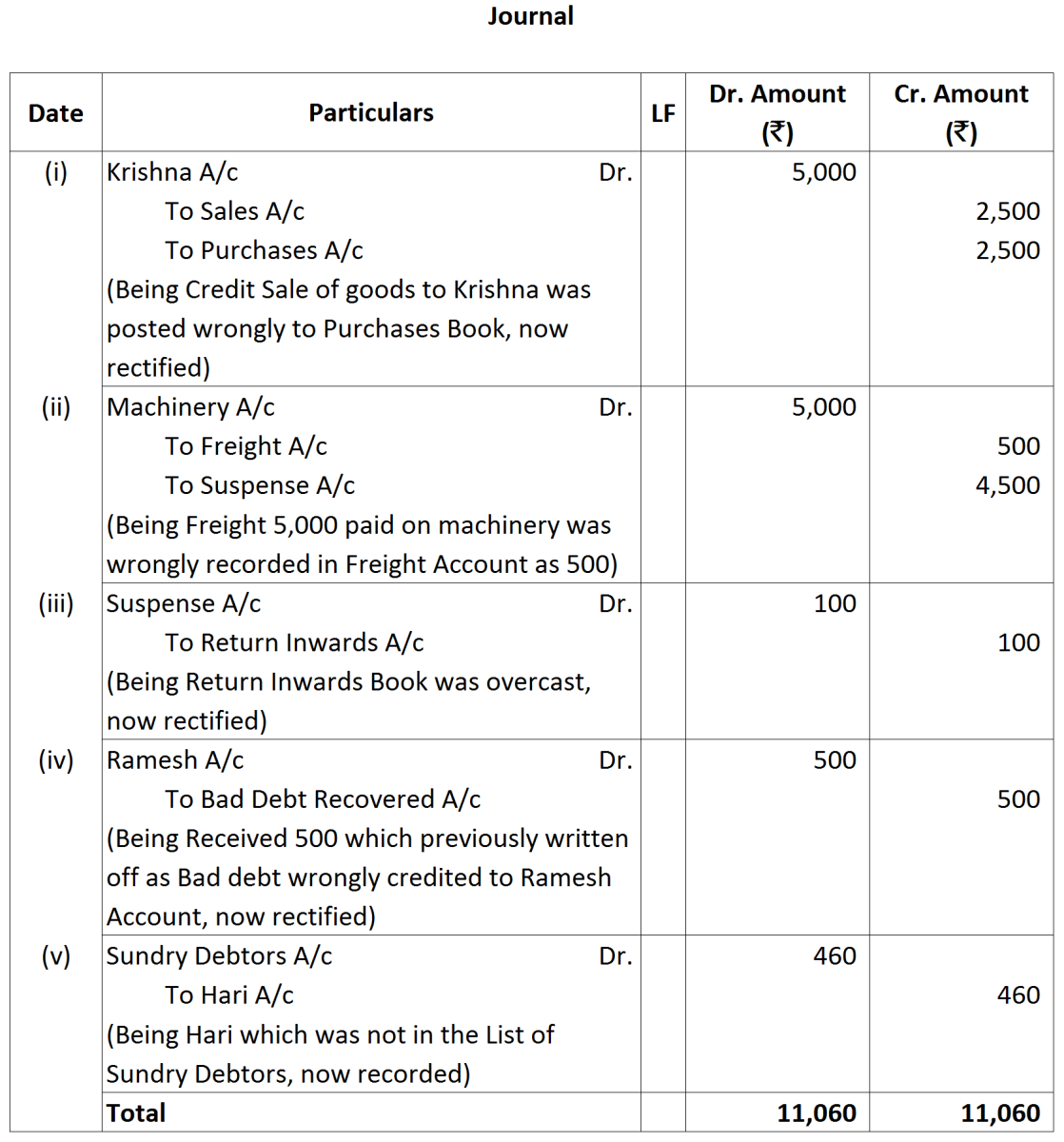

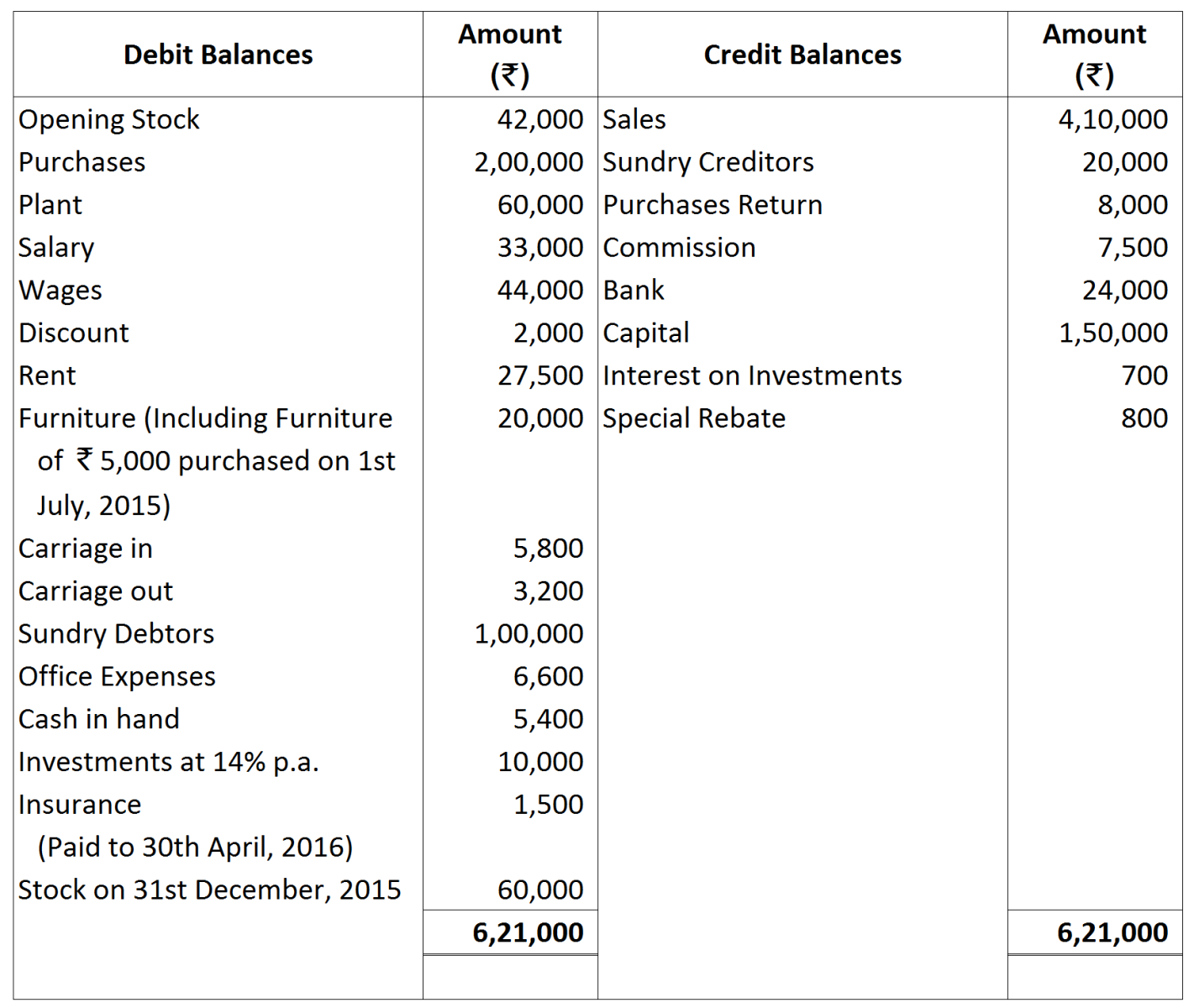

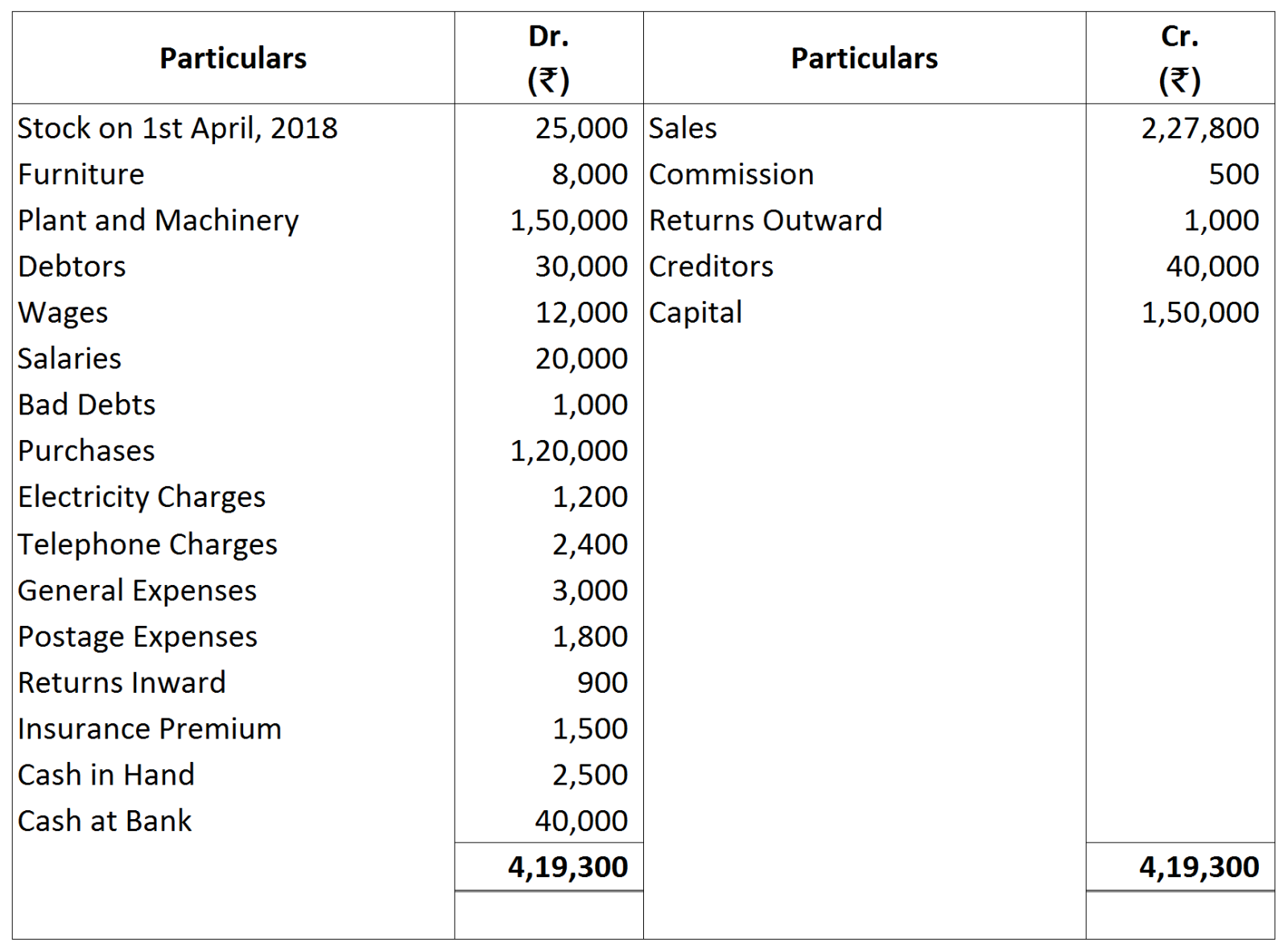

Question

- What are the different causes that make a Trial Balance incorrect?

- Pass the rectifying Journal entries:

- A credit sale of goods for ₹ 2,500 to Krishna has been wrongly passed through the Purchases Book.

- ₹ 5,000 paid for freight on machinery purchased was debited to the Freight Account as ₹ 500.

- The Returns Inward Book has been wrongly overcasted by ₹ 100.

- An amount of ₹ 500 due from Ramesh which had been written off as bad debt in previous year was recovered and had been posted to the Personal Account of Ramesh.

- A sum of ₹ 460 owed by Hari had not been included in the list of debtors.