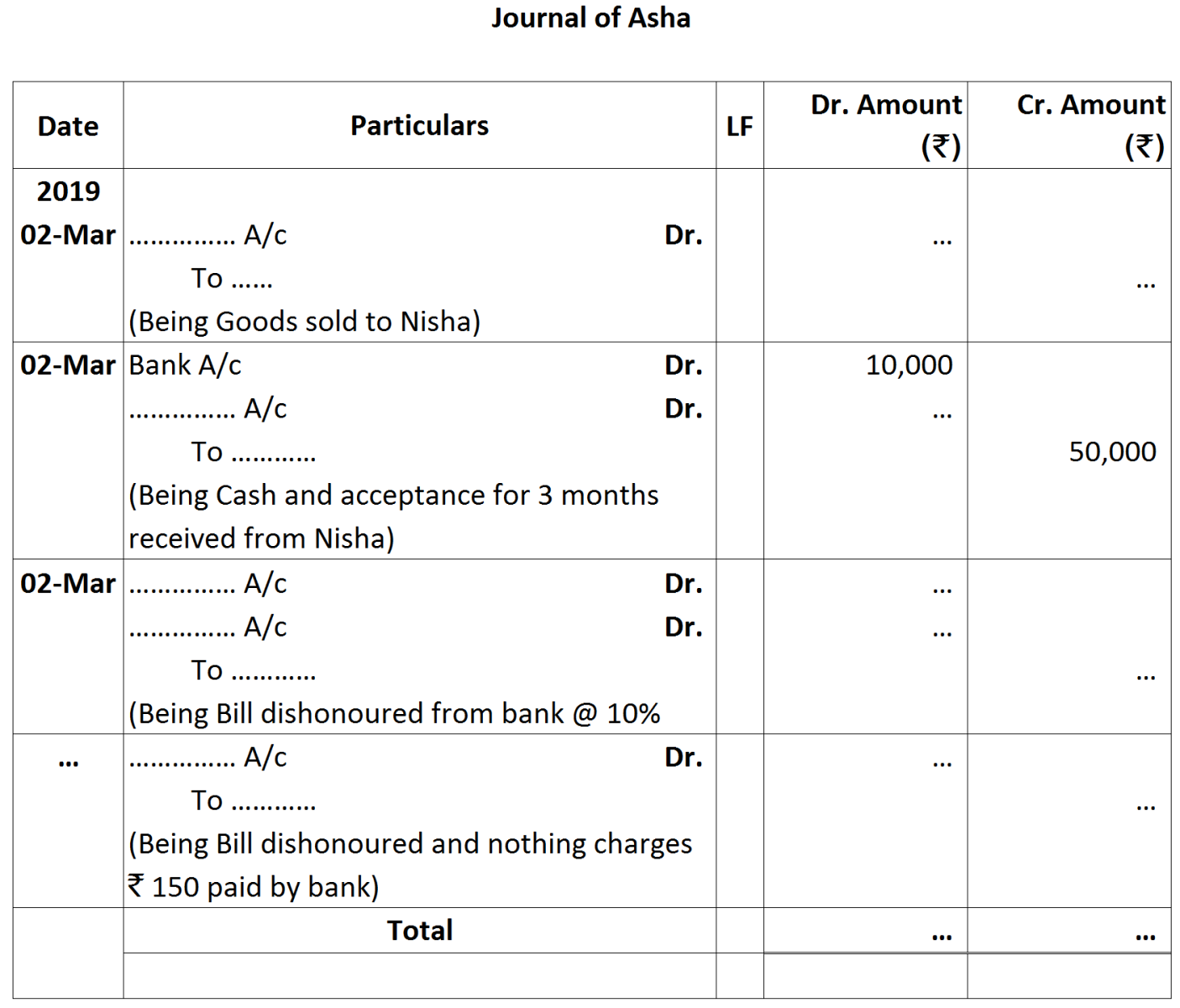

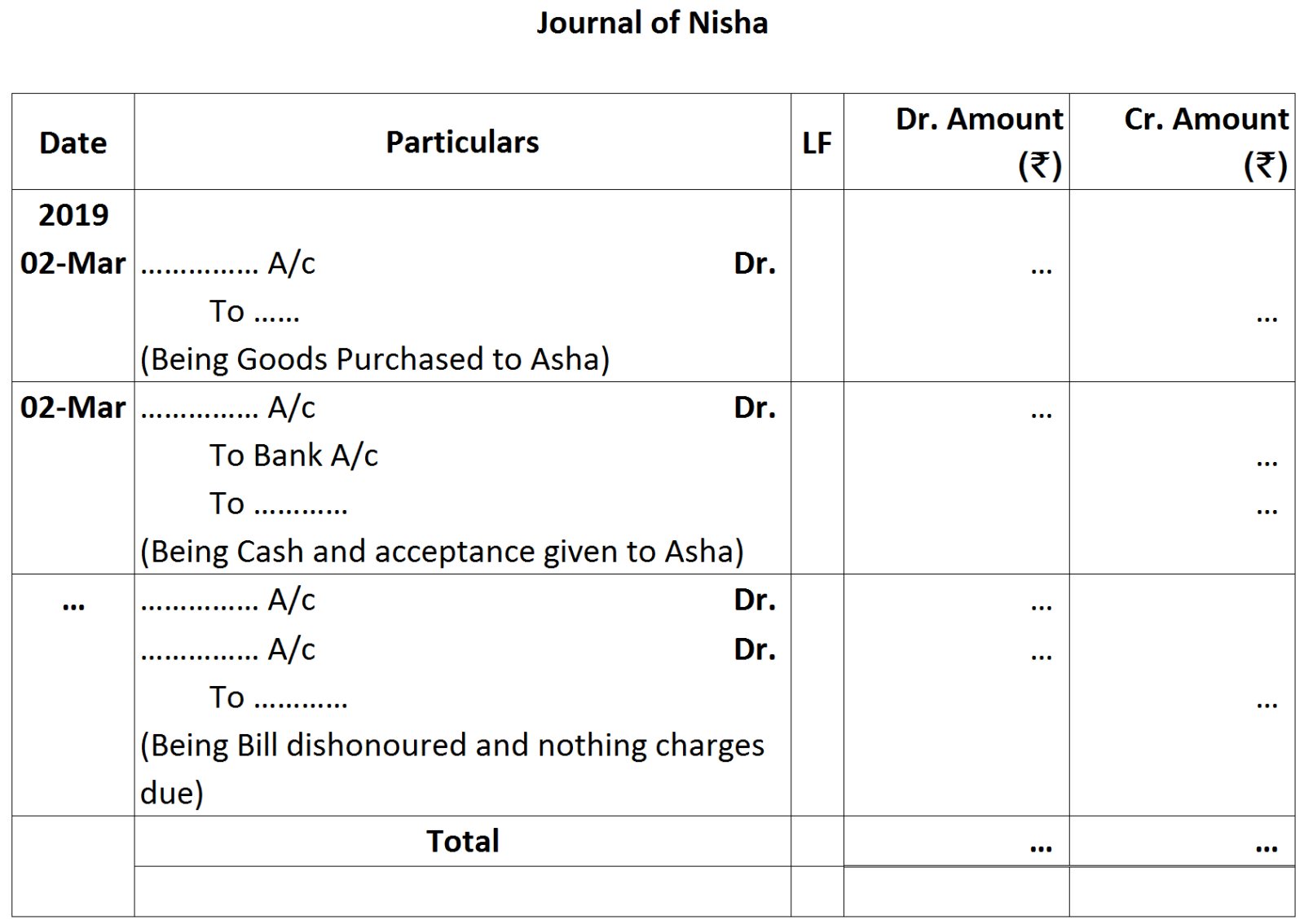

Question

Distinguish between an accomodation bill and a trade bill.

| Basis for Distinction | Trade Bills | Accommodation Bills | |

| 1. | Object | These bills are drawn against trade transaction of sale and purchase. | These bills are drawn for financial assistance. |

| 2. | Consideration | These bills are drawn against proper consideration. | These bills are drawn without consideration. |

| 3. | Proof of Dedt | These bills are proof of debt. The drawee is a debtor. | These bills are not a proof of debt because the drawee is not a debtor. |

| 4. | Distribution of the proceeds | When these bills are discounted, the full proceeds remain with the drawer. | When these bills are discounted, the proceeds may be share by drawer and drawee in pre-determined ratio. |

Generate a complete, print-ready paper with questions like this in minutes — across 16+ boards, with answer keys.

|

2017

|

|

|

June 5

|

Bought from Mohan Lal & Co., Kanpur (U.P)

|

|

20 Godrej Chairs @ ₹ 2,000 each

|

|

|

5 Godrej Tables @ ₹ 6,000 each

|

|

|

Trade Discount 20%

|

|

|

June 10

|

Purchased from Bharat Bhushan & Sons, Varanasi (U.P)

|

|

5 Almirahs @ ₹ 12,000 each

|

|

|

2 Revolving Chairs @ ₹ 20,000 each

|

|

|

Trade Discount 10%

|

|

|

June 14

|

Purchased from Surya Traders, Lucknow (U.P)

|

|

80 Desks @ ₹ 2,500 each

|

|

|

10 Sofa Sets @ ₹ 20,000 each

|

|

|

Trade Discount @ 15%

|

|

|

June 20

|

Purchased for cash from Gopi Chand Haldi Ram, Delhi

|

|

4 Tables @ ₹ 5,000 each

|

|

|

25 June

|

Bought Furniture for office use from New Furniture House, Faridabad on Credit

|

|

5 Chairs @ ₹ 2,500 per Chair.

|

|

|

2 Tables @ ₹ 5,000 per Table.

|