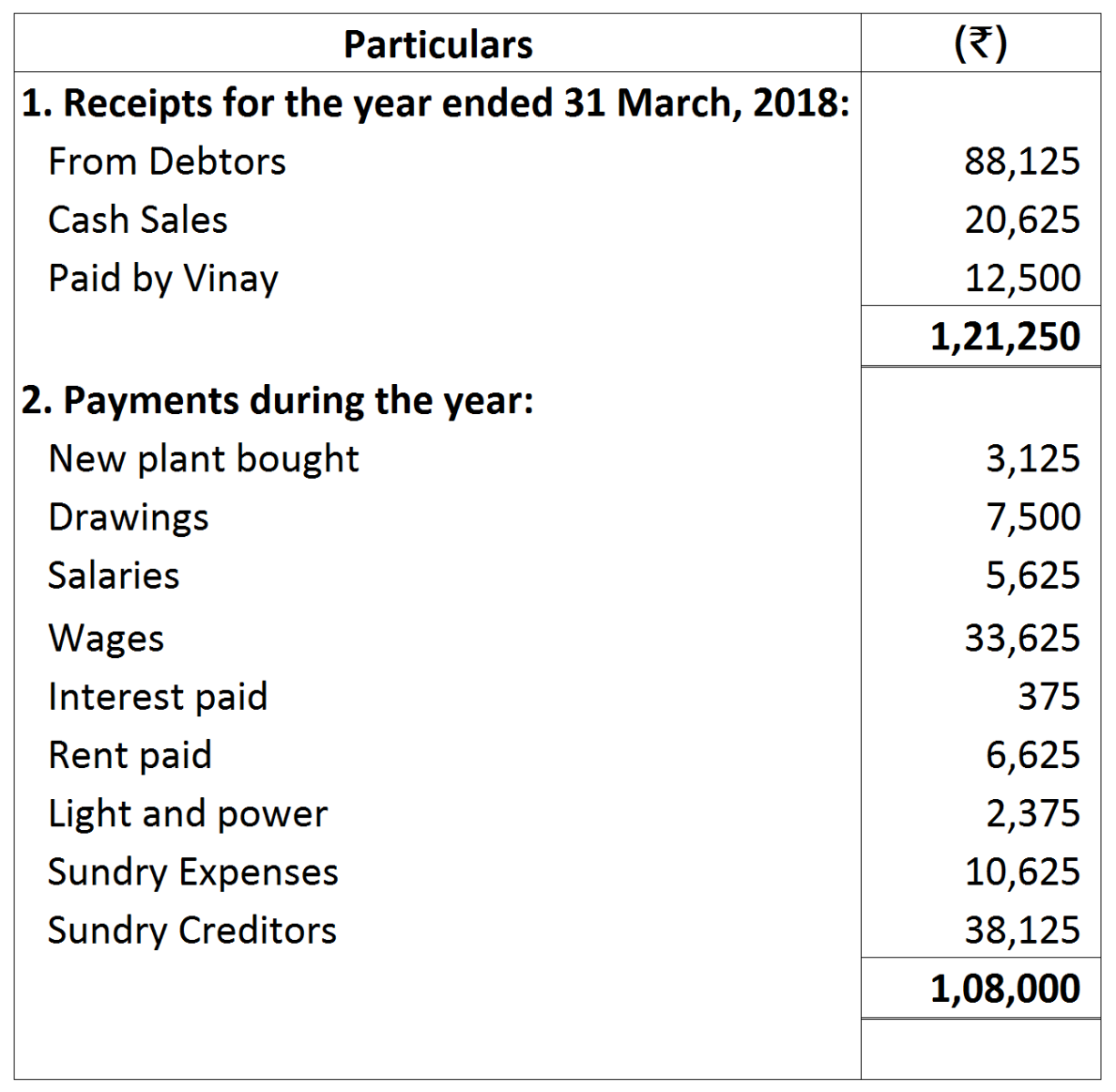

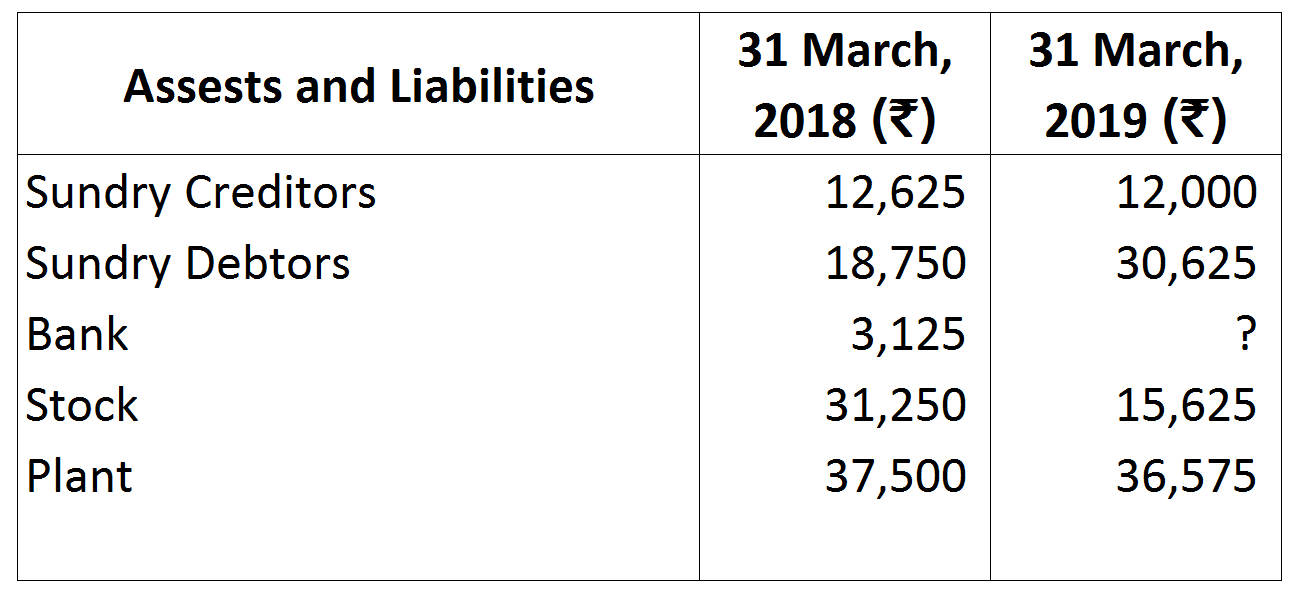

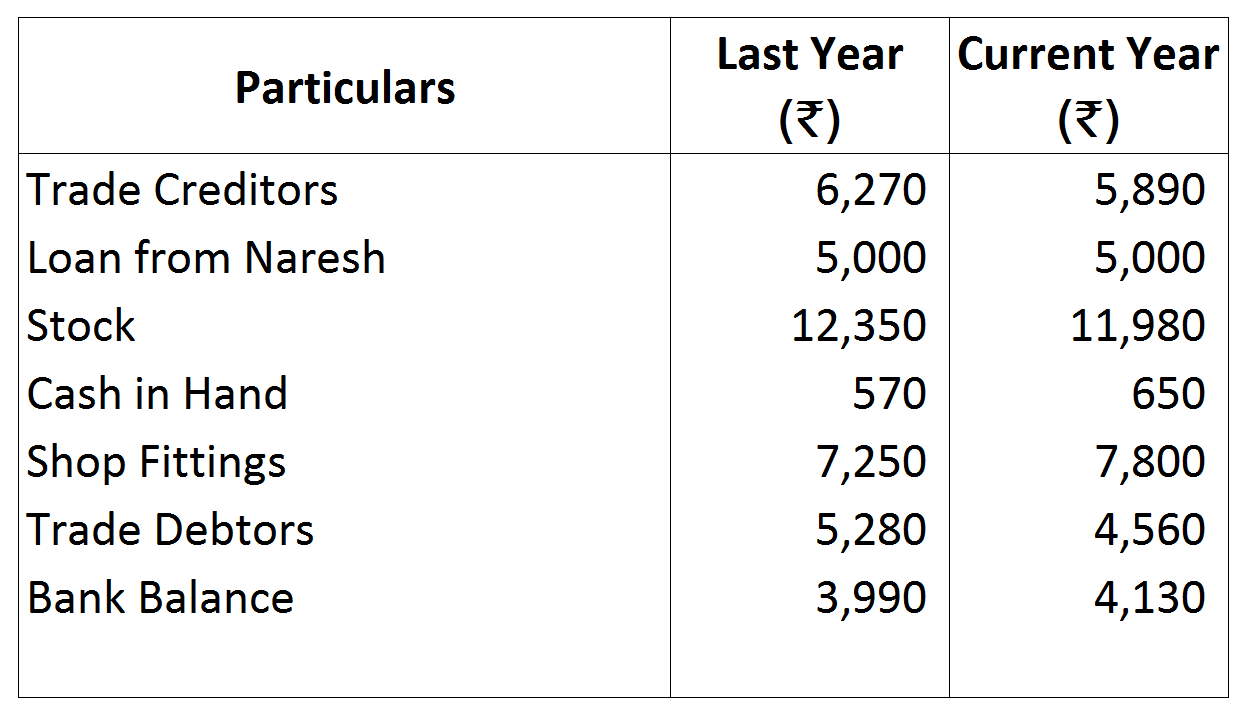

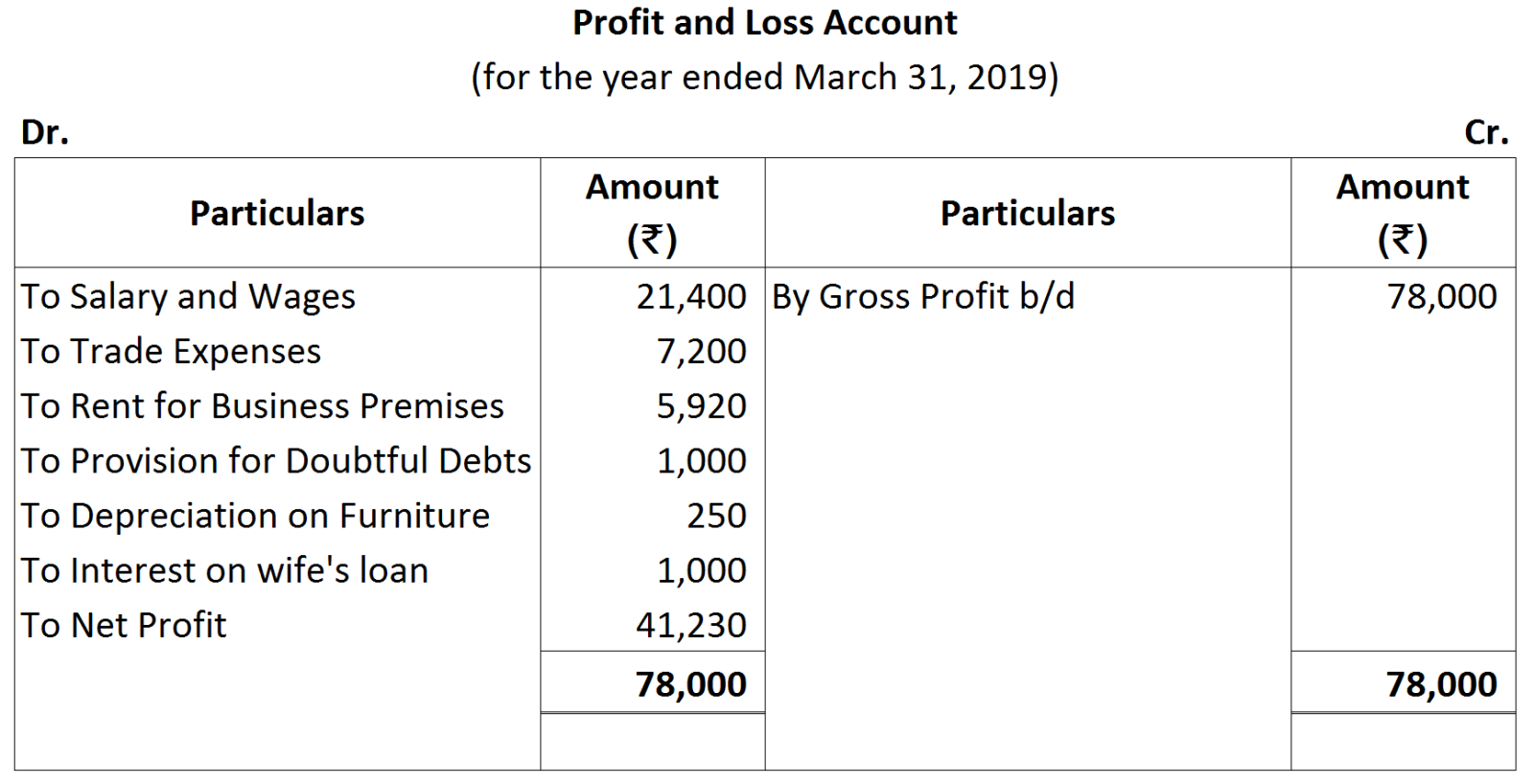

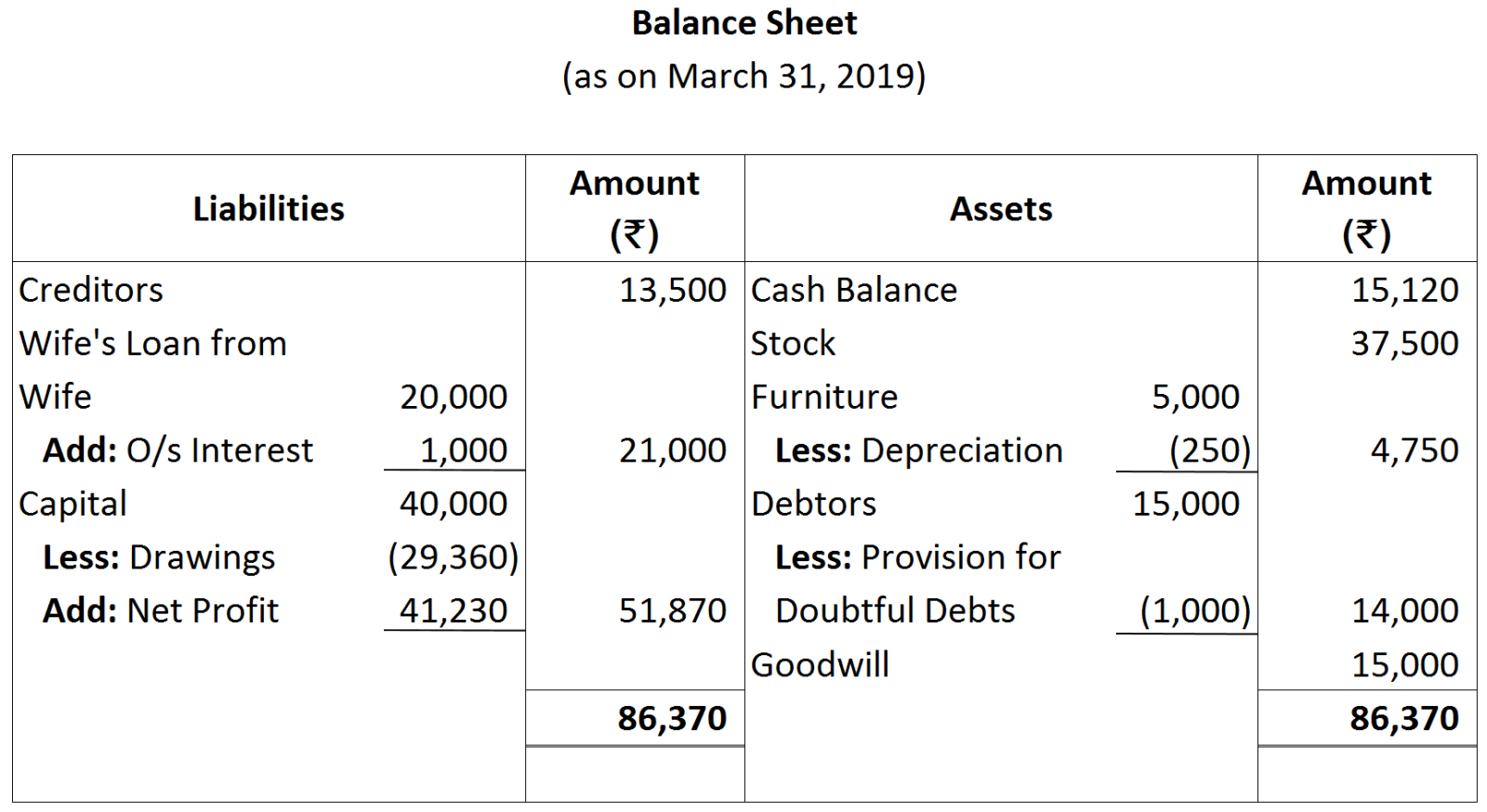

Question 16 Marks

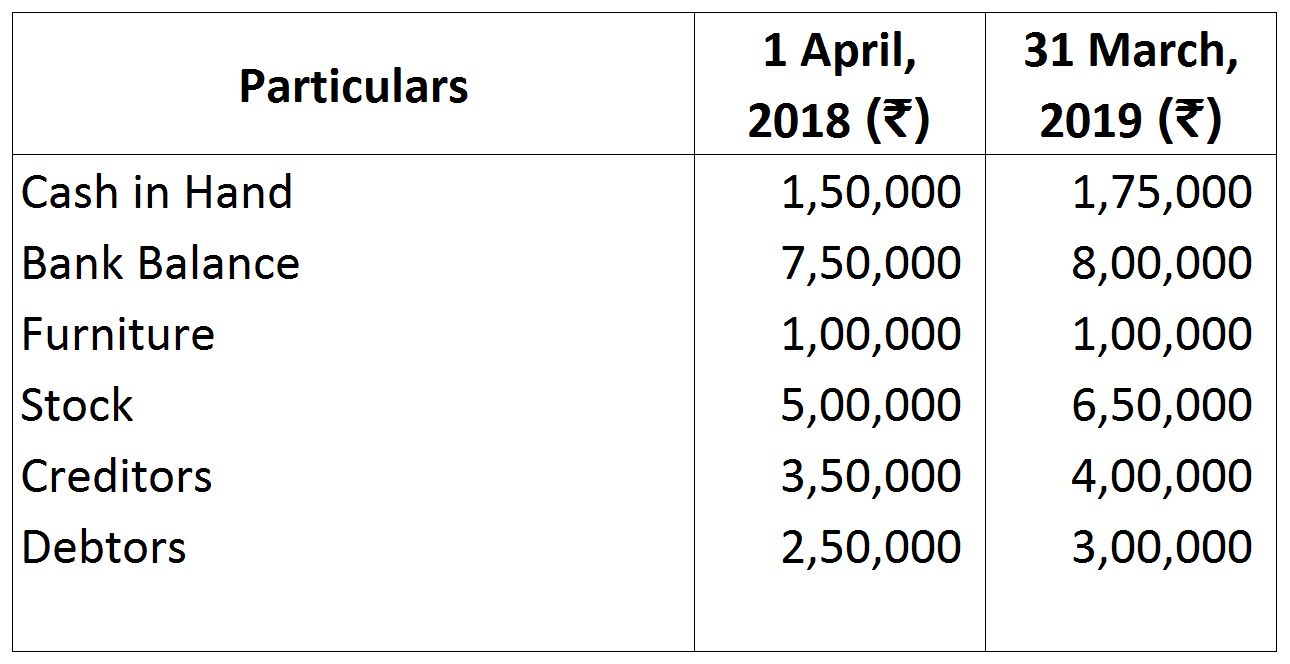

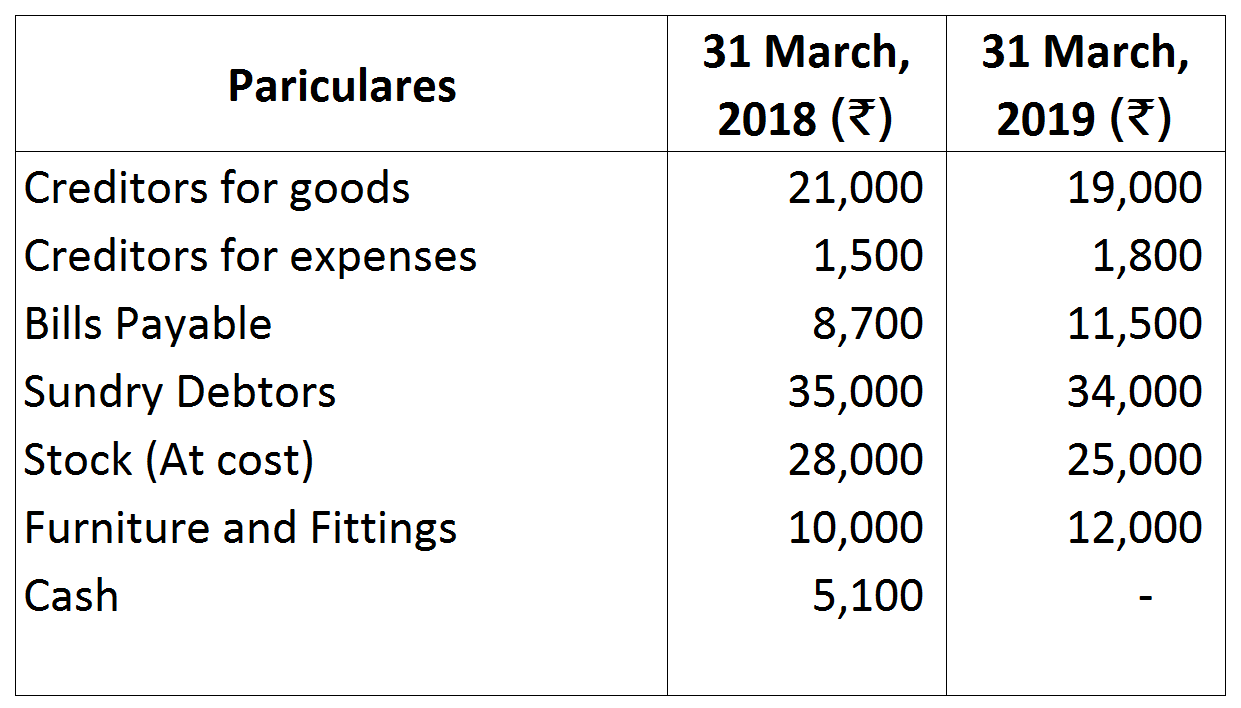

Hari maintains his books of account on Single Entry System. His books provide the following information:

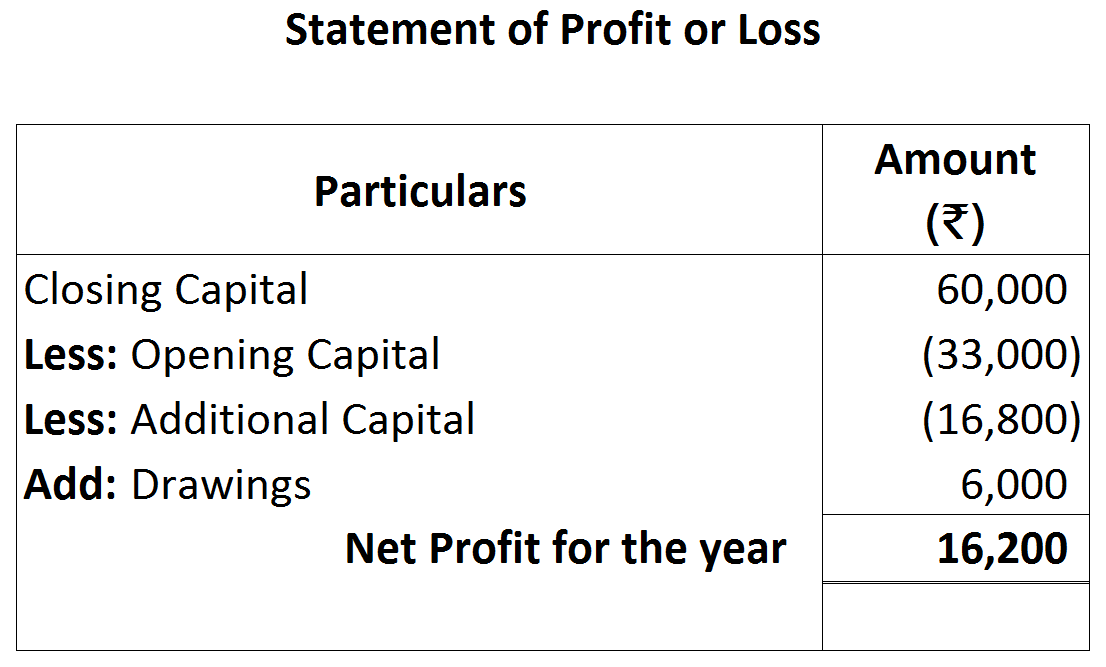

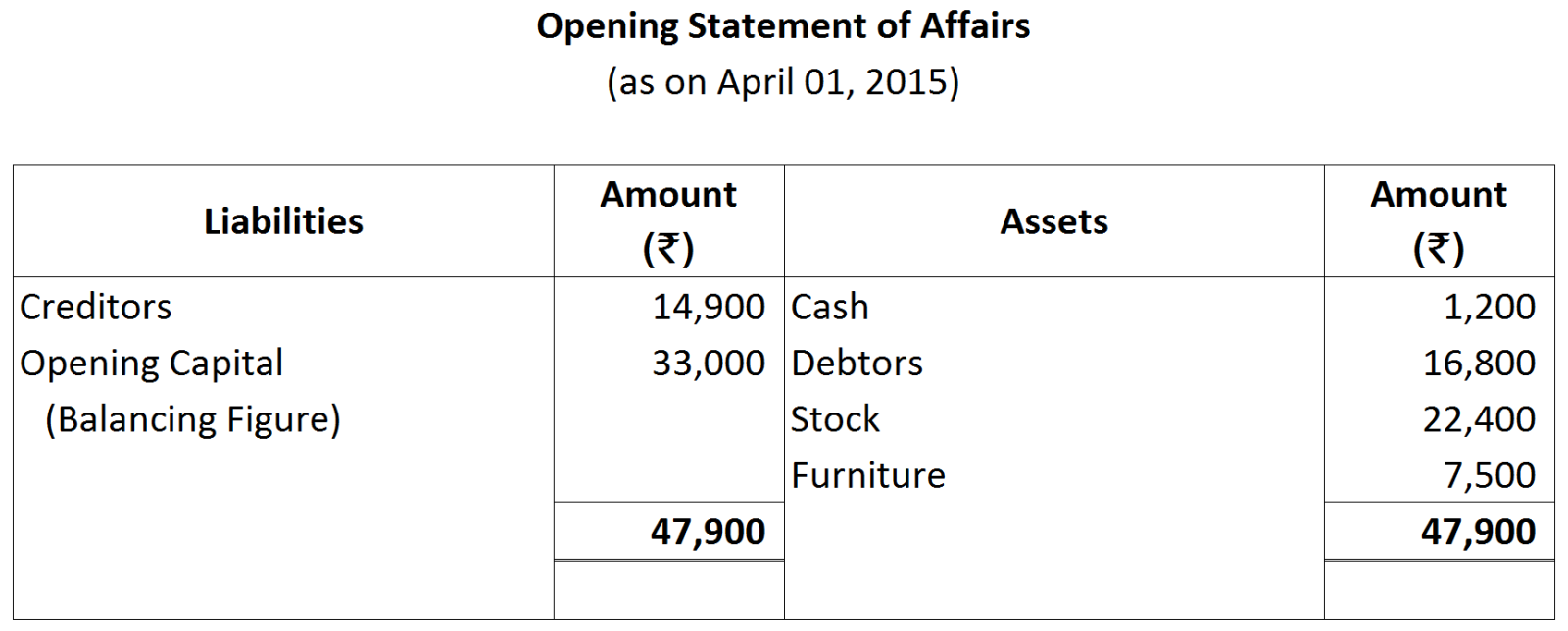

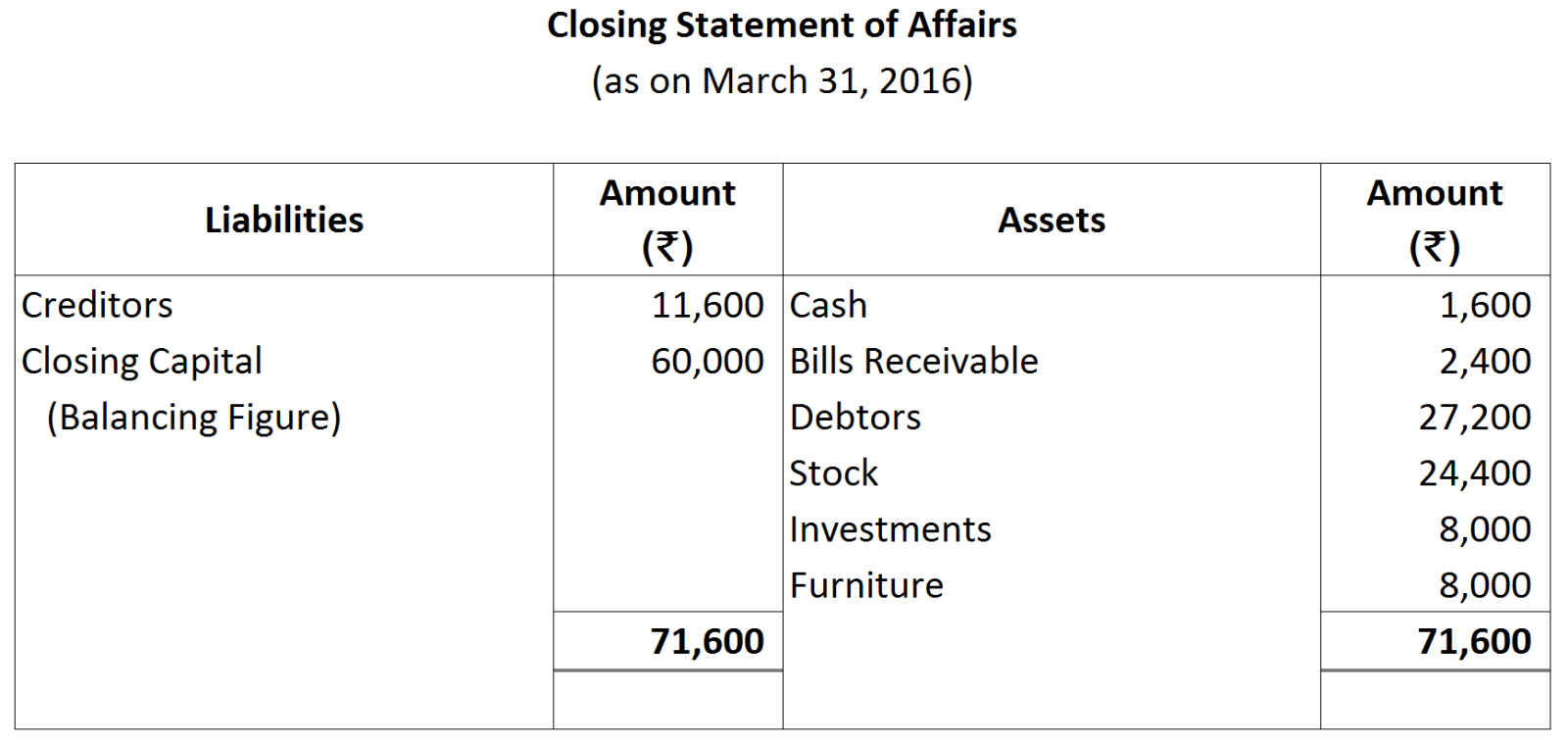

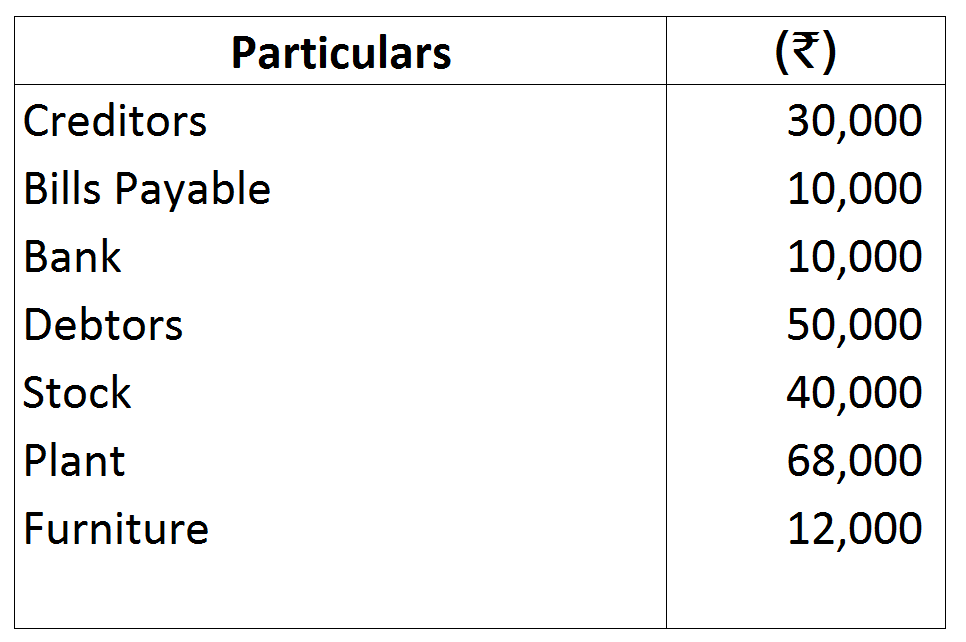

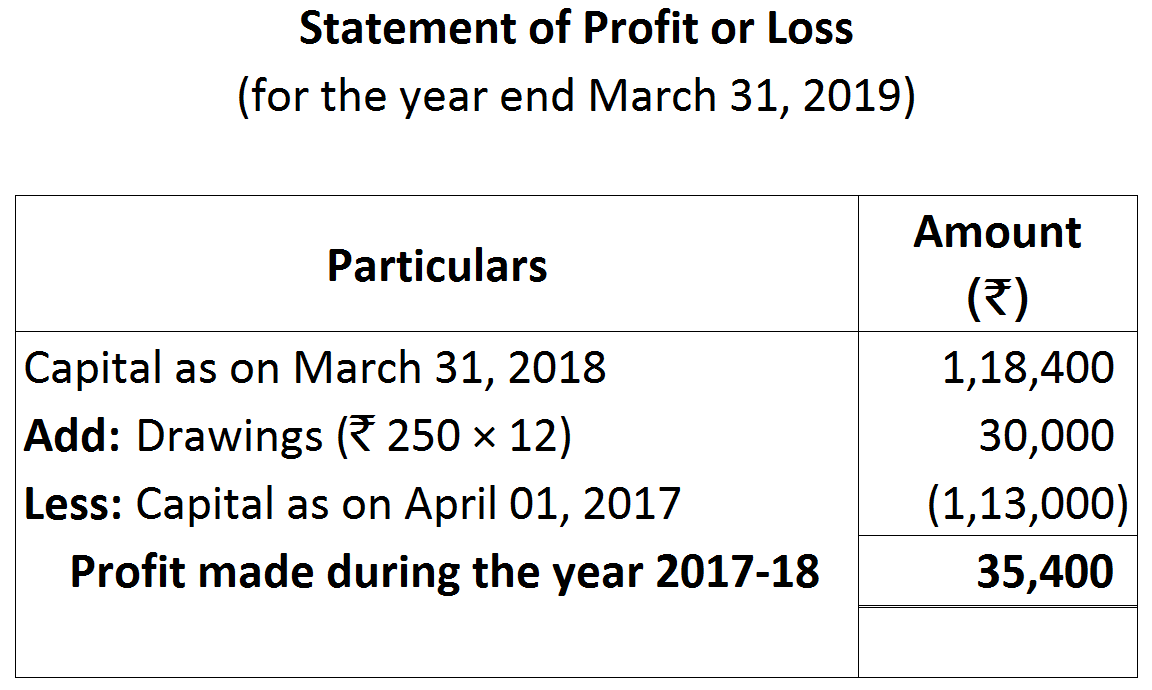

His drawings during the year were ₹ 5,000 Depreciate furniture by 10% and provide a reserve for Bad and Doubtful Debts at 10% on Sundry Debtors. Prepare the statement showing the profits for the year.

His drawings during the year were ₹ 5,000 Depreciate furniture by 10% and provide a reserve for Bad and Doubtful Debts at 10% on Sundry Debtors. Prepare the statement showing the profits for the year.

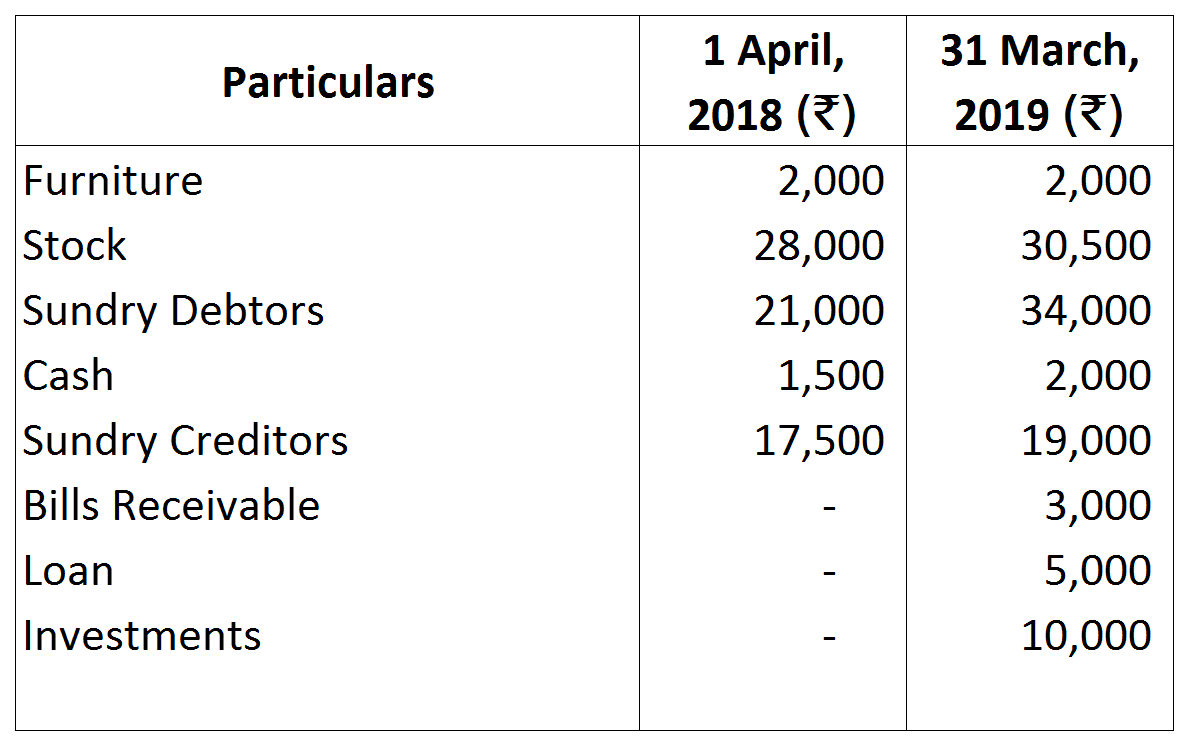

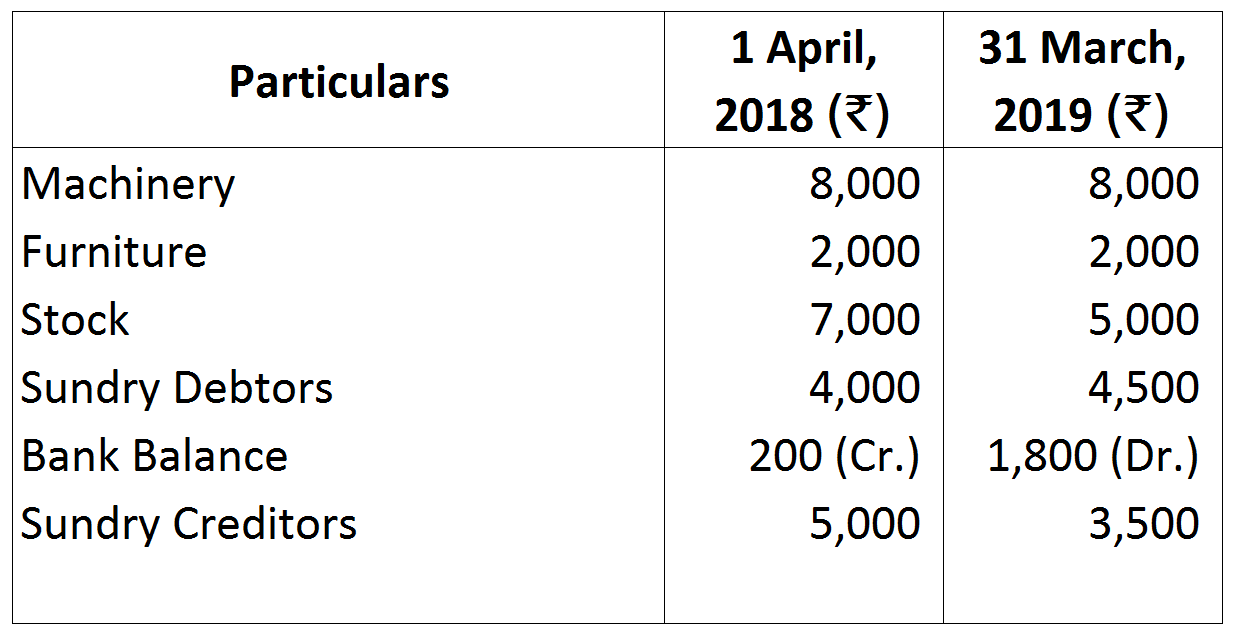

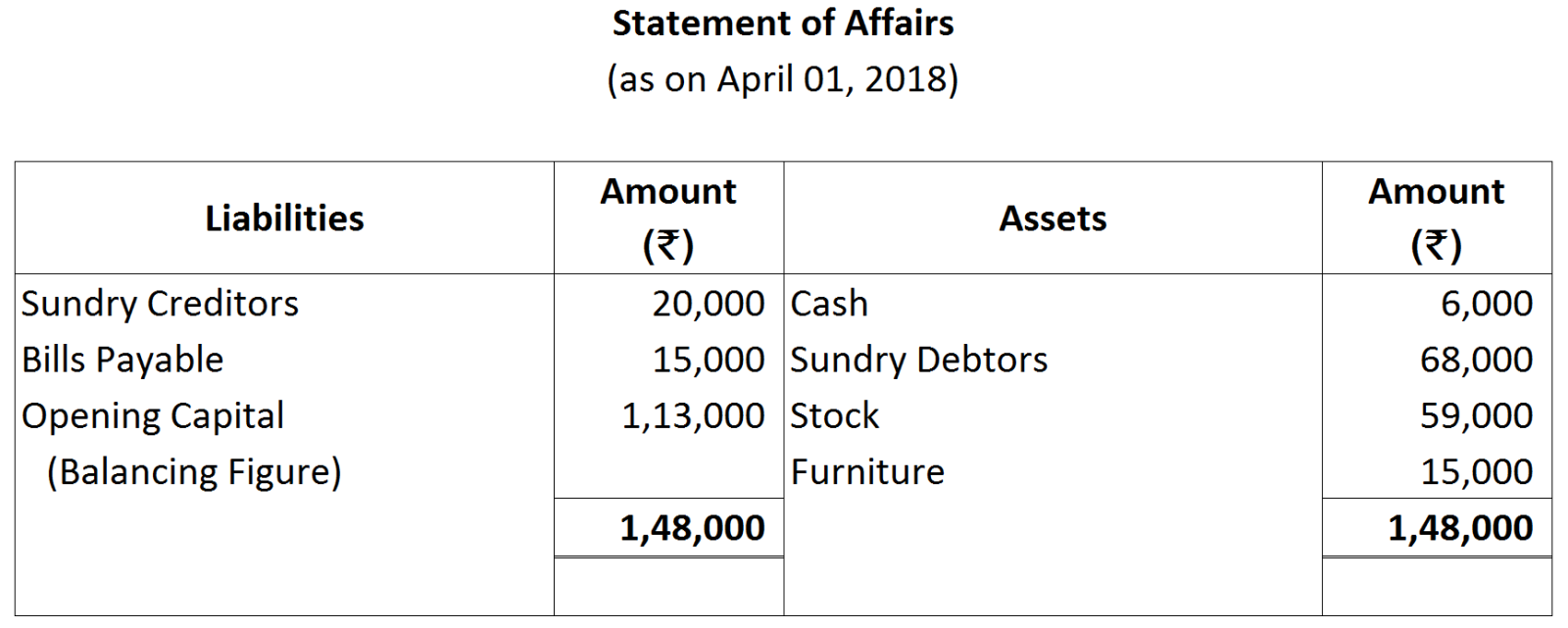

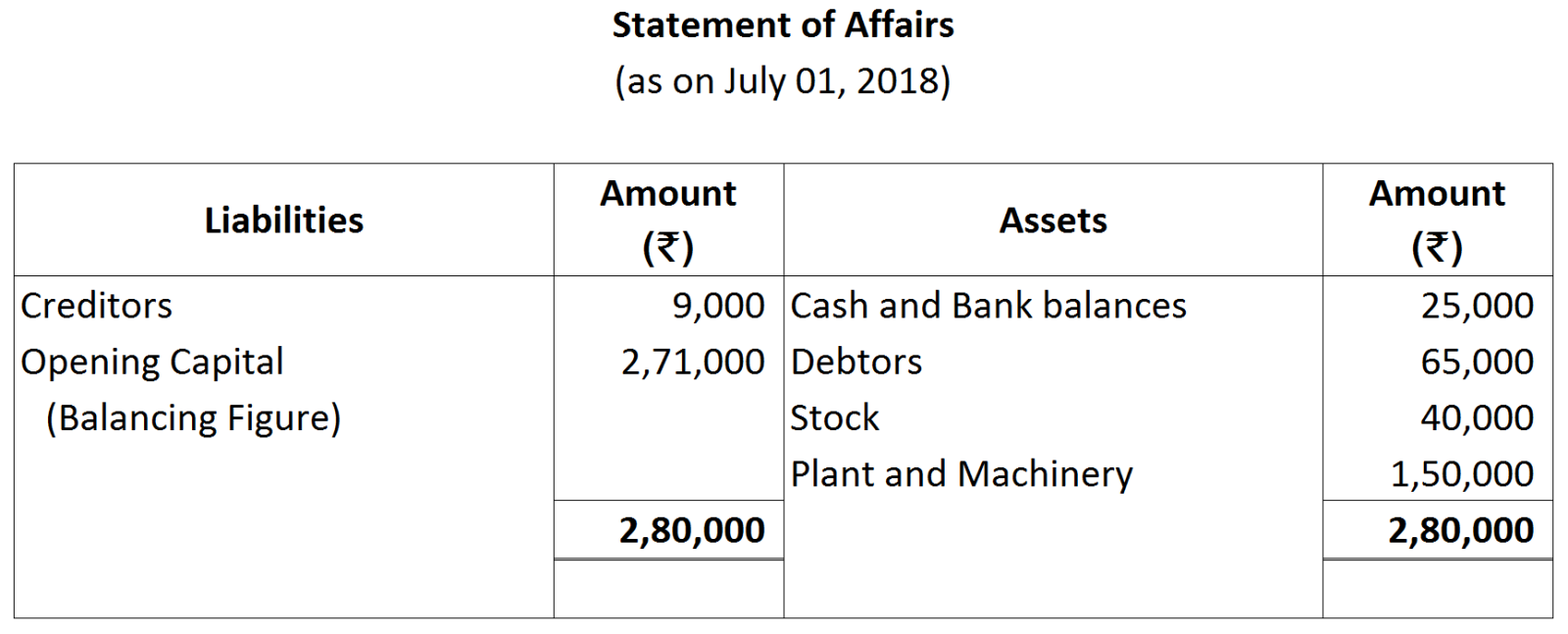

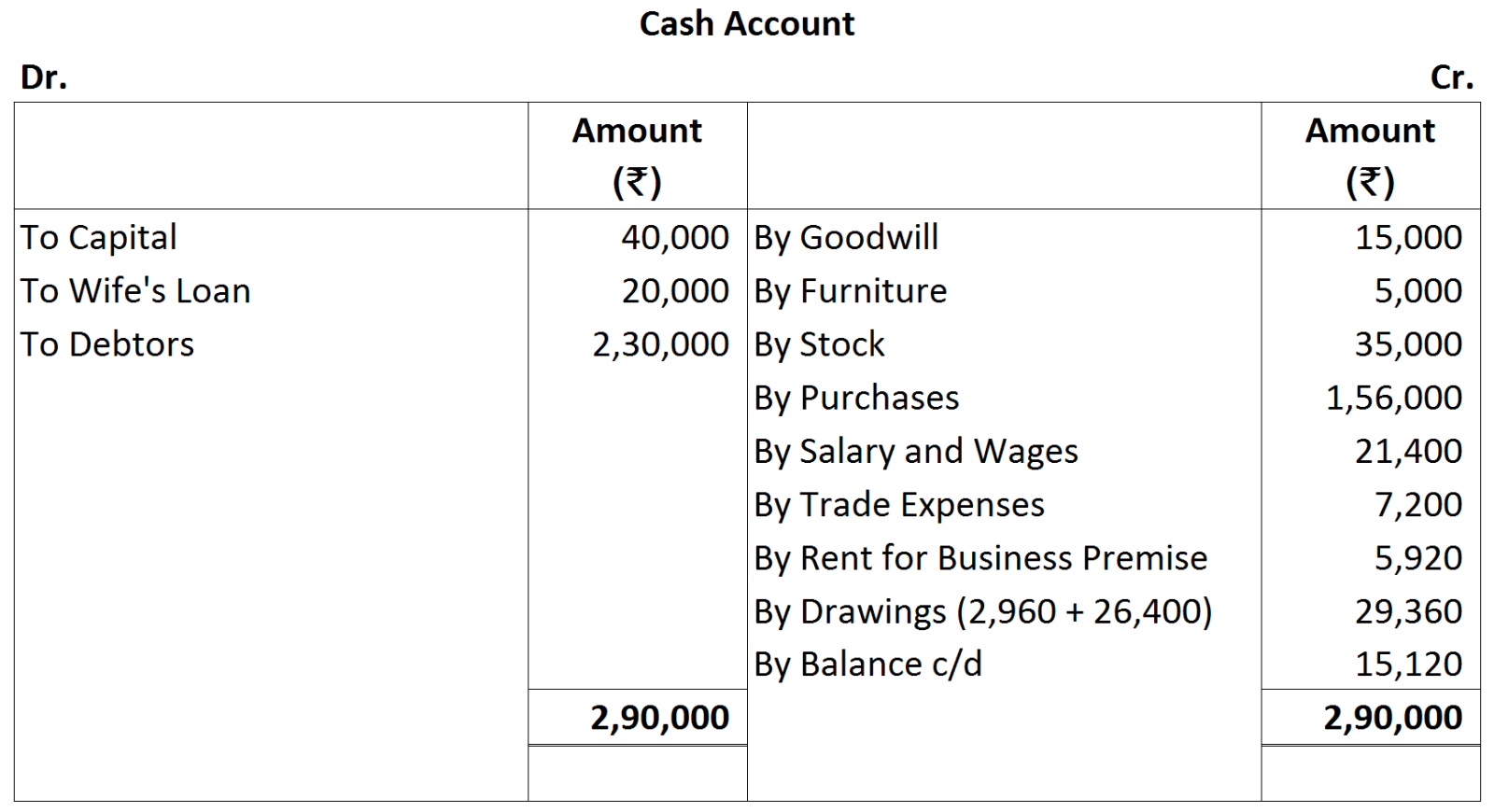

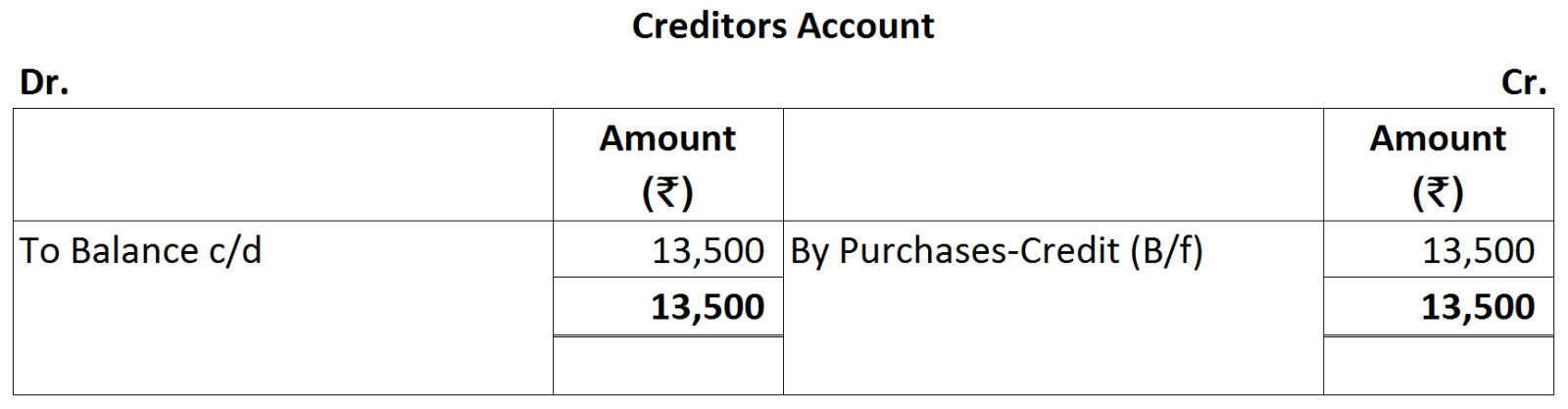

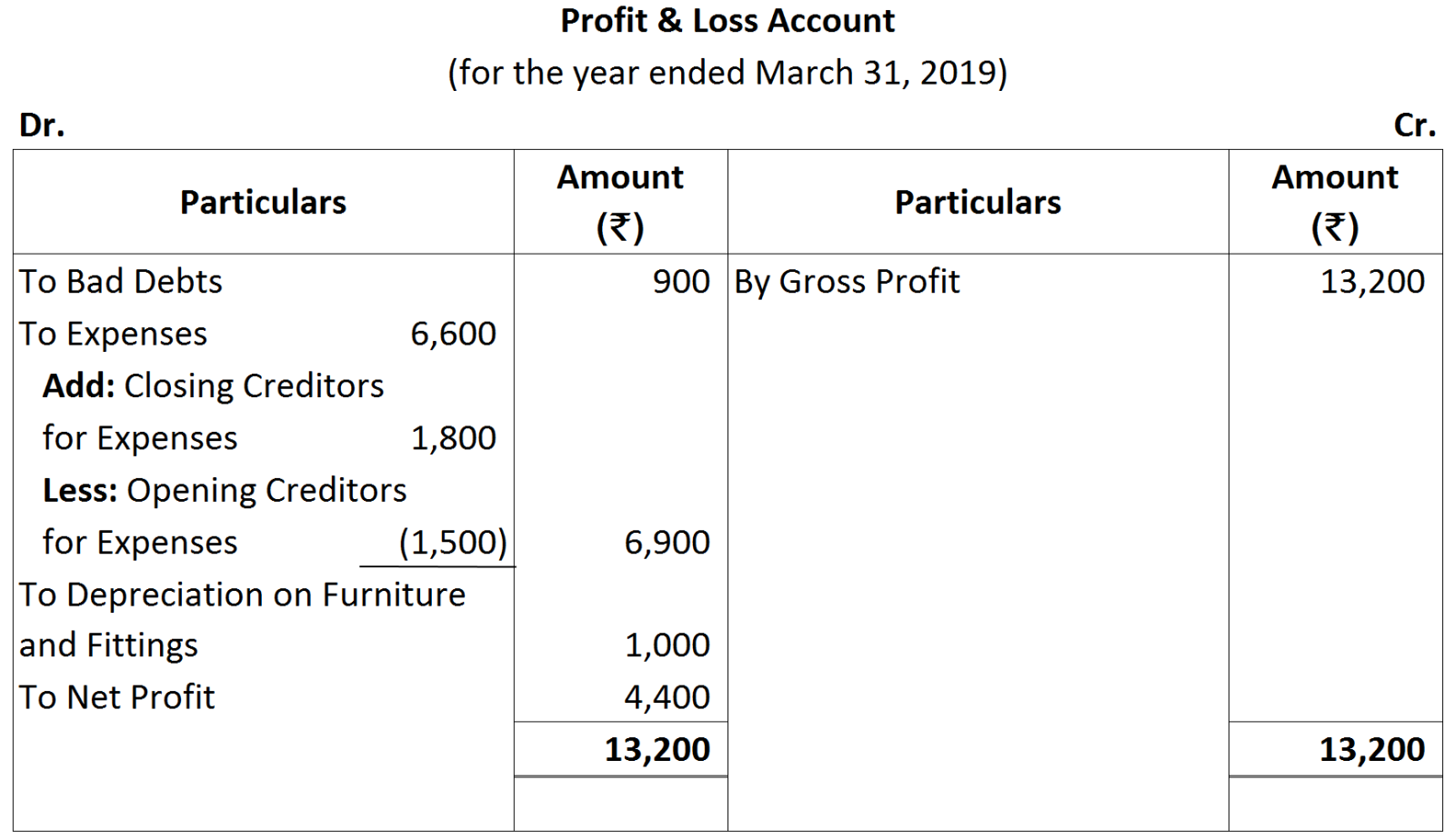

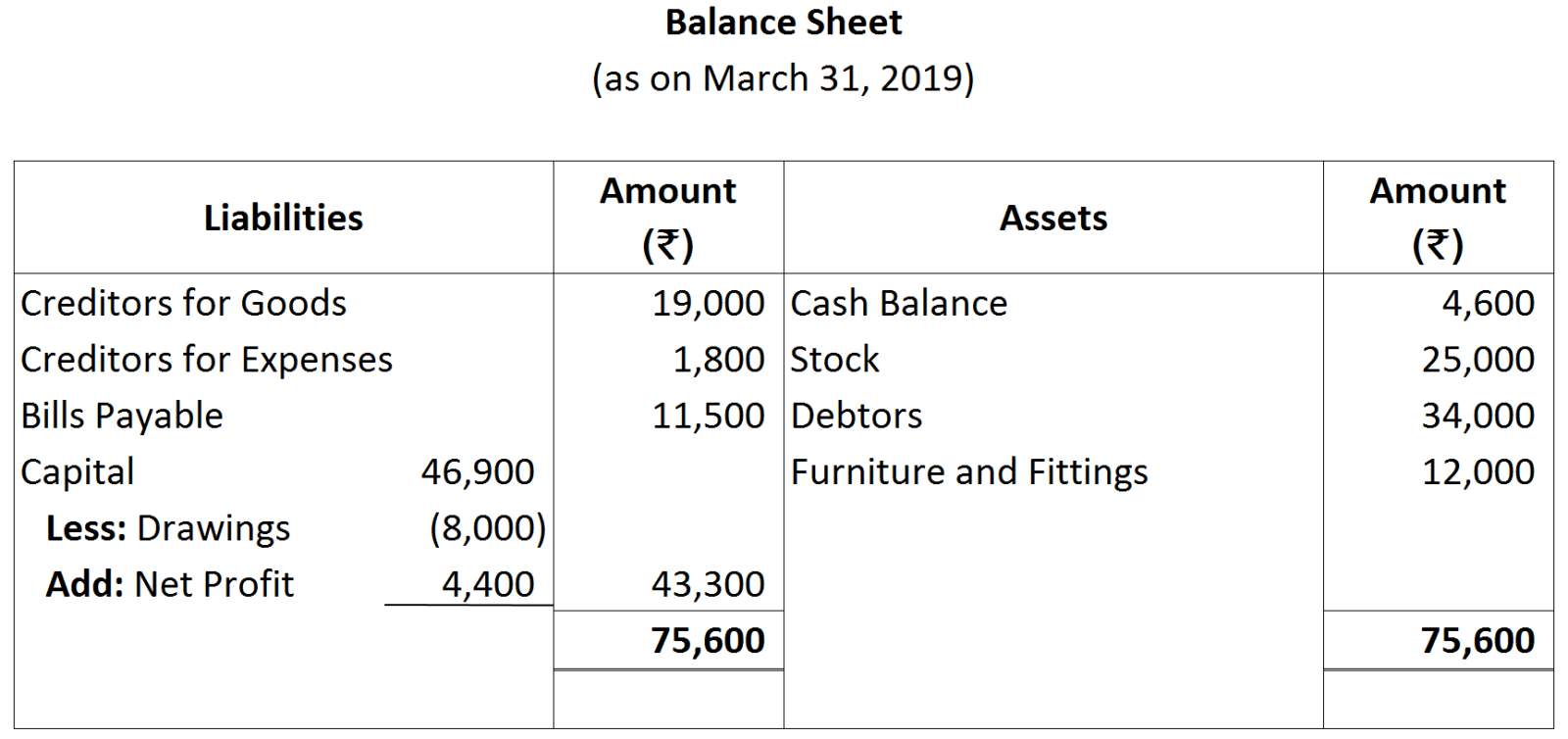

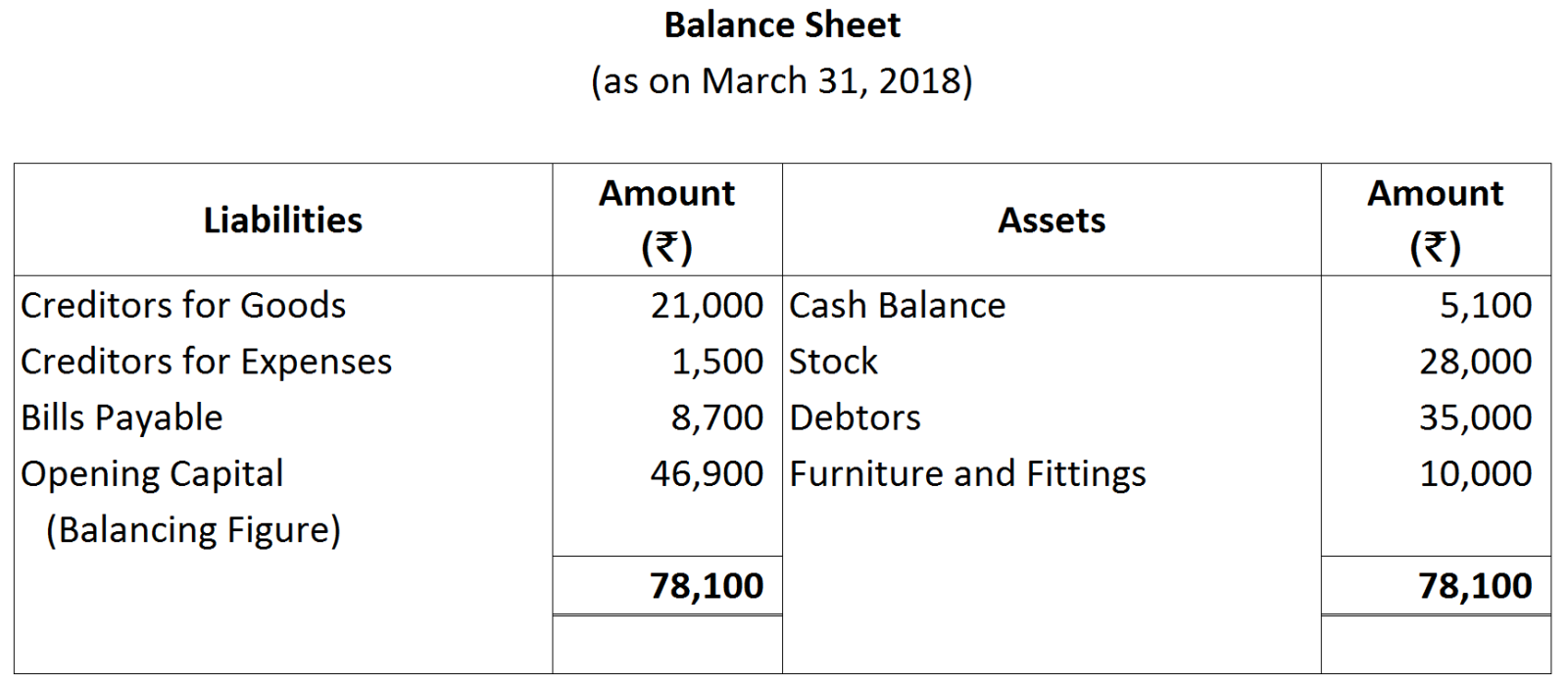

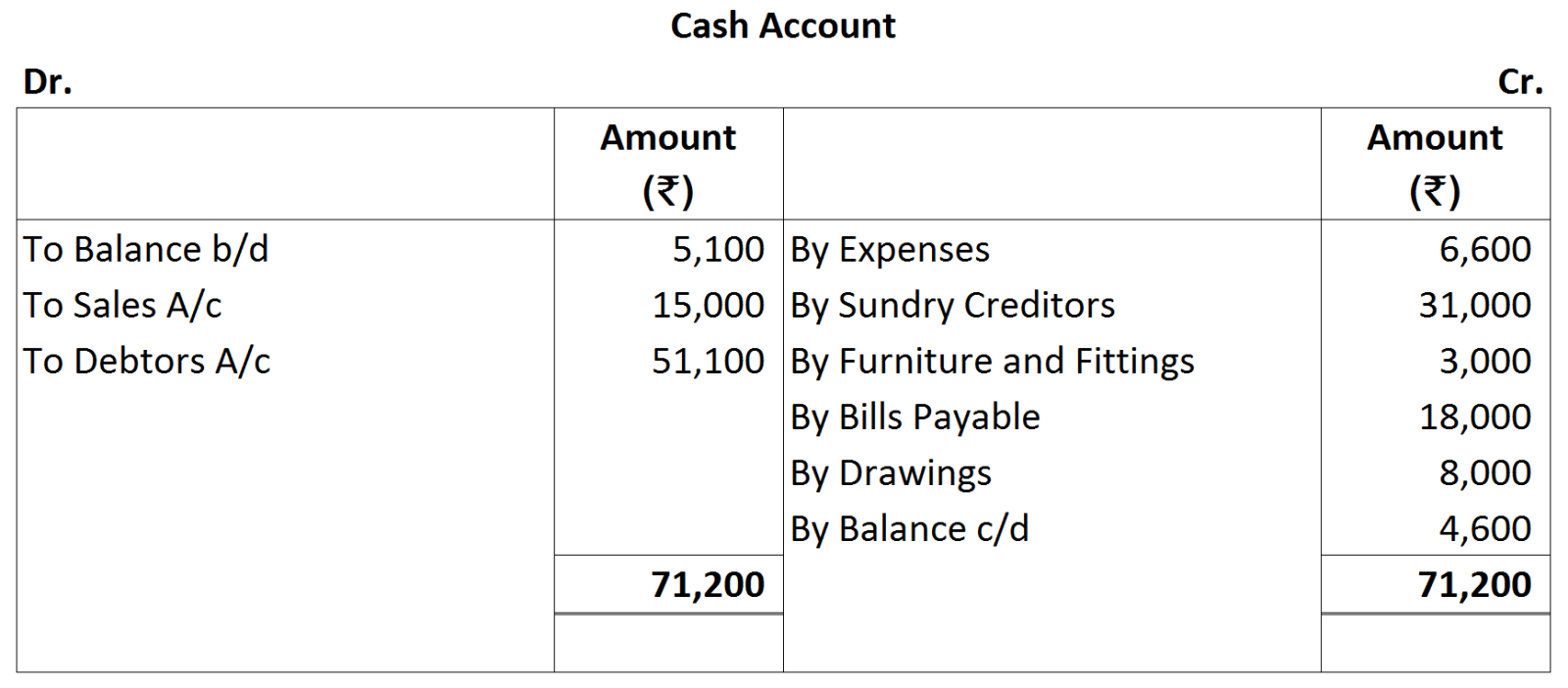

Working Notes:

Working Notes:

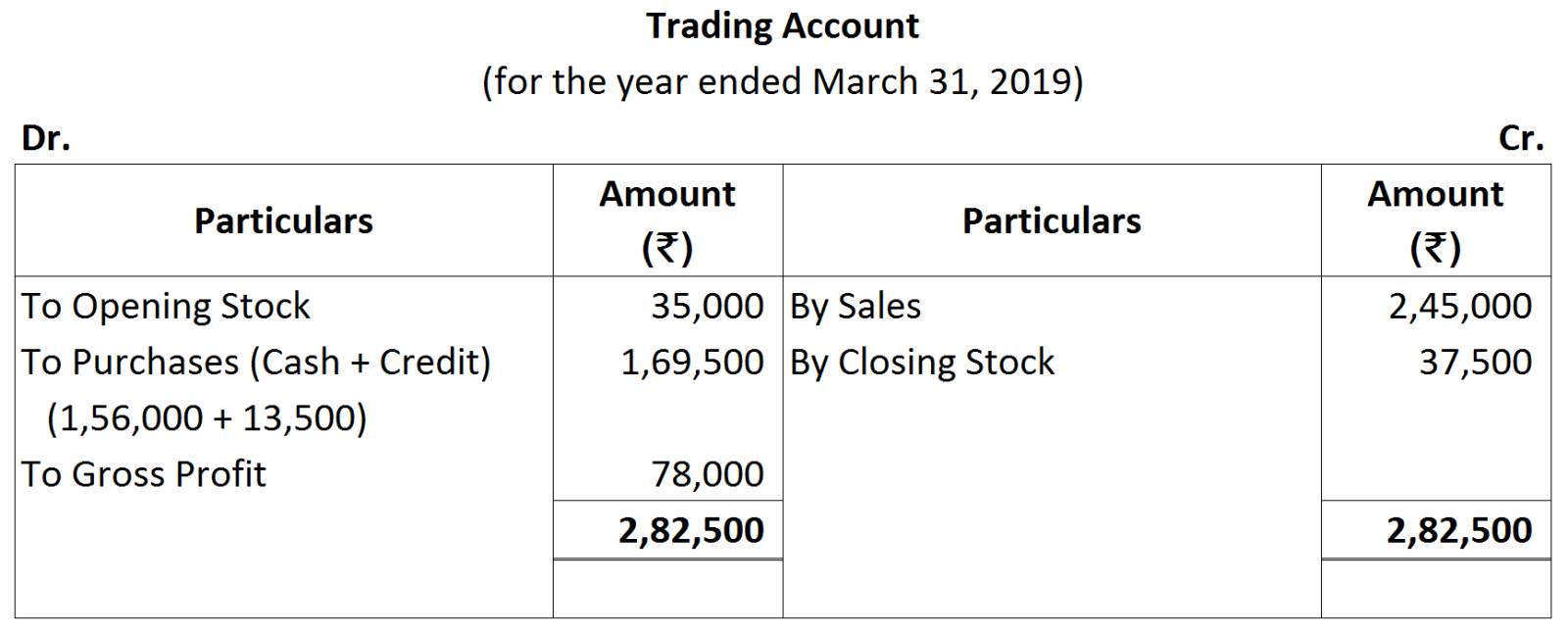

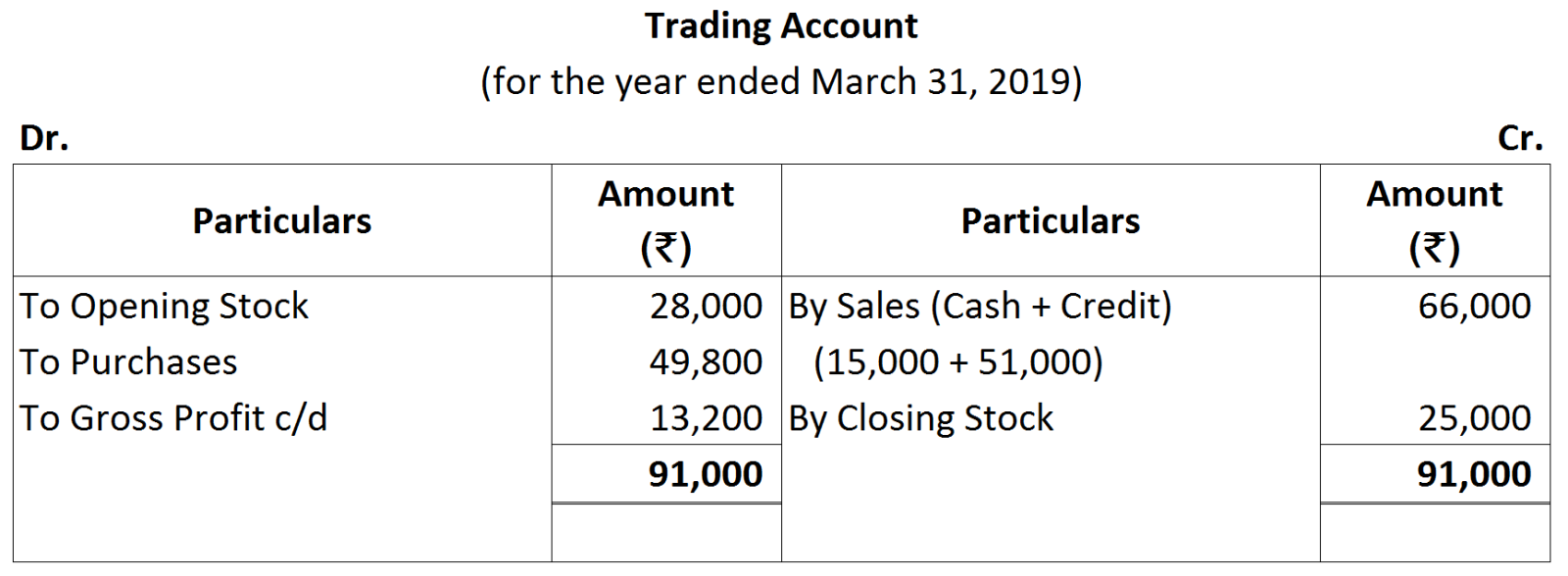

Cost of Goods Sold = Opening Stock + Purchases - Closing Stock

Cost of Goods Sold = Opening Stock + Purchases - Closing Stock

.

.

Working Notes:

Working Notes: Interest on Drawings $=\frac{4,200\times6\times1}{100\times12}=₹ \ 21$

Interest on Drawings $=\frac{4,200\times6\times1}{100\times12}=₹ \ 21$

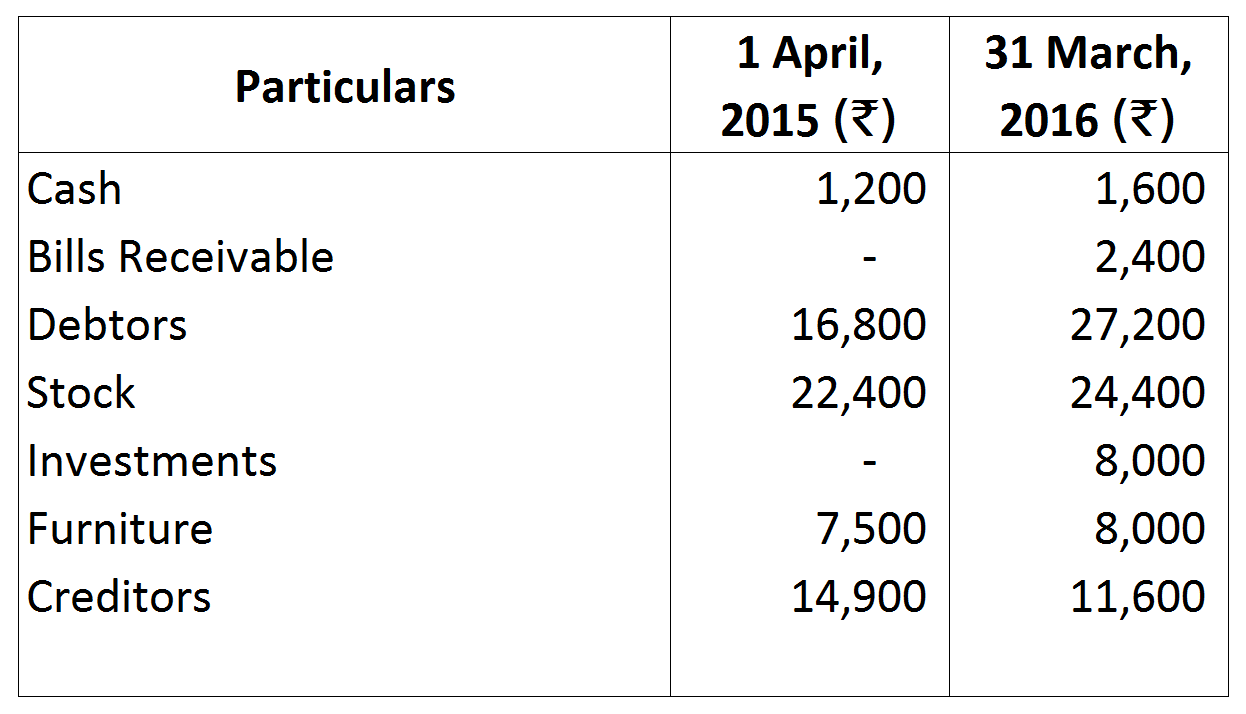

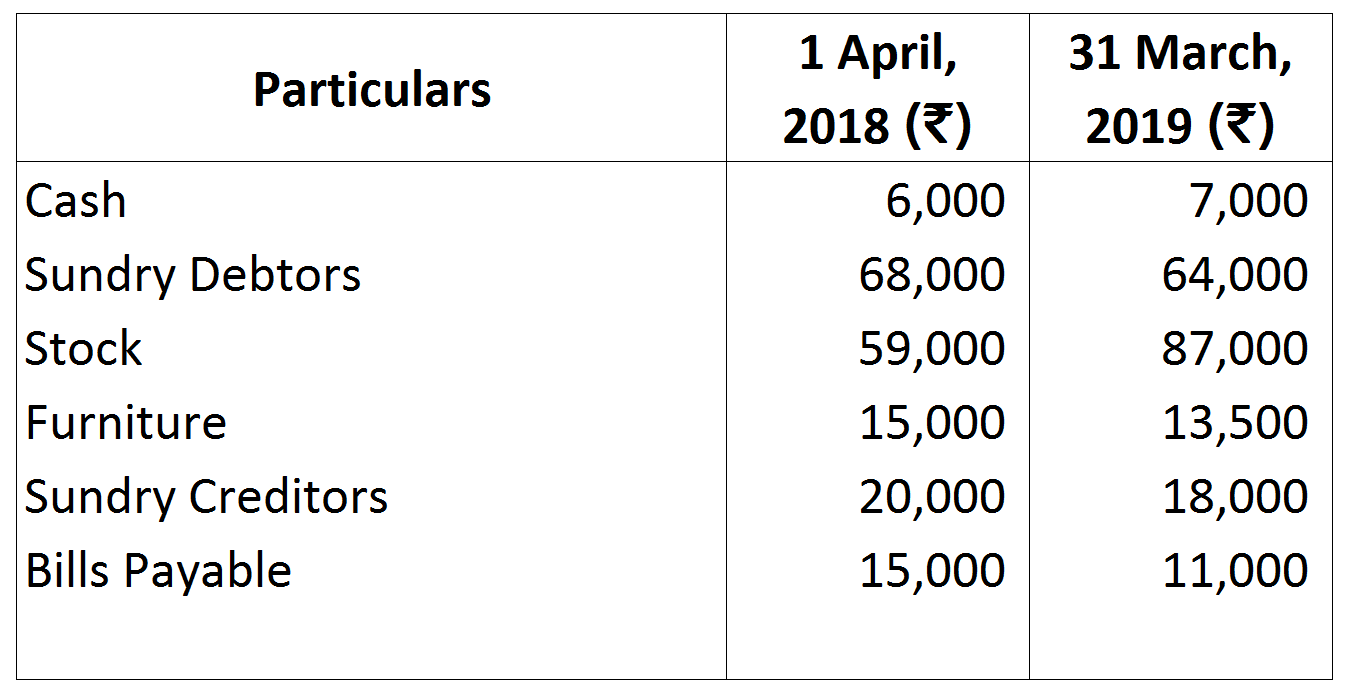

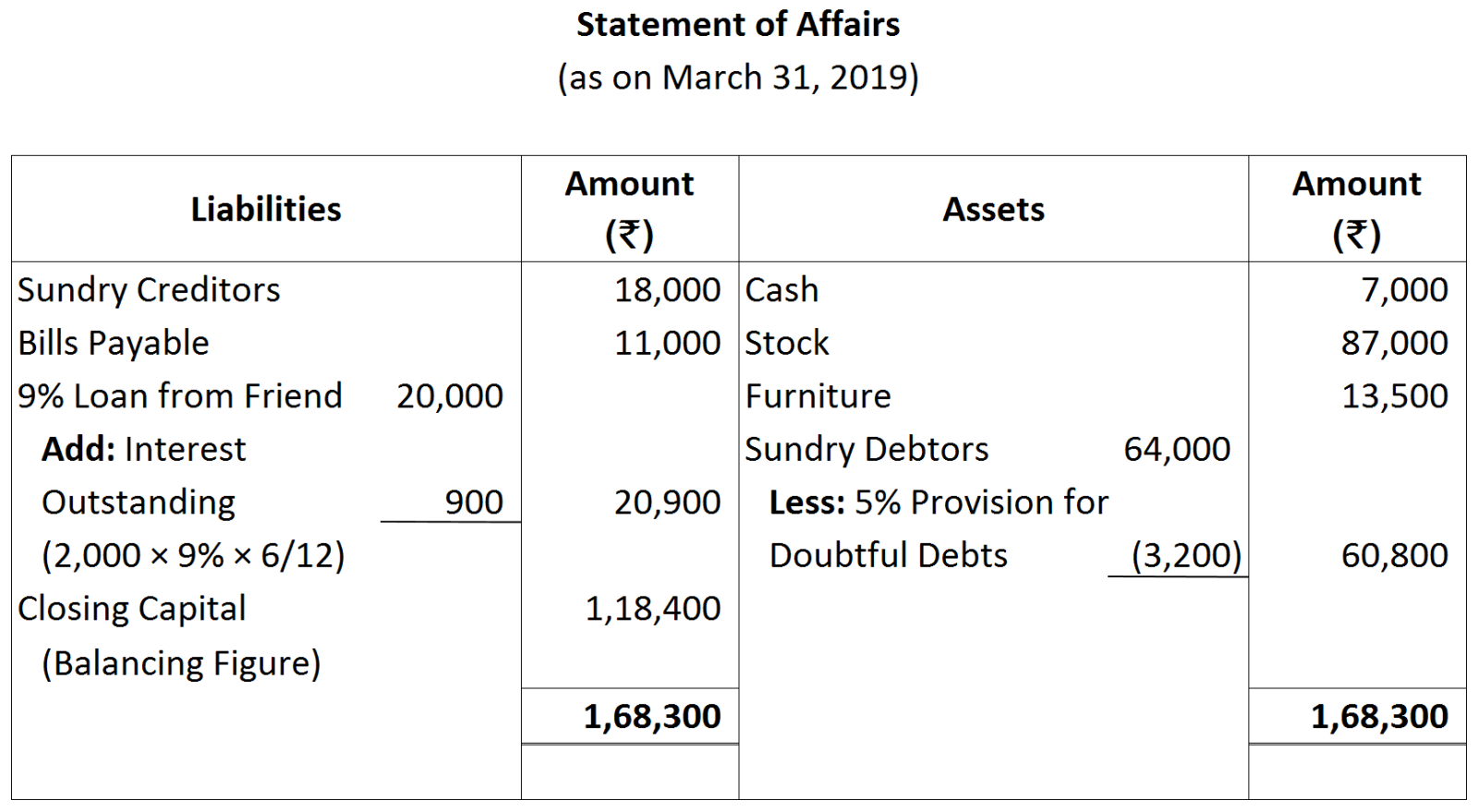

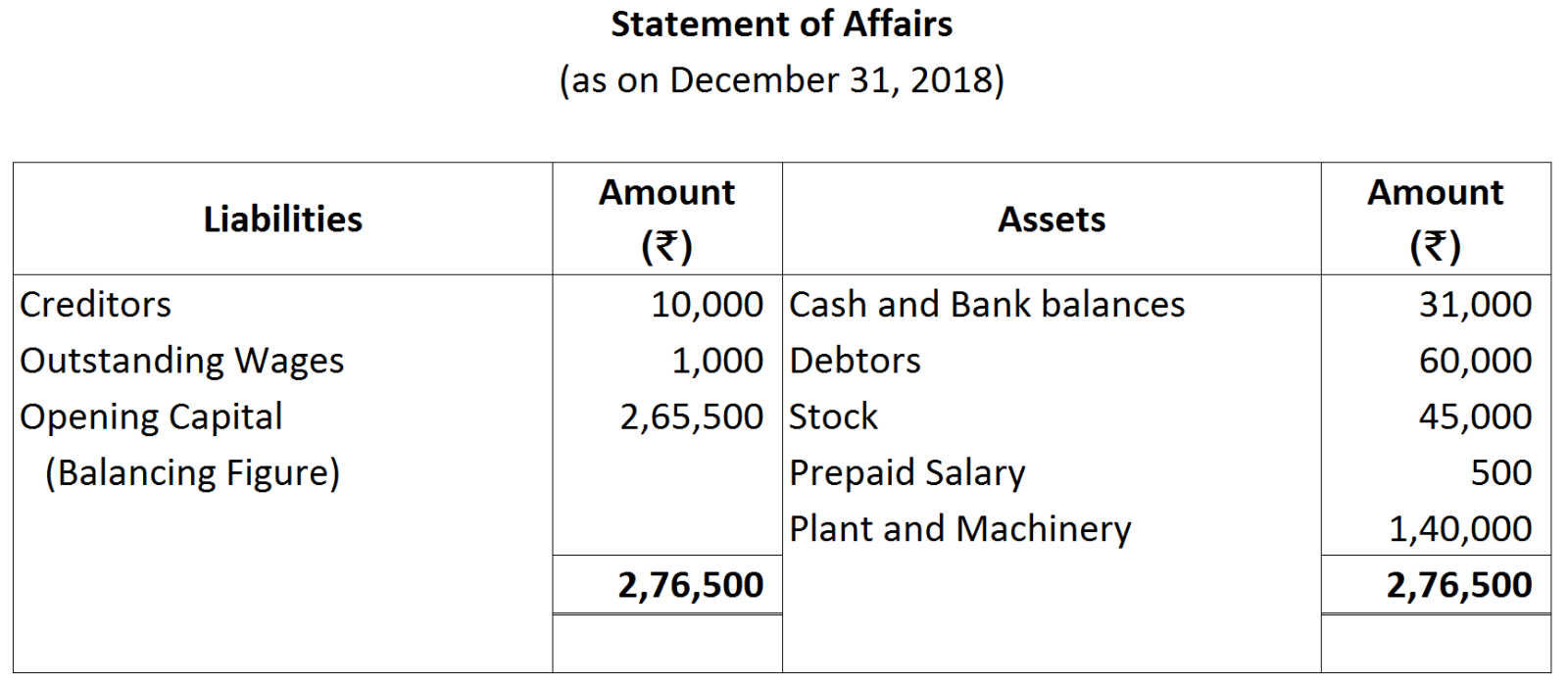

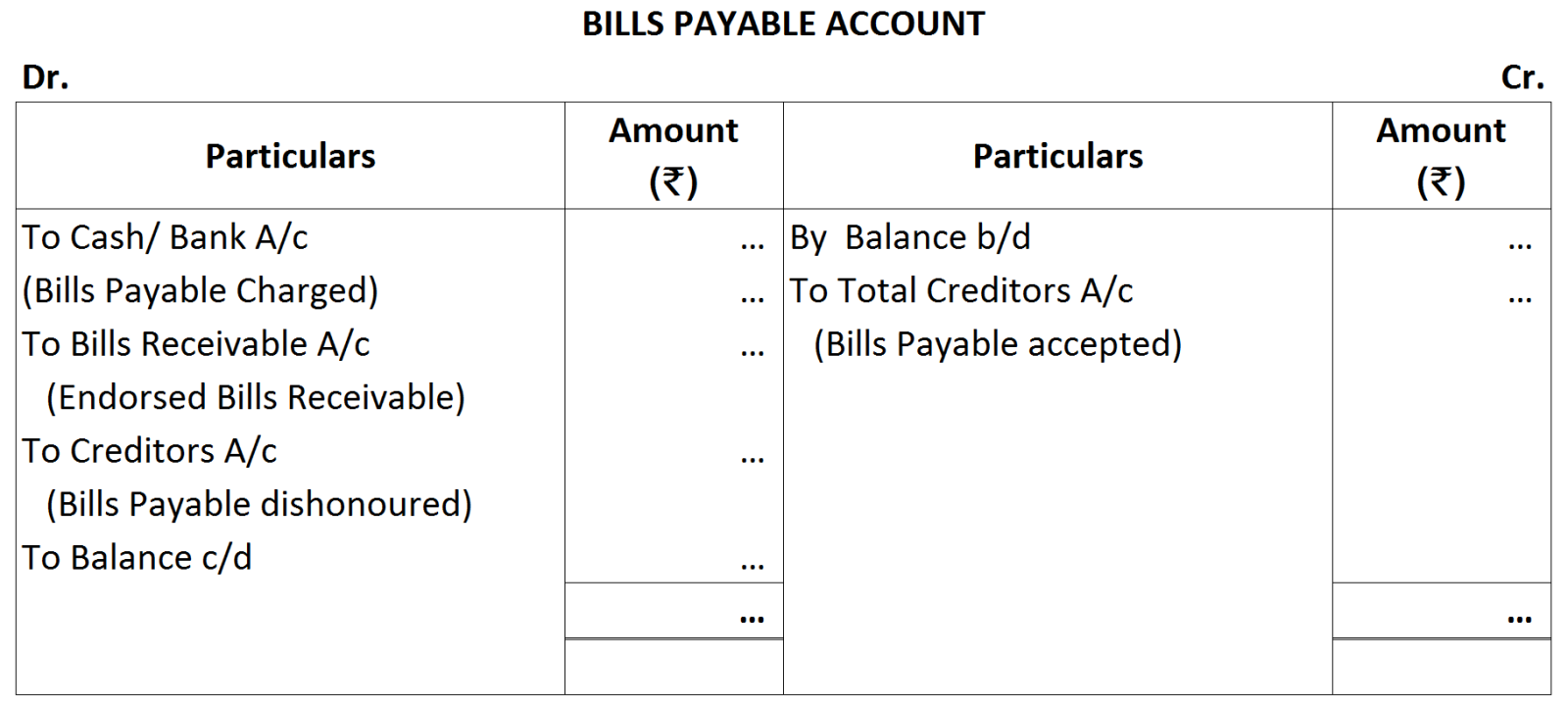

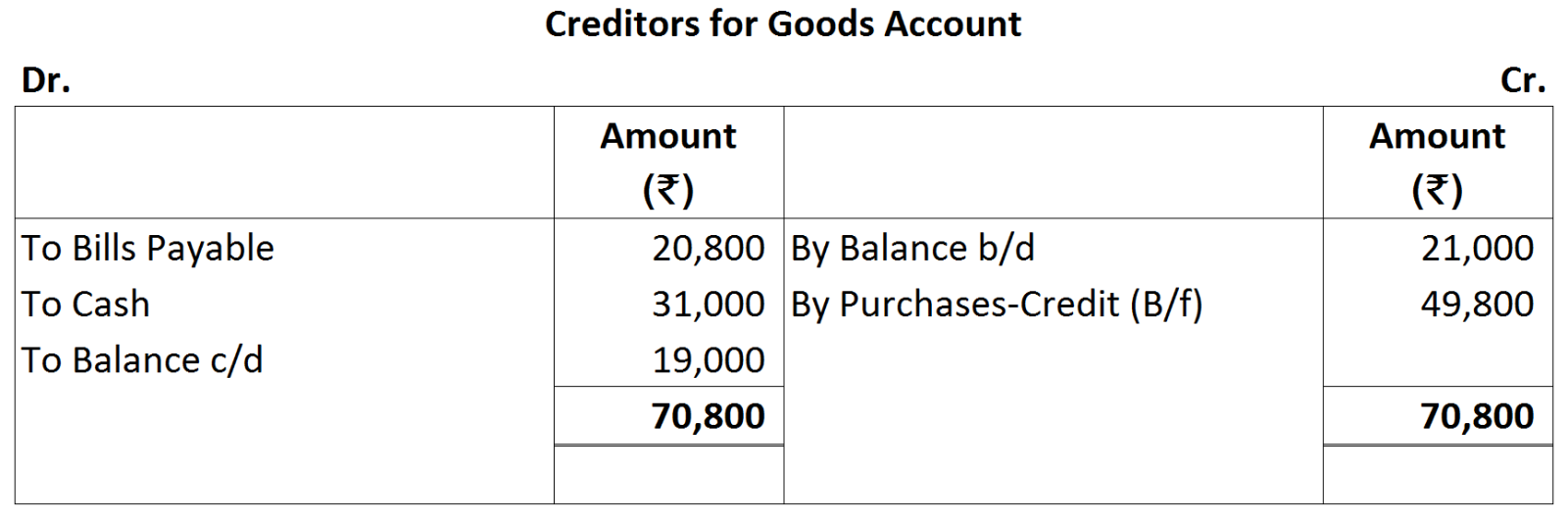

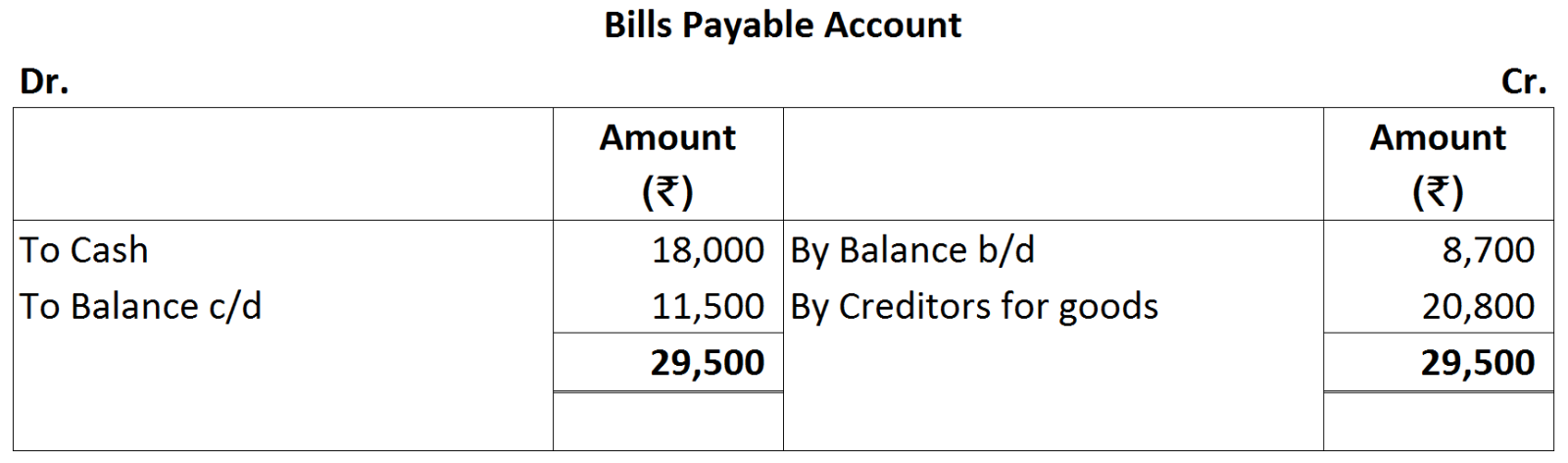

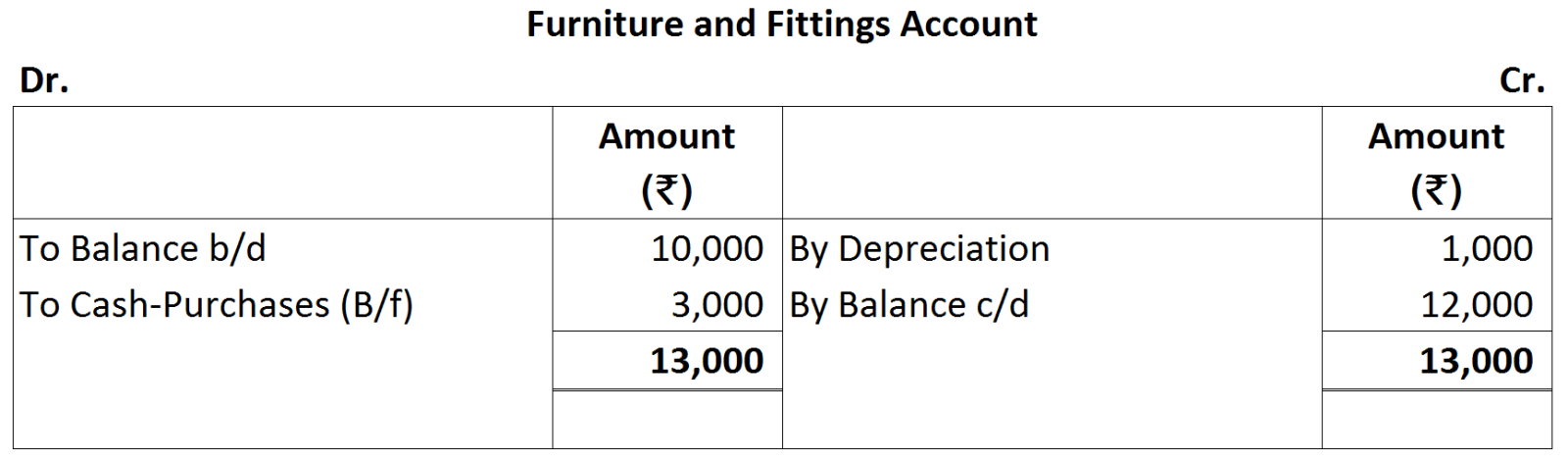

Working Notes:

Working Notes:

Working Notes:

Working Notes:

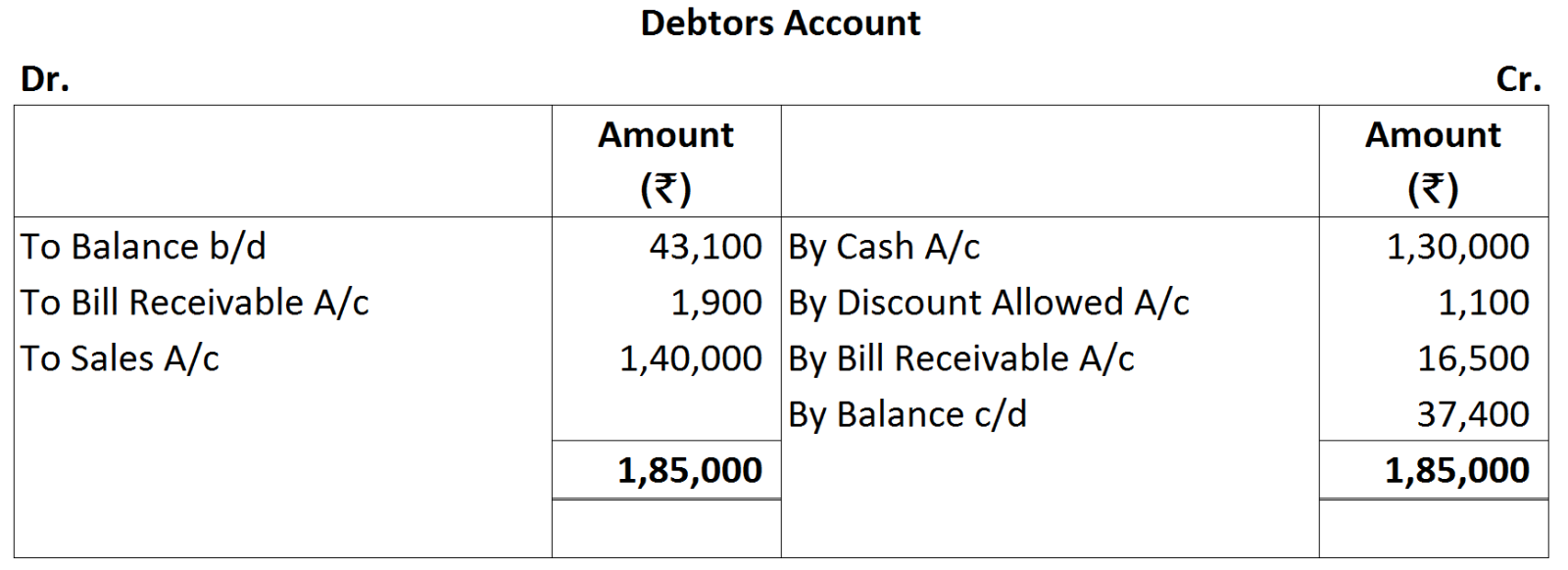

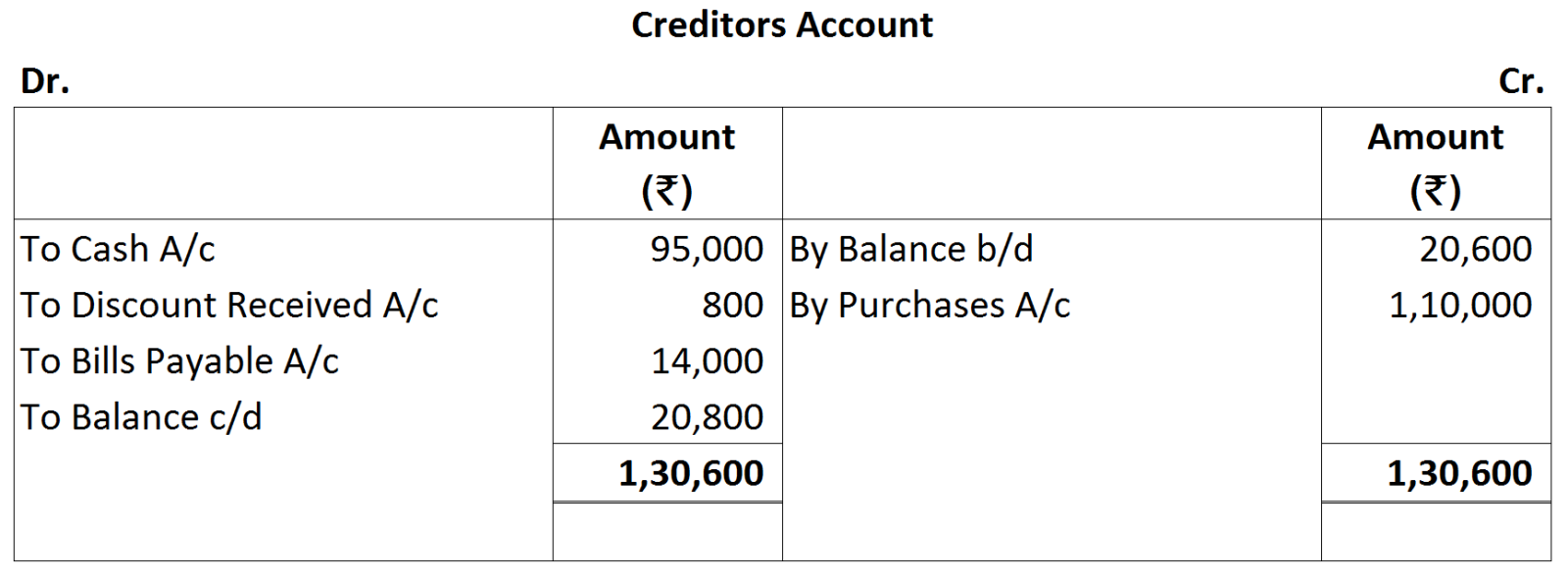

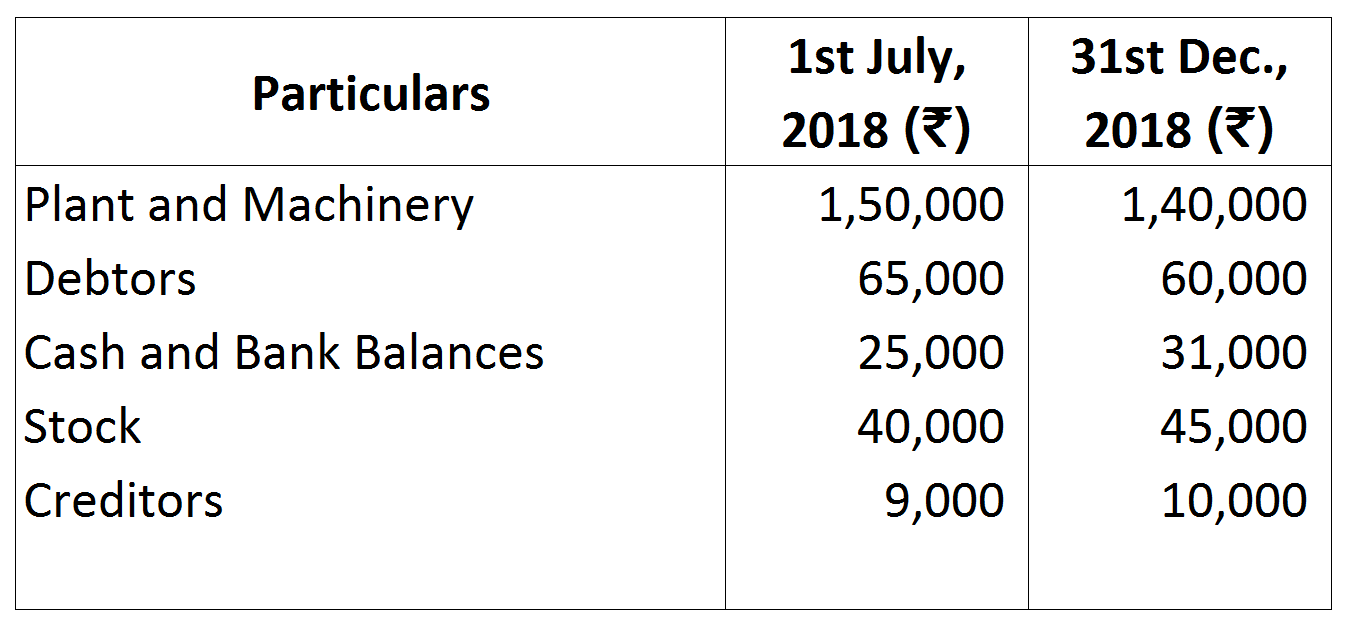

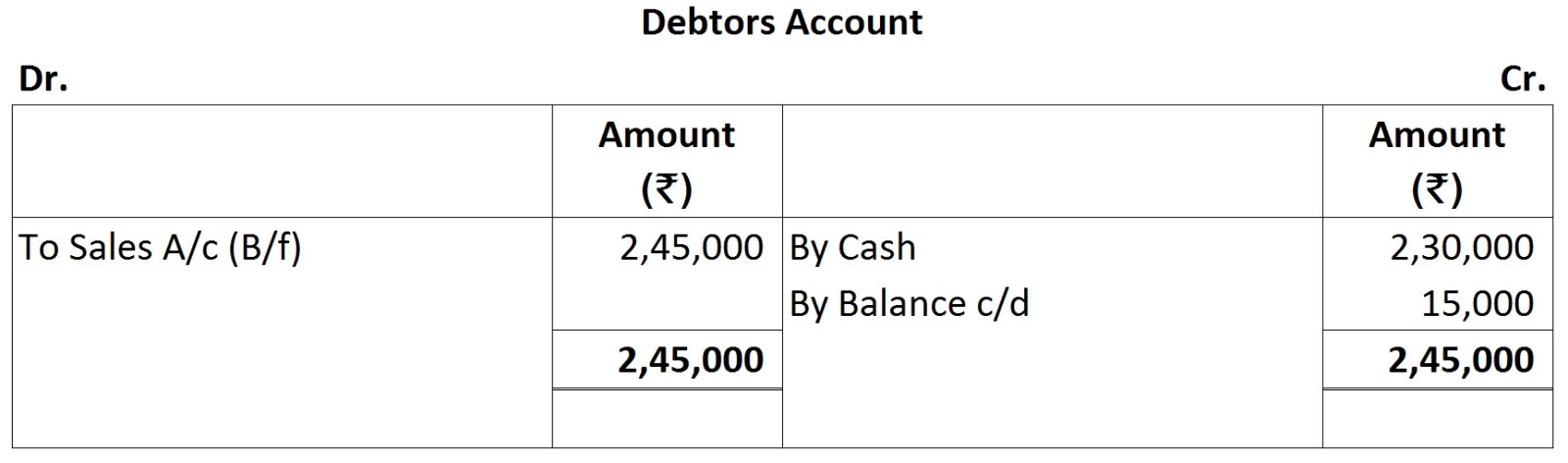

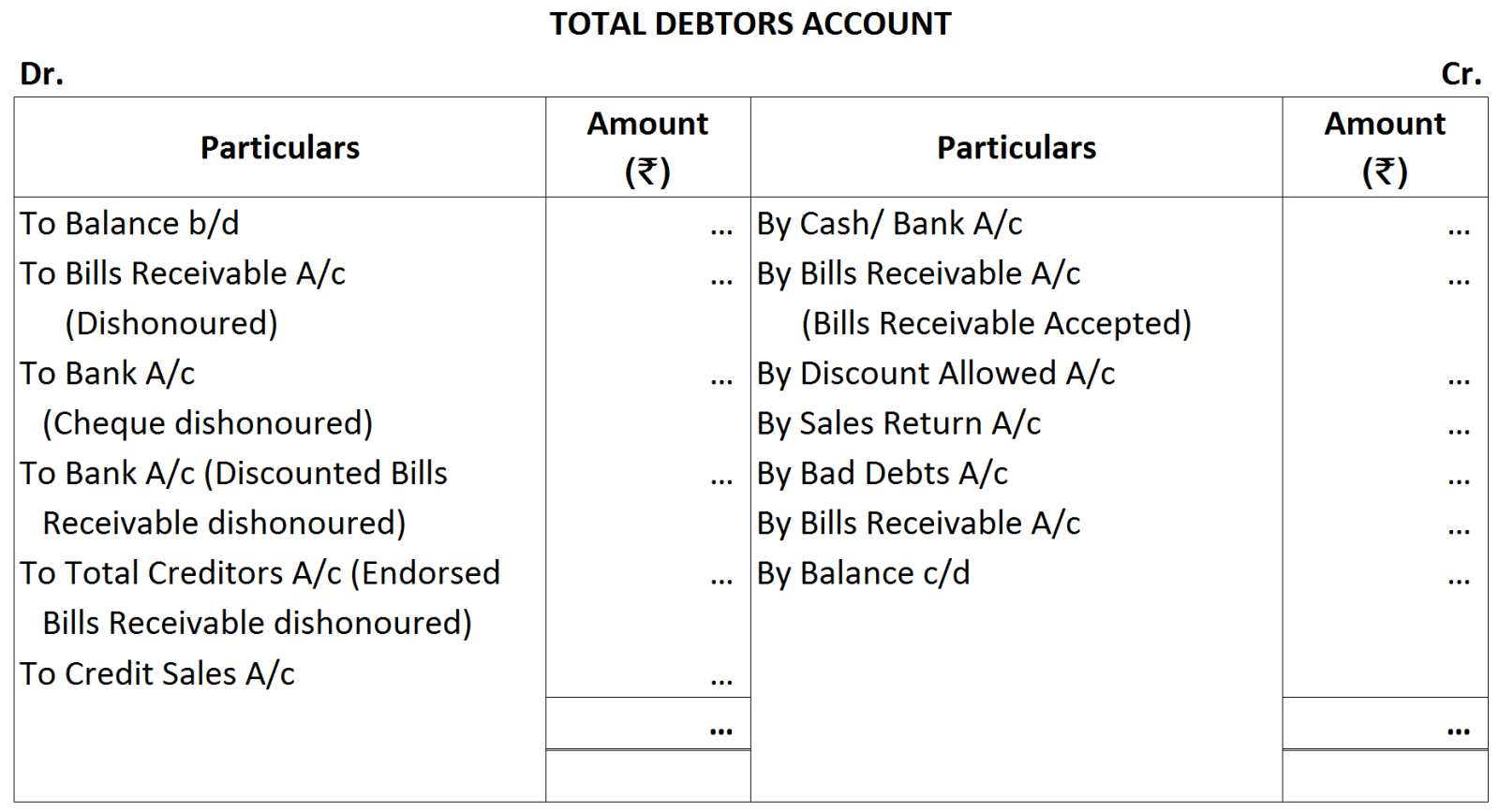

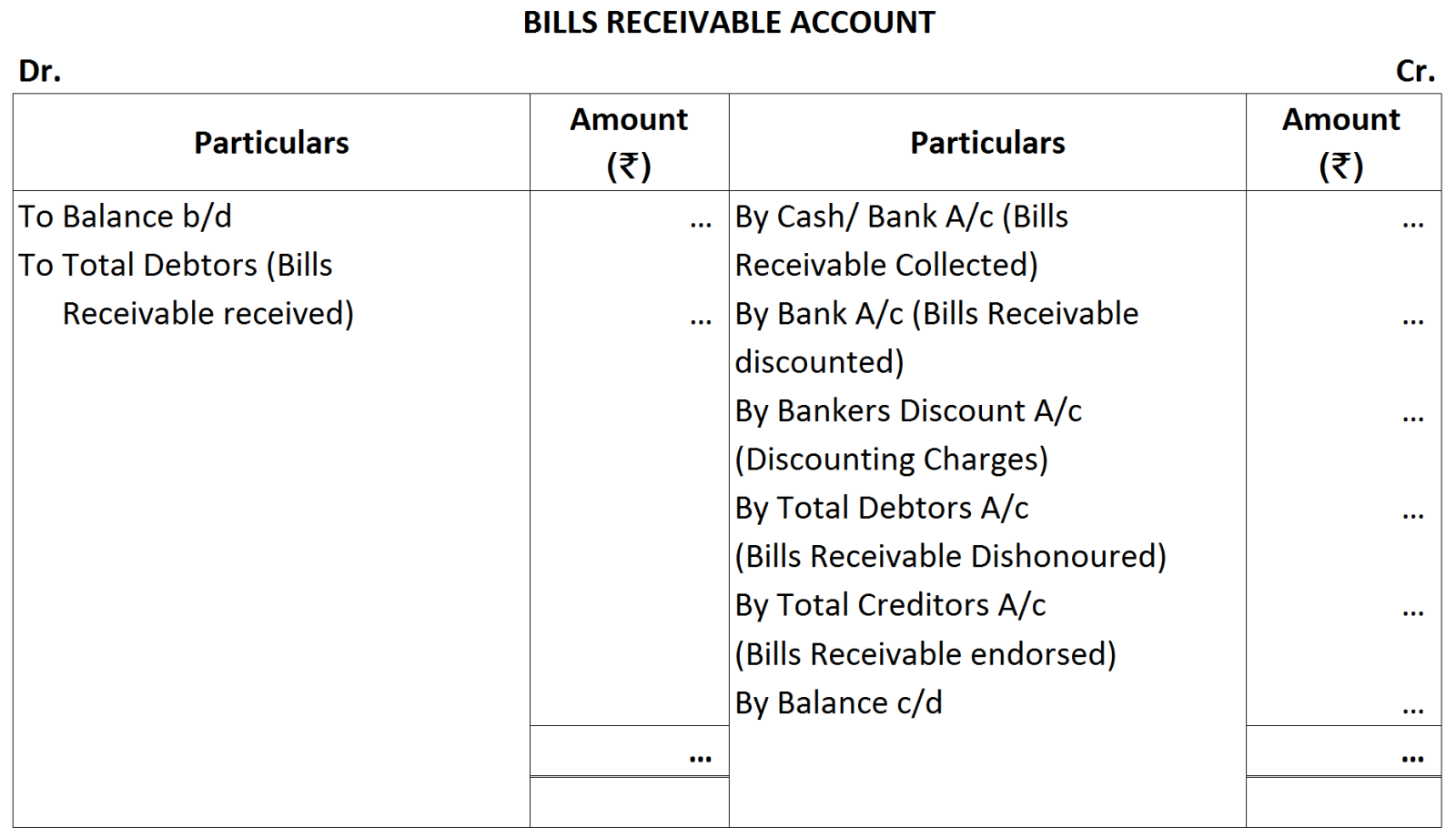

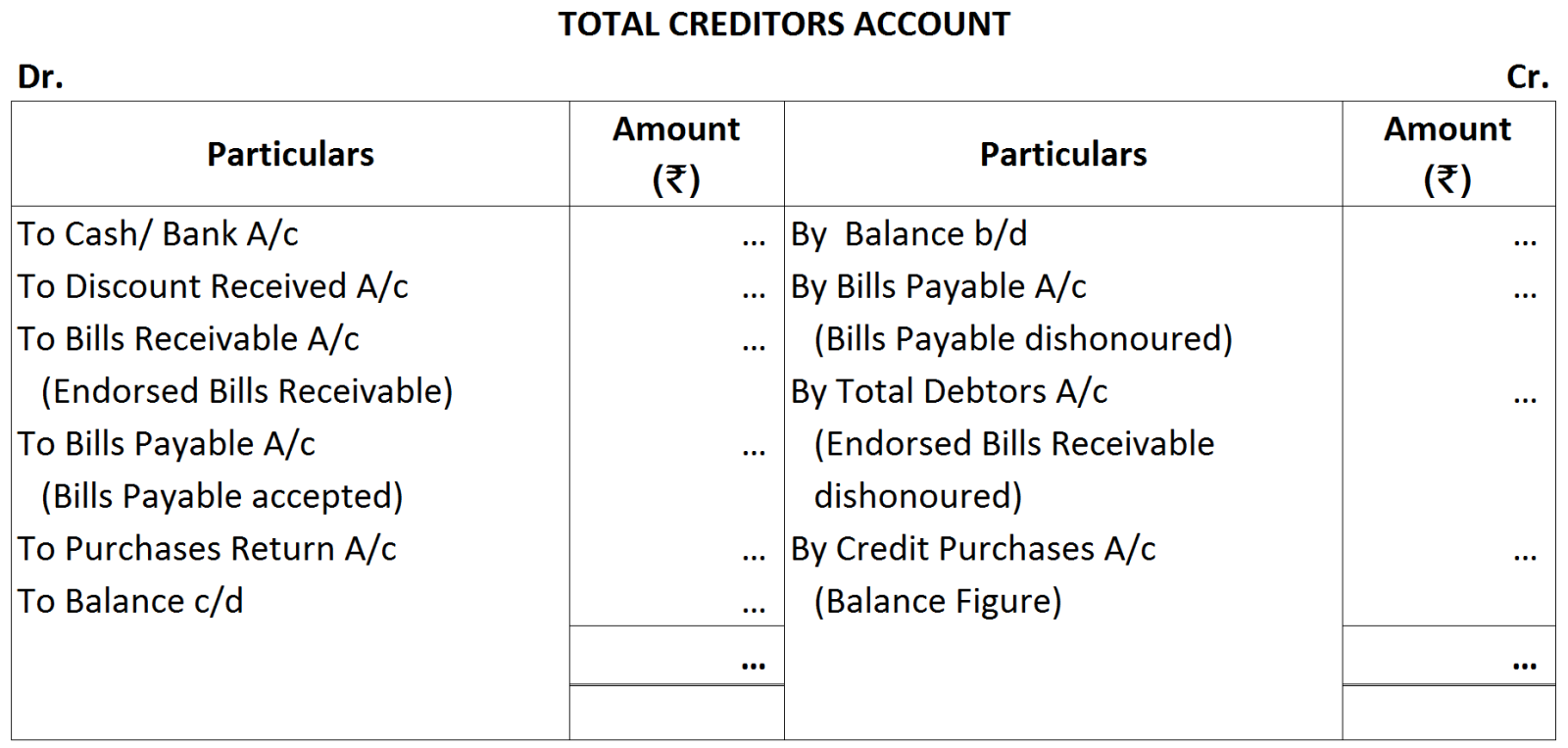

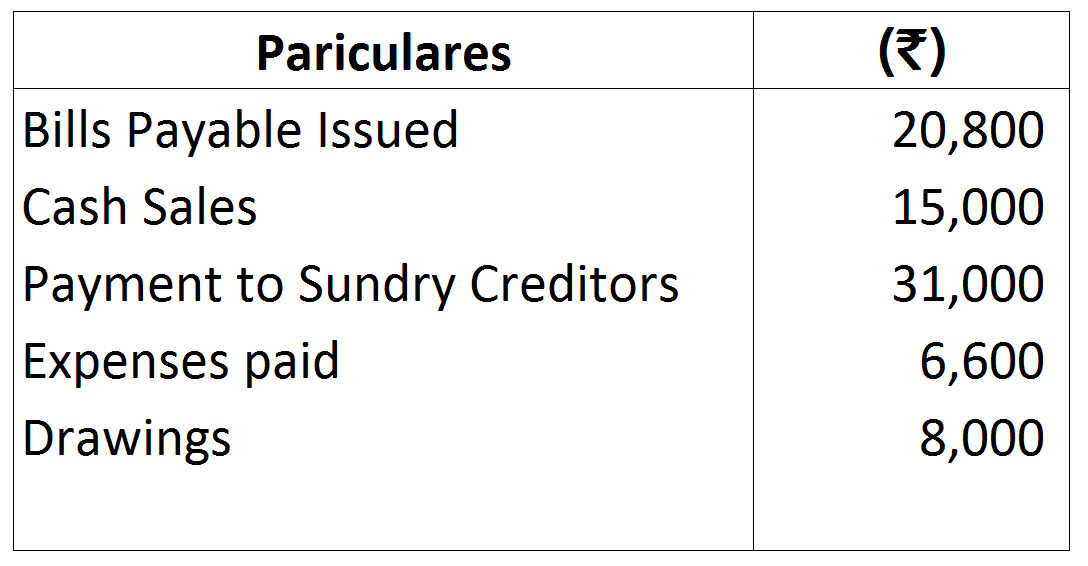

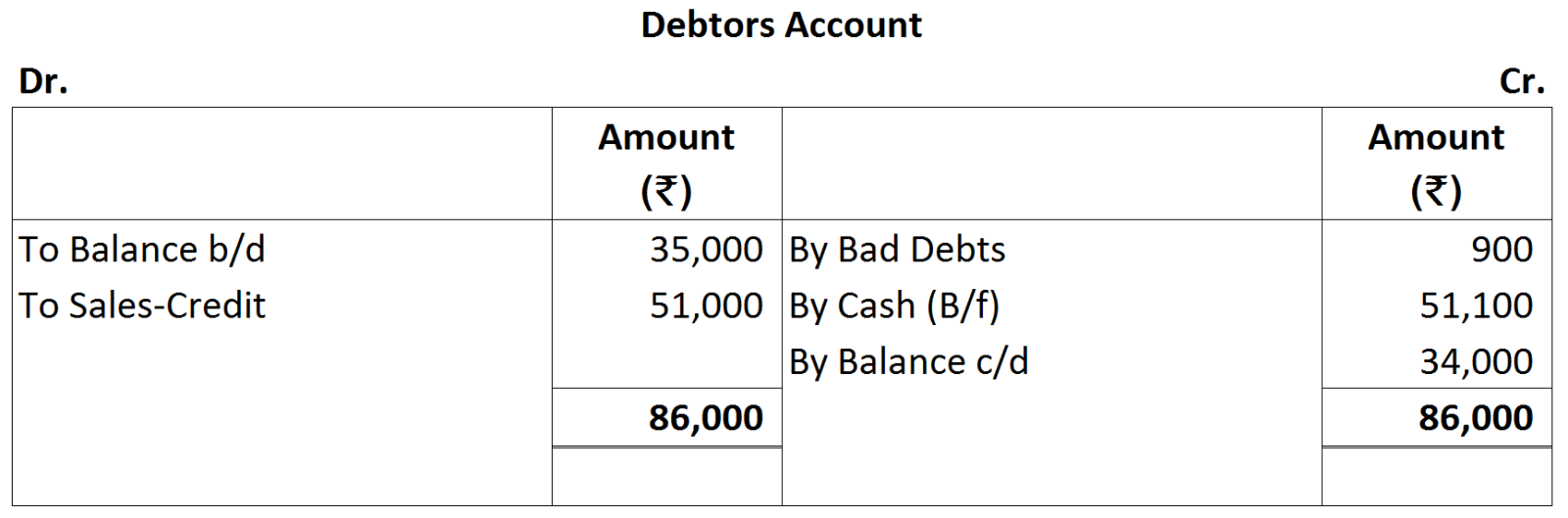

Computation of Cost of Goods Sold and Credit Sales:

Computation of Cost of Goods Sold and Credit Sales: