹ 500, i.e. why the cash account is credited.

Simultaneously, the amount of goods increases by ₹ 500, so purchases account will be debited. Debit and credit depend on the nature of accounts involved; such as assets, expenses, income, liabilities and capital. There are five types of Accounts.

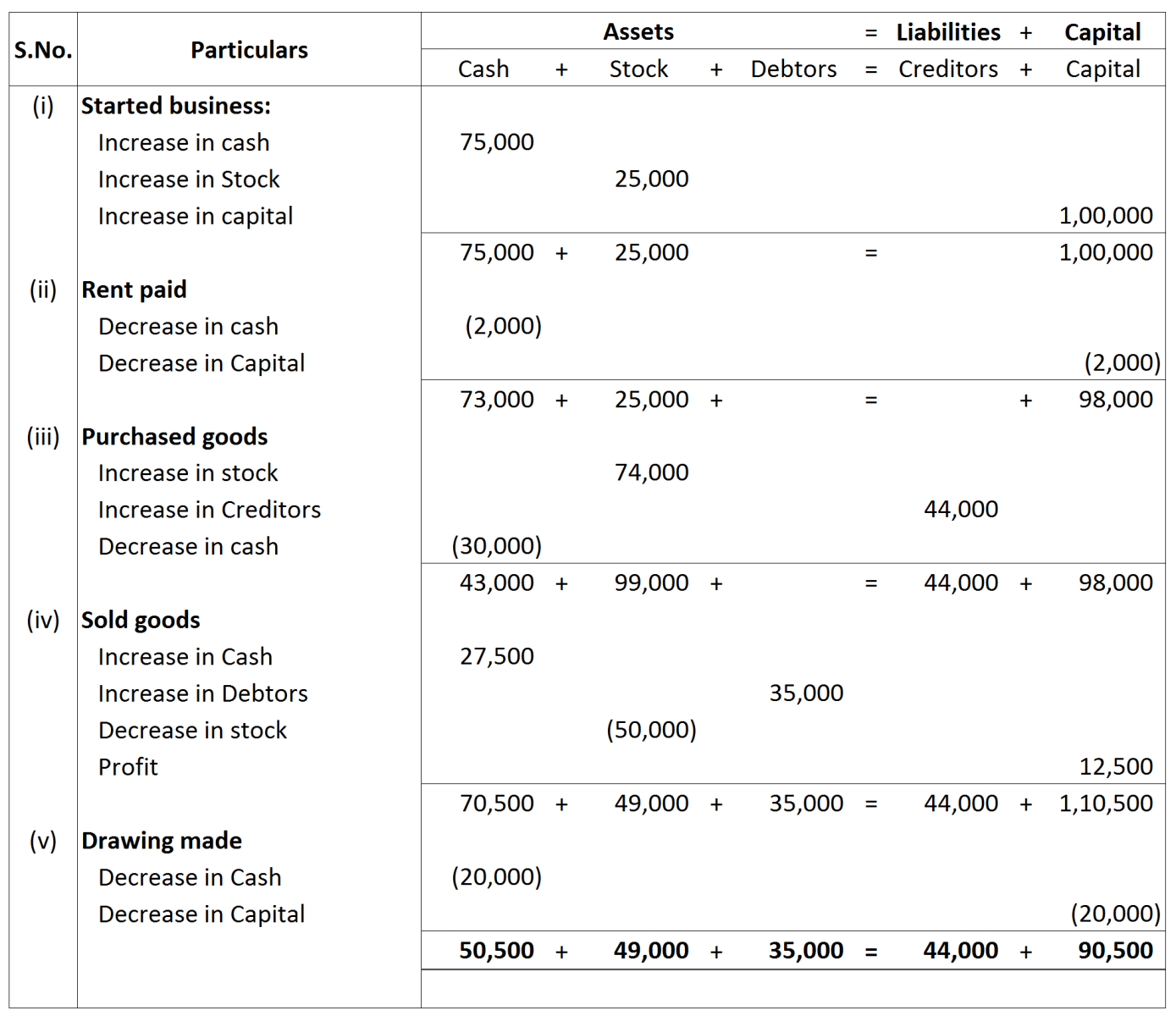

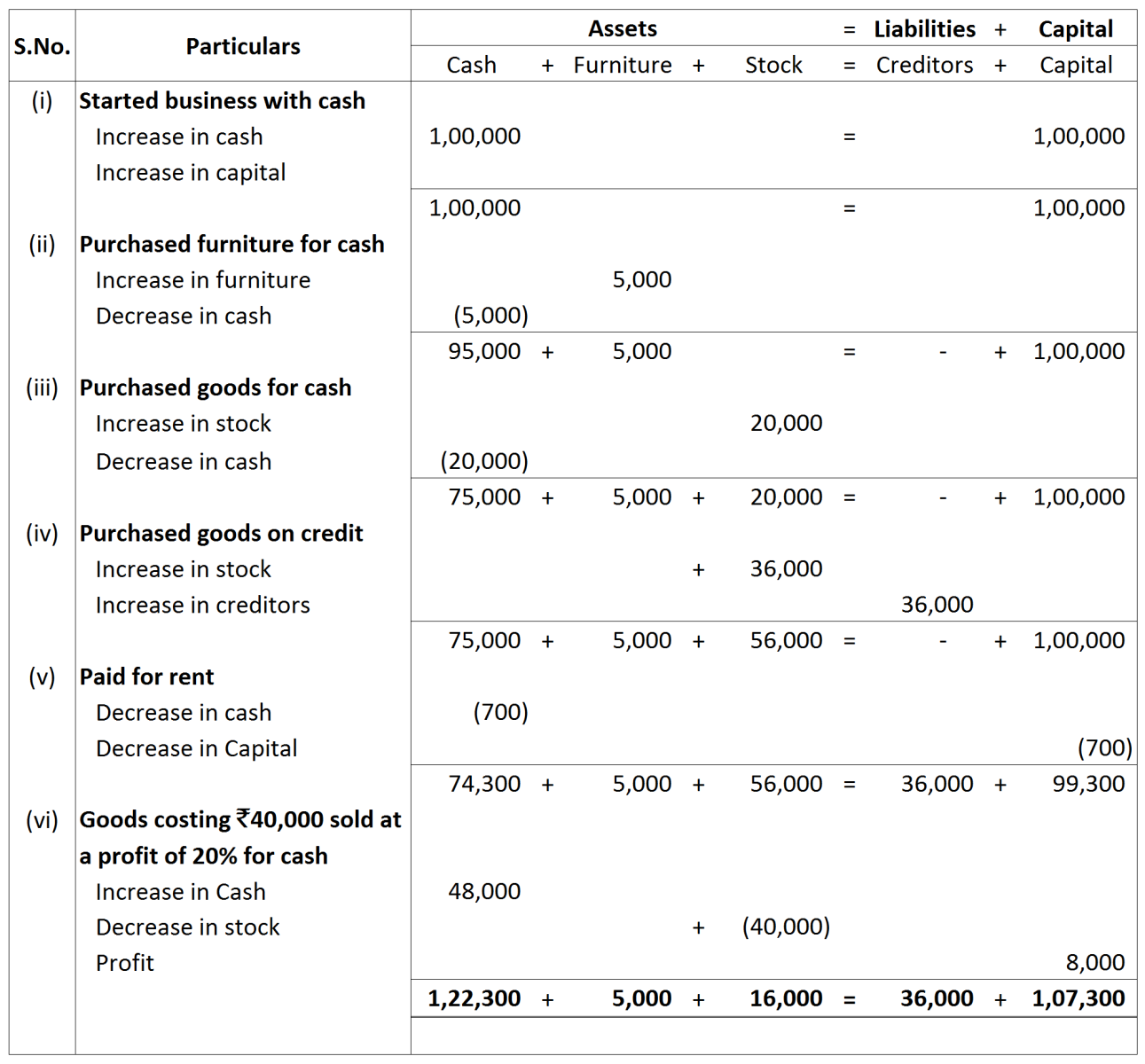

- Assets: These include all properties or legal rights owned by a firm for its operations, such as cash in hand, plant and machinery, bank, land, building, etc. All assets have debit balance. If assets increase, they are debited and if assets decrease, they are credited.

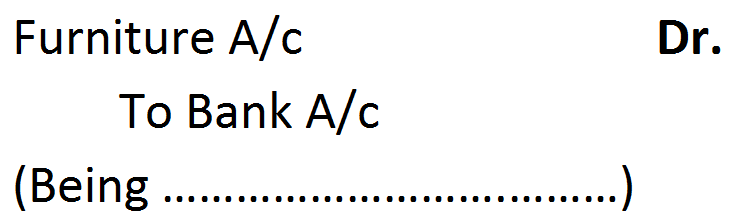

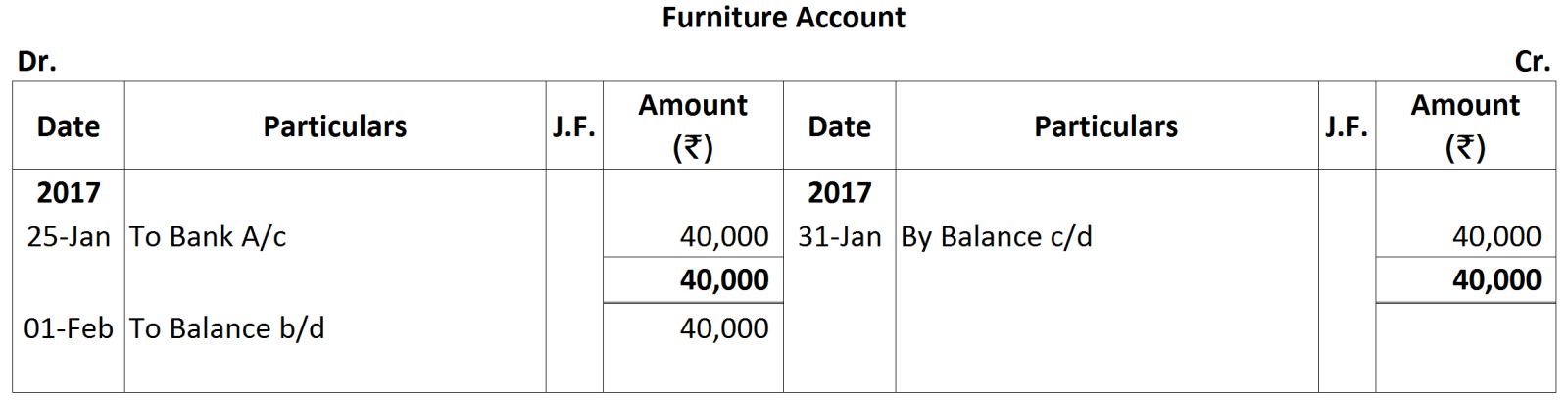

For example, furniture purchased and payment made by cheque. The journal entry is:

Here, furniture and bank balance, both are assets to the firm. As furniture is purchased, so furniture account will increase, and will be debited. On the other hand, payment of furniture is being made by cheque that reduces the bank balance of the business, so bank account will be credited.

- Expense: It is made to run business smoothly and to carry day to day business activites.

All expenses have debit balance. If an expense is incurred, it must be debited.

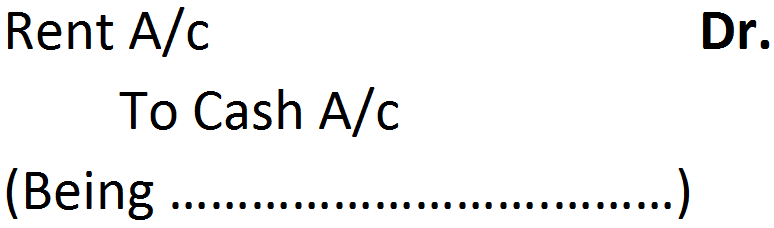

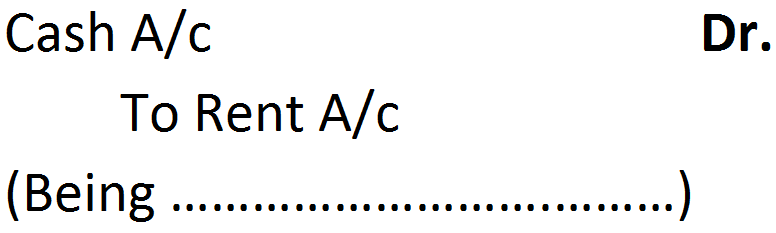

For example, rent paid. The journal entry is:

Here, rent is an expense. All expenses have debit balance. Hence, rent is debited. On the other hand, as rent is paid in cash that reduces the cash balances, so cash account is credited.

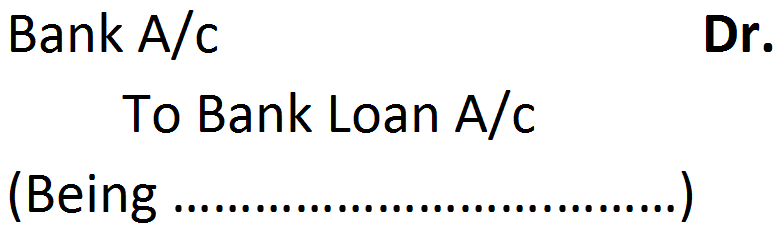

- Liability: Liability is an obligation of business. Increase in liability is credited and decrease in liability is debited.

For example, loan taken from bank. The journal entry is:

Here, loan from bank is a liability to the firm. As all liabilities have credit balance, so loan from bank has been credited because it increases the liabilities.

- Income: Income means profit earned during an accounting period from any source. Income also means excess of revenue over its cost during an accounting period. Income has credit balance because it increases the balance of capital.

For example, rent received from tenant. The journal entry is:

Here, rent is an income; hence, rent account has been credited and cash has been debited, as rent received increases the cash balances.

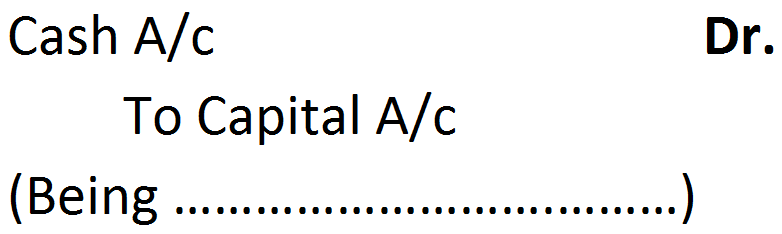

- Capital: Capital is the amount invested by the proprietor in the business. Capital has credit balance. Increase in capital is credited and decrease in capital is debited

For example, additional capital introduced by owner. The journal entry is:

As additional capital is introduced, so the amount of capital will increase, i.e. why, capital account is credited. On the other hand, as capital is introduced in form of cash, so the cash balances decrease, i.e. why, cash account is debited.

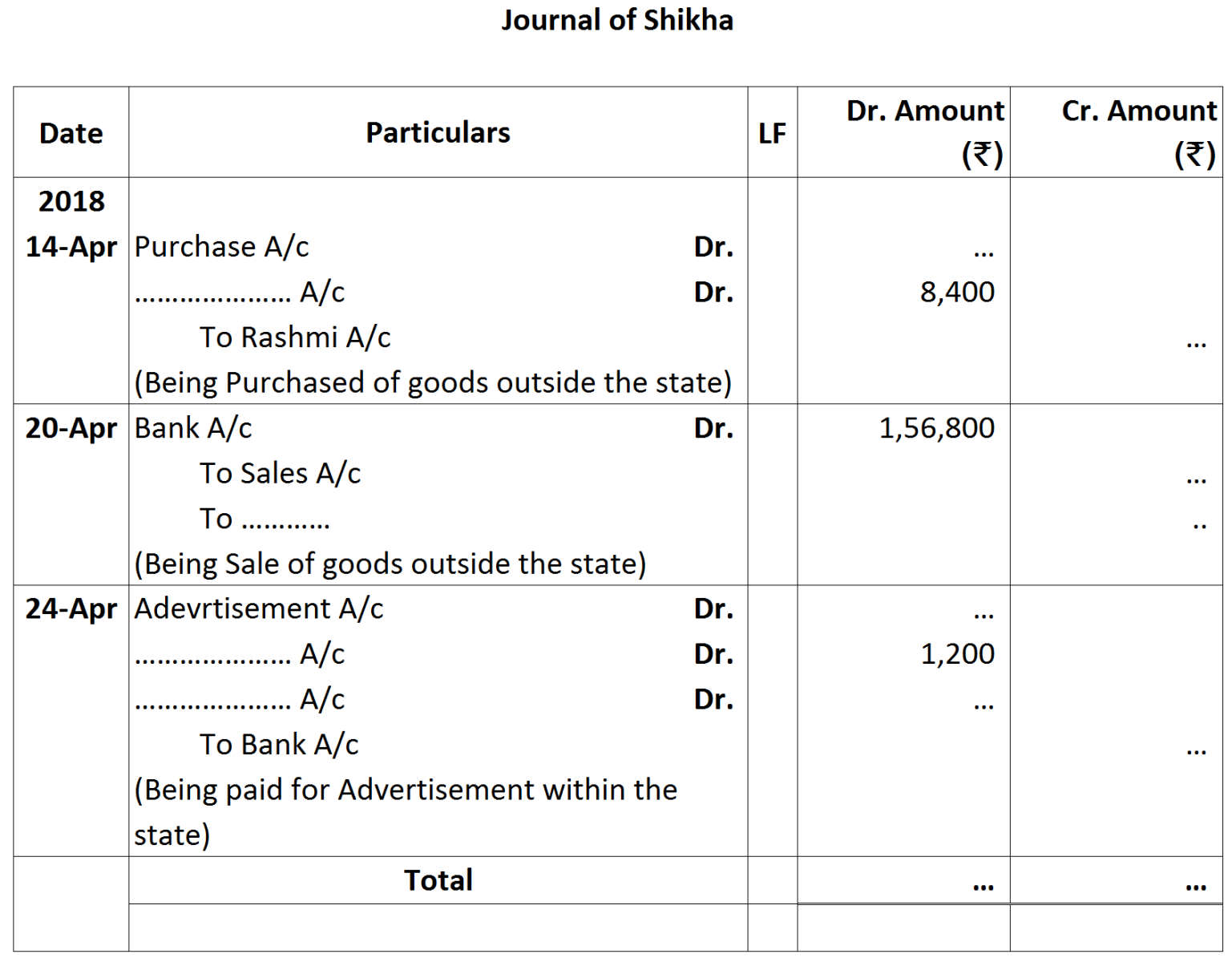

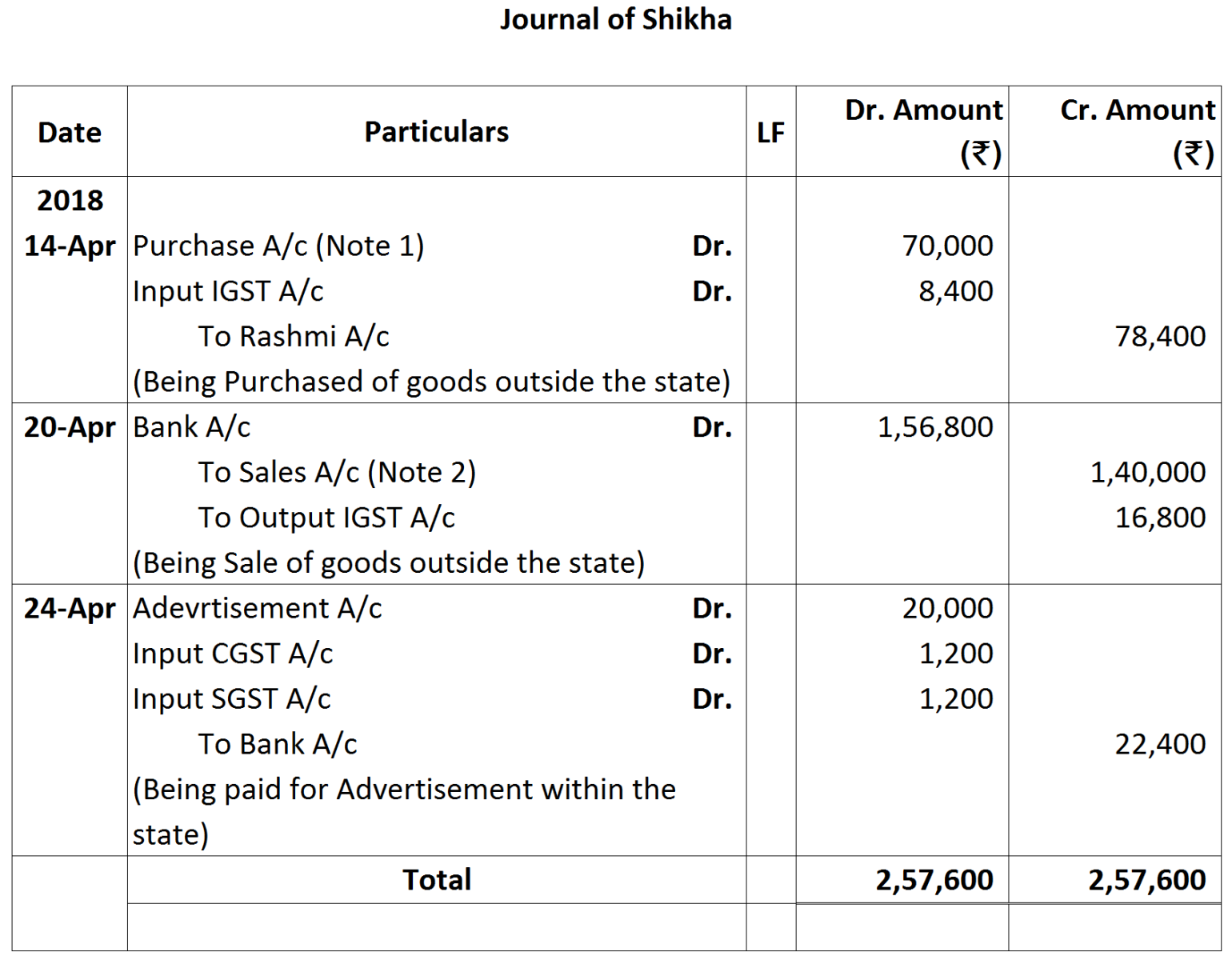

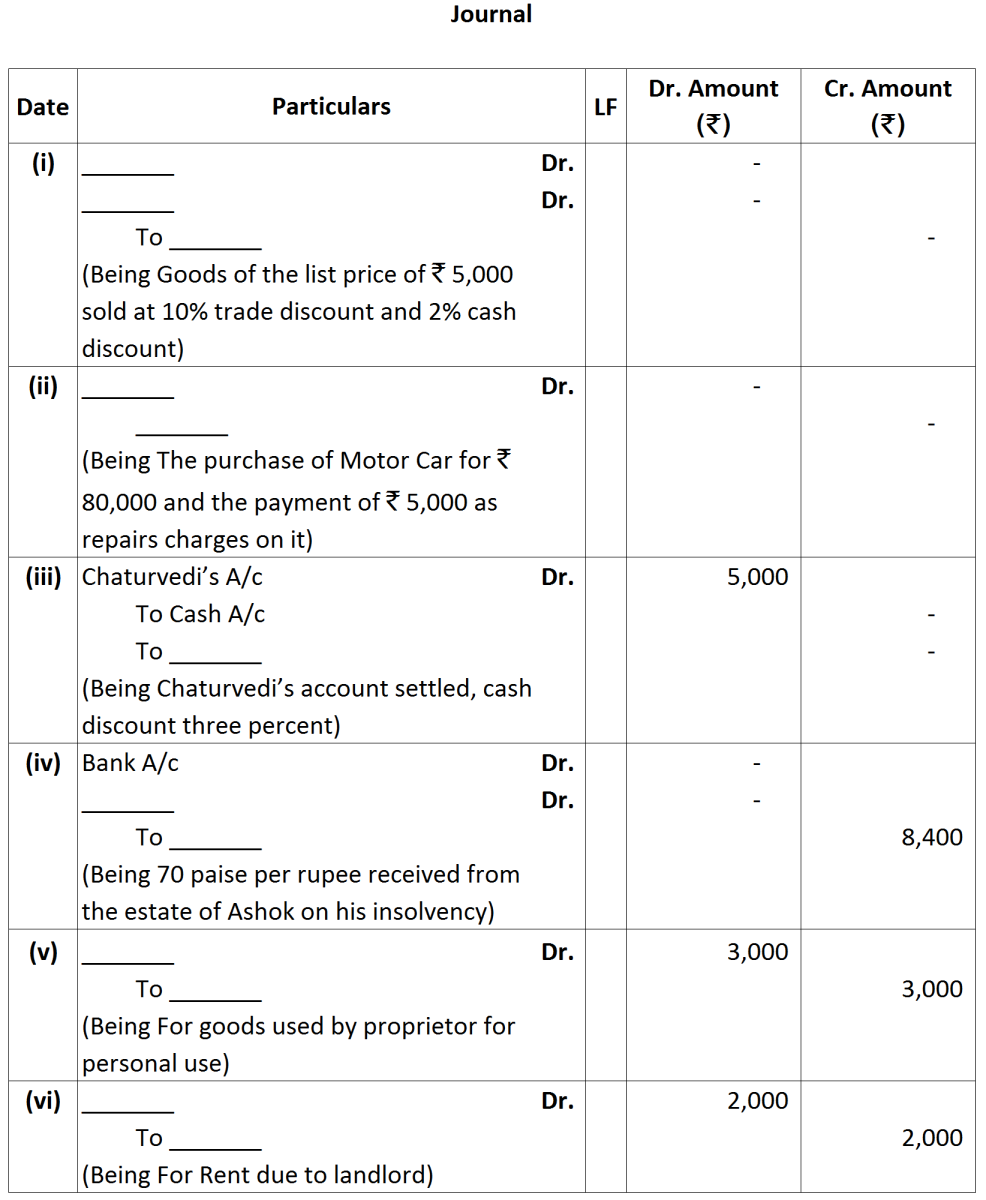

$8,400\times\frac{100}{12}=₹\ 70,000$

$8,400\times\frac{100}{12}=₹\ 70,000$

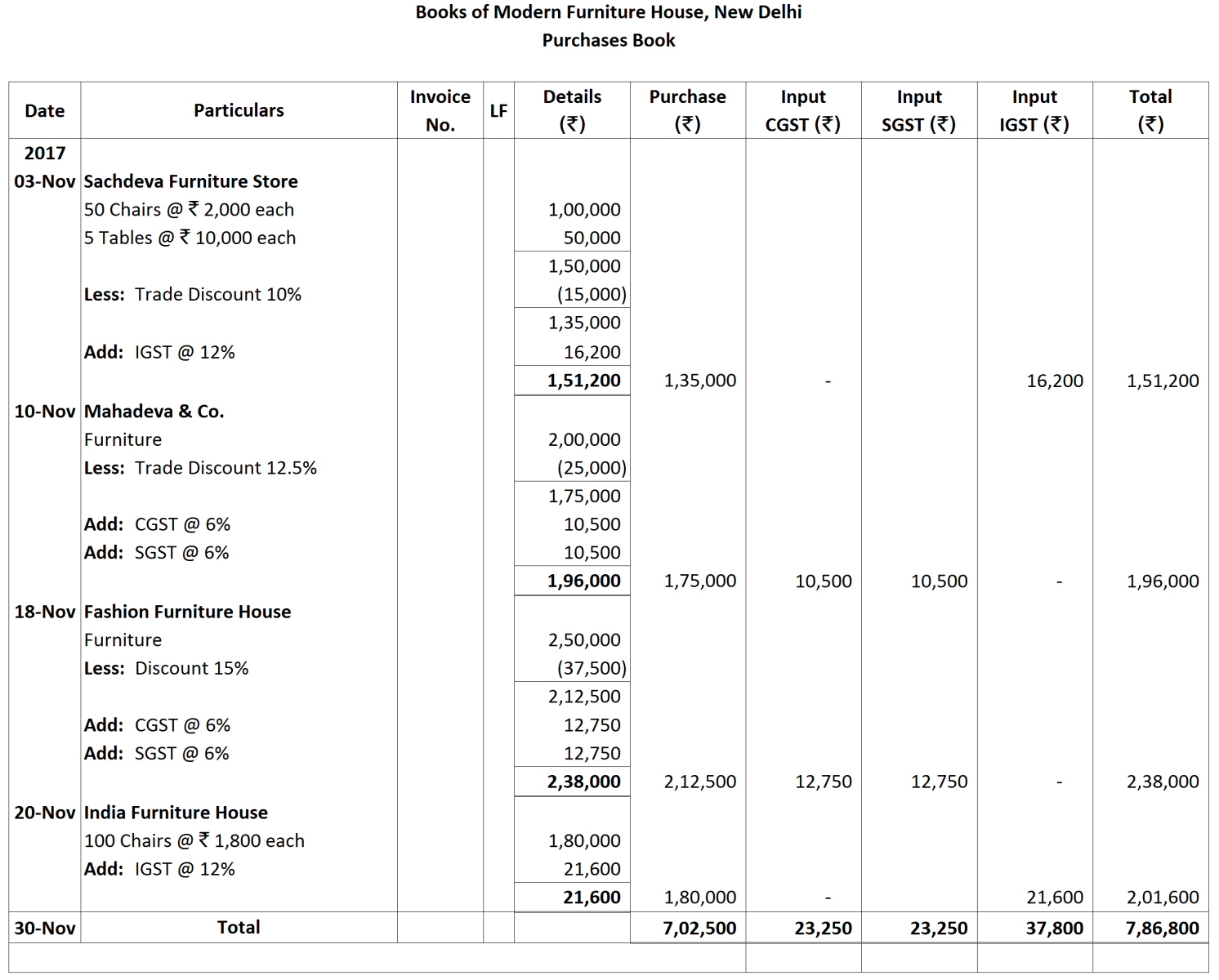

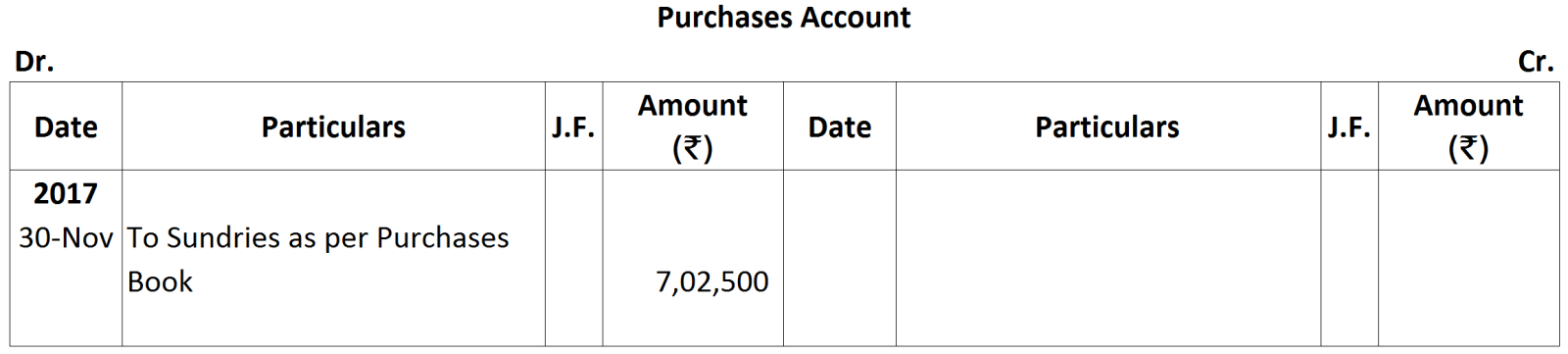

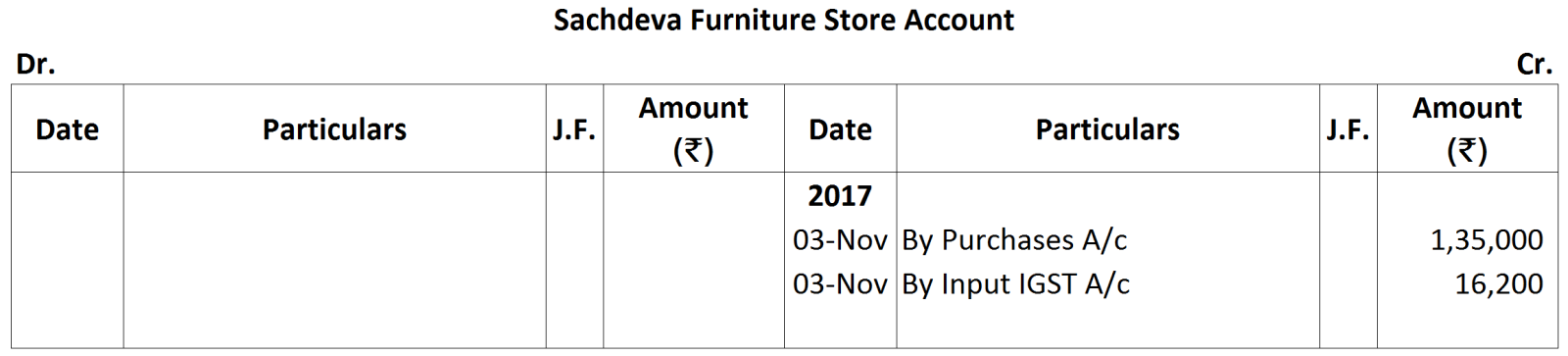

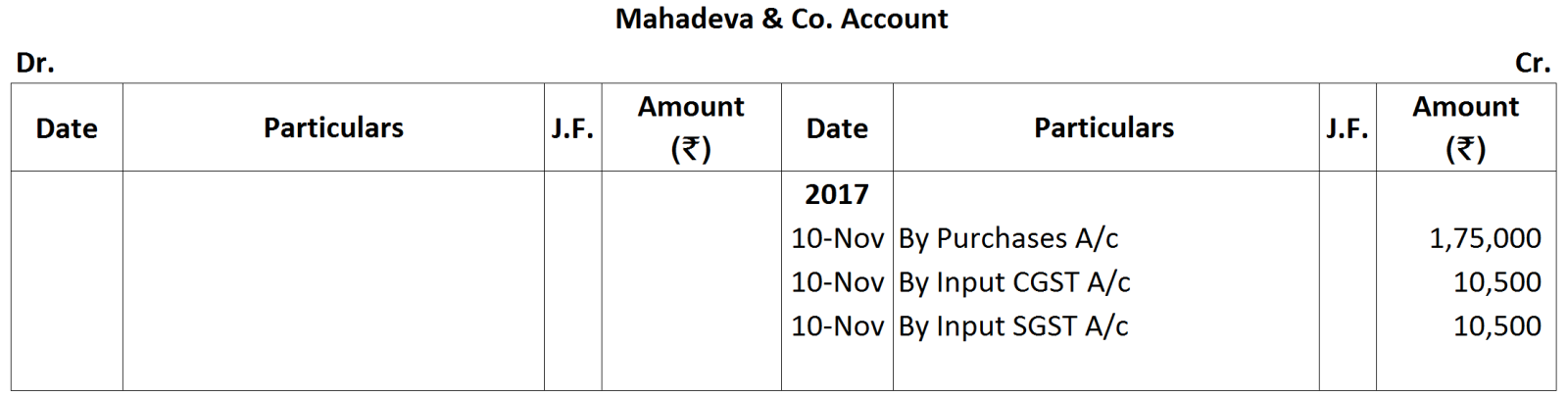

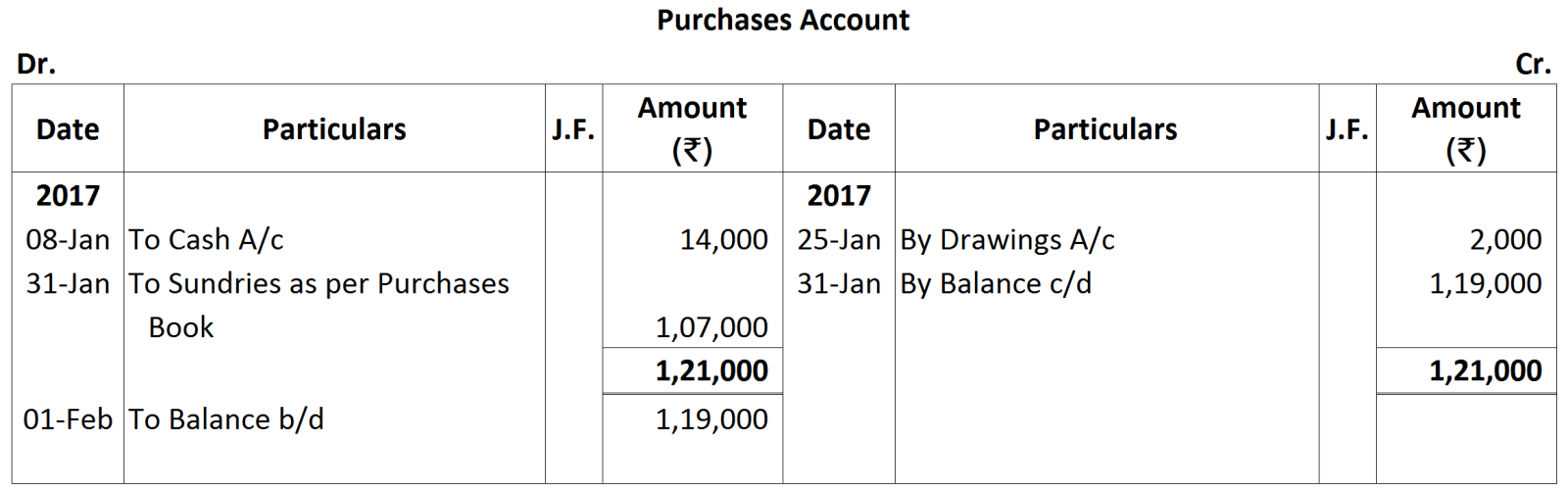

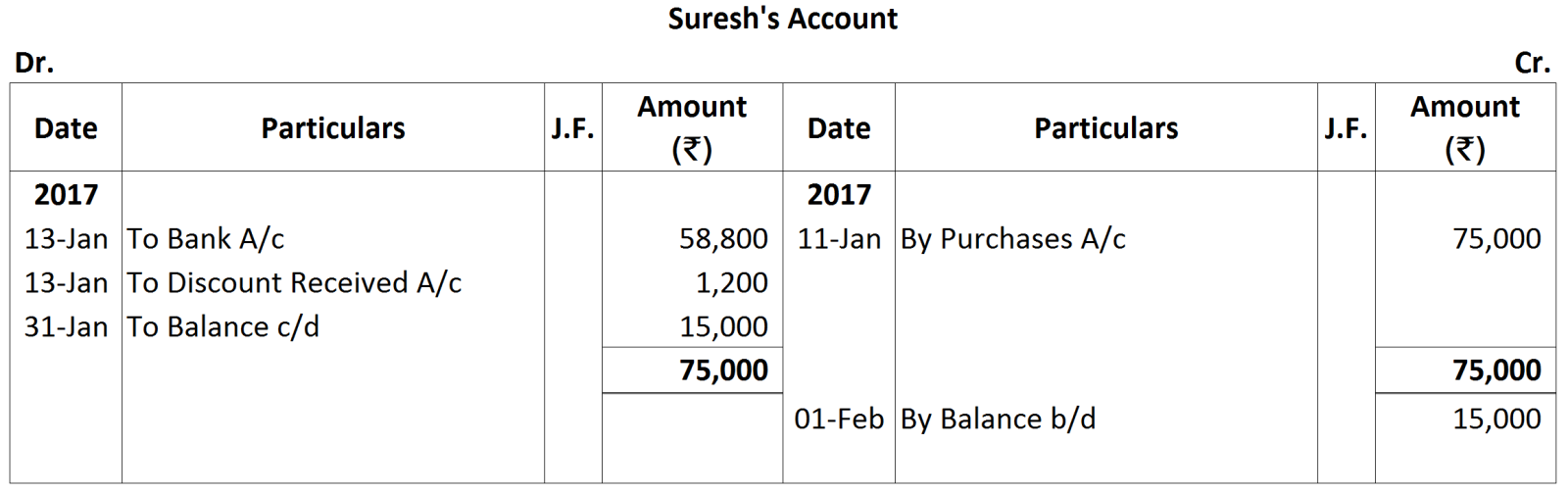

Working Note:

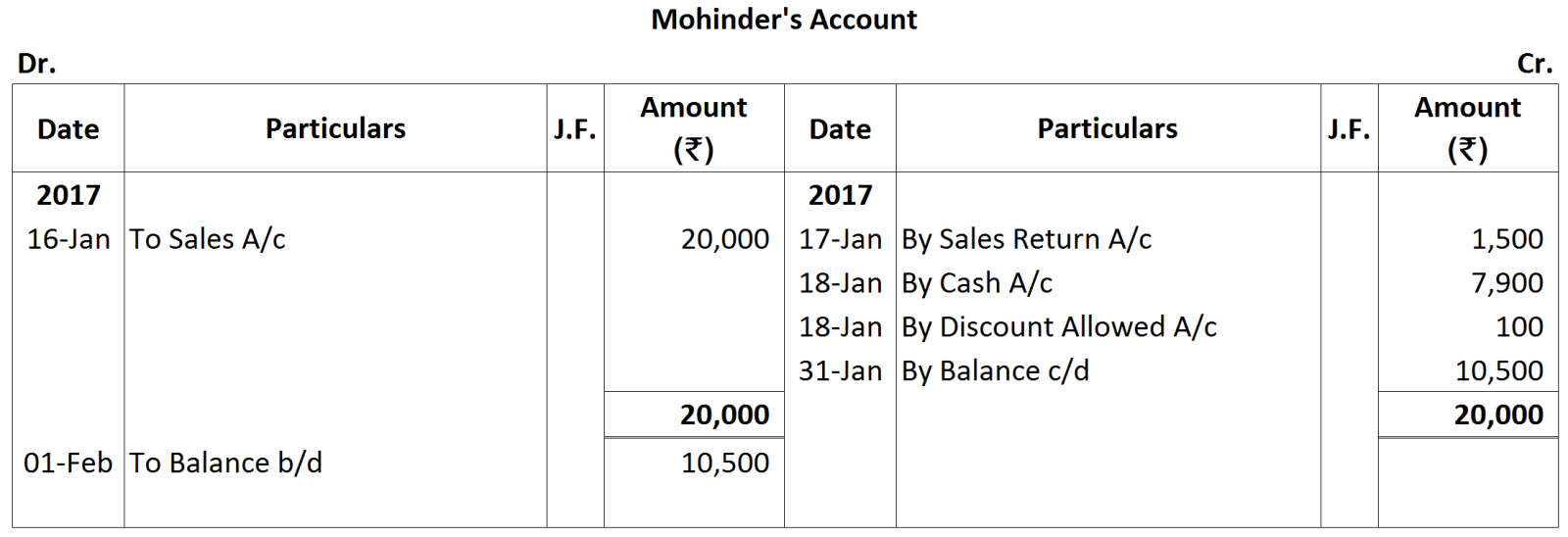

Working Note:

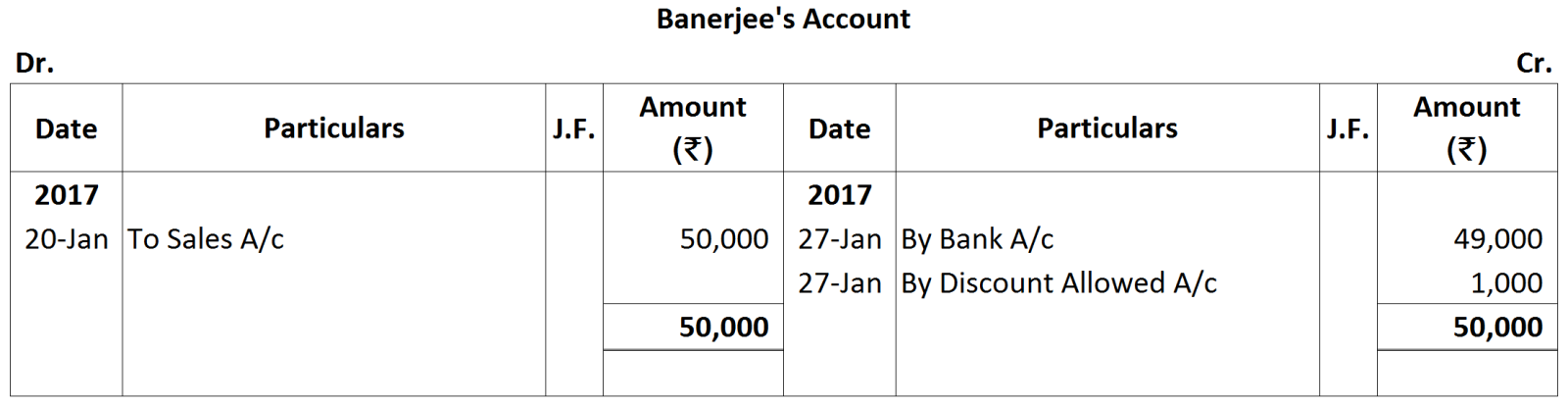

Working Note:

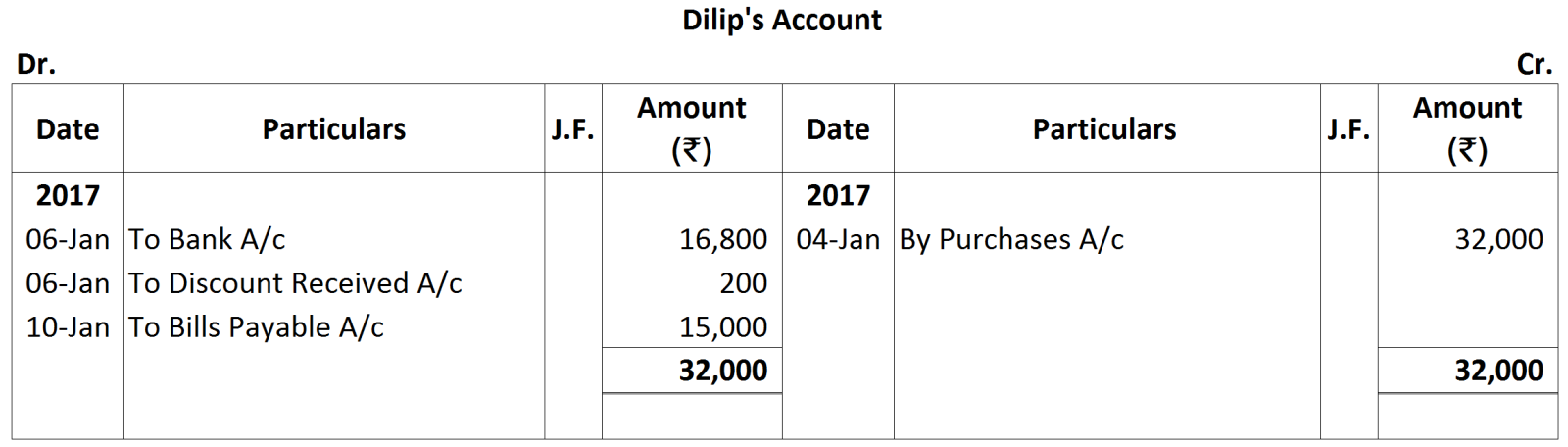

Working Note:

Working Note:

Working Note:

Working Note:

Working Note: