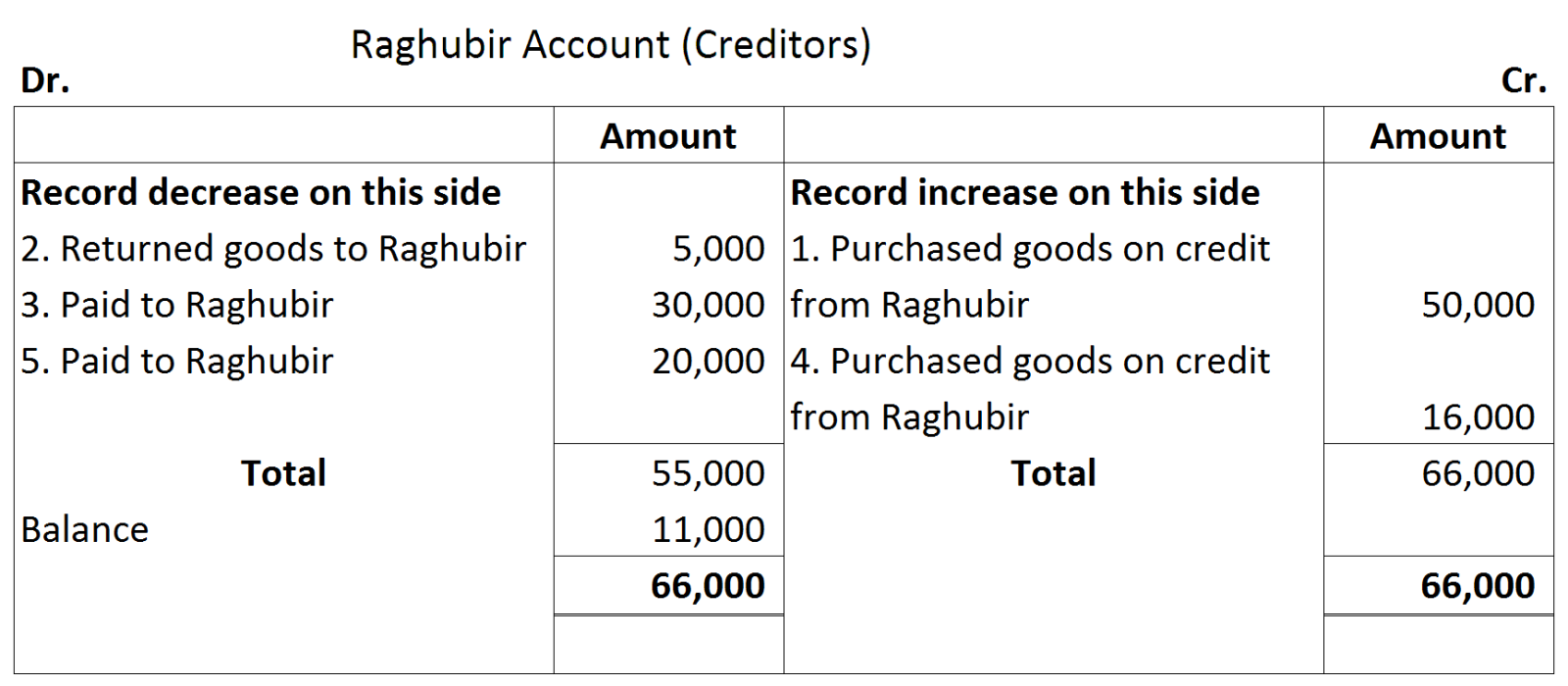

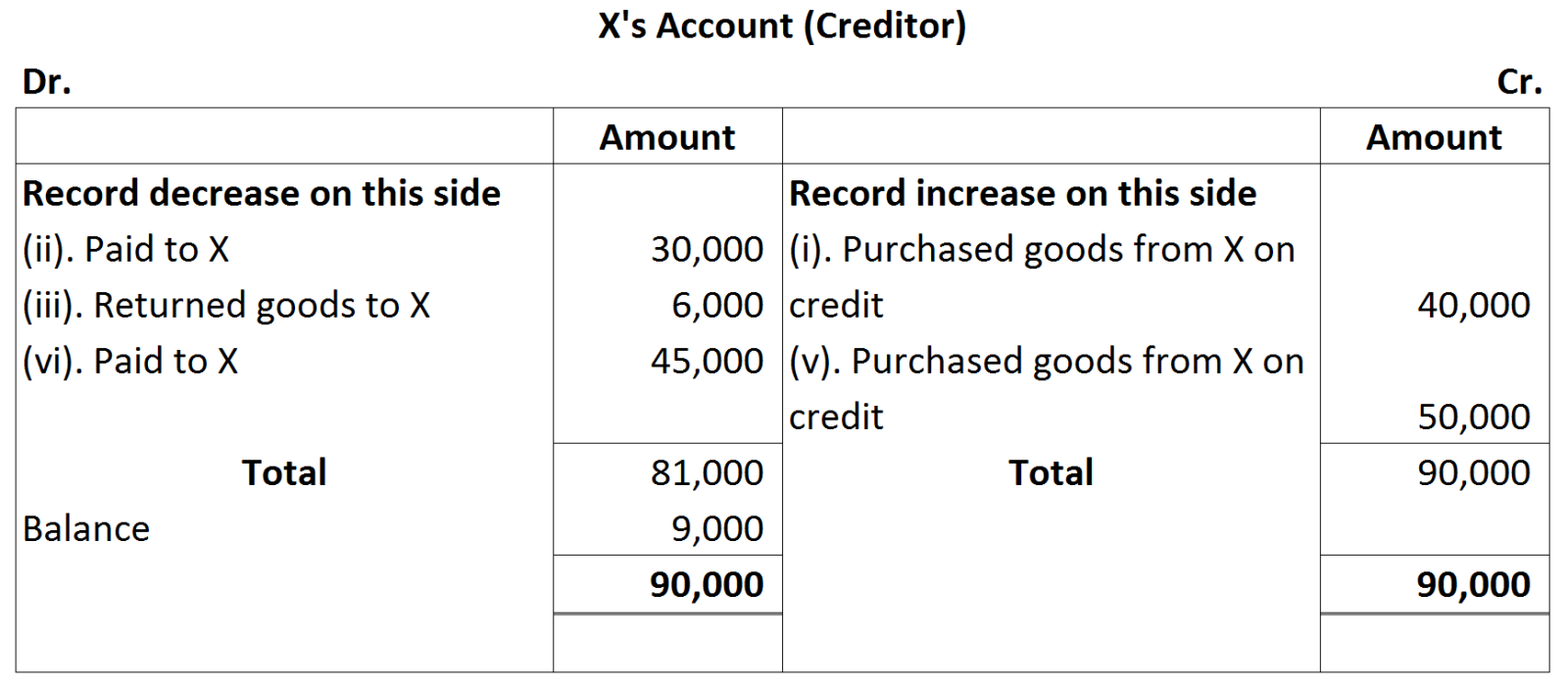

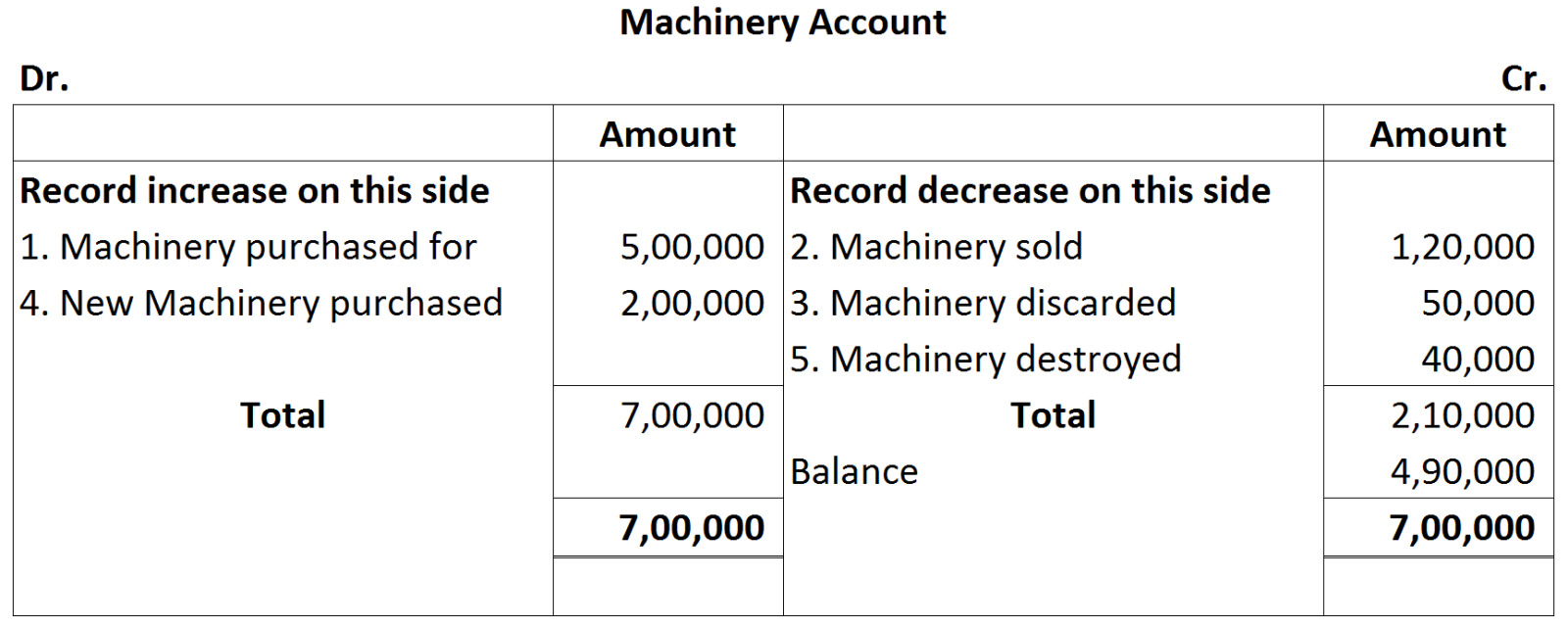

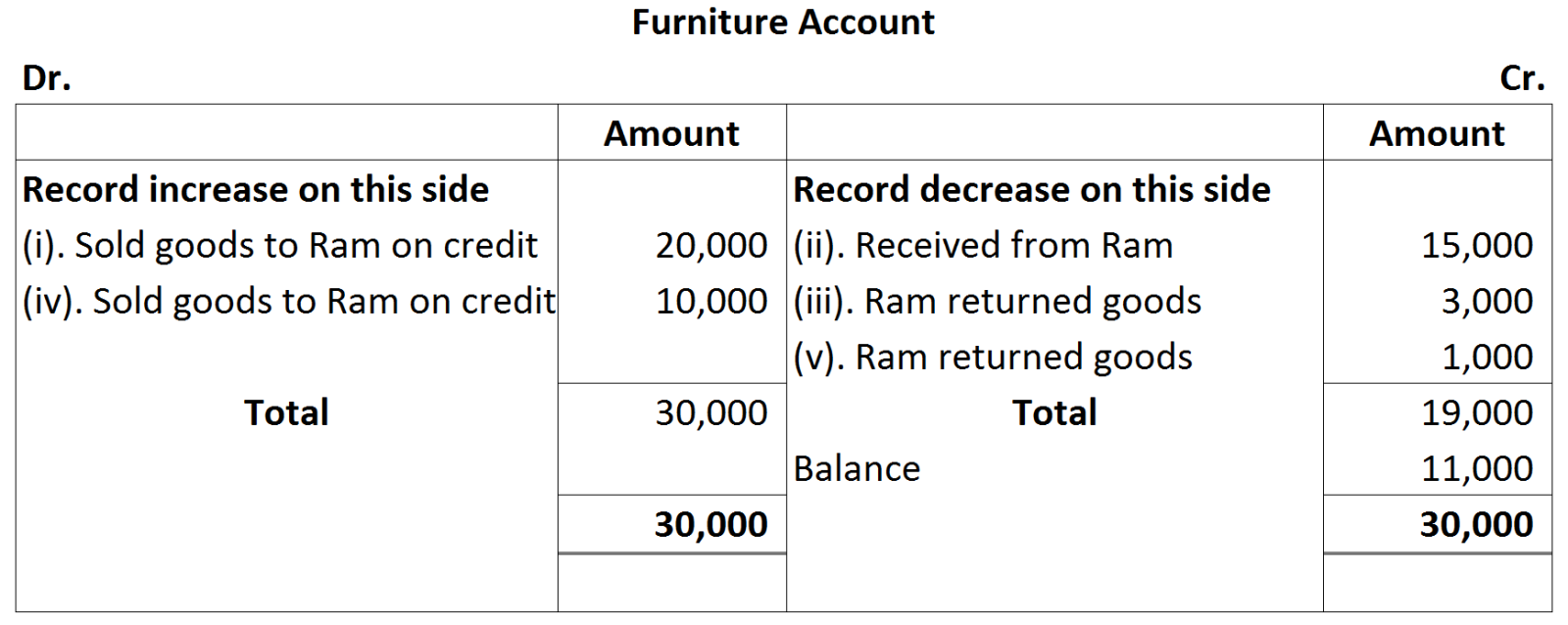

Question 13 Marks

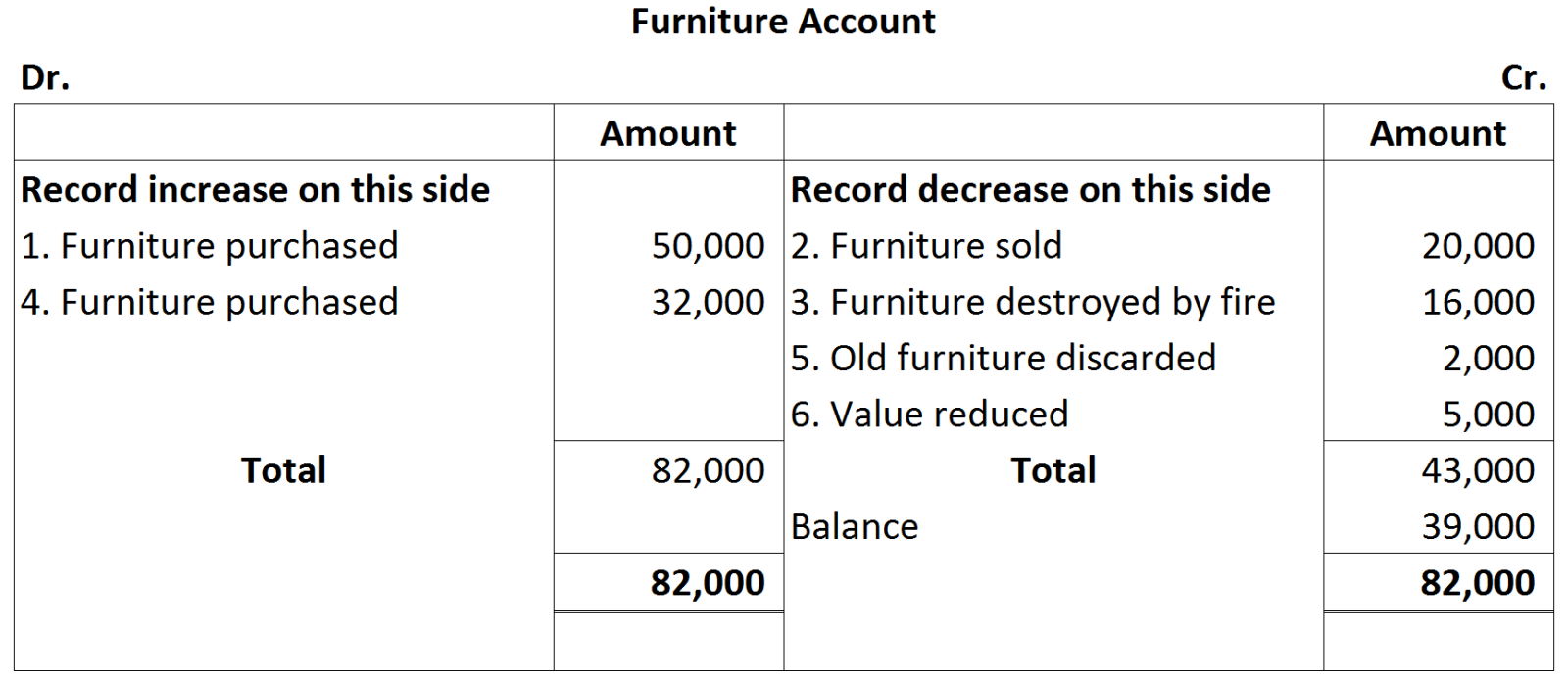

Write a short note on 'balancing an account'. Explain by balancing a Cash Account.

Answer

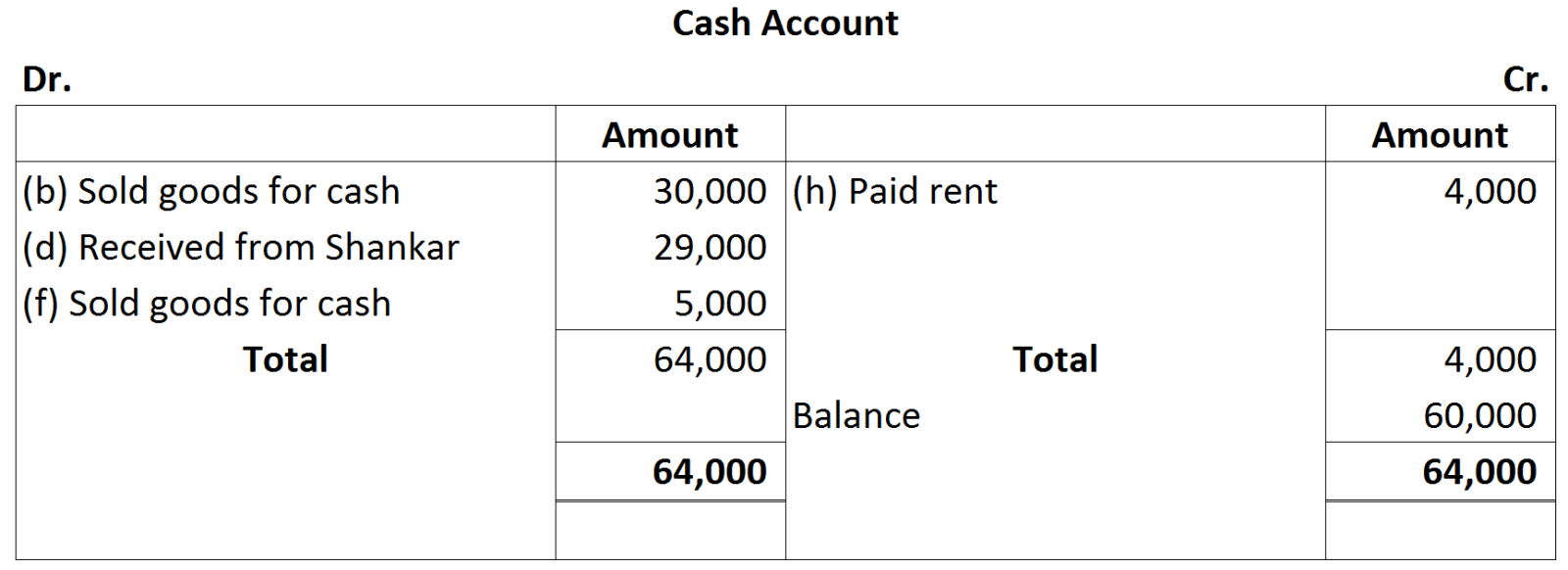

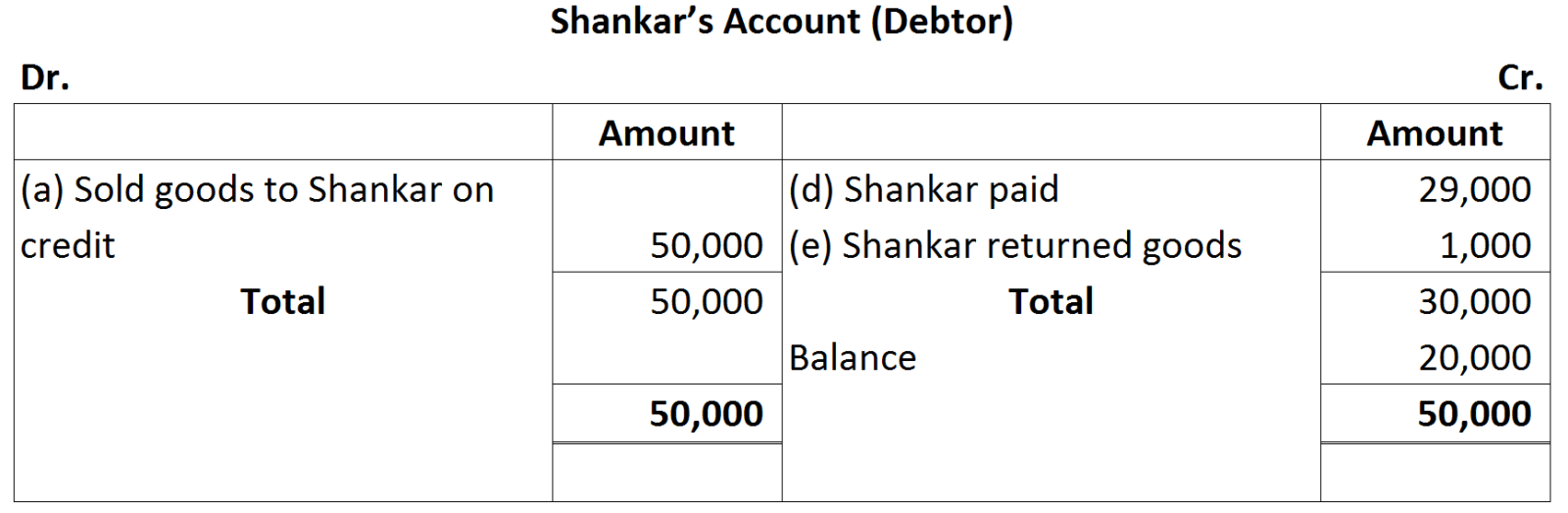

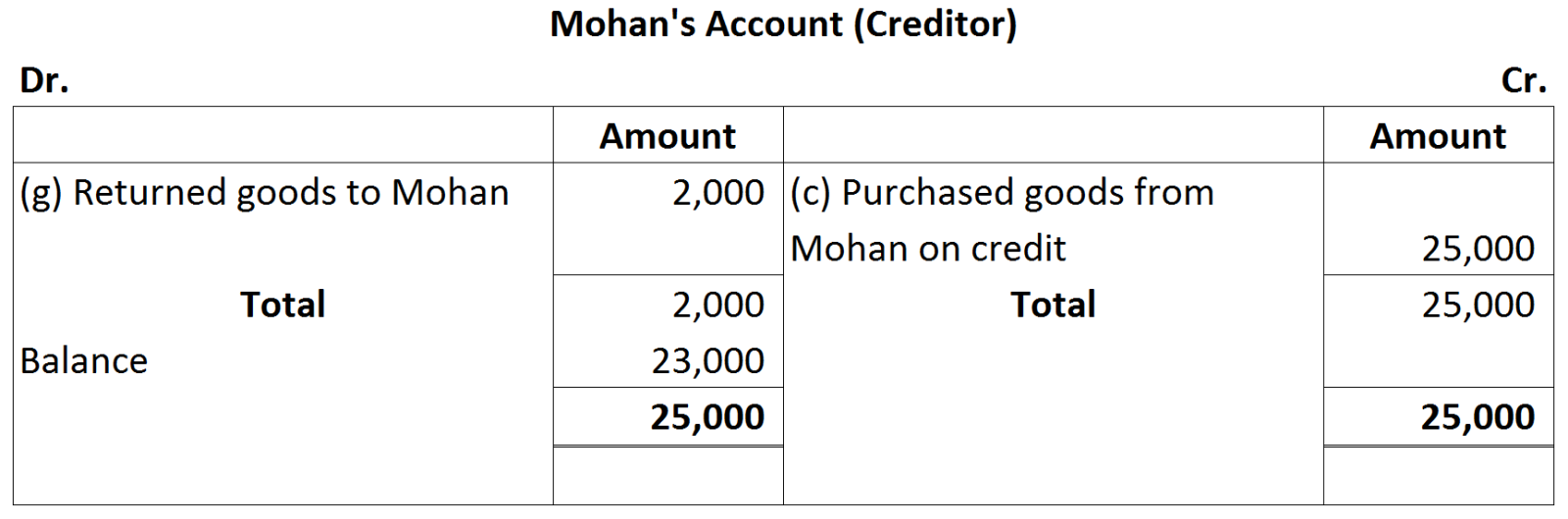

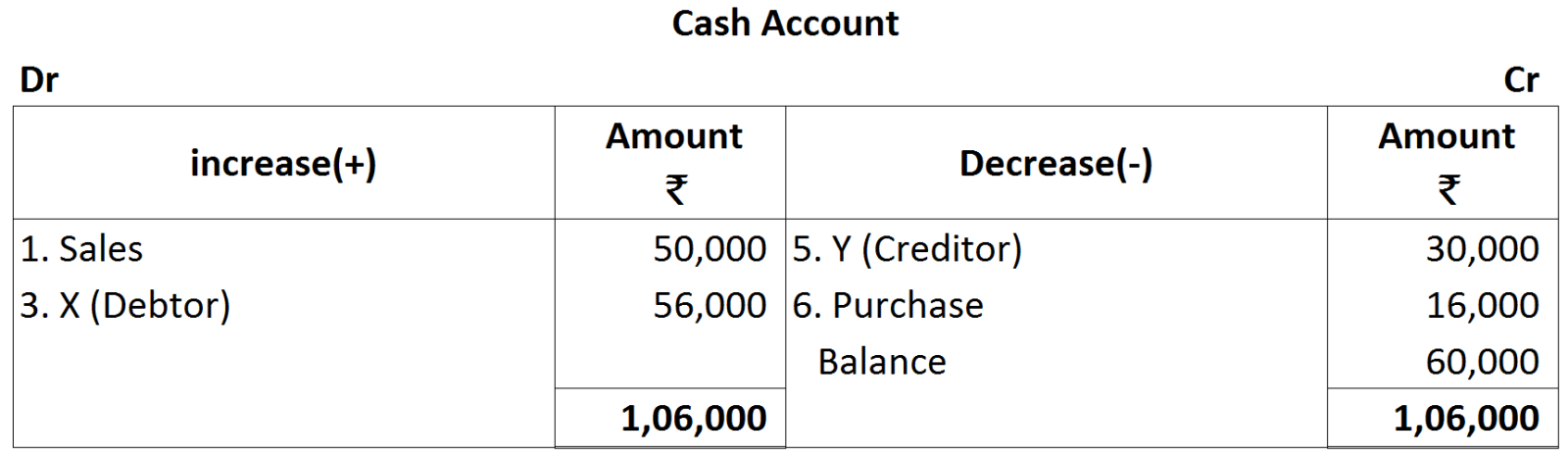

View full question & answer→A balance of an account is the difference between the total of its debit and credit sides. If the total of debit side is more than the total of credit side, the account is said to have a debit balance. It has a credit balance when total of credit side is more than the total of debit side. Balancing a Cash Account.

| ₹ | ₹ | ||||

| 1. | Cash sales | 50,000 | 2. | Sold goods to X on credit | 80,000 |

| 3. | Cash received from X | 56,000 | 4. | Purchased goods from Y on credit | 44,000 |

| 5. | Paid to Y | 30,000 | 6. | Cash purchases from Y | 16,000 |

$15,000\times\frac{100}{6}=₹\ 2,50,000$

$15,000\times\frac{100}{6}=₹\ 2,50,000$